Laparoscopic Gynecological Procedures Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

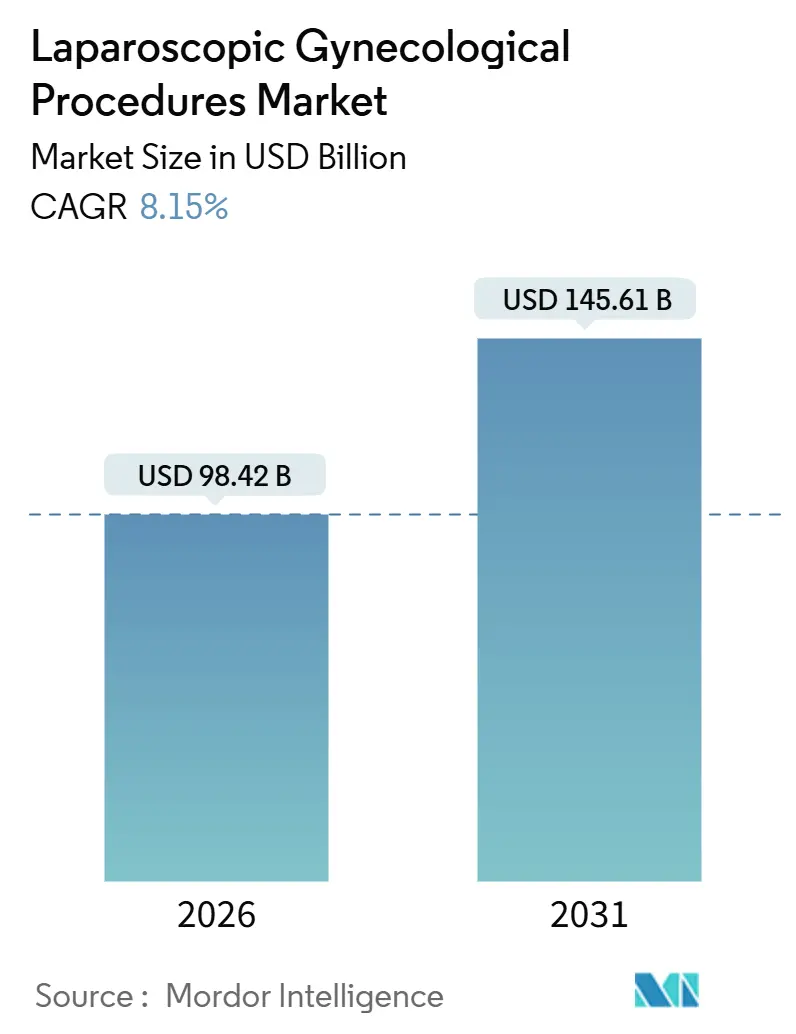

| Market Size (2026) | USD 98.42 Billion |

| Market Size (2031) | USD 145.61 Billion |

| Growth Rate (2026 - 2031) | 8.15% CAGR |

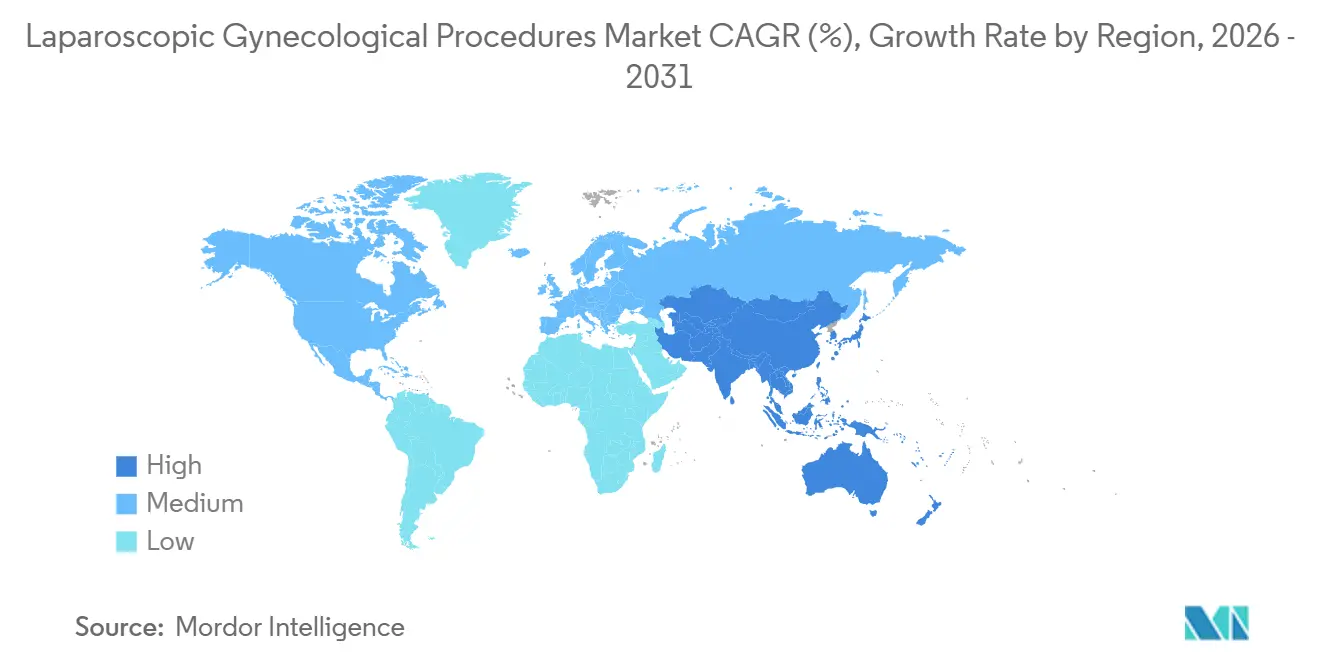

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

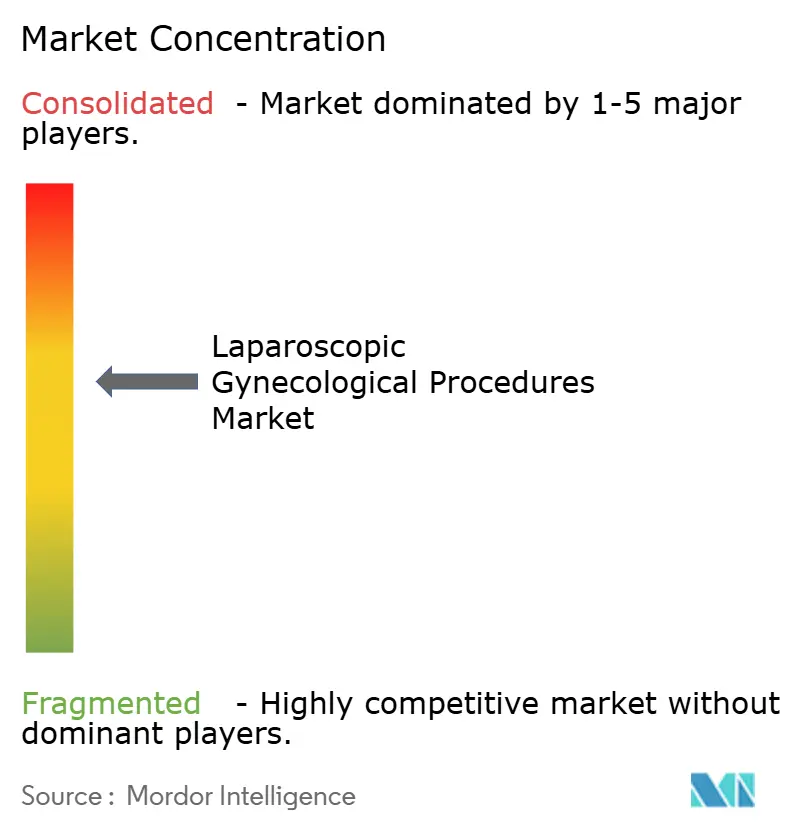

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laparoscopic Gynecological Procedures Market Analysis by Mordor Intelligence

The Laparoscopic Gynecological Procedures Market size is estimated at USD 98.42 billion in 2026, and is expected to reach USD 145.61 billion by 2031, at a CAGR of 8.15% during the forecast period (2026-2031).

Platform advances that shorten learning curves, site-of-service reforms that reward same-day discharge, and patient demand for faster recovery are anchoring this expansion. Ambulatory surgery centers are drawing case volume once tied to multi-day inpatient stays, while AI-guided imaging and energy devices cut operative time and blood loss. Insurers now bundle episodes of care, steering members toward high-volume teams that deliver predictable outcomes. Robots with force-sensing tools, vNOTES techniques that avoid visible scars, and registry-backed quality metrics together reinforce the shift from open to minimally invasive practice.

Key Report Takeaways

- By procedure, laparoscopic hysterectomy captured 69.55% of the laparoscopic gynecological procedures market share in 2025 and endometrial excision is advancing at a 10.25% CAGR through 2031.

- By care delivery mode, inpatient settings held 55.53% of revenue in 2025 while ambulatory surgery centers are expanding at a 12.85% CAGR to 2031.

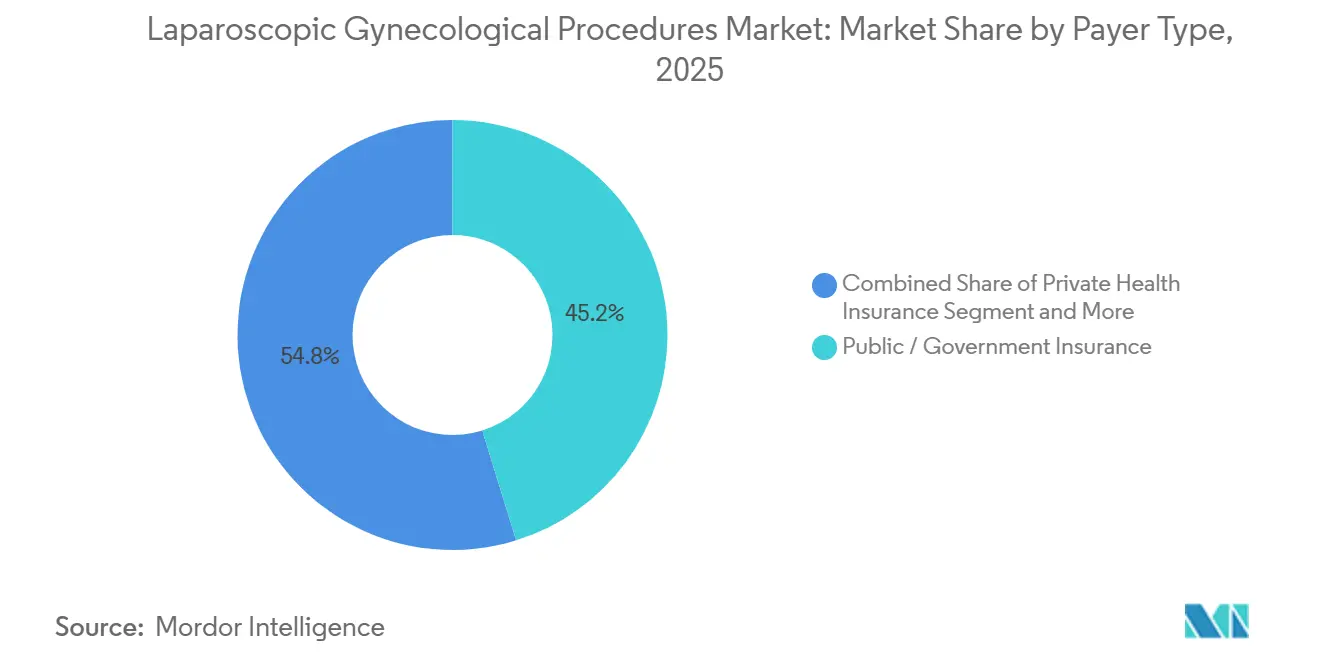

- By payer type, public programs contributed 45.23% of 2025 revenue and private insurance shows an 11.15% CAGR across the forecast horizon.

- By geography, North America generated 42.15% of 2025 value and Asia-Pacific is the fastest-growing region with a 10.51% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Laparoscopic Gynecological Procedures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Minimally-invasive surgery preference surge | +2.1% | Global, highest in North America and Western Europe | Medium term (2-4 years) |

| Technological leaps in optics, energy, and robotics | +1.8% | North America, Europe, APAC urban centers | Long term (≥ 4 years) |

| Rising prevalence of fibroids and endometriosis | +1.5% | Global, elevated in APAC and Sub-Saharan Africa | Long term (≥ 4 years) |

| ASC day-surgery economics reshaping procedure mix | +1.3% | North America, Western Europe, Australia | Short term (≤ 2 years) |

| AI-enabled digital operating rooms | +0.9% | North America, select European centers | Medium term (2-4 years) |

| vNOTES adoption | +0.6% | Europe and emerging in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Minimally-Invasive Surgery Preference Surge

Patient expectations for shorter recovery and smaller scars continue to redirect demand toward laparoscopy and robotics. A 2024 JAMA Surgery study showed women returned to normal activity 18 days sooner after laparoscopic hysterectomy than after open surgery. Social media amplifies these stories, encouraging referral shifts toward surgeons who advertise minimally invasive credentials. Updated 2024 guidance from ACOG recommends laparoscopic hysterectomy as first-line whenever feasible, strengthening the trend. Urban centers with robotic capacity absorb complex cases, while smaller hospitals face volume thresholds they struggle to meet. This divergence underlines why the laparoscopic gynecological procedures market keeps concentrating in high-throughput facilities.

Technological Leaps in Optics, Energy, and Robotics

FDA clearance of the da Vinci 5 system in March 2024 introduced force-sensing instruments that restore haptic cues and cut inadvertent tissue trauma. Surgical Endoscopy’s 2024 meta-analysis reported a 13.67-minute mean time savings when 3D cameras replaced 2D scopes. Advanced energy platforms now seal and divide vessels in one motion, reducing instrument exchanges. Medtronic’s Hugo study, launched October 2025, targets a 30% list-price discount versus incumbents, challenging hospitals to rethink capital budgets. Johnson & Johnson’s single-column OTTAVA robot further reduces footprint constraints, a key adoption barrier in older OR suites. These shifts enlarge the laparoscopic gynecological procedures market by removing technical and cost hurdles.

Rising Prevalence of Fibroids and Endometriosis

Fertility and Sterility estimated in 2024 that endometriosis now affects about 10% of women of reproductive age, up from prior estimates, a pattern tied to delayed childbearing and sharper imaging modalities. Fibroids remain ubiquitous, and when medical therapy fails, surgery follows. Excisional approaches outperform ablation in long-term disease control, fueling demand for precise laparoscopic techniques. The WHO’s 2024 action plan calls for broader surgical access in low-resource regions, adding to global procedure volume. Asia-Pacific faces the steepest case-growth curve, aiding regional expansion in the laparoscopic gynecological procedures market.

ASC Day-Surgery Economics Reshaping Procedure Mix

CMS added laparoscopic hysterectomy to the ASC covered list in January 2024, instantly unlocking a 20-30% facility-fee advantage over hospital outpatient departments[1]Centers for Medicare & Medicaid Services, “CMS Updates to ASC Covered Procedures List,” CMS, cms.gov. UnitedHealthcare and Anthem tightened prior authorization for inpatient stays, accelerating migration to same-day settings. Health Affairs reported same-day discharge rates climbing from 42% in 2023 to 61% in 2025 under ERAS pathways. Equity partnerships attract high-volume surgeons to ASC chains, aligning incentives around efficiency. Although rural areas lag due to limited facility density, metropolitan markets display rapid share capture, deepening the economic foundation of the laparoscopic gynecological procedures market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High episode cost and reimbursement variability | -1.2% | Global, most acute in the United States and emerging markets | Short term (≤ 2 years) |

| Global shortage of MIS-trained gynecologic surgeons | -0.9% | Sub-Saharan Africa, South Asia, rural North America | Long term (≥ 4 years) |

| Regulatory headwinds over contained morcellation | -0.6% | North America, Europe | Medium term (2-4 years) |

| Sustainability scrutiny on single-use consumables | -0.4% | Europe and select U.S. health systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Episode Cost and Reimbursement Variability

Robotic cases add USD 2,000-3,500 in disposables and depreciation versus standard laparoscopy, eroding margins unless surgeons exceed 50 cases annually, a threshold many do not meet. Medicare trimmed 2024 surgeon fees for laparoscopic hysterectomy by 3.2%, and commercial payers tie reimbursement to readmission metrics, shifting risk to providers. In India, Ayushman Bharat reimburses only INR 18,000 (USD 215) for laparoscopic hysterectomy, well below cost, discouraging participation. Such mismatches complicate capital planning and slow adoption in cost-sensitive regions, applying downward pressure on the laparoscopic gynecological procedures market CAGR.

Global Shortage of MIS-Trained Gynecologic Surgeons

The AAGL reported in 2024 that only 38% of U.S. residency programs host minimally invasive fellowships, and retirement of open-trained seniors widens the gap. A 2025 Lancet Global Health survey found 14 sub-Saharan countries without a single fellowship-trained laparoscopic gynecologic surgeon. Simulation labs and tele-proctoring help, but bandwidth and funding gaps persist. The learning curve for robotic hysterectomy is 20-40 cases, deterring mid-career physicians who fear short-term productivity loss. Scarce talent restricts geographic spread, muting growth for the laparoscopic gynecological procedures market in underserved zones.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Procedure: Hysterectomy Dominance Meets Excision Momentum

Laparoscopic hysterectomy accounted for 69.55% of the laparoscopic gynecological procedures market share in 2025 as the most common major surgery for women over 40. This dominance reflects definitive treatment for fibroids, adenomyosis, and abnormal bleeding. Myomectomy addresses fertility preservation but demands multi-layer suturing and meticulous tissue extraction. Colpopexy corrects prolapse by anchoring the vaginal cuff to the sacral promontory and has regained traction after transvaginal mesh restrictions. Diagnostic laparoscopy now pairs with therapy, lowering its standalone contribution.

Laparoscopic endometrial excision is projected to grow at a 10.25% CAGR to 2031, the highest among procedure types, and is expected to lift the laparoscopic gynecological procedures market size for this niche markedly. Randomized data in 2024 showed excision halves five-year reoperation compared with ablation, a finding that resonates with value-based insurers. Adnexal surgery benefits from opportunistic salpingectomy protocols that reduce ovarian cancer risk, endorsed by SGO in 2024[2]Society of Gynecologic Oncology, “Opportunistic Salpingectomy Guidelines,” SGO, sgo.org. New curved vessel-sealing tools approved by FDA in late 2024 broaden the reach of robotic platforms in complex cases.

By Care Delivery Mode: ASC Surge Reshapes Inpatient Mix

Inpatient facilities retained 55.53% of volume in 2025, mainly for high-risk patients with obesity or coagulopathy. Outpatient hospital units offer under-23-hour observation and handle intermediate acuity. Ambulatory surgery centers, expanding at a 12.85% CAGR, gain from CMS policy shifts and payer steerage, lifting the overall laparoscopic gynecological procedures market size in the outpatient setting.

Robotic systems extend complex hysterectomies into ASC suites, compressing the technical threshold for same-day discharge. An Obstetrics & Gynecology study in 2025 documented a 2.1% unplanned admission rate after robotic hysterectomy in ASCs, comparable to hospital outpatient benchmarks. Insurers demand medical necessity evidence—BMI > 40, extensive adhesions—before approving inpatient care, reinforcing ASC momentum within the laparoscopic gynecological procedures market.

By Payer Type: Private Insurance Outpaces Public Programs

Public insurance, led by Medicare, contributed 45.23% of 2025 revenue. Medicaid’s role shifts by state, with non-expansion regions imposing extra prior authorization. Private carriers are growing at an 11.15% CAGR and encourage center-of-excellence networks that package the laparoscopic gynecological procedures market size into bundled episodes. High-deductible plans expose patients to real pricing, prompting migration to lower-fee ASCs.

Walmart set a USD 12,000 reference price for laparoscopic hysterectomy in 2024, creating a national benchmark for self-insured employers. Medicare Advantage plans test 90-day bundled payments covering imaging, surgery, and recovery, aligning physician, facility, and rehab incentives. These experiments accelerate efficiency and shape purchasing behaviors across the laparoscopic gynecological procedures market.

Geography Analysis

North America generated 42.15% of 2025 revenue, supported by 4,565 installed da Vinci systems and mature ERAS pathways that enabled 61% same-day discharge for laparoscopic hysterectomy. Canada pilots robotic hubs where multiple hospitals share platforms to stretch capital budgets, and Mexico’s private sector courts U.S. medical tourists with pricing 40-60% below domestic rates.

Asia-Pacific will post a 10.51% CAGR to 2031, the fastest among regions. China’s provincial quality registries launched in 2025 benchmark outcomes and reward minimally invasive adoption. Indian hospital chains such as Apollo and Fortis reported a 38% rise in robotic gynecology volume during 2025, emphasizing urban middle-class demand. Japan expanded reimbursement for laparoscopic colpopexy in 2024, while Australia cleared the Hugo robot in September 2025, injecting price competition.

Europe navigates the Medical Device Regulation that took full effect in May 2024, raising post-market reporting requirements. Germany and the United Kingdom lead in robot installs, with NHS England allocating GBP 150 million to equip 30 more hospitals by 2027. France’s health authority now favors laparoscopic over vaginal hysterectomy for women with prior cesareans, citing lower bladder injuries. Italy and Spain face budget limits but teaching centers in Milan and Barcelona promote vNOTES to reduce equipment spend.

The Middle East invests through Vision 2030, allocating SAR 2 billion to expand minimally invasive capacity in Saudi Arabia[3]Saudi Vision 2030, “Healthcare Sector Investment Allocation,” Government of Saudi Arabia, vision2030.gov.sa. South Africa’s private sector matches Western standards, yet public hospitals grapple with equipment shortages. Sub-Saharan Africa’s surgeon gap, highlighted by a 2025 Lancet survey, curtails adoption despite rising disease burden. South America is led by Brazil’s SUS public system, but Argentina’s capital constraints stalled new robot purchases since 2024.

Competitive Landscape

Competition in the laparoscopic gynecological procedures market centers on technology access, payer contracting, and surgeon throughput. Integrated delivery networks such as HCA Healthcare and Kaiser Permanente use scale to negotiate bundled rates and deploy capital for new robots. Academic medical centers chase complex cases that bolster teaching missions and justify high-end platforms. Independent ASCs counter with transparent pricing, short wait times, and equity incentives for high-volume surgeons, typically undercutting hospital fees by up to 30%.

Intuitive Surgical’s da Vinci 5 brought force-sensing tools and perfusion imaging to market in 2024, raising the standard for tactile feedback. Medtronic counters with a lower-priced Hugo platform under U.S. investigational study since October 2025, while Johnson & Johnson’s compact OTTAVA system received IDE approval in November 2024, aiming at space-constrained ORs. Patent pipelines emphasize AI-guided dissection and automated suturing, suggesting software will differentiate future offerings.

Supply chains adapt to sustainability mandates; hospitals increasingly demand reusable ports yet still pay premiums for single-use energy inserts. Vendors respond with reprocessing programs that balance carbon goals and sterility concerns. Negotiations now involve episode-of-care warranties where manufacturers share risk for instrument failure. Moderate fragmentation persists as the top five U.S. health systems account for less than 45% of laparoscopic gynecological procedures market volume, leaving room for insurgent ASC chains and regional hospital groups.

Laparoscopic Gynecological Procedures Industry Leaders

HCA Healthcare

Ascension Health

Mayo Clinic

Cleveland Clinic Health System

Kaiser Permanente

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Fiji’s first laparoscopic hysterectomy performed at Lautoka Hospital under Aspen Medical management, marking a milestone for Pacific women’s health.

- June 2025: Cleveland Clinic published ERAS outcomes for laparoscopic hysterectomy showing a 78% same-day discharge rate and a 1.9% 30-day readmission, outperforming national averages and informing adoption across 12 other systems.

Global Laparoscopic Gynecological Procedures Market Report Scope

As per the scope of the report, laparoscopic gynecological procedures are minimally invasive surgical techniques performed on the female reproductive system using small incisions and a laparoscope (a thin, lighted tube with a camera).

The segmentation of the laparoscopic gynecological procedures market is categorized by procedure, care delivery mode, payer type, and geography. By procedure, it includes laparoscopic hysterectomy, laparoscopic myomectomy, laparoscopic colpopexy, laparoscopic endometrial excision, laparoscopic adnexal surgery, and diagnostic laparoscopy. By care delivery mode, it is segmented into inpatient (≥24-hr LOS), outpatient hospital (≤23-hr LOS), and ambulatory surgery centers/day-care. By payer type, the market is divided into public/government insurance, private health insurance, and self-pay & others. By geography, the segmentation covers North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| Laparoscopic Hysterectomy |

| Laparoscopic Myomectomy |

| Laparoscopic Colpopexy |

| Laparoscopic Endometrial Excision |

| Laparoscopic Adnexal Surgery |

| Diagnostic Laparoscopy |

| Inpatient (?24-hr LOS) |

| Outpatient Hospital (?23-hr LOS) |

| Ambulatory Surgery Centers / Day-Care |

| Public / Government Insurance |

| Private Health Insurance |

| Self-pay & Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Procedure | Laparoscopic Hysterectomy | |

| Laparoscopic Myomectomy | ||

| Laparoscopic Colpopexy | ||

| Laparoscopic Endometrial Excision | ||

| Laparoscopic Adnexal Surgery | ||

| Diagnostic Laparoscopy | ||

| By Care Delivery Mode | Inpatient (?24-hr LOS) | |

| Outpatient Hospital (?23-hr LOS) | ||

| Ambulatory Surgery Centers / Day-Care | ||

| By Payer Type | Public / Government Insurance | |

| Private Health Insurance | ||

| Self-pay & Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the laparoscopic gynecological procedures space in 2026 and how fast is it growing?

The segment is valued at USD 98.42 billion in 2026 and is advancing at an 8.15% CAGR toward USD 145.61 billion by 2031.

Which procedure currently generates the highest revenue?

Laparoscopic hysterectomy leads with 69.55% of total 2025 revenue thanks to its role as the definitive treatment for fibroids and adenomyosis.

Why are ambulatory surgery centers gaining share so quickly?

CMS and private payer rule changes now reimburse many laparoscopic codes in ASCs, yielding 20-30% facility-fee savings and driving a 12.85% CAGR for ASC volumes.

What makes Asia-Pacific the fastest-growing region?

China's 2025 quality registries, India's large hospital chains investing in robots, and rising endometriosis awareness collectively deliver a 10.51% regional CAGR.

How do robotic systems justify their higher upfront cost?

Force-sensing tools, 3D vision, and integrated energy devices trim operative time, lower complication rates, and enable same-day discharge, which align with bundled-payment incentives.

What is a key barrier limiting wider adoption in low-resource settings?

A global shortage of fellowship-trained minimally invasive surgeons - especially in Sub-Saharan Africa and rural South Asiarestricts procedure availability despite growing disease burden.

Page last updated on: