Laboratory Equipment Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 25.04 Billion |

| Market Size (2031) | USD 45.45 Billion |

| Growth Rate (2026 - 2031) | 12.67% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laboratory Equipment Services Market Analysis by Mordor Intelligence

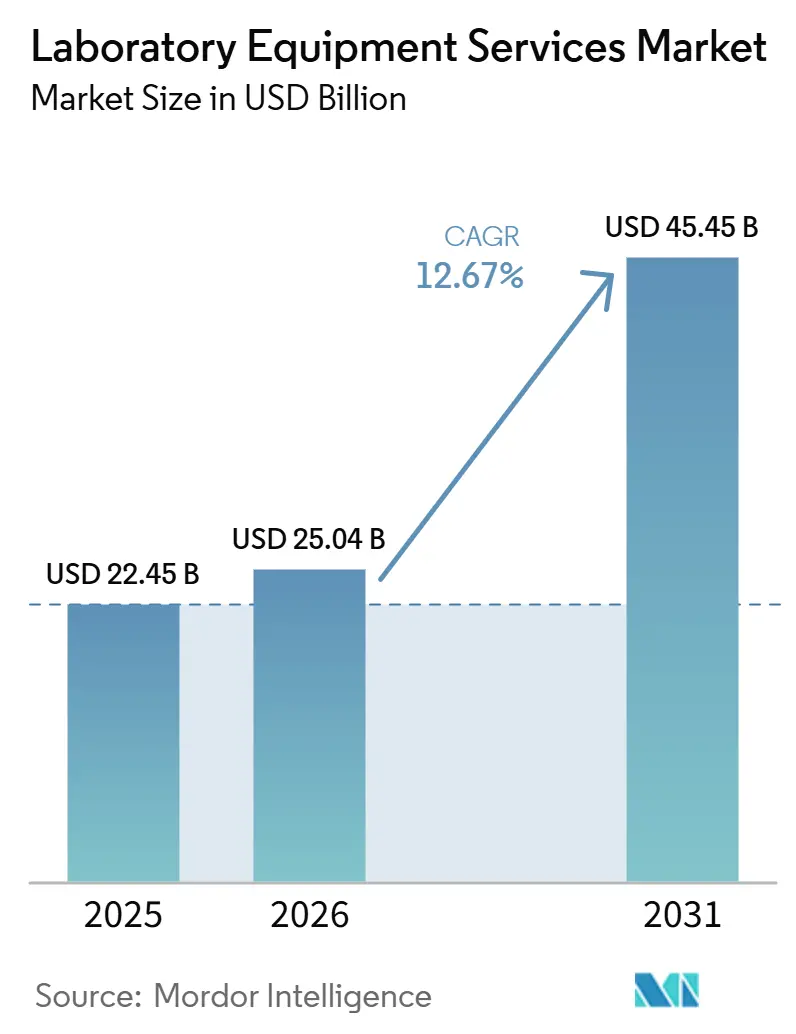

The Laboratory Equipment Services Market size is projected to be USD 22.45 billion in 2025, USD 25.04 billion in 2026, and reach USD 45.45 billion by 2031, growing at a CAGR of 12.67% from 2026 to 2031.

The laboratory equipment services market is expanding because laboratories now rely on more complex instruments across pharmaceutical, biotechnology, and clinical settings, and those systems need regular maintenance, calibration, and qualification to stay productive. The laboratory equipment services market is also moving away from one-time repair work toward broader service agreements that cover uptime, compliance, and lifecycle support, which changes how buyers evaluate operating costs. The laboratory equipment services market remains shaped by OEM advantages in proprietary software, parts access, and factory-trained service teams, while independent and multi-vendor providers compete where customers need lower cost structures and faster local support. Demand also improves when laboratories choose to outsource servicing instead of building internal capabilities for specialized instruments, especially where staffing depth is limited and regulatory expectations remain strict. The laboratory equipment services market therefore, benefits from both new instrument placements and the recurring service burden that follows every installation across regulated and research-heavy environments.

Key Report Takeaways

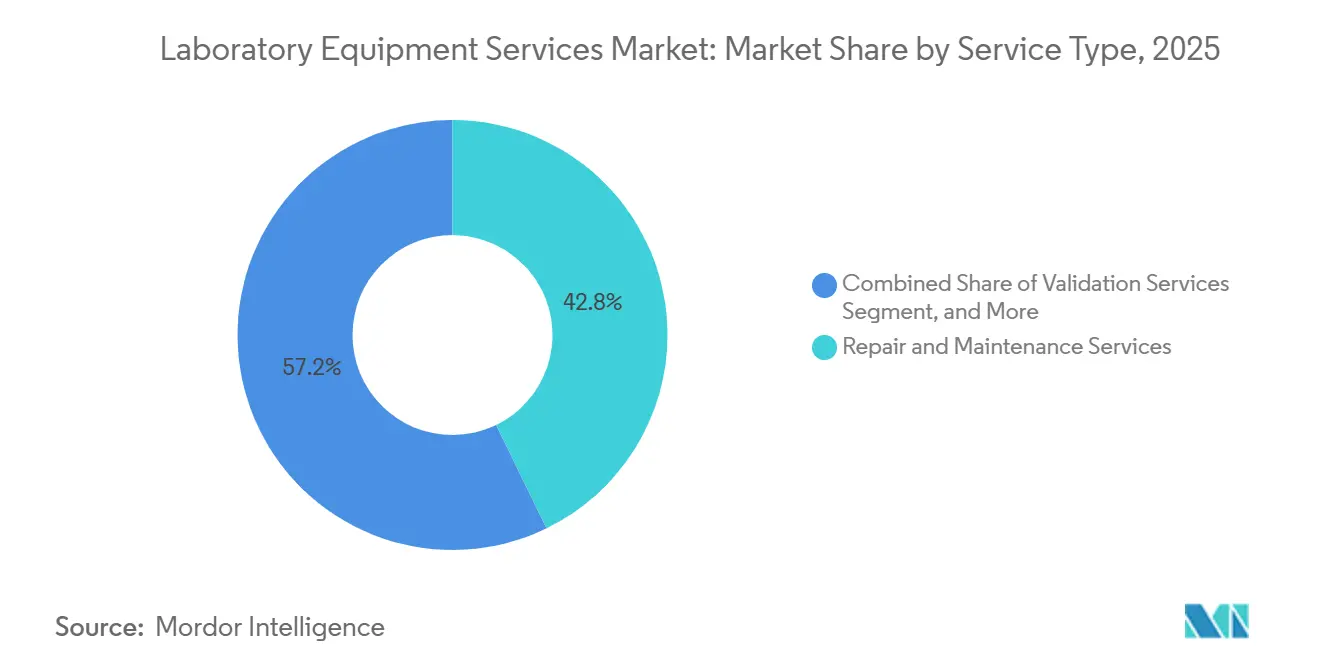

- By service type, repair and maintenance services held 42.83% revenue share in 2025, while validation services are forecast to expand at 14.71% CAGR through 2031.

- By service provider, original equipment manufacturers held 46.38% share in 2025, while the same segment is projected to record the highest CAGR at 13.32% through 2031.

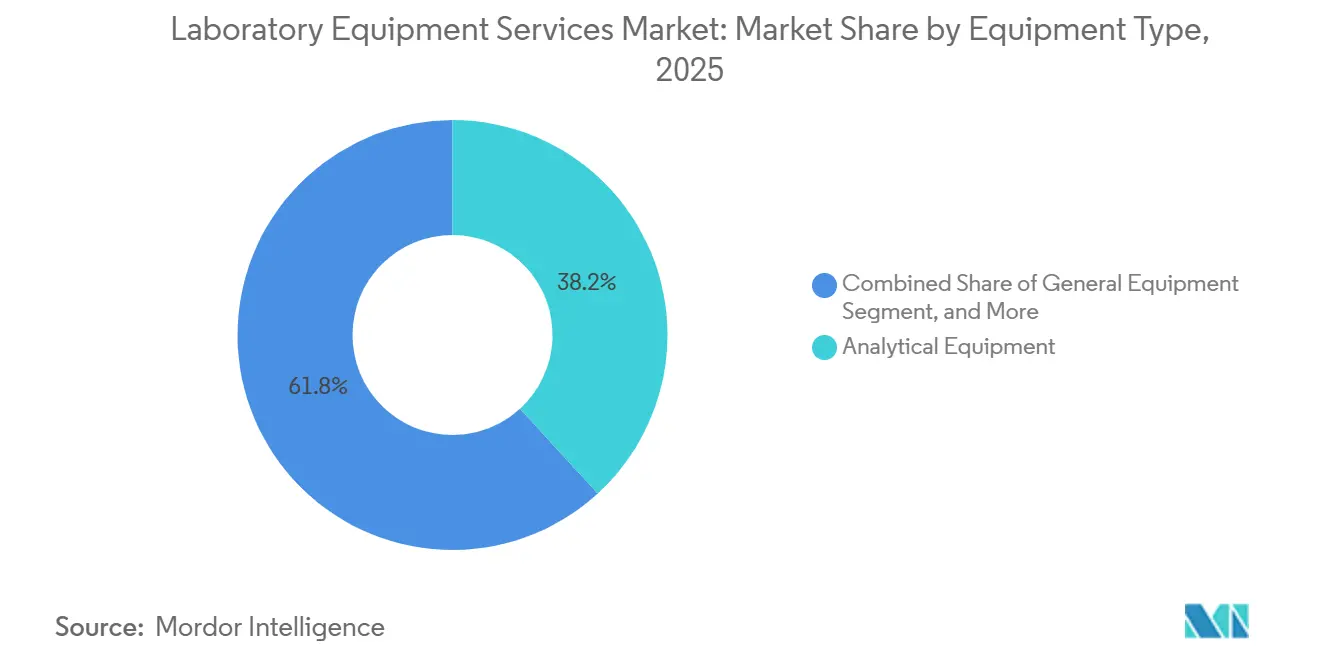

- By equipment type, analytical equipment accounted for 38.16% share in 2025 and is advancing at a 14.59% CAGR through 2031.

- By contract type, standard service contracts held 41.63% share in 2025, while customized service contracts are projected to grow at 13.07% CAGR through 2031.

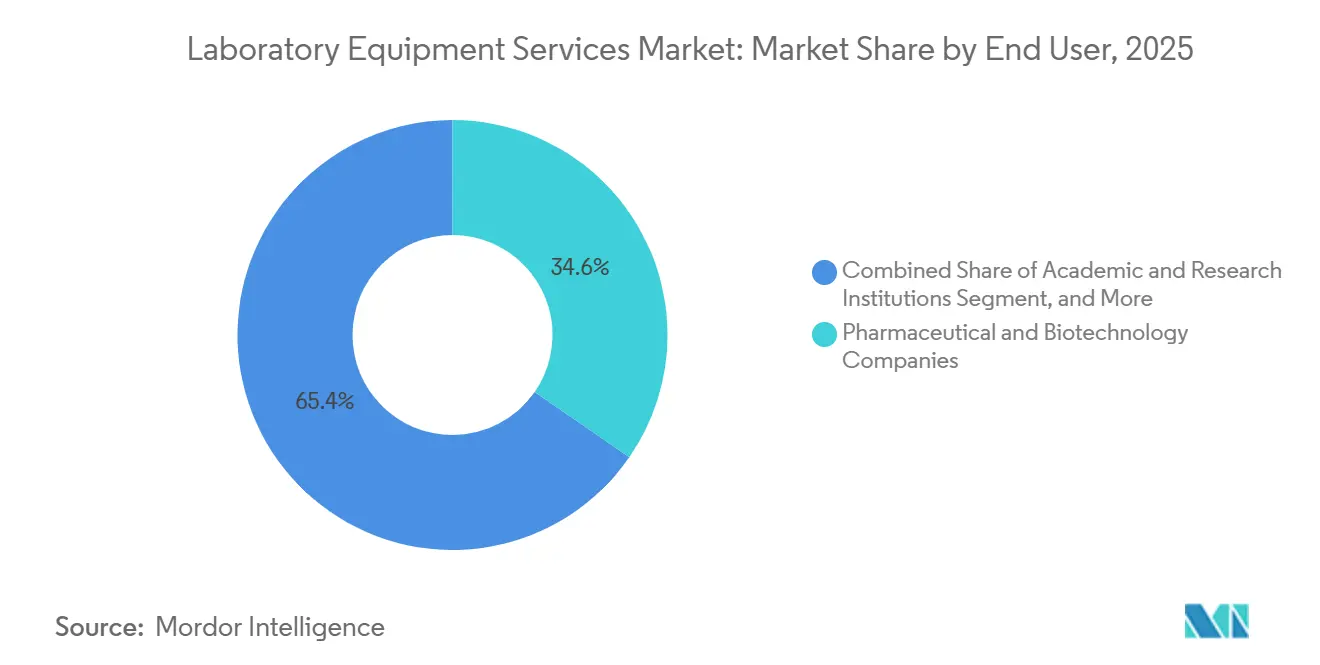

- By end user, pharmaceutical and biotechnology companies held 34.63% share in 2025, while academic and research institutions are forecast to expand at 13.91% CAGR through 2031.

- By geography, North America held 40.63% share in 2025, while Asia-Pacific is projected to grow at 12.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Laboratory Equipment Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Need For Lab Uptime and Downtime Avoidance | +2.3% | Global | Short term (≤ 2 years) |

| Outsourcing Of Multi-Vendor Service Management | +1.8% | North America and EU core, spill-over to APAC | Medium term (2-4 years) |

| Growth In Pharma, Biotech, And Diagnostic Lab Infrastructure | +3.2% | Global, APAC fastest | Long term (≥ 4 years) |

| Remote Diagnostics And Predictive Maintenance Adoption | +1.5% | Global | Medium term (2-4 years) |

| Multi-Asset Compliance Burden In Regulated Laboratories | +1.6% | North America and EU | Medium term (2-4 years) |

| Under-Reported Skill Shortage For High-End Instrument Servicing | +1.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Need For Lab Uptime and Downtime Avoidance

The laboratory equipment services market is benefiting from the higher cost of unplanned downtime in pharmaceutical and clinical laboratories. Laboratories that run regulated workflows cannot easily absorb outages because missed runs, delayed results, and interrupted quality control steps can quickly disrupt operations. That pressure is pushing service contracts closer to a fixed operating requirement instead of a discretionary purchase. The laboratory equipment services market is also seeing stronger demand for preventive and managed coverage because the cost gap between planned maintenance and emergency intervention keeps widening as instruments become more complex. Large campuses with mixed instrument fleets are especially open to multi-vendor service programs because a single provider can coordinate uptime across several platforms. This makes uptime support a practical purchasing priority rather than a secondary after-sales consideration.

Growth In Pharma, Biotech, and Diagnostic Lab Infrastructure

The laboratory equipment services market continues to gain support from expanding pharmaceutical, biotechnology, and diagnostics infrastructure. Every new analytical system, validation workflow, and specialized platform adds a long-tail need for recurring service, calibration, and compliance support once the equipment is installed. That effect is stronger in regulated settings because servicing does not end with the original sale and instead follows the asset through its full operating life. Danaher reported that bioprocessing equipment orders grew more than 30% year over year in Q1 2026, which points to a larger installed base that will require future service coverage.[1]Danaher Corporation, “Danaher Reports Fourth Quarter and Full Year 2025 Results,” Danaher Investor Relations, danaher.com Agilent Technologies and Veeda Lifesciences also launched a joint Analytical Center of Excellence in Bengaluru in May 2026, which reflects the rising technical depth of laboratory infrastructure in India and the related need for high-end support services.[2]Agilent Technologies and Veeda Lifesciences, “Agilent And Veeda Lifesciences Launch Joint Analytical Center Of Excellence,” Veeda Lifesciences Press Release, veedalifesciences.com The laboratory equipment services market therefore, grows not only because more instruments are sold, but because each placement creates recurring obligations for repair, qualification, and performance assurance.

Remote Diagnostics and Predictive Maintenance Adoption

The laboratory equipment services market is changing as connected instruments make remote diagnostics and predictive maintenance more practical. Service models are shifting from scheduled visits toward condition-based intervention, where performance data can signal problems before a failure stops laboratory work. That change lowers emergency service needs and helps providers shorten repair cycles when a problem does occur. Waters reported USD 1.19 billion in service revenue for full-year 2025, equal to 37.5% of total company sales, and service revenue grew 7% year over year, which shows how customers continue to rely on broader support plans.[3]Waters Corporation, “Waters Corporation (NYSE: WAT) Reports Fourth Quarter and Full-Year 2025 Financial Results,” Waters Corporation Investor Relations, waters.com Waters also promotes instrument performance, analytical method, and compliance support through its service offerings, which reflect the rising value of connected and customized service structures. The laboratory equipment services market now gives a clearer advantage to providers that can combine data access, remote troubleshooting, and predictive tools across large installed bases.

Under-Reported Skill Shortage For High-End Instrument Servicing

The laboratory equipment services market is also supported by a limited supply of skilled people who can maintain advanced laboratory systems. The challenge is not limited to general laboratory staffing, because high-end platforms require hands-on experience that takes years to build and is not widely distributed across regions. The U.S. Bureau of Labor Statistics projects 13% employment growth for medical and clinical laboratory technologists and technicians over the next decade, which signals sustained pressure on the available talent pipeline. When laboratories cannot hire or retain enough qualified personnel, they tend to move more servicing responsibility outside the organization. That shift is particularly relevant for analytical instruments, where downtime risk is high and internal teams often cannot cover every service need with the required depth. The laboratory equipment services market therefore gains demand even in periods when equipment procurement cycles become uneven.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Service Contract Cost For Advanced Instruments | -1.8% | Global | Short term (≤ 2 years) |

| OEM Lock-In And Proprietary Parts Access Constraints | -1.4% | Global | Medium term (2-4 years) |

| Budget Pressure In Academic And Public Research Labs | -1.2% | North America and Europe | Medium term (2-4 years) |

| Digital Integration Risk Across Mixed-Vendor Installed Base | -0.9% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Service Contract Cost for Advanced Instruments

The laboratory equipment services market still faces resistance when advanced instruments carry high annual service costs. Service contracts for complex systems such as mass spectrometers, flow cytometers, and multi-dimensional chromatography platforms can range from USD 20,000 to USD 80,000 per instrument each year, which can consume a meaningful share of operating budgets. Smaller laboratories and mid-sized organizations often respond by narrowing coverage, delaying upgrades, or choosing time-and-material service instead of comprehensive agreements. That behavior does not remove service demand, but it can slow the adoption of full-scope contracts in cost-sensitive accounts. The restraint is strongest where procurement scale is limited and buyers cannot negotiate better pricing across a broader instrument fleet. It also pushes providers to offer more modular and outcome-linked contracts that can fit constrained budgets more effectively.

OEM Lock-In and Proprietary Parts Access Constraints

The laboratory equipment services market remains constrained by OEM control over proprietary parts, calibration tools, and diagnostic software. That control can limit how far third-party providers can go when they service newer or highly specialized systems, especially in regulated laboratories that need full traceability. The restriction does not eliminate competition, but it does narrow the practical service options for customers that run sensitive workflows. Compliance expectations around calibration records, software validation, and documented service history also make some laboratories more cautious when they consider non-OEM support structures. Independent providers are still building alternatives through refurbishment channels, software workarounds, and multi-vendor support models, but those efforts take time to scale. The laboratory equipment services market therefore keeps a structural bias toward OEMs in parts of the installed base where access barriers remain high.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Validation Demand Reshapes the Service Revenue Mix

Repair and maintenance services held 42.83% share in 2025, while Validation Services are projected to grow at 14.71% CAGR through 2031. The largest revenue contribution still comes from the simple fact that large installed bases need ongoing upkeep to remain productive and compliant. Laboratories in pharmaceutical and clinical settings cannot defer core repair activity for long because instrument availability directly affects test throughput, release timelines, and reporting commitments. Validation Services are growing faster because qualification work becomes necessary whenever an instrument is installed, moved, upgraded, or materially serviced. That makes validation an embedded requirement in regulated workflows rather than an optional extension.

The laboratory equipment services market is also seeing a more balanced mix between basic support and compliance-heavy service work within this segment group. Calibration remains a stable revenue stream because accuracy directly affects product release, test validity, and audit readiness in regulated environments. Preventive Maintenance Services are gaining steady relevance as customers shift from reactive service calls toward planned upkeep. Managed and Contract Services are expanding because many laboratories prefer a single provider that can coordinate multi-site and multi-vendor support. Training, Education, and Certification Services remain smaller, but they matter more where internal skill gaps make correct instrument use and routine upkeep harder to sustain.

By Service Provider: OEM Dominance Holds, But Structural Pressure Builds

Original equipment manufacturers held 46.38% share in 2025 and are also projected to grow at 13.32% CAGR through 2031. This position reflects their control over proprietary software, original parts, factory-trained engineers, and documentation that supports regulated servicing. The laboratory equipment services market still gives OEMs a clear advantage when customers buy new, technically complex instruments and attach service coverage at the point of sale. That pattern is especially visible in instrument categories where service access is hard to replicate without direct manufacturer authorization. It also explains why OEMs can keep growing despite the price premium that often accompanies their contracts.

The laboratory equipment services industry still leaves room for independent providers, especially where buyers need lower cost structures and mixed-fleet support. Third-party Service Providers remain relevant in mid-market accounts that value flexibility and want a single contract across several brands. Distributor-Led Service Providers hold a narrower role, but they can fill technical gaps in emerging markets and underserved locations where OEM field coverage is thinner. Legacy instrument fleets that have moved beyond active OEM support create another opening for independent service specialists. Multi-vendor managed service agreements also remain one of the clearest spaces where third parties can compete on coordination and response flexibility rather than on proprietary access alone.

By Equipment Type: Analytical Complexity Sustains Dominant Share and Growth

Analytical equipment accounted for 38.16% of the laboratory equipment services market size in 2025 and is forecast to advance at 14.59% CAGR through 2031. This segment leads because analytical systems are difficult to calibrate, heavily software-linked, and central to high-value workflows in pharmaceutical, biotech, and research laboratories. Instruments such as mass spectrometers, chromatography systems, and spectrophotometers also tend to carry higher service intensity than simpler equipment. The laboratory equipment services market, therefore, draws a larger share of spending from platforms where technical failure can quickly disrupt regulated testing or development work. Growth is reinforced by continued demand for complex research applications tied to biologics, genomics, and GLP-1-related work.

General Equipment forms a broad and stable service base because laboratories use centrifuges, incubators, and other core systems every day across many settings. Specialty Equipment is adding stronger service demand as tools such as flow cytometers and imaging systems spread into cell therapy and advanced clinical research. Support Equipment remains smaller in revenue terms, but it still requires consistent servicing because environmental monitoring and safety systems support compliant operating conditions. Analytical platforms stay ahead because the cost of downtime, the skill needed for servicing, and the dependence on software all remain higher than in most other categories. That combination helps this segment hold both the largest current position and the strongest forward growth profile.

By Contract Type: Customization Pressure Challenging Standardized Agreements

Standard service contracts held 41.63% share in 2025, while customized service contracts are projected to grow at 13.07% CAGR through 2031. Standard agreements still lead because they fit procurement norms, support budget planning, and remain easier to deploy across broad instrument fleets. The laboratory equipment services market is nonetheless shifting toward more tailored coverage because laboratories want contracts that reflect asset condition, usage levels, response expectations, and compliance needs. Buyers are showing less interest in identical annual packages when instrument complexity and operational criticality differ widely across the fleet. That is why customized structures are growing faster, even though standardized contracts remain the current base.

The change is also tied to how providers frame value. Waters offers FlexCHOICE service options that allow laboratories to tailor coverage by instrument type, service level, and contract duration, which reflects the practical move toward modular service design. Outcome-linked contracts that focus on uptime windows, service response, and performance expectations are becoming more appealing where downtime carries a high financial penalty. Smaller academic and clinical laboratories still tend to keep standard contracts because predictable pricing matters more in those settings. Larger pharmaceutical and biotechnology users are more willing to pay for customized structures when those agreements align more closely with instrument risk and workflow requirements.

By End User: Pharma Anchors Revenues, Research Institutions Accelerate

Pharmaceutical and biotechnology companies held 34.63% share in 2025, while academic and research institutions are projected to grow at 13.91% CAGR through 2031. Pharmaceutical and biotechnology users remain the largest revenue base because they operate large instrument estates under strict GMP and qualification requirements. In these environments, even short service interruptions can affect analytical development, quality control, and batch release activity. That keeps the laboratory equipment services market closely linked to the operating needs of drug development and manufacturing customers. Their service spending is also supported by the technical sophistication of the instruments they use every day.

Academic and Research Institutions are growing faster because long-cycle research infrastructure investment continues to support new installations and broader laboratory capability in several regions. Clinical and Diagnostic Laboratories remain a stable source of demand because utilization rates are high, and the accuracy depends on regular servicing and calibration. Government Research Facilities add recurring volumes through structured procurement programs, often favoring providers that can meet traceability and documentation requirements. Industrial Laboratories in food safety, environmental testing, and materials analysis create a more distributed opportunity where third-party and multi-vendor providers can compete effectively. Danaher announced a partnership with AstraZeneca in May 2025 to develop and commercialize precision medicine diagnostics, which shows the depth of collaboration large pharmaceutical customers now expect from instrumentation and service partners.

Geography Analysis

North America held 40.63% of the laboratory equipment services market share in 2025, making it the largest regional contributor. The region benefits from a dense concentration of pharmaceutical and biotechnology research campuses, strong clinical diagnostics infrastructure, and mature multi-vendor support ecosystems. The United States remains central to demand for validation, calibration, and maintenance because recurring service is closely tied to regulated manufacturing and laboratory operations. Thermo Fisher Scientific announced a USD 2 billion investment in U.S. manufacturing and laboratory services capacity in 2025, including USD 1.5 billion in capital expenditures and USD 500 million in R&D, which supports future installed-base growth and related service demand.

Europe remains a substantial part of the laboratory equipment services market because of its established pharmaceutical base, research activity, and specialized manufacturing footprint. Germany stands out as the region’s largest national laboratory services economy in the source draft, supported by a strong domestic base of analysis, biotechnology, and laboratory technology manufacturers. The United Kingdom, France, and Italy also contribute meaningfully because research intensity and regulated diagnostic activity continue to support recurring service needs. Demand across Europe is further reinforced by compliance expectations in clinical and testing environments, which keep validation and calibration activity important even when broader spending conditions become less favorable.

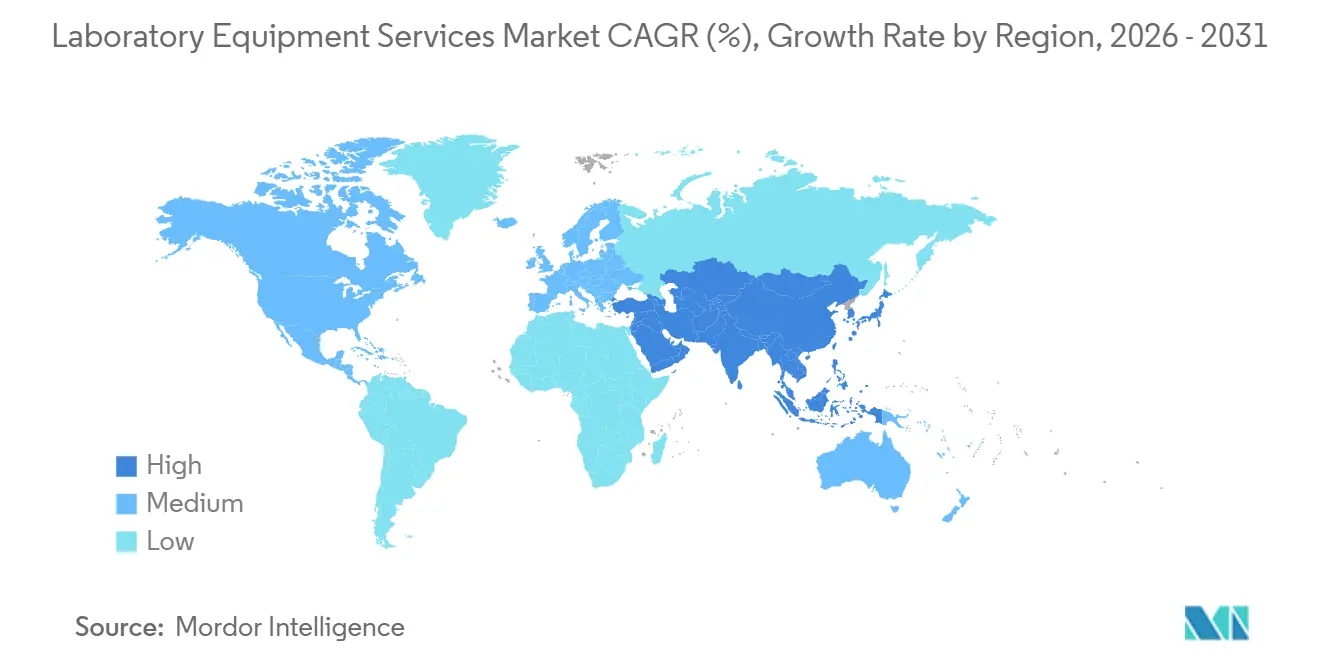

Asia-Pacific is the fastest-growing geography in the laboratory equipment services market at 12.91% CAGR through 2031. China, India, South Korea, Australia, and Japan are all adding pharmaceutical manufacturing, contract research, and diagnostics capacity that expands the regional installed instrument base. Agilent Technologies and Veeda Lifesciences launch a joint Analytical Center of Excellence in Bengaluru in May 2026, which underlines the rising sophistication of India’s bioanalytical infrastructure and the service opportunity around advanced mass spectrometry systems. The laboratory equipment services market in Asia-Pacific also benefits from the fact that many laboratories are building capability quickly and need outside support to maintain uptime and audit readiness. Middle East and Africa, along with South America, remain earlier-stage opportunities, with demand concentrated more heavily in clinical diagnostics, petrochemical quality control, and selected multinational coverage networks.

Competitive Landscape

The laboratory equipment services market shows moderate concentration, with large OEMs such as Thermo Fisher Scientific, Agilent Technologies, Danaher, and Siemens Healthineers holding strong positions in premium service categories. Their advantage comes from proprietary ecosystems that combine parts access, service documentation, software control, and factory-trained field teams. This gives them a durable edge in high-complexity instruments and in regulated settings where traceability matters as much as response time. At the same time, the laboratory equipment services market still includes a wide field of third-party specialists and multi-vendor providers that compete on flexibility, local coverage, and lower overall service cost.

Strategic moves in 2025 and 2026 show how providers are trying to deepen their role across the full instrument lifecycle. Thermo Fisher Scientific announced a USD 2 billion investment in U.S. manufacturing and laboratory services operations over four years, which signals confidence in future domestic demand and in the value of service-linked installed-base expansion. Danaher announced a precision medicine diagnostics partnership with AstraZeneca in May 2025, showing how service capabilities now sit closer to broader workflow and commercialization strategy. Agilent Technologies and Veeda Lifesciences launch a joint center in Bengaluru in 2026, which extends support around high-end analytical workflows and connects instruments more directly with development services.

Independent providers are still finding attractive openings where customers run mixed fleets and want a single service partner across brands. Multi-vendor management is especially relevant in mid-market pharmaceutical, academic, and clinical laboratories that need coordination but cannot justify full OEM coverage across every system. Technology is becoming a larger differentiator because providers that can support uptime tracking, remote diagnostics, and audit documentation can defend stronger pricing. Waters reported that service revenue grew 7% year over year in 2025, while service represented 37.5% of total company sales, which illustrates the recurring value embedded in established service platforms. The laboratory equipment services market, therefore remains competitive, but it is not evenly open because the highest-value portions still favor players with installed-base depth, proprietary access, and integrated support infrastructure.

Laboratory Equipment Services Industry Leaders

Becton, Dickinson and Company

Agilent Technologies, Inc.

Sartorius AG

Thermo Fisher Scientific Inc.

Waters Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Agilent Technologies and Veeda Lifesciences launched a joint Analytical Center of Excellence in Bengaluru, India, combining Agilent's mass spectrometry platforms with Veeda's bioanalytical and clinical research infrastructure. The collaboration targets inspection-ready analytical workflows for global biopharma sponsors navigating GLP-1 and complex biologics regulatory requirements.

- March 2026: Royston Instruments Ltd acquired a controlling stake in Biosan SIA, a Riga-based developer and manufacturer of laboratory instruments and life science solutions. The acquisition expands Royston's scientific instrumentation and service capabilities across European laboratory markets.

- January 2026: Ingersoll Rand acquired Scinomix, Inc., a provider of laboratory automation and sample management solutions, integrating it into the Life Sciences platform of its Precision and Science Technologies segment. The deal enables Ingersoll Rand to offer comprehensive end-to-end instrument solutions across laboratory environments.

- January 2026: Velaris acquired Markes International from Schauenburg International, adding Markes' thermal desorption and analytical solutions to Velaris' portfolio of laboratory automation brands. The acquisition expands Velaris' service capabilities and geographic reach across Europe and North America.

Global Laboratory Equipment Services Market Report Scope

The Laboratory Equipment Services Market encompasses the global provision of services that ensure the optimal performance, accuracy, reliability, and regulatory compliance of laboratory equipment throughout its operational lifecycle. These services include installation, repair and maintenance, calibration, validation, preventive maintenance, managed and contract services, and training programs designed to maximize equipment uptime, extend asset life, and maintain data integrity.

The Laboratory Equipment Services Market is segmented by service type, service provider, equipment type, contract type, end user, and geography. Based on service type, the market is categorized into repair and maintenance services, calibration services, validation services, preventive maintenance services, managed and contract services, and training, education, and certification services. By service provider, the market is segmented into original equipment manufacturers (OEMs), third-party service providers, and distributor-led service providers. Based on equipment type, the market comprises analytical equipment, general equipment, specialty equipment, and support equipment. By contract type, the market is divided into standard service contracts and customized service contracts. Based on end user, the market includes pharmaceutical and biotechnology companies, clinical and diagnostic laboratories, academic and research institutions, government research facilities, and industrial laboratories. Geographically, the market is analyzed across North America (the United States, Canada, and Mexico), Europe (Germany, the United Kingdom, France, Italy, Spain, and the Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, and the Rest of Asia-Pacific), the Middle East & Africa (GCC, South Africa, and the Rest of the Middle East & Africa), and South America (Brazil, Argentina, and the Rest of South America).

| Repair and Maintenance Services |

| Calibration Services |

| Validation Services |

| Preventive Maintenance Services |

| Managed and Contract Services |

| Training, Education, and Certification Services |

| Original Equipment Manufacturers |

| Third-Party Service Providers |

| Distributor-Led Service Providers |

| Analytical Equipment |

| General Equipment |

| Specialty Equipment |

| Support Equipment |

| Standard Service Contract |

| Customized Service Contract |

| Pharmaceutical and Biotechnology Companies |

| Clinical and Diagnostic Laboratories |

| Academic and Research Institutions |

| Government Research Facilities |

| Industrial Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Repair and Maintenance Services | |

| Calibration Services | ||

| Validation Services | ||

| Preventive Maintenance Services | ||

| Managed and Contract Services | ||

| Training, Education, and Certification Services | ||

| By Service Provider | Original Equipment Manufacturers | |

| Third-Party Service Providers | ||

| Distributor-Led Service Providers | ||

| By Equipment Type | Analytical Equipment | |

| General Equipment | ||

| Specialty Equipment | ||

| Support Equipment | ||

| By Contract Type | Standard Service Contract | |

| Customized Service Contract | ||

| By End User | Pharmaceutical and Biotechnology Companies | |

| Clinical and Diagnostic Laboratories | ||

| Academic and Research Institutions | ||

| Government Research Facilities | ||

| Industrial Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in laboratory equipment services through 2031?

Growth is tied to rising instrument complexity, stronger uptime needs, expanding regulated workflows, and more outsourcing of specialized maintenance. The sector is projected to reach USD 45.45 billion by 2031 from USD 25.04 billion in 2026 at a 12.67% CAGR.

Which service category leads revenue and which grows the fastest?

Repair and maintenance services led with 42.83% share in 2025, while validation services are projected to grow the fastest at 14.71% CAGR through 2031.

Why do OEMs hold the largest provider position?

OEMs held 46.38% share in 2025 because they control proprietary parts, service software, and compliance documentation, all of which matter in high-complexity and regulated laboratory environments.

Which equipment category creates the strongest service opportunity?

Analytical equipment is the strongest category because it held 38.16% share in 2025 and is projected to grow at 14.59% CAGR, supported by high calibration sensitivity and software-intensive operation.

Which region is most important for current demand and which region is expanding the fastest?

North America held the largest share at 40.63% in 2025, while Asia-Pacific is projected to grow the fastest at 12.91% CAGR through 2031 as pharmaceutical, diagnostics, and research capacity expands.

Page last updated on: