Klinefelter Syndrome Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.48 Billion |

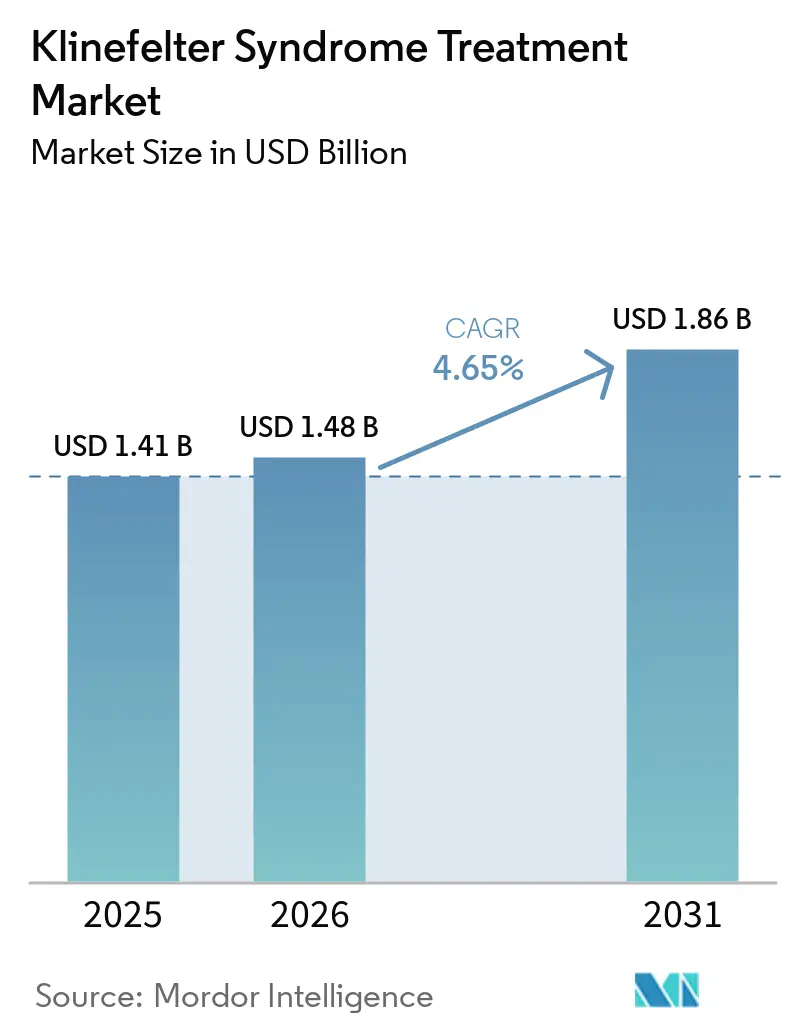

| Market Size (2031) | USD 1.86 Billion |

| Growth Rate (2026 - 2031) | 4.65% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Klinefelter Syndrome Treatment Market Analysis by Mordor Intelligence

The Klinefelter Syndrome Treatment Market size was valued at USD 1.41 billion in 2025 and is estimated to grow from USD 1.48 billion in 2026 to reach USD 1.86 billion by 2031, at a CAGR of 4.65% during the forecast period (2026-2031).

The market is supported by the fact that Klinefelter syndrome remains the most common sex chromosome abnormality in males, affecting 1 in 500 to 660 male births, yet fewer than half of affected people are identified during their lifetime, which keeps a large pool of patients outside formal care today and available for future diagnosis and treatment entry. The market is also shifting from episodic androgen replacement toward a broader lifelong model that includes hormonal treatment, fertility support, and long-term surveillance for cardiometabolic and bone health needs, which raises care intensity after diagnosis. Earlier detection through rising clinician awareness, widening use of prenatal genetic screening, and updated pediatric guidance in countries such as Japan is improving the chance that patients enter treatment before infertility becomes the first trigger for diagnosis. The market remains commercially attractive because better oral and long-acting testosterone formats are reducing adherence barriers, while fertility protocols using micro-TESE plus ICSI are broadening the treatment pathway for men who want biological fatherhood. The market still faces a ceiling from underdiagnosis, high fertility costs, and the sequencing challenge between testosterone use and fertility preservation, but the large untreated population and evidence of better outcomes with therapy keep the long-term opportunity intact.

Key Report Takeaways

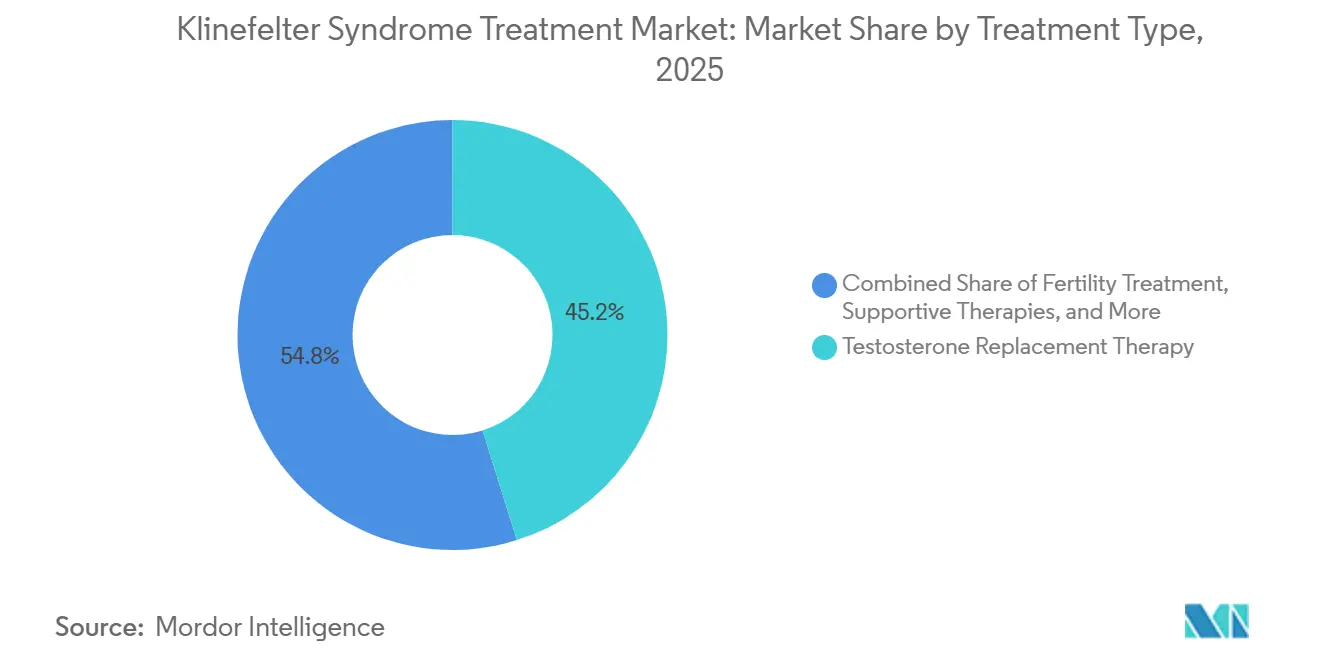

- By treatment type, testosterone replacement therapy led with 45.1% revenue share in 2025, while fertility treatment is projected to expand at 7% CAGR through 2031.

- By route of administration, injectables held 49.2% of the Klinefelter syndrome treatment market share in 2025, while oral and buccal products are forecast to grow the fastest at 6.5% CAGR through 2031.

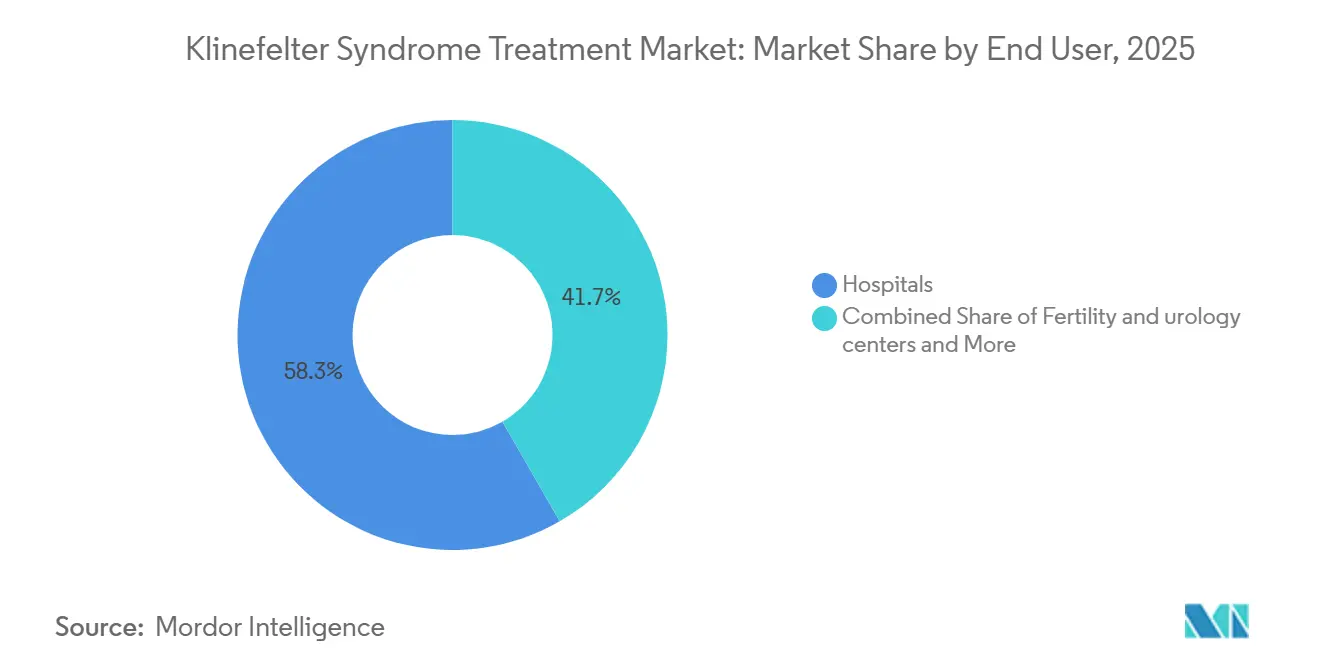

- By end user, hospitals accounted for 58.3% of revenue in 2025, while fertility and urology centers are expected to record the highest CAGR at 6.3% through 2031.

- By age group, adults represented 51.1% of demand in 2025, while adolescents are set to grow the fastest at 6.3% CAGR through 2031.

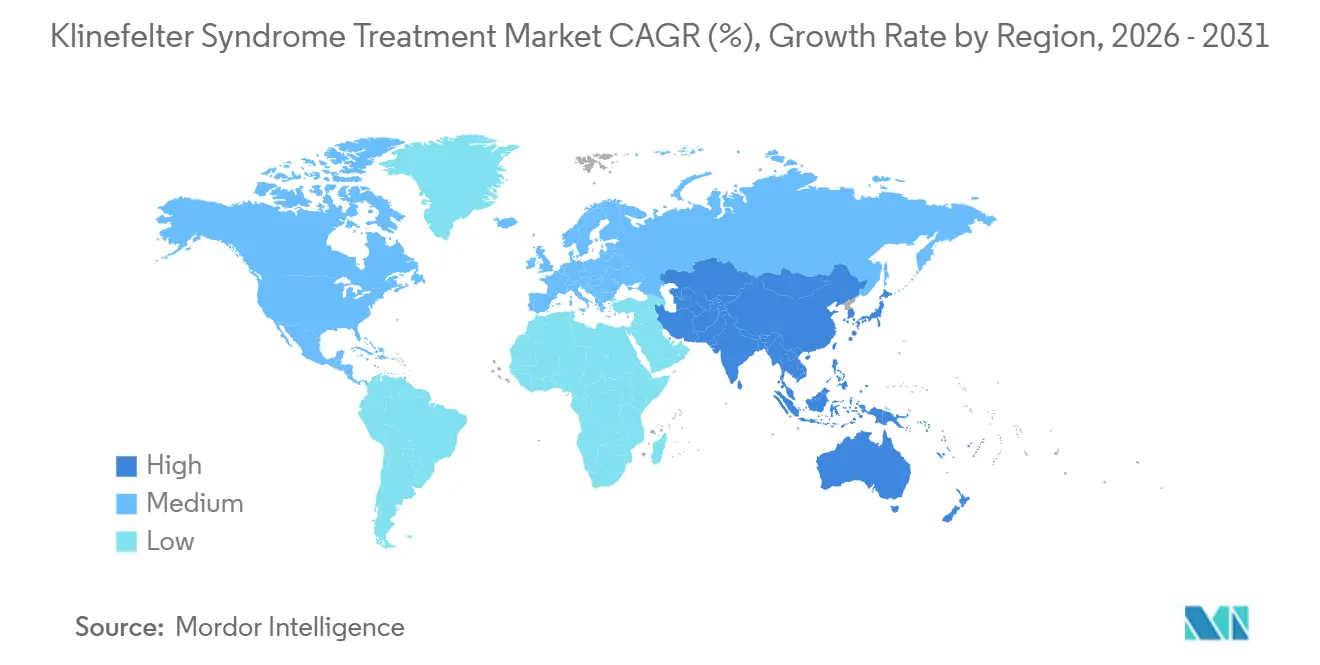

- By geography, North America held 45.2% of the Klinefelter syndrome treatment market size in 2025, while Asia-Pacific is projected to expand at 5.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Klinefelter Syndrome Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Earlier diagnosis through awareness growth | +0.8% | Global, with early gains in North America and Northern Europe | Short term (≤ 2 years) |

| Better adherence from oral and long-acting testosterone | +0.7% | North America and Europe, with spillover into Asia-Pacific | Medium term (2-4 years) |

| Fertility success improving through micro-TESE plus ICSI | +0.9% | Global, with Asia-Pacific and Europe as core markets | Medium term (2-4 years) |

| Reimbursement and rare-disease policy support broadening access | +0.6% | Europe and North America primary, nascent in Asia-Pacific | Medium term (2-4 years) |

| Prenatal and pediatric screening widening lifetime treatment pools | +0.5% | North America, Europe, and East Asia | Long term (≥ 4 years) |

| Cardiometabolic and bone-health surveillance raising care intensity | +0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Earlier Diagnosis via Rising Clinician and Patient Awareness

The Klinefelter syndrome treatment market continues to be shaped by a diagnosis gap that remains unusually wide for a condition this common, with fewer than 50% of affected males identified during their lifetime and median diagnosis still concentrated between ages 28 and 31. That late timing matters because many men only enter care during infertility workups, which delays hormonal support, bone protection, metabolic follow-up, and fertility planning that could have started years earlier. Since 2024, the diagnostic toolkit has improved as machine-learning approaches using electronic health records and hormone profiles moved closer to practical early identification in general practice, which shifts case finding away from late specialist referral.

The Klinefelter syndrome treatment market benefits when diagnosis happens earlier because earlier-identified patients have better glycolipid control, stronger bone health, and more usable fertility windows, which supports longer and more intensive treatment use over time. Updated pediatric guidance in Japan and stronger attention to fertility-related presentation in European centers are also moving the patient journey forward, especially for adolescents who would previously have entered treatment much later. The same trend is reinforced by expanding prenatal and pediatric genetic screening, because diagnosed children and adolescents are more likely to move into structured monitoring and then lifelong care rather than entering the Klinefelter syndrome treatment market only after adulthood infertility appears.

Better Adherence from Oral and Long-Acting Testosterone Formats

The market is gaining from formulation progress that addresses one of testosterone therapy’s oldest commercial problems, which is poor persistence when treatment is inconvenient or clinic dependent. In July 2025, the FDA revised the prescribing information for KYZATREX and removed the boxed warning for blood pressure increases, which lowered a meaningful barrier to broader prescribing in adult hypogonadism management[1]“KYZATREX Prescribing Information,” U.S. Food and Drug Administration, fda.gov.. XYOSTED also remained an important example of the home-based shift, because its subcutaneous autoinjector format supports weekly self-administration and its label update preserved a favorable treatment profile for patients who prefer to avoid clinic injection routines. These changes matter commercially because at-home oral and self-injected formats expand the prescriber base beyond specialist endocrinology centers and make telehealth follow-up more practical for stable patients.

The Klinefelter syndrome treatment market still relies heavily on long-acting injectables, and Danish prescription tracking showed that parenteral formulations remained the dominant mode of testosterone use, which means new formats are challenging a strong installed habit rather than entering an empty category. Even so, every step that reduces travel, clinic scheduling, and regimen complexity supports better adherence, and better adherence directly increases the commercial value of lifelong hormonal care in the Klinefelter syndrome treatment market.

Expanding Fertility Success through Micro-TESE plus ICSI

The Klinefelter syndrome treatment market is also being lifted by the steady normalization of fertility treatment, because biological fatherhood is no longer seen as unattainable for many azoospermic patients with this condition. Micro-TESE combined with ICSI now achieves sperm retrieval in 40%-50% of relevant patients, which has made fertility care a realistic clinical pathway rather than an exceptional intervention. A 2025 study from Henan Provincial People’s Hospital reported a 47.7% sperm retrieval rate in 260 patients and found no significant difference in clinical pregnancy between synchronous fresh protocols and asynchronous cryopreserved protocols. That finding is commercially important because fertility centers can separate sperm retrieval from female partner stimulation schedules, which improves throughput and reduces pressure on tightly coordinated treatment windows.

The Klinefelter syndrome treatment market gains further support when early fertility counseling and sperm banking assessment are encouraged during adolescence, since that creates a better-prepared adult treatment pool and reduces last-minute decision making when infertility surfaces. As retrieval and live birth outcomes continue to look comparable to non-Klinefelter non-obstructive azoospermia after successful retrieval, fertility services are moving closer to routine inclusion in care pathways across the Klinefelter syndrome treatment market.

Broader Reimbursement and Rare-Disease Policy Support

The market benefits when reimbursement is predictable, because patients need recurring hormone therapy, specialist visits, and surveillance that can extend for decades after diagnosis. France illustrates the supportive end of the access spectrum, where full reimbursement pathways for relevant care reduce financial interruption and help keep long-term management inside the formal health system. Europe’s broader policy environment also matters because the European Parliament raised formal questions in 2025 on rare-disease access gaps, which signals continued pressure for more consistent orphan and specialty care availability across member states.

The Klinefelter syndrome treatment market also expands when annual endocrine follow-up is standardized, since bone density, hematologic monitoring, cardiometabolic surveillance, and reproductive counseling all create recurring touchpoints instead of sporadic treatment episodes[2]“EAU Guidelines on Sexual and Reproductive Health,” European Association of Urology, uroweb.org.. This higher care intensity is becoming more relevant because metabolic syndrome and osteoporosis are frequent in the population, so surveillance itself drives sustained service use even outside fertility-related intervention. Taken together, reimbursement support and structured follow-up make revenue in the market more durable, because diagnosed patients are more likely to remain in coordinated treatment rather than cycling in and out of isolated care episodes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High out-of-pocket cost of fertility and multidisciplinary care | -0.7% | Global, most acute in Asia-Pacific and South America | Medium term (2-4 years) |

| Persistent underdiagnosis and late referral in primary care | -0.8% | Global, most acute in developing markets | Long term (≥ 4 years) |

| Testosterone and fertility sequencing dilemma | -0.5% | Global | Medium term (2-4 years) |

| Thin disease-specific innovation pipeline | -0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Cost of Fertility and Multidisciplinary Care

The market still loses potential demand when patients must pay for fertility procedures, specialist consultations, and long-term monitoring out of pocket, because the full care model is expensive even before repeated cycles are considered. Markets without strong reimbursement structures face the greatest limitation, since micro-TESE, ICSI, hormonal treatment, imaging, and multispecialty reviews are difficult to sustain for middle-income households over time. This is especially restrictive because the clinically preferred model now spans endocrinology, urology, genetics, psychology, and cardiometabolic follow-up rather than a single prescription encounter. The commercial effect is that comprehensive care remains concentrated in tertiary centers, while many patients receive fragmented or episodic treatment for metabolic syndrome, osteoporosis, and reproductive issues instead of coordinated management.

The market is also restrained by the fertility and testosterone sequencing problem, because early testosterone use can suppress residual spermatogenesis and forces clinicians and families to make timing decisions that may delay one part of care to preserve another. On top of that, the disease-specific pipeline remains thin, so most commercial activity still depends on adapted testosterone formats and fertility technologies rather than a broader wave of dedicated innovation that could justify stronger payer engagement.

Persistent Underdiagnosis and Late Referral in Primary Care

The Klinefelter syndrome treatment market is most constrained by diagnostic inertia in frontline care, because a large share of men never reaches treatment at all even though the condition is relatively common. The Danish nationwide cohort published in 2025 showed that undiagnosed men had materially worse mortality outcomes, and even among diagnosed men a meaningful treatment gap remained despite evidence supporting therapy use. Primary care physicians often face a heterogeneous phenotype instead of a single classic presentation, which means partial or atypical signs can be missed until infertility becomes the first issue serious enough to trigger referral. The evidence base around quality-of-life outcomes also remains thin, and a 2025 systematic review found that only a small fraction of adult studies reported those outcomes, which weakens the practical case for early referral in routine settings.

The market therefore faces a paradox where better prenatal and pediatric pathways are improving future entry, but the much larger existing adult pool is still underdetected and reaches care late. Until primary care recognition improves and referral becomes earlier, the Klinefelter syndrome treatment market will continue to grow below its true treatable prevalence despite steady progress in therapy formats and fertility success.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: TRT Leadership Intact, Fertility Care Rising Faster

Testosterone replacement therapy held 45.1% of the Klinefelter syndrome treatment market share in 2025, which kept it as the leading treatment category because most diagnosed patients ultimately require hormone support for long-term hypogonadism management. Long-acting injectable testosterone remained the clinical anchor within TRT, but oral and subcutaneous options are expanding the prescriber base and lowering the need for clinic-dependent administration. Transdermal gels keep an important role in pubertal initiation because flexible dose escalation fits the gradual nature of adolescent hormonal induction better than large depot exposure. Intranasal testosterone and implantable pellets remain smaller niches, but they help broaden the treatment toolkit for patients who need different dosing patterns or adherence support. The Klinefelter syndrome treatment market also includes supportive and developmental therapies that generate recurring demand because language and neurodevelopmental issues remain common across the patient journey.

The market size for fertility treatment is projected to grow at 7% CAGR from 2026 to 2031, which makes it the fastest-expanding treatment category even though it starts from a smaller revenue base. That growth is tied to the normalization of micro-TESE plus ICSI, wider use of hormonal optimization before sperm retrieval, and stronger fertility counseling earlier in the patient pathway. Evidence supporting cryopreservation as a clinically workable alternative to same-cycle fresh use reduces scheduling friction and helps fertility programs serve more patients with less procedural urgency. Surgical care and comorbidity management add another layer of procedure-based revenue, especially when fertility workups uncover broader endocrine and reproductive needs that require coordinated intervention. The result is that fertility care is not replacing TRT within the Klinefelter syndrome treatment market, but instead extending the lifetime sequence of care by adding a high-value phase before or alongside ongoing hormonal treatment.

By Route of Administration: Injectables Still Lead, Oral Use Builds Momentum

Injectables accounted for 49.2% of the Klinefelter syndrome treatment market size in 2025, reflecting the long-standing preference for testosterone undecanoate and other depot formulations that deliver stable hormonal exposure with less frequent clinic visits. This route remains deeply embedded in institutional endocrinology practice, especially in North America and Europe where long-acting intramuscular therapy has a long prescribing history and clear monitoring routines. The route’s staying power also comes from physician familiarity, because once stable patients are established on depot therapy there is less pressure to change unless convenience or tolerability becomes a concern. The Klinefelter syndrome treatment market therefore still relies on injectables as the default route for many adult patients, particularly those entering care late through specialist channels. That entrenched base means route mix will change gradually rather than abruptly, even as new patient cohorts show stronger interest in home-based options.

Oral and buccal testosterone is forecast to grow at 6.5% CAGR through 2031, which makes it the fastest-rising administration route in the Klinefelter syndrome treatment market. KYZATREX has helped that shift because label refinement in 2025 improved the product’s prescribing profile and made oral therapy easier to consider in broader practice settings. Transdermal products keep a stable place in pediatric-to-adult transition care, where smaller dose steps are useful and treatment initiation is often more cautious. Intranasal testosterone appeals to patients who want to avoid depot exposure and injection discomfort, while implantable pellets remain relevant where very long dosing intervals improve persistence. Over time, convenience, flexibility, and home use are likely to take a larger share of the Klinefelter syndrome treatment market, but that growth is building on injectable primacy rather than removing it.

By End User: Hospitals Hold Scale, Specialist Centers Gain Speed

Hospitals captured 58.3% of the Klinefelter syndrome treatment market size in 2025 because initial diagnosis, testosterone initiation, fertility workups, micro-TESE procedures, and multidisciplinary assessment still cluster in tertiary care settings. They remain the center of complex case management because endocrinology, andrology, imaging, reproductive medicine, and surgical support are easier to coordinate inside large institutional systems. Endocrinology clinics represent the next major care node, since they manage routine monitoring for hematologic parameters, hormone response, bone health, and long-term treatment adjustment after initiation. The Klinefelter syndrome treatment market therefore still leans heavily on hospital infrastructure whenever the patient journey includes fertility preservation, surgery, or late-stage diagnosis with multiple comorbidities. This structure supports hospital revenue share even as parts of TRT monitoring gradually move into less intensive settings.

Fertility and urology centers are projected to expand at 6.3% CAGR through 2031, making them the fastest-growing end-user group in the market. Their rise reflects growing awareness that infertility is often the key moment when men with Klinefelter syndrome finally enter specialized care, and it also reflects higher micro-TESE and ICSI volumes. The October 2024 combination of Hamilton Thorne and Cook Medical Reproductive Health under Astorg strengthens this channel further by creating a more integrated global supplier base for IVF laboratory instruments and consumables. Home-based follow-up is also growing as oral and self-injection formats spread, although testosterone’s controlled-substance status in the United States still limits how far virtual care can replace in-person initiation and monitoring. Community pharmacies and imaging services remain the smaller tail of the Klinefelter syndrome treatment market, but they grow steadily as overall treatment prevalence rises and surveillance becomes more routine.

By Age Group: Adults Lead Today, Adolescents Expand Lifetime Value

Adults represented 51.1% of demand in 2025, which reflects the continuing reality that many patients in the Klinefelter syndrome treatment market first present during infertility evaluation in their late 20s or 30s. Adult entry also remains linked to formal confirmation of hypogonadism, which keeps hormonal treatment tied to specialist evaluation even when symptoms may have been present for years before diagnosis. A 2025 clinical paper also noted that some older patients with longer AR exon 1 CAG repeat length may merit treatment despite testosterone values that appear close to normal, which suggests that strict thresholds can still miss symptomatic adults. This supports continued adult demand in the Klinefelter syndrome treatment market because a large diagnosed but undertreated population still exists even in mature healthcare systems. Adults are therefore likely to remain the largest revenue group through the forecast period, even as earlier detection improves in younger cohorts.

Adolescents are expected to grow at 6.3% CAGR from 2026 to 2031, which makes them the fastest-expanding age segment in the Klinefelter syndrome treatment market. Their strategic importance is greater than their current revenue base because this is the stage when puberty support, fertility counseling, and long-term treatment habits are established. Japan’s 2025 DSD guidance recommends structured puberty assessment from age 9 and hormonal treatment from age 12 for confirmed hypogonadism, which materially widens the adolescent treatment-entry window. Children remain the smallest group, but prenatal and early genetic identification is creating a more visible cohort that can enter speech, psychological, and developmental support years before hormone therapy begins. As these younger cohorts mature, they are likely to enter the Klinefelter syndrome treatment market with stronger disease awareness, earlier surveillance, and more deliberate fertility planning than older adults who were diagnosed late.

Geography Analysis

North America held 45.2% of the Klinefelter syndrome treatment market share in 2025, making it the largest regional contributor because the United States combines high testosterone use, advanced fertility infrastructure, and early uptake of new oral and self-injection formats. The 2025 FDA label refinements for KYZATREX and the continued positioning of XYOSTED support broader prescribing confidence and make home-centered follow-up more practical for selected adult patients. The United States remains the core national engine inside the Klinefelter syndrome treatment market because it has the deepest product availability and the strongest mix of endocrinology, reproductive medicine, and telehealth channels. Canada adds support through structured referral systems, while Mexico contributes a smaller share due to more limited rare-disease support and lower treatment intensity.

Europe is the second-largest region in the Klinefelter syndrome treatment market, supported by established clinical guidance, disciplined follow-up norms, and reimbursement structures that keep diagnosed patients in care. France and Germany stand out because reimbursed hormonal treatment and specialist access reduce interruption risk in long-term management, which gives the region a more predictable treatment base. Fertility centers across Germany, the United Kingdom, France, Italy, and Spain are also strengthening the region’s role as micro-TESE becomes more routine in azoospermic Klinefelter syndrome patients. Europe’s clinical position is reinforced by continued attention to early fertility evaluation and long-term endocrine surveillance, both of which raise lifetime treatment depth inside the Klinefelter syndrome treatment market.

Asia-Pacific is projected to grow at 5.8% CAGR from 2026 to 2031, making it the fastest-growing region in the Klinefelter syndrome treatment market. Japan is central to that growth because the 2025 pediatric endocrine guidance formalized structured puberty monitoring and earlier hormonal initiation, which can bring patients into care years ahead of prior practice. Across East Asia, wider prenatal and pediatric screening is gradually improving early entry, while large adult underdiagnosed populations still leave meaningful room for future conversion into treatment. The Middle East and Africa remains a nascent part of the Klinefelter syndrome treatment market, although fertility awareness and specialist center expansion in GCC countries are creating early procedure demand. South America, led by urban centers in Brazil and Argentina, continues to face cost barriers and weaker policy support, which limits treatment penetration despite improving reproductive healthcare capacity.

Competitive Landscape

The Klinefelter syndrome treatment market remains moderately fragmented because care is spread across branded testosterone products, generic hormonal therapies, fertility procedures, developmental support services, and specialist monitoring rather than a single disease-specific platform. Competition within testosterone therapy is shaped less by molecule novelty and more by delivery format, patient convenience, and the ability to keep men on treatment over long periods. Companies tied to oral capsules, transdermal systems, long-acting injections, and self-injection devices are therefore competing on adherence and prescribing ease instead of breakthrough efficacy differences. The Klinefelter syndrome treatment market also shows a split structure, where hormone therapy is broad and fragmented while selected fertility equipment categories are moving toward tighter concentration[3]Astorg, “Astorg Completes Take-Private of Hamilton Thorne and Concurrent Acquisition of Cook Medical Reproductive Health,” Astorg, astorg.com..

A clear strategic move came in October 2024, when Astorg completed the take-private of Hamilton Thorne and the concurrent acquisition of Cook Medical Reproductive Health, creating a larger integrated supplier across IVF laboratory consumables and equipment. That deal matters for the Klinefelter syndrome treatment market because fertility and urology centers need high-precision tools for sperm retrieval and laboratory handling, and integrated supply can improve workflow and procurement consistency. Another strategic move is Marius Pharmaceuticals’ continuing effort to build oral testosterone around a cleaner regulatory profile after the 2025 KYZATREX label revision, which supports broader physician adoption and could widen use beyond specialist settings. A third move comes from XY Therapeutics, whose Phase 2a program targeting the RANKL/RANK/OPG pathway remains one of the few visible attempts to create disease-specific differentiation in male infertility that includes Klinefelter syndrome populations.

The thin innovation pipeline is still a defining feature of the Klinefelter syndrome treatment market, because most revenue today depends on optimizing known testosterone and assisted reproduction tools rather than introducing new disease-specific products. This keeps the commercial field open to many participants, but it also limits pricing power and makes execution on access, adherence, and service delivery more important than pure research depth. Companies that reduce friction around treatment persistence are likely to gain most, since the Danish 2025 cohort showed better survival outcomes among treated men while many diagnosed patients still remained untreated. The Klinefelter syndrome treatment market therefore rewards firms that can keep patients inside care pathways across fertility decisions, endocrine follow-up, and cardiometabolic surveillance rather than simply win an initial prescription. Overall competition is unlikely to consolidate sharply at the full-market level in the near term, because treatment remains multidisciplinary and the patient journey still crosses several provider and product categories.

Klinefelter Syndrome Treatment Industry Leaders

Pfizer Inc.

AbbVie Inc.

Merck KGaA

Ferring Pharmaceuticals

Endo Pharmaceuticals Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Hikma Pharmaceuticals PLC and Marius Pharmaceuticals (Marius) have partnered through a licensing agreement to bring KYZATREX (testosterone undecanoate) CIII capsules to the Canadian market. KYZATREX is an oral prescription medication designed to help adult men with testosterone replacement therapy, specifically for those dealing with conditions caused by low or absent levels of natural testosterone, known as male hypogonadism.

- July 2025: The FDA revised the prescribing information for Marius Pharmaceuticals' KYZATREX (testosterone undecanoate) oral capsules, removing the boxed warning for blood pressure increases and updating venous thromboembolism guidance, significantly lowering the prescribing barrier for primary care physicians managing KS-related hypogonadism. This label change is expected to accelerate oral TRT adoption in the United States.

Global Klinefelter Syndrome Treatment Market Report Scope

As per the scope of the report, Klinefelter syndrome treatment involves managing symptoms and associated health issues since there is no cure for the genetic condition itself. The primary approach typically includes testosterone replacement therapy to address testosterone deficiency, support for speech, language, and learning difficulties, fertility options such as assisted reproductive technologies, and psychological support.

The Klinefelter syndrome treatment market is segmented by treatment type into testosterone replacement therapy, which includes injectable testosterone, transdermal testosterone, oral/buccal testosterone, intranasal testosterone, and implantable testosterone. It also includes fertility treatment, comprising pre-treatment hormonal optimization, surgical sperm retrieval, assisted reproductive technology, and donor sperm pathway. Additionally, supportive and developmental therapies, as well as surgical and comorbidity management, are part of the segmentation. By route of administration, the market is categorized into injectable, transdermal, oral/buccal, intranasal, and implantable methods. By end user, the market is segmented into hospitals, endocrinology clinics, fertility and urology centers, home-based care and telehealth monitoring, and other end users. By age group, the market is divided into children, adolescents, and adults. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Testosterone Replacement Therapy | Injectable Testosterone |

| Transdermal Testosterone | |

| Oral / Buccal Testosterone | |

| Intranasal Testosterone | |

| Implantable Testosterone | |

| Fertility Treatment | Pre-treatment hormonal optimization |

| Surgical sperm retrieval | |

| Assisted reproductive technology | |

| Donor sperm pathway | |

| Supportive and Developmental Therapies | |

| Surgical and Comorbidity Management |

| Injectable |

| Transdermal |

| Oral / Buccal |

| Intranasal |

| Implantable |

| Hospitals |

| Endocrinology clinics |

| Fertility and urology centers |

| Home-based care and telehealth monitoring |

| Other End Users |

| Children |

| Adolescents |

| Adults |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Testosterone Replacement Therapy | Injectable Testosterone |

| Transdermal Testosterone | ||

| Oral / Buccal Testosterone | ||

| Intranasal Testosterone | ||

| Implantable Testosterone | ||

| Fertility Treatment | Pre-treatment hormonal optimization | |

| Surgical sperm retrieval | ||

| Assisted reproductive technology | ||

| Donor sperm pathway | ||

| Supportive and Developmental Therapies | ||

| Surgical and Comorbidity Management | ||

| By Route of Administration | Injectable | |

| Transdermal | ||

| Oral / Buccal | ||

| Intranasal | ||

| Implantable | ||

| By End User | Hospitals | |

| Endocrinology clinics | ||

| Fertility and urology centers | ||

| Home-based care and telehealth monitoring | ||

| Other End Users | ||

| By Age Group | Children | |

| Adolescents | ||

| Adults | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Klinefelter syndrome treatment market in 2026?

The Klinefelter syndrome treatment market stands at USD 1.48 billion in 2026 and is forecast to reach USD 1.86 billion by 2031 at a 4.65% CAGR.

What is the main factor limiting Klinefelter syndrome treatment adoption?

Persistent underdiagnosis remains the biggest limit, with fewer than half of affected people identified during their lifetime and many adult men entering care only during infertility evaluation.

Which treatment category leads current revenue?

Testosterone replacement therapy is the largest category, holding 45.1% of revenue in 2025 because long-term hypogonadism management remains central after diagnosis.

Which area is growing fastest within care delivery?

Fertility treatment is growing the fastest at 7% CAGR through 2031, supported by micro-TESE plus ICSI and stronger evidence for cryopreserved sperm use.

Why is Asia-Pacific expanding faster than other regions?

Asia-Pacific is projected to grow at 5.8% CAGR through 2031 because updated pediatric guidance and wider early screening are bringing patients into care earlier, especially in East Asia.

What shapes competition in Klinefelter syndrome treatment today?

Competition is driven by adherence-friendly testosterone formats, fertility center capability, and a still-thin disease-specific pipeline, while Astorg's 2024 fertility equipment deal shows rising concentration in selected IVF supply categories.

Page last updated on: