Laboratory Temperature Control Units Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

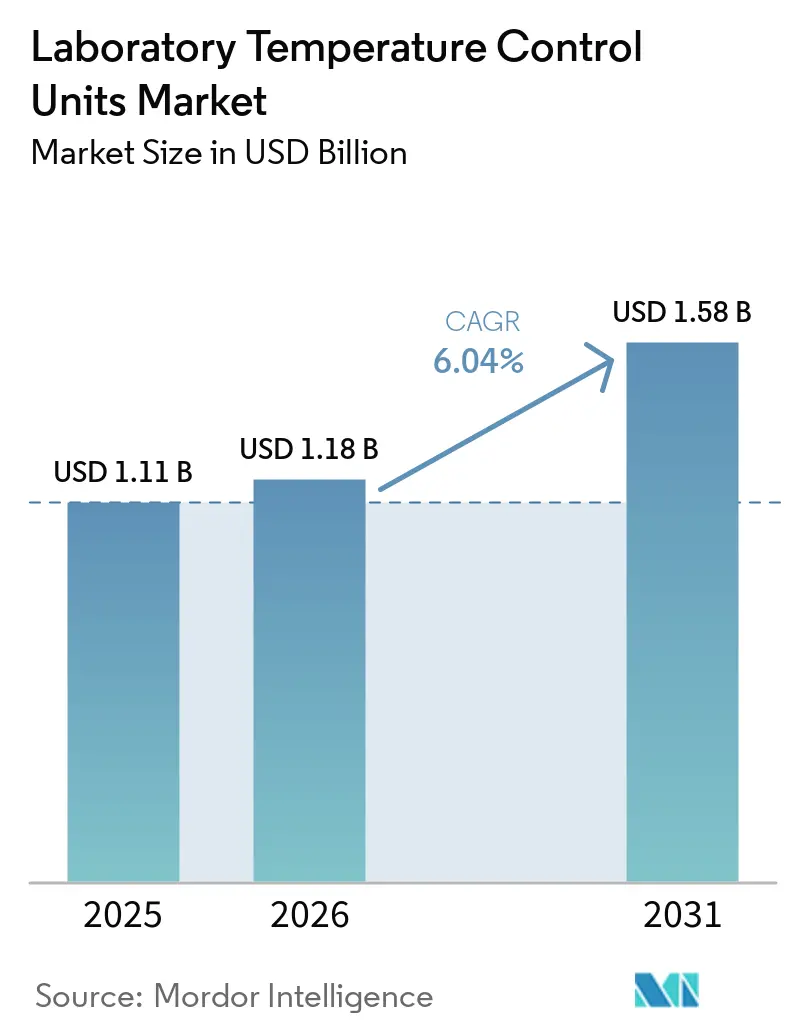

| Market Size (2026) | USD 1.18 Billion |

| Market Size (2031) | USD 1.58 Billion |

| Growth Rate (2026 - 2031) | 6.04% CAGR |

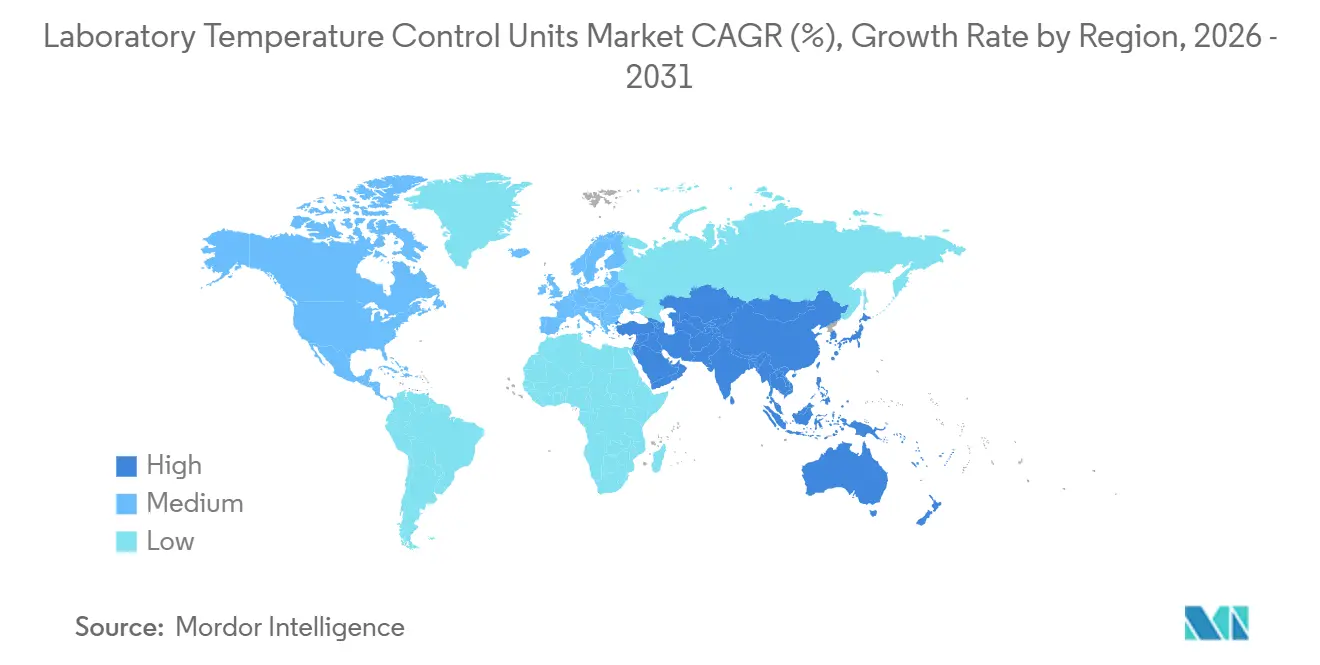

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

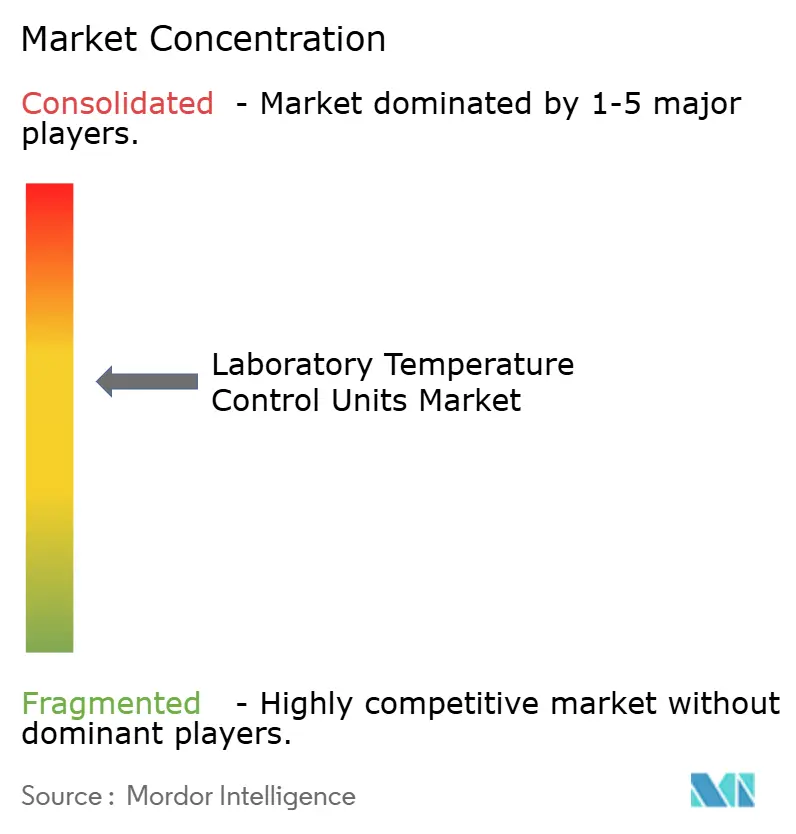

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Laboratory Temperature Control Units Market Analysis by Mordor Intelligence

The Laboratory Temperature Control Units Market size is projected to expand from USD 1.11 billion in 2025 and USD 1.18 billion in 2026 to USD 1.58 billion by 2031, registering a CAGR of 6.04% between 2026 to 2031.

Policy pressure to phase down high global warming potential refrigerants is reshaping design choices and accelerating product refresh cycles across both benchtop and floor-standing platforms, which supports multi-year replacement demand in mature labs. A rapid rise in throughput for mass spectrometry, electron microscopy, and other precision instruments is increasing the need for tighter thermal stability and higher uptime, which expands premium adoption in the laboratory temperature control units market. North America benefits from stringent energy and performance rules for chillers, while Asia-Pacific gains momentum from capital spending in pharmaceuticals and semiconductors that multiplies installed base growth in the laboratory temperature control units market. Manufacturers are aligning roadmaps with natural-refrigerant portfolios, variable-speed compressors, and data logging that integrate with validated workflows to protect data integrity in regulated environments.[1]European Commission, “Documentation - F-Gas Legislation - Fluorinated Greenhouse Gases,” European Commission, climate.ec.europa.eu

Key Report Takeaways

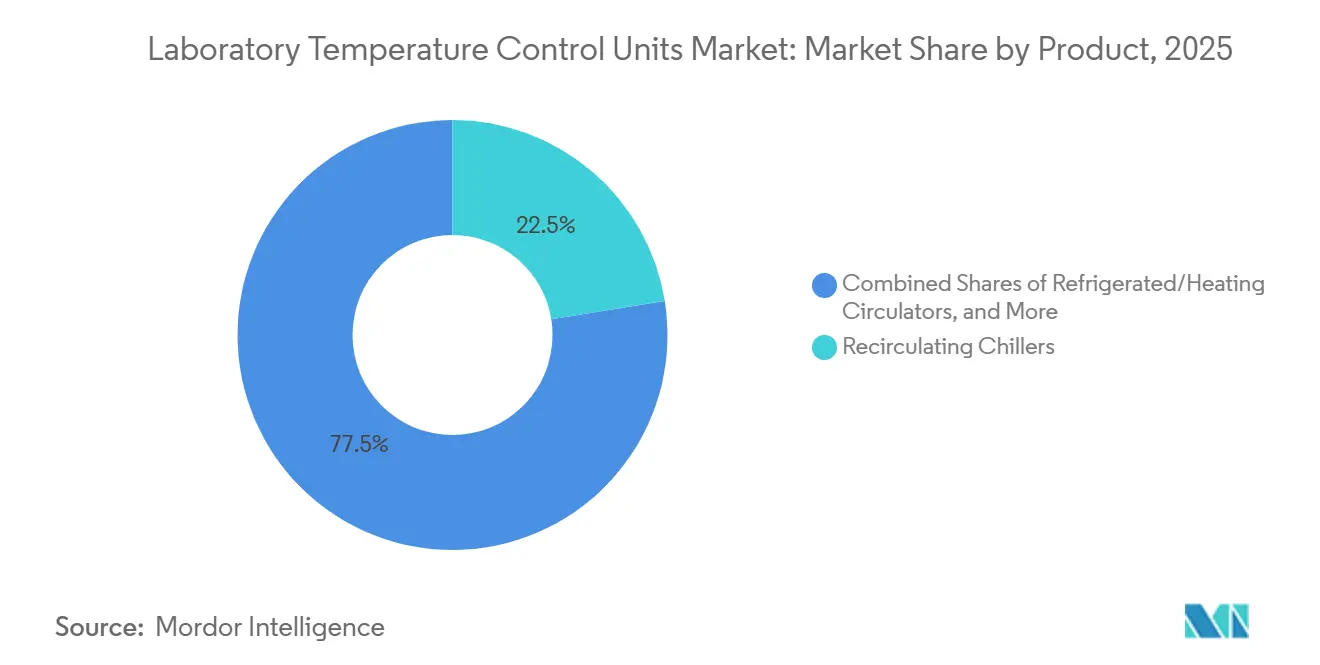

- By product, recirculating chillers led with 22.45% revenue share in 2025, while highly dynamic temperature control systems are projected to grow at an 8.85% CAGR through 2031.

- By cooling technology, air-cooled systems commanded 46.22% share in 2025, while thermoelectric Peltier units are set to expand at an 8.03% CAGR.

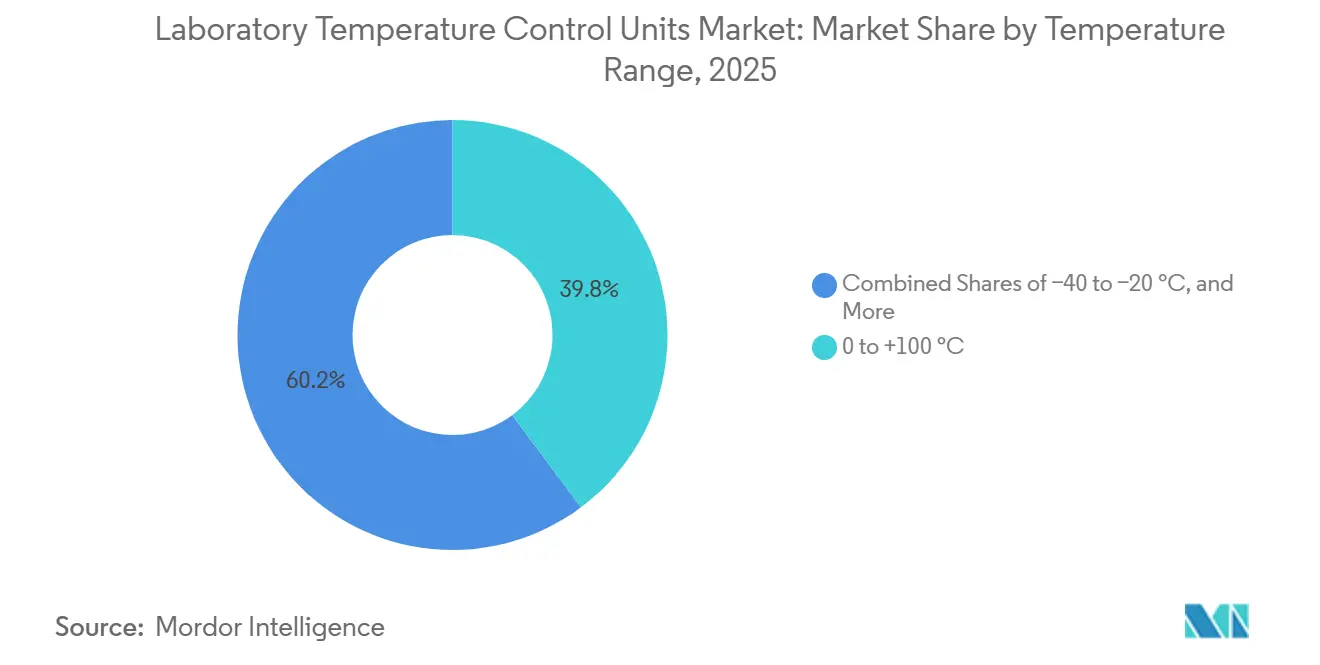

- By temperature range, the 0 to +100 °C bracket accounted for 39.80% share in 2025, while below −40 °C systems are forecast to advance at a 9.39% CAGR to 2031.

- By capacity, the 2–5 kW tier held 28.22% share in 2025, while sub-0.5 kW units are expected to grow at an 8.86% CAGR.

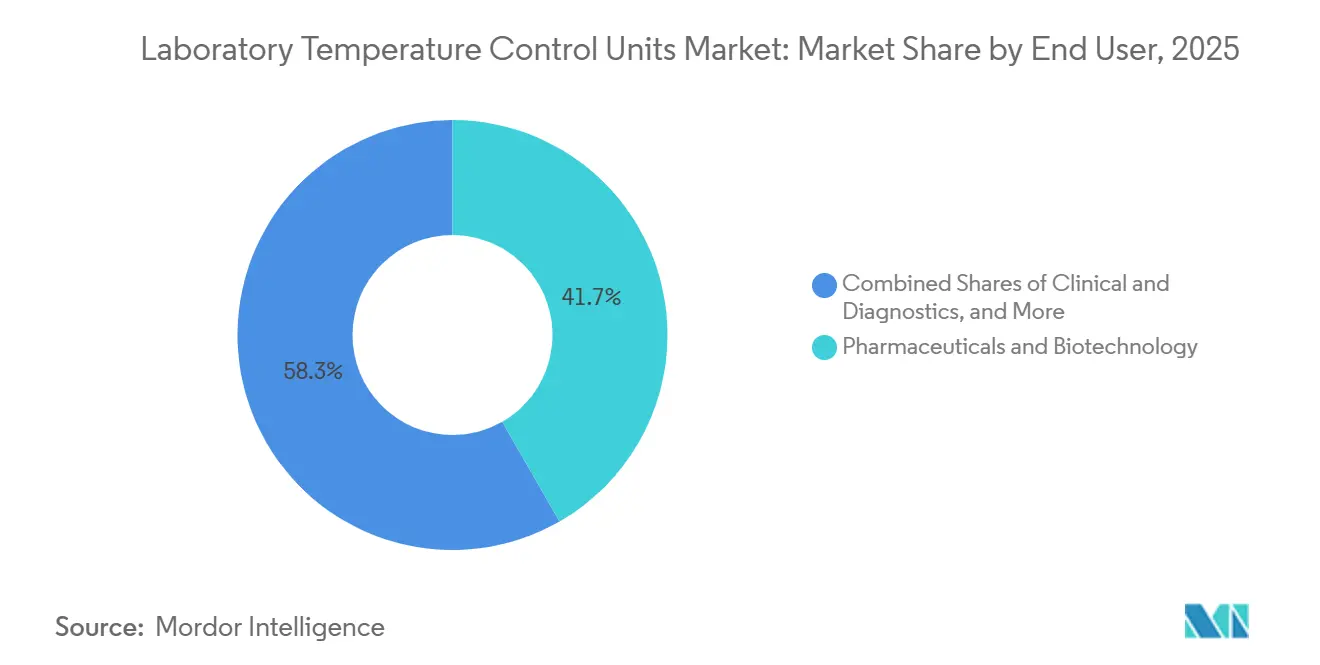

- By end user, pharmaceuticals and biotechnology accounted for 41.72% share in 2025, while clinical and diagnostics is projected to grow at a 7.01% CAGR.

- By application, analytical instruments support held 24.93% share in 2025, while bioprocessing and cold-chain labs are set to expand at an 8.03% CAGR.

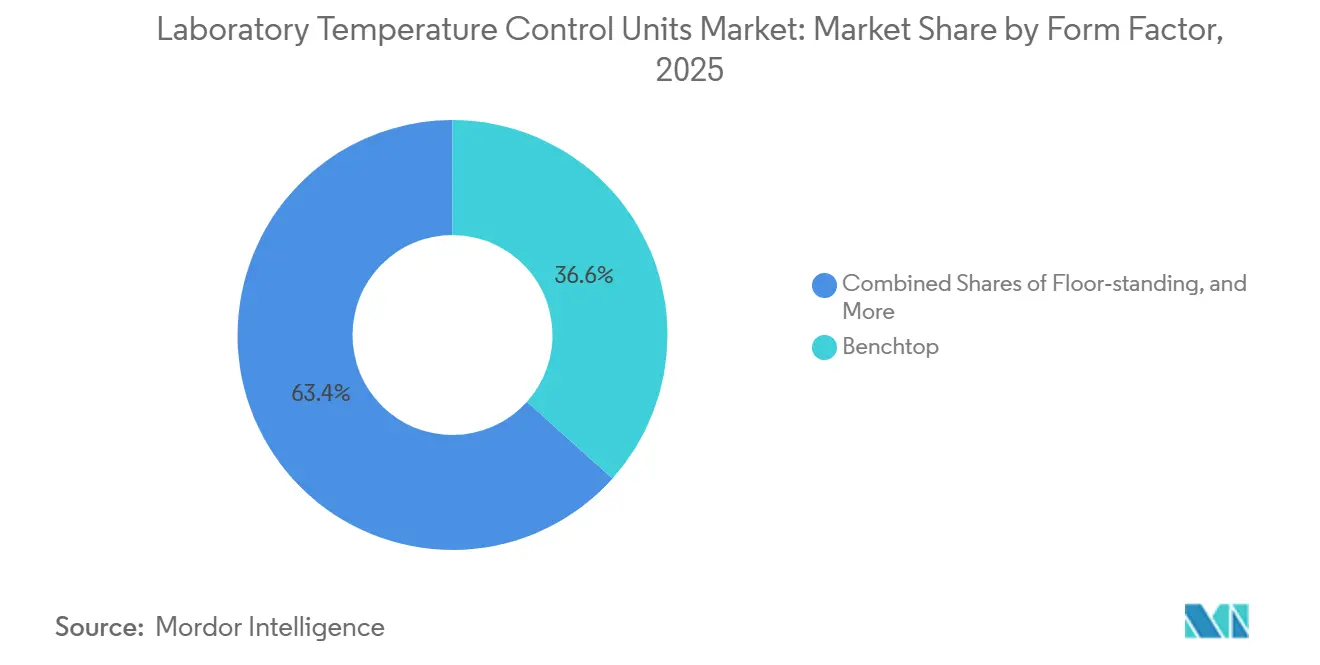

- By form factor, benchtop configurations led with 36.63% share in 2025, while integrated or OEM modules are projected to grow at a 7.58% CAGR.

- By distribution channel, direct sales accounted for 61.83% share in 2025, while e-Commerce are expected to expand at a 7.46% CAGR.

- By geography, North America captured 34.82% of revenue in 2025, while Asia-Pacific is forecast to record a 10.48% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Laboratory Temperature Control Units Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pharma and biotech R&D intensification boosts precision thermal control demand | +1.8% | Global, with concentrated gains in North America and APAC core markets | Medium term (2-4 years) |

| APAC lab build-out and instrument installs expand installed base for TCUs | +1.5% | China, India, Singapore, Taiwan, spill-over to Southeast Asia | Short term (≤ 2 years) |

| Regulatory shift to low GWP refrigerants accelerates product refresh and retrofits | +1.2% | Europe, North America, with adoption pressure in export-oriented APAC manufacturers | Medium term (2-4 years) |

| Lab sustainability, energy and water efficiency standards replace single pass cooling with recirculating systems | +0.9% | North America, Western Europe, emerging in Middle East academic institutions | Long term (≥ 4 years) |

| Rising cooling needs for analytical instruments with higher throughput and uptime | +1.1% | Global, especially pharmaceutical QC labs and contract testing facilities | Short term (≤ 2 years) |

| Thermoelectric or Peltier control adoption in microfluidics, organ on chip, and live cell imaging | +0.7% | North America and EU research institutes, early uptake in Singapore and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Pharma And Biotech R&D Intensification Boosts Precision Thermal Control Demand

Pipeline pressure and patent cliffs are forcing biopharma to maintain or raise laboratory capital spending in 2026, which increases the installed base of precision cooling and heating systems needed to keep high-value assays within tight tolerances. Surveyed R&D leaders highlighted throughput and error-rate gains from lab modernization in 2025, and those priorities now cascade into procurement specifications that call for tighter setpoint control and validated data logging that protect data integrity in regulated labs. As capital flows to biologics, cell therapy, and next-generation modalities, cooling requirements shift toward dynamic temperature control for reaction kinetics and stability windows that are narrower than legacy workflows, which expands premium adoption in the Laboratory Temperature Control Units market. Executive partnerships in China during 2025 and 2026 redirected deal value to sites that are scaling new labs and analytical cores, which expands the addressable installed base for thermal control in APAC hubs.

India’s Bio SHAKTI allocation of approximately USD 1.08 billion over five years is being executed in 2026 as upgrades to National Institutes of Pharmaceutical Education and Research, clinical trial sites, and biosimilar capacity come online, which raises demand for recirculating chillers, refrigerated circulators, and water baths across synthesis, validation, and staging workflows. This set of actions lifts specification density per lab and expands refresh cycles in the laboratory temperature control units market.

APAC Lab Build-Out And Instrument Installs Expand Installed Base For TCUs

China’s pharmaceutical production rose 6.6% in 2026 compared to 3.6% in 2025, which aligns capital budgets with more biopharma-oriented pipelines that intensify temperature control needs at each step from R&D to QC. Taiwan’s Industrial Technology Research Institute broke ground on a 12-inch semiconductor pilot line in February 2026 with completion targeted by end-2027, which expands precision cooling demand around lithography, etch, and metrology tools that require sub-0.1 °C stability. Multiple Indian expansions in 2026, including Alkem’s formulations site at Ujjain and Lupin’s peptide capacity at Dabhasa, are embedding centralized or modular temperature control architectures to manage multi-reactor thermal loads in validated suites.

A growing base of analytical instruments in APAC is also raising point-of-use demand for compact chillers that integrate over digital controls and can be networked for alarms, which broadens entry points for the laboratory temperature control units market. Cleanroom and instrument density are increasing across Shanghai, Suzhou, Hyderabad, and Hsinchu clusters, which supports higher per-site TCU penetration. That mix of pharma and semiconductor projects narrows lead times for compliant units as APAC integrators synchronize specifications to global validation standards, which raises the installed base growth rate in the laboratory temperature control units market.

Regulatory Shift To Low GWP Refrigerants Accelerates Product Refresh And Retrofits

The European Union’s F-Gas Regulation 2024/573 restricts stationary chillers above 12 kW from using refrigerants with GWP 750 or higher from January 2027 and requires the elimination of F-gases for units at or below 12 kW by January 2032 unless safety codes mandate them, which forces design exits for high-GWP chemistries and speeds lifecycle replacements. R-404A prices spiked in step with quota tightening, which triggered redesigns to natural refrigerants such as CO2 and propane and raised demand for pressure-rated components and new control strategies that sustain stability under different thermodynamic regimes[3]SMC Corporation, “SMC Guide to EU F-Gas Regulation,” SMC Corporation, smc.eu. The U.S. EPA proposed compliance-date extensions in September 2025 to align safety standards for flammable and high-pressure refrigerants with the availability of compliant equipment, which gave additional time to categories such as refrigerated centrifuges and semiconductor chillers while still locking in the overall transition.

Canada’s energy-efficiency standards for water-cooled positive displacement chillers in the 264–528 kW range set explicit COP and IPLV benchmarks that push variable-speed and high-efficiency heat exchangers, which spill over into laboratory-grade platforms and inform procurement criteria. These policy changes encourage buyers to advance refresh cycles and favor units with natural refrigerants and high energy performance, which increases premium mix in the laboratory temperature control units market. Vendors that pre-certified R-744 or R-290 portfolios are positioned to capture compliance-driven demand across the E.U., U.S., and Canada.

Lab Sustainability, Energy And Water Efficiency Standards Replace Single Pass Cooling With Recirculating Systems

Water tariffs and discharge permits in major U.S. metros are pushing laboratories to end once-through cooling and adopt recirculating chillers that reduce water usage and stabilize thermal loads per instrument suite. Continuous-duty GC-MS and LC-MS stacks are among the heaviest water users in single-pass systems, so replacing them with closed-loop units delivers rapid utility savings and improves environmental reporting for many sites. Energy-efficient chillers with variable-speed fans and pumps, heat recovery options, and adaptive control logic are gaining traction as buyers focus on total cost of ownership and sustainability credentials.

Sustainability rules also translate to noise and heat-load constraints in dense labs, which supports premium configurations that balance performance with comfort and HVAC burden. This set of factors expands retrofit and new-build demand in the laboratory temperature control units market as facilities codify recirculation and efficiency into standard operating criteria.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compliance costs and redesigns driven by new F-Gas or GWP limits | -0.8% | Europe immediate, North America phased, APAC export manufacturers | Short term (≤ 2 years) |

| Total cost of ownership constraints in constrained lab spaces | -0.5% | Urban research centers in North America, Europe, and APAC megacities | Medium term (2-4 years) |

| Migration to central plant or closed loops in new labs reduces some benchtop chiller demand | -0.4% | New lab construction in North America and Western Europe, emerging in Singapore and GCC states | Long term (≥ 4 years) |

| Technician certification and low GWP refrigerant servicing complexity | -0.3% | Global, acute in emerging markets with limited HVAC training infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Compliance Costs And Redesigns Driven By New F Gas/GWP Limits

Transitioning to natural refrigerants imposes flammability or high-pressure design requirements that add cost and complexity to small and mid-capacity units, which erodes margins for vendors without scale. Laboratory campuses with restrictions on A3 refrigerants must either engineer ventilation and safety interlocks or opt for alternatives that still complicate footprint and power, which slows some conversions. The EPA noted in September 2025 that certain applications required compliance extensions due to safety-standard timing and performance gaps, which confirms the engineering complexity still being resolved for precision categories. European guidance and industry notes from 2025 through 2026 signaled that tightening quotas and new bans on high-GWP refrigerants would raise servicing costs and strand some installed equipment, which accelerates end-of-life decisions but can delay near-term purchases as buyers evaluate options.

The need to qualify multiple SKUs by region or converge on the strictest platform reduces speed to market, which can compress vendor pipelines. These factors temper some 2026 ordering but do not change the medium-term need for compliant replacements across the laboratory temperature control units market.

Total Cost Of Ownership Constraints In Constrained Lab Spaces

Benchtop and floor-standing chillers can increase in-room heat loads and noise levels in dense labs, which adds HVAC burden and raises the total cost of ownership when buildings are capacity-constrained. Vendors have introduced variable-speed fans and low-noise designs to reduce acoustic impact, but premium configurations raise upfront prices relative to baseline air-cooled units. Distributors report that budget-limited buyers continue to select air-cooled units despite the long-run electricity and HVAC costs, which slows efficiency-led upgrades in some segments.

Water-cooled options eliminate in-room heat but require building loops or plumbing, which are not always available in leased or modular spaces. The delta between premium low-noise chillers and baseline units can push payback beyond three years when HVAC savings are modest, which adds friction in capital approvals. This cost tension slows replacements in some labs within the laboratory temperature control units market even as performance requirements continue to rise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Recirculating Chillers Anchor Installed Base While Dynamic Systems Surge

Recirculating chillers commanded 22.45% of the laboratory temperature control units market size in 2025, driven by continuous-duty use in QC labs, contract testing, and instrument clusters that require closed-loop stability and validated logging. These units circulate water-glycol or silicone oil to external heat exchangers and cover broad capacity ranges with tight stability, which aligns with regulated workflows and standardized facilities. Refrigerated or heating circulators combine heater elements with vapor-compression cooling, which supports protocols that pass through ambient and sub-ambient setpoints during one run. Heating circulators serve applications above ambient and remain attractive in evaporation, distillation, and jacketed vessel workflows that do not require sub-ambient control. Water baths and shaking water baths are common in cell culture, kinetics, and dissolution testing based on familiarity and ease of use at lower price points.

Highly dynamic temperature control systems are projected to grow at an 8.85% CAGR through 2031 as reaction calorimetry, pilot-scale processing, and semiconductor development lean on fast ramps and precise overshoot control for safety and yield. The laboratory temperature control units market continues to benefit from controller improvements that integrate with laboratory information systems and building management dashboards. Vendors are embedding multi-point sensors, redundant circuits, and alarm logic that support uptime guarantees in GMP environments. Product roadmaps highlight natural-refrigerant adoption and inverter-driven compressors that balance energy use with steady-state stability to pass qualification tests.

By Cooling Technology: Air-Cooled Dominance Meets Thermoelectric Disruption

Air-cooled systems led with 46.22% of laboratory temperature control units market share in 2025, supported by simple installation and the ability to operate without building plumbing or chilled-water loops. Water-cooled chillers reduce in-room heat load and often deliver higher coefficients of performance, but they require building integration and treatment regimes that some sites lack. Thermoelectric or Peltier platforms are set to grow at an 8.03% CAGR as microfluidics, organ-on-chip, and live-cell imaging benefit from vibration-free and refrigerant-free operation with precise setpoint control. Cryogenic and CO2-assisted systems serve ultra-low-temperature needs below −80 °C in freeze-drying and cryopreservation, which keeps them focused on specific protocols rather than general lab cooling. Hybrid approaches are still rare in labs due to maintenance complexity and space requirements. The adoption curve shows complementary roles as thermoelectric expands at the low end and air- or water-cooled platforms handle higher loads.

Advances in fan and compressor control improve seasonal efficiency while maintaining stability under varied ambient conditions. Controller options with Ethernet or RS232 and data logging support audit trails and alarm routing, which matters in regulated environments. Semiconductor and imaging labs prize low-noise profiles that reduce vibration and acoustic artifacts, which reinforces demand for premium air-cooled units with adaptive fans. Where central plant loops exist, water-cooled units remain compelling due to energy efficiency and heat management. As vendors complete natural-refrigerant conversions, performance characteristics will continue to tighten around stability metrics. This set of changes keeps the laboratory temperature control units market focused on application fit across capacity, noise, footprint, and integration.

By Temperature Range: Ambient Workhorses And Cryogenic Pioneers

The 0 to +100 °C band accounted for 39.80% of 2025 demand as most analytical instruments, cell culture, and jacketed reactors operate in that span with moderate stability goals. Systems below −40 °C are forecast to expand at a 9.39% CAGR through 2031 as ultra-low-temperature freezers, freeze-drying, and environmental testing scale in bioprocessing and materials labs. Multi-stage refrigeration and CO2 cascade strategies are displacing legacy blends to meet EU transition rules while sustaining low-temperature performance targets. Near-ambient control remains the dominant use case for detector cooling, column ovens, and dissolution baths across pharmaceutical and environmental testing. Wider spans that move from sub-ambient to elevated temperatures continue to back refrigerated or heating circulators. Compliance with ICH stability and validation protocols drives demand for logging and control features that support audit readiness in QC environments.

Above +100 °C, oil-based circulators enable materials and polymer processes that require stability at elevated setpoints. This area benefits from control algorithms that reduce overshoot and improve ramp tracking for safety and data quality. As more protocols combine sub-ambient segments with heating above ambient, buyers often consolidate on platforms that span a wider range with strong stability. Natural-refrigerant platforms are expanding into more of these categories as vendors complete redesigns and address safety considerations. Validation kits and calibration services influence purchase decisions in labs that must re-qualify workflows after equipment changes. These trends sustain a strong replacement and upgrade cadence in the laboratory temperature control units market.

By Capacity: Miniaturization Drives Sub-0.5 kW Surge

The 2–5 kW tier held 28.22% share in 2025 due to multi-instrument cooling, pilot-scale reactors, and centralized loops that support several benchtop users. The sub-0.5 kW category is projected to grow at an 8.86% CAGR, driven by compact LC-MS, GC, PCR, and imaging platforms that either integrate small modules or require small external chillers with simple digital interfaces. Popular compact units fit benchtops and offer USB or Ethernet control with modest power draw, which suits crowded labs and mobile setups. The 0.5–2 kW band covers rotary evaporation, mid-size environmental chambers, and small freeze-dryers, with stable demand as labs refresh around compliance timelines. Above 5 kW, usage blends into industrial process cooling with selective lab deployments in core facilities. Capacity selection continues to hinge on instrument heat load with headroom for ambient shifts and lifecycle performance drift.

Connectivity and redundancy are becoming important even in mid-capacity tiers as buyers weigh uptime and service support. Controller options that route alarms to facilities teams reduce response time and protect samples and data. As natural-refrigerant platforms proliferate, vendors are improving COP at each capacity tier to offset new thermodynamic constraints. This dynamics reinforces value in premium segments of the laboratory temperature control units market where lifecycle risk carries more weight than initial price. Alignment with building systems and compliance documentation further distinguishes higher-capacity offerings in regulated sites.

By End User: Pharmaceuticals Lead While Clinical Diagnostics Accelerate

Pharmaceuticals and biotechnology led with 41.72% of laboratory temperature control units market share in 2025, reflecting 24/7 analytical operations and validated GMP facilities that require high reliability and data integrity. Surveys show biopharma sustained or increased lab-modernization investments in 2025, which translated into more validated, connected chillers and circulators across R&D and QC in 2026.

Academic and research institutes follow as the second-largest segment, often selecting flexible controllers and multi-instrument connectivity to accommodate changing projects. Clinical and diagnostics is projected to grow at a 7.01% CAGR, supported by decentralized testing and compact analyzers that favor sub-0.5 kW solutions with touchscreen control and remote alerts. CROs and CDMOs constitute an important share due to cross-functional needs from discovery to pilot production. Their procurement emphasizes validated systems and service-level agreements that guarantee uptime.

By Application: Analytical Instruments Command Share While Bioprocessing Surges

Analytical instruments support accounted for 24.93% share of the laboratory temperature control units market size in 2025 as LC or GC-MS, NMR, and EM installations increased their reliance on external thermal control to protect resolution and mass accuracy. GC-MS inlet and cryotrap profiles, such as those offered by Shimadzu’s OPTIC-4, illustrate the heat pulses and rapid ramps that external chillers must match during continuous duty[2]Shimadzu Corporation, “OPTIC-4 - Specs,” Shimadzu Corporation, shimadzu.com. Lab reactors and process development require dynamic control and safety interlocks that track exotherms and endotherms with fast ramps under varying loads. Sample conditioning and thermal testing extend from pharmaceutical stability to environmental stress screens for electronics, which favors validated chambers and circulators with compliant logging.

Bioprocessing and cold-chain labs are expected to expand at an 8.03% CAGR through 2031, backed by cell therapy, viral vectors, and monoclonal antibodies that depend on consistent freeze-thaw kinetics. Microfluidics and live-cell imaging tend toward thermoelectric modules that avoid vibration and provide quiet operation for high-resolution optics. Vendors are responding with application-specific control profiles and integration kits that allow instruments to interlock with external chillers. Single-use and plate-based freeze-thaw systems that reach −80 °C and below are expanding in CGT workflows and align with validated data integrity and GMP needs.

By Form Factor: Benchtop Units Lead While Integrated Modules Gain

Benchtop systems led with 36.63% in 2025, reflecting strong demand for compact footprints, rapid setup, and point-of-use flexibility in labs with constrained space. Floor-standing units address higher loads and centralized solutions with redundant circuits, which remain common in QC labs and core facilities. Rack-mounted units serve semiconductor and telecom test environments where vertical integration and cleanroom compatibility are priorities. Integrated or OEM modules are projected to grow at a 7.58% CAGR as instrument manufacturers embed cooling to optimize performance, validation, and service under a single warranty. Under-counter and portable options fill niche needs with small footprints and ruggedized designs used in field or bedside diagnostics. This diversity sustains wide coverage across lab types and workflows in the laboratory temperature control units market.

Form factor preferences track capacity, integration, and validation priorities. Benchtops lead when flexibility and speed of redeployment matter most, while OEM integration appeals when compliance and warranty simplicity carry more weight. Connectivity and alarm routing are increasingly standard, even on compact units, to support fleet management. Natural-refrigerant adoption is moving across all form factors as redesigns homogenize controls and compressors. Shorter lead times and validation documentation continue to differentiate suppliers. These factors support broad and steady adoption in the laboratory temperature control units market.

By Distribution Channel: Direct Sales Dominate While eCommerce Rises

Direct sales held 61.83% in 2025 as buyers demanded application engineering, validation support, and integration assistance that required trained field teams. Pharmaceutical and biotechnology buyers often require three quotes, IOQ packages, and service-level agreements, which favor OEM-direct channels that maintain documentation and spare parts. Distributors and e-commerce are projected to grow at 7.46% as academic and startup labs look for transparent pricing and quick delivery across standard SKUs. Hybrid models that couple distributor reach with OEM technical support are becoming common to safeguard service quality while scaling access. Online content with datasheets, videos, and reviews assists pre-sales qualification across common configurations. These patterns reflect a stable channel mix that continues to favor high-touch engagements for validated deployments within the laboratory temperature control units market.

As RFPs increasingly include refrigerant compliance, energy efficiency, and connectivity, direct channels maintain an edge in custom configuration and integration. Distributors continue to scale breadth and logistics to serve fast-turn needs in standard use cases. Post-install service attachments remain a key profit lever for both models. Combined, they support broad availability and service coverage as compliance timelines advance and refresh cycles accelerate.

Geography Analysis

North America captured 34.82% of the laboratory temperature control units market size in 2025, driven by regulated pharmaceutical operations, instrument clusters across leading research universities, and validated workflows that raise demand for uptime guarantees and service contracts. Energy and performance rules for chillers concentrate spend on efficient units with variable-speed components and plate heat exchangers, which align with procurement documents in Canada and the United States.

Asia-Pacific is projected to record a 10.48% CAGR through 2031, reflecting pharmaceutical and semiconductor capacity expansions that multiply the installed base for precision cooling. China’s 2026 production gains in pharmaceuticals and a broader reorientation to higher-value biopharma reinforce demand from R&D to QC. Taiwan’s ITRI pilot line in 2026 and Rigaku’s metrology center in 2025 expand demand for tight temperature control in metrology and process R&D[4]PR Newswire Staff, “ITRI Breaks Ground on Advanced Semiconductor R&D Center Featuring a 12-Inch Pilot Line,” PR Newswire, prnewswire.com. India’s manufacturing expansions in 2026, including Alkem and Lupin projects, incorporate centralized and modular TCU architectures in validated suites, which raises both point-of-use and plant-integrated demand.

Europe maintains a mature installed base but faces binding refrigerant rules that push rapid transitions to R-290, R-744, and solid-state thermal control where feasible. The EU F-Gas pathways set near-term bans in 2027 and 2032 by capacity, which accelerates redesigns and procurement shifts to compliant systems. That environment rewards suppliers with natural-refrigerant portfolios and established validation support.

Competitive Landscape

The laboratory temperature control units market shows moderate fragmentation in 2026, with the top tier comprised of multinationals and specialized thermal control vendors that compete on refrigerant roadmaps, energy performance, and validation support. Suppliers that have launched CO2 or propane-based lines are positioning for the EU and North American timelines, while also improving partial-load efficiency with inverter-driven compressors and adaptive fans. Product lines marketed as green or compliant now include detailed safety features, training programs, and spare-parts kits to facilitate field retrofits. Documentation packages and connectivity to building systems are becoming strategic differentiators as labs elevate audit readiness and remote alerting. This shift supports premium mix in the laboratory temperature control units market as compliance and data integrity rise in priority.

Strategic moves in 2025 and 2026 emphasize portfolio breadth and workflow integration. Launched product families with natural refrigerants and speed-controlled compressors highlight lower partial-load energy use and reduced refrigerant charges per unit. On the services side, vendors are scaling remote diagnostics, predictive maintenance, and multiyear service agreements that stabilize revenue and raise attachment rates. In parallel, instrument makers and integrators are embedding thermal control in turnkey solutions to reduce qualification time and simplify warranties. These steps create stickiness and raise switching costs in the laboratory temperature control units market.

Laboratory Temperature Control Units Industry Leaders

-

Thermo Fisher Scientific Inc.

-

LAUDA

-

JULABO GmbH

-

PolyScience

-

Peter Huber Kältemaschinenbau SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Peter Huber announced new Peltier-based and natural-refrigerant laboratory TCUs at Analytica 2026 in Munich, including an ultra-compact Piccolo recirculating chiller using thermoelectric technology and expanded Unistat dynamic systems focused on precise and sustainable cooling aligned to upcoming European restrictions.

- November 2025: JULABO introduced the VALEGRO H Series as an all-around laboratory temperature control platform, designed to consolidate multiple legacy circulator families and target pharma, biotech, and analytical instrument cooling applications.

Global Laboratory Temperature Control Units Market Report Scope

As per the scope of the report, laboratory temperature control units are specialized devices used to regulate and maintain precise temperature conditions within a laboratory environment. They are designed to provide consistent temperature control for experiments, samples, or equipment, ensuring accuracy and repeatability in scientific processes. These units typically include features such as temperature regulation, monitoring, and safety mechanisms to achieve and sustain the desired temperature range.

The laboratory temperature control units market report is segmented by product, including recirculating chillers, refrigerated/heating circulators, heating circulators, highly dynamic temperature control systems, laboratory temperature controllers, water baths & shaking water baths, and others. Based on cooling technology, the market is classified into air-cooled, water-cooled, thermoelectric peltier, cryogenic/LN2 or CO2-assisted, and others. By temperature range, the market covers below −40 °C, −40 to −20 °C, −20 to 0 °C, 0 to +100 °C, and Others. In terms of capacity, segmentation includes < 0.5 kw, 0.5–2 kw, 2–5 kw, and > 5 kw. The market is further segmented by end user into pharmaceuticals & biotechnology, academic & research institutes, clinical & diagnostics, and others. By application, the segments comprise analytical instruments support, lab reactors & process development, sample conditioning & thermal testing, bioprocessing & cold-chain labs, microfluidics & live-cell imaging, and others. Based on form factor, the market includes benchtop, floor-standing, rack-mounted, integrated/OEM modules, and others. Distribution channels are categorized into direct sales, distributors, and ecommerce. Geographically, the market spans North America, Europe, Asia-Pacific, Middle East and Africa, and South America, with market forecasts provided in terms of value in USD. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally.

| Recirculating Chillers |

| Refrigerated/Heating Circulators |

| Heating Circulators |

| Highly Dynamic Temperature Control Systems |

| Laboratory Temperature Controllers |

| Water Baths & Shaking Water Baths |

| Others (Micro-temperature Control Units, Reactor Temperature Control Units, etc.) |

| Air-cooled |

| Water-cooled |

| Thermoelectric (Peltier) |

| Cryogenic/LN2 or CO2-assisted |

| Others (Hybrid vapor-compression, Absorption Cooling Systems) |

| Below −40 °C |

| −40 to −20 °C |

| −20 to 0 °C |

| 0 to +100 °C |

| Others (+ 100 to +300 °C, Above +300 °C) |

| < 0.5 kW |

| 0.5 – 2 kW |

| 2 – 5 kW |

| > 5 kW |

| Pharmaceuticals & Biotechnology |

| Academic & Research Institutes |

| Clinical & Diagnostics |

| Others (CROs, CDMOs) |

| Analytical Instruments Support (LC/GC-MS, NMR, EM) |

| Lab Reactors & Process Development |

| Sample Conditioning & Thermal Testing |

| Bioprocessing & Cold-Chain Labs |

| Microfluidics & Live-cell Imaging |

| Others (Reagent Preparation & Storage Conditioning, Vaccine Development & Formulation Testing) |

| Benchtop |

| Floor-standing |

| Rack-mounted |

| Integrated/OEM Modules |

| Others (Under-counter Units, Portable) |

| Direct Sales |

| Distributors |

| e-Commerce |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Recirculating Chillers | |

| Refrigerated/Heating Circulators | ||

| Heating Circulators | ||

| Highly Dynamic Temperature Control Systems | ||

| Laboratory Temperature Controllers | ||

| Water Baths & Shaking Water Baths | ||

| Others (Micro-temperature Control Units, Reactor Temperature Control Units, etc.) | ||

| By Cooling Technology | Air-cooled | |

| Water-cooled | ||

| Thermoelectric (Peltier) | ||

| Cryogenic/LN2 or CO2-assisted | ||

| Others (Hybrid vapor-compression, Absorption Cooling Systems) | ||

| By Temperature Range | Below −40 °C | |

| −40 to −20 °C | ||

| −20 to 0 °C | ||

| 0 to +100 °C | ||

| Others (+ 100 to +300 °C, Above +300 °C) | ||

| By Capacity | < 0.5 kW | |

| 0.5 – 2 kW | ||

| 2 – 5 kW | ||

| > 5 kW | ||

| By End User | Pharmaceuticals & Biotechnology | |

| Academic & Research Institutes | ||

| Clinical & Diagnostics | ||

| Others (CROs, CDMOs) | ||

| By Application | Analytical Instruments Support (LC/GC-MS, NMR, EM) | |

| Lab Reactors & Process Development | ||

| Sample Conditioning & Thermal Testing | ||

| Bioprocessing & Cold-Chain Labs | ||

| Microfluidics & Live-cell Imaging | ||

| Others (Reagent Preparation & Storage Conditioning, Vaccine Development & Formulation Testing) | ||

| By Form Factor | Benchtop | |

| Floor-standing | ||

| Rack-mounted | ||

| Integrated/OEM Modules | ||

| Others (Under-counter Units, Portable) | ||

| By Distribution Channel | Direct Sales | |

| Distributors | ||

| e-Commerce | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the size and growth outlook for the Laboratory Temperature Control Units market through 2031?

The Laboratory Temperature Control Units market size is expected to increase from USD 1.11 billion in 2025 to USD 1.18 billion in 2026 and reach USD 1.58 billion by 2031, at a 6.04% CAGR over 2026-2031.

Which end users account for the largest share in 2026 planning cycles?

Pharmaceuticals and biotechnology led with 41.72% in 2025 due to validated R&D and GMP operations, and they continue to drive premium adoption in 2026 as modernization and uptime needs rise.

Which product categories are expanding fastest in this space?

Highly dynamic temperature control systems have the steepest growth profile at an 8.85% CAGR through 2031, reflecting fast ramps and precision control needs in reaction development and semiconductor workflows.

How are regulations affecting equipment choices in 2026?

EU F-Gas rules restrict high-GWP refrigerants from 2027 for larger chillers and from 2032 for smaller units, and the U.S. EPA has proposed phased timelines by application, which accelerates shifts to natural refrigerants and compliant designs.

Where is regional growth most pronounced?

Asia-Pacific is projected to record a 10.48% CAGR through 2031, supported by pharmaceutical build-outs and semiconductor investments in China, India, and Taiwan that expand the installed base for precision temperature control.

What capacities are most common for analytical instruments like LC-MS or GC-MS?

Typical LC or GC-MS stacks run 1.2-1.8 kW of thermal load, and buyers often select 2 kW chillers with headroom to maintain stability across ambient changes and lifecycle wear.

Page last updated on: