Label Printing Machine Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

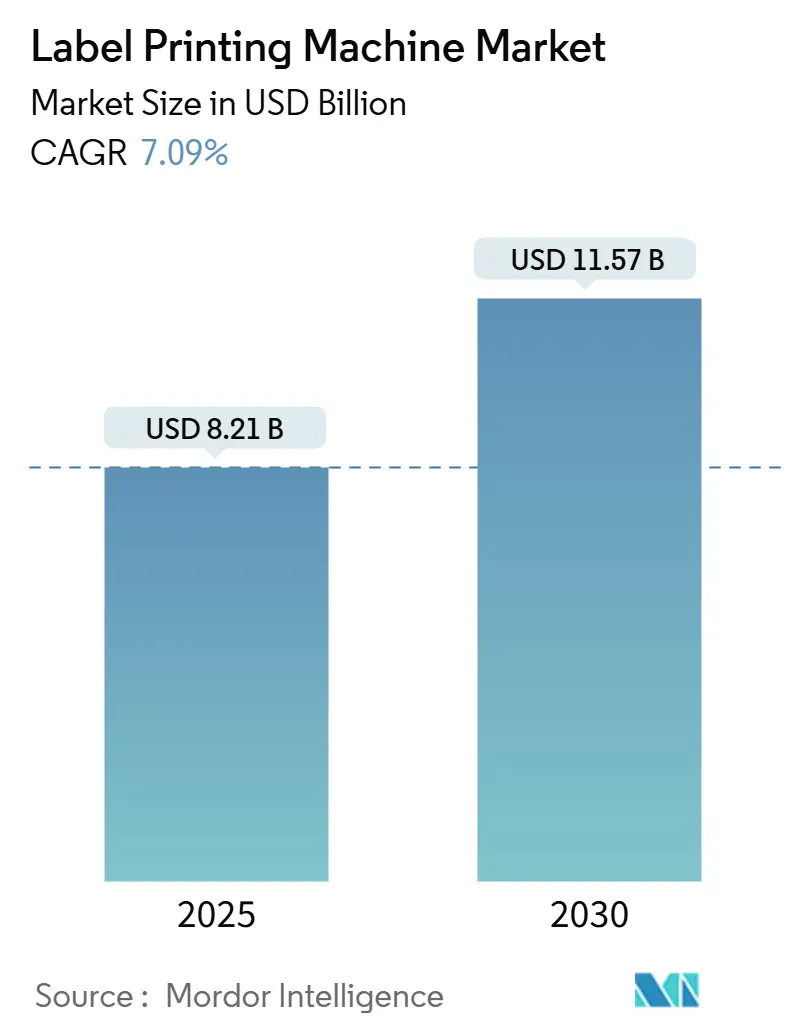

| Market Size (2025) | USD 8.21 Billion |

| Market Size (2030) | USD 11.57 Billion |

| Growth Rate (2025 - 2030) | 7.09% CAGR |

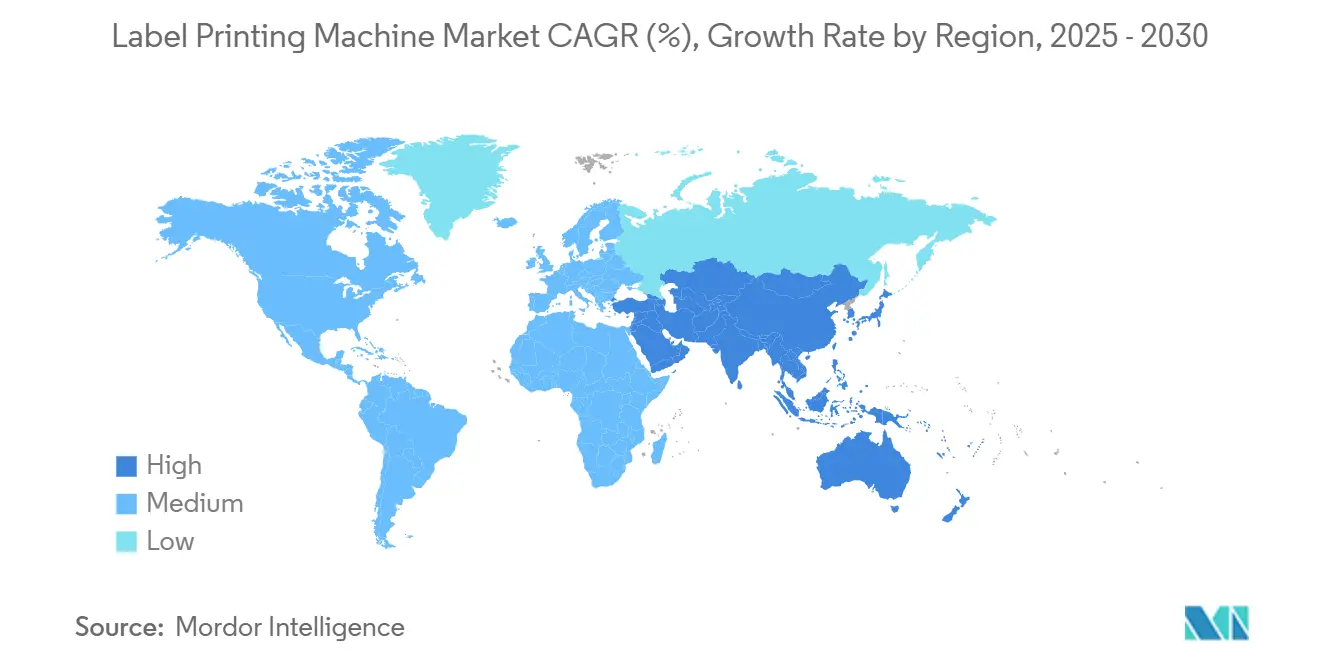

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

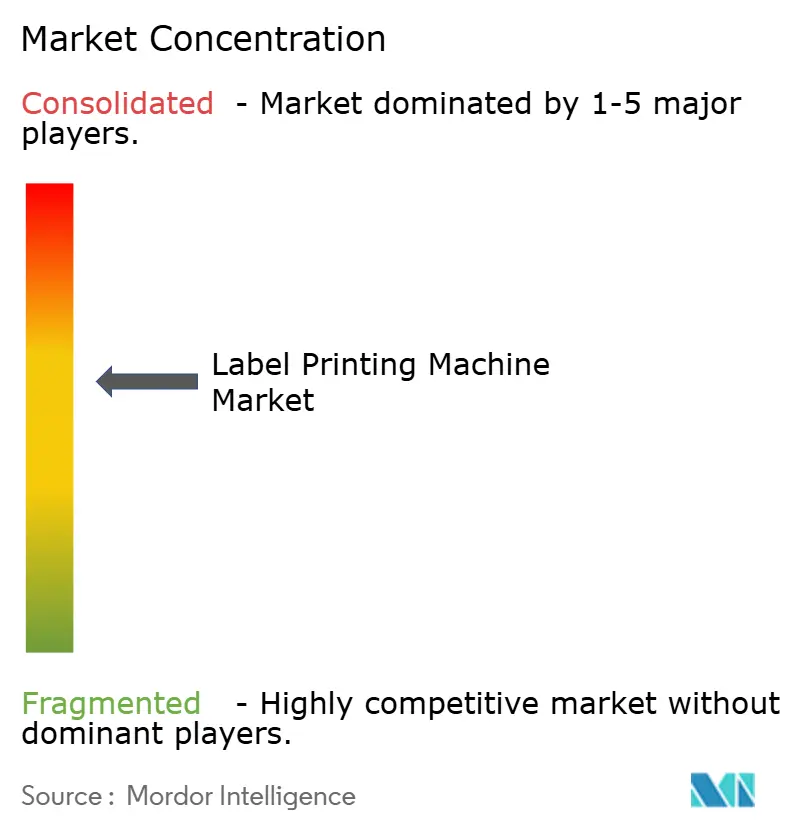

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Label Printing Machine Market Analysis by Mordor Intelligence

The label printing machine market size is estimated at USD 8.21 billion in 2025 and is projected to reach USD 11.57 billion by 2030, growing at a 7.09% CAGR. Ongoing pharmaceutical serialization mandates, fast-moving consumer goods (FMCG) automation, and the rise of craft beverage brands that demand short-run, variable graphics are lifting equipment demand. The United States Drug Supply Chain Security Act now requires unit-level serialization, prompting converters to adopt digital and hybrid presses that can print variable data and verify codes in-line. In parallel, the European Union's Packaging and Packaging Waste Regulation requires 70% recyclability and 30% recycled polyethylene terephthalate content in food-contact packaging by January 2030, prompting rapid reformulation of materials and inks. Energy-efficient UV-LED inks that eliminate the need for mercury lamps, along with inline finishing modules that consolidate die-cutting and inspection, further reinforce capital spending. North American craft breweries and Asia-Pacific cosmetics startups increasingly rely on short-setup digital presses to support frequent stock-keeping unit (SKU) changes, accelerating the shift from plate-based flexography to agile hybrid platforms.

Key Report Takeaways

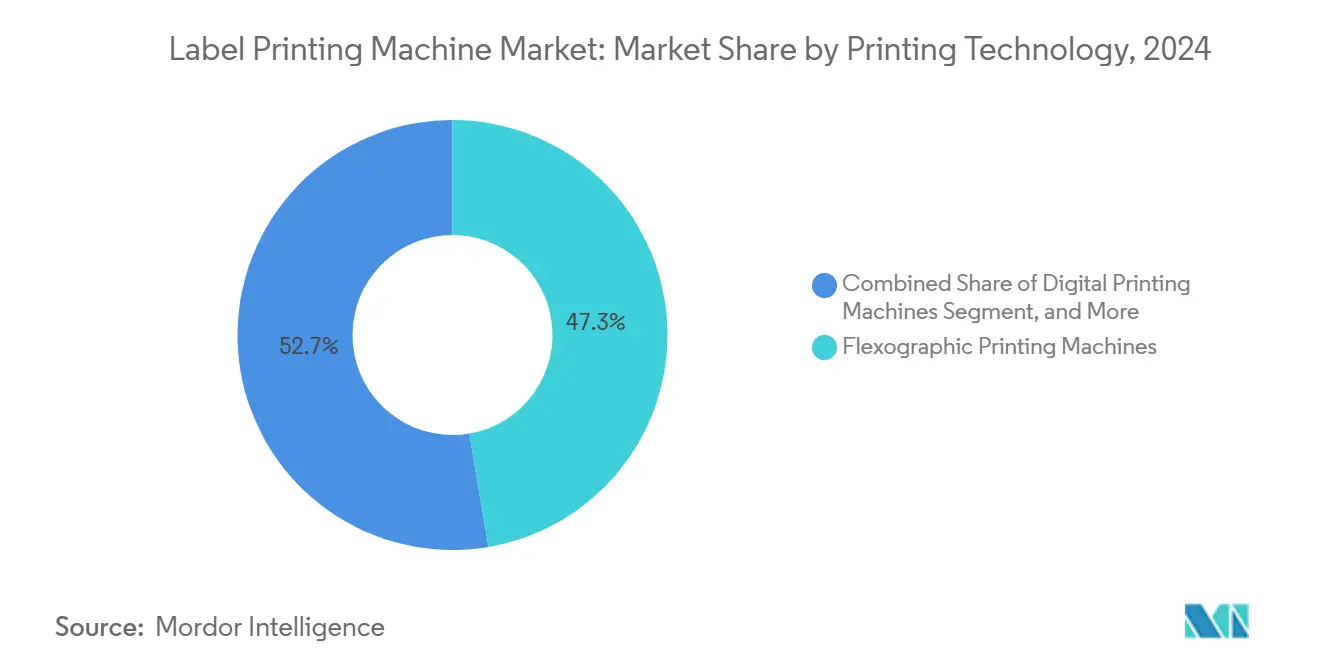

- By printing technology, flexographic presses captured 47.32% of the label printing machine market share in 2024.

- By product type, the label printing machine market size for inline systems is projected to grow at a 9.56% CAGR between 2025–2030.

- By ink type, UV-curable formulations captured 44.74% of the label printing machine market share in 2024.

- By application, the label printing machine market size for cosmetics and personal care is projected to grow at a 9.25% CAGR between 2025–2030.

- By substrate, paper captured 37.15% of the label printing machine market share in 2024.

- By geography, the label printing machine market size for Asia-Pacific is projected to grow at a 9.93% CAGR between 2025–2030.

Global Label Printing Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Transformation of FMCG Packaging Lines | +1.8% | Global with focus on North America and Europe | Medium term (2–4 years) |

| Shrinking Print Runs Demanding Short-Setup Technologies | +1.5% | Global, most visible in Asia-Pacific craft beverage and cosmetics sectors | Short term (≤ 2 years) |

| Regulatory Push Toward Smart and Functional Labels | +1.6% | North America and Europe with spillover to Asia-Pacific pharmaceutical hubs | Medium term (2–4 years) |

| Shift to Sustainable Water-Based and UV-LED Inks | +1.2% | Europe and North America | Long term (≥ 4 years) |

| Expansion of Craft Beverage and Boutique Brands | +0.7% | North America, Europe, emerging Asia-Pacific urban centers | Short term (≤ 2 years) |

| Integration of Inline Finishing and Inspection Systems | +0.9% | Global, early adoption in pharmaceuticals and cosmetics | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Regulatory Push Toward Smart and Functional Labels

Serialization rules in the United States and Europe require that every prescription drug package carry unique identifiers. Digital and hybrid presses print two-dimensional barcodes and alphanumeric serials at line speed without plates, then verify every code with inline cameras. Domino’s N730i module integrates a 1,200-dpi engine with R-Scan verification, so converters avoid separate inspection steps. Pharmaceutical converters capture premium pricing for compliance; however, small industrial label shops often lack the capital and talent to deploy similar systems, thereby widening profit gaps across converter tiers.

Digital Transformation of FMCG Packaging Lines

FMCG firms embed presses directly on packaging lines to remove pre-printed inventory and enable same-day artwork changeovers. Canon’s LabelStream 4000 runs at 75 m/min with Pantone-certified output, supporting daily regional promotions.[1]Canon Inc., “LabelStream Product Line,” Canon.com Inline placement reduces working capital tied up in obsolete labels, but it also magnifies downtime risk, prompting vendors to issue four-hour service guarantees that strain field networks. Chinese entrants offering lower-priced digital units add pricing pressure, accelerating commoditization at the entry tier.

Shrinking Print Runs Demanding Short-Setup Technologies

Average print runs decreased from 10,000 linear meters in 2019 to fewer than 5,000 linear meters in 2024, as craft breweries and e-commerce brands prefer limited batches. The Brewers Association notes that craft beer revenue growth is expected to exceed 8% through 2030, with many breweries ordering only 500 labels per SKU. Xeikon’s PX3300HD delivers plate-equivalent quality on uncoated paper, making same-day digital output viable for premium wines and seasonal beers. Flexographic suppliers are facing declining sales of plates and rollers, prompting them to launch hybrid presses that retain some analog stations while incorporating inkjet heads.

Shift to Sustainable Water-Based and UV-LED Inks

European volatile organic compound limits and extended producer responsibility rules push converters to adopt low-emission chemistries. UV-LED arrays reduce energy consumption by up to 70% and eliminate the need for mercury disposal. Rhode Island’s Regulation 21 caps solvent content at 25% or requires 90% capture, making thermal oxidizers expensive compliance tools. Epson’s SurePress L-4733A uses water-based ink that meets food-contact regulations without requiring post-print washing; however, slower drying on films still favors UV-LED for speed-critical jobs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Outlay for Hybrid Presses | -0.9% | Global, acute for small and mid-size converters | Short term (≤ 2 years) |

| Volatility in Raw Material Prices for Print Substrates | -0.7% | Global, pronounced in North America and Europe | Medium term (2–4 years) |

| Deficit of Skilled Operators for High-End Digital Presses | -0.5% | Global, most severe in the Asia-Pacific | Long term (≥ 4 years) |

| Supply Chain Disruptions in Semiconductor Components | -0.6% | Global, cascades through digital press production | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Outlay for Hybrid Presses

Hybrid presses that blend flexographic and inkjet stations cost more than USD 2 million. Printing United Alliance reports 58.6% of converters deferring purchases in 2025 because payback periods exceed five years. Mark Andy’s DSiQ-730 lists at USD 2.5 million, limiting its audience to the largest converters. Leasing or pay-per-print models ease cash flow but shift residual-value risk to manufacturers, squeezing margins.

Volatility in Raw Material Prices for Print Substrates

The Producer Price Index for coated and laminated multi-web materials stood at 271.05 in March 2025, nearly flat year over year yet still well above the 2021 range. Recycled polyethylene terephthalate (rPET) carries a 20-30% premium over virgin resin. Avery Dennison’s rPET liner, launched in June 2025, is priced 15% above virgin alternatives. Frequent substrate repricing erodes converter margin visibility and discourages the use of long-term contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Printing Technology: Digital Growth Narrows the Gap

Flexographic systems accounted for 47.32% of 2024 revenue, driven by cost efficiency on runs exceeding 10,000 linear meters and compatibility with textured papers and metalized films. Digital units are projected to post a 9.62% CAGR to 2030, driven by the demand for variable data and sub-500-unit economics resulting from serialization, SKU proliferation, and online packaging integration. Hybrid architectures, such as the Mark Andy DSiQ-730, combine the quality of inkjet printing with the speed of flexography, allowing converters to handle long runs while printing variable content without slowing down their production lines.[2]Mark Andy, “DSiQ-730 Hybrid Press,” MarkAndy.com Canon’s LabelStream 4000 now reaches 75 m/min, only 25% shy of midrange flexo, signaling a closing speed gap.

Screen Holdings’ Truepress Jet L350UVSAI delivers seven colors at 60 m min for cosmetics labels that require wide gamuts. Recurring plate and anilox sales still provide flexo makers with a cash-generating installed base; however, Xeikon’s TX300 with Titon dry toner eliminates liquid ink waste and reduces makeready time to under five minutes, eroding that advantage. Flexographic vendors are pushing service packages and consumable bundles to retain clients amid digital migration. Digital suppliers respond with cloud diagnostics that predict maintenance before downtime. Letterpress remains niche for boutique wines, and gravure retains ultra-long runs for multinational beverages. Screen printing stays relevant for industrial chemical labels needing thick deposits. As digital maturation continues, the label printing machine market is poised for technology mix shifts rather than outright displacement.

By Product Type: Narrow Web Dominates While Inline Systems Surge

Narrow web presses accounted for 41.63% of 2024 revenue, reflecting their dominance in the pharmaceutical, cosmetics, and food industries, where label widths rarely exceed 330 mm. Inline presses that integrate die-cutting, lamination, and inspection are expected to grow at a rate of 9.56% annually, the fastest among product types. By eliminating offline steps, converters trim labor and waste, improving turnaround. Wide web presses serve logistics labels up to 670 mm but carry high capital costs. Sheet-fed digital units, while agile, lack continuous finishing, limiting throughput.

Nilpeter’s Chennai expansion supplies 48-50 narrow web flexo units yearly for India and nearby markets. Mettler-Toledo’s V15 inspection head attaches directly to presses, verifying codes at 120 m min and satisfying pharmaceutical compliance. GlobalVision’s 2025 cloud platform enables supervisors to run audits remotely, thereby mitigating skilled labor shortages. However, each inline module adds USD 200,000-500,000, a hurdle for smaller firms. The evolving mix favors converters that can finance comprehensive inline ecosystems.

By Ink Type: UV-LED Accelerates Under Sustainability Pressure

UV-curable inks accounted for 44.74% of 2024 revenue, while UV-LED formulations are expected to record a 9.78% CAGR through 2030, driven by energy savings and mercury-free curing. Water-based inks hold a share in food labels due to their low migration; however, slower drying on films limits their speed. Solvent-based systems offer industrial chemical resistance but face stringent regulations regarding volatile organic compounds. Toner-based dry electrophotographic presses, such as the Xeikon TX300, generate no liquid waste, making them appealing in environments where environmental audits are strict.

Rhode Island’s solvent cap makes thermal oxidizers an expensive retrofit, nudging converters toward LED and aqueous chemistries. UV-LED arrays consume 3-5 kW, compared to 15-20 kW for mercury lamps, resulting in annual power savings of USD 10,000-15,000 on a single line. Epson’s SurePress L-4733A achieves food-contact certification without washing, satisfying European Regulation 1935/2004. As recyclability targets near, ink suppliers collaborate with substrate manufacturers to ensure labels can be washed off during polyethylene terephthalate (PET) reclamation.

By Application: Cosmetics Growth Outpaces Food Staples

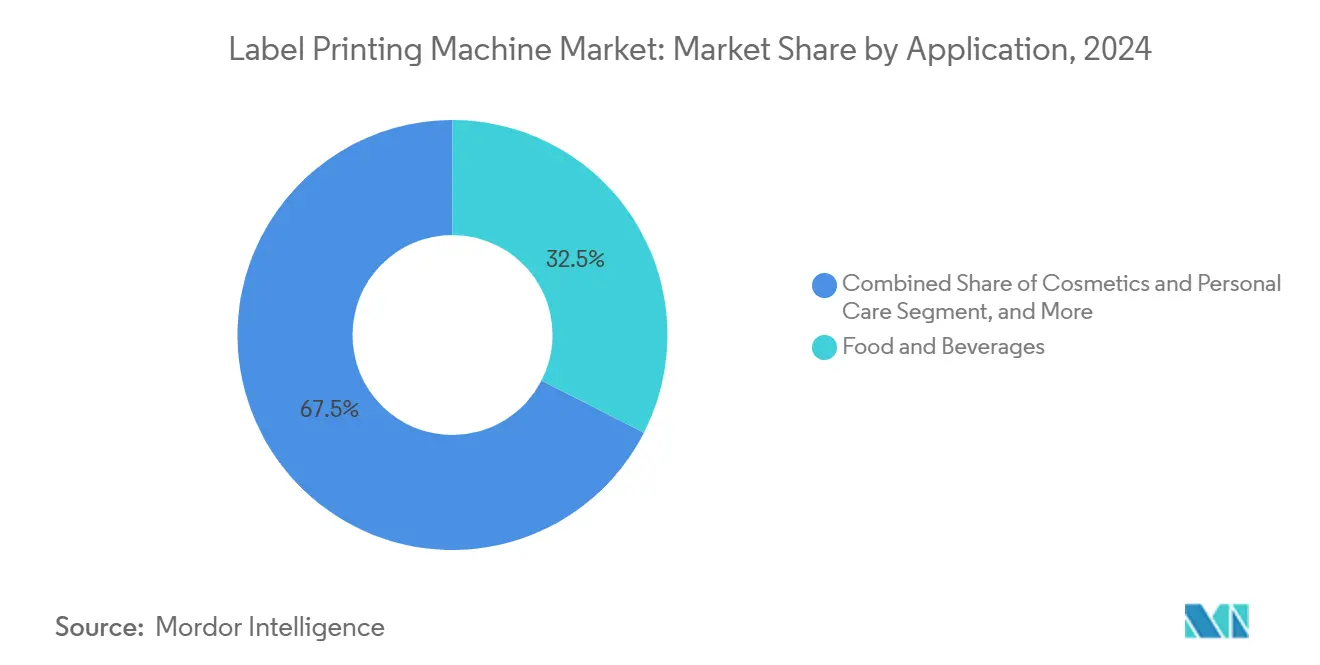

Food and beverages accounted for 32.51% of the 2024 application revenue, primarily due to the mandatory provision of nutrition information and high unit volumes. The cosmetics and personal care market is expected to grow at a rate of 9.25% annually, driven by premium branding and urbanization in the Asia-Pacific region. Craft breweries alone anticipate strong revenue expansion, with many buying only 500 labels per batch, a pattern that favors short-run digital jobs. Pharmaceutical labels are subject to strict serialization, prompting converters to adopt hybrid presses with 100% inspection capabilities. Industrial labels need solvent and abrasion resistance, keeping screen printing relevant, while logistics tags support automated scanning in e-commerce fulfillment.

Konica Minolta’s AccurioLabel230 with DC330Mini converting offers metallic and specialty inks for boutique cosmetics, demonstrating rising demand for value-added embellishment. Domino’s electric pallet labeler automates logistics end-points, extending the equipment scope beyond traditional pressrooms. Application diversity ensures that the label printing machine market does not rely on a single demand driver.

By Substrate Material: Plastic Films Advance on Recycling Mandates

Paper substrates accounted for 37.15% of 2024 revenue, thanks to their cost and recyclability credentials. Plastic films are expected to post a 9.34% CAGR through 2030 as the European regulation mandating a 30% recycled polyethylene terephthalate content takes effect. Polyethylene films are suitable for shrink sleeves, polypropylene dominates clear labels, polyester targets premium cosmetics, while polyvinyl chloride faces potential bans due to its poor recyclability. Foils and metalized papers keep a foothold in spirits labels that seek metallic luster. Synthetic papers, such as PPG’s Teslin, offer tear resistance for outdoor applications.

Avery Dennison’s rPET liner carries a price premium yet meets CleanFlake recycling standards, which helps drive uptake among sustainability-focused brands. Brook + Whittle patented a BlockOut shrink sleeve that detaches during reclamation to avoid contaminating resin streams. Converters must balance recycling-ready structures with performance on high-speed lines, guiding substrate mix decisions.

Geography Analysis

North America accounted for 38.52% of 2024 revenue and is projected to grow at a 7.09% CAGR through 2030. Serialization under the Drug Supply Chain Security Act drives pharmaceutical investment, while the expansion of craft beer boosts short-term digital demand. Rhode Island’s volatile organic compound rule forces ink transitions, trimming margins, but spurring UV-LED adoption. Bobst’s Atlanta Competence Center trains operators locally, improving service reach.

The Asia-Pacific region is expected to post the fastest growth rate of 9.93%, led by India and China, where pharmaceutical output and FMCG manufacturing are expected to increase under localization policies. Nilpeter’s Chennai line supplies regional converters with narrow web presses. Japan’s QR labeling for all drugs and India’s 300-drug QR mandate strengthen digital press pull.[3]Pharmaceuticals and Medical Devices Agency, “QR Code Labeling Requirements,” Pmda.go.jp Limited operator skill in color management remains a brake, prompting suppliers to add automation and remote support.

Europe, South America, and the Middle East and Africa collectively make up the balance. Europe enforces recyclability and solvent caps, prompting converters to shift toward water-based and UV-LED solutions. The United Kingdom deferred producer responsibility fees to 2025, offering a temporary cost reprieve. South America sees strong craft beverage adoption, whereas Middle Eastern and African growth centers on pharmaceuticals and logistics. Heidelberg and Gallus showcased hybrid units at Labelexpo 2025, underscoring European appetite for variable data with flexographic speed.

Competitive Landscape

The label printing machine market remains fragmented, with no vendor holding more than 15% global share. Hybrid presses that combine flexographic and inkjet stations, such as Mark Andy’s DSiQ-730, cater to the pharmaceutical and cosmetics sectors that require serialization at high speeds. Mettler-Toledo’s V15 module makes an inline 360-degree inspection table stakes for compliance.

Vendors establish regional competence centers to shorten service response times. Bobst added hubs in Atlanta and Florence, and Nilpeter expanded its Indian capacity. Chinese manufacturers now offer digital presses at sub-USD 1 million, operating at competitive speeds, which is pressuring established brands. Adobe PDF Print Engine ubiquity erases a software differentiator, intensifying price competition.

Vendors that embed inline QR and verification capabilities can maintain premium pricing in regulated niches, while producers of commodity logistics labels negotiate thinner margins. Semiconductor shortages lengthen delivery of printhead controllers, forcing suppliers to allocate limited stock to higher-margin pharmaceutical lines.

Label Printing Machine Industry Leaders

Mark Andy, Inc.

Bobst Group SA

Canon Inc.

HP Inc.

Heidelberg Druckmaschinen AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Xeikon launched the TX300 label press featuring Titon dry-toner technology, eliminating liquid ink waste and cutting makeready below five minutes.

- June 2025: Avery Dennison released an rPET liner containing 30% post-consumer content to meet European recyclability targets.

- January 2025: Domino presented the Mx-Series electric pallet labeler that automates logistics tagging.

- December 2024: WLS launched the Autonomy digital label printer for budget-conscious converters.

Global Label Printing Machine Market Report Scope

The Label Printing Machine Market refers to the global industry that manufactures and supplies machines designed to print labels for various applications across sectors such as food & beverage, pharmaceuticals, logistics, retail, and industrial products. These machines are essential for product identification, branding, regulatory compliance, and supply chain management.

The Label Printing Machine Market Report is Segmented by Printing Technology (Flexographic, Digital, Offset Lithography, Gravure, Screen, Letterpress, Hybrid), Product Type (Narrow Web, Wide Web, Sheet-Fed, In-Line), Ink Type (UV-Curable, Water-Based, Solvent-Based, UV-LED, Toner-Based), Application (Food and Beverages, Pharmaceuticals, Cosmetics and Personal Care, Industrial, Logistics and Transport, Retail), Substrate Material (Paper, Plastic Films, Foils, Fabric, Other), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Flexographic Printing Machines |

| Digital Printing Machines |

| Offset Lithography Machines |

| Gravure Printing Machines |

| Screen Printing Machines |

| Letterpress Printing Machines |

| Hybrid Printing Machines |

| Narrow Web Label Printing Machines |

| Wide Web Label Printing Machines |

| Sheet-Fed Label Printing Machines |

| In-Line Label Printing Machines |

| UV-Curable Inks |

| Water-Based Inks |

| Solvent-Based Inks |

| UV-LED Inks |

| Toner-Based Inks |

| Food and Beverages |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| Industrial Labels |

| Logistics and Transport |

| Retail and Consumer Goods |

| Paper | |

| Plastic Films | Polyethylene (PE) Films |

| Polypropylene (PP) Films | |

| Polyvinyl Chloride (PVC) Films | |

| Polyester (PET) Films | |

| Foils and Metalized Substrates | |

| Fabric and Textile | |

| Other Substrate Materials |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Printing Technology | Flexographic Printing Machines | ||

| Digital Printing Machines | |||

| Offset Lithography Machines | |||

| Gravure Printing Machines | |||

| Screen Printing Machines | |||

| Letterpress Printing Machines | |||

| Hybrid Printing Machines | |||

| By Product Type | Narrow Web Label Printing Machines | ||

| Wide Web Label Printing Machines | |||

| Sheet-Fed Label Printing Machines | |||

| In-Line Label Printing Machines | |||

| By Ink Type | UV-Curable Inks | ||

| Water-Based Inks | |||

| Solvent-Based Inks | |||

| UV-LED Inks | |||

| Toner-Based Inks | |||

| By Application | Food and Beverages | ||

| Pharmaceuticals | |||

| Cosmetics and Personal Care | |||

| Industrial Labels | |||

| Logistics and Transport | |||

| Retail and Consumer Goods | |||

| By Substrate Material | Paper | ||

| Plastic Films | Polyethylene (PE) Films | ||

| Polypropylene (PP) Films | |||

| Polyvinyl Chloride (PVC) Films | |||

| Polyester (PET) Films | |||

| Foils and Metalized Substrates | |||

| Fabric and Textile | |||

| Other Substrate Materials | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What will be the size of the label printing machine market by 2030?

It is projected to reach USD 11.57 billion in 2030, climbing from USD 8.21 billion in 2025.

Which printing technology is growing fastest in label equipment?

Digital presses are expected to register a 9.62% CAGR from 2025 to 2030 as variable-data demand soars.

Why are UV-LED inks gaining traction in label production?

They cut energy use up to 70%, remove mercury lamps, and comply with emerging volatile organic compound limits.

What region is forecast to post the strongest growth in equipment demand?

Asia-Pacific is set to expand at a 9.93% CAGR to 2030 thanks to pharmaceutical and FMCG manufacturing growth.

How do hybrid presses improve converter economics?

They combine flexographic speed with digital variability, letting converters run long jobs while printing unique codes without slowing the line.

What key restraint could slow capital spending on new presses?

Acquisition costs above USD 2 million for hybrid platforms dissuade small and mid-size converters from upgrading.

Page last updated on: