Japan Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 7.15 Billion |

| Market Size (2026) | USD 7.46 Billion |

| Market Size (2031) | USD 9.11 Billion |

| Growth Rate (2026 - 2031) | 4.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Printed Circuit Board Market Analysis by Mordor Intelligence

The Japan printed circuit board market size was valued at USD 7.15 billion in 2025 and expected to grow from USD 7.46 billion in 2026 to reach USD 9.11 billion by 2031, at a CAGR of 4.08% during the forecast period (2026-2031). A gradual pivot from commodity multilayer boards to high-layer-count, high-frequency substrates underpins this expansion, with demand driven by artificial-intelligence servers, advanced driver-assistance systems, and nationwide 5G rollouts. Surging domestic output, illustrated by a 113.8% year-over-year jump in January 2025 production, signals robust short-term momentum as fabricators ramp capacity to support original-equipment manufacturers and export customers. Rising capital-expenditure commitments, anchored by Ministry of Economy, Trade and Industry subsidies, are accelerating re-shoring of multilayer and IC-substrate lines while helping local suppliers counter lower-cost Korean and Chinese rivals. At the same time, flexible circuits and high-speed laminates are registering the fastest growth rates because foldable smartphones, wearables, and millimeter-wave telecom gear require thinner dielectrics, finer lines, and tighter tolerances. Competitive intensity remains pronounced, as three incumbents control roughly 60% of high-end capacity while facing pressure from nimble entrants commercializing additive printing and glass-core technologies.

Key Report Takeaways

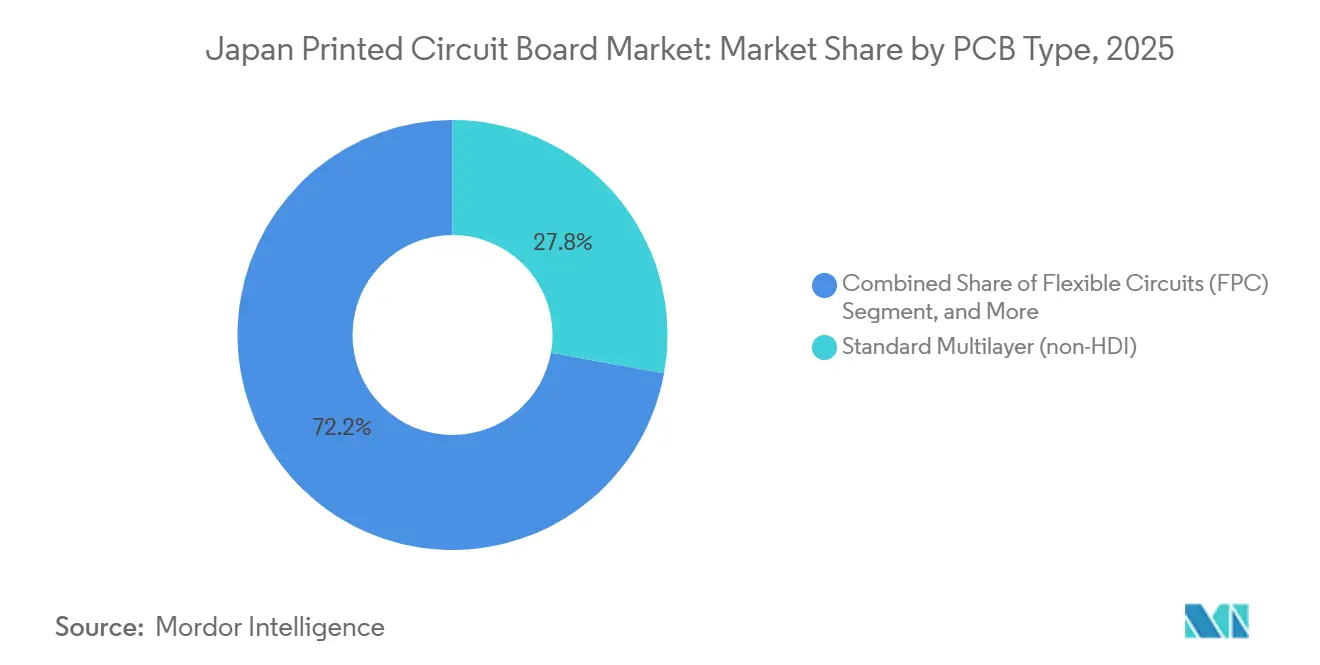

- By PCB type, standard multilayer boards led with 27.84% revenue share in 2025, whereas flexible circuits are forecast to grow at a 5.42% CAGR through 2031.

- By substrate material, FR-4 laminates accounted for 41.87% of the Japan printed circuit board (PCB) market share in 2025, while high-speed, low-loss chemistries are set to expand at a 5.01% CAGR during 2026-2031.

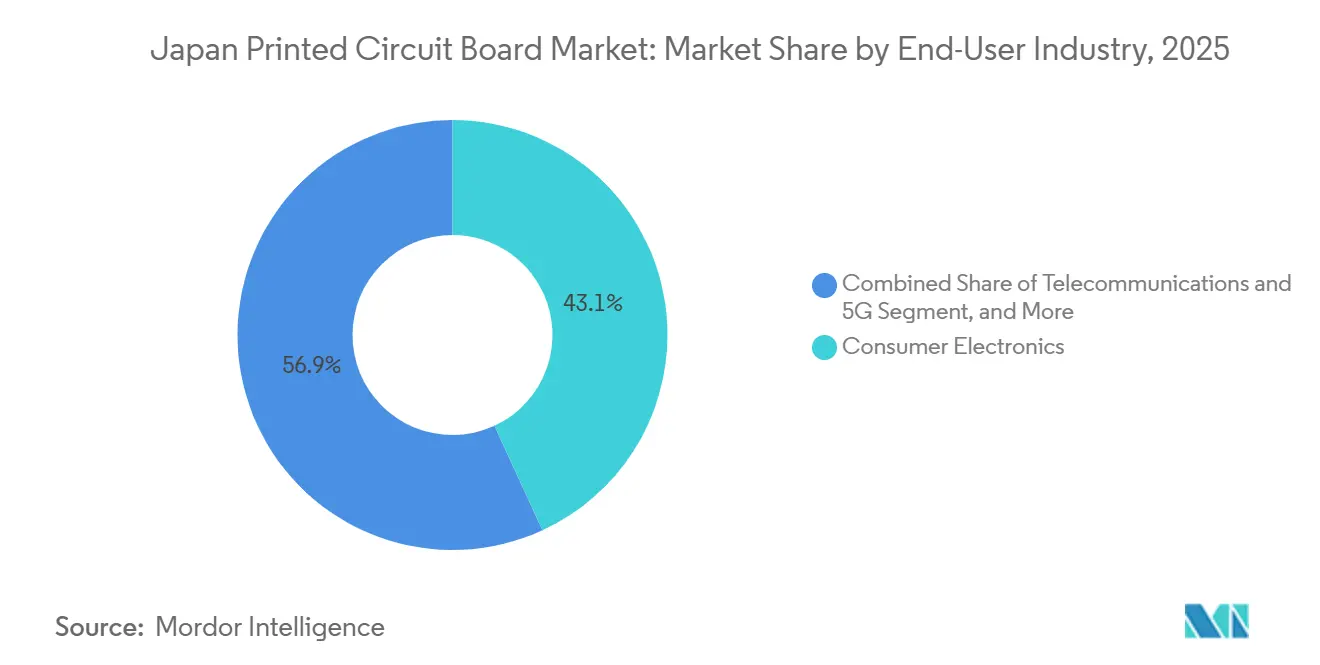

- By end-user industry, consumer electronics accounted for 43.12% of the Japan PCB market in 2025, yet telecommunications and 5G infrastructure are advancing at the fastest 5.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing domestic demand for advanced driver-assistance systems modules | +0.8% | Toyota City, Yokohama, Hiroshima clusters | Medium term (2-4 years) |

| Re-shoring of high-layer-count PCB production encouraged by METI subsidies | +0.7% | Gifu, Yamagata, Gunma | Short term (≤ 2 years) |

| Surge in IC substrate capacity additions for AI accelerators | +0.9% | Gifu, Nagano | Short term (≤ 2 years) |

| Consumer appetite for premium 5G smartphones and wearables | +0.6% | Tokyo, Osaka, Nagoya | Medium term (2-4 years) |

| Commercialization of glass-based core PCB technologies | +0.5% | National | Long term (≥ 4 years) |

| Adoption of power-dense SiC inverters in rail and industrial drives | +0.4% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Domestic Demand for Advanced Driver-Assistance Systems Modules

Revised Road Transport Vehicle Act rules, effective April 2025, require collision-avoidance functions in all new passenger cars, prompting the integration of radar, lidar, and cameras across model lineups.[1]Yano Research Institute, “Automotive Sensor Market Report 2024,” yano.co.jp Each Level 2-plus platform now carries 6-12 high-frequency boards operating at up to 77 GHz, raising layer counts above 10 and reducing trace widths to below 75 µm. CMK derived 85.6% of fiscal 2023 sales from automotive boards and targets a 15.8% compound annual growth rate for in-vehicle HDI through fiscal 2026, underscoring sector pull on domestic capacity.

Re-Shoring of High-Layer-Count PCB Production Encouraged by METI Subsidies

The 2024 semiconductor strategy earmarked more than JPY 10 trillion for domestic capacity, cutting effective capital costs by up to 30% on multilayer lines and requiring 60% local raw-material sourcing by 2027.[2]Ministry of Economy, Trade and Industry, “Semiconductor and Digital Industries Strategy,” meti.go.jp Ibiden has committed JPY 130 billion across the Ogaki, Kawama, and Ono sites, while Meiko tripled HDI output at its Tendo plant, collectively re-anchoring supply for boards with 16+ layers or sub-50 µm line-and-space geometries.

Surge in IC Substrate Capacity Additions for AI Accelerators

Hyperscale data centers are installing GPUs and tensor processors that require flip-chip BGAs with more than 3,000 I/O and a 500 W thermal budget. Ibiden’s Ono plant, opened in October 2025, targets near-monopoly positions in these substrates.[3]Ibiden Co. Ltd., “Ono Plant Begins Operations,” ibiden.com Sumitomo Bakelite recorded JPY 91.3 billion in semiconductor-material sales in fiscal 2024 and is expanding resin lines to support backend assembly, enabling substrate average selling prices to rise 12-15% annually since 2024.

Consumer Appetite for Premium 5G Smartphones and Wearables

Nationwide 5G coverage reached 98.4% by fiscal year 2024, significantly accelerating the adoption of flagship devices that incorporate 8-12 flexible circuits per handset. Nitto Denko’s ultra-thin, halogen-free circuit lines are specifically designed to support camera and battery modules. Additionally, Sumitomo Electric has set a target to achieve JPY 360 billion in electronics revenue by fiscal year 2025, driven by the development of 30 µm-pitch flexible circuits for applications in medical devices and connected-vehicle technologies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging skilled workforce and talent pipeline gaps | -0.6% | Nationwide shortages | Long term (≥ 4 years) |

| High electricity costs versus Korea and mainland China | -0.5% | All prefectures | Short term (≤ 2 years) |

| Slow qualification cycles for automotive OEMs | -0.3% | Vehicle supply chain | Medium term (2-4 years) |

| Limited local supply of ultra-low Dk/Df laminates | -0.2% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Skilled Workforce and Talent Pipeline Gaps

In 2023, the proportion of individuals aged 65 and older in Japan increased to 29% of the total population. Additionally, enrollment in electronics vocational programs declined by 18% between 2019 and 2024, contributing to ongoing shortages of skilled technicians. Wage inflation rose by 4.2% in 2024. Although Meiko allocated JPY 5.3 billion toward automating inspection processes, achieving full automation remains impractical for production characterized by low volumes and high product variety.

High Electricity Costs Versus Korea and Mainland China

During the first half of 2025, wholesale prices averaged USD 76 per MWh, representing a 15% increase compared to the same period in the previous year. These prices are forecast to rise further, reaching USD 87 in 2026, as the costs associated with LNG imports remain elevated. Energy expenditures now account for 12% of the production costs for multilayer boards, which is double the level recorded in 2020. This significant increase has compelled domestic fabricators to specialize in quick-turn, high-tolerance jobs, while the production of commodity volumes continues to migrate offshore.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PCB Type: Flexible Circuits Capture Share From Legacy Multilayer Boards

Flexible circuits are projected to grow at a 5.42% CAGR through 2031, lifted by foldable smartphones, wearables, and automotive sensor ribbons. Standard multilayer boards retained 27.84% of 2025 revenue, but face commoditization as offshore suppliers underprice domestic players. High-density interconnect volumes rise alongside radar modules and 5G radios that need sub-100 µm vias, while IC substrates benefit from AI-server demand. Rigid-flex boards dominate implantables and avionics, where reliability outweighs cost.

Nitto Denko’s CISFLEX series enables 30-µm traces for flagship camera modules, and Sumitomo Electric’s semi-additive flex processes target medical scopes and connected-vehicle sensors. Rigid 1-2-sided boards persist in white-goods and legacy consoles but decline as surface-mount modules proliferate. Metal-core and ceramic boards, though small, secure higher margins due to demanding thermal performance. This mix shift underscores why the Japan PCB market keeps tilting toward value-added flex and substrate products.

By Substrate Material: High-Speed Laminates Support Telecom Infrastructure

FR-4 accounted for 41.87% of 2025 revenue, anchored in automotive and consumer devices, where UL94-V0 compliance and cost control prevail. Yet high-speed laminates with Dk below 3.5 and Df below 0.005 are projected to expand at a 5.01% CAGR as millimeter-wave antennas and 100-Gbps switches proliferate. Polyimide films power flex circuits that must endure 260 °C reflow, while packaging resins, such as Ajinomoto build-up film, underpin IC substrates with more than 10 layers.

Kyocera’s ceramic-filled materials hold ±10 µm pattern precision for radar and 5G radios. Domestic shortages of ultra-low-loss laminates force imports that add 4-6 weeks to lead times and expose suppliers to currency swings. Liquid-crystal polymer and emerging glass-core stacks remain at pilot scale but promise dimensional stability for post-2028 AI accelerators. Consequently, the Japan PCB market size for high-speed chemistries will continue to grow faster than the legacy FR-4 base.

By End-User Industry: Telecommunications And 5G Lead Growth

Telecommunications and 5G infrastructure are set to expand at a 5.67% CAGR through 2031, the fastest among end-user sectors, as operators deploy Open-RAN radios and 100-Gbps backhaul. Consumer electronics retained 43.12% of 2025 demand but faces plateauing handset volumes, prompting a shift in emphasis to premium tiers with higher board content. Automotive and EV platforms consume 2-3 m² of boards per vehicle, six times more than internal-combustion models, boosting demand for rigid and HDI boards.

Computing and data centers rely on high-layer substrates for AI accelerators, while industrial drives adopt silicon-carbide inverters that need thick-copper boards. Healthcare applications, though small in volume, command premium margins for biocompatible flex circuits. Aerospace and defense require MIL-PRF-certified boards for satellite and fighter programs, sustaining demand for low-volume, high-reliability runs. As these verticals diversify, the Japan PCB market maintains balanced exposure across cyclical segments.

Geography Analysis

Domestic production remains concentrated in Gifu, Yamagata, and Gunma, where subsidy-backed expansions are underway, yet Tokyo, Osaka, and Nagoya supply most downstream electronics assembly. Japan printed circuit board market size growth in central Honshu benefits from proximity to automotive clusters and skilled labor, while Kyushu fabs emphasize flex circuits for smartphone exporters. The country’s export-to-output ratio climbed after January 2025’s 113.8% surge in production, illustrating rising competitiveness despite energy-cost headwinds.

Gifu's Ono plant bolsters IC-substrate capacity tailored for AI servers, while Yamagata's Tendo facility triples its output of automotive HDIs, aligning demand hotspots with their respective supply bases. While rural prefectures enjoy the advantage of lower real estate costs, they grapple with staffing challenges exacerbated by an aging demographic. Ultra-low-loss laminate imports, funneled through Pacific ports, extend lead times by an additional four to six weeks, putting pressure on just-in-time models.

Government infrastructure spending extends 5G coverage to 98.4% of the population, driving radio-unit deployments even in remote prefectures, which in turn lifts local board demand for telecom OEMs. Renewable-energy mandates encourage onsite solar arrays that offset high utility tariffs, especially in sun-rich Shizuoka and Yamanashi. As manufacturing footprints rebalance, the Japan printed circuit board market continues shifting from coastal commodity fabs to inland high-value centers.

Competitive Landscape

Ibiden, Meiko Electronics, and CMK collectively control about 60% of domestic HDI and IC-substrate capacity, giving the Japan printed circuit board market a moderately concentrated profile. Ibiden monopolizes certain AI server substrates after the Ono expansion, while Meiko leverages its IATF 16949 certification to win automotive awards that require 18-24 months of qualification. CMK focuses on radar boards and has invested in automated optical inspection to boost yields.

Smaller entrants exploit niche processes: Elephantech uses nanocopper inkjet printing, which reduces copper waste by 70% and shortens lead times to 5 days, funded by a JPY 2.291 billion NEDO grant. Nippon Electric Glass and Dai Nippon Printing pioneer glass-core and through-glass-via stacks that promise dimensional stability for post-2028 packages. Shinko Electric’s 2025 delisting signals consolidation pressure as sub-scale players struggle to fund multi-billion-yen process nodes.

Competitive strategies emphasize vertical integration and automation to offset energy and labor costs. Large players deploy panel-level packaging and modified semi-additive processes for high-layer builds, whereas mid-tier firms position around quick-turn prototypes and low-volume, high-mix runs. Compliance with IATF 16949 and ISO 13485 remains a gatekeeper, and only shops sustaining Cpks above 1.67 capture long-cycle automotive or medical contracts. Technology bifurcation, subsidy support, and additive breakthroughs together keep the Japan printed circuit board market dynamic.

Japan Printed Circuit Board Industry Leaders

Ibiden Co., Ltd.

Meiko Electronics Co., Ltd.

CMK Corporation

Kyocera Corporation

Shinko Electric Industries Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Ibiden began commercial operations at the Ono plant in Gifu, adding advanced semiconductor substrate capacity aimed at AI server packages.

- June 2025: Shinko Electric completed delisting from the Tokyo Stock Exchange following a Japan Investment Corporation tender offer valued at JPY 180 billion.

- March 2025: JEITA reported domestic PCB production of JPY 49.619 billion, up 106.8% year over year, with assemblies up 109.7%.

- February 2025: Fujitsu Interconnect Technologies transferred ownership to MBK Partners and FormFactor to accelerate advanced-substrate investment.

Japan Printed Circuit Board Market Report Scope

The Japan Printed Circuit Board Market Report is Segmented by PCB Type (Standard Multilayer (non-HDI), Rigid 1-2 Sided, High-Density Interconnect (HDI), Flexible Circuits (FPC), IC Substrates (Package Substrates), Rigid-Flex, Other PCB Types), Substrate Material (Glass Epoxy (FR-4), High-Speed Low-Loss, Polyimide (PI), Packaging Resins (BT / ABF), Other Substrate Materials), and End-user Industry (Consumer Electronics, Computing and Data Centers, Telecommunications and 5G, Automotive and EV, Industrial and Power, Healthcare / Medical, Aerospace and Defense, Other End-user Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided |

| High-Density Interconnect (HDI) |

| Flexible Circuits (FPC) |

| IC Substrates (Package Substrates) |

| Rigid-Flex |

| Other PCB Types |

| Glass Epoxy (FR-4) |

| High-Speed / Low-Loss |

| Polyimide (PI) |

| Packaging Resins (BT / ABF) |

| Other Substrate Materials |

| Consumer Electronics |

| Computing and Data Centers |

| Telecommunications and 5G |

| Automotive and EV |

| Industrial and Power |

| Healthcare / Medical |

| Aerospace and Defense |

| Other End-user Industries |

| By PCB Type | Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided | |

| High-Density Interconnect (HDI) | |

| Flexible Circuits (FPC) | |

| IC Substrates (Package Substrates) | |

| Rigid-Flex | |

| Other PCB Types | |

| By Substrate Material | Glass Epoxy (FR-4) |

| High-Speed / Low-Loss | |

| Polyimide (PI) | |

| Packaging Resins (BT / ABF) | |

| Other Substrate Materials | |

| By End-user Industry | Consumer Electronics |

| Computing and Data Centers | |

| Telecommunications and 5G | |

| Automotive and EV | |

| Industrial and Power | |

| Healthcare / Medical | |

| Aerospace and Defense | |

| Other End-user Industries |

Key Questions Answered in the Report

How large is the Japan PCB market in 2026 and what is its forecast size for 2031?

The Japan PCB market size was USD 7.46 billion in 2026 and is projected to reach USD 9.11 billion by 2031 at a 4.08% CAGR.

Which PCB type is growing the fastest in Japan?

Flexible circuits are expanding the quickest, with a forecast 5.42% CAGR during 2026-2031 thanks to foldable smartphones and wearables.

What segment holds the largest Japan PCB market share today?

Standard multilayer boards led with 27.84% revenue share in 2025, mainly serving automotive and industrial control modules.

Why are high-speed laminates important for Japanese telecom applications?

Millimeter-wave antennas and 100-Gbps switches need dielectric constants below 3.5 and very low loss, driving 5.01% CAGR in high-speed materials.

How are subsidies reshaping domestic PCB capacity?

METI incentives cut capital costs by up to 30%, leading Ibiden, Meiko, and others to add multilayer and IC-substrate lines in Gifu and Yamagata.

What is the main challenge facing PCB fabricators in Japan?

An aging skilled workforce and electricity prices that are 15-20% higher than Korean and Chinese levels strain competitiveness.

Page last updated on: