Saudi Arabia Construction and Demolition Waste Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

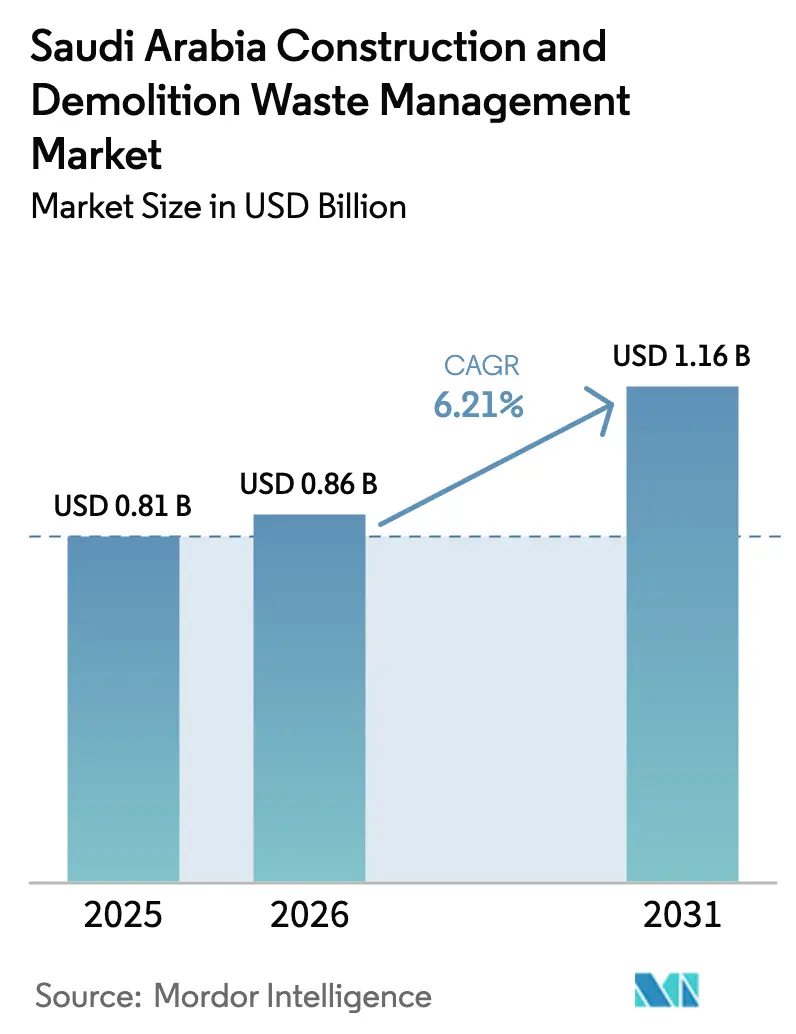

| Base Year Market Size (2025) | USD 0.81 Billion |

| Market Size (2026) | USD 0.86 Billion |

| Market Size (2031) | USD 1.16 Billion |

| Growth Rate (2026 - 2031) | 6.21% CAGR |

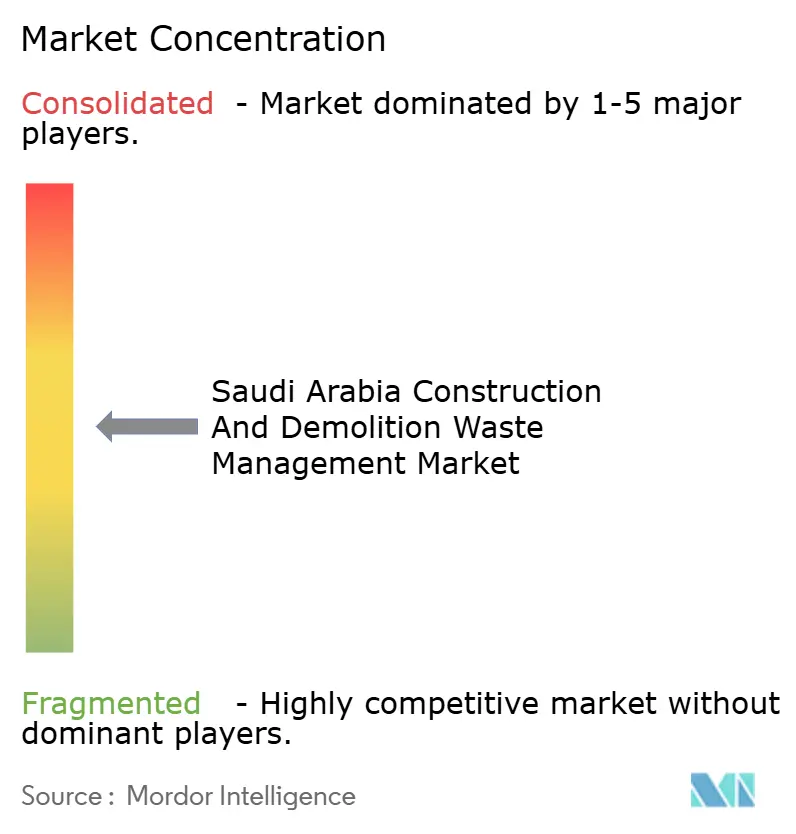

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Construction and Demolition Waste Management Market Analysis by Mordor Intelligence

The Saudi Arabia Construction And Demolition Waste Management Market size is expected to increase from USD 0.81 billion in 2025 to USD 0.86 billion in 2026 and reach USD 1.16 billion by 2031, growing at a CAGR of 6.21% over 2026-2031.

Recycling and material recovery are expected to emerge as the fastest-growing service segment in the Saudi Arabia construction and demolition (C&D) waste management market, driven by tightening regulatory enforcement and shifting landfill economics. Increasing landfill costs and stricter compliance requirements are encouraging contractors to adopt on-site segregation, mobile crushing, and localized processing solutions to reduce disposal volumes and transportation costs. At the same time, growing adoption of digital tools such as route optimization and material tracking is improving operational efficiency across large construction projects. As infrastructure development accelerates under national programs, service providers offering integrated capabilities across collection, processing, and recycled material offtake are gaining a competitive advantage, positioning recycling as a core pillar of the evolving C&D waste management ecosystem.

Key Report Takeaways

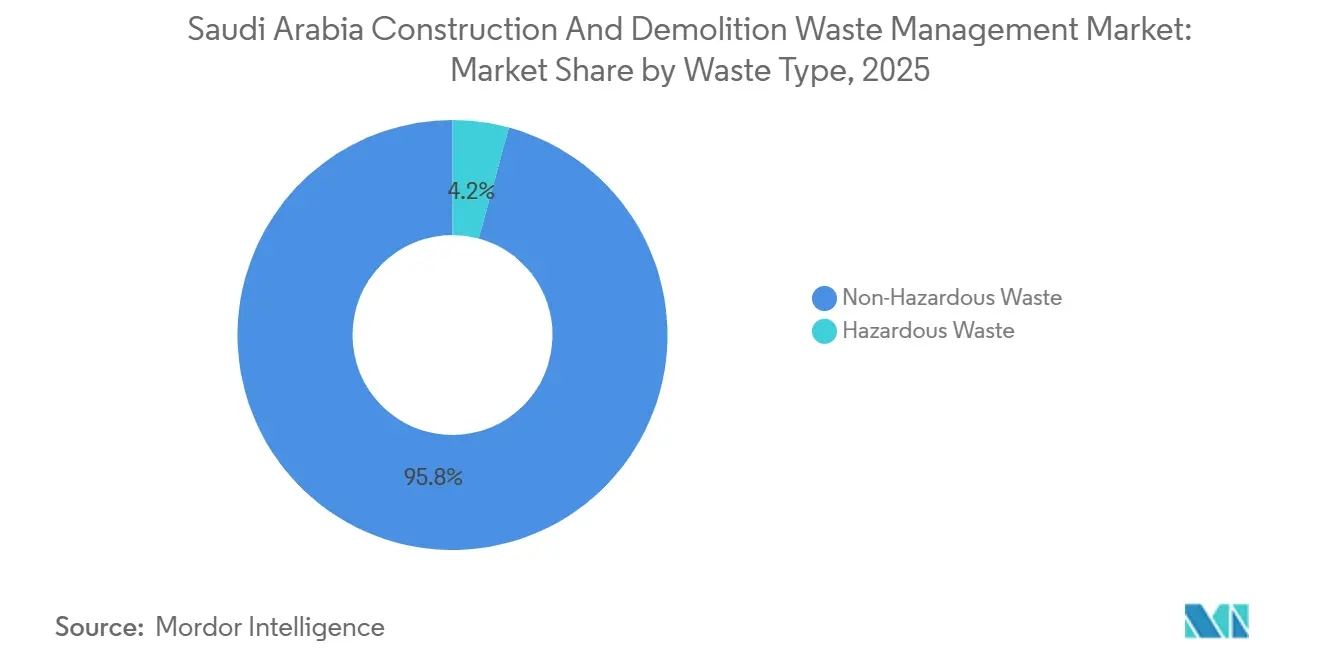

- By waste type, non-hazardous streams held 95.76% of the Saudi Arabia construction and demolition waste management market share in 2025, while hazardous streams are projected to grow at a 6.34% CAGR through 2031.

- By material, concrete and bricks accounted for 55.10% of the Saudi Arabia construction and demolition waste management market size in 2025, and asphalt is forecast to expand at a 6.52% CAGR to 2031.

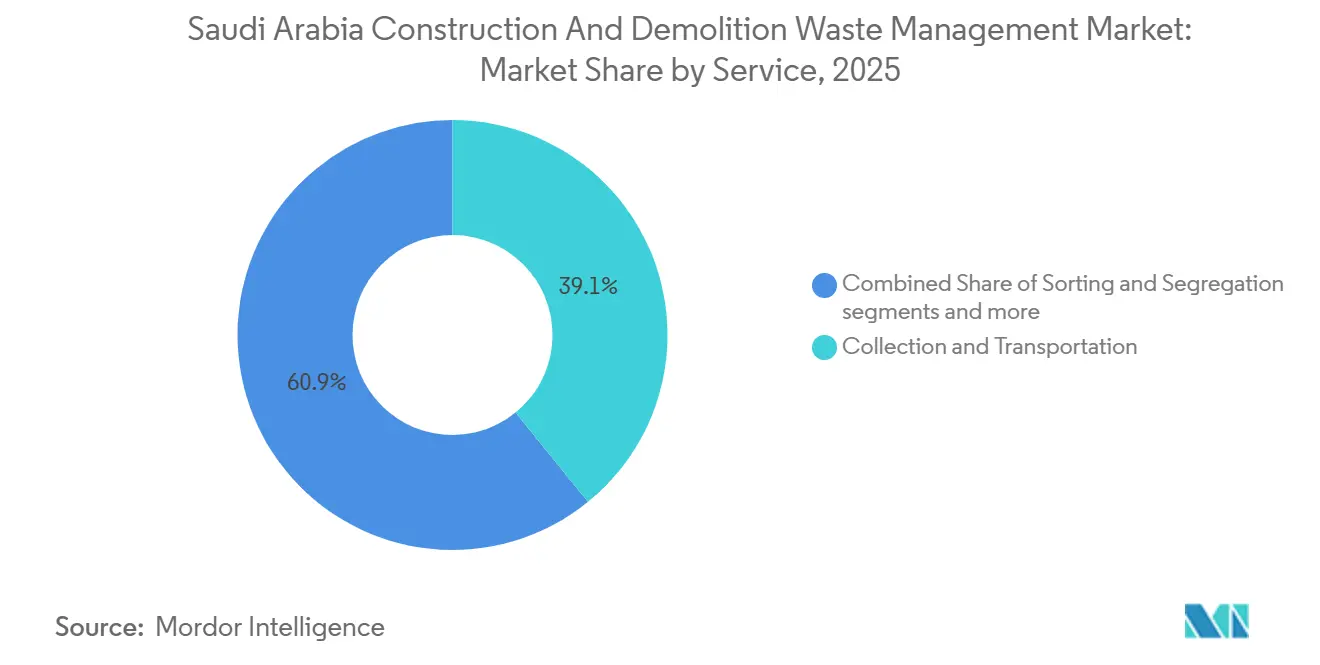

- By service, collection and transportation led with 39.14% share in 2025, while recycling and material recovery is set to record a 6.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Construction and Demolition Waste Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 and Government Regulations | +1.8% | National, with early enforcement in Riyadh, Jeddah, Mecca, Dammam, Madina | Medium term (2-4 years) |

| Development of Advanced Recycling Infrastructure | +1.5% | Core urban clusters, with spillover to industrial cities | Long term (≥ 4 years) |

| Mandatory Recycled Content Requirements | +1.2% | NEOM, Red Sea Project, Diriyah Gate, expanding nationally | Medium term (2-4 years) |

| Economic Benefits and Cost Savings | +0.9% | National | Short term (≤ 2 years) |

| Saudi Investment Recycling Company Leadership | +0.7% | Riyadh and Jeddah, plus emerging giga-project zones | Long term (≥ 4 years) |

| Technological Advancements in Waste Processing | +0.6% | Riyadh, Jeddah, with pilots in Dammam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 and Government Regulations

Royal Decree M/3 elevates construction and demolition waste from a disposal burden to a regulated resource by adding stringent penalties that include fines up to USD 8 million and potential imprisonment for violators. The National Center for Waste Management enforces technical guidelines that require on-site segregation and third-party audits for projects larger than 10,000 square meters, which integrates recycling targets into core project controls. Master plans for priority clusters call for more than 840 treatment and recovery facilities by 2040, including dedicated C&D capacity to align supply with rising demand from giga-project execution windows. Permitting in these clusters is increasingly tethered to documented diversion plans and named processors, which strengthens enforcement at the point of building approval and compresses timelines for compliance upgrades. Consolidated oversight by the National Center for Waste Management replaces fragmented municipal rules and reduces barriers to cross-regional scaling for qualified operators. Early enforcement in the largest cities is cascading to adjacent jurisdictions, which support more uniform practices within the Saudi Arabia Construction and Demolition Waste Management Market.

Development of Advanced Recycling Infrastructure

High-capacity automated facilities in Riyadh run at 600 tonnes per hour with targeted recovery rates near 90%, which sets the performance bar for mid-tier rivals and shapes procurement standards. A static sorting plant commissioned in 2024 uses an enclosed modular picking station and a light-material removal system to extract up to 6 tonnes per hour of contaminants from a 50-tonnes-per-hour feed, which improves purity and throughput under extreme-heat conditions. Recognition in early 2025 for record-scale C&D recycling underscores a shift toward vertically integrated models that bundle collection, sorting, and downstream product sales.[1]AJ, “Advancing Saudi Arabia’s Circular Economy and Sustainable Future,” GPCA, gpcachem.org National master plans extend the infrastructure runway past 2030, with extensive pipelines in priority clusters that will absorb demand spikes from giga-project execution phases. International partners are committing to hub models that expand treatment capacities for multiple waste streams, which signals confidence in the Kingdom’s regulatory and pricing trajectory. Enclosed and electrified systems reduce weather-related downtime and enhance worker safety, which reinforces the cost case for modernized lines in the Saudi Arabia Construction and Demolition Waste Management Market.

Mandatory Recycled Content Requirements

NEOM tender language requires verified recycled content in concrete, asphalt, and rebar, which links contract compliance to access to certified secondary materials and traceable offtake. The Red Sea Project enforces a 70% on-site C&D recycling mandate, which drives adoption of mobile crushers and closed-loop flows within project perimeters. Government advocacy is moving toward standardized acceptance of post-consumer recycled products in new building projects, which aligns future public procurement with circular outcomes once technical standards are finalized.[2]Saudi Arabia | Towards Osaka Blue Ocean Vision,” G20 Marine Plastic Litter, g20mpl.org As quality specifications mature, public-sector thresholds for recycled inputs are expected to become part of baseline tender requirements, which stabilizes demand and supports bankability. These changes accompany the ongoing development of national specifications for recycled aggregates, which are critical for uniform acceptance across municipalities and agencies. Together, content mandates and standards are shaping predictable offtake pipelines across concrete, asphalt, and steel in the Saudi Arabia Construction and Demolition Waste Management Market.

Economic Benefits and Cost Savings

Landfill tipping fees at USD 70 per ton in 2026 compress the historical cost advantage of disposal and redirect volumes into recovery, where project budgets can capture both cost savings and compliance value. Recycled concrete aggregates in Jeddah are priced at USD 20 to 30 per ton for inactivated grades and USD 30 to 45 per ton for alkali-activated grades, which enables competitive bids for road subbases, pavements, and fills. Digital marketplaces list stock levels and prices for recycled aggregates, which helps contractors evaluate cost and availability against quarry options before mobilizing. This transparency reduces procurement risk during peak construction windows, which supports continuous operations without costly delays. On-site diversion at giga-projects cuts hauling distances and fuel use when mobile sort and crush units are deployed, which lowers logistics costs while meeting permit targets. Savings compound with avoided gate fees and improved schedule control, which strengthens the business case for recycling in the Saudi Arabia Construction and Demolition Waste Management Market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Investment Requirements | -0.9% | National, acute in secondary cities with limited PPP frameworks | Medium term (2-4 years) |

| Fragmented Regulatory Framework and Limited Collaboration | -0.6% | Variable across 25 regional clusters, more pronounced beyond the top five cities | Short term (≤ 2 years) |

| Inadequate Source Segregation and Sorting Practices | -0.5% | National, with gaps in residential zones and small sites | Medium term (2-4 years) |

| Quality Concerns with Recycled Aggregates | -0.4% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Investment Requirements

Capital-intensive equipment for waste-to-energy and hazardous waste treatment requires long import lead times, which extend project schedules and delay operating cash flows. Environmental impact assessments, licensing, and zoning clearances can push permitting to 12 to 18 months, which increases development risk and financing costs. Concession frameworks with 15 to 25 year tenors improve revenue visibility yet demand significant upfront equity, which can be difficult for mid-tier operators to secure. Strategic co-financing, such as the USD 625 million program between SIRC and EIG Partners, helps mobilize capital for circular infrastructure and spreads risk across asset classes. Currency-linked procurement exposures and perceived technology risks can elevate borrowing costs, which raises hurdle rates and tempers the entry of smaller firms. Despite these headwinds, public sponsors and international partners continue to develop multi-asset programs that include C&D capacity expansions in the Saudi Arabia Construction and Demolition Waste Management Market.

Fragmented Regulatory Framework and Limited Collaboration

Academic research places the absence of harmonized circular economy rules near the top of execution barriers for large construction programs, which reflects practitioner uncertainty on codes and thresholds for recycled content. While the national model defines 25 service clusters, master plans advance faster in the five largest cities than in secondary municipalities, which leaves uneven timelines for infrastructure and enforcement. Variations in municipal enforcement increase compliance costs for contractors and can slow on-site adoption of segregation and tracking practices. Stakeholders report overlapping permits and unclear acceptance thresholds for recycled aggregates and other secondary products, which complicate bid preparation and slow capital deployment. These gaps extend tendering timelines as operators buffer for regulatory ambiguity in project models, which can deter first-time entrants. Shared data platforms and digital compliance solutions are expected to reduce friction as agencies align standards and reporting in 2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Waste Type: Hazardous Streams Drive Specialized Infrastructure

Non-hazardous streams claimed 95.76% of the Saudi Arabia Construction and Demolition Waste Management Market size in 2025, while hazardous C&D waste is forecast to expand at a 6.34% CAGR through 2031 as tighter licensing, on-site segregation, and audits elevate capture of specialized fractions. Enforcement under Royal Decree M/3 and technical guidance for projects above 10,000 square meters have made improper handling costly, which is shifting material flows into compliant pathways. Gypsum and drywall require dedicated lines to avoid cross-contamination of concrete aggregates, which adds USD 10 to 15 per ton in processing costs but unlocks reuse channels in cement and soil conditioning. High-throughput automated facilities remain tuned for inert streams like concrete and bricks, which support scale in non-hazardous recovery, while hazardous fractions rely on smaller-batch thermal and chemical treatment assets.

Port and industrial zones are expanding integrated treatment capabilities that overlap with hazardous portions of C&D waste, which positions specialized operators to serve marine and industrial adjacencies. Anchor plants in the capital combine enclosed sorting, picking, and light-fraction extraction to sustain high recovery at scale for non-hazardous flows, which improves product quality and consistency for repeat orders. This division of labor is leading to co-location models where hazardous specialists operate near large inert recyclers to share logistics and access assured feedstock. Together, these moves show the Saudi Arabia Construction and Demolition Waste Management industry maturing into a two-track system that aligns asset design with regulatory risk and material profiles.

By Material: Asphalt Recycling Accelerates Amid Pavement Renewal Cycles

Concrete and bricks commanded 55.10% share in 2025, while asphalt is projected to be the fastest-growing material with a 6.52% CAGR to 2031 within the Saudi Arabia Construction and Demolition Waste Management Market, reflecting rising acceptance of recycled inputs in pavements and base layers. Procurement rules at flagship developments require verified recycled content in concrete, asphalt, and rebar, which translates policy into steady demand for certified secondary feedstock. Automated lines that integrate overband magnets and dedicated light-fraction removal equipment improve purity and recovery, which supports higher-value applications for recycled aggregates. Timber and composite materials continue to face end-use constraints, which leaves a larger share of the product mix in aggregate classes where standards are advancing, and buyers are scaling orders.

Contamination control remains central to cement-grade aggregates, which is why enclosed picking stations and pre-crush light-fraction extraction are being deployed at scale. Jeddah-based research demonstrates that alkali activation improves recycled aggregate properties, which enables upgraded applications that can command higher realized prices. National standards under development will guide consistent acceptance for recycled aggregates across structural and pavement uses, which reduces specification risk during bidding and approval. Digital marketplace listings for graded products, including RC 3/4, are making offtake more predictable by aligning contractor needs with available inventory in real time, which supports the Saudi Arabia Construction and Demolition Waste Management industry's move into performance-based supply.

By Service: Recycling Gains Momentum as Landfill Economics Shift

Collection and transportation accounted for 39.14% in 2025, yet recycling and material recovery are projected to deliver the highest growth at a 6.71% CAGR through 2031 in the Saudi Arabia Construction and Demolition Waste Management Market, as gate fees and permit rules change the cost equation. Gate fees at USD 70 per ton in 2026 reduce the incentive to landfill mixed loads and favor on-site or near-site sorting and crushing that retain material value and reduce hauling. Licensing now links large-project permits to third-party audits and on-site segregation, which creates service demand for verified sorting and reporting. Mobile crushing, transfer stations, and modular MRFs are increasingly used to cut transport distances and keep pace with demolition schedules, which improves throughput and compliance.

Digital route optimization and material tracking are expanding through partnerships such as Aramco Digital and Diversys Software, which embed predictive analytics and compliance automation into field operations. Fleet and container sensors, adapted from municipal waste systems, are increasingly being applied to C&D skip logistics to improve load factors and reduce idle trips. Processing capacity is scaling through modular lines and regional hubs, which pressures incumbents to upgrade or consolidate. These shifts are moving the Saudi Arabia Construction and Demolition Waste Management industry toward integrated service models.

Geography Analysis

Priority clusters led by Riyadh, Jeddah, Mecca, Dammam, and Madina anchor the near-term infrastructure pipeline, with national plans calling for more than 840 treatment and recovery facilities by 2040 that include dedicated C&D capacity. Riyadh retains a significant share of national waste generation in 2025 and is prioritized for new facilities within the national framework, which supports steady feedstock and scale for high-capacity lines. The capital’s anchor facility combines high-throughput sorting and advanced light-fraction removal to deliver consistent quality aggregates for public and private demand, which stabilizes local circular flows. Digital marketplace listings reinforce offtake by linking verified processors to contractors under recycled-content procurement clauses in city programs.

The Eastern Province benefits from strong industrial adjacencies that overlap with hazardous dimensions of C&D waste and from new chemical processing and treatment units commissioned in Jubail, which can adapt to specialized fractions as enforcement tightens. Coastal giga-projects enforce strict on-site diversion and recycled content, which promotes mobile crushing, localized loops, and reduced reliance on distant landfills or transfer networks. These requirements reshape collection patterns across large footprints by prioritizing intra-project flows that cut haulage and schedule risk. Additional facilities staged across secondary municipalities aim to close infrastructure gaps and backstop diversion targets as Vision-aligned projects scale through 2030.

Mecca and Madina, both listed among the priority clusters, require flexible capacity solutions that can absorb renovation and construction surges while maintaining diversion objectives. As licensing and third-party audits become more consistent across regions, data and compliance platforms are expected to streamline enforcement and reporting. Foreign and domestic investors are targeting corridors where master planning, policy clarity, and procurement mandates converge, which signals a supportive environment for continued capital deployment. These developments reinforce the position of the Saudi Arabia Construction and Demolition Waste Management Market as a proving ground for circular construction models under national policy goals.

Competitive Landscape

The Saudi Arabia Construction and Demolition Waste Management Market exhibits a moderate concentration anchored by a vertically integrated national player that combines collection, automated sorting, and online offtake, which raises performance and service benchmarks for the ecosystem.[3]SIRC Marketplace: Home,” Saudi Investment Recycling Company, circe.sirc.sa Automated lines with enclosed picking stations and light-fraction extraction are lifting recovery and improving consistency, which encourages public buyers to specify recycled content in more tenders. Mid-tier and specialist firms are competing in niche geographies and materials, particularly metals and hazardous fractions, where they can operate alongside large inert recyclers without direct price compression. Transparent marketplace pricing for graded aggregates further supports repeat orders and stable cash conversion cycles for integrated players.

Strategic financing continues to underpin multi-asset programs in circular infrastructure, including a USD 625 million initiative aligned with C&D-adjacent projects that diversify revenue into refuse-derived fuels and tire processing. Industry leaders are linking operations with research and pilot deployments to improve process control and material performance, which shortens time to commercial scale for innovations tested in local conditions. Industrial and port partnerships expand footprints into marine and hazardous waste streams that intersect with C&D, which broadens service portfolios and captures new feedstock sources. Digital collaborations focus on end-to-end tracking, compliance automation, and predictive analytics, which help integrate collection, processing, and offtake planning at scale.

Marketplace tools listing real-time volumes and prices support contracting for graded recycled aggregates and tighten links between processors and project owners. Operators that connect collection fleets, modular processing lines, and digital sales channels can defend margin as gate-fee arbitrage narrows across regions. Technology-forward plants that standardize optical sorting, enclosed picking, and pre-crush light-fraction removal continue to lift recovery rates and lower contamination risk, which improves offtake confidence. These strategies are shaping competition in the Saudi Arabia Construction and Demolition Waste Management Market by rewarding scale, integration, and data-backed reliability in new concessions and private contracts.

Saudi Arabia Construction and Demolition Waste Management Industry Leaders

Averda

Veolia Middle East

Al Sharif Group Holding

AESG

Sustainability Chain Contracting

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Reviva and Jubail Integrated Waste Management and Recycling Company completed startup and commissioning of chemical processing and wastewater treatment units that can treat over 100,000 metric tons of spent caustic and 250,000 metric tons of wastewater annually.

- January 2025: SIRC’s subsidiary Akam received a Guinness World Record for operating the largest construction and demolition recycling plant by capacity, achieving a 90% material recovery rate at its Al Khair facility in Riyadh.

- March 2025: Aramco Digital and Diversys Software formed a partnership to deploy end-to-end digital infrastructure for waste and resource management with predictive analytics, tracking, and compliance monitoring

- May 2025: SIRC signed a Memorandum of Understanding with EIG Partners to co-finance USD 625 million in circular-economy projects, including RDF and tire processing facilities, which, while not directly part of C&D waste streams, strengthen the broader recycling ecosystem and infrastructure synergies.

Saudi Arabia Construction and Demolition Waste Management Market Report Scope

The Saudi Arabia Construction and Demolition Waste Management Market Report is Segmented by Waste Type (Non-Hazardous Waste, Hazardous Waste), by Material (Concrete & Bricks, Asphalt, Metal, Timber, Soil and Sand, Gypsum & Drywall, Others), and by Service (Collection & Transportation, Sorting & Segregation, Recycling & Material Recovery, Landfilling & Disposal). The Market Forecasts are Provided in Terms of Value (USD).

| Non-Hazardous Waste |

| Hazardous Waste |

| Concrete & Bricks |

| Asphalt |

| Metal |

| Timber |

| Soil and Sand |

| Gypsum & Drywall |

| Others (Plastic, Wood, Glass) |

| Collection & Transportation |

| Sorting & Segregation |

| Recycling & Material Recovery |

| Landfilling & Disposal |

| By Waste Type | Non-Hazardous Waste |

| Hazardous Waste | |

| By Material | Concrete & Bricks |

| Asphalt | |

| Metal | |

| Timber | |

| Soil and Sand | |

| Gypsum & Drywall | |

| Others (Plastic, Wood, Glass) | |

| By Service | Collection & Transportation |

| Sorting & Segregation | |

| Recycling & Material Recovery | |

| Landfilling & Disposal |

Key Questions Answered in the Report

What is the size of the Saudi Arabia Construction and Demolition Waste Management Market in 2026 and where is it heading by 2031?

The market is USD 0.86 million in 2026 and is forecast to reach USD 1.16 million by 2031, at a 6.21% CAGR over 2026-2031.

Which policies are driving growth in the Saudi Arabia Construction and Demolition Waste Management Market?

Royal Decree M/3 penalties, mandatory on-site segregation and audits for large projects, and cluster-based infrastructure plans are the primary drivers.

Which segments lead by share and by growth within the market?

Non-hazardous waste leads by share at 95.76% in 2025, while hazardous streams post the fastest growth at 6.34% CAGR; by material, concrete and bricks lead at 55.10% with asphalt growing at 6.52% CAGR; by service, collection and transportation leads at 39.14% while recycling and material recovery grows at 6.71% CAGR.

How do landfill fees and recycled aggregate prices affect project budgets in 2026?

Gate fees at USD 70 per ton support the economic case for recovery, while recycled aggregates are priced near USD 20 to 30 per ton for standard grades and USD 30 to 45 per ton for alkali-activated grades.

What technologies are improving C&D recycling performance in Saudi Arabia?

Enclosed modular picking stations, light-fraction removal systems, and digital tracking platforms are raising recovery, purity, and compliance across large facilities and fleets.

Page last updated on: