Japan Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

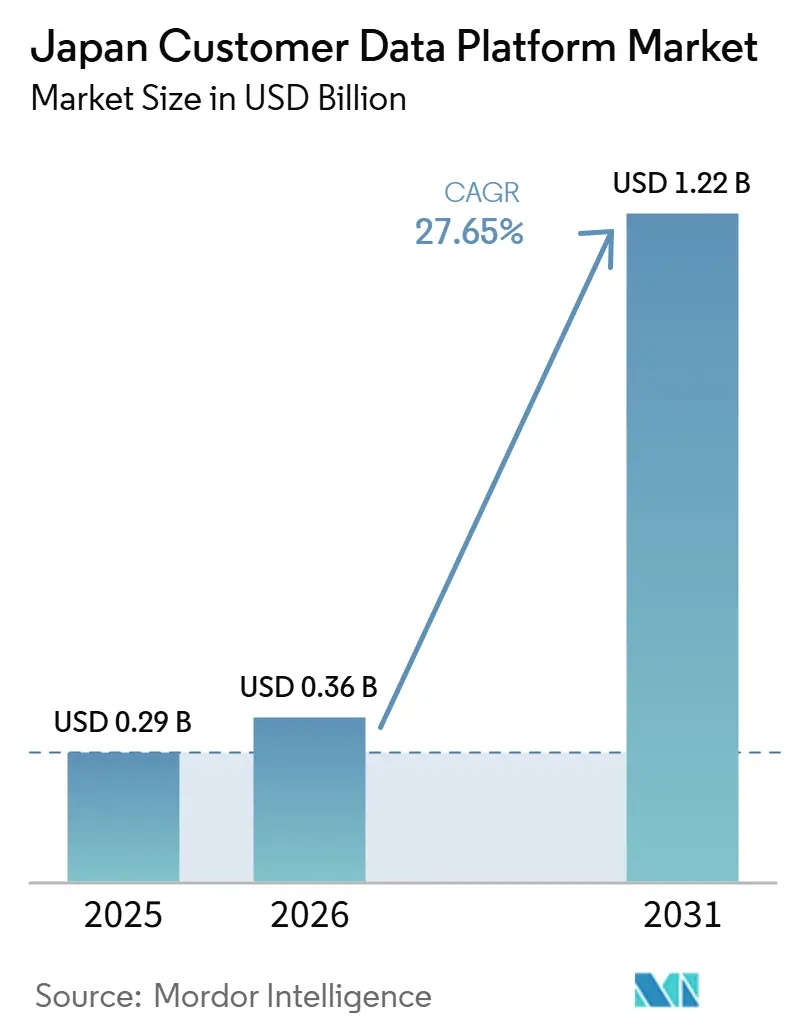

| Base Year Market Size (2025) | USD 0.29 Billion |

| Market Size (2026) | USD 0.36 Billion |

| Market Size (2031) | USD 1.22 Billion |

| Growth Rate (2026 - 2031) | 27.65% CAGR |

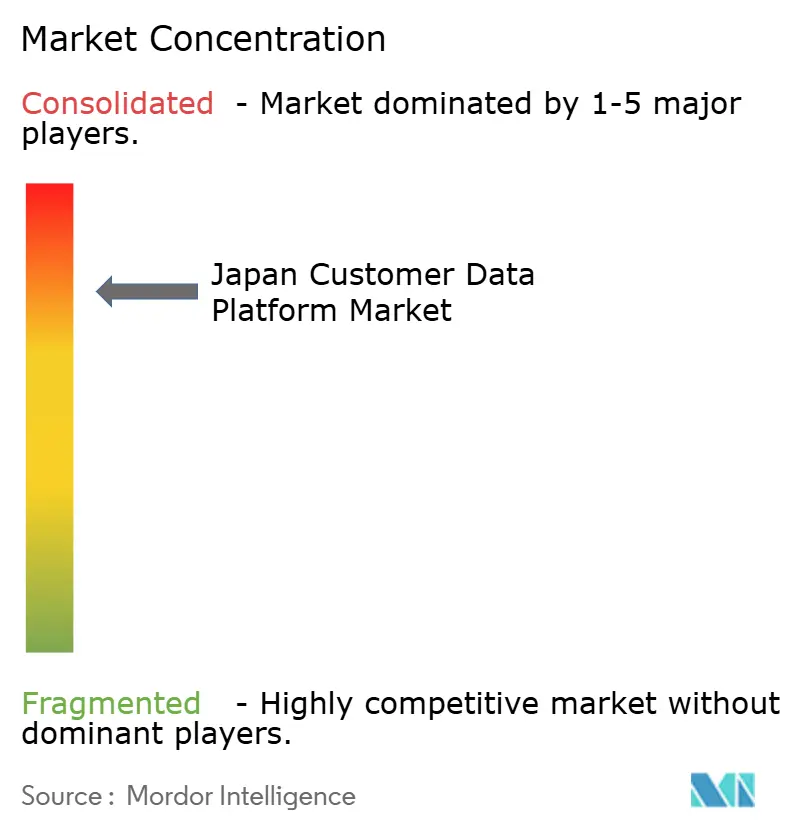

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Customer Data Platform Market Analysis by Mordor Intelligence

The Japan customer data platform market size is expected to increase from USD 0.29 billion in 2025 to USD 0.36 billion in 2026 and reach USD 1.22 billion by 2031, growing at a CAGR of 27.65% over 2026-2031. Demand is rising because many enterprises still manage offline retail records, loyalty databases, mobile engagement data, and e-commerce activity in separate systems, which keeps identity unification high on digital investment agendas. The June 2025 digital society priority plan provided stronger policy support for enterprise data linkage, which helped move more projects from pilot work to live deployment. Better cloud readiness is also making platform rollout easier, even as regulated users continue to keep sensitive workloads under tighter governance models. Competitive pressure remains uneven because Treasure Data keeps a strong local base, while Salesforce, Adobe, and Braze are targeting accounts that already use their wider marketing platforms. The next phase of growth will depend on how quickly enterprises outside the top tier improve governance, deployment readiness, and internal execution as privacy obligations and talent shortages raise the cost of delay.

Key Report Takeaways

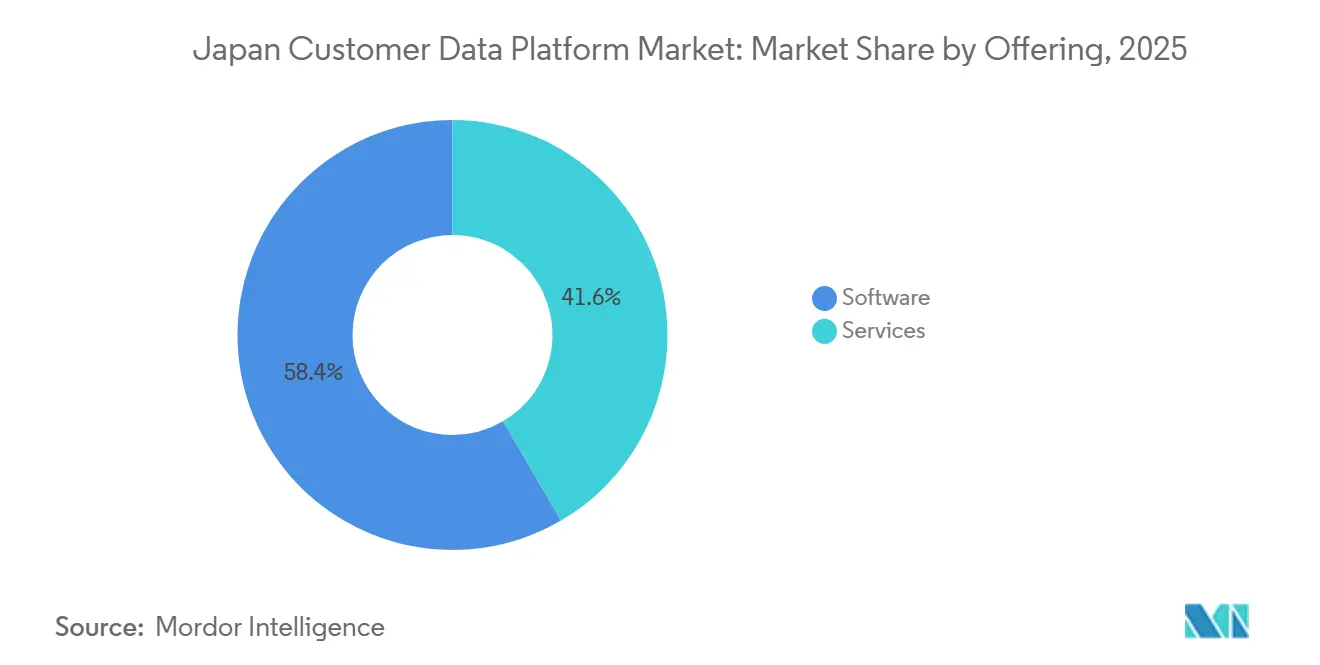

- By offering, software held 58.42% share of the Japan customer data platform market in 2025, while services are projected to expand at a 29.73% CAGR through 2031.

- By deployment mode, cloud held a 63.19% share in 2025, while hybrid deployment is expected to record the fastest growth at a 31.84% CAGR through 2031.

- By organization size, large enterprises accounted for 61.27% of the market share in 2025, while SMEs are projected to grow at a 30.16% CAGR through 2031.

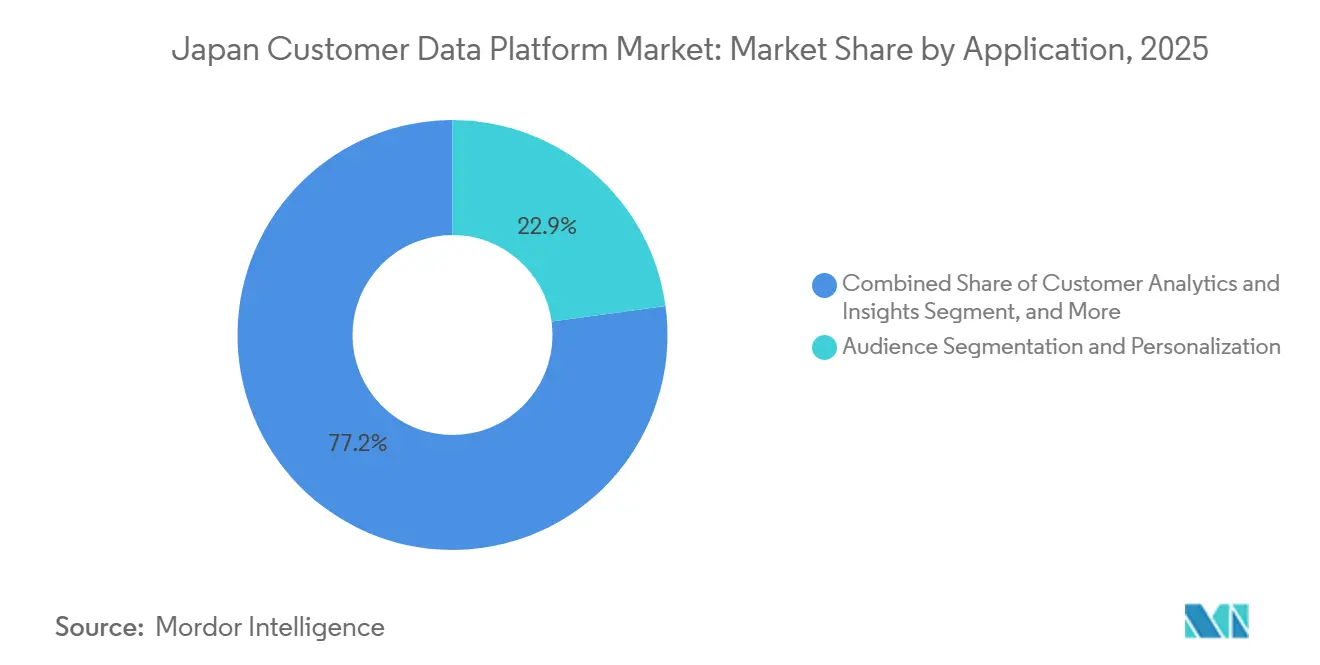

- By application, audience segmentation and personalization led with a 22.85% share in 2025, while customer analytics and insights are expected to expand at a 32.41% CAGR through 2031.

- By end-user industry, retail and e-commerce held 25.64% share in 2025, while healthcare and life sciences are projected to grow at a 28.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unified Customer Profiles Across Offline and Digital Touchpoints | +5.5% | Japan-wide, with the highest concentration in Tokyo, Osaka, and Nagoya metro areas | Medium term (2-4 years) |

| AI and Machine Learning Adoption in Marketing Decisioning | +7.2% | National, with early gains among enterprise retailers and financial services firms in the Tokyo-Kansai corridor | Short term (≤ 2 years) |

| Retail Media, E-Commerce, and First-Party Data Activation | +4.8% | National, with spillover into regional prefectures through digital commerce and drugstore retail networks | Short term (≤ 2 years) |

| Consent Management and Data Governance Pressure | +3.9% | National, with compliance urgency strongest in BFSI, healthcare, and retail | Medium term (2-4 years) |

| Composable CDP Architecture Demand in Data-Mature Enterprises | +3.1% | Tokyo metropolitan area, with early adopters in Osaka and Nagoya enterprise clusters | Long term (≥ 4 years) |

| LINE-Centric Engagement and Identity Resolution Needs | +2.8% | National, with the highest density in mobile-first consumer verticals such as retail, beauty, and food services | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated AI and Machine Learning Adoption in Marketing Decisioning

AI is becoming a structural part of enterprise marketing operations, and that shift is speeding up refresh cycles across the Japan customer data platform market as buyers reassess older platforms against newer agent-led models. Treasure Data launched Marketing Super Agent in January 2026, bringing audience intelligence, strategy support, creative development, activation, and real-time optimization into a single, governed enterprise workspace.[1]Treasure Data, Inc., “Treasure Data Launches Marketing Super Agent,” Treasure AI, treasure.ai Treasure Data then repositioned its broader platform in May 2026 as Treasure AI, which showed that vendors now view the CDP less as a passive database and more as a live context layer for autonomous execution. Salesforce Japan took a similar path in March 2026, combining Data 360, MuleSoft, and Informatica into a unified, trusted context model to provide AI agents with cleaner, governed customer data across systems. That vendor behavior is changing evaluation criteria across the Japan customer data platform market because procurement now depends more on workflow automation and live context delivery than on audience building alone. It also favors platforms that can connect governed data, decision logic, and execution in a single environment rather than relying on loosely linked external tools.[2]Salesforce Japan Co., Ltd., “Salesforce Provides Trusted Context for AI Agents in the Japanese Market in Collaboration with Informatica,” Salesforce Japan, salesforce.com

Rising Need for Unified Customer Profiles Across Offline and Digital Touchpoints

A large share of customer activity in Japan still sits across physical stores, loyalty programs, e-commerce systems, and LINE-linked business accounts, which keeps identity resolution central to the Japan customer data platform market. Kao’s My Kao platform handled close to 10 million annual visitors and 1.6 million monthly unique users, underscoring why simple data stitching is no longer enough for enterprise profile management.[3]Dentsu Soken, “1st Party Data Integration and Direct Customer Marketing Platform, Kao Corporation Case,” Dentsu Soken, dentsusoken.com TOPPAN and Treasure Data launched a hybrid customer experience service in November 2025 that connected CDP data with direct mail, sampling, and contact center activity, reflecting the need to bridge physical and digital contact points into a single flow. That operating model is especially important in the Japan customer data platform market because the local commerce environment still depends heavily on offline conversion paths that global digital-first products often treat as secondary. The Digital Agency’s June 2025 priority plan also included data linkage and utilization in the country’s formal digital agenda, providing enterprises with stronger backing for broader rollout decisions. As a result, vendors that can unify retail, loyalty, service, and messaging identities are in a stronger position than those that build mainly for browser-led activation.

Rapid Shift Toward Retail Media, E-Commerce, and First-Party Data Activation

Retail media is expanding quickly in Japan, and that is raising the value of first-party identity activation across the Japan customer data platform market as cookie-dependent targeting becomes less reliable.[4]True Data Co., Ltd., “Hakuhodo DY ONE’s AudienceOne and True Data Advertising Purchase Data Launch Japan’s First Integration,” True Data, truedata.co.jp Catalina Marketing Japan launched AOUMI in August 2025 as a national retail media network built on ID-POS purchase data from major drugstores and supermarkets. Hakuhodo DY ONE and True Data also launched Japan’s first linkage between a DMP and purchase data in January 2025, which enabled targeting across OTT, DOOH, and metaverse channels using purchase segments drawn from close to 60 million consumers. Honeys used the OmniSegment CDP to unify data from close to 10 million members across more than 800 stores and digital channels, enabling abandoned cart recovery and dormant customer reactivation through AI-led personalization. These cases matter because the Japan customer data platform market is not only supporting campaign delivery, but it is increasingly tied to retail media participation, conversion recovery, and shopper monetization across hybrid commerce networks. Vendors that can extend CDP data into clean-room-compatible, retail media-ready workflows are, therefore, better aligned with where enterprise budgets are moving.

Increased Regulatory Pressure on Consent Management And Data Governance

Privacy governance is becoming a stronger design factor across the Japan customer data platform market because APPI obligations now affect how live customer profiles, digital identifiers, and downstream activation rules are managed. Japan’s privacy framework treats cookies, IP addresses, and device IDs as person-related information in relevant contexts, making consent management a key factor for cross-channel personalization programs. The regulatory direction is also pushing enterprises to keep consent signals closer to the active profile layer rather than leaving them in separate compliance records that are slow to update. That pressure favors vendors with native consent and preference controls because those tools reduce the risk of mismatched permissions across campaign, analytics, and service workflows. It also meets the hybrid deployment demand in the Japan customer data platform market, as regulated users want stronger control over where sensitive records reside and how identity data moves. In practice, compliance is no longer a separate workstream; it is now part of platform selection, architecture choice, and service demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy CRM, POS, and Marketing Stack Integration Complexity | -3.6% | National, with the sharpest pressure in manufacturing, traditional retail, and banking | Long term (≥ 4 years) |

| In-House Data Engineering and CDP Administration Talent Shortage | -2.9% | National, with deeper gaps in regional cities than in Tokyo and Osaka | Medium term (2-4 years) |

| Difficult ROI Justification for Mid-Sized and Traditional B2B Users | -2.1% | National, most visible outside large enterprise and high-frequency B2C verticals | Medium term (2-4 years) |

| Identity Matching and Data Quality Gaps During Implementation | -1.7% | National, concentrated in organizations with fragmented POS and legacy CRM schemas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity With Legacy CRM, POS, And Marketing Stacks

Legacy integration remains a major brake on the Japan customer data platform market, as many enterprises still run customized ERP, CRM, and POS systems that were not built for real-time profile orchestration. Chiba Bank’s 2025 rollout required NTT Nippon Info to build a custom layer with Snowflake as an intermediary before Treasure Data CDP could unify account data and digital behavior signals. That example showed that even well-resourced institutions face multi-step architecture work before the platform can reach day-to-day business use. Dentsu Soken launched DendroBium in November 2025 as a composable CDP construction service on Databricks, directly addressing this integration burden through a lakehouse-led model with implementation support. Even so, the approach still depends on data engineering capability and coordinated system work that many mid-sized firms do not yet manage internally. Longer integration cycles delay value realization, widen implementation risk, and keep services demand high across the Japan customer data platform market.

Shortage of In-House Data Engineering and CDP Administration Talent

Talent availability is another clear restraint because enterprises often buy the platform before they build the internal operating capability needed to sustain the Japan customer data platform market at scale. The 2025 White Paper on Small Enterprises from METI identified technology skill deficits as the main barrier to digital transformation progress among smaller firms. SMRJ reported in February 2026 that 39.1% of SMEs were engaged in or considering DX and that AI utilization rose to 28.4%, yet platform administration capacity remained a practical bottleneck for turning interest into execution. That shortfall is helping managed services gain ground because buyers need migration help, operating support, and faster path-to-value models rather than software access alone. Treasure Data’s migration support and Replace and Growth program, which reduced migration effort by up to 60%, reflected the commercial pull of service-heavy delivery in this environment. Unless the talent base deepens more broadly, vendors with strong implementation and managed-service capacity will continue to capture a larger share of near-term demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Growth Is Being Lifted By Execution Needs

Software held 58.42% of the Japan customer data platform market share in 2025, and that lead reflected the scale of existing platform subscriptions across retail, banking, and manufacturing accounts that had already committed to formal customer data programs. The software layer remained the base of most deployments because enterprises first needed the core identity, profile, segmentation, and orchestration engine before they could expand into broader service-led operating models. Large organizations also tended to buy into broader ecosystems, which meant software renewals were often tied to existing cloud, CRM, or analytics contracts rather than evaluated as isolated purchases. That purchasing pattern gave the software segment a durable installed base, particularly in areas where CDP adoption had already moved beyond proof-of-concept work into ongoing enterprise programs. It also explains why software leadership remained intact even as implementation burdens made the operating side of the business increasingly important with each new rollout.

Services are projected to expand at a 29.73% CAGR, and that pace shows where the Japan customer data platform market size is moving fastest as deployment complexity rises faster than in-house readiness. PrimeNumber’s prime Insight-First CDP, launched in June 2026, used AI agents to generate insight reports and design blueprints, promised live deployment in as few as 2 months, and targeted close to half the cost of traditional packaged platforms. Dentsu Soken’s DendroBium followed a similar approach by combining lakehouse architecture, analytics design, and implementation consulting within a single client engagement. These offers show that buyers are paying for operational delivery, migration support, and architecture simplification as much as for software capability. The services segment is therefore benefiting from the same issues that restrain adoption, meaning implementation difficulty is also creating a larger revenue pool for providers that can carry projects from design to production.

By Deployment Mode: Hybrid Models Are Closing The Gap With Pure Cloud

Cloud held 63.19% of the Japan customer data platform market in 2025, and that lead came from enterprise-standardization in hyperscaler environments with local data center support and greater operational flexibility. Cloud deployments also aligned well with faster activation needs, as marketing teams sought more scalable access to analytics, audience tools, and orchestration layers without waiting for internal infrastructure buildouts. For many commercial users, the cloud model reduced deployment friction by keeping CDP functions closer to the rest of the modern marketing and analytics stack. This helped the cloud segment stay ahead even as compliance debates became sharper and more detailed across regulated verticals. It also gave global vendors a clearer entry path, with local data center readiness and platform ecosystem depth already in place.

Hybrid deployment is expected to record the fastest growth at a 31.84% CAGR, indicating that the Japan customer data platform market is adapting to residency, governance, and workload separation needs rather than abandoning cloud adoption. Large banks, insurers, and manufacturers often need cloud-scale compute for AI and analytics while still keeping selected records or systems under tighter internal control. Treasure Data’s Composable Audience Studio answered that requirement with a zero-copy federated query model that runs against customer environments in Snowflake or Databricks without relocating batch data. That approach matters in Japan because privacy obligations and legacy estates often make full data movement harder than theoretical platform diagrams suggest. On-premises deployments still retained relevance in older regulated institutions, but the faster growth path clearly sat with flexible hybrid models that let enterprises balance cloud agility with control.

By Organization Size: SME Adoption Is Rising From A Smaller Base

Large enterprises held a 61.27% share in 2025, reflecting that the Japan customer data platform market was initially built around retailers, major banks, and industrial groups with existing data teams and formal martech budgets. These organizations had the transaction scale, loyalty depth, and internal sponsorship needed to justify enterprise-wide profile unification earlier than smaller firms. They were also more likely to work with system integrators and global platform vendors, which reduced some of the organizational hesitation that slows first-time adopters. That mix of budget, data volume, and vendor access kept large enterprises ahead even as more compact offerings entered the market. In practice, the largest buyers still set the direction for product requirements, delivery models, and partner ecosystems across the Japan customer data platform market.

SMEs are projected to grow at a 30.16% CAGR, making them the fastest-growing buyer group as lower-priced SaaS tiers and support-led delivery reduce the barrier to entry. SMRJ reported that cloud utilization among SMEs reached nearly 75%, indicating that a significant portion of the technical base for CDP adoption was already in place by early 2026. The same survey also showed AI utilization at 28.4%, up by 14.1 percentage points, indicating rising openness to data-driven operating models, even if execution remained uneven. METI’s 2025 SME white paper made clear that unclear returns on digital investment still held back decision-making, so ROI visibility remained more important than technical access for this segment. Vendors that package customer reactivation, cart recovery, and loyalty uplift into clearer templates are therefore better placed to convert SME interest into live subscription revenue.

By Application: Analytics Is Moving Ahead of Legacy Targeting Priorities

Audience segmentation and personalization held a 22.85% share in 2025, reflecting the long-standing importance of loyalty-led targeting across retail and financial services use cases in the Japan customer data platform market. Many enterprises first adopted CDP functions to improve message relevance, connect offline and digital histories, and support campaign decisions with a more complete customer record. That kept segmentation at the center of commercial use by directly supporting near-term activation, retention, and campaign personalization. Retail examples, such as Honeys, showed that the practical value of unified segments still extended to cart recovery and dormant user reactivation across store and e-commerce channels. The installed base built around these everyday activation needs explains why segmentation remained the largest application block even as the product category itself expanded.

Customer analytics and insights are projected to grow at a 32.41% CAGR, making this the fastest-growing part of the Japan customer data platform market as buyers shift from describing past behavior to predicting future actions. Kao’s My Kao deployment showed that predictive analysis at consumer scale depends on a platform built for unified data handling rather than on a reporting layer attached to older CRM systems. Marketing Super Agent and Salesforce’s trusted context architecture both rely on governed identity and live signals, which means analytics quality is becoming a required input for the next wave of automation. This shifts the application mix because orchestration, profile unification, and consent management now depend more heavily on strong analytic context than they did in earlier CDP deployments. As that pattern spreads, enterprises are likely to treat analytics infrastructure as a core production layer rather than as a downstream reporting function.

By End-User Industry: Healthcare Is Catching Up To Retail’s Lead

Retail and e-commerce held a 25.64% share in 2025, making the segment the clearest commercial anchor for the Japan customer data platform market, as it combines high transaction frequency, rich loyalty data, and expanding retail media monetization. Retailers were also early adopters because they could more easily connect direct revenue outcomes to personalization, reactivation, and media activation than many other industries. National retail media growth further strengthened this lead by making unified purchase and customer identity data more valuable for both advertisers and merchants. That operating logic kept retail at the top even as other verticals began building their own first-party data programs focused on compliance and service improvement. The segment still sets many product expectations for activation speed, identity quality, and omnichannel decisioning across the broader vendor landscape.

Healthcare and life sciences are projected to grow at a 28.93% CAGR, indicating where the Japan customer data platform market is poised to expand next as health data reforms broaden the scope for consented data use. The 2025-2026 reform direction created more legal and operational space for secondary use of medical data and personal health records inside consent-based data platforms. In May 2026, SMBC Group, Fujitsu, and SoftBank entered an alliance to build a Japan-developed healthcare data platform for secure medical data management and AI-enabled personal health applications. That move showed that CDP-like architectures are reaching deeper into healthcare institutions, where trust, permission control, and data portability matter as much as marketing activation. BFSI, telecom, media, manufacturing, and public administration remain important, but healthcare is now one of the clearest growth pools beyond the retail core.

Geography Analysis

The Japan customer data platform market remained centered on the Greater Tokyo metropolitan area, as most of the country’s largest enterprises in retail, banking, insurance, consumer goods, and IT services maintain their headquarters there. Tokyo-based organizations led first-wave deployments because they were closer to major system integrators, digital agencies, and CDP vendor teams that could support more complex implementations. The local concentration of implementation partners also reduced friction in architecture design, integration planning, and ongoing administration for early adopters. That concentration still leaves regional labor pools thinner, which matters because deployment quality depends heavily on data engineering and operating support rather than on software access alone. The Ministry of Internal Affairs and Communications published its Digital Infrastructure Development Plan 2030 in June 2025, which targeted data center decentralization to regional areas with available power capacity.

The Osaka-Kansai corridor formed the second major demand cluster in the Japan customer data platform market, supported by pharmaceutical companies, consumer goods manufacturers, healthcare institutions, and large retailers with strong regional roots. Health data reform momentum gave this corridor additional weight because healthcare-related organizations had stronger reasons to modernize their consented data-handling and service personalization models. Retailers and drugstore chains based in the region also had reason to participate in national retail media networks that depend on stronger first-party data activation. Expo 2025 in Osaka supported wider digital marketing investment through 2025 and helped bring visitor personalization use cases into local deployment discussions. Outside Tokyo, Osaka, and Nagoya, regional financial institutions still looked underpenetrated, especially where branch CRM data and digital channel signals remained separated.

Japan’s position as the home market for LINE and Yahoo Japan's commercial identity services presents the Japan customer data platform market with a distinct identity challenge that is less common in other Asia-Pacific countries. LY Corporation unified LINE Business ID and Yahoo Japan Business ID in June 2025, creating a more common enterprise identity layer but also raising the value of better profile reconciliation across social, loyalty, e-commerce, and offline records. Enterprises, therefore, need stronger identity quality in Japan than in many markets where social-commerce identity is less central to customer journeys. SMRJ reported in February 2026 that 39.1% of SMEs were engaged in or considering DX activities, which suggested that regional demand would still be shaped more by national enterprise mandates and public policy than by broad-based organic SME adoption in the near term.

Competitive Landscape

The Japan customer data platform market was consolidated in 2026, with Treasure Data operating as the strongest local incumbent and a second tier of Salesforce Data 360, Adobe Experience Platform, Braze, Tealium, and Oracle competing through broader ecosystem ties. Treasure Data held an estimated 28% domestic share, supported by enterprise relationships, Japanese-language operations, and a product roadmap tailored to local deployment realities. The company strengthened that position again in May 2026, when it relaunched under the Treasure AI concept and announced new partnerships in voice data capture, enrichment, and synthetic data support. Salesforce also made one of the biggest competitive moves in March 2026 by integrating Informatica Japan into its legal entity and combining Data 360, MuleSoft, and Informatica inside a single trusted context model. Those moves show that leadership in the Japan customer data platform market now depends on ecosystem depth, governed data flow, and execution support rather than on profile storage alone.

Open space remained visible at 2 levels, one around simpler SME-grade offers and another around deeper vertical configurations for healthcare, manufacturing, and government where generic horizontal products still leave local gaps. Domestic challengers such as Dentsu Soken’s DendroBium, primeNumber’s prime Insight-First CDP, and b→dash were important because they used cloud data warehouse foundations to lower costs and better align with local integration needs. PrimeNumber’s June 2026 launch was especially notable because it targeted retail and distribution users with AI-generated blueprinting and shorter deployment cycles, which directly addressed mid-market pain points. Treasure Data’s January 2026 Marketing Super Agent and Salesforce’s agent-centered architecture also made clear that AI-led orchestration had become the main competitive field rather than a side feature. That shift is raising pressure on every supplier in the Japan customer data platform market to prove not only data quality, but also workflow usefulness and time-to-value.

Technical architecture is also a competitive issue because regulated enterprises increasingly test whether a vendor can support scale without forcing unnecessary data movement. Treasure Data’s zero-copy Composable Audience Studio appealed to accounts that needed analytics across Snowflake or Databricks while keeping stronger control over residency and batch data placement. That capability aligned with the direction of privacy governance and the realities of complex enterprise data estates in Japan. The result was a market with a clear leader, credible global challengers, and growing domestic specialists, but not a fully fragmented vendor field.

Japan Customer Data Platform Industry Leaders

Treasure Data, Inc.

Salesforce, Inc.

Tealium, Inc.

Plaid, Inc.

Adobe Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: primeNumber launched "prime Insight-First CDP," a composable CDP solution for Japan's retail and distribution sector that uses AI agents to auto-generate customer insight reports and CDP design blueprints, targeting deployment in 2-4 months at an estimated 50% cost reduction versus packaged CDP alternatives. The launch directly targets a gap in the mid-market segment that incumbent vendors have not addressed at accessible price points.

- May 2026: SMBC Group, Fujitsu, and SoftBank entered a basic business alliance to build a Japan-developed healthcare data platform enabling secure medical data management, AI health agents, and personal health record portability under individual consent. This consortium represents a major structural bet on first-party health data activation and signals that CDP-adjacent architectures are penetrating Japan's healthcare value chain at the institutional level.

- May 2026: Treasure Data announced its new Japan FY2026 business strategy, formally relaunching as "Treasure AI," an Agentic Experience Platform, with 4 new strategic pillars including voice data capture through a partnership with PLAUD Inc., a data enrichment alliance with V-Point Marketing, which leverages a 130-million member database, and a synthetic data capability through zypl.ai for AI model training where real data is scarce.

- April 2026: Japan's Cabinet approved and submitted to the Diet an APPI amendment bill introducing administrative fines, biometric data rules, children's data protections, and expanded PPC enforcement powers, expected to take effect within 2 years of promulgation.

Japan Customer Data Platform Market Report Scope

The Japan customer data platform market refers to the ecosystem of software and associated services that enable organizations in Japan to collect, unify, and manage customer data from multiple touchpoints into a single, persistent database. These platforms are designed to break down data silos, creating comprehensive customer profiles that can be leveraged for advanced audience segmentation, personalized marketing campaigns, customer journey orchestration, and predictive analytics. The market encompasses cloud, on-premises, and hybrid deployment models tailored to the operational needs of large, small, and medium enterprises across sectors such as retail, BFSI, healthcare, and IT. By integrating consent and preference management capabilities, CDPs help Japanese businesses comply with stringent local data protection regulations, such as the Act on the Protection of Personal Information (APPI), while enhancing customer experience, driving brand loyalty, and improving overall marketing return on investment.

The Japan Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), and End-User Industry (Retail and E-Commerce, BFSI, Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size outlook for the Japan customer data platform market through 2031?

The Japan customer data platform market is expected to grow from USD 0.36 billion in 2026 to USD 1.22 billion by 2031 at a CAGR of 27.65%.

Why are enterprises in Japan adopting customer data platforms more actively now?

Adoption is rising because enterprises need unified profiles across stores, loyalty programs, LINE, and e-commerce, while digital policy support and stronger AI use are pushing projects beyond pilot stages.

Which deployment model currently leads in Japan?

Cloud led with a 63.19% share in 2025, although hybrid is forecast to grow faster as regulated users balance cloud scale with tighter data control needs.

Which application area is growing the fastest in Japan?

Customer analytics and insights are expected to grow at a 32.41% CAGR through 2031 as enterprises move from historical reporting to predictive decision support.

Why is healthcare becoming more important for CDP vendors in Japan?

Healthcare and life sciences are projected to grow at a 28.93% CAGR because health data reforms and new platform alliances are widening the role of consent-based data use.

Who are the main competitors serving enterprise demand in Japan?

Treasure Data remains the strongest local incumbent, while Salesforce, Adobe, Braze, Tealium, Oracle, and domestic composable providers such as Dentsu Soken and primeNumber continue to compete for enterprise accounts.

Page last updated on: