Japan Plastic Waste Management Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

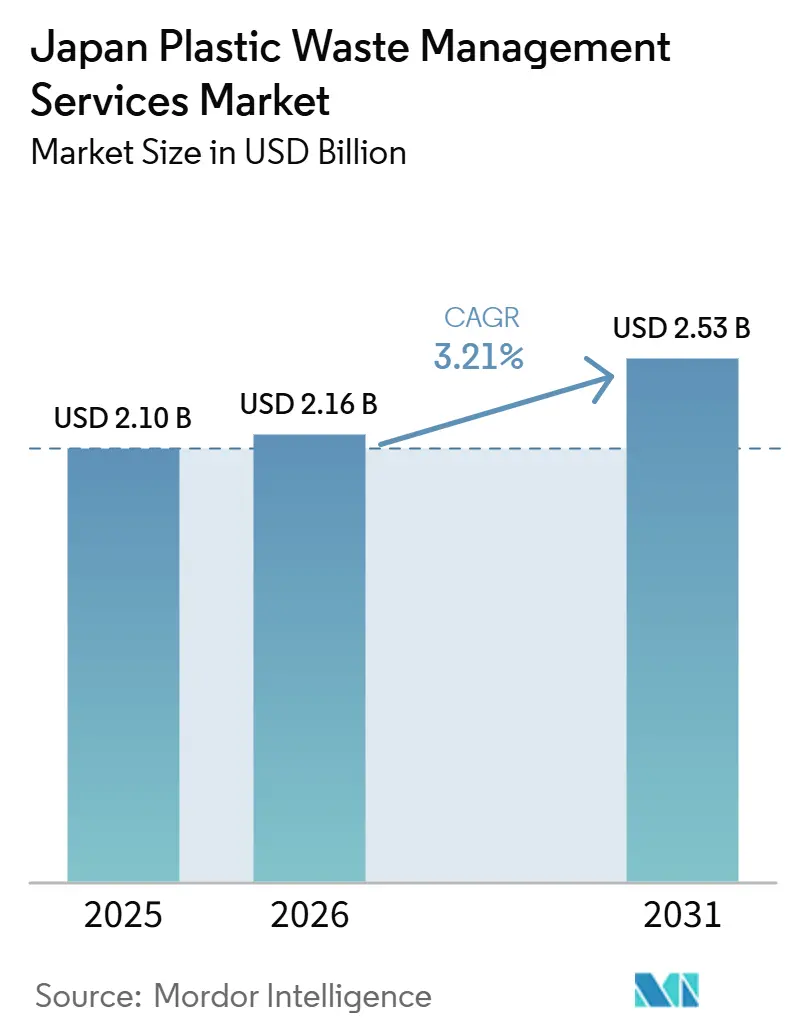

| Base Year Market Size (2025) | USD 2.10 Billion |

| Market Size (2026) | USD 2.16 Billion |

| Market Size (2031) | USD 2.53 Billion |

| Growth Rate (2026 - 2031) | 3.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Plastic Waste Management Services Market Analysis by Mordor Intelligence

The Japan Plastic Waste Management Services Market size was valued at USD 2.10 billion in 2025 and is estimated to grow from USD 2.16 billion in 2026 to reach USD 2.53 billion by 2031, at a CAGR of 3.21% during the forecast period (2026-2031).

Japan generated 9.11 million tons of plastic waste in fiscal 2024, of which 89% was effectively utilized. However, 67% of that utilized volume still moved through thermal recycling, leaving room for higher-value recovery services in the Japan plastic waste management services market. Tighter domestic compliance rules from 2026 are pushing manufacturers to formalize plans for recycled material use and strengthen reporting, underscoring the need for licensed handling, sorting, and documentation support across the Japan plastic waste management services market. The market is also benefiting from policy support for new recycling capacity and from a broader shift toward integrated treatment platforms that combine recovery, traceability, and energy generation within a single operating chain. Landfill use remains structurally limited in Japan, with less than 1% of total waste treatment going to landfills, which keeps value concentrated in treatment technologies rather than low-margin disposal within the Japan plastic waste management services market. This setting favors operators that can scale industrial contracts, build stronger municipal links, and invest in processing depth as compliance, infrastructure renewal, and domestic resource security continue to shape the Japan plastic waste management services market.

Key Report Takeaways

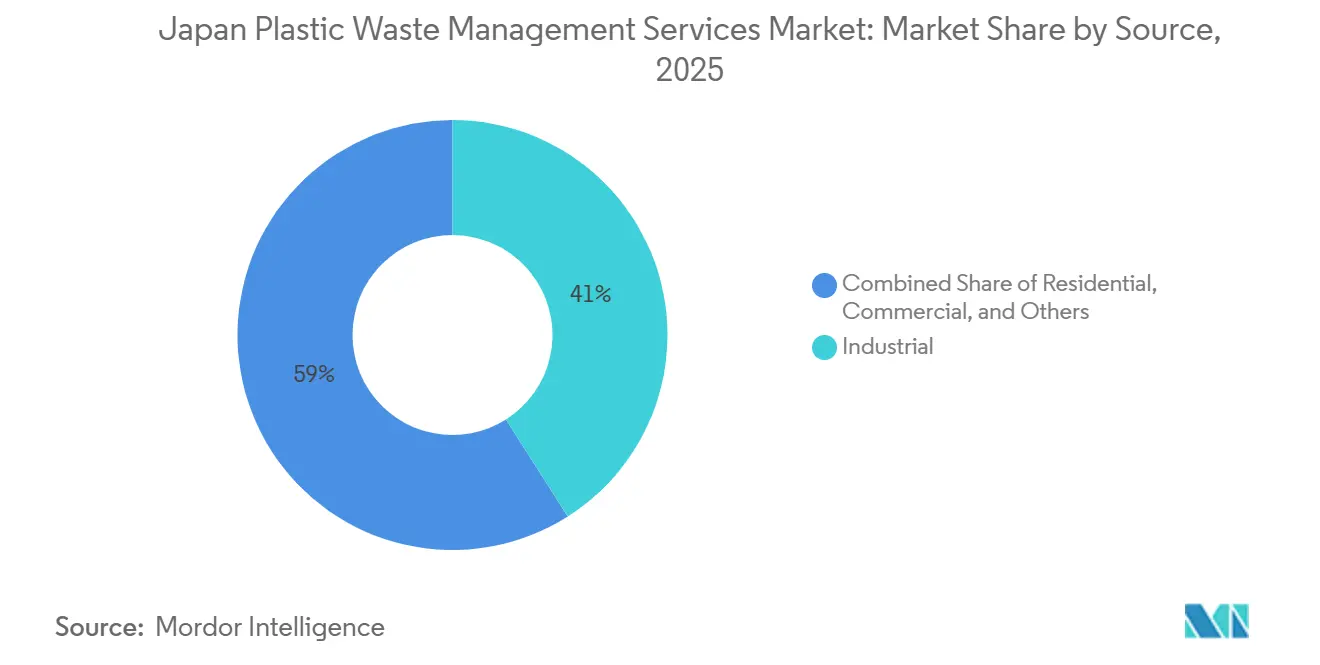

- By source, industrial waste accounted for 41.0% of the Japan plastic waste management services market share in 2025, while commercial streams are projected to be the fastest-growing at a 3.90% CAGR through 2031.

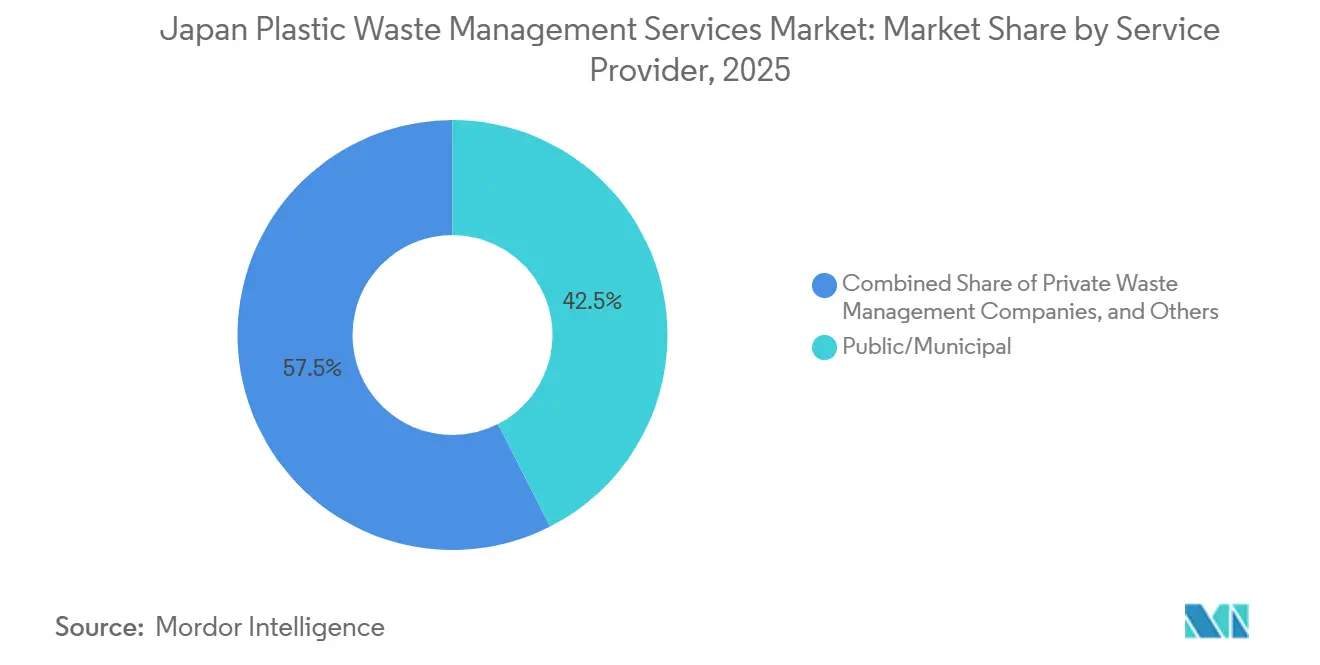

- By service provider, public/municipal accounted for 42.50% of the Japan plastic waste management services market size in 2025, and private waste management companies are expected to register 6.10% CAGR through 2031.

- By service type, collection, transportation, sorting & segregation accounted for 40.60% in 2025, and disposal/treatment is expected to register 5.20% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Plastic Waste Management Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Industrial Waste Segregation and Disposal Rules | +1.0% | Japan-wide, strongest in Aichi, Kanagawa, Osaka | Long term (≥ 4 years) |

| Rising Outsourcing of Industrial Waste Management | +0.8% | Aichi, Shizuoka, Hyogo, Kanagawa | Medium term (2-4 years) |

| Expansion of Waste-to-Energy Infrastructure | +0.7% | Yokohama, Osaka, Sapporo, Niigata and nearby regions | Long term (≥ 4 years) |

| Strong Municipal Segregation and Collection Infrastructure | +0.6% | Japan-wide, especially municipalities with active packaging recycling programs | Medium term (2-4 years) |

| Landfill Scarcity Supporting Recycling and WtE Adoption | +0.5% | All prefectures, strongest in Tokyo and Osaka-Kansai | Long term (≥ 4 years) |

| Smart Collection and Digital Tracking Adoption | +0.4% | Metropolitan regions and mid-sized cities with digital programs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Industrial Waste Segregation and Disposal Regulations

Japan’s industrial waste rules are no longer limited to basic compliance, and they now shape how service demand is formed across the Japan plastic waste management services market. The 2026 regulatory tightening requires affected manufacturers to prepare recycled-material-use plans and report on implementation progress, which raises the value of operators that can manage traceable flows and documentation with fewer errors. A related shift is the certification pathway tied to plastic collection performance, because operators aligned with compliant manufacturers can gain stronger, long-term positions than peers who offer only basic transport or treatment capacity. METI’s first design certifications under the Plastic Resource Circulation Act in 2026 also created a clearer route for products and recovery systems that fit approved circularity standards.[1]Ministry of Economy, Trade and Industry, “First Design Certifications Issued Under the Plastic Resource Circulation Act,” METI, meti.go.jp This favors service providers with better sorting capability, stronger audit trails, and established downstream links. The result is a Japan plastic waste management services market that increasingly rewards licensed specialists over small operators that compete mainly on route economics.

Rising Outsourcing of Industrial Waste Management

Industrial outsourcing has become a structural demand driver in the Japan plastic waste management services market because waste generators face a heavier compliance burden under the manifest system. Many manufacturers now prefer service partners that can handle collection, treatment, traceability, and final reporting in a single arrangement rather than managing these tasks internally. This shift supports recurring contracts and also reduces switching once a provider becomes embedded in the client’s compliance workflow. The trend also aligns with the recent consolidation in waste services, where larger operators have been building regional networks to serve national accounts with consistent standards. That makes outsourced contracts easier to scale across plants, especially for automotive, electronics, and chemical producers with facilities in multiple prefectures. The Japan plastic waste management services market therefore gains not only from volume transfer to contractors, but also from higher contract depth as outsourced work moves beyond hauling into managed compliance services.

Expansion of Waste-to-Energy (WtE) Infrastructure

Waste-to-energy capacity is expanding in Japan through plant replacement, equipment modernization, and longer operating contracts, which supports the higher-value side of the Japan plastic waste management services market. Municipal buyers are replacing older facilities with systems that can recover more energy, improve emissions performance, and operate for extended periods under long-term design-build-operate structures. JFE Engineering’s award for Niigata City’s new energy recovery facility reflects this long-cycle investment pattern. It shows that municipal treatment demand is shifting toward advanced infrastructure rather than short-life assets. The same trend is evident in Yokohama and other cities, where replacement rather than greenfield growth is driving capacity renewal. This matters because treatment revenue is less exposed to pure collection competition and carries stronger after-service potential for engineering-led operators. As a result, the Japanese plastic waste management services market is seeing a greater value shift toward platforms that combine treatment, energy recovery, and long-term operating contracts.

Smart Waste Collection and Digital Tracking Adoption

Digital tools are becoming increasingly relevant in the Japan plastic waste management services market as traceability is moving from an efficiency feature to a contractual requirement. Borzoi AI’s collection navigation pilot in Chofu City demonstrated that real-time reporting, route visibility, and field documentation can be implemented without incurring significant hardware costs. ShinMaywa Industries and LECIP also launched an IoT-enabled refuse compactor system that tracks location, load status, and operating logs, which supports better fleet control and more consistent client reporting. These tools improve route discipline, but their greatest value lies in documented proof of service and auditable handling records. That is important for commercial and industrial waste generators that need clearer evidence of where waste moved and how it was treated. The Japan plastic waste management services market is therefore moving toward service differentiation based not only on physical handling capacity, but also on the ability to generate usable compliance data.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Workforce and Labor Shortages | -0.5% | Japan-wide, critical in rural municipalities and mid-tier cities | Long term (≥ 4 years) |

| High Operating Costs for Collection and Transportation | -0.4% | Japan-wide, strongest in rural and remote prefectures | Medium term (2-4 years) |

| High Capital Needs for Advanced Treatment Facilities | -0.3% | Urban and peri-urban areas needing facility upgrades | Long term (≥ 4 years) |

| Volatile Energy and Fuel Prices | -0.2% | Japan-wide, acute in collection and transportation activities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Workforce and Labor Shortages

Japan’s labor profile is a structural restraint for the Japan plastic waste management services market because waste handling depends on steady field staffing, skilled vehicle operation, and reliable local service coverage. The OECD reported that Japan’s working-age population fell from 87.3 million at its 1995 peak to 73.7 million in 2024, which shows the scale of long-term labor tightening. The IMF also found that 30% of firms reported labor shortages in 2024, which indicates that competition for workers extends well beyond sanitation and environmental services. For waste operators, this raises labor costs and complicates route reliability, especially in regional markets where recruitment pools are thinner. It also gives private groups an advantage by enabling them to invest in multilingual hiring systems and structured workforce planning before visa expansion. Over time, the Japan plastic waste management services market is likely to reward companies that can consistently address staffing bottlenecks and treatment capacity gaps.[2]International Monetary Fund, “The Impact of Aging and AI on Japan's Labor Market,” IMF Working Paper, imf.org

High Operating Costs for Waste Collection and Transportation

Collection and transport remain cost-intensive parts of the Japan plastic waste management services market because Japan’s geography creates long routes, uneven density, and a high reliance on specialized vehicles. Fuel cost swings, vehicle wear, and route certification needs place pressure on smaller operators that lack strong geographic concentration. When transport margins tighten, operators often respond by reducing pickup frequency or consolidating loads, which weakens sorting quality. Lower sorting quality reduces the value of recovered material and can also raise downstream treatment costs. The issue is therefore broader than logistics expenses, because it affects service quality and resource recovery simultaneously. In the Japan plastic waste management services market, cost discipline in collection is becoming a basic condition for preserving margins further down the chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Industrial Contracts Anchor Market Volume

Industrial generators held 41% of the Japan plastic waste management services market share in 2025, making them the largest source segment by value. This leadership reflects the concentration of automotive, electronics, and chemical manufacturing across major industrial belts, where waste streams are larger, more regulated, and more complex to manage. In the Japan plastic waste management services industry, industrial contracts also tend to be longer and more documentation-heavy because the manifest system requires clear traceability from generation to final treatment. That produces recurring revenue for licensed operators and supports better asset utilization across sorting, treatment, and recovery facilities. Residential waste remains an important volume base, but its service economics are more closely tied to municipal systems and public collection frameworks.

Commercial waste is projected to expand at a 3.9% CAGR through 2031, making this segment the fastest-growing source in the Japan plastic waste management services market. The rise comes from broader producer responsibility obligations, stronger ESG reporting pressure, and reduced flexibility for mixed-plastic disposal through export channels. This matters because commercial generators often need more tailored services than households but lack the scale of large industrial clients, creating room for mid-tier operators with flexible contract models. The others category, which includes institutional and agricultural streams, is also rising as product-specific plastic collection practices become more formalized. Across the Japan plastic waste management services market, source mix is therefore gradually shifting toward segments where compliance depth and contract customization matter more than pure collection scale.

By Service Provider: Private Operators Build Structural Momentum

Public and municipal providers retained 42.5% of the Japan plastic waste management services market in 2025, maintaining their leading position by provider type. Their strength comes from broad residential coverage, established local collection systems, and long-standing public service arrangements that remain central to daily waste handling. At the same time, their role is strongest in upstream collection, while downstream recovery and specialized treatment are increasingly shared with private partners. That distinction is important because the Japan plastic waste management services market is creating greater value through deeper treatment, better data handling, and specialized compliance support. Municipal systems still anchor baseline volume, but they do not control every high-growth service layer.

Private waste management companies are forecast to grow at a 6.1% CAGR through 2031, making them the fastest-growing provider group in the Japan plastic waste management services market. Their momentum comes from specialization in hazardous streams, industrial contracts, chemical recycling pathways, and documentation support for corporate clients. Veolia’s integrated waste platform in Japan shows how private operators are combining recycling facilities with licensed final disposal to win larger mandates from industrial customers. Producer responsibility organizations are also becoming more relevant as product compliance rules expand, adding another layer between waste generators and physical handlers. In the Japan plastic waste management services industry, that institutional layer can direct more work toward operators that can meet national-scale reporting and traceability requirements.

By Service Type: Treatment Mix Shifts Toward Higher-Order Processing

Collection, transportation, sorting, and segregation accounted for 40.6% of the Japan plastic waste management services market in 2026, making it the largest service type by value. That leadership reflects Japan’s well-developed source separation culture, municipal collection routines, and established packaging recovery infrastructure. The segment is mature rather than weak, and its lower growth rate mainly shows that network penetration is already high across much of the country. In practice, this means leading operators in this layer must protect margin through better routing, digital visibility, and cleaner material recovery. The Japan plastic waste management services market still depends on this service base because every downstream recovery option starts with effective collection and separation.

Disposal and treatment are projected to grow at a 5.2% CAGR through 2031, making it the fastest-growing service category in the Japan plastic waste management services market. Japan’s reliance on landfills remains minimal, with less than 1% of total waste treatment sent to landfills, so treatment value is concentrated in incineration with energy recovery and newer recycling pathways. PWMI data also show that thermal recycling accounted for 67% of plastic waste utilization in fiscal 2024, highlighting the continued dominance of energy recovery in the current treatment mix.[3]Plastic Waste Management Institute of Japan, “Plastic Products Production, Waste, Recycling, and Disposal Status,” PWMI, pwmi.or.jp Consulting, audit, and training services are also gaining relevance as compliance obligations become more formal and more frequent. Across the Japan plastic waste management services market, the strongest value growth is therefore moving toward service lines that can combine physical treatment with regulatory assurance and operational reporting.

Geography Analysis

Japan's plastic waste management services market size stands at USD 2.16 billion in 2026. It will reach USD 2.53 billion by 2031, which means the full national geography remains the relevant operating frame for demand, infrastructure, and regulation. The country’s urban concentration creates dense waste flows in large coastal cities, while service delivery is harder in sparsely populated, mountainous areas. Tokyo remains the primary hub for commercial and industrial plastic waste, and it also serves as the main testing ground for digital collection tools and smart container systems. Chofu City’s AI-based collection pilot and Tokyo Dome City’s smart bin deployment show how the capital continues to shape operating models that may later spread into the wider Japan plastic waste management services market.

Regional differences are clearer than national totals suggest. The OECD reported that 146 subnational governments had adopted Circulating and Ecological Economy initiatives, but the depth and operating maturity of these programs varied sharply across prefectures. Kansai remains important because it combines industrial waste generation with established service networks across Osaka, Kyoto, and Hyogo. Hokkaido and parts of Tohoku face different conditions, with lower density, more difficult route economics, and greater dependence on anchor facilities that can justify regional collection flows. J&T Recycling’s new Sapporo biogas plant illustrates how a regional anchor model can support wider resource recovery in capacity-constrained areas. Southern prefectures are also seeing infrastructure renewal, which may create new openings for specialists in refurbishment, treatment operations, and municipal support contracts.

Geographic waste flows are changing as domestic processing becomes more important than export routing. Port-linked cities such as Yokohama, Osaka, and Kobe have historically sat close to outbound channels, but tighter controls on waste exports are encouraging more domestic handling and processing investment. This change matters because port-adjacent industrial zones already have logistics links, client density, and treatment demand that can support larger integrated platforms. Research in Sustainability also showed that local implementation capacity influences how effectively plastic waste governance is carried out, which means private operators may find the strongest growth in prefectures where compliance support and processing infrastructure are still catching up.

Competitive Landscape

The Japan plastic waste management services market shows moderate consolidation, with DOWA Holdings, JFE Environment, TRE Holdings, Takuma, and Kanadevia forming a visible leadership group. At the same time, many regional operators remain active in collection and localized treatment. This structure reflects high capital needs, licensing requirements, and the importance of documented process chains under Japan’s waste rules. Companies with established treatment infrastructure and long operating histories still hold a strong advantage because new entrants cannot easily match their compliance systems, route density, and municipal relationships. The Japan plastic waste management services market therefore supports competition, but it does not reward undifferentiated entry.

A clear strategic pattern is the move toward end-to-end service portfolios. Veolia strengthened that model through its 2025 acquisition of Zeeklite and then presented a more integrated industrial waste solution in Japan in 2026, combining recycling assets with licensed final disposal capacity. That matters because industrial clients increasingly prefer a single accountable vendor for collection, treatment, documentation, and final handling. Another competitive pattern is the push toward infrastructure-led growth, where engineering-heavy companies use long municipal treatment contracts to secure revenue visibility and downstream service opportunities. JFE Engineering’s long-term vision and its municipal recycling collaborations align with this direction, demonstrating how engineering capability can strengthen its competitive position in the Japan plastic waste management services market.

Technology is becoming the second major basis of competition after scale. Operators that can provide better tracking, higher-quality sorting, and more reliable reporting can defend pricing even when transport and basic handling remain competitive. This is especially relevant for corporate generators that now need stronger evidence of waste destination and resource recovery outcomes. The Japan plastic waste management services market is also creating space for operators that can expand treatment depth, especially where chemical recycling capacity and data-backed compliance services remain limited. As a result, market leadership is likely to depend less on collection reach alone and more on the ability to integrate infrastructure, reporting, and specialized processing into a single operating model.

Japan Plastic Waste Management Services Industry Leaders

DOWA Holdings

JFE Environment Corporation

TRE Holdings Corporation

Takuma Co., Ltd.

Daiei Kankyo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Kanadevia Inova (a subsidiary of Kanadevia Corporation) received notice to proceed with the construction of a state-of-the-art WtE plant in Rome, Italy, leveraging the group's WtE technology platform. At the same time, its domestic order backlog stood at approximately JPY 897.7 billion (USD 5.53 billion) as of FY2025.

- April 2026: Veolia Japan formally announced a fully integrated end-to-end industrial waste solution in Japan, combining plastic packaging recycling facilities (Ecos Factory, Green Loop, Circular PET) with licensed final disposal capacity via Zeeklite, targeting industrial clients requiring single-vendor accountability across the full waste treatment chain.

- June 2025: Veolia Japan GK completed the acquisition of Zeeklite Co., Ltd. from ORIX Environmental Resources Management Corporation. Zeeklite operates one of Japan's largest private landfills in Yonezawa City, Yamagata Prefecture, specializing in the disposal of hazardous and general industrial waste.

- May 2025: J&T Recycling Corporation (JFE Engineering Group) completed Hokkaido's largest food waste biogas plant in Sapporo City, establishing a local energy production-and-consumption loop and bringing the group's national food-recycling power generation network to 6 sites.

Japan Plastic Waste Management Services Market Report Scope

The Japan Plastic Waste Management Services Market Report is Segmented by Source (Residential, Commercial, Industrial, and Others), by Service Provider (Public/Municipal, Private Waste Management Companies, and Others), and by Service Type (Collection, Transportation, Sorting & Segregation, Disposal / Treatment, and Others). The Market Forecasts are Provided in Terms of Value (USD).

| Residential |

| Commercial (retail, office, etc.) |

| Industrial |

| Others (institutional, agricultural, etc) |

| Public/Municipal |

| Private Waste Management Companies |

| Others - Producer Responsibility Organizations (PROs), etc. |

| Collection, Transportation, Sorting & Segregation | |

| Disposal / Treatment | Landfill |

| Recycling & Resource Recovery | |

| Incineration & Waste-to-Energy | |

| Others (Chemical Treatment, Composting, etc.) | |

| Others (Consulting, Audit & Training, etc.) |

| By Source | Residential | |

| Commercial (retail, office, etc.) | ||

| Industrial | ||

| Others (institutional, agricultural, etc) | ||

| By Service Provider | Public/Municipal | |

| Private Waste Management Companies | ||

| Others - Producer Responsibility Organizations (PROs), etc. | ||

| By Service Type | Collection, Transportation, Sorting & Segregation | |

| Disposal / Treatment | Landfill | |

| Recycling & Resource Recovery | ||

| Incineration & Waste-to-Energy | ||

| Others (Chemical Treatment, Composting, etc.) | ||

| Others (Consulting, Audit & Training, etc.) | ||

Key Questions Answered in the Report

What is the 2031 outlook for plastic waste management services in Japan?

The sector is projected to reach USD 2.53 billion by 2031 from USD 2.16 billion in 2026, with a 3.2% CAGR over 2026-2031.

Which source segment leads demand in Japan?

Industrial waste led with 41% of revenue in 2025, supported by the country’s automotive, electronics, and chemical manufacturing base.

Which provider group is growing the fastest?

Private waste management companies are growing the fastest, with a projected 6.1% CAGR through 2031.

Which service type is expanding the quickest?

Disposal and treatment is the fastest-growing service type, with a 5.2% CAGR through 2031, as landfill use stays minimal and treatment depth rises.

Why are digital tools becoming more important in Japan’s waste services?

Operators now need stronger traceability, route visibility, and auditable service records, which makes AI navigation, IoT fleet tracking, and smart bins more valuable.

What is shaping competition among leading operators in Japan?

Competition is shifting toward integrated platforms that combine collection, treatment, recycling, documentation, and energy recovery, with Veolia, JFE-linked entities, and other domestic leaders pushing that model.

Page last updated on: