Late-Stage Customization And Postponement Packaging Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

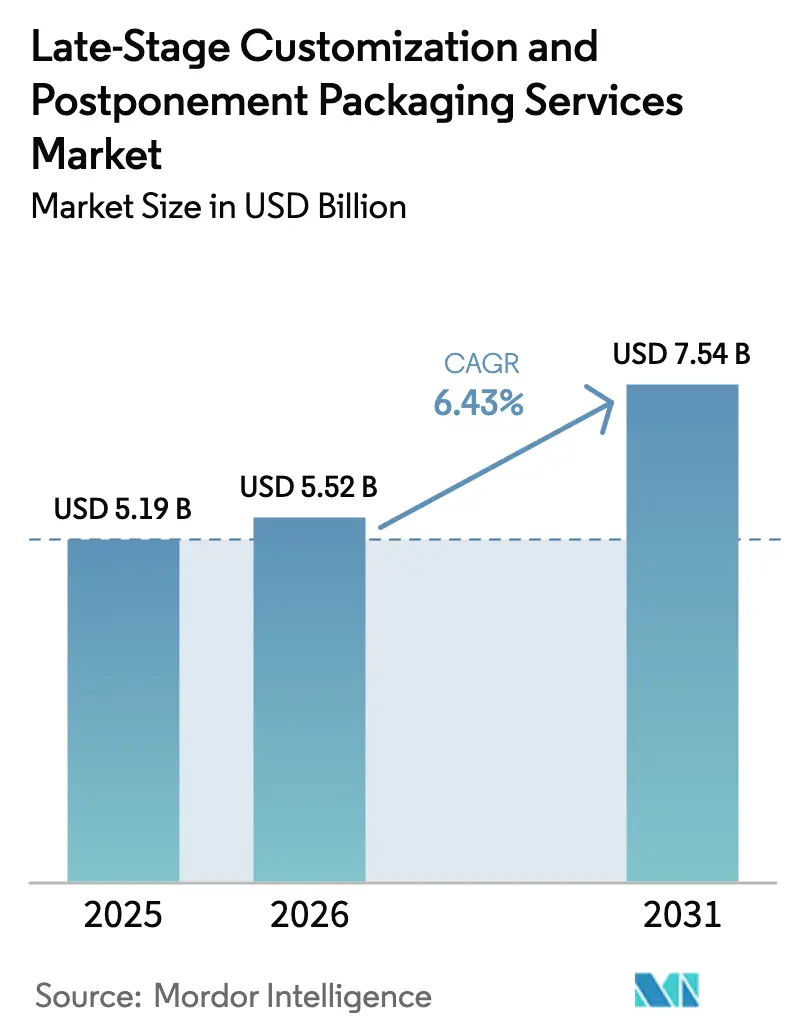

| Market Size (2026) | USD 5.52 Billion |

| Market Size (2031) | USD 7.54 Billion |

| Growth Rate (2026 - 2031) | 6.43% CAGR |

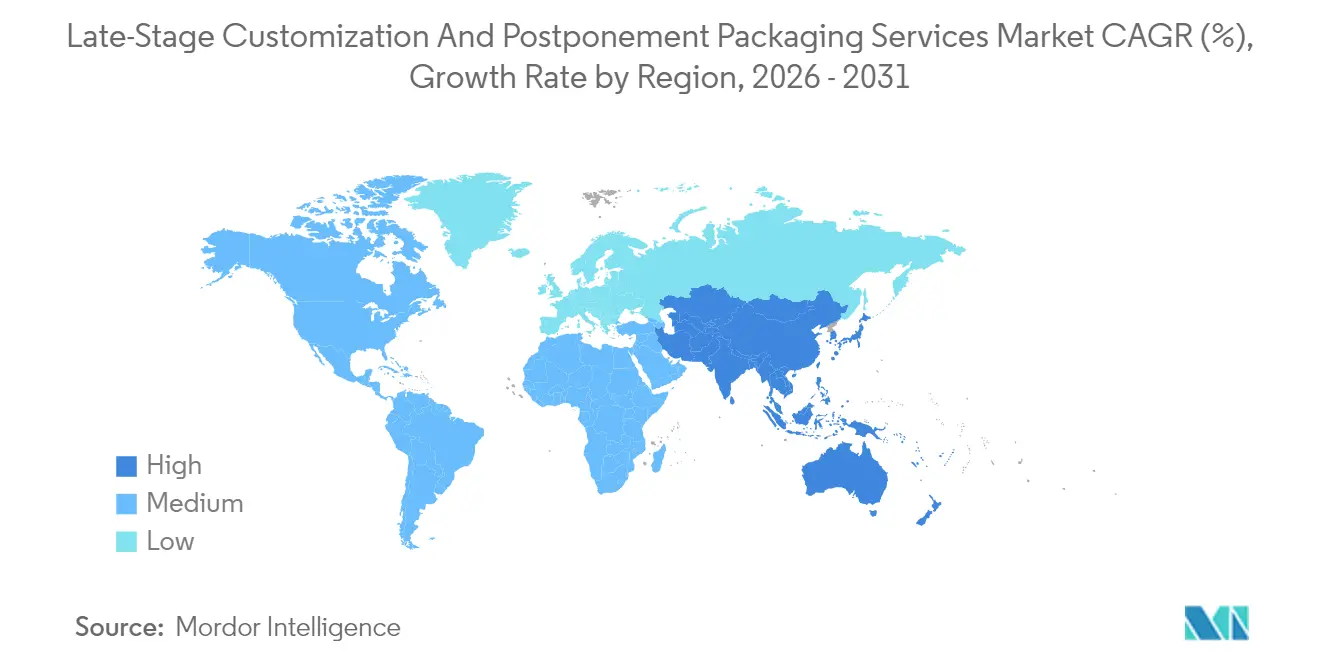

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

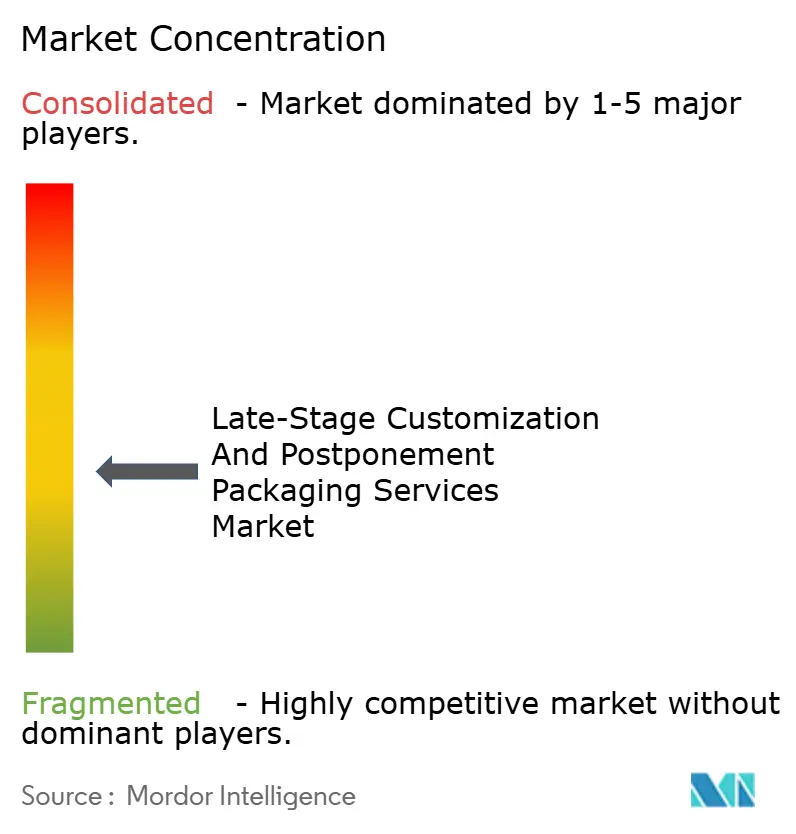

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Late-Stage Customization And Postponement Packaging Services Market Analysis by Mordor Intelligence

The Late-Stage Customization and Postponement Packaging Services market size in 2026 is estimated at USD 5.52 billion, growing from 2025 value of USD 5.19 billion with 2031 projections showing USD 7.54 billion, growing at 6.43% CAGR over 2026-2031. Heightened omnichannel activity, continuous SKU expansion, and rising expectations for personalization keep demand robust. Brands defer finishing operations until a customer order is confirmed, reducing finished-goods inventory, slashing obsolescence risk, and capturing premium pricing from mass-customized packs. Logistics leaders and specialty converters are racing to automate high-mix lines, while predictive analytics are shortening order-to-ship windows from weeks to days. Sustainability regulations add momentum by rewarding right-sized packs that travel lighter and are more easily recyclable. Capital-intensive automation, cybersecurity safeguards, and multi-country compliance frameworks temper near-term growth yet simultaneously raise entry barriers for smaller rivals, shaping a disciplined competitive field.

Key Report Takeaways

- By service type, kitting and assembly captured 33.58% of the Late-Stage Customization and Postponement Packaging Services Market share in 2025.

- By packaging format, the Late-Stage Customization and Postponement Packaging Services Market size for pouches and sachets is projected to grow at a 7.62% CAGR between 2026-2031.

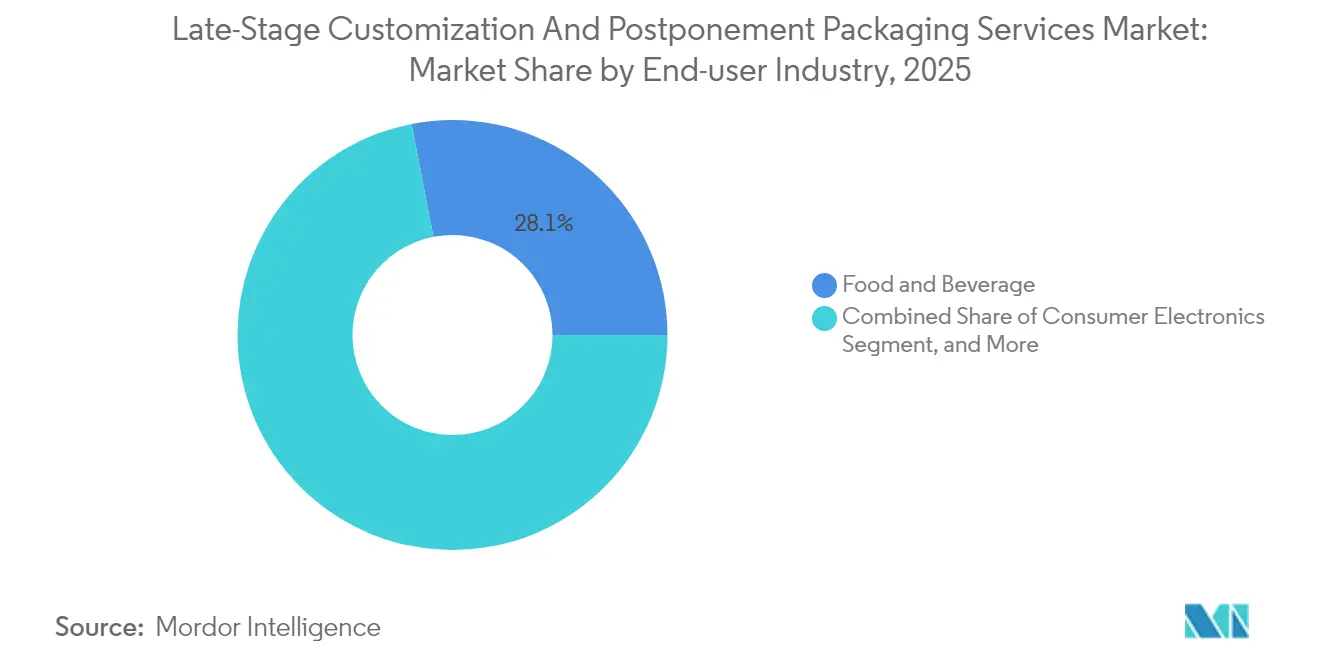

- By end-user industry, food and beverage companies captured 28.05% of the Late-Stage Customization and Postponement Packaging Services Market share in 2025.

- By geography, the Late-Stage Customization and Postponement Packaging Services Market size in Asia-Pacific is projected to grow at 8.21% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Late-Stage Customization And Postponement Packaging Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid SKU-Proliferation in Omnichannel Retail | +1.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Mass-Personalization Trend in Beauty and Nutraceuticals | +0.9% | Global, led by North America and Asia-Pacific | Long term (≥ 4 years) |

| Retailers Shifting Toward Inventory-Light Models | +1.1% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Automation in Late-Stage Packaging Lines | +0.8% | Asia-Pacific core, spillover to North America and Europe | Medium term (2-4 years) |

| Sustainability Push for Right-Sized Packaging | +0.7% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Data-Driven Demand Sensing and Agile Fulfillment | +0.6% | Global, advanced implementation in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid SKU-Proliferation in Omnichannel Retail

SKU counts have multiplied fivefold since 2020 as retailers chase niche consumer segments across webstores, social commerce, and quick-commerce channels. Amazon alone deployed more than 150 label variants for similar items in 2025 to satisfy marketplace-specific language and promotion rules.[1]Amazon, “Private Label Strategy and Packaging Innovations,” Investor Relations, ir.aboutamazon.com This avalanche of configurations forces brand owners to delay pack-outs until the last mile, fueling steady order intake for service providers that can run over 200 changeovers per shift and still meet next-day cut-off times. Complex labeling mandates in the pharmaceutical industry add another layer, making flexible digital print and vision inspection systems indispensable.

Mass-Personalization Trend in Beauty and Nutraceuticals

Beauty majors now empower shoppers to tailor ingredients, dosage, and pack graphics online, then rely on postponement hubs to blend, bottle, and label within 24 hours. L’Oréal disclosed that 60% of premium skincare units shipped in 2025 carried some level of late-stage personalization. These bespoke lines command 20-30% price uplifts while slashing finished-goods inventory by up to 40%, validating the payback on agile pack-out cells. Compliance remains strict: nutraceutical lots must trace individual ingredient batches and meet Food and Drug Administration serialization rules, amplifying demand for data-rich workflows.

Retailers Shifting Toward Inventory-Light Models

Walmart reduced store-level inventory by 35% between 2024 and 2025 by outsourcing pack-outs to near-market postponement centers, which kit seasonal items hours before store delivery. Target achieved 48-hour turnaround for limited-edition drops through similar partnerships, sidestepping the six-week cycles required for pre-packed imports. The model frees cash, trims markdowns, and aligns presentation to hyper-local tastes, keeping the Late-Stage Customization and Postponement Packaging Services market on a solid growth footing.

Automation in Late-Stage Packaging Lines

Robotic cartoners, collaborative labelers, and AI-driven conveyors now execute changeovers in under 30 seconds versus 15-minute manual resets. Omron’s latest platform handles 200 formats an hour, cutting defect rates by 45%. Although price tags range from USD 2 to 5 million per line, scale players secure 3-year paybacks through labor savings and volume upside, accelerating consolidation across the Late-Stage Customization and Postponement Packaging Services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for High-Mix Line Changeovers | -0.8% | Global, particularly affecting smaller providers | Short term (≤ 2 years) |

| Regulatory Complexity Across Multi-Country SKUs | -0.6% | Global, most severe in Europe and North America | Long term (≥ 4 years) |

| Cyber-Physical Security Risks in Connected Lines | -0.4% | Global, heightened in developed markets | Medium term (2-4 years) |

| Brand-Owner Skepticism Toward Outsourcing Core Pack Ops | -0.5% | Global, strongest in traditional industries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for High-Mix Line Changeovers

Flexible systems that fold, fill, label, and seal hundreds of pack styles cost USD 2-5 million each. Smaller converters struggle to fund twin lines for redundancy, which delays fleet upgrades and limits their geographic reach. Deutsche Post committed USD 200 million to automate Asia-Pacific hubs in 2025, illustrating the scale threshold newcomers must match.

Regulatory Complexity Across Multi-Country SKUs

A single pharmaceutical postponement hub may manage 50 labeling regimes, encompassing languages, barcodes, safety icons, and recyclability proofs. The European Union’s 2025 directive now requires material-level recyclability reporting that feeds data back to the shipper for every export pack. Non-compliance leads to multi-million-dollar recalls, prompting brand owners to limit volumes to partners with proven regulatory expertise and certified quality systems.[2]European Union, “Packaging and Packaging Waste Directive Updates,” eur-lex.europa.eu

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Assembly Operations Drive Market Leadership

Kitting and assembly generated the largest slice of the Late-Stage Customization and Postponement Packaging Services market size in 2025 as manufacturers bundled components, accessories, and inserts into channel-specific packs. The segment thrives on high-volume demand from e-commerce players that push 40% of private-label items through kitting workflows. Automated pick-to-light systems and collaborative robots lift throughput, making kitting lines a core profit engine for multi-site providers.

Postponement packaging, despite having a smaller base, registers the highest 8.02% CAGR, thanks to an expanding uptake in cosmetics, electronics, and pharmaceuticals. Growth accelerates as cloud order-management platforms provide precise instructions to line-side printers and labelers, eliminating tooling delays and enabling on-demand variance. As clients migrate from bulk shipments to store-ready packs, demand for custom pack-out and bundling services rises steadily, particularly for promotional tech accessories that refresh quarterly.

By Packaging Format: Sustainability Reshapes Format Preferences

Corrugated cartons retain their leadership position with 30.62% of the Late-Stage Customization and Postponement Packaging Services market share, as they meet retailer strength specifications, stack efficiently, and are recyclable in existing curbside streams. Right-sizing algorithms reduce board usage by up to 18% per shipper, highlighting carton versatility. Pouches and sachets outpace every other format, expanding at a 7.62% annual rate as personal care and snacks shift toward lightweight flexibles that reduce freight emissions by 30%. Brands capitalize on extended shelf impressions by printing vivid variable graphics just seconds before shipping.

Blister and clamshell packs remain critical to regulated healthcare channels, where tamper-evident packaging is mandatory. Bottles and jars dominate the premium nutraceutical and cosmetics markets, particularly when glass conveys quality cues. Secondary retail-ready displays rise in line with the growth of the club-store channel, prompting service providers to invest in multi-depth die-cutters and color-accurate print lines. Recycled-content mandates in Europe and pending laws in North America are driving experimentation with fiber-based and compostable materials, influencing the format mix across the Late-Stage Customization and Postponement Packaging Services market.

By End-user Industry: Electronics Lead Digital Transformation

Consumer electronics is forecasted to grow at an annual rate of 8.04% through 2031, the fastest pace among verticals. Rapid product refresh cycles and regional accessory bundles force brands to keep devices in generic bulk until last-minute pack-out in destination hubs. Apple and Samsung each orchestrated multi-region phone launches in 2025 with less than two weeks of finished goods inventory on hand, demonstrating the agility of postponement.

Food and beverage anchors drive revenue with a 28.05% share, following decades of outsourced co-packing relationships. Tight shelf-life windows and allergen labeling regulations support stable, recurring volumes. Cosmetics and personal care continue their surge in personalization, utilizing print-on-demand labels for ingredient callouts and QR-linked skin diagnostics. Pharmaceuticals maintain premium fee structures due to cold-chain, serialization, and audit requirements, ensuring healthy profitability for certified operators.

Geography Analysis

North America accounts for 32.18% of 2025 revenue, underlined by the deepest e-commerce penetration and harmonized logistics standards. Hub clusters in Ohio, Texas, and California enable one-day service to over 70% of U.S. households. The FDA's pathways for label amendments further streamline the postponement of prescription drugs. Canada’s bilingual labeling keeps steady work flowing to border-state packers.

Asia-Pacific is projected to deliver an 8.21% CAGR through 2031, the steadiest climb in the Late-Stage Customization and Postponement Packaging Services market. China’s manufacturing base couples assembly and pack-out within megasites, cutting export lead times by a week. Government incentives in Vietnam, Malaysia, and India reduce import duties on automation hardware, encouraging local service providers to adopt robotics. Japan and South Korea sit at the frontier of high-mix automation, fielding cobots that can swap end-effectors autonomously.

Europe maintains mid-single-digit growth under a dense compliance umbrella. The 2025 Packaging and Packaging Waste Directive encourages the adoption of digital twin tracking, enabling converters to document the recycled inputs. Germany and the Netherlands coordinate cross-border fulfillment via rail-linked distribution parks. Demand for recyclable and returnable formats unlocks new assignments for partners that validate cradle-to-gate emissions reductions.

Competitive Landscape

Competition is moderately fragmented, with no operator exceeding a 15% global market share. Logistics conglomerates such as Deutsche Post, XPO, and Kuehne + Nagel invest heavily in multi-client automated hubs, while niche specialists build reputations in the life sciences or premium beauty sectors.[3]Kuehne + Nagel International AG, “Joint Venture with Omron for Packaging Robotics,” home.kuehne-nagel.com Capital scale, global lane coverage, and regulatory expertise distinguish the top tier.

In 2025, Deutsche Post earmarked USD 200 million for Asia-Pacific robotics, and XPO purchased Tjoapack to deepen pharmaceutical know-how, signaling momentum toward consolidation. Technology adoption is now the sharpest wedge in the Late-Stage Customization and Postponement Packaging Services market. AI scheduling, computer vision QC, and digital twin simulations reduce labor, prevent recalls, and increase throughput.

Providers that integrate smart packaging data into demand-sensing engines win contract extensions as brand owners pursue inventory-light agendas. White-space potential persists in Africa and parts of Latin America where modern postponement hubs remain scarce. Temperature-controlled biologics and blockchain traceability represent premium niches with high compliance hurdles that limit intrusions from low-capex newcomers.

Late-Stage Customization And Postponement Packaging Services Industry Leaders

Deutsche Post AG

XPO, Inc.

Ryder System, Inc.

GXO Logistics, Inc.

Geodis S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Deutsche Post DHL Group announced a USD 200 million investment in automated packaging facilities across Asia-Pacific, expanding late-stage customization capacity.

- October 2025: XPO Logistics completed the USD 180 million acquisition of Tjoapack’s European operations, enhancing pharmaceutical postponement services.

- September 2025: GXO Logistics launched its Smart Packaging platform, mixing AI and machine learning to cut changeover times 40%.

- August 2025: Ryder System opened a 500,000 ft² automated packaging facility in Ohio aimed at high-mix electronics and automotive assignments.

Global Late-Stage Customization And Postponement Packaging Services Market Report Scope

The Late-Stage Customization and Postponement Packaging Services Market Report is Segmented by Service Type (Kitting and Assembly, Labeling and Printing, Custom Pack-Out and Bundling, Postponement Packaging, and Other Service Types), Packaging Format (Corrugated Cartons, Pouches and Sachets, Blister and Clamshell Packs, Bottles and Jars, Secondary Retail-Ready Displays, and Other Packaging Formats), End-user Industry (Food and Beverage, Cosmetics and Personal Care, Pharmaceuticals, Consumer Electronics, and Others End-user Industry), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD) and tracks the services market for the study scope for the segments captured.

| Kitting and Assembly |

| Labeling and Printing |

| Custom Pack-Out and Bundling |

| Postponement Packaging |

| Other Services |

| Corrugated Cartons |

| Pouches and Sachets |

| Blister and Clamshell Packs |

| Bottles and Jars |

| Secondary Retail-Ready Displays |

| Other Packaging Formats |

| Food and Beverage |

| Cosmetics and Personal Care |

| Pharmaceuticals |

| Consumer Electronics |

| Others End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service | Kitting and Assembly | ||

| Labeling and Printing | |||

| Custom Pack-Out and Bundling | |||

| Postponement Packaging | |||

| Other Services | |||

| By Packaging Format | Corrugated Cartons | ||

| Pouches and Sachets | |||

| Blister and Clamshell Packs | |||

| Bottles and Jars | |||

| Secondary Retail-Ready Displays | |||

| Other Packaging Formats | |||

| By End-user Industry | Food and Beverage | ||

| Cosmetics and Personal Care | |||

| Pharmaceuticals | |||

| Consumer Electronics | |||

| Others End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Late-Stage Customization and Postponement Packaging Services market in 2026?

The market is valued at USD 5.52 billion in 2026 and is projected to grow to USD 7.54 billion by 2031 at a 6.43% CAGR.

Which region is growing fastest for late-stage packaging services?

The Asia-Pacific region posts the highest 8.21% CAGR through 2031, driven by manufacturing consolidation and rising demand for personalization.

What service type dominates industry revenue today?

Kitting and assembly lead with a 33.58% share in 2025, thanks to its versatility across e-commerce and promotional bundling.

Why are pouches and sachets outpacing other formats?

They deliver lightweight, right-sized, and recyclable benefits, helping brands cut freight emissions and comply with stricter sustainability rules.

How has automation changed operational economics?

Robotics and AI now enable sub-30-second changeovers, increasing line utilization while reducing defect rates by up to 45%.

Which end-use vertical shows the fastest adoption?

Consumer electronics advances at an 8.04% CAGR as device makers rely on postponement to manage rapid product refresh cycles across global markets.

Page last updated on: