Jet Nebulizers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

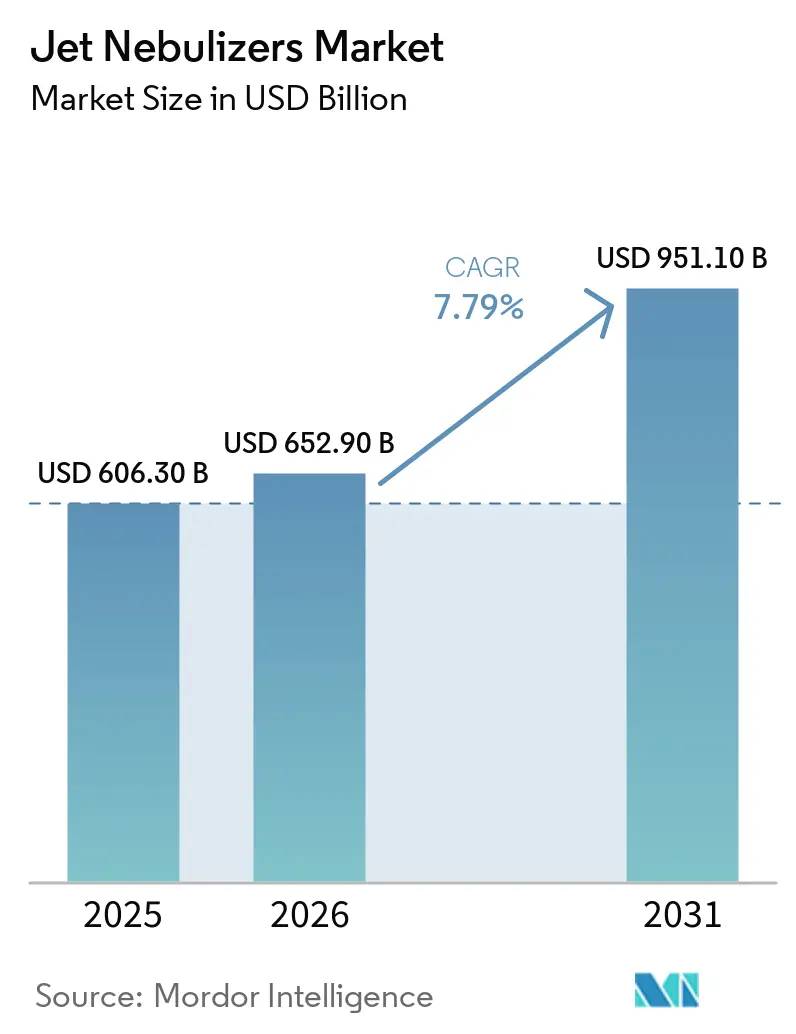

| Market Size (2026) | USD 652.90 Billion |

| Market Size (2031) | USD 951.10 Billion |

| Growth Rate (2026 - 2031) | 7.79% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Jet Nebulizers Market Analysis by Mordor Intelligence

The Jet Nebulizers Market size was valued at USD 606.30 billion in 2025 and is estimated to grow from USD 652.90 billion in 2026 to reach USD 951.10 billion by 2031, at a CAGR of 7.79% during the forecast period (2026-2031).

Demand remains resilient because hospitals, clinics, and home-care providers continue to favor the low acquisition cost, broad drug compatibility, and proven reliability of pneumatic platforms even as vibrating-mesh devices penetrate critical-care units. Breath-actuated configurations scale in pediatric and cystic-fibrosis programs because they curb medication waste and improve lung deposition, while disposable vented circuits gain traction in emergency departments that prioritize infection-control compliance. Government reimbursement reforms in the United States, China, and India shift chronic respiratory care to home settings and expand funding for compressor-based therapy, sustaining hardware replacement cycles and consumables pull-through. Meanwhile, emerging-market price sensitivity and expanding COPD prevalence ensure that generic bronchodilator regimens delivered through jet systems remain the first-line option across low- and middle-income regions.

Key Report Takeaways

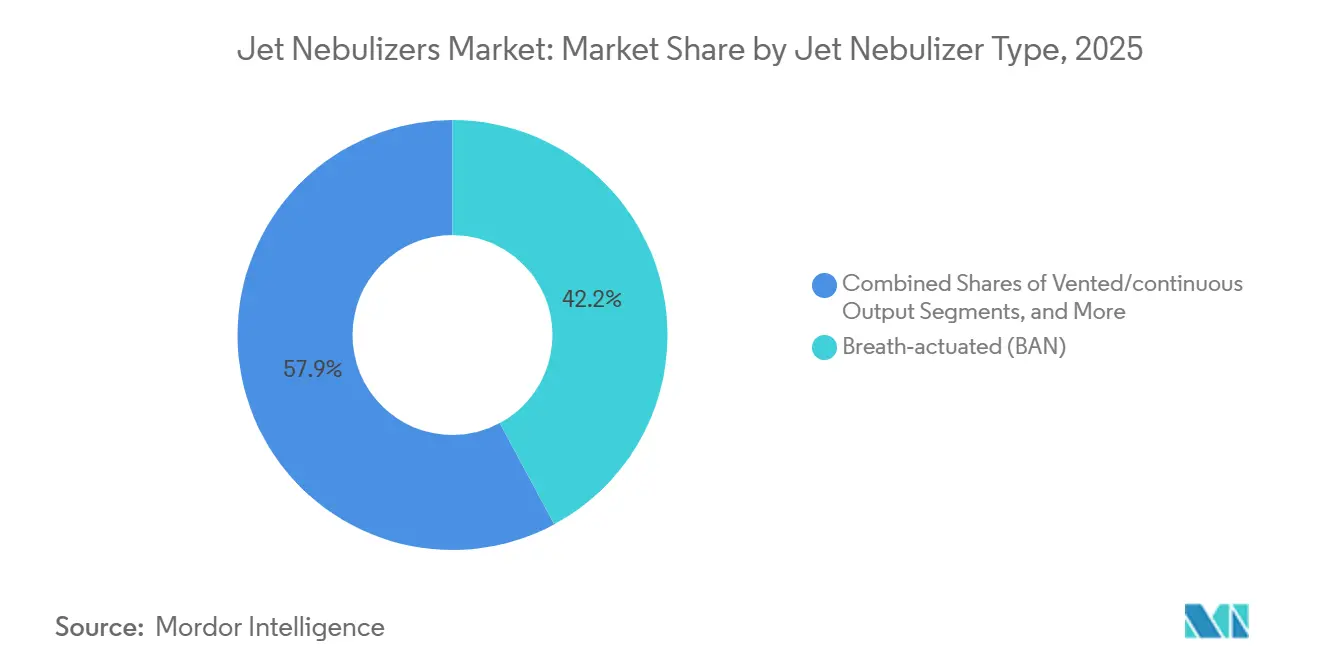

- Breath-actuated systems led with a 42.15% share of the jet nebulizers market in 2025. Vented or continuous-output systems are projected to expand at a 9.14% CAGR through 2031, the fastest among product types.

- COPD applications accounted for 41.65% of 2025 revenue within the jet nebulizers market. Asthma indications are forecast to grow at a 9.35% CAGR to 2031, outpacing all other therapeutic areas.

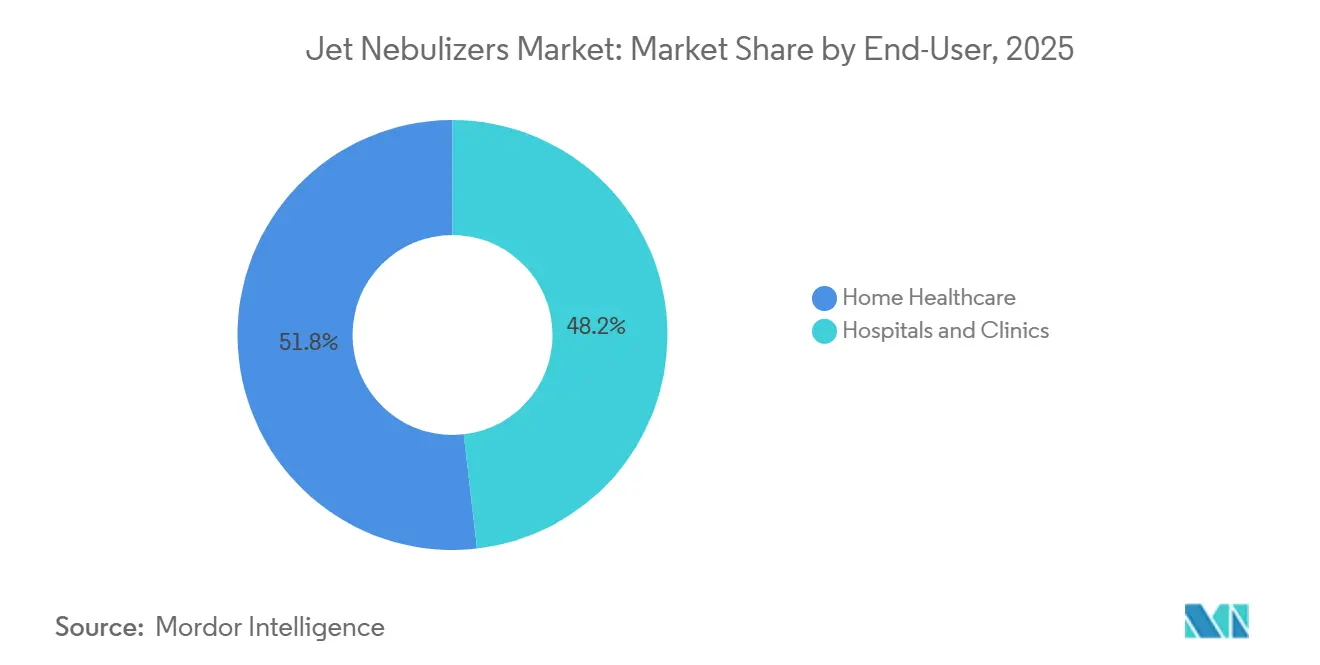

- Hospitals and clinics held 48.19% of the jet nebulizer market share in 2025. Home healthcare is set to advance at a 9.22% CAGR through 2031 as reimbursement rules favor compressor jets.

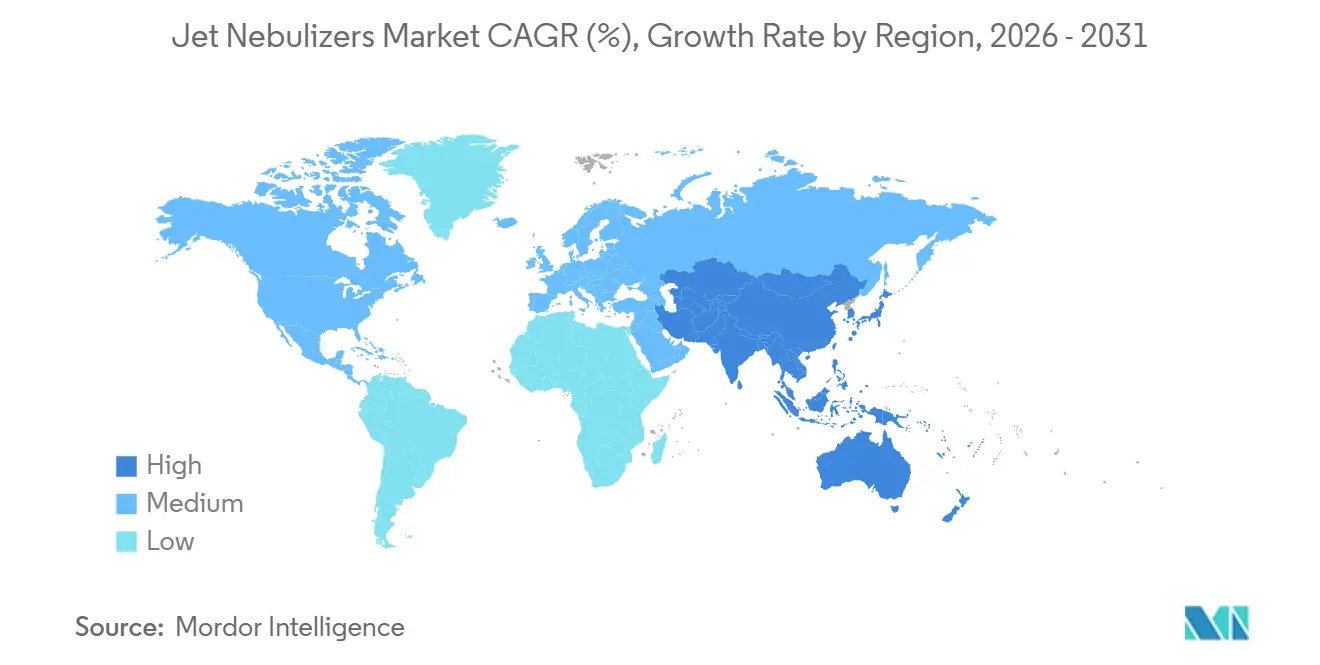

- North America captured 38.19% of 2025 revenue in the jet nebulizers market. Asia-Pacific is positioned for the quickest regional expansion at a 9.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Jet Nebulizers Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising COPD and asthma burden expanding inhaled therapy demand | +1.8% | Global, with APAC accounting for 60% of COPD deaths | Long term (≥ 4 years) |

| Shift to home-based respiratory care and DME coverage supports compressor-based therapy | +1.5% | North America & Europe, spill-over to urban APAC | Medium term (2-4 years) |

| Hospital workflow preference for reliable, low-cost SVNs in acute care | +1.2% | Global, strongest in North America emergency departments | Short term (≤ 2 years) |

| Cost-effectiveness and broad drug compatibility of jet systems vs. Alternatives | +1.0% | Global, pronounced in MEA and South America | Long term (≥ 4 years) |

| Breath-actuated jet designs reduce waste and improve deposition | +0.9% | North America & Europe, early adoption in Japan | Medium term (2-4 years) |

| Drug-device labeling lock-ins for certain inhaled antibiotics sustain installed base | +0.7% | North America & Europe (cystic fibrosis centers) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global COPD and Asthma Crisis Fuels Surge in Inhaled Therapy Demand

Over 500 million individuals suffer from COPD or asthma globally, resulting in 4 million annual fatalities. The Asia-Pacific region accounts for approximately 60% of COPD-related deaths, with China reporting 99.9 million cases and India 55.3 million. Urban air pollution exacerbates these conditions, particularly in megacities like Beijing, Delhi, and Jakarta, which exceed recommended PM2.5 limits. Data from the UK registry spanning 2004-2023 indicates over 10 million diagnosed patients, with stable incidence in affluent areas but rising in underprivileged urban zones. This significant epidemiological burden ensures a consistent demand for the Jet nebulizers market, particularly among individuals facing challenges with metered-dose inhalers or cognitive impairments.

Home Respiratory Care and DME Coverage Boosts Compressor Therapy Adoption

The Centers for Medicare & Medicaid Services, in its 2025 DMEPOS fee schedule, simplified prior authorization for compressor nebulizers, benefiting both suppliers and patients. The Home Health Prospective Payment System's annual device functionality resurveys favor durable wall-powered compressors over battery-dependent mesh units, particularly in rural areas. China's 2024 expansion of insurance coverage for respiratory devices under its "Healthy China 2030" initiative promotes home treatments to reduce hospital readmissions. India's National Health Mission is piloting community distribution of subsidized jet nebulizers to improve adherence and reduce emergency department visits. With compressor jets priced between USD 30-100 and mesh alternatives starting at USD 400, the affordability of compressors is evident.

Emergency Departments Favor Cost-Effective, Reliable SVNs for Acute Care

Emergency departments commonly integrate small-volume jet nebulizers into oxygen flowmeter circuits, benefiting from minimal training and procurement costs. Updated infection-control guidelines for 2024 recommend single-patient reservoir use and daily disinfection, encouraging hospitals to adopt disposable vented circuits. A 2025 survey by the American Association for Respiratory Care revealed that 78% of U.S. emergency rooms prefer vented-jet kits as their primary bronchodilator. While treatment duration with these kits is longer than mesh devices, their disposable kit price of USD 5-15 aligns with cost-containment goals in value-based care.

Jet Nebulizers Outshine Alternatives in Cost-Effectiveness and Drug Compatibility

Jet nebulizers efficiently accommodate bronchodilators, corticosteroids, mucolytics, and antibiotics, streamlining pharmacy operations. A 2024 pharmacoeconomic analysis across five European health systems found jet-based COPD treatments to be the most cost-effective over a decade, due to their compatibility with generic drugs and lower procurement costs. In regions like Sub-Saharan Africa and Latin America, budget constraints and unreliable cold chains for biologics make pneumatic compressors the preferred choice for essential respiratory care.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Infection-control concerns and aerosolization risks in clinical settings | -0.9% | Global, most acute in North America & Europe hospital settings | Short term (≤ 2 years) |

| Competition from vibrating mesh nebulizers in hospitals | -1.1% | North America & Europe critical-care units, expanding to APAC | Medium term (2-4 years) |

| EU MDR Transition/Recertification Burden Curtails Legacy SKUs | -1.8% | Europe | Medium term (2-4 years) |

| Performance Variability/Residual Volume in Jets Complicates Dose Consistency | -0.9% | Global, most acute in North America & Europe hospital settings | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Infection-Control Concerns and Aerosolization Risks in Clinical Settings

In 2024, consensus statements emphasized that continuous-output jets generate aerosol plumes capable of transporting pathogens, including SARS-CoV-2, for up to 30 minutes in poorly ventilated rooms. In response, hospitals are investing in disposable circuits and implementing negative-pressure rooms. These measures, while enhancing safety, increase per-treatment costs and reduce the cost-efficiency of jets. Outpatient clinics with limited ventilation are restricting nebulizer use, constraining market growth outside acute care.

Competition From Vibrating Mesh Nebulizers in Hospitals

Mesh platforms complete treatments in as little as five minutes, significantly reducing caregiver time. They integrate seamlessly into ventilator circuits, maintaining uninterrupted breaths, which aligns well with critical-care workflows. A 2025 survey revealed that 62% of European ICUs have adopted mesh devices as the primary delivery system for bronchodilators in mechanically ventilated patients. Although retail prices are higher, procurement teams prioritize efficiency gains, redirecting capital budgets away from jet replacements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Jet Nebulizer Type: Breath-Actuated Systems Lead, Vented Designs Accelerate

In 2025, breath-actuated systems captured 42.15% of the Jet nebulizers market share, driven by their precise dosing capabilities in therapies for cystic fibrosis and bronchiectasis. These systems use mechanical valves that activate only during inhalation, enhancing the delivered dose while reducing cabin contamination. The market for breath-actuated jet nebulizers is expected to grow steadily as clinicians value their reduced wastage and compatibility with high-cost antibiotics. However, competitive pricing pressures are prompting hospitals to explore mid-priced breath-enhanced models as part of inventory optimization strategies.

Vented or continuous-output jets, though less advanced, are projected to grow at a 9.14% CAGR through 2031. This growth is supported by hospital infection-control policies that favor single-use kits to reduce cross-contamination. Disposable versions simplify sterilization compliance and decrease nursing labor, making them a preferred choice for emergency department stocking.

By Application: COPD Anchors Revenue, Asthma Drives Growth

In 2025, COPD accounted for 41.65% of the Jet nebulizers market revenue. The chronic nature of COPD, frequent exacerbations, and a large patient base in countries like China and India drive the demand for these devices. Many elderly COPD patients face challenges with the coordination required for metered-dose inhalers, further reinforcing the reliance on jet nebulizers. Additionally, hospitals' bulk stocking of generic bronchodilators in vials ensures consistent demand for compressor circuits. Asthma is expected to be the fastest-growing application, with a projected 9.35% CAGR. This growth is fueled by the increasing adoption of pediatric home therapy and the need for nebulization of inhaled corticosteroid-bronchodilator combinations.

By End-User: Hospitals Dominate, Home Healthcare Surges

In 2025, hospitals and clinics contributed 48.19% of the device's revenue, reflecting their established protocols in emergency and ICU settings that prioritize small-volume jets for rapid bronchodilation. Procurement decisions are influenced by acquisition costs and compatibility with wall-mounted oxygen, solidifying jet nebulizers as a primary choice despite longer treatment durations. The industry also benefits from recurring bulk orders for disposable kits, which align with updated infection-control standards. Home healthcare is experiencing significant growth, with a 9.22% CAGR projected through 2031. This expansion is driven by reimbursement updates, particularly in the U.S. and China, which have reduced the financial burden of compressor platforms.

Geography Analysis

In 2025, North America accounted for 38.19% of the revenue, supported by Medicare Part B coverage and a widespread adoption of small-volume jet protocols in emergency departments. With approximately 16 million U.S. adults affected by COPD, there is consistent demand for bronchodilator kits. However, hospital consolidations and a shift to value-based payment models are limiting volume growth, as providers increasingly focus on preventive care to reduce readmissions. While Canada offers partial reimbursements for compressor platforms, its provincial formularies prioritize generic albuterol to manage drug costs. This focus restricts the adoption of premium antibiotic-device bundles. In Mexico, while the Instituto Mexicano del Seguro Social provides coverage for chronic respiratory diseases, a significant 40% of the population remains uninsured, hindering broader market penetration.

Asia-Pacific emerges as the fastest-growing region, with a 9.41% CAGR projected through 2031. This growth is primarily driven by expanding public insurance schemes in China and India, which are enhancing access to medical devices. China's "Healthy China 2030" initiative is broadening reimbursements, and pilot programs in India's tier-2 cities are redirecting substantial patient volumes from hospital settings to home care. Additionally, air quality issues in major cities are intensifying disease severity, leading to increased prescriptions for nebulized rescue therapies. Japan's aging demographic ensures steady demand, though stringent price controls limit profit margins. Meanwhile, universal coverage and a rising prevalence of asthma in urban areas are driving moderate growth in South Korea and Australia. In contrast, countries like Indonesia, Thailand, and Vietnam are highly price-sensitive, showing a preference for economy-grade compressors and disposable circuits.

Europe's market dynamics are varied. With tighter Medical Device Regulation deadlines set for May 2024, many small manufacturers have been compelled to withdraw non-recertified SKUs, leading to a reduction in product variety and a slowdown in replacements.

Competitive Landscape

The Jet nebulizers market is moderately concentrated, with the five largest vendors, PARI, OMRON, Philips Respironics, Drive DeVilbiss, and Medline, collectively accounting for approximately 50% of global revenue. These companies achieve this through proprietary drug-device pairings and extensive multinational distribution networks. PARI utilizes its eFlow and LC Plus platforms, integrating them into antibiotic labels. Philips Respironics enhances sales by bundling its products with home oxygen concentrators. By 2025, OMRON had surpassed 50 million nebulizer shipments, strengthening its brand presence in pharmacies and both online and offline retail channels.

Regional players such as Yuwell, Rossmax, and Microlife are gaining market share in the Asia-Pacific and Latin American regions. They achieve this by leveraging cost-efficient manufacturing facilities and offering bundled packages with oxygen concentrators. In a strategic initiative, Yuwell entered into a USD 27.2 million equity partnership with Inogen in January 2025, expanding its global footprint and enhancing its research and development capabilities. Meanwhile, start-ups are targeting niche segments: AeroRx Therapeutics is advancing AERO-007, a nebulized LABA/LAMA for COPD. The company aims to pair this formulation with a breath-actuated jet, positioning it as a first-line maintenance therapy.

Jet Nebulizers Industry Leaders

Drive DeVilbiss Healthcare Inc.

OMRON Healthcare, Inc.

PARI Respiratory Equipment, Inc.

Koninklijke Philips N.V.

GE Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: PARI obtained a European patent for MOLBREEVI, pairing its eFlow mesh platform with an inhaled antibiotic for chronic Pseudomonas treatment in cystic-fibrosis patients.

- October 2025: AeroRx Therapeutics closed a USD 21 million Series A round led by Avalon BioVentures to fund late-stage trials of inhaled AERO-007, the first nebulized LABA/LAMA combination under development for COPD maintenance.

- January 2025: Yuwell acquired a USD 27.2 million investment from Inogen, forming a strategic alliance to co-develop portable oxygen concentrators and nebulizers for North American and European launch.

Global Jet Nebulizers Market Report Scope

As per the scope of the report, a jet nebulizer is a medical drug delivery device that uses pressurized gas to convert liquid medication into a fine mist or aerosol that a patient can easily breathe directly into their lungs.

The jet nebulizer market is segmented by type, application, end-user, and geography. By type, the market includes breath-actuated (BAN), breath-enhanced (BE), and vented/continuous output nebulizers. By application, it is segmented into asthma, COPD, cystic fibrosis, and other respiratory issues (e.g., bronchiolitis, bronchiectasis). By end-user, the market includes hospitals & clinics, home healthcare, and ambulatory, urgent care, & emergency centers. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Breath-actuated (BAN) |

| Breath-enhanced (BE) |

| Vented/continuous output |

| Asthma |

| COPD |

| Cystic Fibrosis |

| Other Respiratory (e.g., bronchiolitis, bronchiectasis) |

| Hospitals & Clinics |

| Home Healthcare |

| Ambulatory/Urgent Care/Emergency Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Jet Nebulizer Type | Breath-actuated (BAN) | |

| Breath-enhanced (BE) | ||

| Vented/continuous output | ||

| By Application | Asthma | |

| COPD | ||

| Cystic Fibrosis | ||

| Other Respiratory (e.g., bronchiolitis, bronchiectasis) | ||

| By End-user | Hospitals & Clinics | |

| Home Healthcare | ||

| Ambulatory/Urgent Care/Emergency Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the Jet nebulizers market be by 2031?

It is projected to reach USD 951.1 million by 2031, expanding at a 7.79% CAGR from 2026 to 2031.

Which product type commands the biggest revenue share?

Breath-actuated systems led with 42.15% Jet nebulizers market share in 2025.

Which segment is growing the fastest?

Vented or continuous-output jets are forecast to post a 9.14% CAGR through 2031.

Which end-user setting shows the quickest uptake?

Home healthcare is advancing at a 9.22% CAGR as Medicare and Asian public insurers expand coverage.

Which region is expected to grow most rapidly?

Asia-Pacific is projected to record a 9.41% CAGR thanks to China's and India's reimbursement reforms.

How concentrated is competition?

The top five suppliers control roughly half of revenue, signaling moderate concentration.

Page last updated on: