Japan Robotics CNC Turning Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

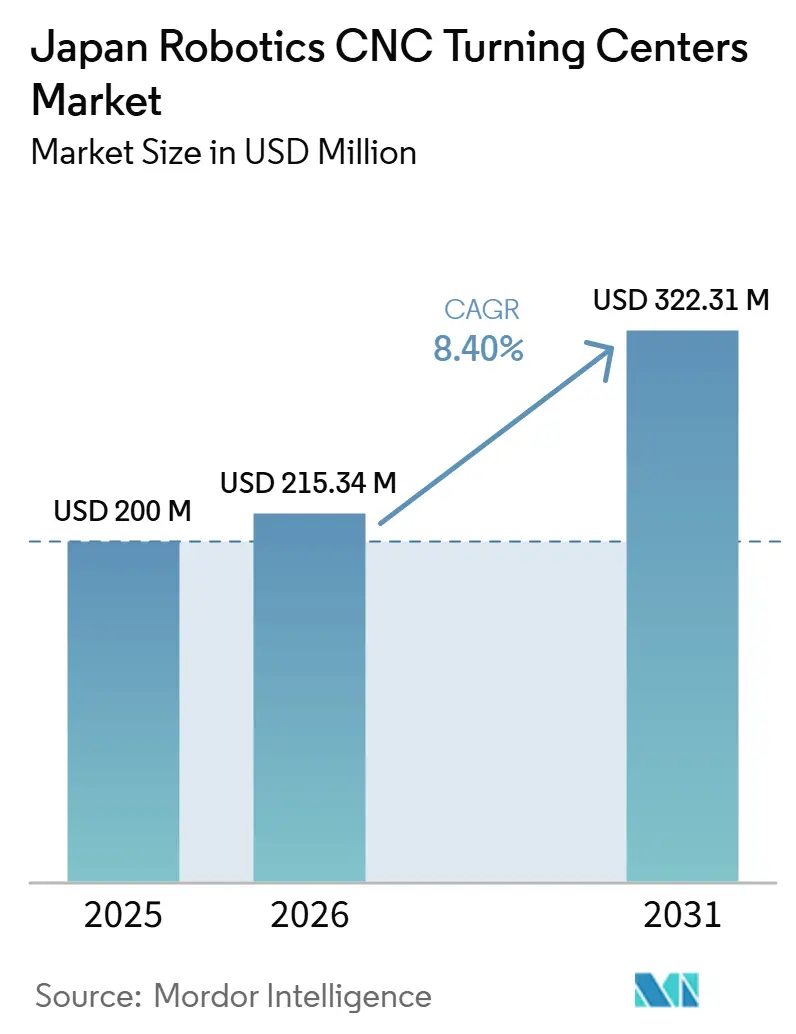

| Base Year Market Size (2025) | USD 200 Million |

| Market Size (2026) | USD 215.34 Million |

| Market Size (2031) | USD 322.31 Million |

| Growth Rate (2026 - 2031) | 8.40% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Robotics CNC Turning Centers Market Analysis by Mordor Intelligence

The Japan Robotics CNC Turning Centers Market size is projected to be USD 200 million in 2025, USD 215.34 million in 2026, and reach USD 322.31 million by 2031, growing at a CAGR of 8.40% from 2026 to 2031.

The Japan robotics CNC turning centers market is moving on a stronger footing because manufacturers now face a lasting shortage of skilled labor, and that makes robotic turning cells a practical production requirement rather than an optional upgrade. Policy support also remains important because Society 5.0 and Connected Industries continue to push factories toward connected, data-sharing production systems that fit the design of modern robotic CNC turning cells. Japan entered 2026 with a favorable installed base for upgrades, as NC machines already accounted for more than 93% of output in 2025, creating a broad digital foundation for robotic retrofits and OEM-integrated cells. The Japan robotics CNC turning centers market also benefits from a strong local supply, as Japan produced 38% of global industrial robots, and industry orders at the Japan Robot Association rose sharply in 2025, improving access to equipment and supporting product development by domestic OEMs. Even with this support, high capital costs, price pressure in the mid-tier, and the shortage of integration talent continue to slow deployment, while AI-enabled vision, predictive maintenance, and digital simulation are helping the Japan robotics CNC turning centers market expand into medical, aerospace, and energy applications in addition to automotive demand.

Key Report Takeaways

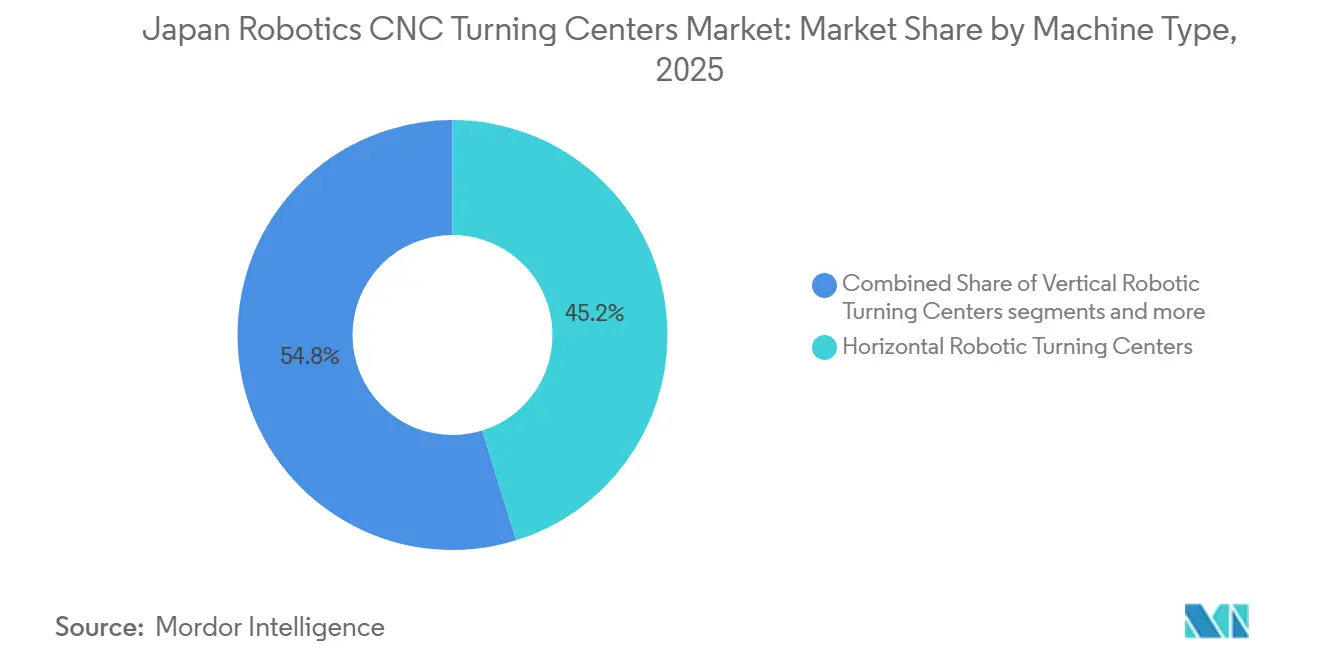

- By machine type, horizontal robotic turning centers led with 45.2% of the Japan robotics CNC turning centers market share in 2025, while multi-tasking robotic turning centers are projected to expand at a 10.2% CAGR through 2031.

- By robot type, articulated robots held 57.6% of the market in 2025, while collaborative robots are forecast to grow at an 11.3% CAGR through 2031.

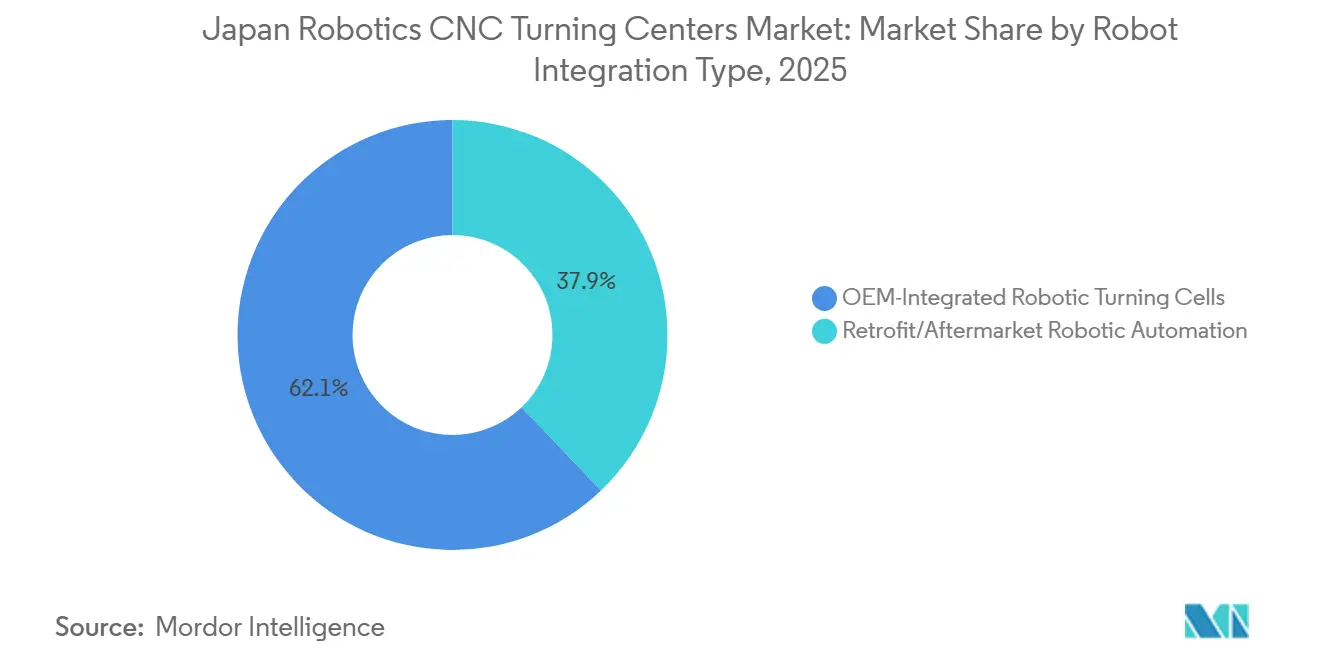

- By robot integration type, OEM-integrated robotic turning cells accounted for 62.1% of the Japan robotics CNC turning centers market size in 2025, while retrofit/aftermarket robotic automation is expected to advance at a 12.4% CAGR through 2031.

- By end-user industry, automotive and commercial vehicles captured 37.6% share in 2025, while medical devices and surgical instruments are set to record the fastest CAGR at 13.2% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Robotics CNC Turning Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demographic Labor Shortages Driving Automation | +2.1% | National, with acute concentration in automotive manufacturing hubs such as Aichi, Shizuoka, and Gunma | Short term (≤ 2 years) |

| EV Transition Driving Robotic Retooling | +1.8% | National, led by the Toyota City cluster in Chubu and Nissan and Honda facilities in Kanto. | Medium term (2-4 years) |

| Society 5.0 Supporting Industrial Automation | +1.5% | National, with stronger traction in large enterprises and Tier 1 suppliers | Medium term (2-4 years) |

| Machine Tool OEMs Embedding Robotics Natively | +1.2% | National, with early adoption in aerospace and medical device clusters | Short term (≤ 2 years) |

| Smart-CNC Penetration Supporting Robotic Upgrades | +0.7% | National, across the installed base of NC-equipped turning centers | Medium term (2-4 years) |

| Strong Domestic Machine Tool and Robotics Ecosystem Driving Innovation | +0.5% | National, with concentration in Chubu, Kinki, and Kanto industrial belts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demographic Labor Shortages Driving Automation

Japan’s manufacturing employment stood at 10.46 million in 2024, and the decline in the working-age population has kept the labor pool under steady pressure even as industrial output remains active.[1]Ministry of Health, Labour and Welfare, “2025 Monozukuri White Paper,” Ministry of Health, Labour and Welfare, mhlw.go.jp Shortages remain most severe in skilled machining and tooling roles, which directly increases the appeal of robotic turning cells that can stabilize loading and unloading and improve repeatability on the shop floor.[2]Organisation for Economic Co-operation and Development, “Artificial Intelligence and the Labour Market in Japan,” OECD, oecd.org The IMF also reported that around half of the surveyed firms in 2024 lacked sufficient qualified full-time employees, indicating that the strain is not limited to a small part of the manufacturing base. In the Japan robotics CNC turning centers market, this shifts purchase decisions away from a narrow payback calculation and toward production continuity. It also means that demand is less tied to short-term order cycles because factories still need to protect throughput even when hiring does not improve.

EV Transition Driving Robotic Retooling

Japan’s automotive supply chain is now reworking machining requirements as automakers move further into battery electric production and platform changes. Suzuki began EV production in Japan in fiscal 2026, and Mazda plans to introduce its dedicated battery EV platform in 2027, which keeps capital planning active across component suppliers. Japan already had 132,766 robots operating in the automotive sector by the end of 2023, so the installed automation base is large enough to support upgrades rather than relying solely on greenfield investment.[3] International Monetary Fund, “Japan Labour Market Working Paper,” International Monetary Fund, imf.org The Japan robotics CNC turning centers market gains from this change because EV parts, such as motor shafts and reducer housings, need tighter process control, fewer setups, and more stable surface quality. This keeps demand focused on robotic turning cells with in-process gauging, better repeatability, and stronger multi-tasking capability.

Society 5.0 Supporting Industrial Automation

Japan’s Cabinet Office continues to define Society 5.0 as a national strategy that links AI, IoT, robotics, and the physical production environment into a more connected industrial system. METI’s Connected Industries program translates that vision into factory requirements by stressing real-time data sharing across machines, systems, and enterprises. The June 2025 economic and fiscal policy direction also kept labor shortages and digital technologies linked in public policy, which helped preserve automation as a legitimate route for factory investment. For the Japan robotics CNC turning centers market, this increases the value of machines that support open connectivity and smoother integration with factory software. It also improves the position of vendors that can show proven interfaces, shared data architecture, and easier network-level deployment.

Machine Tool OEMs Embedding Robotics Natively

The Japan robotics CNC turning centers market is also being shaped by a clear move from aftermarket automation toward native OEM integration. Okuma’s ARMROID places the robot within the machine structure and allows motion setup via the CNC interface, reducing the operating burden for shops with limited robotics expertise. Nakamura-Tome’s RoboSync takes a different approach by enabling transfers between turning centers and related equipment from different manufacturers, supporting mixed-machine environments. FANUC’s M-810 Machining Robot widened the scope for machining tasks on heavier steel workpieces after commercial shipments started in August 2025. Together, these moves reduce integration friction and allow OEMs to capture more of the value that previously sat with third-party system integrators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Costs | -1.9% | National, with disproportionate impact on SME machine shops in Nagano, Niigata, and Gifu precision machining clusters | Short term (≤ 2 years) |

| Shortage of Robotics Integration and Programming Talent | -1.5% | National, with broad understaffing across technical domains | Medium term (2-4 years) |

| Slow Automation Adoption by Aging SME Machine Shops | -1.1% | National, concentrated in small-batch precision subcontractors with fewer than 50 employees. | Medium term (2-4 years) |

| Rising Price Competition from China and South Korea | -0.8% | National, most acute in the mid-tier robotic turning cell range | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Costs

A robotic CNC turning cell still demands a high upfront investment because the machine, robot, vision system, safety equipment, and software all add to the purchase price. This matters most in Japan’s dense base of small precision shops, many of which operate with limited free cash flow even when their technical capability is strong. OECD work on SME automation also shows that financing constraints remain one of the most common barriers to adoption. In the Japan robotics CNC turning centers market, the result is slower decision-making among first-time automation buyers and a greater preference for smaller upgrades over full-cell replacement. That keeps the addressable demand real, but it delays conversion from interest to installed capacity.

Shortage of Robotics Integration and Programming Talent

METI projected in 2025 that Japan could face a shortfall of 3.26 million workers in the AI and robotics fields by 2040 if current training trends continue. The Linux Foundation reported that 70% to 73% of Japanese organizations were understaffed across major technology domains in 2025, and the OECD found that the shortage of AI-related talent was the most important operational issue for 62.4% of Japanese companies in 2023. This creates a difficult situation for the Japan robotics CNC turning centers market because the same labor shortage that pushes factories toward automation also limits deployment and maintenance capacity. Orders can be placed, but commissioning still depends on programmers, integration engineers, and support specialists. Unless training and subsidy-backed skill development widen meaningfully, this bottleneck will continue to slow the pace of rollout through much of the forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Multi-Tasking Formats Redefine the EV-Era Turning Cell

Horizontal robotic turning centers held 45.21% of the market in 2025, which made them the largest machine type in the Japan robotics CNC turning centers market share mix. Their lead came from their strong fit with high-volume automotive component production, where horizontal spindle orientation supports stable chip evacuation, compact robotic loading layouts, and long-established process routines. This format also matched the installed production logic of many Tier 1 suppliers, so replacement and upgrade cycles continued to favor horizontal configurations. Vertical robotic turning centers played a narrower but stable role, handling heavier, larger-diameter parts such as brake discs, flywheels, and industrial flanges. The other category, including Swiss-type and gang-tool systems, remained important in micro-precision work, where bar-fed consistency and small-part tolerances support higher-value robotic investments.

Multi-tasking robotic turning centers are projected to grow at a 10.21% CAGR through 2031, which makes them the fastest-growing machine type in the Japan robotics CNC turning centers market. The reason is straightforward: EV drivetrain parts often require several operations in a single setup, and each avoided transfer reduces the risk of alignment errors on tolerance-sensitive components. Yamazaki Mazak’s QRX-50MSY, introduced in October 2025 for high-volume EV drivetrain work, showed that OEM roadmaps are already aligning with this need. The same shift also extends to non-automotive sectors, as premium applications in aerospace, energy, and other precision fields value fewer setups and greater repeatability. METI’s March 2025 sector vision supports this direction by pushing Japan’s parts and tooling base toward higher-value-added customer sectors, which naturally favors multi-tasking platforms.

By Robot Type: Cobots Unlock the SME Market That Articulated Robots Cannot Reach

Articulated robots held 57.63% share in 2025, and that leadership reflected their established role in high-volume CNC machine tending across automotive and other repetitive production environments. JARA reported that machining-application robot shipments rose 47.9% year over year to 6,332 units in the fourth quarter of 2025, which confirmed sustained demand in this application class. Articulated robots remain the reference option when payload range, flexible movement, and reliable cycle performance matter more than a minimal footprint. Gantry and Cartesian robots still hold a niche in transfer-line work where linear precision and direct load handling carry more value than multi-axis flexibility. In the Japan robotics CNC turning centers market, this keeps articulated systems strongest where factories run higher repetition, larger part flow, and structured layout discipline.

Collaborative robots are forecast to grow at an 11.26% CAGR between 2026 and 2031, making them the fastest-growing robot type in the Japan robotics CNC turning centers market size outlook. Their growth comes less from replacing articulated robots and more from expanding automation into shops that could not previously justify a fenced robotic cell. Many smaller Japanese machine shops lack floor space, dedicated robot engineers, and the budget for full integration packages. FANUC America’s CRX-3iA launch in April 2026 demonstrated how this category is designed for tight spaces and quick deployment, directly addressing those barriers. That makes cobots important not only because they are simpler to install, but because they open a new user base within the Japan robotics CNC turning centers market that had remained outside the core automation cycle.

By Robot Integration Type: Retrofit Segment Reframes the Installed Base as an Opportunity

OEM-integrated robotic turning cells accounted for 62.14% of the market in 2025, which made them the dominant integration model in the Japan robotics CNC turning centers market. Their appeal is clear because they arrive pre-tested, pre-certified, and aligned with the machine control, reducing commissioning time and simplifying warranty complexity. Shops that lack in-house robotics staff often prefer this route because accountability remains with a single vendor. FANUC’s demonstration of G-code-based cobot programming for CNC machine tending reinforced this advantage by allowing machine operators to work through familiar programming logic. This model also fits well with growing safety and compliance expectations because the integrated system is easier to validate from the start.

Retrofit/aftermarket robotic automation is projected to grow at a 12.37% CAGR through 2031, which makes it the fastest-growing integration type in the Japan robotics CNC turning centers market. Japan’s factories already operate a very large installed base of robots and machine tools, so many users can improve productivity with add-on automation rather than replacing a full turning center. Nakamura-Tome’s RoboSync directly addresses the mixed-machine reality of these shops by supporting transfer across equipment from different manufacturers. That makes retrofit especially relevant in clusters where small and mid-sized firms own workable CNC assets but need a lower-cost path into automation. It also creates room for recurring revenue from software, maintenance, and integration services after the initial sale.

By End-User Industry: Automotive Anchors Volume as Medical Devices Drives Premium Growth

Automotive and commercial vehicles accounted for 37.61% of the Japan robotics CNC turning centers market in 2025, keeping the segment firmly in first place among end-user industries. Japan’s large vehicle production base and deep supplier network continue to support that position, and the sector’s robot stock reached 132,766 units by the end of 2023. This matters because the current retooling cycle covers EV, hybrid, and hydrogen-related component programs, keeping equipment demand active across several powertrain paths. Aerospace and defense, oil and gas, energy, and general industrial machinery also remain relevant because they involve complex precision parts where unit value supports premium automation. Electrical, electronic, and semiconductor equipment is an emerging user group, as turned parts for process equipment demand high roundness and surface quality.

Medical devices and surgical instruments are forecast to grow at a 13.24% CAGR through 2031, which makes them the fastest-growing end-user segment in the Japan robotics CNC turning centers market. Demand in this segment is driven by a mix of domestic demographic pressures, stringent process validation requirements, and the need for repeatable finishing on small, high-precision parts. Bone screws, surgical tools, and minimally invasive device components all require stable dimensional control across diverse part families, which improves the value case for robotic turning. METI’s March 2025 industry vision also identified medical devices as a high-value-added target sector for Japan’s parts industry, providing this end market with policy support and technical relevance. As a result, medical demand adds a premium growth layer to the Japan robotics CNC turning centers market rather than simply increasing unit volume.

Geography Analysis

The Japan robotics CNC turning centers market size stood at USD 215.3 million in 2026, and this single-country market reflects a rare combination of strong robotics production capacity and severe labor pressure in manufacturing. Japan produced 38% of global industrial robots and operated 435,299 robots in domestic factories by 2023, which gave the country one of the deepest industrial automation bases in the world. Demand in the Japan robotics CNC turning centers market closely tracks the country’s industrial geography rather than broad national averages. The Chubu region, especially Aichi, Shizuoka, and Mie, remains central because of its dense concentration of automotive and supplier activity. The Kanto belt supports demand for electronics, precision instrumentation, and semiconductor equipment, while Kansai adds a steady base from general machinery and specialty equipment production.

Nagano and Niigata host some of Japan’s most concentrated groups of small precision-turning subcontractors, especially in micro-precision bar work and specialized lathe operations. These districts matter because they offer one of the clearest openings for retrofit/aftermarket robotic automation integration, even though many firms still face capital and staffing constraints. OECD regional evidence also showed that AI adoption reached 13.8% in Tokyo and remained below 5% in Hokuriku and several rural prefectures, mirroring the uneven pace of automation across industrial areas. METI programs aimed at smart manufacturing and digital adoption, therefore, matter most in these secondary clusters because they help extend investment beyond the largest factory groups.

Japan’s export position also supports domestic technology standards in the Japan robotics CNC turning centers market. NC machine tool exports reached USD 5.4 billion in 2025, which showed that Japanese production quality remained competitive in global markets. China took the largest share of exports, indicating that Japanese producers remain relevant even in highly contested industrial markets. Imports remained much lower at USD 0.45 billion in 2025, and Germany overtook China as the top import source, suggesting that import demand is concentrated in specialized, premium categories rather than mainstream turning center needs. This low import dependence strengthens the position of domestic OEMs and keeps the national market structure relatively defensible through the forecast period.

Competitive Landscape

The Japan robotics CNC turning centers market shows moderate concentration, as a relatively small group of domestic OEMs and robotics suppliers controls much of the machine, control, robot, and integration stack. Competition is no longer centered solely on raw cutting performance, as buyers now place greater value on native automation, vision support, gauging, and connectivity. This favors companies that can deliver a complete cell and a simpler deployment path, especially for customers with limited engineering staff. Okuma has leaned into this direction through ARMROID, which places the robot within the machine footprint and lowers the skill requirement for day-to-day operation. Nakamura-Tome has addressed a different pain point through RoboSync, which targets mixed-machine environments that need smoother material transfer without forcing full equipment replacement.

FANUC has strengthened its strategic position through product and software moves rather than solely through hardware. The start of commercial shipments of the M-810 Machining Robot in August 2025 expanded the range of robotic machining for heavier steel applications. In 2026, FANUC also more closely linked its robotics roadmap to AI through collaborations with NVIDIA and Gemini integration, demonstrating that software-led differentiation is becoming more visible in the Japan robotics CNC turning centers market. These steps matter because they can shorten setup time, support simulation before deployment, and reduce reliance on specialist programmers over time.

There is still open space in lower-cost cells for SME shops and in pre-validated precision solutions for healthcare manufacturing. This gap remains important because many incumbent product structures were built for larger enterprises and established automation buyers. The Japan robotics CNC turning centers market also faces rising pressure from Chinese producers in the mid-tier, where pricing has become more aggressive, and capabilities have improved. South Korean suppliers are also broadening their competitive reach through international expansion, which adds pressure in segments where service depth and global support matter. Even so, Japanese vendors retain a strong home-market position because they combine domestic robotics supply, established machine tool brands, and close alignment with local manufacturing requirements.

Japan Robotics CNC Turning Centers Industry Leaders

DMG MORI Co., Ltd.

Yamazaki Mazak Corporation

FANUC Corporation

Okuma Corporation

Yaskawa Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: FANUC Corporation and Vention announced a strategic collaboration combining FANUC's full industrial and collaborative robot portfolio with Vention's AI-driven MachineMotion platform, enabling CNC machine loading and unloading deployable through a unified design-to-operate environment, reducing system integration lead time for robotic turning cell adoption for manufacturers lacking in-house integrators.

- May 2026: FANUC Corporation announced a strategic collaboration with Google to integrate Gemini enterprise AI into its robot systems, enabling collaborative and industrial robots to receive and execute natural language operational instructions, a step toward zero-code robotic CNC cell programming that directly addresses Japan's robotics talent bottleneck.

- May 2026: FANUC strengthened its collaboration with NVIDIA, incorporating NVIDIA Isaac Sim for photorealistic factory digital twin simulation and NVIDIA Jetson Thor for on-edge AI inference, enabling manufacturers to train and validate robotic CNC turning cell operations virtually before physical deployment, shortening commissioning cycles.

- April 2026: Okuma launched the MULTUS U1000 and MULTUS U2000, compact 5-axis simultaneous turn-mill machines requiring only 8.2 m² of floor space and designed with integrated automation attachment points, directly targeting high-mix, low-volume manufacturers constrained by facility footprint in Japan's dense SME factory environments.

Japan Robotics CNC Turning Centers Market Report Scope

The Japan Robotics CNC Turning Centers Market is Segmented by Machine Type (Horizontal Robotic Turning Centers, Vertical Robotic Turning Centers, and more), by Robot Type (Articulated Robots, and more), by Robot Integration Type (OEM, Retrofit/Aftermarket Robotic Automation), by End-User Industry (Oil, Gas, and Energy, Aerospace & Defense, and more), The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Horizontal Robotic Turning Centers |

| Vertical Robotic Turning Centers |

| Multi-Tasking Robotic Turning Centers |

| Others |

| Articulated Robots |

| Collaborative Robots (Cobots) |

| Gantry/Cartesian Robots |

| OEM-Integrated Robotic Turning Cells |

| Retrofit/Aftermarket Robotic Automation |

| Automotive and Commercial Vehicles |

| Aerospace & Defense |

| Medical Devices and Surgical Instruments |

| Electrical, Electronics and Semiconductor Equipment |

| Oil, Gas, and Energy |

| General Industrial Machinery |

| Others |

| By Machine Type | Horizontal Robotic Turning Centers |

| Vertical Robotic Turning Centers | |

| Multi-Tasking Robotic Turning Centers | |

| Others | |

| By Robot Type | Articulated Robots |

| Collaborative Robots (Cobots) | |

| Gantry/Cartesian Robots | |

| By Robot Integration Type | OEM-Integrated Robotic Turning Cells |

| Retrofit/Aftermarket Robotic Automation | |

| By End-User Industry | Automotive and Commercial Vehicles |

| Aerospace & Defense | |

| Medical Devices and Surgical Instruments | |

| Electrical, Electronics and Semiconductor Equipment | |

| Oil, Gas, and Energy | |

| General Industrial Machinery | |

| Others |

Key Questions Answered in the Report

What is the 2031 value forecast for Japan robotics CNC turning centers?

The market is forecast to reach USD 322.3 million by 2031 from USD 215.3 million in 2026, with an 8.4% CAGR over 2026-2031.

What is driving the adoption of robotic CNC turning cells in Japan?

The main driver is the long-running shortage of skilled manufacturing labor, supported by policy pressure for connected and automated production systems.

Which machine type is growing fastest in Japan?

Multi-tasking robotic turning centers are projected to grow the fastest, at a 10.2% CAGR through 2031, as they reduce setups and support EV-era precision needs.

Which robot type leads current demand?

Articulated robots led in 2025 with 57.6% share because they remain the most proven option for high-volume CNC machine tending.

Which end-user segment is expected to expand the fastest?

Medical devices and surgical instruments are expected to grow the fastest, at a 13.2% CAGR through 2031, driven by stringent precision and validation requirements.

Why are retrofit robotic solutions gaining traction in Japan?

Retrofit systems are growing quickly because many shops already own usable CNC turning assets and need a lower-cost path to automation rather than full machine replacement.

Page last updated on: