Japan Frontline Worker Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

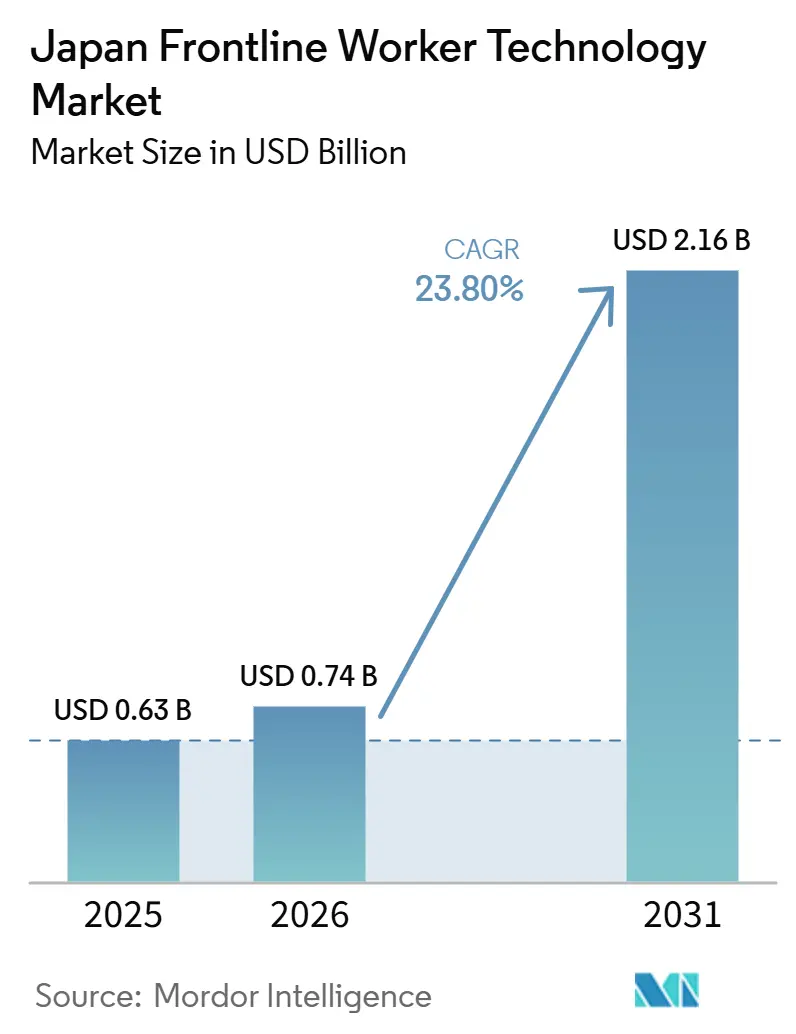

| Base Year Market Size (2025) | USD 0.63 Billion |

| Market Size (2026) | USD 0.74 Billion |

| Market Size (2031) | USD 2.16 Billion |

| Growth Rate (2026 - 2031) | 23.80% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Frontline Worker Technology Market Analysis by Mordor Intelligence

The Japan frontline worker technology market size is expected to increase from USD 0.63 billion in 2025 to USD 0.74 billion in 2026 and reach USD 2.16 billion by 2031, growing at a CAGR of 23.80% over 2026-2031. Growth is being shaped by labor shortages that are pushing employers to digitize scheduling, communication, safety, and workforce coordination for deskless teams across factories, hospitals, logistics sites, and construction environments. The Japan frontline worker technology market is also benefiting from larger enterprise software commitments, expanding AI infrastructure, and rising pressure to connect field operations with payroll, HR, and compliance systems within a single operating layer. Demand is moving beyond basic workflow digitization because buyers increasingly want platforms that can support analytics, automation, and operational decision support for shift-based work. Domestic technology firms and global software vendors are both expanding their frontline offerings, raising competition and widening the set of localized solutions available to Japanese buyers. Legacy integration remains the main constraint, but vendors that can offer simpler deployment, Japanese-language usability, and pre-integrated stacks are well placed to capture the next phase of adoption.

Key Report Takeaways

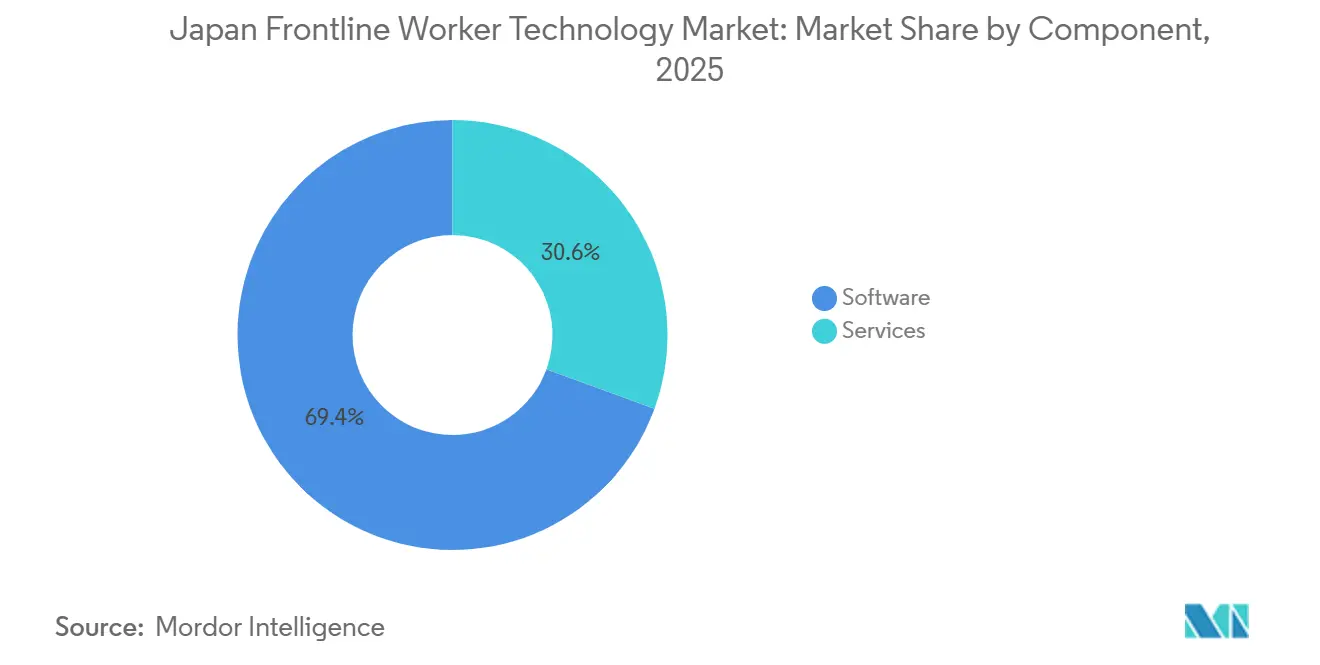

- By component, software led with 69.43% share in 2025, while services are projected to expand at a 25.92% CAGR through 2031.

- By deployment, cloud-based deployments accounted for 63.91% of the Japan frontline worker technology market size in 2025 and are projected to grow at a 26.74% CAGR through 2031.

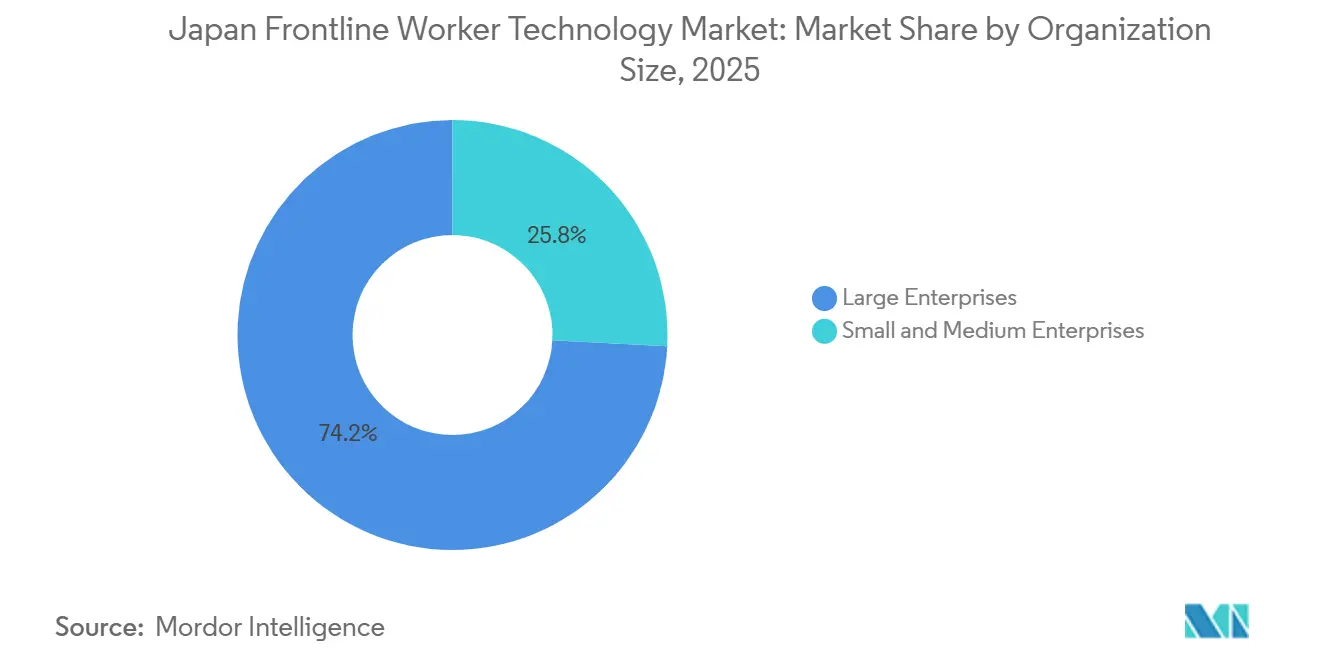

- By organization size, large enterprises held 74.16% of the Japan frontline worker technology market share in 2025, while SMEs are projected to expand at a 26.31% CAGR through 2031.

- By application, employee communication and engagement captured 24.86% of the market in 2025, while workforce analytics and performance management are projected to grow at a 28.18% CAGR through 2031.

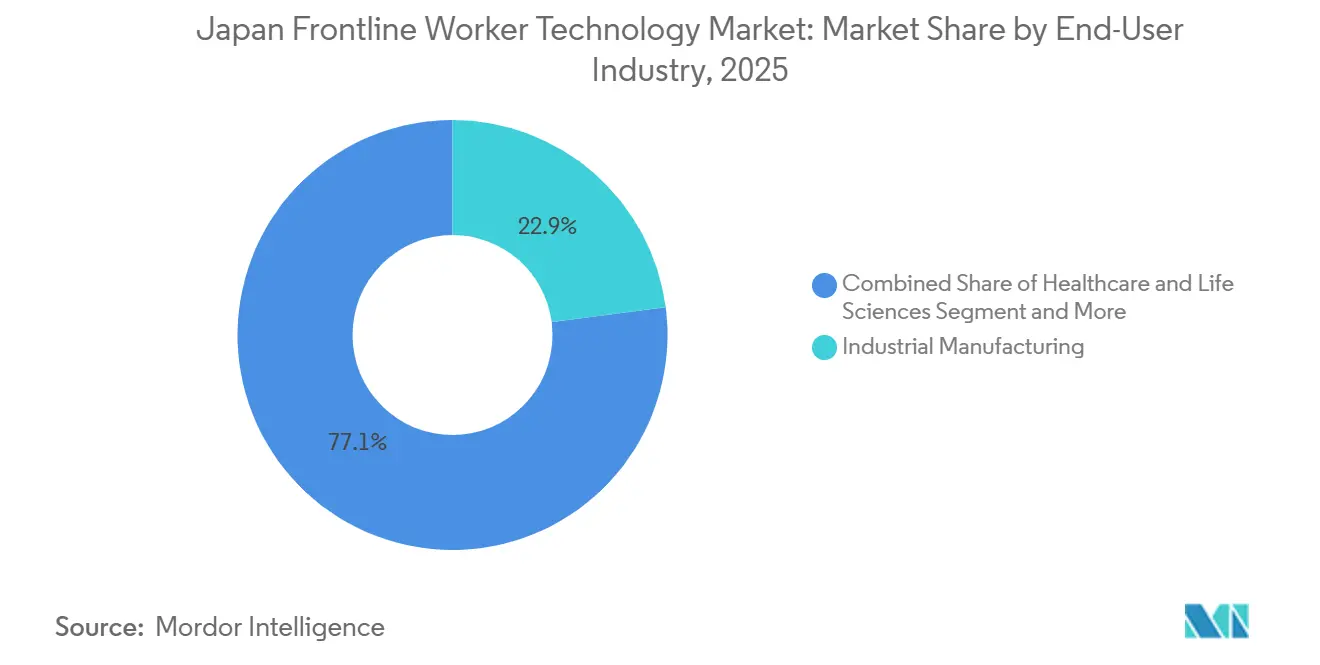

- By end-user industry, industrial manufacturing accounted for 22.94% share in 2025, while healthcare and life sciences are projected to expand at a 27.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Frontline Worker Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Workforce Driving Ergonomic And Productivity Technology Adoption | +5.8% | National, with concentrated impact in Aichi, Osaka, and Hokkaido industrial and eldercare clusters | Long term (≥ 4 years) |

| Mobile-First Digitization Of Deskless Workflows | +4.9% | National, strongest gains in the Tokyo metropolitan area and adjacent prefectures | Medium term (2-4 years) |

| AI-Led Labor Forecasting And Schedule Optimization | +4.2% | National, with accelerated uptake in shift-intensive retail, food service, and logistics belts | Medium term (2-4 years) |

| Unified HR, Payroll, Scheduling, And Communication Stacks | +3.5% | National, broadest impact in SME-dense service corridors | Medium term (2-4 years) |

| Connected Safety Monitoring For High-Density Industrial Sites | +2.1% | Aichi, Osaka, and Kanagawa heavy industrial zones, with spillover to construction clusters | Short term (≤ 2 years) |

| Privacy-Aware Design For Shared Devices And Frontline Identity Management | +1.3% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Workforce Driving Ergonomic And Productivity Technology Adoption

The Japan frontline worker technology market is being pushed by a demographic shift that is turning workforce preservation into a direct buying priority for employers. Japan had a very high share of older citizens in 2024, and age pressure was even sharper in labor-intensive fields such as construction and agriculture, where the available worker base is already strained.[1]Carnegie Endowment, “Japan’s Aging Society as a Technological Opportunity,” Carnegie Endowment for International Peace, carnegieendowment.org In this setting, buyers are not treating frontline tools as optional upgrades, because many firms now need digital systems that help older staff stay productive and help newer staff learn faster. Hitachi showed the commercial value of this approach when its Frontline Coordinator Naivy AI agent improved inexperienced worker performance by nearly 30% in verification trials at a Renesas Electronics plant.[2]Hitachi Ltd., “Hitachi Develops ‘Frontline Coordinator - Naivy’ as a Next-Generation AI Agent,” Hitachi, hitachi.com The Japan Institute of International Affairs stated in May 2026 that companies are under pressure to turn frontline know-how into AI-ready operational data and to redesign workflows around AI-enabled execution, thereby supporting the broader adoption of workplace tools that can capture and structure field knowledge.[3]Japan Institute of International Affairs, “Japan’s Winning Strategy in the Era of Physical AI,” Japan Institute of International Affairs, jiia.or.jp The Japan frontline worker technology market should continue to benefit from this pressure, as aging raises both the cost of inaction and the value of systems that support training, safety, and task consistency.

Mobile-First Digitization Of Deskless Workflows

The Japan frontline worker technology market is also benefiting from the fact that many deskless jobs still lag behind office roles in access to digital tools. OECD data published in November 2025 showed a wide workplace AI gap between service occupations, such as accommodations and food services, and the information and communications sector, indicating that adoption is held back by workflow design and tool fit rather than by worker readiness alone.[4]Organization for Economic Co-operation and Development, “AI Use in the Japanese Workplace,” OECD, oecd.org That gap matters because paper forms, bulletin boards, and verbal updates do not create a gradual path into digital work, so companies often need a full platform shift rather than a minor feature upgrade. Staffbase expanded its Japan capabilities in 2026 and launched Japanese-language AI Podcast and AI Assistant features that help frontline staff access internal communication via smartphones and audio, directly addressing the low-information environment common on factory and logistics floors. The same pattern supports broader adoption of mobile-first interfaces in the Japan frontline worker technology market because they reduce reliance on PCs and align with the daily routines of workers who move across shifts, sites, and tasks. As more employers try to close communication gaps between headquarters and the field, mobile delivery is likely to remain one of the most practical routes into platform adoption.

AI-Led Labor Forecasting And Schedule Optimization

The Japan frontline worker technology market is moving toward AI-driven labor forecasting, as employers increasingly need scheduling systems that can balance skills, leave, shift rules, and operational demand in real time. OECD evidence from 2025 showed that AI use among Japanese employees remained low even as business interest was rising, suggesting a large deployment gap that vendors can address with tools that solve clear operational problems. Microsoft also reported in 2026 that Japanese executives expect stronger AI-human collaboration, which supports demand for scheduling systems that can fit into everyday workforce management rather than remain isolated pilot projects. For buyers in retail, food service, logistics, and healthcare, the value of these tools lies in reducing planner workload while making scheduling decisions more consistent and auditable. The Japanese frontline worker technology market benefits because schedule optimization often becomes the first AI use case with visible labor and compliance value. Once employers trust those outputs, adjacent demand tends to spread into analytics, communication, and performance management.

Unified HR, Payroll, Scheduling, And Communication Stacks

The Japan frontline worker technology market is consolidating around integrated platforms because employers increasingly want one operating layer across attendance, payroll, scheduling, and communication. METI-linked digital transformation guidance for SMEs has given companies and software partners a clearer framework for sequencing front-office, middle-office, and back-office digitization, supporting bundled deployments rather than isolated tools. JETRO also highlighted government support for digital adoption, which helps smaller companies move into cloud systems that connect workforce administration with daily operations. This matters in the Japan frontline worker technology market because disconnected systems create manual re-entry, fragmented records, and slower decisions across shift-based teams. Integrated stacks are therefore attracting attention not only for convenience but also because they reduce labor overhead for businesses with limited administrative capacity. The stronger this integration trend becomes, the harder it will be for point solutions to defend their role unless they offer clear workflow depth or a unique regulatory fit.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Integration Complexity Across HR, Payroll, POS, And EHR Systems | -3.2% | National, most acute in large enterprise and government-adjacent sectors | Long term (≥ 4 years) |

| Workforce Data Privacy And Mobile Cybersecurity Exposure | -2.1% | National, with heightened concern in healthcare and financial services | Medium term (2-4 years) |

| Shared-Device Identity And Digital Access Gaps | -1.4% | National, with the greatest impact in manufacturing and logistics sites using shared-device workflows | Medium term (2-4 years) |

| Manager And Worker Distrust Of Opaque Scheduling AI | -0.9% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Legacy Integration Complexity Across HR, Payroll, POS, And EHR Systems

The Japan frontline worker technology market still faces a major drag from legacy systems that were not built for cloud interoperability or real-time data exchange. OECD findings from 2025 showed that 35.3% of Japanese companies already using generative AI saw integration with existing systems as a material challenge, highlighting how back-end complexity can significantly slow front-end adoption. In many large organizations, HR, payroll, POS, and clinical records still sit across separate vendor stacks, so a frontline deployment often depends on custom connectors before the business can see full value. Advantech documented this issue in Japan through a manufacturing case in which real-time production visibility required a custom architecture linking machines, SCADA systems, digital forms, and ERP workflows, even though the project later eliminated 1,020 hours of annual manual paperwork.[5]Advantech, “Bridging the Labor Gap in Japan, Digital Transformation with Nippon RAD and Advantech’s Solutions,” Advantech, advantech.com That pattern means vendors with pre-built links into dominant enterprise systems hold a practical advantage in the Japan frontline worker technology market, especially where buyers cannot afford long deployment cycles. Until legacy replacement moves faster, integration effort will remain one of the clearest reasons some deployments stall or scale more slowly than planned.

Workforce Data Privacy And Mobile Cybersecurity Exposure

The Japan frontline worker technology market also has to navigate rising privacy and cybersecurity concerns as more tools capture location, behavioral, and health-related data on mobile and shared devices. OECD reporting from 2025 found that 54.9% of Japanese companies adopting generative AI cited security risks as a key concern, indicating that risk perception is broad and not limited to a small set of regulated sectors. The issue becomes sharper in healthcare and industrial safety settings because employers may handle both worker health data and operational records on the same device or workflow. Microsoft has been positioning cybersecurity and AI infrastructure together in Japan, which reflects the fact that buyers increasingly treat secure deployment as part of the purchase decision rather than a later add-on. In the Japan frontline worker technology market, vendors that can minimize the movement of sensitive data and support stronger identity controls are better positioned to win regulated accounts. Privacy concerns are therefore not only a compliance issue, but also shape product design, deployment scope, and the speed of enterprise approval.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Leadership Sets The Revenue Base While Services Expand With Deployment Needs

Software accounted for 69.43% of the Japan frontline worker technology market in 2025, which made it the largest component by a wide margin. This position reflects strong demand for scheduling, communication, analytics, and learning tools that sit closest to daily frontline operations. The Japan frontline worker technology market share in software also benefits from contract stickiness, as large clients often buy several modules over the course of longer enterprise relationships. Once communication and workforce coordination move to a single platform, switching becomes harder because the software is tied to payroll flows, labor rules, and internal user habits. That pattern keeps software at the center of the Japan frontline worker technology market even as competition widens across global and domestic vendors.

Services are projected to grow at a 25.92% CAGR through 2031, indicating that deployment support is becoming increasingly valuable as adoption broadens. The Japan frontline worker industry is not only buying licenses, because many firms also need integration, configuration, training, and operational support to move away from paper-led workflows. This is especially relevant where internal IT capacity is limited, and buyers want guided rollouts that reduce disruption across shifts and sites. METI-linked SME digital transformation frameworks have also supported more structured deployment roadmaps, giving implementation partners a greater role in platform adoption and scaling. As the Japan frontline worker technology market shifts toward AI-enabled, multi-module systems, services should continue to rise, as implementation depth becomes part of the value captured in each software sale.

By Deployment: Cloud Builds The Fastest Adoption Path While Hybrid Keeps Strategic Relevance

Cloud-based deployment held 63.91% of the market in 2025 and is projected to grow at a 26.74% CAGR through 2031. That makes Cloud the clear lead model in the Japanese frontline worker technology market, especially for companies that want lower upfront complexity and faster access across distributed teams. The cloud model is a strong fit for deskless work because employees can access applications on smartphones and other mobile devices rather than on fixed office infrastructure. It also supports frequent product updates, which matters in categories such as communication, analytics, and workforce coordination, where functionality is evolving quickly. For many buyers, cloud adoption is therefore becoming the default route into the Japanese frontline worker technology market.

Hybrid deployment still has strategic relevance because some sectors cannot migrate all workflows to a standard cloud architecture at once. Microsoft expanded Azure Local in 2026 for organizations that need customer-controlled infrastructure for mission-critical workloads, which reinforces the continued value of mixed deployment models in regulated and operationally sensitive settings.[6]Microsoft News Center, “Microsoft Deepens Its Commitment to Japan with 10 Billion Investment in AI Infrastructure, Cybersecurity, and Workforce,” Microsoft, microsoft.com In hospitals and large retail chains, legacy record systems and operational software often still require local integration points even as user-facing workflows become more modern. That leaves room for vendors that can give buyers the flexibility to combine centralized administration with local control over certain data and workloads. The Japan frontline worker technology market should therefore remain cloud-led, but hybrid capability will stay important where privacy, continuity, or older infrastructure shape deployment choices.

By Organization Size: Large Enterprises Lead Current Spend While SMEs Form The Next Expansion Layer

Large enterprises accounted for 74.16% of the market in 2025, indicating that the early revenue base of the Japan frontline worker technology market has been built by organizations with larger budgets and existing enterprise software estates. These buyers often entered first through scheduling, HR, and communication tools, and they are now extending spending into analytics, compliance, and operational visibility. Their installed bases also give major vendors a stable route for cross-selling new frontline capabilities into existing enterprise accounts. This is one reason the Japan frontline worker technology market has seen strong interest from global platform vendors with deep HCM and ERP relationships. Large enterprises still anchor today’s revenue, but their role is gradually shifting from initial adoption to platform expansion.

SMEs are projected to grow at a 26.31% CAGR through 2031, making them the fastest-growing segment in the Japan frontline worker technology market. OECD data showed that AI adoption rose sharply with company size in Japan, suggesting smaller businesses still have a meaningful adoption gap that can close over the forecast period. JETRO’s digital support initiatives also help reduce cost and adoption barriers for smaller firms entering cloud services for the first time. The Japan frontline worker industry is therefore opening up to vendors that can simplify deployment, lower entry costs, and align with the operating realities of companies with limited administrative staff. As that happens, SME demand is likely to increase, with more first-time buyers and greater pressure for practical all-in-one products.

By Application: Communication Holds The Largest Base While Analytics Moves Up The Value Curve

Employee communication and engagement accounted for 24.86% of the application market in 2025, making it the largest application area. This reflects the basic need to deliver operational updates, policy changes, and shift information to workers who have often relied on physical notices or verbal instructions. In the Japan frontline worker technology market, communication is often the first digital layer because it delivers immediate value without requiring a full process redesign. Staffbase’s Japan expansion and Japanese-language AI communication features underline how strongly vendors see this use case as an entry point for deskless teams. Once organizations establish that first digital connection, they are better positioned to add scheduling, analytics, and knowledge tools on top of it.

Workforce analytics and performance management are projected to grow at a 28.18% CAGR through 2031, which makes them the fastest-expanding application in the Japanese frontline worker technology market. That growth shows a clear shift from descriptive task monitoring toward prescriptive workforce optimization based on operational data. OECD data on low AI use across several manual occupations suggests that many employers are still early in this journey, leaving room for analytics adoption to accelerate as more workflows become digitized. The value proposition is growing because managers want better visibility into staffing, performance, and compliance across distributed sites without relying on fragmented spreadsheets or verbal updates. As data collection expands through communication and scheduling tools, analytics should continue to gain weight in the Japan frontline worker technology market because it turns operational records into measurable management actions.

By End-User Industry: Manufacturing Holds The Largest Base While Healthcare Advances The Fastest

Industrial manufacturing accounted for 22.94% of the Japan frontline worker technology market in 2025, making it the largest end-user segment. Manufacturing remains central because it combines high frontline worker density with complex shifts, safety demands, and persistent labor shortages. The Japan frontline worker technology market is highly relevant in this setting because factories need better coordination among task execution, workforce availability, and operational oversight. Hitachi’s Naivy verification at a Renesas plant showed how AI-supported frontline coordination can improve performance among less experienced workers in an industrial environment. This helps explain why manufacturing continues to set the base level of demand across software, analytics, and workforce management use cases.

Healthcare and life sciences are projected to grow at a 27.63% CAGR through 2031, which makes them the fastest-growing end-user group in the Japan frontline worker technology market. Fujitsu introduced an AI agent platform for healthcare in August 2025, designed to support staff reallocation and reduce waiting times, demonstrating how frontline tools are moving into broader hospital operations and care delivery workflows. Sumitomo Corporation also completed the rollout of the FIKAIGO service across all 290 SOMPO Care residential facilities in June 2025, directly supporting more than 10,000 care workers through automated shift scheduling and related back-office support. These examples show that healthcare and eldercare demand is not limited to experimentation, because real deployments are already occurring at a meaningful scale. As medical and care providers face staffing shortages and stronger digitalization pressure, this segment is likely to remain one of the clearest growth engines for the Japan frontline worker technology market.

Geography Analysis

The Japan frontline worker technology market size stands at USD 0.74 billion in 2026 and is forecast to reach USD 2.16 billion by 2031 at a 23.80% CAGR, which reflects one of the strongest growth profiles for targeted frontline solutions in the region. Japan is attracting investment in front-office and operational digitization because labor pressure is forcing employers to modernize how they manage deskless work across industries and care settings. Microsoft is investing USD 10 billion in Japan from 2026 to 2029 across AI infrastructure, cybersecurity, and workforce development, including training support for frontline industrial workers. The same announcement noted that 94% of Nikkei 225 companies use Microsoft 365 Copilot, which suggests that the broader enterprise software base in Japan is becoming more ready to extend AI into field operations. OECD reporting also showed clear regional variation in workplace AI use, with Tokyo and the Kanto region far ahead of some rural prefectures, indicating that adoption capacity remains uneven across the country.

The strongest near-term demand centers sit in industrial and population-heavy corridors where labor shortages, infrastructure, and enterprise concentration combine. Chubu, especially Aichi Prefecture, remains important because automotive and precision manufacturing operations there have high frontline staffing needs and complex processes. Kansai also stands out because Osaka and Kobe bring together industrial, logistics, healthcare, and service-sector demand that matches several of the main use cases in the Japan frontline worker technology market. Hitachi’s work on frontline AI in industrial settings fits this geographic pattern because its practical value is clearest where skills transfer and production continuity matter most. Tokyo and adjacent prefectures remain influential in platform rollout because they combine larger enterprise footprints with stronger access to digital talent, partner ecosystems, and implementation capacity.

Hokkaido and Tohoku represent a different opportunity set because agriculture, logistics, and eldercare are more prominent there, and labor shortages are often more severe in absolute terms. In these areas, adoption is likely to favor simpler, mobile-first, cloud-led tools that reduce infrastructure dependency and support Japanese-language frontline use. The Japan frontline worker technology market size is therefore not only a metropolitan story, because the medium-term expansion path also depends on how effectively vendors reach non-urban sites with practical deployment models. Japan’s growth profile also stands apart from many Asia-Pacific peers because value creation is increasingly coming from integrated, AI-enabled stacks rather than from first-time software penetration alone. That makes the Japan frontline worker technology market more dependent on localization, workflow depth, and compliance fit than on volume alone.

Competitive Landscape

The Japan frontline worker technology market is moderately fragmented, with competition spread across global enterprise software vendors, frontline-focused specialists, and domestic technology groups with existing industrial or healthcare relationships. Microsoft, SAP, and Oracle remain influential because many large customers already use their HCM and ERP systems, which gives them a direct route into adjacent frontline capabilities. In this part of the Japan frontline worker technology market, the main advantages come from deep integration, account control, and the ability to bundle workforce tools into broader enterprise platforms. Purpose-built vendors such as WorkForce Software, Deputy, Connecteam, Beekeeper, Staffbase, and WorkJam compete differently by focusing on deskless-first usability, mobile delivery, and faster workflow configuration. Staffbase reinforced this strategy through a Japan-dedicated support expansion in January 2026 and a Japanese-language AI feature launch in April 2026, showing how localization is becoming a real requirement rather than a marketing add-on.

Hardware-linked players add a separate layer of competition because mobile devices, rugged endpoints, and edge systems remain important in field environments. Panasonic Connect strengthened that position in May 2026 through its collaboration with Red Hat to preload edge software on TOUGHBOOK devices for industrial automation and related frontline settings. This kind of move matters in Japan's frontline worker technology market because some buyers still prefer tightly integrated hardware and software combinations for operational continuity and security. Domestic incumbents also have an important structural edge because they already serve large Japanese clients across IT, OT, healthcare systems, and public-sector projects. That installed trust can make local deployment, integration, and support more credible than what a new entrant can offer on a stand-alone basis.

Hitachi illustrates this domestic advantage through its Lumada 3.0 direction and the Naivy AI agent, which extends frontline augmentation into a broader environment of enterprise and operational data. Fujitsu is building a similar position in healthcare through its AI agent platform created with NVIDIA and shaped around medical workflow knowledge, which gives it relevance in one of the fastest-growing end-user categories. L is B has also shown the value of local specialization by expanding its direct communication platform across all Obayashi construction sites in April 2026. The Japan frontline worker technology market is therefore becoming more competitive, but scale alone is not enough because language fit, regulatory readiness, and deployment credibility still shape who wins. Vendors that combine local workflow understanding with broader platform depth are likely to remain best positioned as the market moves from basic digitization into integrated frontline operating systems.

Japan Frontline Worker Technology Industry Leaders

Fujitsu Limited

NEC Corporation

Panasonic Connect Co., Ltd.

Honeywell International Inc.

Zebra Technologies Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Red Hat and Panasonic Connect announced a collaboration to preload Red Hat Device Edge on Panasonic TOUGHBOOK ruggedized devices, targeting real-time edge data processing for industrial automation, smart manufacturing, and defense applications, directly relevant to Japan's heavy industrial frontline environments.

- April 2026: Microsoft announced a USD 10 billion investment in Japan from 2026 to 2029, covering AI infrastructure, cybersecurity, and workforce training. The investment includes a partnership with the Japanese Electrical, Electronic, and Information Technology Union, providing foundational AI skills to approximately 580,000 frontline industrial workers and scaling nationally from a pilot launched in October 2025.

- January 2026: Staffbase strengthened its Japan-dedicated support infrastructure by adding a specialized Japanese-language onboarding and operations team, ahead of the April 2026 launch of AI Podcast and AI Assistant features for frontline workers without PCs.

- November 2025: Staffbase launched "Employee AI," positioned as the world's first AI-native employee experience platform, in Tokyo. The platform addresses Japan's 7% employee engagement rate by delivering personalized, role-specific audio and conversational AI content to frontline workers across manufacturing, healthcare, retail, and logistics sectors.

Japan Frontline Worker Technology Market Report Scope

The Japan Frontline Worker Technology Market Report is Segmented by Component (Software, and Services), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Employee Communication and Engagement, and More), and End-User Industry (Retail and E-Commerce, Industrial Manufacturing, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Employee Communication and Engagement |

| Workforce Execution and Task Management |

| Workforce Scheduling and Coordination |

| Learning and Knowledge Enablement |

| Workforce Analytics and Performance Management |

| Safety and Compliance Management |

| Other Applications |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Hospitality |

| Construction |

| Government and Public Administration |

| Other Industries |

| By Component | Software |

| Services | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Employee Communication and Engagement |

| Workforce Execution and Task Management | |

| Workforce Scheduling and Coordination | |

| Learning and Knowledge Enablement | |

| Workforce Analytics and Performance Management | |

| Safety and Compliance Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Industrial Manufacturing | |

| Healthcare and Life Sciences | |

| Transportation and Logistics | |

| Hospitality | |

| Construction | |

| Government and Public Administration | |

| Other Industries |

Key Questions Answered in the Report

What is the current and forecast value of the Japan frontline worker technology market?

The Japan frontline worker technology market size is USD 0.74 billion in 2026 and is forecast to reach USD 2.16 billion by 2031 at a CAGR of 23.80%.

What is driving adoption of frontline worker technology in Japan?

The strongest demand drivers are labor shortages, workforce aging, mobile-first digitization of deskless work, and rising interest in AI-based scheduling and analytics.

Which component leads spending in Japan frontline worker technology?

Software led the market with 69.43% share in 2025, reflecting strong demand for scheduling, communication, analytics, and learning tools.

Which deployment model is expanding the fastest?

Cloud-based deployment is the largest and fastest-growing model, with 63.91% share in 2025 and a projected 26.74% CAGR through 2031.

Which end-user segment is growing the fastest?

Healthcare and life sciences are projected to grow at a 27.63% CAGR through 2031, supported by staffing shortages and digitalization needs in care delivery.

What is shaping competition among vendors in Japan?

Competition is split across global enterprise suites, specialist frontline software firms, and domestic incumbents that bring stronger local integration, language fit, and client relationships.

Page last updated on: