Laboratory And Bioanalytical Contract Research Organization (CRO) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

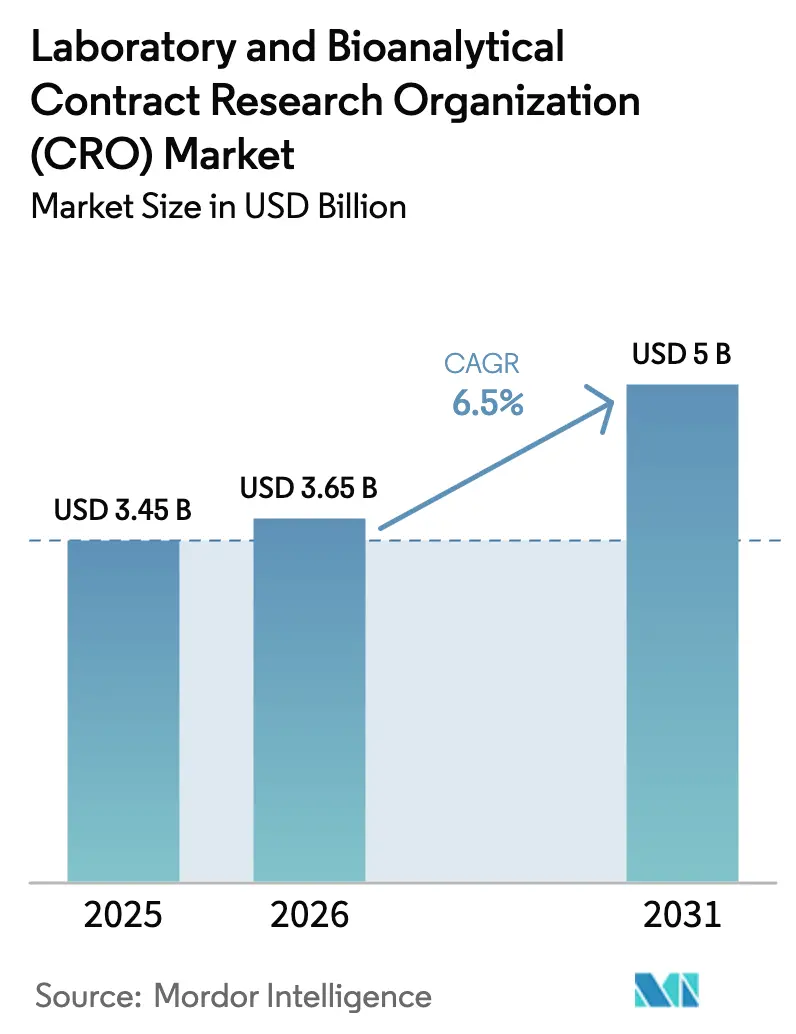

| Market Size (2026) | USD 3.65 Billion |

| Market Size (2031) | USD 5 Billion |

| Growth Rate (2026 - 2031) | 6.50% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laboratory And Bioanalytical Contract Research Organization (CRO) Market Analysis by Mordor Intelligence

The Laboratory And Bioanalytical Contract Research Organization Market size is projected to be USD 3.45 billion in 2025, USD 3.65 billion in 2026, and reach USD 5 billion by 2031, growing at a CAGR of 6.5% from 2026 to 2031.

Sponsors are steering budgets toward specialized partners that combine GLP-compliant toxicology, high-resolution bioanalysis, and AI-enabled informatics, thereby compressing internal fixed costs and accelerating filing timelines. The FDA Modernization Act 2.0 has lifted statutory animal-testing mandates, expanding demand for organ-on-chip and computational toxicology, while the June 2024 draft guidance on biosimilar interchangeability is shifting evidentiary focus toward immunogenicity assays and pharmacokinetic comparability data. North American CROs retain advantages in regulatory proximity, yet geopolitical uncertainty tied to the proposed BIOSECURE Act is encouraging sponsors to diversify vendors across Europe and India [1]Reuters, “U.S. House Advances BIOSECURE Act Targeting China-Based Biotech Firms,” reuters.com. Layered onto these structural factors is a pronounced talent squeeze for LC-MS/MS specialists, which is widening pricing power for providers that can combine automation with deep scientific benches and pristine audit trails.

Key Report Takeaways

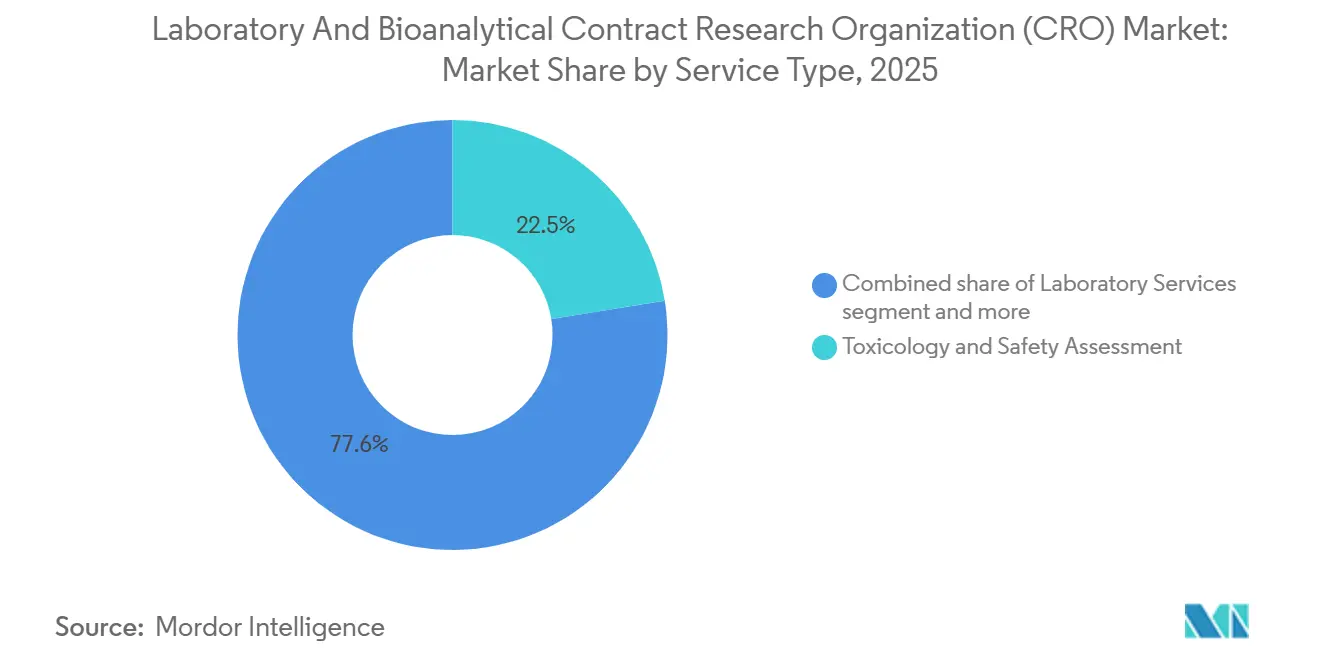

- By service type, toxicology and safety assessment held 22.45% of laboratory & bioanalytical CRO market share in 2025, whereas bioanalytical testing is forecast to grow at a 7.00% CAGR through 2031.

- By clinical phase, Phase III work captured 55% of sponsor outlays in 2025, while Phase I spending is advancing at a 6.89% CAGR to 2031.

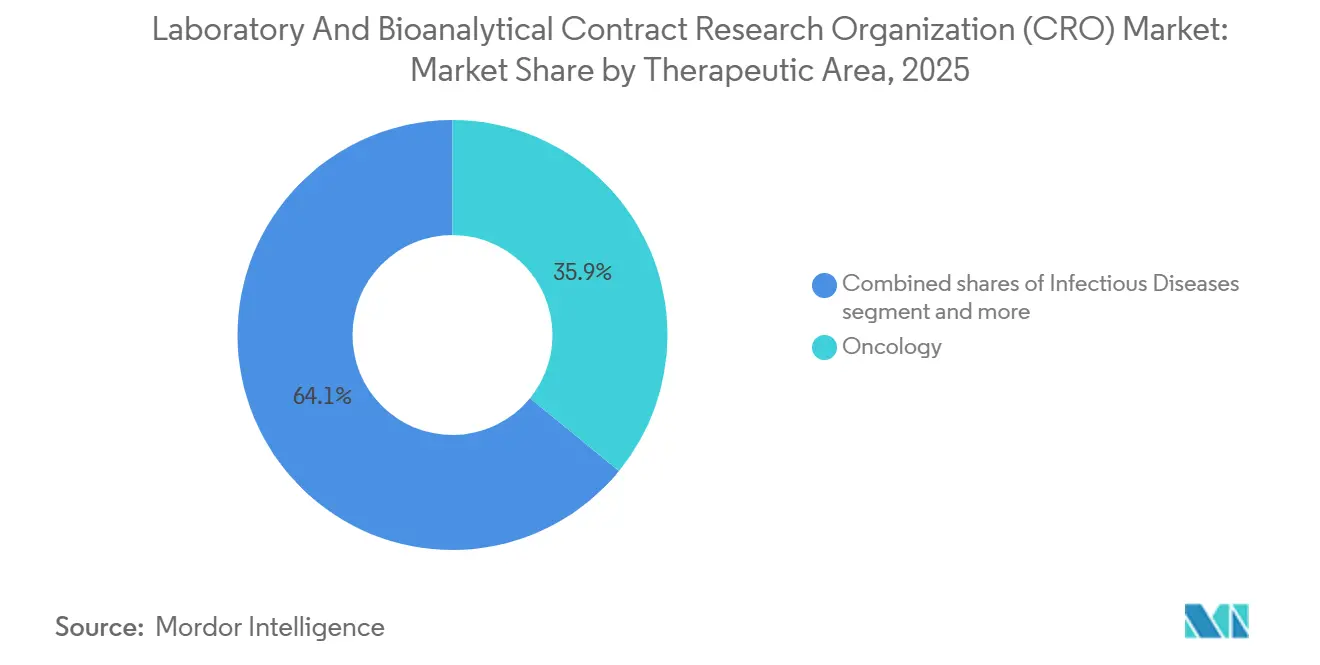

- By therapeutic area, oncology commanded 35.89% revenue share in 2025; infectious-disease programs are projected to post the fastest 7.02% CAGR through 2031.

- By sponsor cohort, large-pharma clients controlled 55.34% of the laboratory & bioanalytical CRO market size in 2025, but medical-device and combination-product developers are expanding at a 7.12% CAGR.

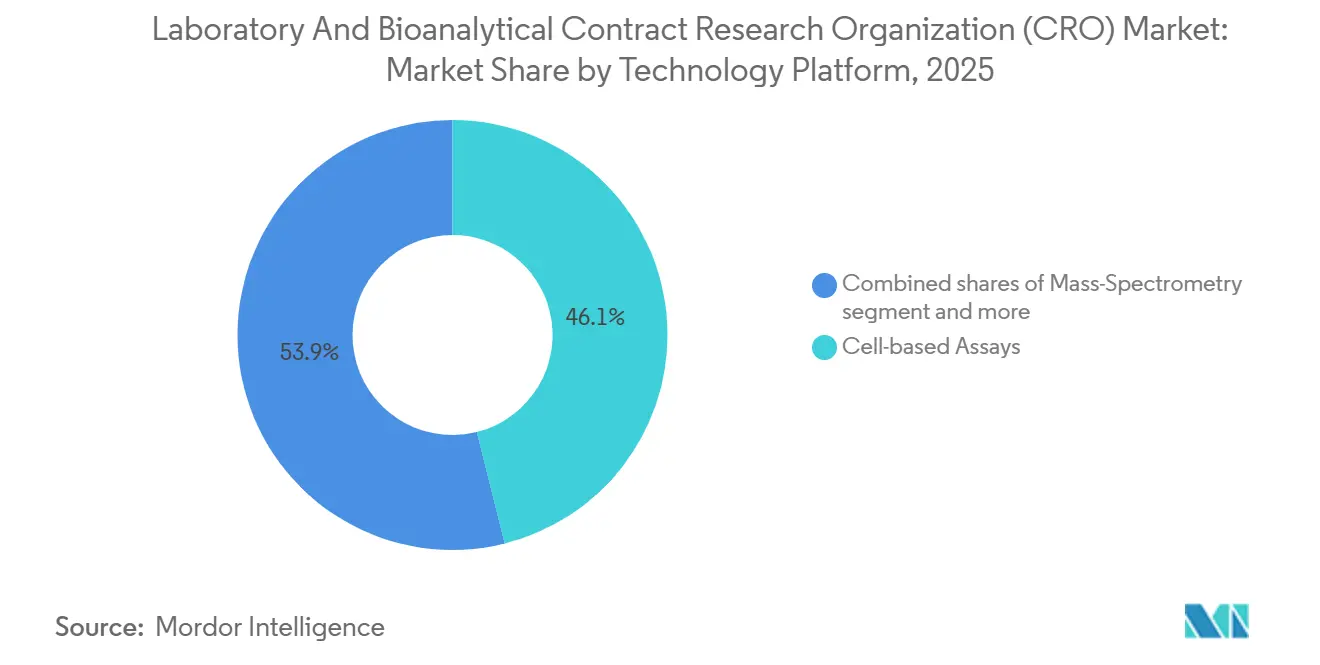

- By technology, cell-based assays generated 46.1% of 2025 revenue, whereas mass-spectrometry platforms are set to grow at a 7.23% CAGR to 2031.

- North America held 44.56% of 2025 revenue, yet Asia-Pacific is positioned for the fastest 7.50% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Laboratory And Bioanalytical Contract Research Organization (CRO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Complexity of Biologics | +1.2% | Global, concentrated in North America and EU | Long term (≥ 4 years) |

| Increasing R&D Outsourcing to Reduce Time & Cost | +1.5% | Global, strongest in North America and Asia-Pacific | Medium term (2–4 years) |

| Regulatory Stringency for GLP/GCP Compliance | +0.9% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Expansion of Cell & Gene Therapy Pipelines | +1.3% | North America & EU core, early APAC adoption | Medium term (2–4 years) |

| AI-Enabled Bioinformatics Creating New Service Lines | +0.8% | North America & EU, selective APAC hubs | Short term (≤ 2 years) |

| Biosimilar Interchangeability Studies Post-2025 | +0.7% | Global, led by North America & EU regulatory clarity | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Complexity of Biologics

Monoclonal antibodies, bispecific constructs, and antibody-drug conjugates now dominate oncology and immunology pipelines, each demanding multi-species toxicology, intricate immunogenicity profiling, and high-sensitivity PK assays that exceed small-molecule requirements. Sponsors spent an average of USD 8 million per biologic for preclinical safety in 2024, nearly double small-molecule outlays, thereby favoring CROs with in-house primate colonies and sub-nanogram analytical capabilities. EMA’s ICH S6(R1) enforces rigorous species-selection justification, propelling providers to invest in translational scientists and specialized vivaria that smaller labs cannot afford. ADC programs further amplify workload because antibody, linker, and payload must each meet standalone validation, tripling assay volumes and forging durable client relationships with CROs that can manage the full stack.

Increasing R&D Outsourcing to Reduce Time & Cost

Early-stage biotech firms typically operate with 18- to 24-month funding runways, outsourcing up to 80% of preclinical studies to preserve capital for clinical milestones [2]Biotechnology Innovation Organization, “BIO Industry Survey 2025,” bio.org. The 2025 BIO survey recorded a 22% reduction in headcount for internal preclinical teams, with budgets shifted toward milestone-based CRO contracts that align cash burn with value inflection points. Large pharmas are also rationalizing vendor lists; Pfizer and Novartis each trimmed preclinical CRO rosters by about 30% between 2023 and 2025, consolidating volume under master service agreements that lock in capacity and harmonize data formats. This trend enlarges average contract values for top-tier providers but squeezes mid-tier generalists, reinforcing the importance of differentiated scientific talent and global site networks. Outsourcing penetration is projected to remain above 65% across the laboratory & bioanalytical CRO market through 2031 as virtual R&D operating models become the norm

Regulatory Stringency for GLP/GCP Compliance

The FDA conducted 412 GLP inspections in fiscal 2024, issuing 37 warning letters, up 12% from 2023, mostly tied to data-integrity lapses and inadequate audit trails [3]U.S. Food and Drug Administration, “Good Laboratory Practice Program,” fda.gov. Sponsors now require dual North American and European certifications and blockchain-ready LIMS platforms as table-stakes for vendor selection. Typical compliance upgrades cost USD 2 million to USD 5 million per site, escalating capital intensity and deterring new entrants. Japan’s PMDA has joined the enforcement wave with unannounced inspections targeting CROs that support IND filings, while the EMA demands mutual-acceptance documents for every non-clinical module. The tightening net around electronic-record reliability creates a premium for providers that maintain robust QA teams and cultivate transparent dialogue with regulators.

Expansion of Cell & Gene Therapy Pipelines

The FDA has cleared more than 30 cell and gene therapies and projects 10-20 new approvals annually through 2027, each requiring biodistribution, immunotoxicity, and tumorigenicity assessments that differ markedly from standard safety packages. CAR-T and CRISPR-based programs obligate CRO expertise in flow cytometry, next-generation sequencing, and lengthy primate studies to monitor delayed adverse events. January 2024 CMC guidance emphasized robust preclinical comparability data when manufacturing scales up, channeling more work to laboratories that can execute cross-batch analytics with regulatory rigor. Bluebird Bio and CRISPR Therapeutics each spent over USD 50 million on preclinical activities in 2024, illustrating the capital intensity that favors CROs equipped with high-end instrumentation and dedicated ATMP talent pools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cap-ex for Cutting-Edge Instrumentation | -0.5% | Global, most acute in emerging APAC markets | Medium term (2–4 years) |

| Compliance Risk & Penalty Exposure | -0.3% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Shortage of Skilled Bioanalytical Scientists | -0.4% | Global, most severe in North America & EU | Long term (≥ 4 years) |

| Data-Integrity Breaches in Cloud-Based Labs | -0.2% | Global, concentrated in digitally advanced markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cap-ex for Cutting-Edge Instrumentation

Thermo Fisher’s Orbitrap Astral lists above USD 1 million, and premium LC-MS/MS benches regularly exceed USD 600,000 per unit, straining mid-tier CRO balance sheets. Waters’ 2024 annual filing showed 14% sales growth to contract labs but a 9% cancellation spike as smaller providers deferred purchases amid tighter credit. Automated liquid-handling robots and high-resolution sequencing gear add further costs, creating a two-tier environment where top-decile CROs amortize instruments across larger client rosters while boutique entrants retreat to less capital-intensive safety assays. Equipment-as-a-service models exist, yet sponsors often question data-quality consistency when critical runs occur on leased platforms.

Compliance Risk & Penalty Exposure

Warning-letter frequency climbed in 2024, and several CROs underwent for-cause inspections that halted sponsor studies until corrective actions were verified. Financial penalties can top USD 0.5 million per citation and, more importantly, trigger sponsor audits that divert billable lab capacity. Providers with decentralized data centers face heightened cybersecurity scrutiny, because any unauthorized manipulation of electronic study records threatens regulatory acceptance across global submissions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Bioanalytical Testing Gains Share as Precision Medicine Expands

Bioanalytical testing accounted for 7.00% CAGR growth prospect to 2031, eclipsing the flat trajectory of routine in-vitro assays as sponsors seek ultra-sensitive quantification of biomarkers in CSF, tumor interstitial fluid, and circulating exosomes. Toxicology and safety assessment retained 22.45% of 2025 laboratory & bioanalytical CRO market share, thanks to enduring GLP requirements, but faces gradual commoditization pressures. Labcorp’s biomarker-services line grew 11% in 2024 on the back of oncology and CNS projects that require multiplex immunoassays and gene-expression readouts. CROs differentiating through AI-driven in-silico toxicity screening now secure higher utilization of premium LC-MS/MS suites, boosting margin despite rising wage costs.

Continued method-validation tightening, exemplified by the FDA’s 2024 update mandating incurred-sample reanalysis, has elevated barriers for start-ups lacking robust QA teams. Consequently, share is migrating toward providers that can guarantee reproducibility across global clone sites. Charles River’s USD 875 million acquisition of Cognate BioServices in 2023 bolstered its cell-based potency-assay capabilities and illustrates how M&A is used to plug capability gaps quickly. These dynamics underpin a forecast in which the bioanalytical slice of the laboratory & bioanalytical CRO market size expands from 2026 through 2031, while standalone chemistry and routine safety pharmacology units grow below the headline CAGR.

By Clinical Phase: Phase I Accelerates as Biotech Front-Loads Risk

Phase III services consumed 55% of 2025 budgets because sponsors must validate pivotal safety endpoints, yet Phase I demand will grow faster at 6.89% CAGR as biotech investors weigh early safety clarity heavily in Series B term sheets. The FDA’s Project Optimus initiative obliges dose-optimization studies earlier in development, expanding pharmacology and PK modeling scopes within Phase I packages. Sponsors increasingly bundle IND-enabling toxicology with first-in-human dosing through single-provider contracts to avoid data-transfer entropy between organizations, a trend that benefits CROs owning both GLP labs and clinical pharmacology units.

Adaptive-design philosophies blur boundaries: seamless Phase I/II protocols reuse preclinical biomarker data to refine patient stratification in real time. However, the FDA Modernization Act 2.0’s allowance of validated alternative models trims some animal-testing needs within the preclinical module. Over the horizon, Phase IV commitments—especially for gene therapies will expand as regulators mandate long-term follow-up, preserving a solid revenue stream for safety specialists with pharmacovigilance extensions. Overall, diversified providers capable of spanning preclinical through Phase IIa stand to capture larger chunks of the laboratory & bioanalytical CRO market.

By Therapeutic Area: Infectious Diseases Surges on Pandemic Preparedness

Oncology maintained 35.89% of 2025 spend as ADCs, CAR-T products, and checkpoint inhibitors dominate pipelines, yet infectious-disease investments will outpace other segments at 7.02% CAGR through 2031 amid heightened pandemic vigilance. BARDA allocated USD 1.2 billion in 2024 to antiviral and vaccine preclinical projects, channeling work to CROs with BSL-3/4 suites. Immunology and inflammation candidates continue to attract venture funding thanks to validated in-vivo models that predict human efficacy, positioning CROs with autoimmune assay benches for steady growth.

Cardiovascular and metabolic pipelines are skewing toward obesity and NASH, which require metabolism cages, telemetry, and lipidomics workflows that few CROs possess at scale. CNS remains constrained by model complexity and blood-brain-barrier challenges, limiting competition to providers with specialized neurobehavioral units. Orphan-disease projects, supported by 16 FDA approvals in 2024, increase demand for bespoke transgenic models and patient-derived cell lines. In aggregate, therapeutic diversity supports balanced capacity utilization across large and mid-sized CRO portfolios.

By Sponsor Type: Medical-Device Hybrids Drive Growth

Large pharma companies owned 55.34% of 2025 revenue, yet device-combination sponsors show the strongest 7.12% CAGR as ISO 10993 alignment smooths regulatory pathways. Biotech and specialty-pharma players push outsourcing penetration above 75% of preclinical spend, relying on milestone payment schedules to conserve cash. Academic and government entities, supported by an 8% NIH budget increase in 2024, are funding translational proof-of-concept studies that often migrate to commercial partners once efficacy signals emerge.

Combination inhalers, drug-eluting stents, and prefilled-syringe biologics require integrated toxicology and materials-science evaluations that favor CROs with cross-disciplinary benches. Abbott and Medtronic both reported >20% increases in outsourced preclinical work on combination products in 2024, confirming the opportunity pool. Meanwhile, large-pharma vendor rationalization is eliminating dozens of duplicate CRO relationships, pressuring mid-tier providers without unique niches but simultaneously freeing budget for boutiques with differentiated assays. This bifurcation shapes competitive dynamics across the laboratory & bioanalytical CRO industry.

By Technology Platform: Mass Spectrometry Leads Innovation

Cell-based assays generated 46.1% of 2025 revenue because CAR-T potency, 3D organoid efficacy, and gene-editing off-target evaluations necessitate biologically relevant in-vitro systems. However, mass spectrometry is slated for 7.23% CAGR thanks to unrivaled quantitative sensitivity and expanding regulatory reliance on metabolite ID data. High-resolution Orbitrap instruments are indispensable for untargeted lipidomics that uncover unforeseen safety liabilities, while triple-quadrupole LC-MS/MS remains the gold standard for trace-level quantification of peptides and small molecules.

Immunoassays remain essential for immunogenicity screens, but ultra-sensitive platforms such as Quanterix Simoa are pushing detection into femtogram ranges, albeit at elevated per-sample costs. NGS adoption is rising fastest in oncology and gene-therapy, where vector-integration and tumor-mutation signatures inform clinical trial design. Bioinformatics platforms that predict toxicology in silico now form a standalone service line: providers licensing AI engines like Schrödinger’s FEP+ compress medicinal-chemistry cycles and secure premium rates. Overall, technology stack breadth is becoming a major determinant of laboratory & bioanalytical CRO market competitiveness.

Geography Analysis

North America captured 44.56% of 2025 revenue, anchored by FDA proximity, dense GLP infrastructure, and a domestic R&D outlay that represents roughly 60% of global pharma spend. Sponsors value same-zone regulatory interactions and the ability to conduct site audits without trans-Pacific travel, keeping pricing power strong. Nevertheless, the laboratory & bioanalytical CRO market is experiencing a geographic rebalancing as Asia-Pacific logs a 7.50% CAGR through 2031. State-subsidized bioparks in China and India offer 30%-40% cost savings while achieving OECD GLP mutual-acceptance, luring projects that do not rely on real-time FDA feedback. Yet the BIOSECURE Act’s potential constraints on U.S. federal contracts with certain China-based CROs prompt risk-averse sponsors to distribute work to Indian, Singaporean, or Vietnamese facilities that pair cost advantages with geopolitical neutrality.

Asia-Pacific’s ascent is underpinned by both export work and indigenous pipelines; China’s 14th Five-Year Plan earmarked USD 10 billion for biopharma infrastructure, and Syngene’s USD 50 million Bangalore expansion in 2024 doubled vivarium capacity to serve U.S. and EU biotechs. Sponsors remain vigilant about IP security, favoring providers with international ISO 27001 certification and transparent audit histories. Over the forecast horizon, regional diversification rather than wholesale relocation will characterize capacity allocation, sustaining a multi-hub structure across the laboratory & bioanalytical CRO market.

Competitive Landscape

Moderate consolidation defines the laboratory & bioanalytical CRO market: the top five players—Charles River Laboratories, Labcorp Drug Development, Eurofins Scientific, WuXi AppTec, and ICON plc jointly control the majority of global revenue. Large sponsors award multi-year master-service agreements to these incumbents to guarantee capacity, harmonize QA, and negotiate favorable pricing, yet boutique specialists thrive in high-barrier niches such as large-molecule immunogenicity (BioAgilytix) or DMPK modeling (Frontage). Technology investment is a core differentiator; providers deploying automated liquid-handling and AI bioinformatics command price premiums, offsetting wage inflation and sustaining gross margins.

Geopolitical currents are redrawing the competitive chessboard. WuXi AppTec’s exposure to the BIOSECURE Act is prompting some U.S. biotech clients to hedge with European or Indian vendors, creating openings for Eurofins, Syngene, and Pharmaron’s non-China sites. Data integrity scandals remain a potent reputational hazard; the FDA issued multiple warning letters in 2024 for audit-trail gaps, steering cautious sponsors toward providers with hardened cybersecurity and blockchain-based LIMS. Talent scarcity also shapes rivalry: CROs funding of in-house academies secures throughput advantages that translate into faster turnaround times and higher client retention.

Emergent disruptors include AI-native players such as Recursion and Exscientia, which license phenomics and quantum-powered chemistry engines to established CROs, embedding digital insights into wet-lab workflows. M&A will continue as incumbents buy niche capabilities—Charles River’s 2023 Cognate acquisition illustrates the premium placed on cell-therapy potency testing. Overall, competitive intensity is forecast to rise, but scale economies, compliance capital, and tech differentiation will sustain entry barriers across the laboratory & bioanalytical CRO industry.

Laboratory And Bioanalytical Contract Research Organization (CRO) Industry Leaders

Charles River Laboratories

Labcorp Holdings Inc

Eurofins Scientific

WuXi AppTec

ICON plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: ICON plc expanded oncology research within its Accellacare Site Network by opening the Brian Moran Cancer Institute at Duly Health and Care in Illinois

- December 2025: Thermo Fisher Scientific opened a Bioprocess Design Center in Hyderabad and expanded Korean and Singaporean sites to meet regional biologics demand.

- September 2025: Parexel partnered with Weave Bio to integrate AI-native regulatory-automation tools, aiming to shorten regulatory-submission timelines.

Global Laboratory And Bioanalytical Contract Research Organization (CRO) Market Report Scope

As per the scope of the report, A Laboratory and Bioanalytical Contract Research Organization (CRO) is a specialized scientific partner that provides high-level analytical support to the pharmaceutical, biotechnology, and medical device industries. Unlike full-service clinical CROs that manage patient logistics, bioanalytical CROs focus specifically on the quantitative and qualitative measurement of drugs, their metabolites, and biomarkers within biological matrices like blood, urine, or tissue. These organizations are critical throughout the drug development lifecycle, particularly in the preclinical and early clinical stages, where they conduct essential pharmacokinetic (PK), pharmacodynamic (PD), and toxicokinetic (TK) studies.

The laboratory & bioanalytical contract research organization (CRO) market is segmented by service type, phase, therapeutic area, sponsor type, technology platform, and geography. By service type, the market is categorized into laboratory services, bioanalytical testing, toxicology & safety assessment, and other specialized services. By phase, the market is divided into pre-clinical, phase I, phase II, phase III, and phase IV / post-marketing. By therapeutic area, it is segmented into oncology, infectious diseases, immunology & inflammation, cardiovascular & metabolic, CNS disorders, and others. By sponsor type, the segmentation includes large pharma, biotech & specialty pharma, medical-device / combination, academic & government. By technology platform, mass-spectrometry, cell-based assays, immunoassays, next-generation sequencing, and bioinformatics & AI platforms. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Laboratory Services |

| Bioanalytical Testing |

| Toxicology & Safety Assessment |

| Other Specialized Services |

| Pre-clinical |

| Phase I |

| Phase II |

| Phase III |

| Phase IV / Post-marketing |

| Oncology |

| Infectious Diseases |

| Immunology & Inflammation |

| Cardiovascular & Metabolic |

| CNS Disorders |

| Other Therapeutic Areas |

| Large Pharma |

| Biotech & Specialty Pharma |

| Medical-Device / Combination |

| Academic & Government |

| Mass-Spectrometry (LC-MS/MS, HR-MS) |

| Cell-based Assays |

| Immunoassays (ELISA, ECL) |

| Next-Generation Sequencing |

| Bioinformatics & AI Platforms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Laboratory Services | |

| Bioanalytical Testing | ||

| Toxicology & Safety Assessment | ||

| Other Specialized Services | ||

| By Phase | Pre-clinical | |

| Phase I | ||

| Phase II | ||

| Phase III | ||

| Phase IV / Post-marketing | ||

| By Therapeutic Area | Oncology | |

| Infectious Diseases | ||

| Immunology & Inflammation | ||

| Cardiovascular & Metabolic | ||

| CNS Disorders | ||

| Other Therapeutic Areas | ||

| By Sponsor Type | Large Pharma | |

| Biotech & Specialty Pharma | ||

| Medical-Device / Combination | ||

| Academic & Government | ||

| By Technology Platform | Mass-Spectrometry (LC-MS/MS, HR-MS) | |

| Cell-based Assays | ||

| Immunoassays (ELISA, ECL) | ||

| Next-Generation Sequencing | ||

| Bioinformatics & AI Platforms | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the laboratory & bioanalytical CRO market be in 2031?

Forecasts indicate the laboratory & bioanalytical CRO market size will reach USD 5 billion by 2031, up from USD 3.65 billion in 2026 at a 6.50% CAGR.

Which service line is expanding fastest?

Bioanalytical testing is set to grow at 7.00% CAGR through 2031 owing to precision-medicine pipelines that need ultra-sensitive pharmacokinetic and biomarker assays.

Where is regional growth strongest?

Asia-Pacific is projected to post a 7.50% CAGR, driven by cost-competitive GLP sites in China and India and state investments in biopharma infrastructure.

What regulatory shift is most influential after 2024?

The FDA’s draft guidance on biosimilar interchangeability lowers switching-study burdens, directing more spend to immunogenicity and PK analytics

What are the top barriers for new CRO entrants?

High capital outlays for mass-spectrometry and automation gear, strict data-integrity compliance, and scarcity of skilled LC-MS/MS scientists deter new competitors

Page last updated on: