Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

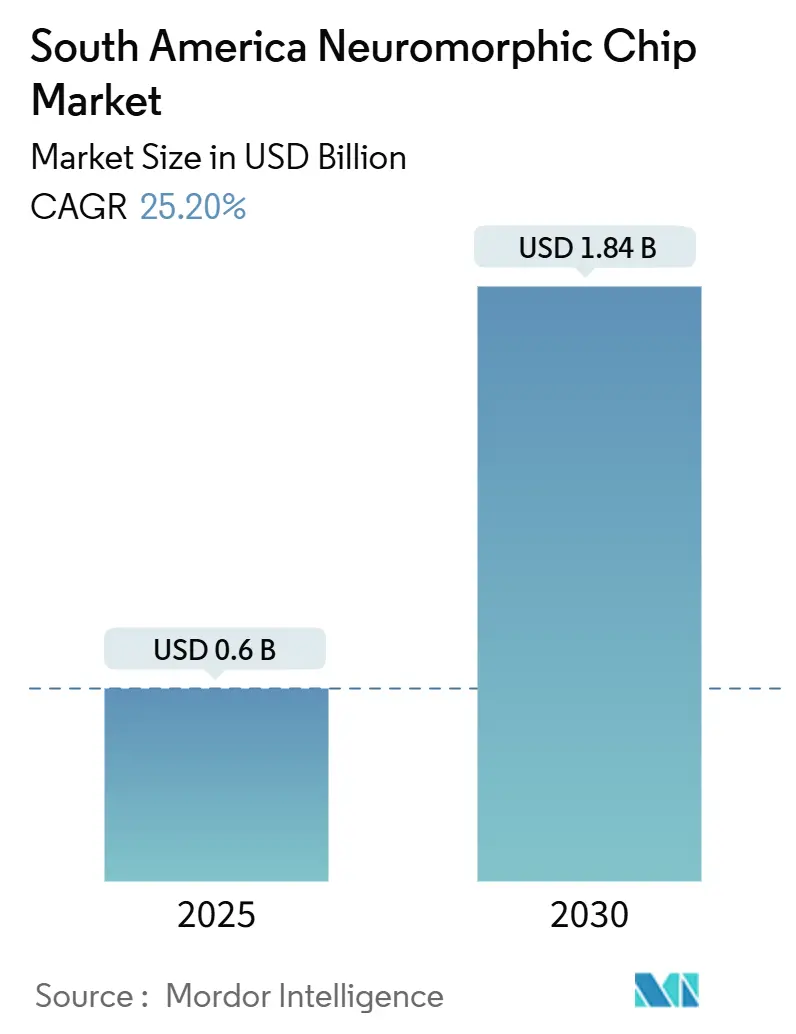

| Market Size (2025) | USD 0.6 Billion |

| Market Size (2030) | USD 1.84 Billion |

| Growth Rate (2025 - 2030) | 25.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Neuromorphic Chip Market Analysis by Mordor Intelligence

The South America neuromorphic chip market size reached USD 0.60 billion in 2025 and is forecast to advance at a 25.20% CAGR, attaining USD 1.84 billion by 2030. Robust funding for sovereign AI infrastructure, rapid adoption of edge computing, and energy-efficient design collectively propel the South America neuromorphic chip market. Governments now view on-device analytics as a route to reduce bandwidth costs and bolster data privacy, which accelerates commercial pilots across defense, healthcare, and fintech domains. Hardware leadership remains clear, while maturing software stacks lower entry hurdles for local developers, shifting attention toward full-stack solutions. Meanwhile, the technology mix is expanding beyond mainstream CMOS into memristor architectures, as regional labs demonstrate tangible power savings in precision agriculture drones and autonomous surveillance. Competitive intensity is rising as global semiconductor leaders race against focused start-ups, giving regional integrators the latitude to craft domain-specific offerings that align with the connectivity limitations of South America.

Key Report Takeaways

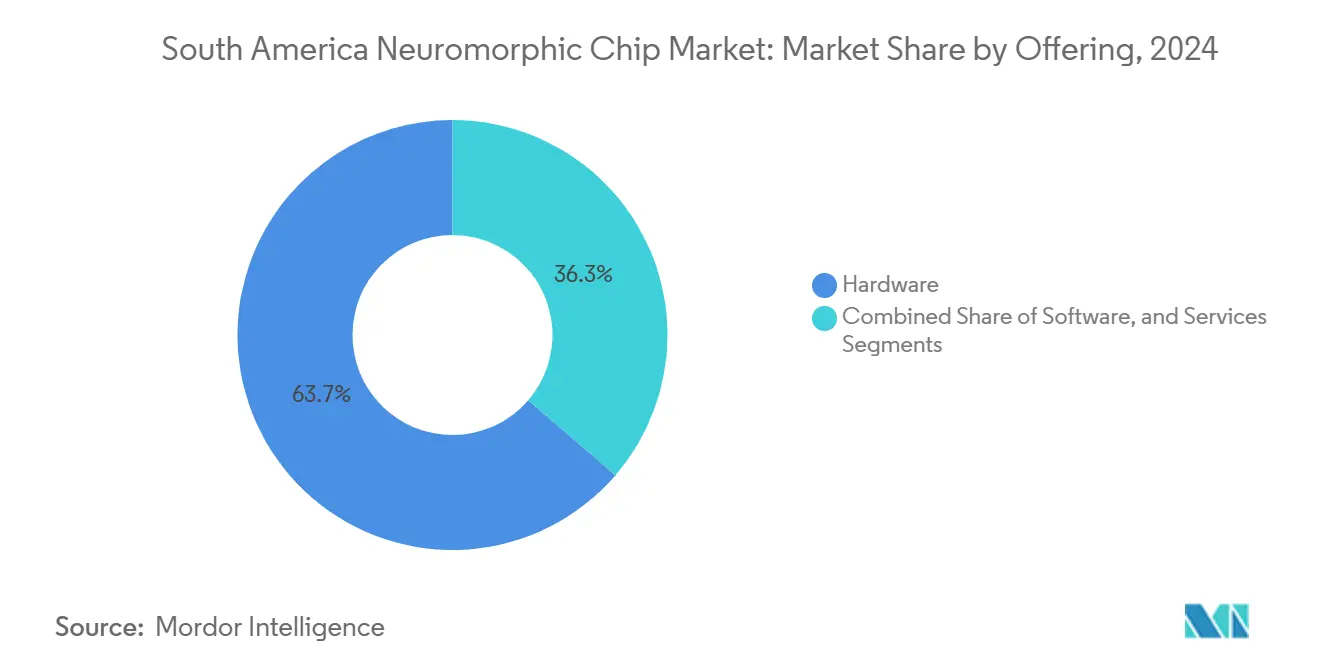

- By offering, hardware captured 63.7% revenue share of the South America neuromorphic chip market in 2024, while software is projected to expand at a 26.91% CAGR through 2030.

- By technology, CMOS held 57.8% of the South America neuromorphic chip market share in 2024; memristor solutions are forecast to grow at a 26.77% CAGR to 2030.

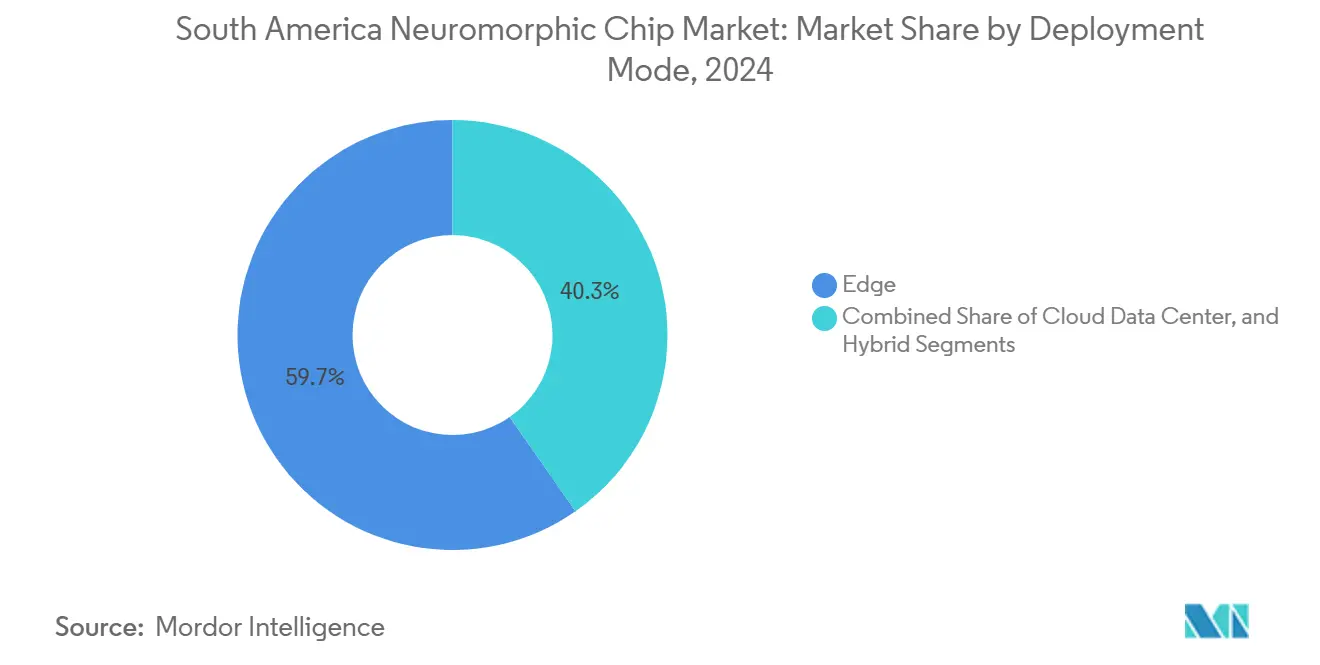

- By deployment mode, edge configurations accounted for 59.7% of the South America neuromorphic chip market size in 2024 and are expected to rise at a 24.5% CAGR through 2030.

- By end-user industry, the aerospace and defense sector led with a 28.96% revenue share of the South America neuromorphic chip market in 2024, whereas the consumer electronics sector is advancing at a 28.08% CAGR through 2030.

- By country, Brazil commanded 42.31% of the South America neuromorphic chip market size in 2024; Argentina exhibits the fastest trajectory, with a 27.01% CAGR to 2030.

South America Neuromorphic Chip Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for AI-enabled microchips | +4.2% | Brazil, Argentina core markets | Medium term (2-4 years) |

| Expansion of edge computing and IoT deployments | +3.8% | Regional, strongest in Brazil and Chile | Short term (≤ 2 years) |

| Increased public and private R&D funding | +3.1% | Brazil RMB 23B plan, Argentina USD 35M program | Long term (≥ 4 years) |

| Precision-agriculture drone vision adoption | +2.9% | Argentina, Brazil agricultural regions | Medium term (2-4 years) |

| FinTech on-device security analytics | +2.4% | Brazil financial sector, regional expansion | Short term (≤ 2 years) |

| Sustainability-driven data-center retrofits | +1.8% | Urban centers across South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for AI-enabled microchips

High-frequency AI workloads continue to strain legacy GPU platforms, motivating buyers to test neuromorphic alternatives that execute sparse spiking operations at a fraction of traditional power budgets. Intel’s 2024 Hala Point system posted 50× energy gains for real-time inference, validating commercial readiness and shaping procurement decisions across regional banks and automakers.[1]Intel Corporation, “Intel Hala Point Neuromorphic Research System,” intel.com Brazilian monetary authorities subsequently deployed neuromorphic fraud-detection modules inside digital-currency endpoints, reinforcing the value of local processing. Automotive test beds in São Paulo now integrate spiking-vision accelerators that recognize street objects within 2 milliseconds on sub-5W budgets, aligning with South American traffic safety mandates. As chief information officers shift focus from peak tera-operations toward total cost of ownership, the South America neuromorphic chip market registers uptake from both greenfield pilots and retrofit projects.

Expansion of edge computing and IoT deployments

Patchy fiber backbones and expensive cross-continental links make low-latency cloud calls impractical in many parts of South America. Enterprises react by consolidating analytics at the edge, and neuromorphic silicon addresses the twin challenges of power and bandwidth. In 2025, BrainChip and Raytheon demonstrated a radar-signal workflow that consumed three times less energy than DSP baselines, offering a replicable template for public-safety networks.[2]BrainChip Holdings, “BrainChip and Raytheon Collaborate on AFRL Neuromorphic Radar Processing,” brainchip.com Large-scale IoT grids in Mato Grosso farms now feature spiking cores that continuously monitor soil moisture for months between battery swaps. Remote clinics in Pará process ultrasound frames locally through OpenCare5G neuromorphic gateways, cutting transmission loads by 85% and widening telemedicine reach. These early wins amplify C-suite trust and accelerate multiyear roadmaps to relocate analytics from distant data centers to field assets.

Increased public and private R&D funding

Brazil earmarked RMB 23 billion for AI sovereignty, channeling resources into open-source spiking compilers, multi-wafer prototyping, and early-stage venture funds. Argentina follows with a USD 35 million grant program that prioritizes edge inference for crop analytics and defense robotics. The Brazilian Air Force established an AI laboratory in late 2024 with RMB 6.6 million seed capital devoted to neuromorphic autonomy trials. University consortia partner with Synopsys through the SARA initiative, giving 40 campuses access to licensed neuron-model libraries and design simulators. Venture investors increasingly bundle local domain expertise with global fabrication ties, nurturing start-ups that promise wafer-level efficiency gains tailored to South America's neuromorphic chip market constraints.

Precision-agriculture drone vision adoption

Field robotics must endure heat, dust, and long sorties over vast hectares, making low-power spiking vision indispensable. Delft University flight trials documented 64× faster frame processing and triple battery endurance when swapping GPU boards for neuromorphic co-processors. National cooperatives in Argentina now schedule pest-scouting missions that cover 2,000 ha per drone sortie, feeding yield maps directly into irrigation control loops. The Open-Science Drone Toolkit formalized shared hardware blueprints, enabling agritech integrators in Uruguay and Paraguay to adapt modules without incurring high licensing fees. As agri-exports dominate many national GDP ledgers, government extension agencies champion these energy-efficient fleets, bolstering commercial demand across the South America neuromorphic chip market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High manufacturing and packaging cost | -3.4% | Regional, affecting all markets | Medium term (2-4 years) |

| Limited software toolchains and developer familiarity | -2.8% | Technical centers in Brazil, Argentina | Short term (≤ 2 years) |

| Component supply-chain volatility | -2.1% | Import-dependent markets across region | Short term (≤ 2 years) |

| Regional talent migration | -1.6% | Brazil, Argentina tech hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High manufacturing and packaging cost

Neuromorphic dies require analog-digital co-design and dense Through-Silicon Via (TSV) stacks, which are scarce at foundries serving Latin America. Brazil’s Ceitec restart underscores capital needs exceeding USD 500 million, which forces local firms to rely on Asian subcontractors, thereby extending lead times and incurring freight overhead.[3]Jeffrey Bean and Andreas Kuehn, “Building Resilient Supply Chains: The Case of Semiconductors,” orfamerica.org Custom interposers and micro-bump arrays can increase back-end packaging costs by up to 40% compared to standard GPU parts, putting pressure on consumer price points. Until volume ramps up to neutralize per-unit premiums, many budget-sensitive buyers will delay broad roll-outs, moderating near-term growth for the South America neuromorphic chip market.

Limited software toolchains and developer familiarity

Spiking neural networks diverge from typical tensor paradigms, and debugging asynchronous event streams still feels opaque to most engineers. A 2024 Synopsys SARA survey revealed that 70% of Latin American developers had no hands-on experience with neuromorphic frameworks. Skill gaps translate to longer prototyping cycles and cost overruns, deterring smaller firms from capitalizing on the technology. University curricula now insert semester-long labs, yet competency pipelines will take several cohorts to mature, imposing a short-term drag on deployment velocity inside the South America neuromorphic chip market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Hardware Dominance Drives Infrastructure Build-out

Hardware represented 63.7% of the South America neuromorphic chip market share in 2024, reflecting urgent demand for power-frugal silicon that can operate untethered in remote zones. The segment’s growth anchors the overall South America neuromorphic chip market, where dataloggers, drones, and combat radios now ship with dedicated spiking cores. Intel’s Loihi 2 and BrainChip’s Akida families headline deployments, each bundling on-chip learning engines that remove repetitive cloud calls.[4]Intel Labs, “Intel Loihi 2 Neuromorphic Research Chip,” intel.com Component vendors invest in radiation-hardened variants to satisfy aerospace tenders, while consumer OEMs prioritize neural-voice wake-word chips for always-on mobile interfaces. Subsystems suppliers differentiate themselves via board-level power management and rugged packaging, thereby extending reliability in tropical humidity environments.

Software tools trail but post a 26.91% CAGR as compilers, model converters, and visualization suites grow more intuitive. Start-ups license Python-based SDKs that translate conventional convolution graphs into event-driven equivalents, shaving weeks off pilot timelines. Services remain the smallest slice yet attract foreign systems-integration majors who bundle reference designs, compliance audits, and lifecycle maintenance. Over the forecast period, the hardware segment will cede a modest share to software and services as enterprises demand turnkey stacks, but silicon innovation will still anchor revenue, reinforcing the strategic weight of fabrication alliances within the South America neuromorphic chip market.

By Technology: CMOS Maturity Enables Near-term Adoption

CMOS designs held 57.8% of the South America neuromorphic chip market size in 2024 as fabs leverage proven 28 nm and 14 nm nodes to mass-produce neuron arrays without exotic materials. These parts integrate seamlessly into existing printed circuit board lines, reducing qualification risk for defense and telecom contractors. Samsung Research outlined a 12-layer stack roadmap that doubles synaptic density every two years, ensuring the continued relevance of planar CMOS offerings. Memristor architectures, growing at a 26.77% CAGR, gain mindshare in battery-bound endpoints thanks to analog weight storage that reduces static power draw by double-digit margins. Argentina’s Atomic Energy Commission demonstrated a memristor flight controller that cut avionics wattage to 1.9 W while sustaining nine-hour sorties.

Next-generation optical and spintronic prototypes remain lab-bound, yet they attract grants targeting exascale climate simulation and quantum-safe cryptography. Vendors are increasingly exploring hybrid stacks that embed memristor crossbars atop CMOS control, thereby optimizing the trade-offs between fabrication yield and analog precision. Such heterogenous designs are poised to widen the solution palette and expand the South America neuromorphic chip market, provided material supply chains stabilize.

By Deployment Mode: Edge Computing Addresses Infrastructure Constraints

Edge nodes accounted for 59.7% of installations, underscoring how patchy broadband pushes computation closer to data sources. Farm drones, smart meters, and oil-well monitors exemplify unit volumes, each demanding sub-5 W operation to sustain multi-month missions. The South America neuromorphic chip market thus tilts toward embedded modules with compact thermal envelopes and rugged housings. Cloud data-center interest accelerates at a 27.03% CAGR as hyperscalers pilot neuromorphic acceleration boards that lower rack-level PUE metrics, a critical win amid regional carbon tax legislation. Hybrid topologies emerge when banks or hospitals partition inference to the edge while maintaining model training in secure colocation cages, thereby balancing latency and governance mandates.

Brazilian fintechs illustrate a hybrid value proposition: on-device neuromorphic tokens flag anomalies instantly, while centralized clusters refine fraud models overnight. Edge dominance will persist yet coexist with cloud inserts, demonstrating that workload orchestration, not binary placement debates, will shape future purchasing within the South America neuromorphic chip market.

By End User Industry: Defense Leadership Drives Technology Maturation

Aerospace and defense accounted for 28.96% of revenue in 2024, sustained by multi-year modernization budgets that prioritize autonomous reconnaissance and electronic warfare resilience. The Brazilian Air Force AI laboratory pioneers neuromorphic vision pods that classify inbound drones under jamming noise, yielding decisive strategic value. Consumer electronics are growing at the fastest rate, with a 28.08% CAGR, as handset makers integrate speech-centric, high-performance cores that prolong battery life. Industrial maintenance crews retrofit pumps with neuromorphic vibration sensors that detect bearing wear weeks earlier than FFT-based tools, boosting uptime in Chilean mining towns.

Financial institutions leverage the technology’s always-on encryption analytics to secure mobile payments in high-fraud corridors, whereas healthcare innovators embed spiking inference inside portable ultrasound probes for clinics in the Amazon basin. These cross-sector wins broaden credibility and funnel volume, confirming that early defense sponsorship seeded a technology beachhead that diversified into civil domains across the South America neuromorphic chip market.

Geography Analysis

Brazil posted a 42.31% share in 2024 by leveraging a deep semiconductor talent pool and RMB 23 billion in policy incentives that de-risk fab and pilot projects. Brazil commands nearly half of the regional revenue, propelled by strong public funding, a large consumer base, and the presence of advanced design centers.

Argentina, expanding at a 27.01% CAGR, capitalizes on the Pampas agriculture and defense aerospace niches, funneling memristor research into viable UAV controls that align with its export ambitions. Argentina follows with the fastest growth, driven by government grants focusing on precision agriculture and defense technologies. Its vast farmlands serve as proving grounds where neuromorphic drones and edge gateways tackle real-time agronomic analytics at scale.

Chile leverages robust fiber networks to trial cloud-paired neuromorphic accelerators in banking and tele-health services, while Colombia and Peru explore predictive maintenance for extractive industries. Cross-border academic initiatives, such as the Open-Science Drone Toolkit, lower entry costs and disseminate engineering know-how, thereby knitting a broader regional ecosystem that supports the South America neuromorphic chip market.

Competitive Landscape

The competitive field features multinational semiconductor leaders that supply mature product portfolios alongside agile start-ups developing purpose-built solutions. Intel and Samsung offer broad technology roadmaps, strong channel relationships, and sustained R&D budgets, which afford them early design wins in government projects. Specialized vendors, such as BrainChip and SynSense, focus on ultra-low-power inference engines, carving out niches in the aerospace and industrial sensor markets.

Local system integrators bridge gaps between foreign silicon and domestic regulatory requirements, customizing reference boards and deploying pilot installations. Partnerships between chip suppliers, universities, and government labs form innovation clusters that improve time-to-market. As solution buying eclipses isolated component purchases, ecosystem orchestration becomes a pivotal competitive lever within the South America neuromorphic chip market.

South America Neuromorphic Chip Industry Leaders

Intel Corporation

IBM Corporation

Samsung Electronics Co., Ltd.

SK hynix Inc.

Qualcomm Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Several governments across the region are finalizing fresh AI-infrastructure packages, and Brasília is expected to publish the operating rules for its R$23 billion initiative before year-end, with clear carve-outs for neuromorphic research and roll-outs.

- September 2025: Universities in the Synopsys SARA network opened dedicated courses on neuromorphic programming, a move aimed at easing the shortage of skilled developers and supporting the market’s long-term talent pipeline.

- August 2025: Major Argentine farming cooperatives have reported successful field trials of neuromorphic drones that utilize event-driven vision to monitor crops and detect pests, confirming the technology’s suitability for precision agriculture.

- July 2025: Leading Brazilian fintechs adopted on-device neuromorphic engines for continuous fraud detection, gaining higher security without draining smartphone batteries.

- June 2025: Chile’s top telecom operators have begun lab tests of neuromorphic processors at 5G edge sites, aiming for lower power consumption and faster response times for distributed workloads.

South America Neuromorphic Chip Market Report Scope

The South America Neuromorphic Chip Market is segmented by End-User Industry (Financial Services and Cybersecurity, Automotive, Industrial, Consumer Electronics).

Neuromorphic chips are digitally processed analog chips with a series of networks similar to human brain networks. These chips contain millions of neurons and synapses to augment self intelligence, irrespective of pre-installed codes in normal chips. As a special kind of chips, these are highly capable of manipulating data received through sensors.

By Offering

| Hardware |

| Software |

| Services |

By Technology

| CMOS |

| Memristor |

| Others |

By Deployment Mode

| Edge |

| Cloud Data Center |

| Hybrid |

By End User Industry

| Consumer Electronics |

| Automotive |

| Industrial |

| Financial Services and Cybersecurity |

| Healthcare |

| Aerospace and Defense |

| Telecommunications |

| Other End User Industries |

By Country

| Brazil |

| Argentina |

| Chile |

| Rest of South America |

| By Offering | Hardware |

| Software | |

| Services | |

| By Technology | CMOS |

| Memristor | |

| Others | |

| By Deployment Mode | Edge |

| Cloud Data Center | |

| Hybrid | |

| By End User Industry | Consumer Electronics |

| Automotive | |

| Industrial | |

| Financial Services and Cybersecurity | |

| Healthcare | |

| Aerospace and Defense | |

| Telecommunications | |

| Other End User Industries | |

| By Country | Brazil |

| Argentina | |

| Chile | |

| Rest of South America |

Key Questions Answered in the Report

What is the projected revenue for neuromorphic chips in South America by 2030?

The market is expected to reach USD 1.84 billion by 2030, driven by a 25.20% CAGR.

Which country currently leads regional adoption?

Brazil holds 42.31% share, benefiting from sizable AI funding and an established semiconductor base.

Why are neuromorphic chips favored for edge computing in Latin America?

They deliver high inference performance at very low power, which suits the region’s limited broadband and remote deployment needs.

Which end-user segment is expanding fastest?

Consumer electronics shows the highest growth, advancing at a 28.08% CAGR through 2030 as handset makers embed always-on AI.

What is the main barrier to wider deployment?

High manufacturing and advanced packaging costs remain the primary restraint, raising unit prices for budget-sensitive buyers.

How are universities supporting ecosystem growth?

Programs like Synopsys SARA supply design tools and training to more than 40 campuses, expanding the developer talent pipeline.

Page last updated on: