Laboratory Supplies Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

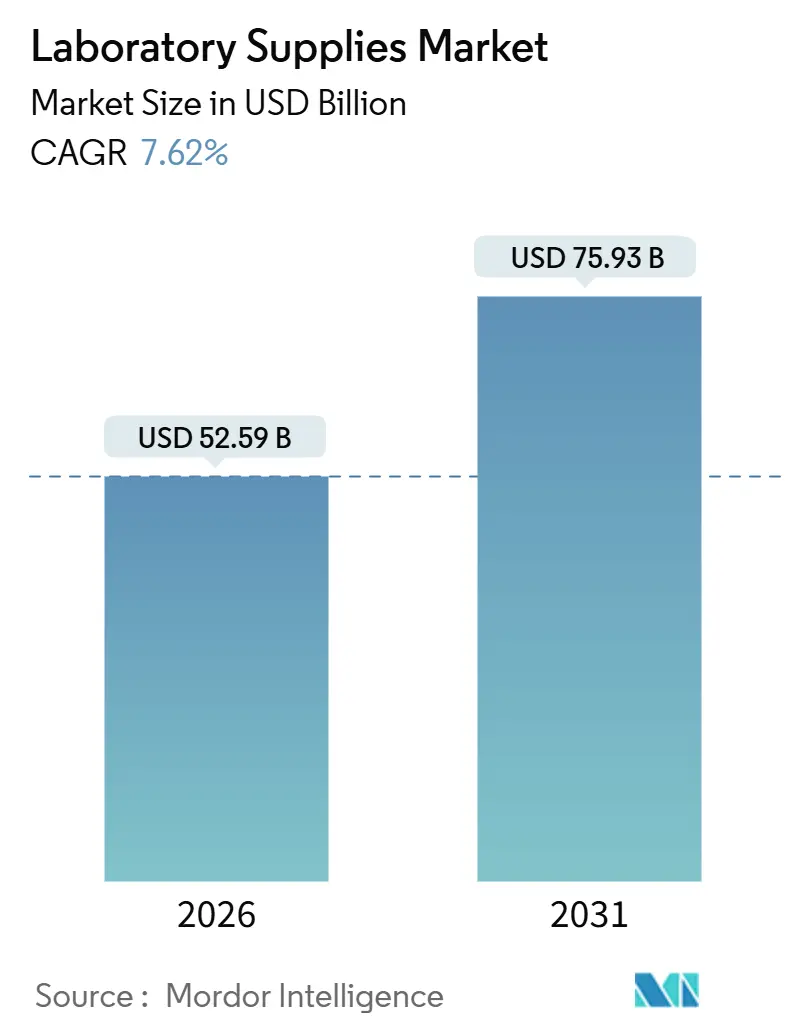

| Market Size (2026) | USD 52.59 Billion |

| Market Size (2031) | USD 75.93 Billion |

| Growth Rate (2026 - 2031) | 7.62% CAGR |

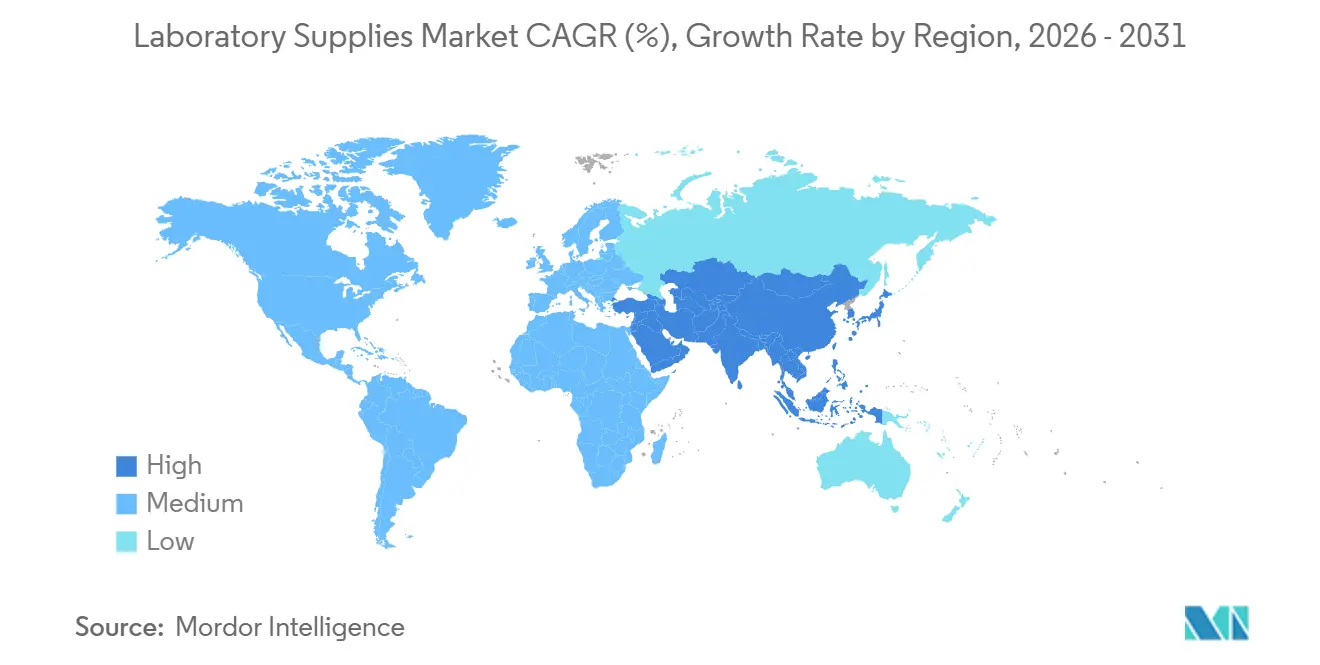

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

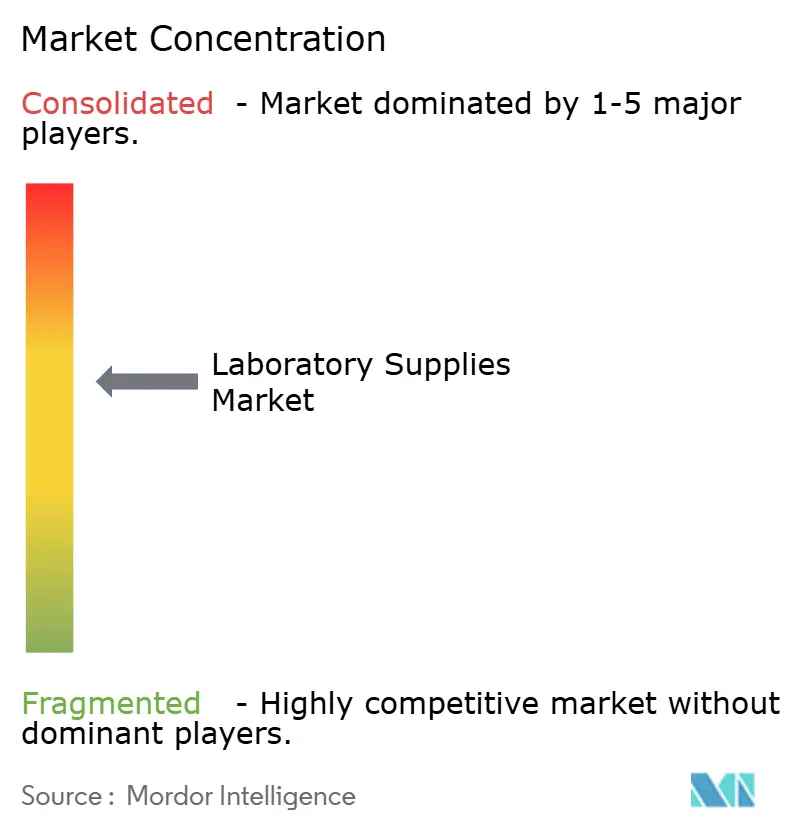

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laboratory Supplies Market Analysis by Mordor Intelligence

The Laboratory Supplies Market size is estimated at USD 52.59 billion in 2026, and is expected to reach USD 75.93 billion by 2031, at a CAGR of 7.62% during the forecast period (2026-2031).

Research budgets in life sciences, clinical diagnostics, and biotechnology continue to expand, boosting demand for analytical instruments, automation platforms, and single-use consumables. Disposables will outpace equipment because biofoundries and contract laboratories favor contamination-free workflows, while regulatory scrutiny of data integrity and sustainability steers procurement toward connected systems and bio-based polymers. Leading vendors are accelerating acquisitions to assemble full-service portfolios, and smaller robotics specialists keep chipping away at niche opportunities by offering open-source, low-cost alternatives. Moving forward, geographic growth remains fastest in Asia-Pacific, yet North America still anchors the laboratory supplies market through steady funding of academic and government research programs.

Key Report Takeaways

- By product type, equipment held 61.45% of the laboratory supplies market share in 2025; disposables and consumables are forecast to grow at a 10.04% CAGR through 2031.

- By application, clinical diagnostics and pathology accounted for 44.23% of the laboratory supplies market size in 2025 and is projected to expand at an 8.0% CAGR to 2031.

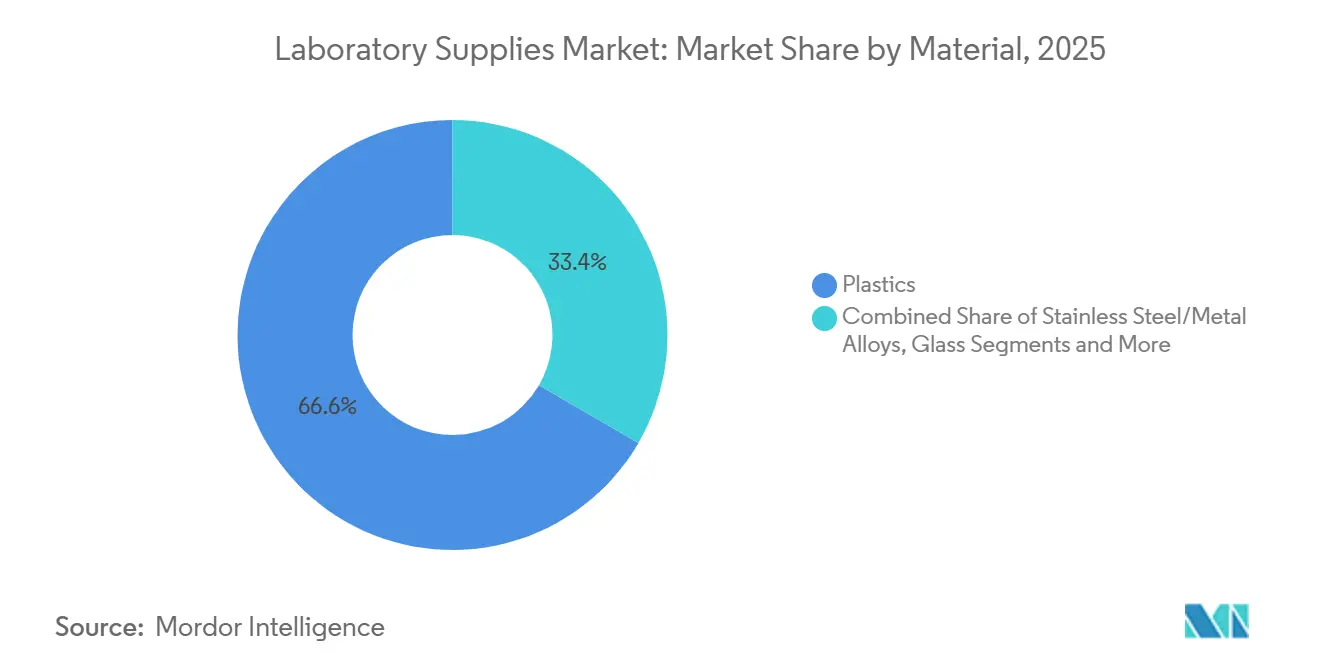

- By material type, plastics captured 66.63% revenue share in 2025; biodegradable and bio-based polymers are advancing at an 11.45% CAGR through 2031.

- By end user, pharmaceutical and biotechnology companies led with 39.14% of the laboratory supplies market share in 2025, while contract research and testing laboratories are on track for a 10.53% CAGR to 2031.

- By geography, North America held 36.46% in 2025, and Asia-Pacific is set to record a 9.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Laboratory Supplies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Global R&D Expenditure in Life Sciences and Biotechnology | +1.5% | North America, Western Europe, APAC hubs | Long term (≥ 4 years) |

| Expansion of Clinical Diagnostics & Molecular Testing Volumes | +1.3% | Global, strong in APAC & Middle East | Medium term (2-4 years) |

| Rising Adoption of Automation & High-Throughput Platforms | +1.2% | North America, EU, fast-growing in APAC | Medium term (2-4 years) |

| Accelerated Post-COVID-19 Healthcare Infrastructure Funding | +0.9% | Emerging markets (India, Brazil, GCC) | Short term (≤ 2 years) |

| Proliferation of Biofoundries Driving Disposable Demand | +0.8% | U.S., UK, Netherlands, Singapore | Long term (≥ 4 years) |

| Shift Toward Sustainable / Biodegradable Consumables | +0.7% | EU lead, North America follow | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Global R&D Expenditure in Life Sciences and Biotechnology

Global pharmaceutical and biotechnology R&D budgets reached USD 244 billion in 2025, reflecting persistent investment in precision oncology, cell and gene therapy, and rare-disease programs. Each new molecular entity consumes thousands of assay plates and hundreds of liters of media, creating a direct link between research outlays and purchases across the laboratory supplies market. Government agencies reinforce the trend; the U.S. National Institutes of Health raised appropriations to USD 49.8 billion in fiscal 2025, sustaining demand for chromatography columns, spectrophotometers, and genomic reagents.[1]Francis Collins, “NIH Budget for Fiscal Year 2025,” National Institutes of Health, nih.gov Large emerging economies are catching up, with China surpassing USD 35 billion in biopharmaceutical R&D spending in 2025 and India channeling USD 2 billion in incentives toward biologics facilities that require quality-control laboratories. Academic institutions in Europe and North America budgeted USD 12 billion for instrument upgrades between 2024 and 2026, ensuring recurring procurement of consumables.[2]National Science Foundation, “Synthetic Biology Foundry Grants,” nsf.gov

Expansion of Clinical Diagnostics & Molecular Testing Volumes

Clinical laboratories processed 18% more molecular tests in 2025 than in 2024 after the FDA cleared 47 new in-vitro diagnostic platforms, many designed for liquid-biopsy oncology panels.[3]U.S. Food and Drug Administration, “IVD Device Approvals 2024-2025,” fda.govMedicare reimbursement expanded coverage for multiple tumor types, encouraging hospitals and independent labs to install additional PCR and next-generation sequencing capacity. Pathology facilities in the United States invested USD 4.2 billion in automation during 2025, installing track-based systems able to sort, decap, and aliquot up to 3,000 samples per hour. Infectious-disease surveillance mandates added further momentum in Asia-Pacific, where Singapore required all acute-care hospitals to maintain daily PCR capacity for 10,000 tests by year-end 2024. The rise of point-of-care molecular devices, exemplified by Roche’s approved 15-minute respiratory panel, is pushing disposable cartridge volumes higher.

Rising Adoption of Automation & High-Throughput Laboratory Platforms

Robotic liquid handlers, automated incubators, and integrated screening lines are now mainstream. Entry-level open-source robots priced near USD 5,000 helped Opentrons ship 12,000 units in 2025, tripling its installed base since 2023. Larger pharmaceutical companies favor multi-arm workstations that cost up to USD 2 million but lower assay costs by 60% over five years. Vendors are embedding computer-vision tools that detect pipetting errors in real time, cutting reagent waste by nearly one-fifth. Contract research organizations (CROs) rely on standardized automation to let sponsors transfer assays across sites without revalidation, accelerating outsourcing and lifting recurrent demand in the laboratory supplies market.

Accelerated Post-COVID-19 Healthcare Infrastructure Funding

Governments earmarked USD 85 billion for diagnostic infrastructure upgrades between 2024 and 2026, determined to avoid the shortages that hampered pandemic response. India’s National Health Mission Phase III set aside INR 120 billion (USD 1.44 billion) to establish 1,200 regional hubs equipped with hematology analyzers and PCR systems. Brazil outfitted 500 municipal labs with automated chemistry and hematology platforms in 2025 to move closer to universal coverage. The U.S. Hospital Preparedness Program allocated USD 1.5 billion in fiscal 2025 for biosafety-level-3 facilities, cementing long-term growth in the laboratory supplies market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Advanced Laboratory Equipment | –0.6% | Global, acute in emerging markets | Medium term (2-4 years) |

| Supply-Chain Volatility & Raw-Material Price Fluctuations for Plastics | –0.5% | Regions dependent on petrochemical imports | Short term (≤ 2 years) |

| Increasing Cybersecurity & Data-Integrity Compliance Costs | –0.4% | North America, EU, spreading to APAC | Medium term (2-4 years) |

| Regulatory Scrutiny of Single-Use Plastics Waste | –0.3% | EU lead, other regions catching up | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Laboratory Equipment

Acquiring automated liquid handlers, mass spectrometers, or next-generation sequencers can require USD 500,000 to USD 3 million per unit. Installation and validation add another 20% to 30%, while annual maintenance contracts consume 8% to 12% of purchase price. Public institutions in Brazil and South Africa often defer upgrades because grants arrive late, forcing instruments beyond their recommended service life, which raises downtime risk and limits uptake of the newest consumables required for optimal performance.

Supply-Chain Volatility & Raw-Material Price Fluctuations for Plastics

Polypropylene averaged USD 1,420 per metric ton in Q1 2025, 22% higher than in 2024, squeezing disposable-labware producers that operate on mid-teen gross margins. A six-week shutdown at a polystyrene plant in South Korea and shipping delays through the Suez Canal extended lead times for pipette tips from four to twelve weeks. European firms confronted elevated energy costs as German natural-gas prices tripled versus 2020, driving molding expenses up 15%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Equipment Anchors Revenue, Disposables Drive Growth

Equipment generated 61.45% of 2025 revenue, underlining the installed base that binds day-to-day workflows. Automation upgrades, including robotic liquid handlers and integrated incubators, now account for a rising share of orders because they lower per-assay cost. Disposables are set to grow at a 10.04% CAGR through 2031, easily outpacing other categories as biofoundries, diagnostic labs, and CROs prioritize sterility and quick turnaround. Thermo Fisher posted 28% annual growth in pipette-tip sales during 2025 after cell-therapy facilities mandated ISO Class 5-compatible consumables. New in-vitro diagnostic clearances create proprietary reagent kits that secure recurring income streams. Chemicals and reagents see steady demand, though generic competition from Asia tempers price escalation. Glassware continues its gradual decline; however, high-precision borosilicate items still support spectroscopy and high-temperature reactions where polymers fall short.

Polymer-based single-use bioreactor bags now dominate early-stage biologics production, a switch Sartorius estimates will inject USD 1.2 billion of incremental sales into disposables by 2028. Open-source robots priced at USD 5,000 lengthen equipment life cycles because modular add-ons defer replacement, but they simultaneously boost consumption of tips, plates, and reservoirs. In effect, disposables capture a greater slice of the laboratory supplies market even as overall capital-equipment spending rises.

By Application: Diagnostics Lead, Drug Discovery Accelerates

Clinical diagnostics and pathology laboratories held 44.23% of 2025 revenue, reflecting soaring PCR and liquid-biopsy volumes after broader reimbursement. Drug discovery and development is forecast to grow at a 9.24% CAGR, the fastest among applications, because AI-guided screening and automation compress hit-to-lead timelines. Academic life-science research, environmental testing, and industrial quality control each remain durable contributors but trail diagnostics in growth velocity. Environmental and food labs ramped up LC-MS/MS capacity once the U.S. Environmental Protection Agency finalized PFAS limits, adding fresh orders for extraction cartridges and solvents.

Portable mass spectrometers in forensic settings generate new pockets of demand, and teaching laboratories increasingly adopt microfluidic kits that slash reagent use, a shift that could reshape consumables purchasing by 2028. Meanwhile, point-of-care molecular devices continue to migrate into primary-care offices, increasing total unit count and expanding the laboratory supplies market.

By Material Type: Plastics Dominate, Biopolymers Surge

Plastics commanded 66.63% of 2025 revenue thanks to low-cost injection molding that delivers pipette tips for USD 0.002 each. The category’s ubiquity will continue, yet biopolymers are set to grow at an 11.45% CAGR through 2031 as EU regulations and corporate sustainability programs influence purchasing. Glass maintains a 12% niche where thermal stability and chemical inertness are essential. Stainless-steel and other metals remain critical for reusable labware in GMP-regulated areas, while silicone and elastomers fill specialized roles in seals and tubing.

Greiner Bio-One’s compostable pipette tips and Corning’s tougher Valor Glass illustrate supplier efforts to meet durability and sustainability targets in parallel. Rising polypropylene costs intensify the search for recycled or bio-based inputs, even though such materials command a 15%–25% premium over virgin resin. Overall, plastics retain dominance within the laboratory supplies market, but the mix within the category is shifting rapidly toward greener formulations.

By End User: Pharma Leads, CROs Expand Fastest

Pharmaceutical and biotechnology companies contributed 39.14% of 2025 spending, reflecting sizable R&D budgets and widespread adoption of high-throughput automation. Contract research and testing laboratories are projected to register the highest growth, at a 10.53% CAGR, as drug sponsors outsource to control fixed costs during patent-cliff cycles. Hospitals and diagnostic labs saw an 18% jump in molecular-testing volumes during 2025, reinforcing their role as a steady demand base. Academic institutions remain important purchasers owing to grant-funded instrument replacement cycles.

CROs are now backward-integrating into consumables to leverage their scale, an example being Charles River’s 2024 launch of a private-label pipette-tip line. Such moves promise lower prices for sponsors yet raise competitive pressure on incumbent consumable suppliers. Pharmaceutical firms meanwhile outsource 65% of preclinical toxicology work, lifting consumption of reagents and plates in CRO facilities and adding depth to the laboratory supplies market.

Geography Analysis

North America held 36.46% of 2025 revenue. U.S. federal research funding, anchored by the NIH’s USD 49.8 billion budget, keeps universities and medical centers well supplied with chromatography columns, sequencers, and spectrometers. Canada attracted USD 2.1 billion in life-science foreign investment during 2024, spawning biologics plants that require quality-control labs. The Hospital Preparedness Program in the United States earmarked USD 1.5 billion for biosafety-level-3 capacity in fiscal 2025, ensuring continuing demand for containment hoods and PCR systems.

In Europe Germany’s pharmaceutical output exceeded EUR 45 billion, and the EU Single-Use Plastics Directive forces suppliers to revamp materials, spurring investment in recycling capacity. France’s levy on non-recyclable lab plastics triggered new bio-polymer launches, while the NHS set aside GBP 800 million for lab modernization that includes mass spectrometers and sequencers. Sartorius expanded cleanroom space in Germany to meet demand for single-use bioprocess consumables, underscoring Europe’s pull on global supply chains.

Asia-Pacific will grow at a 9.22% CAGR, driven by China’s USD 180 billion pharmaceutical output in 2025 and India’s USD 2 billion incentive for API sites. Singapore attracted USD 8 billion in biotech investment between 2024 and 2025, and South Korea expanded biologics capacity by 25% in 2025, consuming USD 150 million in disposables. Japan’s plastics-circulation tax encourages recycled content in consumables, nudging material demand toward bio-based variants.

Middle East & Africa and South America are smaller but rising. The Gulf Cooperation Council invested USD 6.2 billion in hospital projects over 2024-2025, each facility fitted with multiple specialized laboratories. Brazil allotted BRL 1.8 billion (USD 360 million) in 2025 to upgrade 500 municipal labs with automated analyzers. South Africa’s pharmaceutical manufacturers installed HPLC systems to satisfy export quality requirements, demonstrating a broader modernization pattern that widens the global footprint of the laboratory supplies market.

Competitive Landscape

The laboratory supplies market remains moderately concentrated. Danaher’s USD 5.7 billion purchase of Abcam added 180,000 antibody SKUs and deepened its presence in proteomics, while Thermo Fisher’s USD 3.1 billion acquisition of Olink broadened multiplex and biomarker-analysis capabilities. Sartorius extended cleanroom capacity in Germany by 15,000 m² to satisfy rising demand for single-use bioreactor bags. Agilent’s BioTek Cytation C10 combined imaging, screening, and liquid handling in one bench-top unit priced at USD 250,000, reducing the need for multiple instruments.

Robotics disruptors inject fresh competition. Opentrons tripled its installed base between 2023 and 2025 by selling affordable, open-source automation platforms. Ginkgo Bioworks licensed its foundry-management software to academic centers, fostering protocol standardization that indirectly boosts consumable pull-through. Corning filed 18 patents on new surface coatings for culture plates in 2024, aiming to capture share in the USD 2.4 billion cell-culture consumables segment.

Regulatory compliance and sustainability credentials serve as competitive moats. Suppliers operating FDA-registered, ISO 13485-certified facilities command double-digit price premiums because pharmaceutical clients prize audit readiness. Vendors that demonstrate closed-loop recycling or carbon-neutral production increasingly win procurement contracts from universities and large biopharma manufacturers, hinting that environmental performance will shape competitive positioning in the laboratory supplies market.

Laboratory Supplies Industry Leaders

Thermo Fisher Scientific

Danaher

Agilent Technologies

Merck KGaA

Revvity Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Agilent Technologies released Altura Ultra Inert HPLC columns tailored for peptide and oligonucleotide biotherapeutics, enhancing separation efficiency for regulatory QC workflows.

- May 2025: Waters Corporation launched BioResolve Protein A affinity columns featuring MaxPeak Premier surface, improving titer measurements for antibody production

- April 2025: QIAGEN confirmed plans to introduce three automated sample-preparation instruments before end-2026, broadening its workflow solutions.

Global Laboratory Supplies Market Report Scope

Laboratory supplies are tools, materials, and equipment, including reusable items like microscopes and single-use consumables like pipette tips, used by scientists, researchers, and medical professionals for experiments, tests, and analyses.

The Laboratory Supplies Market Report is segmented by Product Type, Application, Material Type, End User, and Geography. By Product Type, the market is segmented into Equipment, Disposables/Consumables, Chemicals & Reagents, and Others. By Application, the market is segmented into Biochemistry & Life-Science Research, Clinical Diagnostics & Pathology, Drug Discovery & Development, Environmental & Food Testing, Forensic & Security Laboratories, Industrial Quality Control, and Academic Teaching Labs. By Material Type, the market is segmented into Plastics, Glass, Stainless Steel/Metal Alloys, Silicone & Other Elastomers, Ceramics & Porcelain, and Biodegradable/Bio-based Polymers. By End User, the market is segmented into Academic & Research Institutes, Pharmaceutical & Biotech Companies, Hospitals & Diagnostic Laboratories, Contract Research & Testing Labs, and Others. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America.The market report also covers the estimated market sizes and trends across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Equipment |

| Disposables / Consumables |

| Chemicals & Reagents |

| Others (Glassware, Accessories) |

| Biochemistry & Life-Science Research |

| Clinical Diagnostics & Pathology |

| Drug Discovery & Development |

| Environmental & Food Testing |

| Forensic & Security Laboratories |

| Industrial Quality Control |

| Academic Teaching Labs |

| Plastics (PP, PS, PE) |

| Glass (Borosilicate, Quartz) |

| Stainless Steel / Metal Alloys |

| Silicone & Other Elastomers |

| Ceramics & Porcelain |

| Biodegradable / Bio-based Polymers |

| Academic & Research Institutes |

| Pharmaceutical & Biotech Companies |

| Hospitals & Diagnostic Laboratories |

| Contract Research & Testing Labs (CROs) |

| Others (Food, Environmental, Forensic) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Equipment | |

| Disposables / Consumables | ||

| Chemicals & Reagents | ||

| Others (Glassware, Accessories) | ||

| By Application | Biochemistry & Life-Science Research | |

| Clinical Diagnostics & Pathology | ||

| Drug Discovery & Development | ||

| Environmental & Food Testing | ||

| Forensic & Security Laboratories | ||

| Industrial Quality Control | ||

| Academic Teaching Labs | ||

| By Material Type | Plastics (PP, PS, PE) | |

| Glass (Borosilicate, Quartz) | ||

| Stainless Steel / Metal Alloys | ||

| Silicone & Other Elastomers | ||

| Ceramics & Porcelain | ||

| Biodegradable / Bio-based Polymers | ||

| By End User | Academic & Research Institutes | |

| Pharmaceutical & Biotech Companies | ||

| Hospitals & Diagnostic Laboratories | ||

| Contract Research & Testing Labs (CROs) | ||

| Others (Food, Environmental, Forensic) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the laboratory supplies market in 2031?

The laboratory supplies market size is expected to reach USD 75.93 billion by 2031, reflecting a 7.62% CAGR from 2026.

Which product category will post the fastest growth through 2031?

Disposables and consumables are forecast to grow at a 10.04% CAGR as labs favor single-use workflows for sterility and efficiency.

Why are bio-based polymers gaining momentum in laboratory consumables?

EU regulations mandate recycled or biodegradable content, while corporate sustainability goals push buyers toward bio-based tips, tubes, and flasks.

Which region will record the highest growth rate?

Asia-Pacific is slated for a 9.22% CAGR, driven by expanding pharmaceutical production in China, India, and Southeast Asia.

How are automation trends influencing laboratory equipment purchases?

Affordable open-source robots and integrated high-throughput systems cut assay costs, increase reproducibility, and stimulate recurring consumable demand.

What drives CRO demand for laboratory supplies?

Sponsors outsource more preclinical and analytical work, prompting CROs to invest in standardized automation and large volumes of reagents and disposables.

Page last updated on: