Lactate Meter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

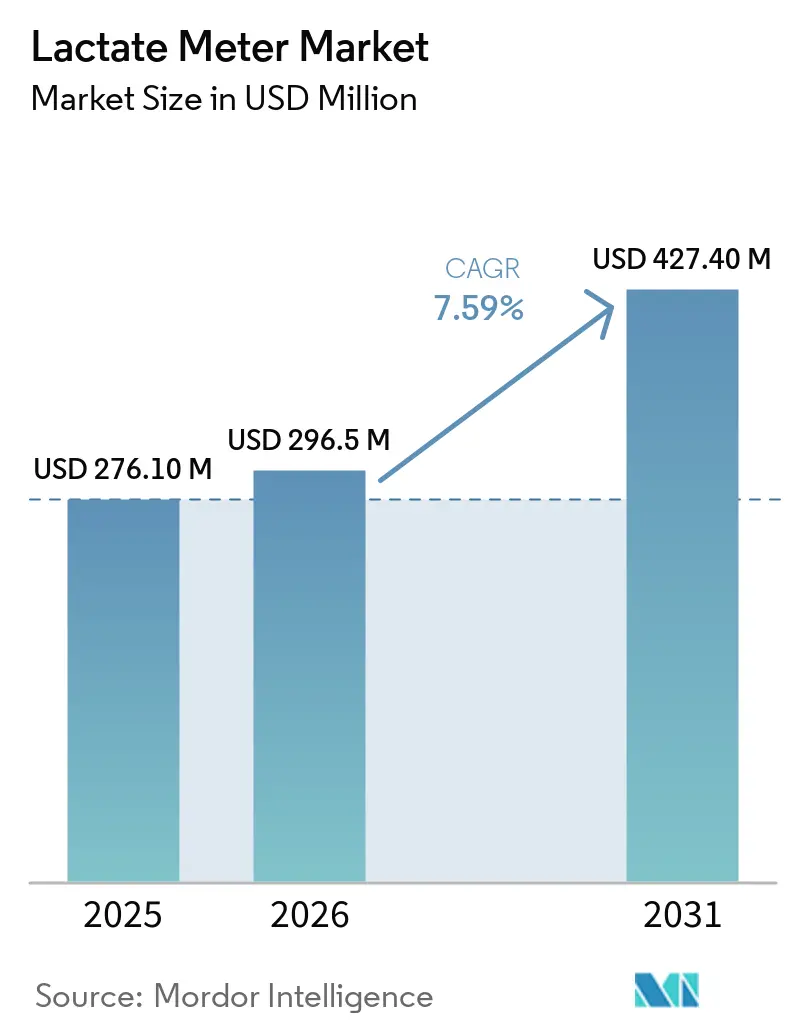

| Market Size (2026) | USD 296.5 Million |

| Market Size (2031) | USD 427.40 Million |

| Growth Rate (2026 - 2031) | 7.59% CAGR |

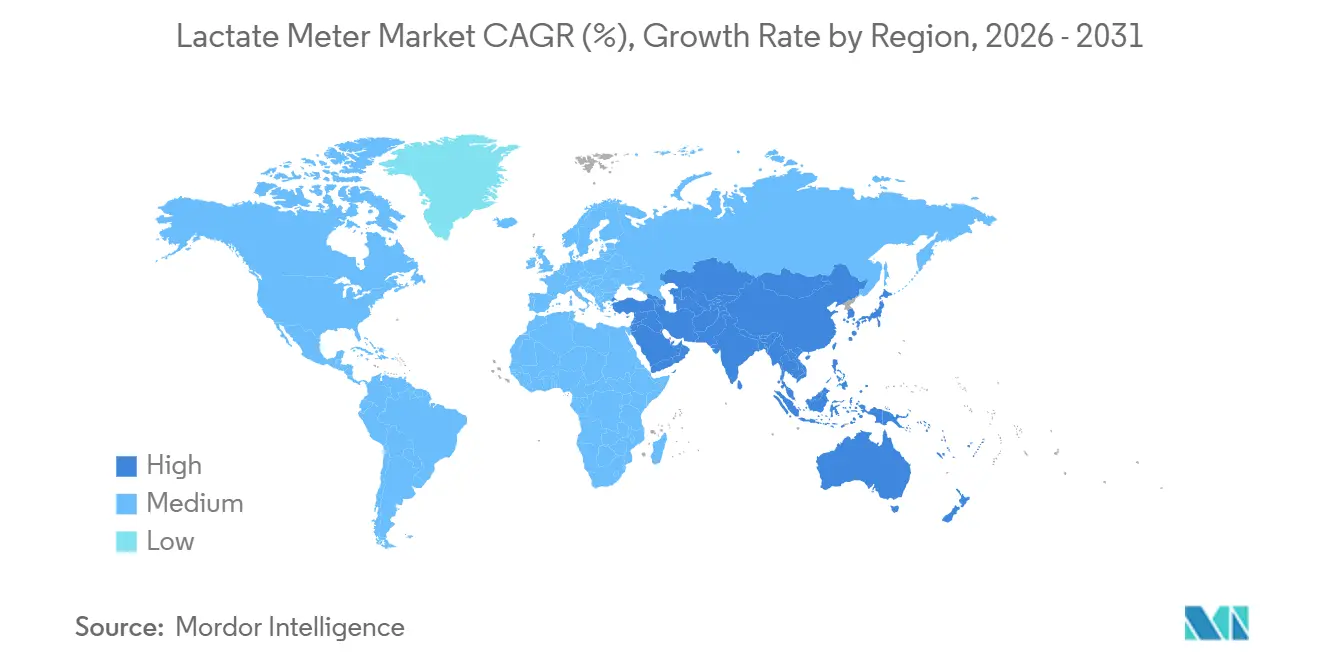

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

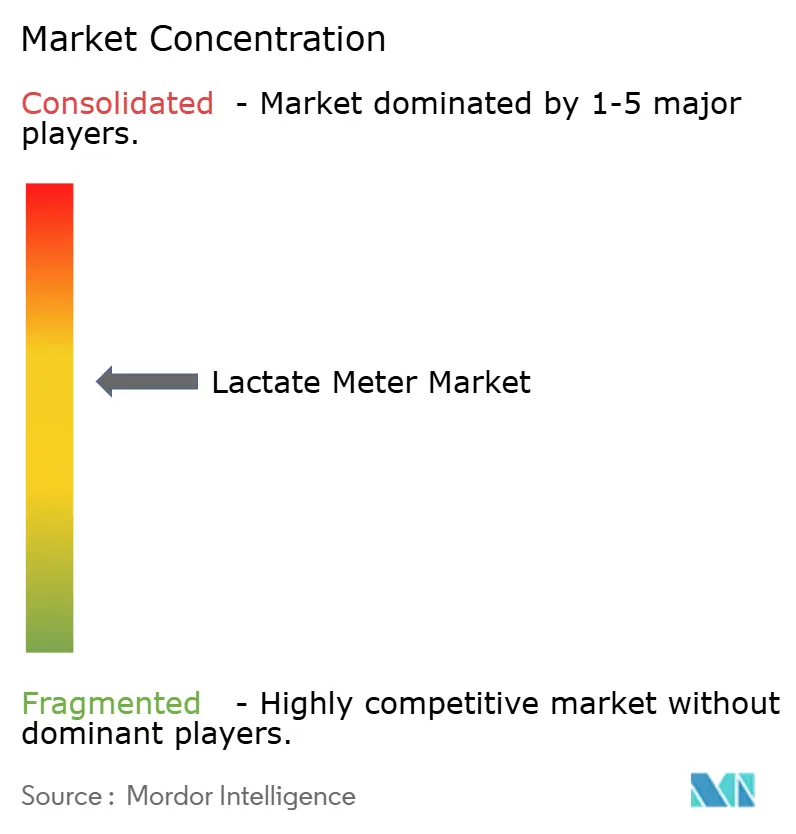

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lactate Meter Market Analysis by Mordor Intelligence

The Lactate Meter Market size is projected to be USD 276.10 million in 2025, USD 296.5 million in 2026, and reach USD 427.40 million by 2031, growing at a CAGR of 7.59% from 2026 to 2031.

This reflects sustained demand from sepsis-bundle compliance, sports-performance programs, and emerging bioprocess monitoring applications. Handheld devices continue to dominate because they cut emergency-department turnaround time to under 2 minutes and allow clinicians to verify resuscitation progress without leaving the bedside. Research laboratories are migrating to optical platforms that push analytical precision below 3 % coefficient of variation, a threshold valued in pharmaceutical process-control loops . Asia-Pacific is closing the gap on North America as Healthy China 2030 and Ayushman Bharat upgrade point-of-care infrastructure in county-level and primary-care facilities. Supply-chain risks linked to lactate-oxidase fermentation and specialty membranes persist, yet contingency sourcing and nanozyme research are diluting single-vendor dependence.

Key Report Takeaways

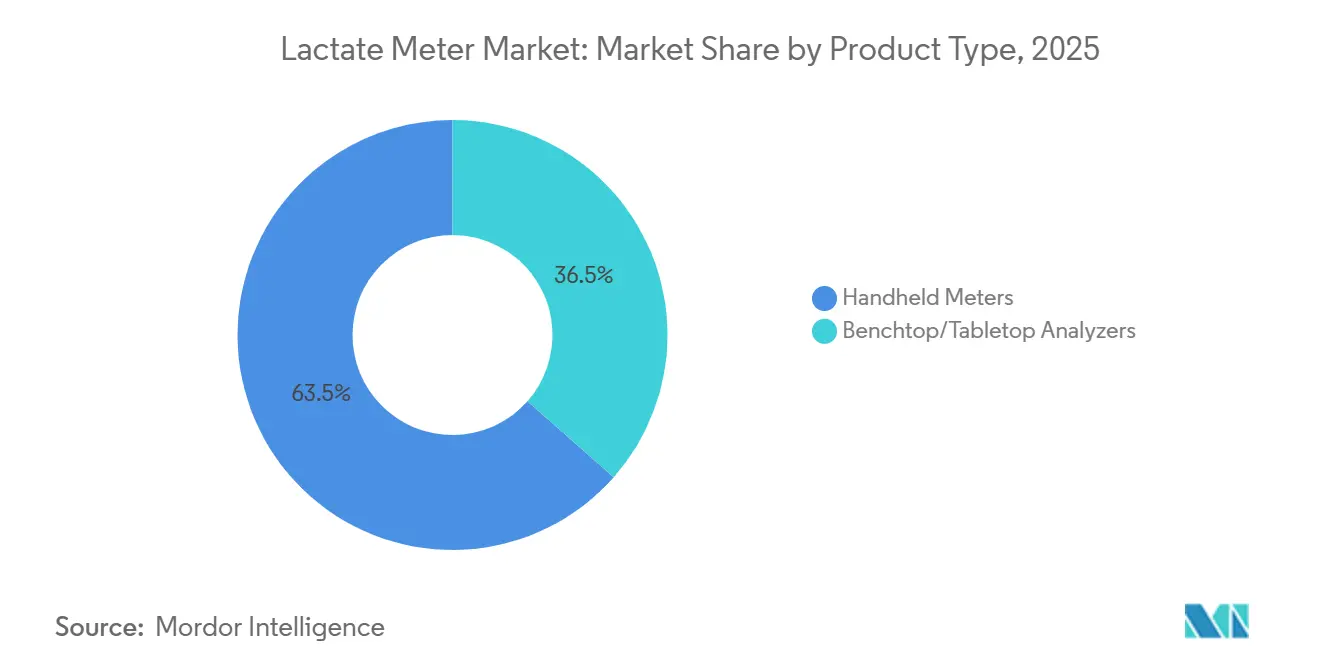

- By product type, handheld meters captured 63.50% of the lactate meter market share in 2025, while benchtop analyzers will expected to grow at 7.80% CAGR through 2031.

- By power source, battery-operated units led with 78.60% of the lactate meter market size in 2025. Chargeable platforms are projected to expand at the fastest rate of 8.00% from 2026 to 2031.

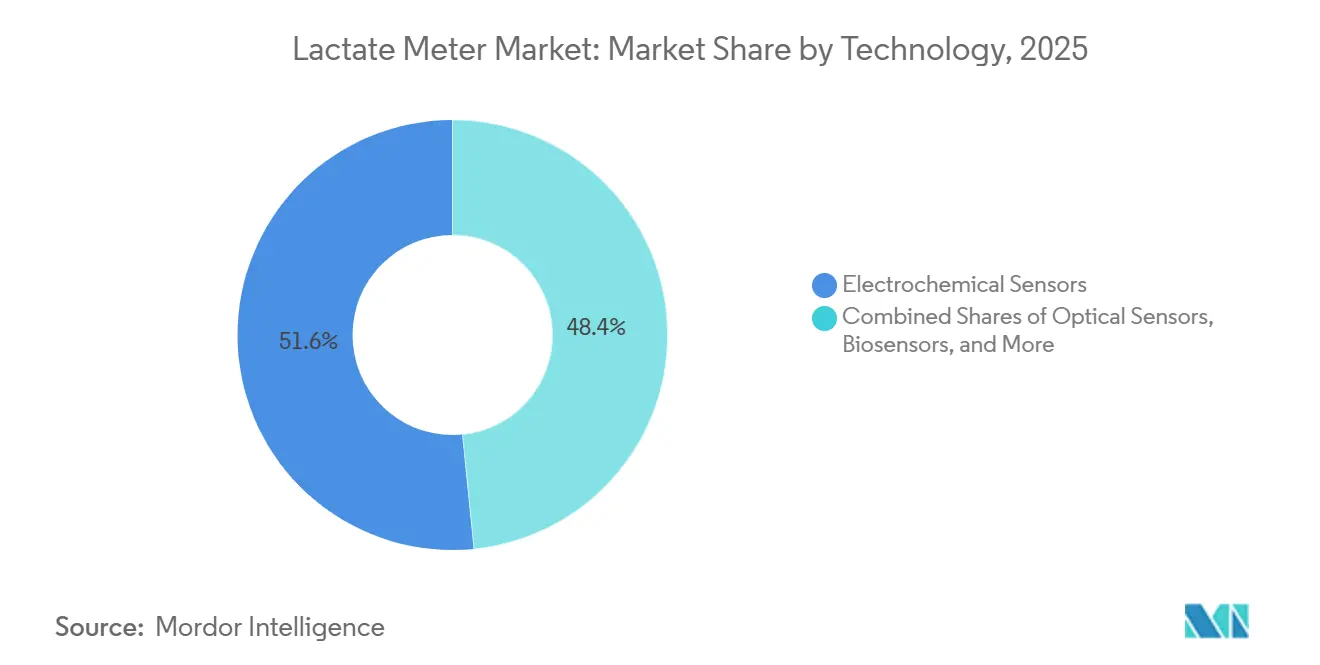

- By technology, electrochemical sensors held 51.60% revenue share in 2025, whereas optical sensors are expected to grow at a CAGR of 7.85% through 2031.

- By application, medical intervention dominated with a 48.40% share in 2025, yet sports performance monitoring is forecast to rise at a 7.89% CAGR through 2031.

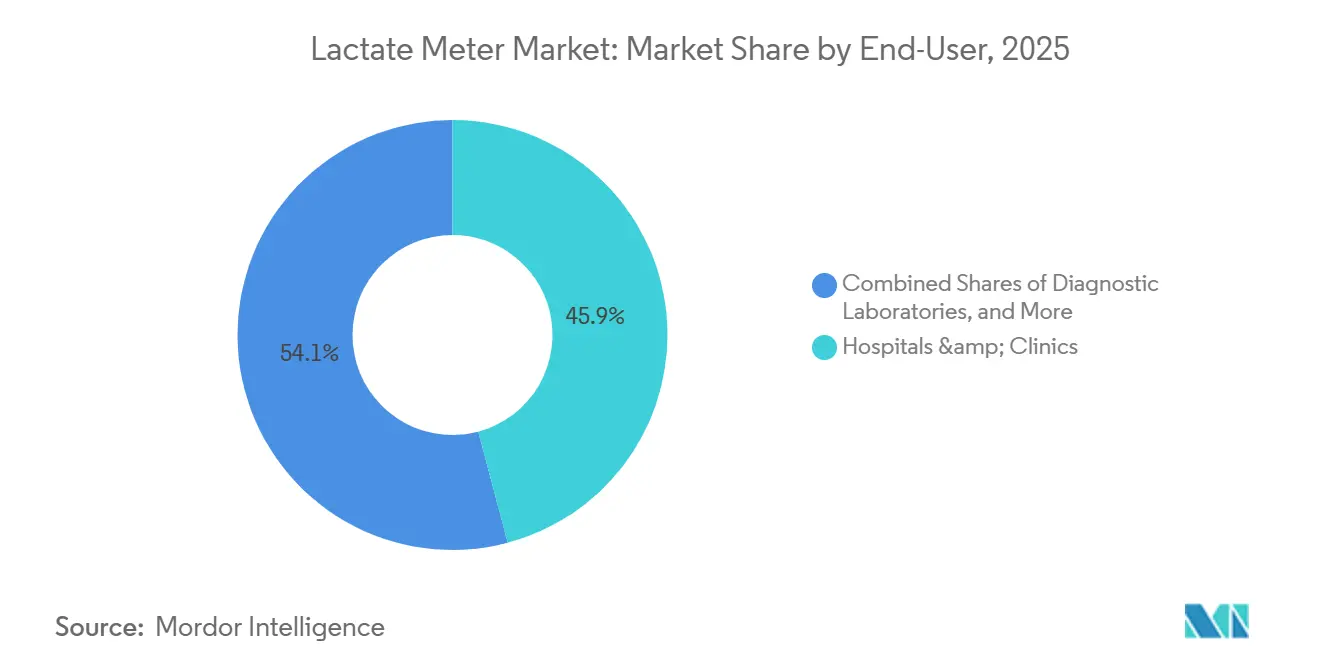

- By end-user, hospitals and clinics commanded 45.87% of demand in 2025, while sports institutes and teams will climb at a 7.92% CAGR to 2031.

- By geography, North America accounted for 42.17% of 2025 revenue, whereas Asia-Pacific is poised to expand at an 8.03% CAGR over the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lactate Meter Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | ( ~ ) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid shift toward handheld and connected POC devices | +1.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Growing adoption by elite & amateur sports programs | +0.9% | North America, Europe, Australia; emerging in China and India | Medium term (2-4 years) |

| ICU protocols mandating lactate tracking for sepsis bundles | +1.4% | Global, with highest penetration in the United States and European Union | Short term (≤ 2 years) |

| Reimbursement expansion for emergency lactate testing | +0.8% | North America and Europe | Short term (≤ 2 years) |

| Wearable sweat-lactate sensors entering pilot deployments | +0.6% | South Korea, Japan, spill-over to North America | Long term (≥ 4 years) |

| Pharma R&D using microfluidic lactate chips | +0.5% | United States, Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift Toward Handheld and Connected POC Devices

Emergency departments have standardized handheld meters to compress lactate turnaround time from 30–45 minutes to under 2 minutes, supporting the Surviving Sepsis Campaign hour-1 bundle. Direct integration with electronic medical records eliminates transcription errors and automates lactate‐clearance trending. Battery-operated designs dominate because they bypass shared charging logistics that complicate shift handover. The FDA’s CLIA-waiver pathway accelerates market entry by limiting performance criteria to a coefficient of variation below 10%.[1]U.S. Food and Drug Administration, “CLIA Waiver Guidance for IVD Devices,” fda.gov Cloud connectivity remains polarizing as hospitals weigh cybersecurity exposure against predictive-maintenance benefits, yet vendors continue to embed Bluetooth modules to future-proof devices. The shift has raised consumable demand because each handheld strip is single-use, linking hardware adoption directly to recurring revenue.

Growing Adoption by Elite & Amateur Sports Programs

Lactate-threshold testing migrated from Olympic training centers to NCAA programs and amateur cycling clubs when meter pricing fell below USD 300 and strip costs dropped under USD 2. Elite soccer academies in Spain and Germany now conduct weekly tests to individualize interval workloads, noting that fixed heart-rate zones misclassify 30% of athletes due to genetic variability. Wearable sweat-lactate pilots run in South Korea and the European Union, reflecting athlete demand for non-invasive options. Sports institutes increasingly favor multi-parameter platforms that also capture glucose and hemoglobin to consolidate diagnostics budgets. Because no ISO standard governs sports lactate devices, vendors bypass lengthy clinical-validation studies, accelerating time-to-market but raising performance variability.

ICU Protocols Mandating Lactate Tracking for Sepsis Bundles

The 2021 guidelines advise measuring lactate within 1 hour of sepsis recognition and repeating every 2–4 hours if values exceed 2 mmol/L. European Society of Intensive Care Medicine 2025 guidance reinforced serial measurement, multiplying test volume and consumables demand. Pre-hospital emergency medical services adopted handheld meters for field triage, extending the addressable base beyond hospital walls. Hospitals equip each resuscitation bay with a dedicated meter to avoid cross-contamination, thereby raising unit shipments. The protocol synergy between ICU and ambulance settings cements lactate as an indispensable metric in shock resuscitation workflows.

Reimbursement Expansion for Emergency Lactate Testing (US & EU)

The 2025 Clinical Laboratory Fee Schedule maintained lactate payment while capping future cuts, stabilizing U.S. revenue expectations.[2]Centers for Medicare & Medicaid Services, “Clinical Laboratory Fee Schedule 2025,” cms.gov European frameworks reimburse lactate within sepsis bundles, encouraging POC adoption that reduces length-of-stay. Private United States insurers cover POC lactate without prior authorization in emergency settings, a policy that contrasts with more restrictive glucose or troponin edits. Higher facility-fee eligibility for POC results boosts hospital margins and favors handheld meters over central laboratory workflows. The reimbursement clarity de-risks capital purchases and underpins supplier pricing power for consumables.

Restraints Impact Analysis*

| RESTRAINT | ( ~ ) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High per-test consumable cost in low-resource settings | -0.7% | Sub-Saharan Africa, South Asia, rural Latin America | Short term (≤ 2 years) |

| Regulatory uncertainty over non-invasive measurement accuracy | -0.5% | United States, European Union | Long term (≥ 4 years) |

| Data-privacy hurdles for cloud-connected meters in the EU | -0.4% | European Union and GDPR-aligned markets | Medium term (2-4 years) |

| Supply-chain exposure to specialty enzymes and membranes | -0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Per-Test Consumable Cost in Low-Resource Settings

Strip prices between USD 2 and USD 8 exceed daily health-spending limits in 47 low-income countries, forcing clinicians to ration tests. Multi-analyte devices aim to amortize costs but raise capital requirements. Paper-based prototypes promise sub-USD 1 pricing yet lack WHO prequalification, and distributor mark-ups in East Africa push retail prices even higher. Rationing undermines early sepsis detection, limiting the lactate meter market in public-sector facilities.

Regulatory Uncertainty Over Non-Invasive Measurement Accuracy

Correlation variability has stalled FDA 510(k) filings, and CE-IVD bodies require larger paired-sample datasets than most prototypes have generated. If a device claims to guide resuscitation, it faces Class IIb scrutiny under EU MDR, extending timelines and compliance costs. Vendors therefore hesitate to finalize designs, delaying commercialization and capping near-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Portability Drives Handheld Dominance

Handheld devices secured 63.50% of the lactate meter market share in 2025 and will climb at a 7.80% CAGR through 2031, bolstered by emergency workflows favoring sub-2-minute turnaround times. Benchtop analyzers serve central laboratories that process up to 500 daily samples and integrate with LIS under HL7 messaging. Despite higher throughput and optical detection that mitigates enzyme drift, their capital cost and 18-month service contracts deter small hospitals. Handheld units prevail in sports monitoring and veterinary practice because coaches and vets conduct field-side testing without power outlets. Benchtop analyzers remain indispensable in pharmaceutical QC labs, validating micro-fluidic chips against reference assays. Regulatory advantages amplify the handheld edge; CLIA-waived status exempts operators from proficiency testing if meters stay below 10% coefficient of variation.[3]Clinical Laboratory Standards Institute, “Laboratory Information Systems Standards,” clsi.org

By Power Source: Battery Economics Outweigh Recharging Convenience

Battery-operated meters controlled 78.60% of 2025 revenue and will grow at 8.00% CAGR as EDs and rural clinics value disposable alkaline cells that eliminate recharging infrastructure. Rechargeable platforms appeal to European sports institutes seeking sustainability alignment with the EU Green Deal. Lithium-ion units support 300–500 cycles but cost USD 100–150 more than battery models, extending payback periods. Infection-control protocols in U.S. hospitals discourage shared chargers, reinforcing disposable preference. Asia-Pacific field clinics adopt solar-assisted chargers, yet battery sales continue to outpace rechargeable shipments. Component shortages in lithium supply chains could erode rechargeables’ cost advantage, further cementing battery dominance in the lactate meter market.

By Technology: Electrochemical Sensors Face Optical Disruption

Electrochemical sensors held 51.60% revenue share in 2025 by leveraging lactate-oxidase catalysis that enables strip costs under USD 2 and readings within 10 seconds. Optical sensors, however, will register the fastest 7.85% CAGR because fluorescence methods achieve <3 % analytical CV, a threshold prized in pharmaceutical bioreactor control. Graphene and carbon-nanotube electrodes in next-generation biosensors deliver two- to three-fold sensitivity gains, yet production scale remains limited. Wearable prototypes universally adopt electrochemical detection due to sweat opacity, keeping that sub-segment tethered to enzyme availability. Chemiluminescent and LDH-based assays stay confined to research labs. As benchtop platforms pivot to optical technology, a dual structure emerges in the lactate meter market: electrochemical supremacy in hand-helds and optical ascendancy in central laboratories.

By Application: Sports Monitoring Outpaces Medical Intervention

Medical intervention accounted for 48.40% of 2025 revenue, encompassing sepsis resuscitation, shock monitoring, and metabolic-acidosis diagnosis, Sports monitoring will accelerate at a 7.89% CAGR as elite academies and amateur clubs institutionalize lactate-threshold testing. Veterinary usage remains niche but strategic, with equine colic diagnostics benefiting from stall-side testing that cuts treatment delay. Wearable sweat-lactate sensors target 50 million recreational athletes in North America and Europe, offering a non-invasive alternative once accuracy improves.

By End-User: Sports Institutes Gain on Hospitals

Hospitals and clinics led with 45.87% of 2025 demand, driven by sepsis mandates and serial ICU monitoring. Sports institutes will rise at a 7.92% CAGR. Diagnostic laboratories process overflow samples from outpatient centers but face volume erosion as handheld meters proliferate. Pharmaceutical companies adopt inline chips for bioreactor oversight, while military medical units deploy portable meters for battlefield triage. Economic incentives diverge: hospitals chase reimbursement margins stabilized by CMS, whereas sports entities view lactate testing as an investment in athlete availability.

Geography Analysis

Asia-Pacific’s 8.03% forecast CAGR signals a structural pivot in the lactate meter market as public-health programs extend POC diagnostics beyond tertiary hospitals into county-level facilities. China alone intends to outfit more than 3,000 county hospitals with handheld meters by 2030 under Healthy China 2030, a policy that embeds lactate testing into early sepsis recognition for rural populations. India’s Ayushman Bharat transformation funds 150,000 health-and-wellness centers, each budgeted for essential diagnostics including lactate strips creating volume orders that improve price elasticity. South Korea and Japan accelerate wearable sensor trials facilitated by robust telecom infrastructure, positioning the region for rapid non-invasive adoption once regulatory clarity emerges.

North America retains technology leadership due to entrenched 510(k) clearances, established reimbursement, and hospital EMR integration. United States. emergency medical services equip ambulances with handheld meters, adding pre-hospital demand that Europe is only beginning to replicate. Canadian provinces subsidize POC lactate in remote Indigenous communities, widening rural access. Mexico’s private-hospital groups import battery-operated meters from U.S. vendors, but public-sector uptake remains limited by strip costs.

Europe’s mature reimbursement anchors steady replacement cycles rather than explosive growth. Germany’s DRG incentives reward hospitals that shorten ICU stays via rapid lactate-clearance tracking, boosting POC throughput. France and Spain focus on connected-device cybersecurity compliance under GDPR, delaying cloud launches but encouraging local data-residency solutions. The United Kingdom leverages NHS England’s sepsis pathway to justify trust-level procurement of handheld meters, although budget constraints enforce competitive tendering that squeezes strip pricing.

Competitive Landscape

The lactate meter market exhibits moderate concentration: Abbott, Roche, EKF Diagnostics, and Nova Biomedical collectively hold the majority of global revenue through established hospital contracts and broad 510(k) and CE-IVD portfolios. Mid-tier entrants such as Arkray exploit local distribution and cost advantages to win regional tenders. Wearable development players including PKvitality and BST Bio Sensor chase first-mover status in non-invasive sports and wellness niches where clinical-grade validation is not yet mandatory.

Technology differentiation centers on connectivity. Abbott and Roche integrate Bluetooth Low Energy and cloud analytics, but European GDPR hurdles slow uptake, creating openings for Asia-Pacific devices that store data locally. EKF Diagnostics upgraded its benchtop platform with touchscreen interfaces and LIS auto-upload, underscoring a pivot toward high-throughput central-lab needs. Nova Biomedical expanded manufacturing to shorten lead times amid enzyme-supply volatility, reinforcing supply reliability as a competitive lever.

Price competition remains strongest in the consumable stream. Top-tier firms negotiate volume-discount contracts with large health systems, whereas smaller vendors bundle meters at low or zero margin to secure strip annuities. Veterinary-specific calibration curves differentiate niche suppliers in equine and companion-animal care. Pharmaceutical R&D represents an emerging battleground as micro-fluidic chips promise subscription-based revenue from bioprocess monitoring, attracting sensor specialists beyond the traditional diagnostics sphere.

Lactate Meter Industry Leaders

EKF Diagnostics Holdings PLC

Nova Biomedical

Arkray, Inc.

ApexBio

F. Hoffmann-La Roche AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Applied Monitoring secured an additional GBP 500,000 (approximately USD 610,000) from the Northeast Venture Fund. This fund, supported by the European Regional Development Fund and managed by Mercia Ventures, will facilitate the commercialization of a non-invasive solution for the continuous monitoring of lactate levels in blood, which is essential for identifying peak exertion in athletes and optimizing their training programs.

- March 2024: Vivachek has announced the global launch of its advanced lactate analyzer, strategically developed to optimize athletic performance.

Global Lactate Meter Market Report Scope

As per the scope of the report, a lactate meter is a portable handheld device used to measure the concentration of lactate in whole blood, typically via a finger prick, providing quick results in mmol/L. It serves as a tool for athletes to determine lactate thresholds for optimizing training intensity and for medical professionals to monitor for conditions like sepsis or shock.

The Lactate Meter Market is segmented by product type, power source, technology, application, end-user, and geography. By product type, the market includes handheld meters and benchtop/tabletop analyzers. By Power Source, the market is segmented into battery-operated and chargeable/rechargeable devices. By technology, the market is segmented into electrochemical sensors, optical sensors, biosensors, and other technologies. By application, the market is categorized into medical intervention, sports performance monitoring, veterinary use, and other applications. By end-user, the market is segmented into hospitals & clinics, diagnostic laboratories, sports institutes & teams, and other end-users. By Geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Handheld Meters |

| Benchtop/Tabletop Analyzers |

| Battery-operated |

| Chargeable/Rechargeable |

| Electrochemical Sensors |

| Optical Sensors |

| Biosensors |

| Other Technology |

| Medical Intervention |

| Sports Performance Monitoring |

| Veterinary |

| Other Applications |

| Hospitals & Clinics |

| Diagnostic Laboratories |

| Sports Institutes & Teams |

| Other End-User |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Handheld Meters | |

| Benchtop/Tabletop Analyzers | ||

| By Power Source | Battery-operated | |

| Chargeable/Rechargeable | ||

| By Technology | Electrochemical Sensors | |

| Optical Sensors | ||

| Biosensors | ||

| Other Technology | ||

| By Application | Medical Intervention | |

| Sports Performance Monitoring | ||

| Veterinary | ||

| Other Applications | ||

| By End-user | Hospitals & Clinics | |

| Diagnostic Laboratories | ||

| Sports Institutes & Teams | ||

| Other End-User | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value of lactate meter market by 2031?

It is expected to reach USD 427.4 million by 2031.

Why are optical sensors gaining traction over electrochemical designs?

Pharmaceutical R&D values optical fluorescence for its <3 % analytical CV, a precision level that supports real-time bioprocess control.

How are sports institutes using lactate testing?

Elite teams and amateur clubs embed weekly lactate-threshold assessments to fine-tune interval training and reduce overtraining risk.

Which region is expected to grow fastest through 2031?

Asia-Pacific, propelled by Healthy China 2030 and Indias Ayushman Bharat diagnostics upgrades, is forecast to post an 8.03% CAGR.

What challenges limit non-invasive sweat-lactate sensors?

Variable blood-sweat correlation and undefined FDA accuracy thresholds delay regulatory approval and commercial launch.

How concentrated is the competitive landscape?

Four multinationals control roughly 52% to 58% of revenue, producing a moderate concentration that still leaves room for regional challengers.

Page last updated on: