Lactation Support Supplements Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

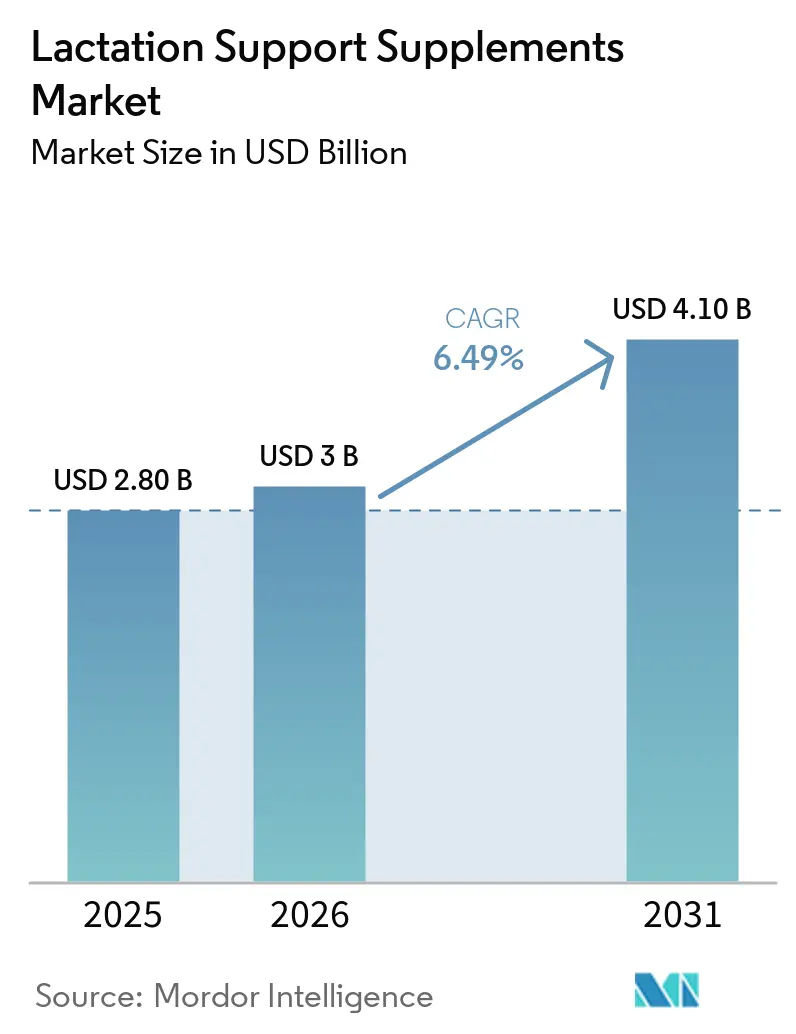

| Market Size (2026) | USD 3 Billion |

| Market Size (2031) | USD 4.10 Billion |

| Growth Rate (2026 - 2031) | 6.49% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lactation Support Supplements Market Analysis by Mordor Intelligence

The Lactation Support Supplements Market size is expected to increase from USD 2.80 billion in 2025 to USD 3 billion in 2026 and reach USD 4.10 billion by 2031, growing at a CAGR of 6.49% over 2026-2031.

Asia Pacific dominated the lactation support supplements market share in 2025, led by traditional Chinese medicine adoption and strong familial influence on purchase intent. In North America, Target’s Baby Boutique rollout and Walmart’s nationwide shelf placements have accelerated mass-channel visibility, while Amazon’s 2026 cGMP mandate removed non-compliant listings and raised consumer trust. FDA’s April 2024 New Dietary Ingredient guidance now obliges reproductive and teratology data, prompting manufacturers to fund clinical trials and emphasize substantiation in marketing claims. Parallel growth in e-pharmacy and direct-to-consumer (DTC) subscriptions is increasing access for mothers who prefer discrete home delivery of clean-label products.

Key Report Takeaways

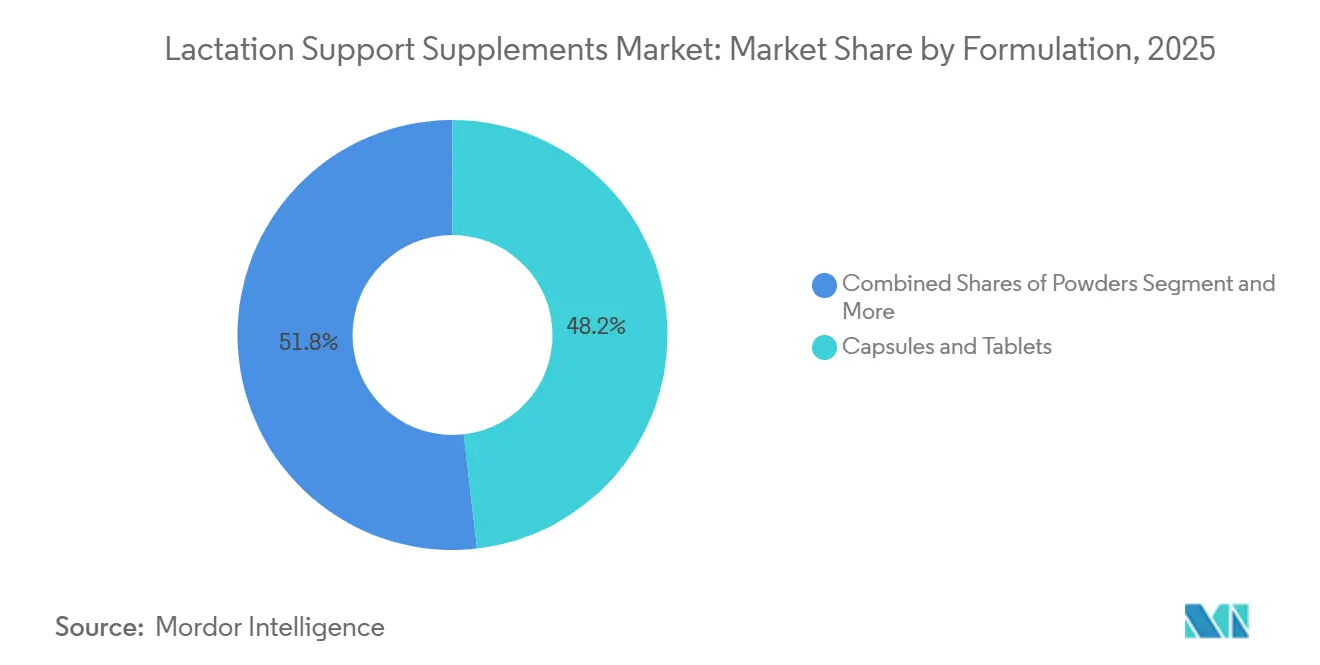

- By formulation, capsules and tablets led with 48.19% revenue share in 2025, while protein-enriched powders are forecast to expand at a 7.56% CAGR through 2031.

- By ingredient type, single-herb products accounted for 56.16% of the lactation support supplements market size in 2025, yet multi-herb blends are the fastest-growing at 8.13% CAGR through 2031.

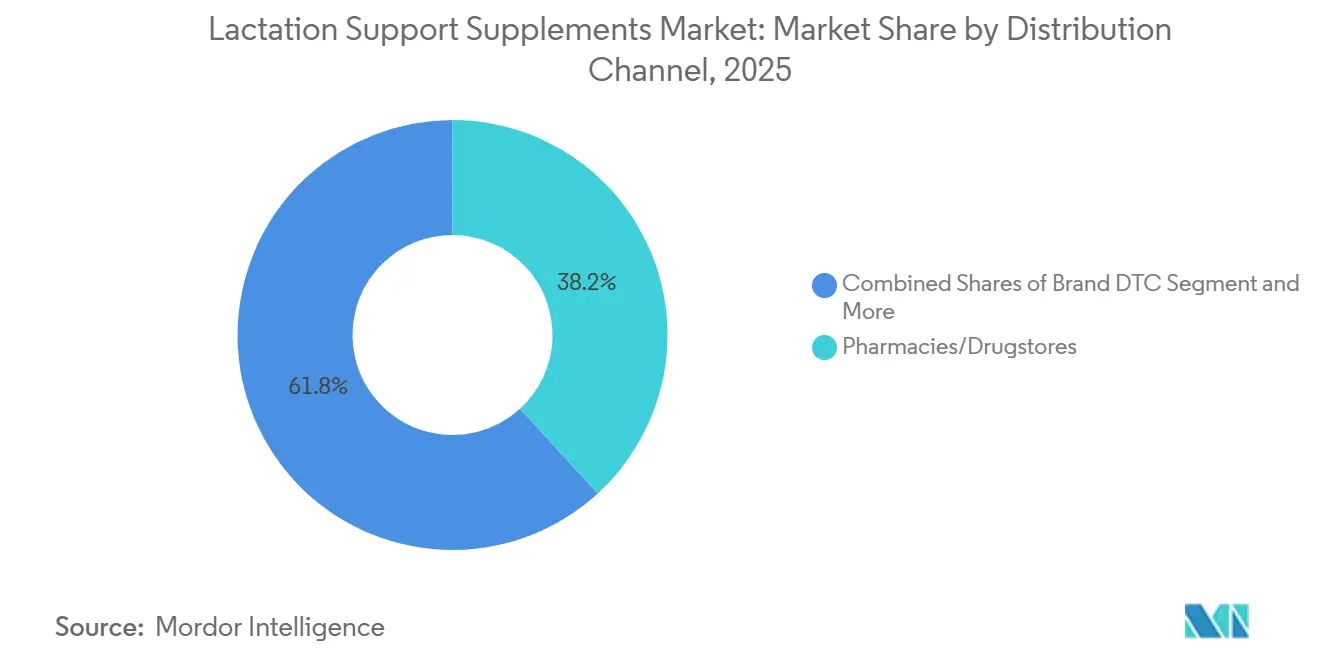

- By distribution channel, pharmacies and drugstores held 38.19% share of the lactation support supplements market size in 2025, whereas online marketplaces are advancing at a 7.88% CAGR to 2031.

- By the end-user stage, early postpartum (0-6 weeks) commanded 43.16% of the lactation support supplements market share in 2025, but extended breastfeeding beyond six months is rising at a 7.58% CAGR through 2031.

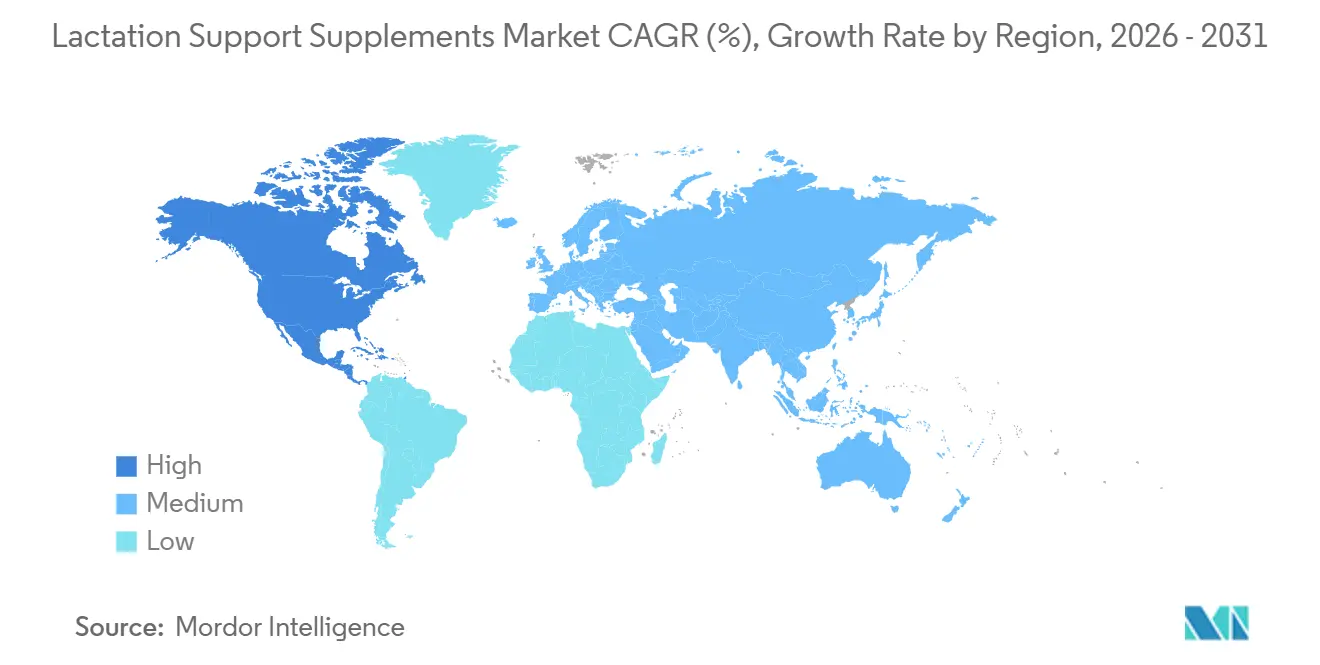

- By geography, Asia-Pacific led the market with 35.18% market share in 2025, whereas North America region is expected to grow at 7.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lactation Support Supplements Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Breastfeeding promotion and postpartum nutrition awareness are accelerating category adoption post-2026 | +1.6% | Global, with concentrated gains in North America, Western Europe, and urban Asia Pacific | Medium term (2-4 years) |

| Rapid expansion of e-commerce, e-pharmacy, and DTC models for maternal supplements | +1.5% | Global, led by North America and Asia Pacific; spillover to Latin America and MEA | Short term (≤2 years) |

| Consumer shift to herbal/clean-label galactagogues and free-from claims | +1.3% | North America, Western Europe, Australia; emerging in urban China and India | Medium term (2-4 years) |

| Fenugreek-free formulations gain share due to side-effect concerns; growth of moringa- and shatavari-led blends | +1.2% | North America core, with early adoption in EU and APAC urban centers | Short term (≤2 years) |

| Big-box retail and mass-channel placement broadening access and trial | +1.4% | North America dominant; selective expansion in Europe and APAC | Short term (≤2 years) |

| Emerging clinical evidence and funded trials for select botanicals improve professional acceptance | +1.5% | Global, with research concentration in India, China, Japan, and North America; regulatory influence from FDA NDI guidance requiring reproductive toxicity data | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Breastfeeding Promotion and Postpartum Nutrition Awareness Accelerating Category Adoption Post-2026

WHO’s 2030 goal to raise exclusive breastfeeding to 60% is mobilizing public-health campaigns that normalize supplements as supportive tools, even while clinical guidelines stay conservative [1]World Health Organization, “Global Breastfeeding Targets,” who.int. In South Asia, 64.7% of formula users cite perceived low milk supply and 52% receive professional formula advice, a gap that brands address with education and testimonials. North America shows only 25% exclusive breastfeeding at six months despite 83% initiation, leaving many mothers seeking interventions to extend nursing duration. Japan’s persistent exclusivity challenges linked to primiparity and the pandemic reinforce consumer interest in adjunct galactagogues even in advanced healthcare systems. Supportive regulatory frameworks, such as Health Canada’s allowance for traditional-use claims, let brands communicate benefits more openly than in the United States.

Rapid Expansion of E-Commerce, E-Pharmacy, and DTC Models for Maternal Supplements

Amazon’s March 2026 cGMP verification rule, plus AI-driven listing audits, purged low-quality products and rewarded fully documented brands, consolidating the lactation support supplements market online. Perelel doubled revenue in 2025 and secured USD 27 million to scale its stage-specific subscription program that mails monthly packs tailored to prenatal, postnatal, and lactation phases. Moom Health’s USD 2.6 million pre-Series A enables geographic reach into Singapore, Malaysia, and Hong Kong, where e-commerce penetration tops 70% in wellness categories. Subscription economics foster predictable inventory and lower acquisition costs, which attracted Unilever Ventures’ earlier USD 6 million Series A stake in 2024. Labeling relief came via the FDA’s late-2025 disclaimer flexibility, allowing concise product pages without legal risk.

Consumer Shift to Herbal/Clean-Label Galactagogues and Free-From Claims

Fenugreek-free recipes now outpace legacy teas after allergenicity and gastrointestinal complaints, including cross-reactivity with ragweed and legumes, gained clinical attention. Bodily’s Organic Lactation Latte, launched in Target’s 200 boutiques, highlights shatavari, moringa, oats, and goat’s rue, positioning itself as an allergen-sensitive alternative. Legendairy Milk entered Sprouts in March 2026 at USD 16.50-32.99, using organic seals and transparent sourcing to justify premium pricing. A randomized 2025 Indian trial showed that a shatavari-centric multi-herb granule lifted six-month exclusive breastfeeding to 69.8% versus 44.8% in placebo, evidence heavily cited by marketers. Clean Label Project certification, now covering more than 159 SKUs across brands, qualifies products for Amazon’s fast-track listing, improving search visibility.

Big-Box Retail and Mass-Channel Placement Broadening Access and Trial

Target’s specialty Baby Boutiques curate over 2,000 wellness-oriented items and merchandise lactation support supplements alongside postpartum care aids, capturing impulse buys on nursery shopping trips. Willow’s breastfeeding accessories and Bodily’s latte launch demonstrate how emerging brands borrow big-box credibility before steering shoppers to DTC channels for repeat orders. Walmart’s adjacency strategy places Legendairy Milk and Traditional Medicinals next to infant formula, converting parents weighing feeding options into trial purchasers. Sprouts’ natural-channel shopper base spends 30% more per basket and rewards premium organic positioning, as evidenced by Legendairy Milk’s launch. State-level supplement registrations in California, New York, and Florida require facility audits and adverse-event monitoring, adding cost layers for brands pursuing U.S. nationwide rollout.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited high-quality clinical evidence for herbal galactagogues; inconsistent efficacy | -1.1% | Global, with heightened scrutiny in North America and Europe; regulatory influence from ACOG guidelines discouraging first-line galactagogue use | Long term (≥4 years) |

| Safety/tolerability issues (allergenicity, GI effects, drug interactions) for certain botanicals | -0.7% | North America and Europe lead safety surveillance; emerging in APAC as adverse event reporting systems mature; regulatory influence from FDA warning letters and Health Canada content restrictions | Medium term (2-4 years) |

| Tightening scrutiny of supplement health claims and substantiation standards | -0.4% | North America and EU core, with FDA DSHEA modernization (March 2026) and FTC enforcement; spillover to APAC markets adopting Codex standards | Medium term (2-4 years) |

| Formulation standardization, allergen disclosure, and cross-border regulatory variability | -0.3% | Global, with compliance complexity highest for companies operating across FDA (US), Health Canada (NHP framework), EFSA (EU), and FSSAI (India) jurisdictions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Limited High-Quality Clinical Evidence for Herbal Galactagogues; Inconsistent Efficacy

A Cochrane review highlighted low-certainty data from small, heterogeneous trials, challenging clinicians who seek reproducible endpoints [2]Cochrane Collaboration, “Galactagogues for Human Milk Production,” cochranelibrary.com. ACOG’s February 2026 update reiterates that galactagogues should follow, not precede, expert lactation assessment, citing unclear benefit-risk profiles. Fenugreek’s perceived usefulness rests largely on anecdote, with controlled trials failing to show consistent volume increases when frequency and technique are controlled. The Academy of Breastfeeding Medicine prioritizes latch correction and increased nursing frequency over supplements, curbing prescriber enthusiasm. FDA’s 2024 guidance mandates developmental toxicity data for prenatal and lactation targets, lengthening the path for unstudied botanicals and deterring small innovators.

Safety / Tolerability Issues and Tightening Scrutiny of Supplement Health Claims

Documented fenugreek cross-reactivity and maple-syrup odor limit compliance, while hypoglycemia risks in diabetic mothers compound liability fears. Prescription galactagogues offer scant refuge: metoclopramide carries tardive dyskinesia warnings, and domperidone is unapproved stateside over arrhythmia concerns, pushing families back toward botanicals despite their own caveats. FDA’s April 2025 warning letter to Mommy’s Bliss for cGMP failures demonstrates escalating enforcement within maternal niches. Stakeholder comments at FDA’s March 2026 DSHEA modernization meeting urged clarity on novel bio-engineered ingredients, hinting at tougher pre-market reviews ahead. Health Canada’s milk-thistle restrictions show how an emergent hepatotoxicity signal can swiftly squeeze ingredient options across North American SKUs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Formulation: Protein-Enriched Powders Challenge Capsule Dominance

Capsules and tablets retained 48.19% share in 2025 because mothers prize portability during early postpartum, yet powders now rise on the dual promise of milk-supply support and 16-19 g of plant protein per serving, widening the value proposition of the lactation support supplements market. Brands such as Milk Dust and Boobie Body sell fusion blends that stir into smoothies, oatmeal, and baked goods, bypassing pill fatigue. Liquid tinctures and ready-to-drink formats like Bodily’s latte offer sensory novelty but battle flavor-masking and sediment issues in consumer reviews. Cookies and gummies inspire impulse buys at baby specialty stores, priced at USD 8-15, broadening category reach to snack occasions.

The lactation support supplements market continues to see powders gain distribution through both big-box and online stores that champion cleaner labels and visible macros. Formulators leverage pea, brown rice, and pumpkin protein to stay allergen-friendly, blending in shatavari or goat’s rue to retain galactagogue positioning. Manufacturers tout solubility advances and natural flavor systems that reduce the gritty mouthfeel that previously constrained adoption. Competitive tension grows as DTC players introduce single-serve sachets for on-the-go parents, challenging incumbents that rely on larger tubs. Looking forward, value-added characteristics, such as probiotic co-microencapsulation, could allow powders to command higher price points without cannibalizing capsule demand.

By Ingredient Type: Multi-Herb Synergy Outpaces Single-Botanical Legacy Products

Single-herb lines still represent 56.16% of spend, reflecting entrenched fenugreek and moringa SKUs in drugstores, yet consumers are shifting toward multi-herb complexes that promise synergistic phytochemical profiles and diluted side-effect risk, fueling an 8.13% CAGR through 2031. Legendairy Milk’s Milkapalooza illustrates the trend by mixing moringa, nettle, fennel, and shatavari in a single capsule. Clinical momentum supports this pivot: a 2025 RCT showed that the shatavari-based Ayush-SS granule raised six-month exclusivity to 69.8% versus 44.8% placebo, an efficacy delta brands trumpet in marketing [3]Journal of Ayurveda and Integrative Medicine, “Ayush-SS Trial,” sciencedirect.com.

The lactation support supplements market benefits when blends enable lower per-ingredient dosages, dampening gastrointestinal complaints tied to higher fenugreek loads. Fenugreek-free positioning has become a badge of clean-label credibility for Bodily, Binto, and several Legendairy SKUs. Non-herbal options that combine vitamins, minerals, and next-generation probiotics (Lactobacillus fermentum CECT5716, HN001) are also advancing, leveraging over 60 human studies for mastitis prevention and maternal mood support. Such formulations expand addressable audiences to mothers who prefer evidence-backed strains over botanicals alone.

By Distribution Channel: Amazon’s cGMP Mandate Consolidates E-Commerce Leadership

Pharmacies and drugstores owned 38.19% of the value in 2025 because healthcare proximity fosters trust, yet online marketplaces now spearhead growth at 7.88% CAGR as Amazon’s verification policies filter out dubious products and give certified brands algorithmic preference. Direct-to-consumer subscriptions like Perelel’s enjoy high retention and improved cash flow, although marketplace scale still dwarfs proprietary sites. Supermarkets such as Walmart amplify reach into rural zones, placing lactation support supplements market options alongside formula to harness cross-category traffic.

The lactation support supplements market gains from Target’s 200-store boutiques, which situate supplements next to recovery gear to capture first-time mothers who window-shop nursery aisles. Clean Label Project’s fast-track deal with Amazon accelerates compliant launches, effectively turning third-party testing into a promotional lever. Over the forecast horizon, Asia Pacific’s high mobile-commerce usage could see regional platforms mimic Amazon’s cGMP gatekeeping, intensifying the premium on documentation and third-party audits.

By End-User Stage: Extended Breastfeeding Beyond Six Months Drives Fastest Growth

Early postpartum (0-6 weeks) remained the largest cohort at 43.16% in 2025, yet the fastest expansion lies in extended breastfeeding supplements, advancing 7.58% CAGR as mothers work to maintain supply amid job re-entry and complementary-feeding phases. WHO highlights that breast milk still covers more than 50% of infants’ energy at 6-12 months and around 33% at 12-24 months, reinforcing the nutritional rationale for sustained galactagogue use. Human milk oligosaccharides remain present at 5.34 g/L at 12 months and 8.47 g/L past 12 months, further incentivizing prolonged nursing.

The lactation support supplements market could unlock white space by formulating stage-specific blends that supplement minerals depleted during prolonged lactation while avoiding oversupply of early-stage nutrients like choline already addressed in prenatal tablets. Brands also explore adaptive dosing, offering lower-concentration SKUs that mothers can titrate based on infant demand. As workplace lactation rooms and insurance reimbursements expand post-2026, demand for portable single-serve sticks and gummies that fit pumping breaks is expected to climb.

Geography Analysis

North America is the fastest-growing region at 7.74% CAGR through 2031, due to synergistic big-box distribution, Amazon quality enforcement, and high DTC adoption. The United States anchors growth, where the majority of breastfeeding mothers already use galactagogues, but only one fourth maintain exclusivity for six months, a gap the lactation support supplements market continues to monetize. Canada’s Natural Health Product rules permit traditional-use structure-function claims, giving marketers latitude, even as milk-thistle limits tighten safety oversight. Mexico’s urban pharmacies stock limited SKUs, yet national breastfeeding campaigns are boosting awareness, offering upside in the medium term.

Asia Pacific held the largest 35.18% share in 2025. China’s 37.5% TCM adoption rate among pregnant and breastfeeding women showcases cultural acceptance, where subjective norms wield stronger influence (β = 0.435) than perceived efficacy in driving purchases. India’s high formula initiation based on perceived insufficiency offers fertile ground for herbal supplement education. Japan’s exclusive breastfeeding hurdles, compounded by twin births and COVID-19 disruptions, are now coupled with positive RCT evidence for human milk-fortified diets, bolstering professional openness to maternal supplements. South Korea, Singapore, and Australia exhibit high online category penetration, aligning with venture-backed expansions like Moom Health.

Europe’s stringent EFSA claim substantiation adds compliance costs but ensures higher ingredient quality, creating a premium segment for clinically supported blends. Middle East and Africa remain nascent; however, GCC pharmacies and South African e-commerce platforms are beginning to list premium galactagogues. South America’s incremental growth rests on Brazil’s public-health breastfeeding drives and Argentina’s specialty-store rollouts, though macro-economic swings and import duties hamper high-priced imports.

Competitive Landscape

The lactation support supplements market shows moderate fragmentation, with more than a few established brands and an influx of digitally native challengers. Traditional medicinals and Gaia Herbs leverage broad shelf space but face margin pressure as cGMP upgrades and third-party testing inflate costs. Legendairy Milk, Pink Stork, and Motherlove differentiate via organic certification and fenugreek-free SKUs targeting allergen-conscious shoppers.

DTC disruptors such as Perelel and Ritual capitalize on stage-specific subscriptions, enhanced retention, and rich first-party data. Perelel’s USD 27 million raise validates investor appetite for predictable recurring revenue, while Malama Health’s USD 9.2 million seed points to Medicaid-oriented service hybrids that bundle supplements with doula support. Technology adoption centers on public-facing certificates (USP Verified, NSF Certified for Sport, Clean Label Project) that now act as table stakes for Amazon visibility.

Pricing bifurcates the lactation support supplements market: mass-market capsules retail at USD 10-15 per 100-count bottle with margins around 30-40%, whereas premium powders and bundles command USD 30-50 per month at 60%+ gross margins. White-space remains for extended-breastfeeding formulas targeting mothers beyond 12 months, a segment few players explicitly address despite evidence of significant HMO benefits. Overall, strategic levers include allergen-free claims, probiotic integration, and protein fortification, each pursued by both incumbents and newcomers.

Lactation Support Supplements Industry Leaders

Traditional Medicinals

Gaia Herbs

Legendairy Milk

Pink Stork

Motherlove Herbal Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Legendairy Milk entered Sprouts Farmers Market nationwide with four organic-certified SKUs priced at USD 16.50-32.99.

- March 2026: Malama Health raised USD 9.2 million to expand its Medicaid-focused maternal health platform that bundles supplements with doula networks.

Global Lactation Support Supplements Market Report Scope

As per the scope of the report, treatment for lactation support supplements, commonly referred to as galactagogues, are substances used with the aim of increasing breast milk production in nursing mothers. These supplements primarily consist of herbal and botanical ingredients, though they can also include specific vitamins and minerals. Common traditional herbs found in these products include fenugreek, shatavari, blessed thistle, milk thistle, fennel, and moringa. They are available in various forms such as capsules, tablets, teas, tinctures, and more.

The lactation support supplements market is segmented by formulation, ingredient type, distribution channel, end-user stage, and geography. Based on formulation, the market is segmented into capsules and tablets, powders, liquid formulations, and others (cookies and gummies, among others). By ingredient type, the market is segmented into single-herb supplements, multi-herb blends, and non-herbal (vitamin–mineral complexes, probiotics). By distribution channel, the market is segmented into online marketplaces (e-commerce/e-pharmacy), brand DTC (subscriptions), pharmacies/drugstores, and supermarkets/hypermarkets. By end users, the market is segmented into early postpartum (0–6 weeks), established lactation (6 weeks–6 months), and extended breastfeeding (>6 months). By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Capsules and Tablets |

| Powders |

| Liquid Formulations |

| Others |

| Single-Herb Supplements |

| Multi-herb Blends |

| Non-herbal |

| Online Marketplaces (e-commerce/e-pharmacy) |

| Brand DTC (subscriptions) |

| Pharmacies/Drugstores |

| Supermarkets/Hypermarkets |

| Early Postpartum (0–6 weeks) |

| Established Lactation (6 weeks–6 months) |

| Extended Breastfeeding (Greater Than 6 months) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Formulation | Capsules and Tablets | |

| Powders | ||

| Liquid Formulations | ||

| Others | ||

| By Ingredient Type | Single-Herb Supplements | |

| Multi-herb Blends | ||

| Non-herbal | ||

| By Distribution Channel | Online Marketplaces (e-commerce/e-pharmacy) | |

| Brand DTC (subscriptions) | ||

| Pharmacies/Drugstores | ||

| Supermarkets/Hypermarkets | ||

| By End-User Stage | Early Postpartum (0–6 weeks) | |

| Established Lactation (6 weeks–6 months) | ||

| Extended Breastfeeding (Greater Than 6 months) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the lactation support supplements market?

The lactation support supplements market size reached USD 3.0 billion in 2026 and is projected to climb to USD 4.1 billion by 2031.

Which formulation segment is expanding fastest through 2031?

Protein-enriched powders are expected to grow at a 7.56% CAGR by 2031, outpacing capsules, tablets, and liquids, per Mordor Intelligence data.

Why are fenugreek-free supplements gaining popularity?

Clinical reports of allergenicity, cross-reactivity with legumes, and gastrointestinal discomfort have steered consumers toward multi-herb or probiotic alternatives that exclude fenugreek.

Which region leads the market, and which is growing fastest?

Asia Pacific held the largest 35.18% share in 2025, while North America is the fastest-growing at 7.74% CAGR through 2031.

Page last updated on: