Japan Bulky Waste Collection Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

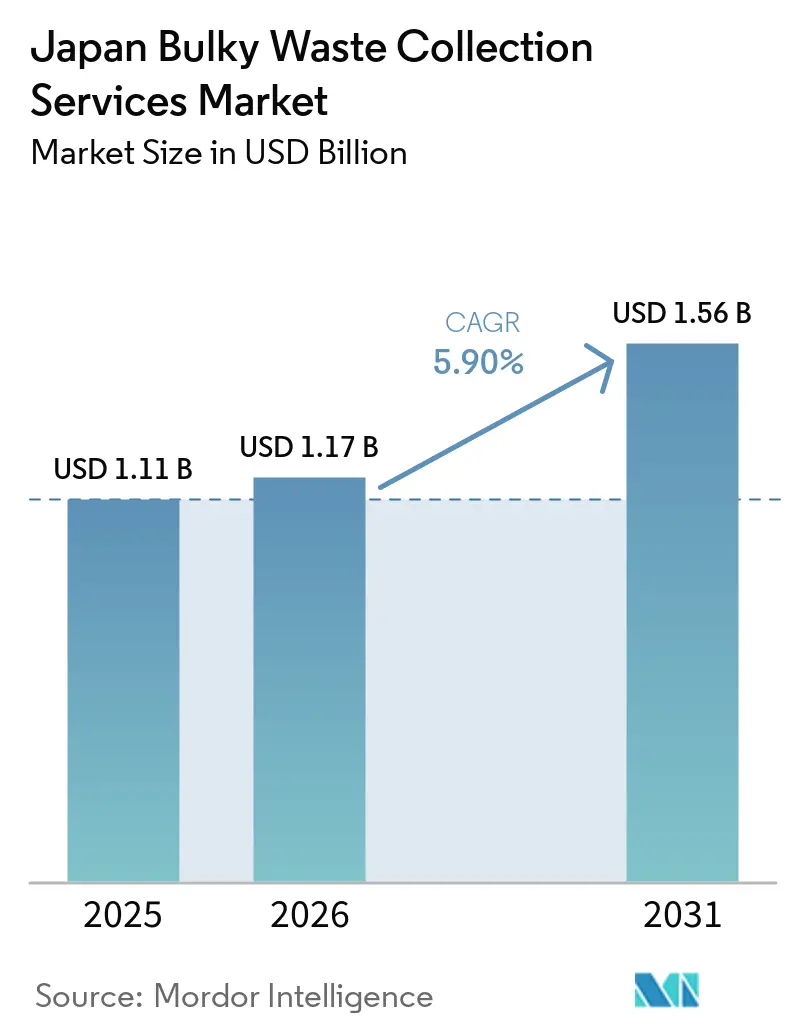

| Base Year Market Size (2025) | USD 1.11 Billion |

| Market Size (2026) | USD 1.17 Billion |

| Market Size (2031) | USD 1.56 Billion |

| Growth Rate (2026 - 2031) | 5.90% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Bulky Waste Collection Services Market Analysis by Mordor Intelligence

The Japan Bulky Waste Collection Services Market size is expected to grow from USD 1.11 billion in 2025 to USD 1.17 billion in 2026 and is forecast to reach USD 1.56 billion by 2031 at 5.90% CAGR over 2026-2031.

The growth outlook aligns with Japan’s push to expand resource circulation as a national priority and scale a JPY 80 trillion (USD 0.51 trillion) circular economy by 2030, which will keep regulatory pressure high on waste diversion and recycling infrastructure. Municipal capacity constraints and dense urban living continue to shape service models that reward route optimization, reverse logistics, and flexible scheduling. Operators that integrate collection with material recovery and compliant treatment will be positioned to capture value as municipal plans expand circular-economy implementation, as corporate Scope 3 disclosures increase. The Japan bulky waste collection services market is also influenced by demographic aging, which shifts volumes toward episodic residential pickups tied to downsizing and estate clearance events rather than weekly cycles.

Key Report Takeaways

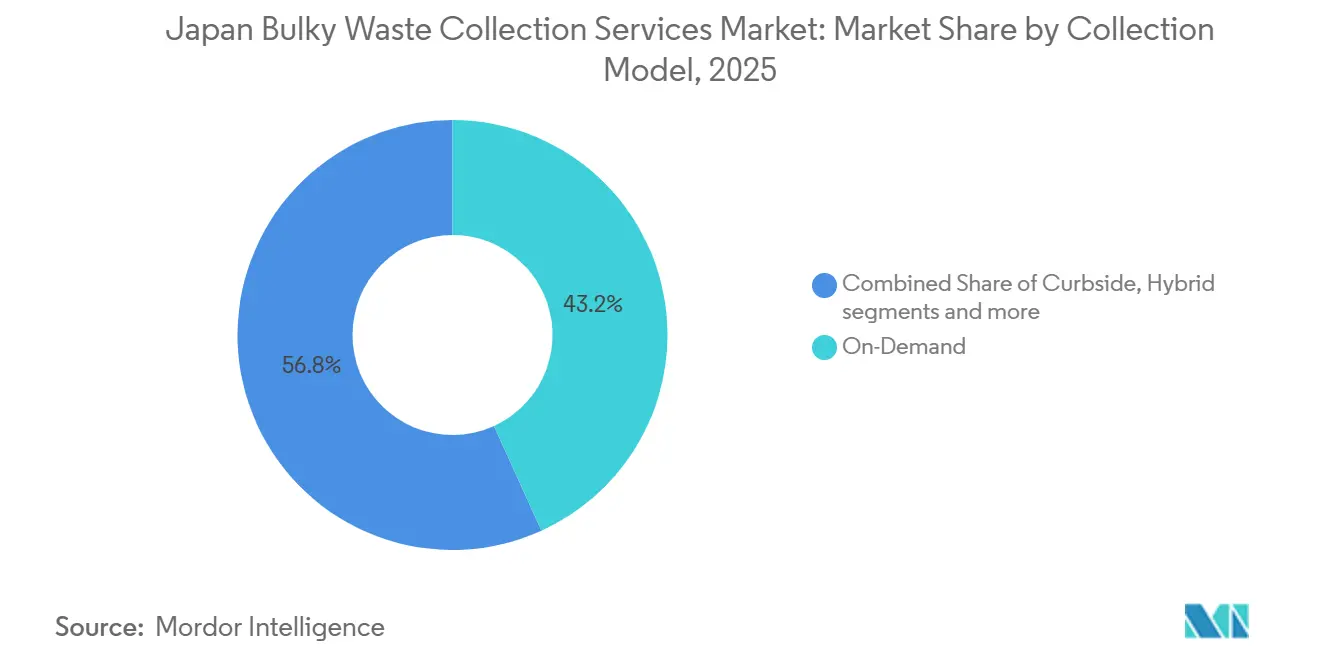

- By collection model, On-Demand held 43.21% of the Japan bulky waste collection services market share in 2025 and is projected to grow at 6.21% CAGR through 2031.

- By source, the Residential segment accounted for 58.78% of the Japan bulky waste collection service market size in 2025 and is slated to grow at a 6.72% CAGR through 2031.

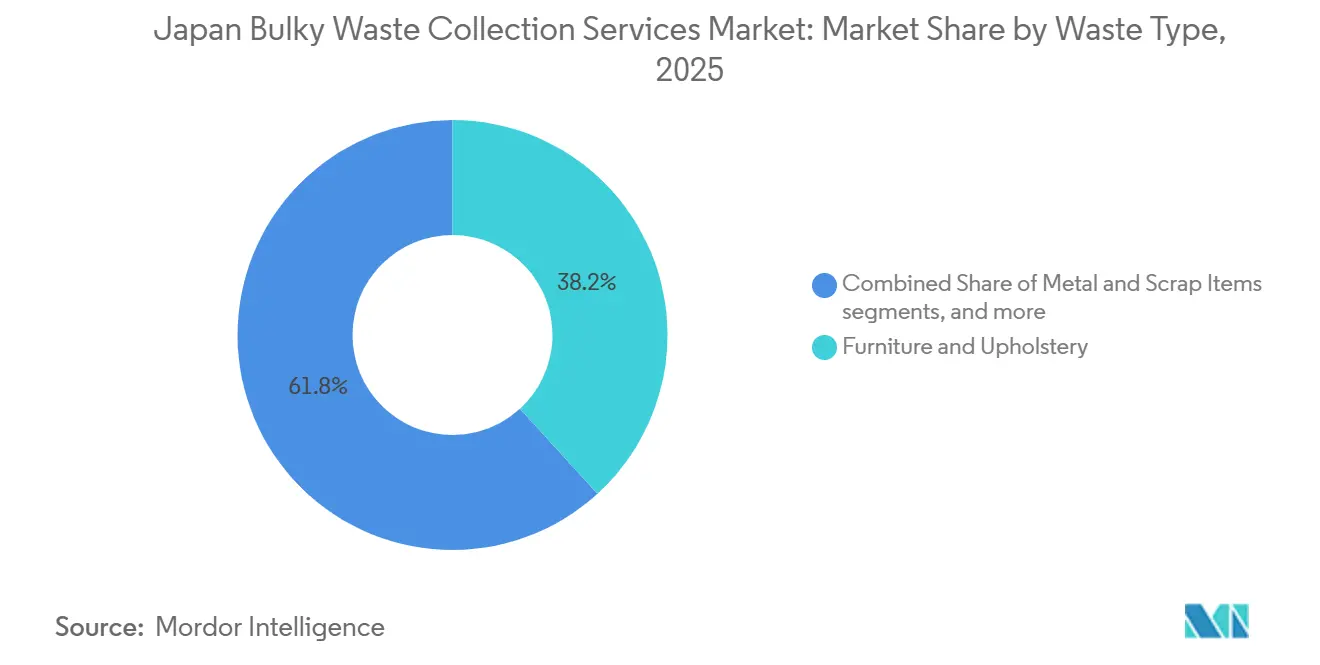

- By waste type, Furniture & Upholstery led with a 38.21% share in 2025 and is expected to expand at a 7.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Bulky Waste Collection Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Landfill Capacity and Land Scarcity | +1.2% | National, acute in Tokyo-Osaka metropolitan corridor | Medium term (2-4 years) |

| Government Policies Promoting 3R Society and Circular Economy | +1.5% | National, with early gains in industrial hubs (Kyushu semiconductor belt, Kanto urban prefectures) | Long term (≥ 4 years) |

| Extended Producer Responsibility (EPR) Laws | +0.9% | National, with compliance pressure highest in municipalities serving electronics manufacturing zones | Medium term (2-4 years) |

| Aging Population Creating Service Demand | +1.1% | National, concentrated in rural prefectures (Akita, Yamaguchi) and suburban Tokyo wards | Long term (≥ 4 years) |

| High Urbanization and Dense Living Conditions | +0.7% | 23 wards in Tokyo, Osaka City, Nagoya metropolitan area | Short term (≤ 2 years) |

| Strict Waste Disposal Regulations and Mandatory Fees | +0.6% | National, with many municipalities enforcing paid bulky waste collection | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Landfill Capacity and Land Scarcity

In Japan, the scarcity of landfills shapes the pricing and service design of bulky waste collection services. National circular economy targets include reducing final disposal volumes toward 2030 in line with the Fifth Basic Plan’s direction, heightening the need to divert bulky items away from final disposal and into recycling streams where feasible[1]Keidanren, “Voluntary Action Plan for Establishing a Sound Material-Cycle Society: Overview,” Keidanren, keidanren.or.jp. Tokyo’s network of high-efficiency incineration plants still produces ash that competes for limited landfill space, which puts pressure on pre-treatment and material recovery to reduce what reaches controlled sites. Bulky waste presents a particular challenge due to its metal content, hazardous components, and dimensions that do not fit standard collection and combustion workflows, which is why Japan relies on a national network of 583 dedicated bulky waste crushing facilities with a daily capacity of 20,401 tons. Providers that capture resale or recycling value upstream ease disposal constraints while strengthening unit economics, making it a competitive differentiator as landfill gate fees and transport burdens rise. Over the medium term, continued policy alignment on resource circulation is likely to favor integrated operators that combine collection, pre-processing, and router-compliant recyclers.

Government Policies Promoting a 3R Society and Circular Economy

Japan has elevated the circular economy to a national strategy, with explicit 2030 targets for input and output recycling rates and a JPY 80 trillion (USD 0.51 trillion) circular market objective, which will shape local government plans and procurement for collection and sorting capacity in the Japan bulky waste collection services market. The Circular Economy Transition Acceleration Package directs closer collaboration between manufacturing and recycling, supports end-of-life solar panel recycling, and expands the supply of recycled materials, driving upstream demand for traceable, segmented collections that can feed compliant processing lines. For service providers, this creates opportunities to offer reverse logistics and pre-sorting at pickup, which helps municipalities meet resource productivity objectives and helps producers comply with lifecycle responsibilities. Industry groups have reported sizable reductions in final disposal of industrial waste since 2000, suggesting that further gains require capturing difficult streams and optimizing cross-prefectural logistics where certification allows wider-area processing. As these policies mature, private operators that can document recovery performance and carbon intensity are positioned to win public contracts and corporate accounts under evolving OECD disclosure rules.

Extended Producer Responsibility (EPR) Laws

Japan’s policy direction is to expand Extended Producer Responsibility, which is relevant for batteries and small electronics. It sets a template for future categories that could include furniture and other large items over time in the Japan bulky waste collection services market. The practical implication for collection providers is growing demand for product-specific reverse logistics and data traceability from pickup through certified processors, which favors operators with integrated networks. Strategic moves in Japan illustrate this shift, including Veolia’s acquisition of Zeeklite, which strengthened vertical integration by adding one of the country’s largest privately controlled landfills with hazardous waste handling to Veolia Japan's existing collection and treatment capabilities. Policy instruments that require design-for-recycling and lifecycle accountability also encourage manufacturers to partner with service providers that can deliver consistent flows to recyclers and document compliance-ready metrics. Over the forecast period, EPR expansion is likely to reward scalable networks that can handle both residential and commercial returns while meeting safety and environmental standards at each stage.

Aging Population Creating Service Demand

Japan’s aging population reshapes service patterns by concentrating bulky waste into episodic events tied to home downsizing, relocations, and estate clearance, rather than steady weekly volumes, which sustains demand for flexible pickup in the Japan bulky waste collection services market. Municipalities face rising requests for personalized scheduling and assisted handling, which strengthens the case for on-demand models that can align vehicle deployment with irregular generation. National initiatives such as Decarbonization Leading Areas and Circulating and Ecological Economy programs incorporate demographic realities and labor constraints into planning, which supports the case for technologies and service bundles that improve route density and productivity. Providers that can tailor residential pickups, offer pre-sorting at the curb, and coordinate with downstream recyclers gain efficiency and a better customer experience. These capabilities are also relevant for rural prefectures with higher aging ratios, where fewer households incur higher per-pickup costs, which can be managed through route planning and integration with social support partners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Waste Management and Treatment | -0.8% | National, with urban municipalities bearing elevated facility construction expenses | Medium term (2-4 years) |

| Severe Labor Shortages in Waste Collection | -1.1% | National, most acute in rural prefectures with declining working-age populations | Long term (≥ 4 years) |

| Language Barriers for Foreign Residents | -0.2% | 23 wards in Tokyo, Osaka City, Kyoto metropolitan area | Short term (≤ 2 years) |

| Complex and Varying Municipal Regulations | -0.4% | National, with many waste categories in select municipalities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Waste Management and Treatment

Operating costs remain a major constraint as collection, transport, intermediate processing, and disposal budgets strain municipal finances in the Japan bulky waste collection services market. National figures show significant annual spending on general waste operations, with urban cores incurring much higher per capita costs due to advanced facility construction and land-related expenses. Industrial waste disposal prices rose 10-20% in 2024 amid persistent fuel, labor, and facility renewal pressures, with further increases projected into 2025, which indirectly affect bulky waste operators through shared fleets and processing hubs. City-level data confirms fee and cost escalation, as seen in Itami City’s trend of higher bulky waste revenues and per-ton processing costs across recent fiscal years. Operators can mitigate pressure by using technology that reduces collection frequency and increases bin capacity utilization, as demonstrated by smart compression bins that lower pickups and support route optimization. Over time, integrated models that co-locate pre-sorting with treatment and capture higher-value materials can offset cost inflation by improving asset utilization and increasing materials revenue.

Severe Labor Shortages in Waste Collection

Labor scarcity has become structural in Japan, constraining growth capacity while raising operating costs in the Japan bulky waste collection services market. Wage inflation is evident in disposal price increases reported by industry operators, with driver and on-site staff shortages a central cause of higher unit costs. Large integrated groups have acknowledged workforce headwinds, even with extensive domestic facility footprints, which are pushing the sector to redesign operations around automation, remote monitoring, and route management. Smart bins that compress contents and transmit fill-level updates cut unnecessary pickups and lighten route loads by reducing the number of trips needed in busy wards. Municipal data also shows extensive use of entrusted private operators and permitted contractors for bulky waste treatment and cross-prefectural transfers, which reflects greater outsourcing to specialized private providers amid municipal workforce gaps. These responses will remain vital as demographic trends continue to reduce the working-age population, while residential bulky waste requests remain episodic and labor-intensive in OECD countries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Collection Model: On-Demand Leads as Demographics Drive Request-Based Services

On-demand collection commanded 43.21% of the Japan bulky waste collection services market share in 2025 and is projected to grow at a 6.21% CAGR through 2031, reflecting alignment with aging household needs and episodic generation patterns. This model’s advantage is its ability to match vehicle dispatch with actual pickup requests, reducing idle time and improving customer satisfaction when downsizing or estate clearance is required [2]Japan Environment Sanitation Center, “Status and Future Initiatives of Waste Management in Local Governments,” JESC, jesc.or.jp. The on-demand format also supports curbside pre-sorting and item-level handling, making downstream recycling more efficient and benefiting municipalities working toward circular-economy targets. The Japan bulky waste collection services market favors providers that route on-demand pickups into facilities designed for crushing and segregation, a capability available across a nationwide base of specialized facilities. These combined advantages underscore why on-demand is growing faster than scheduled curbside services, where route density has declined with falling household counts in some municipalities.

Curbside models still serve suburban contexts where weekly patterns remain predictable, yet they face margin pressure as demographics reduce household concentrations per route. Hybrid approaches that pair scheduled pickups with on-call flexibility can bridge the needs of suburban and rural areas, where demand fluctuates during the forecast period. Contracted B2B collection provides steadier volumes with longer asset replacement cycles for offices and retail, and it benefits from corporate reporting needs around waste recovery and emissions, which shifts vendor selection toward integrated providers that can document outcomes. The Japan bulky waste collection services market size for on-demand services is likely to expand faster than curbside services as reverse logistics requirements deepen, routing platforms improve productivity, and municipal contracts emphasize circular outcomes. Over time, operator differentiation will depend on digital booking, item-level classification, and partnerships with recyclers to capture materials value and reduce landfill exposure.

By Source: Residential Segment Dominates Amid Aging Demographics and Urban Downsizing

Residential sources accounted for 58.78% market share in 2025, leading the segment mix and setting the baseline for service design across the Japan bulky waste collection services market. Residential growth is forecast at 6.72% CAGR through 2031, reflecting the concentration of bulky waste during life events such as home moves, downsizing, and estate resolution as the population ages. Operators that can ensure safe handling of large items and provide scheduling windows tailored to individual residents are better positioned to meet municipal service-quality expectations. Urban density further elevates the need for time-window precision and building access coordination, which links routing software to labor planning and vehicle types configured for tight streets and elevators. The Japan bulky waste collection services industry also benefits from municipal frameworks that license entrusted private operators and allow cross-regional processing where certified, which can ease bottlenecks for high-demand wards.

Commercial sources contribute steady volumes tied to office furniture cycles, retail fixture updates, and institutional replacements. Growth is slower than residential due to longer asset lives and deferred capital spending in some sectors. Still, it offers contract stability and opportunities for value-added services that document recovery rates and carbon metrics for corporate reporting. Municipal and government sources present lower volatility with long-term contracts and predictable budgets, which can stabilize route planning and asset utilization. Industrial generators often fall outside municipal bulky waste rules and rely on permitted handlers, which channel opportunities toward integrated players that can take large items to specialized processing or controlled disposal, where needed. Residential will remain the anchor for the Japan bulky waste collection services market due to demographic composition and municipal service mandates. In contrast, commercial and municipal sources provide portfolio balance and consistent utilization of processing infrastructure.

By Waste Type: Furniture and Upholstery Lead Growth Amid Lifecycle Replacement Cycles

Furniture and upholstery captured 38.21% of Japan's bulky waste collection services market share in 2025 and is expected to grow at a 7.12% CAGR through 2031, driven by tenant turnover norms and residential downsizing cycles. Policy emphasis on resource circulation and design-for-recycling increases pressure to divert recoverable materials, which supports pre-sorting and targeted partnerships with refurbishers or recyclers for wood, textiles, and metals. Integrated players that route furniture streams to crushing and segregation facilities can extract greater value and reduce final-disposal exposure. Metals and scrap remain important for materials revenue. However, margins can vary with global commodity cycles, which reinforces the case for multi-stream collection strategies and price risk management by larger integrated operators.

White goods and appliances follow established take-back and recycling channels that shift some costs to producers and dedicated recyclers, reducing municipal burdens while increasing the need for compliant collection and transport to designated facilities. Construction-related bulky items generally fall under industrial waste rules. They are handled by permitted operators or demolition partners, as seen in alliances designed to improve demolition waste recycling and disaster waste cooperation. Emerging streams, such as end-of-life solar panels, are driving new assets and demonstration projects to prepare for larger volumes later in the decade, with operators building one-stop services from removal to reuse and recycling. The Japan bulky waste collection services market size for furniture and upholstery is set to benefit from integrated networks that can document recovery performance and deliver consistent flows to specialty recyclers.

Geography Analysis

Urban concentration in the Tokyo-Osaka-Nagoya corridor drives a large share of service demand in the Japan bulky waste collection services market, with residential sources prominent and dense living conditions reinforcing the need for efficient scheduling and access control. Kanto prefectures such as Tokyo, Kanagawa, Chiba, and Saitama highlight the role of integrated operators that align collection with treatment and controlled disposal, including through acquisitions that expand capacity and hazardous-handling capabilities. Advanced processing infrastructure in metropolitan areas raises per capita costs yet supports higher diversion when paired with pre-sorting at pickup and targeted reuse partnerships. Technology pilots in urban wards that compress bin contents and enable fill-level routing further cut route frequency and help manage labor shortages. Public policy and intergovernmental reviews reinforce the emphasis on circular practices and decarbonization in cities, which raises the bar for service quality and traceability.

Kansai urban centers, including Osaka City, share the cost profile of high land and advanced facility investment while relying on efficient collection to manage labor gaps. Smart bin deployments have helped reduce unnecessary pickups in busy commercial areas and tourist corridors, improving loading rates and allowing crews to focus on high-yield routes. In parallel, investments in new environmental and recycling hubs in nearby prefectures support wider-area resource circulation and readiness for future streams, such as solar panels and complex ash recycling. These moves align with national objectives and reflect how private capital complements municipal plans to strengthen treatment capacity and improve materials recovery. The Japan bulky waste collection services market benefits from the Ministry of the Environment’s facility network standards and approvals, which ensure technical compliance while enabling cross-regional operations under specific certifications.[3]Ministry of the Environment, Japan, “Japan’s Waste Processing Data (FY2022): Disposal and Facility Overview,” Ministry of the Environment, env.go.jp

In Kyushu and Tohoku, industrial clusters and wide-area consolidation shape localized demand and capacity development. Kyushu’s semiconductor ecosystem has attracted investments in precious-metal recycling and integrated processing that can absorb specialized streams and support circular initiatives tied to manufacturing growth. In Tohoku, acquisitions have extended recycling networks northward to support customers with facilities across multiple regions, enhancing route density and enabling standardized service delivery over larger footprints. Hokkaido and rural prefectures face dispersed populations and winter constraints, which elevate per-pickup costs and reinforce the need to outsource to trusted private operators capable of running efficient inter-municipal logistics. The Japan bulky waste collection services market will continue to reflect these geographic contrasts, with metropolitan areas leading advanced deployments and rural regions relying on wider-area processing agreements under Japan’s Waste Management and Public Cleaning Act framework.

Competitive Landscape

Japan’s bulky waste collection services market remains fragmented, with municipalities owning treatment assets while outsourcing significant portions of collection and transport to private providers. Competitive differentiation rests on route optimization, digital booking, compliant handling, and the ability to deliver traceable recovery outcomes for both public and corporate clients. Global consolidators have moved to deepen integration across the value chain, illustrated by acquisitions that add controlled final disposal and hazardous capabilities to existing collection and treatment portfolios. These strategies reflect policy signals that reward integrated solutions aligned with circular-economy goals and lifecycle accountability.

Domestic leaders are investing in new hubs and digital tools that improve processing readiness for emerging streams and strengthen reporting capabilities. Operators have acquired land for multi-functional environmental and recycling complexes to enable solar panel recycling and related materials processing, and they have begun demonstration projects for reused PV panel power generation that build one-stop removal-to-reuse services. Companies are also rolling out data services that calculate carbon footprints at the process level and align with ISO 14067 and GHG Protocol standards, helping customers meet evolving disclosure rules. These offerings reinforce competitive advantage with corporate accounts and municipalities that are tracking emissions and recovery rates.

At the operational edge, technology is easing labor constraints and improving route economics. Smart compression bins reduce collection frequency while maintaining cleanliness in high-traffic zones, and the resulting route simplification increases average loading rates and reduces fuel use. Partnerships between recyclers and demolition specialists aim to streamline construction and waste flows, highlighting the importance of cross-stream synergies and ready surge capacity for disaster response. Cross-regional acquisitions extend network coverage and help standardize services across dispersed sites, reducing coordination costs for customers that operate in multiple prefectures. Taken together, these moves support a competitive environment in which integrated services, traceable outcomes, and labor-saving technologies are the main differentiators in the Japan bulky waste collection services market.

Japan Bulky Waste Collection Services Industry Leaders

Daiei Kankyo Holdings Co., Ltd.

ORIX Environmental Resources Management Corporation (OERM)

J&T Recycling Corporation

DOWA ECO-SYSTEM Co., Ltd.

Re-Tem Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: DOWA ECO-SYSTEM launched an industry-first carbon footprint calculation system for waste treatment processes, validated by Intertek Certification Japan to ISO 14067:2018 and GHG Protocol Product Standard, enabling customers to access reliable primary data on Scope 3 (Category 5/Waste Treatment) emissions starting June 2026, responding to mandatory climate disclosure requirements for Tokyo Stock Exchange Prime Market companies from fiscal year ending March 2027.

- May 2025: Veolia acquired 100% of Zeeklite Co., Ltd., which operates one of Japan’s largest privately controlled final disposal sites in Yonezawa City, Yamagata Prefecture, handling industrial waste, general waste, and contaminated soil, establishing an integrated system covering collection, transportation, intermediate processing, and final disposal for hazardous waste.

- March 2025: J&T Recycling Corporation, a JFE Engineering group company, formed a business alliance with BESTERRA CO., LTD., a major demolition specialist, to advance the recycling of demolition waste, establish efficient processing schemes for demolition waste, and build cooperation systems for disaster waste management.

Japan Bulky Waste Collection Services Market Report Scope

| Curbside |

| On-Demand |

| Hybrid |

| Contracted B2B |

| Others |

| Residential |

| Commercial |

| Industrial |

| Municipal/Government |

| Others (Religious Institutions, Temporary Disaster Relief Camps, Film/TV Production Sets) |

| Furniture & Upholstery |

| Metal & Scrap Items |

| White Goods/Appliances |

| Construction & Demolition |

| Others (Event-specific Waste, Biomedical/Institutional) |

| By Collection Model | Curbside |

| On-Demand | |

| Hybrid | |

| Contracted B2B | |

| Others | |

| By Source | Residential |

| Commercial | |

| Industrial | |

| Municipal/Government | |

| Others (Religious Institutions, Temporary Disaster Relief Camps, Film/TV Production Sets) | |

| By Waste Type | Furniture & Upholstery |

| Metal & Scrap Items | |

| White Goods/Appliances | |

| Construction & Demolition | |

| Others (Event-specific Waste, Biomedical/Institutional) |

Key Questions Answered in the Report

What is the current size and projected growth of the Japan bulky waste collection services market?

The Japan bulky waste collection services market size is expected to increase from USD 1.11 billion in 2025 to USD 1.17 billion in 2026 and reach USD 1.56 billion by 2031 at a 5.9% CAGR over 2026-2031

Which collection model leads and which is growing fastest in Japan?

On-demand collection led with 43.21% share in 2025 and is forecast to grow at 6.21% CAGR through 2031, reflecting alignment with episodic residential needs.

How do Japan’s circular economy policies influence service providers?

National 2030 circular targets and industry initiatives are driving demand for traceable, pre-sorted pickups and integrated logistics that feed certified recyclers, favoring operators that deliver recovery outcomes and compliant reporting.

What is the largest source category, and why does it matter for operators?

Residential accounted for 58.78% of revenue in 2025, driven by aging demographics and downsizing, which increased demand for flexible scheduling, assisted handling, and curbside pre-sorting.

Which waste type is growing the fastest in Japan's bulky waste collections?

Furniture and upholstery held 38.21% share in 2025 and is projected to grow at 7.12% CAGR through 2031, supported by tenant turnover, downsizing, and rising recovery expectations.

What cost and labor constraints are shaping operator strategies?

Disposal price inflation and labor shortages are pushing operators to adopt smart bins, improve route optimization, and integrate processing to capture materials value and stabilize unit economics.

Page last updated on: