Japan Automotive Reed Sensors/Switches Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

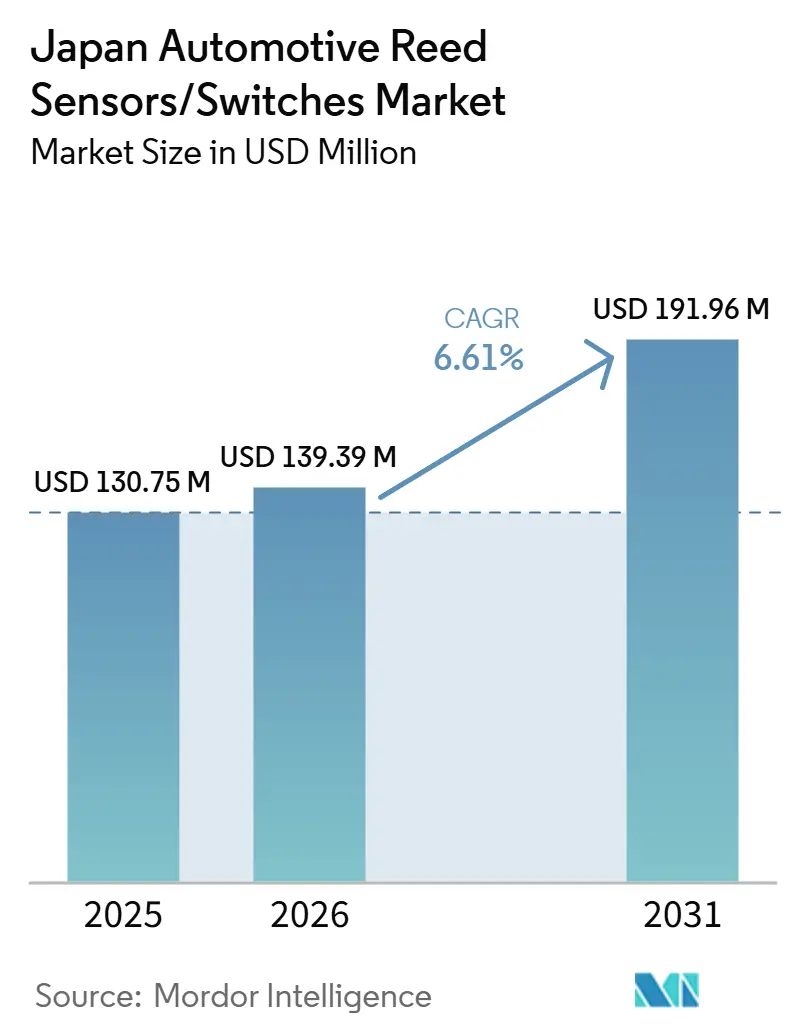

| Base Year Market Size (2025) | USD 130.75 Million |

| Market Size (2026) | USD 139.39 Million |

| Market Size (2031) | USD 191.96 Million |

| Growth Rate (2026 - 2031) | 6.61% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Japan Automotive Reed Sensors/Switches Market Analysis by Mordor Intelligence

The Japan Automotive Reed Sensors/Switches Market size is USD 130.75 million in 2025, USD 139.39 million in 2026, and is projected to reach USD 191.96 million by 2031, growing at a CAGR of 6.61% from 2026 to 2031. Japan’s fleet scale and replacement cycles remain important demand anchors for reed-based sensing. Reed switches continue to be used extensively in door, hood, and trunk closure detection, seat and belt status monitoring, parking and position sensing modules, and fluid-level assemblies. These applications benefit from attributes such as zero standby power, galvanic isolation, and reliable switching performance. Long vehicle service life supports both OEM fitment and a persistent aftermarket replacement stream, sustaining baseline demand across vehicle lifecycles.

Electrification in Japan is primarily hybrid-led, which is structurally supportive of reed sensor and switch content. Hybrid vehicles typically maintain high electronics density across body control, safety, and comfort systems, while adding electrified subsystems that introduce incremental sensing points. While battery electric vehicle volumes remain comparatively limited, continued policy support and the development of the charging ecosystem support the gradual expansion of battery- and charging-related sensing applications. These dynamics position battery and charging systems as the fastest-growing application segment over the forecast period, even as hybrids remain the dominant electrified propulsion type[1]"Reed Switches / MK33 Series (automotive-grade reed components)," Standex Electronics, standexelectronics.com..

Key Report Takeaways

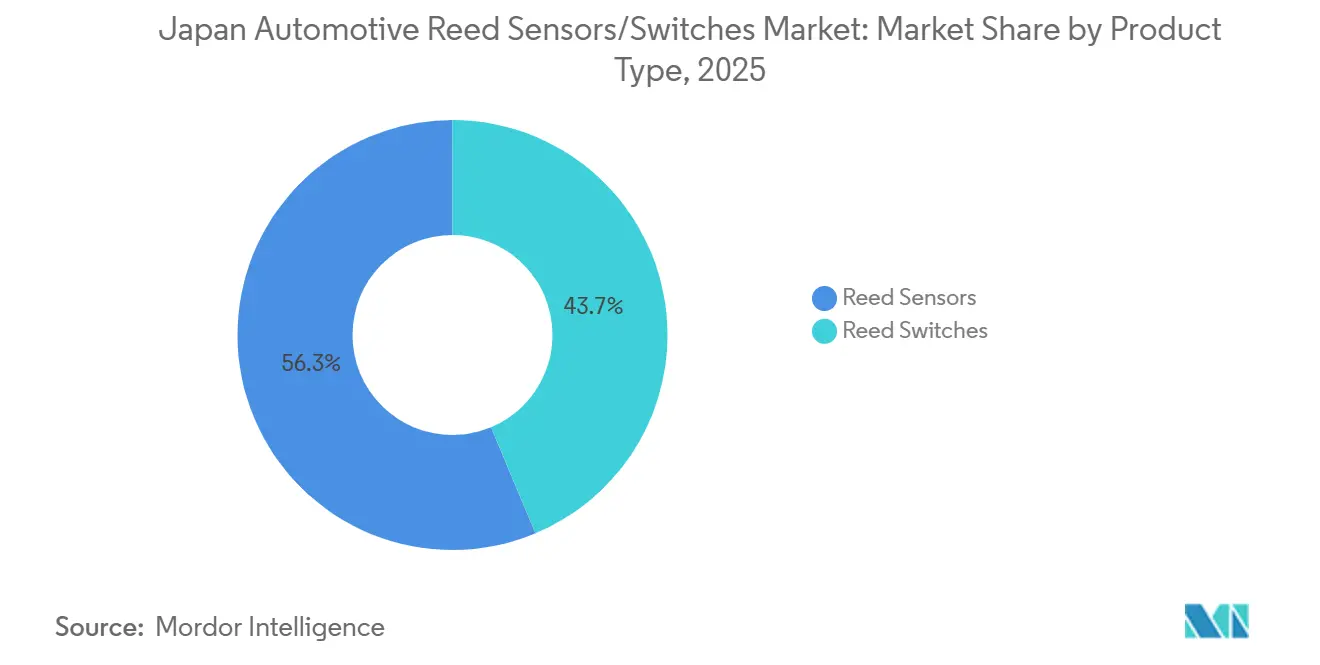

- By product type, reed switches accounted for 56.29% of the market in 2025, while reed sensors are projected to be the fastest-growing product type, registering a CAGR of 7.78% during 2026–2031.

- By application, body electronics represented 28.14% share in 2025, while battery and charging systems are projected to grow fastest over the forecast period, registering a CAGR of 10.58%.

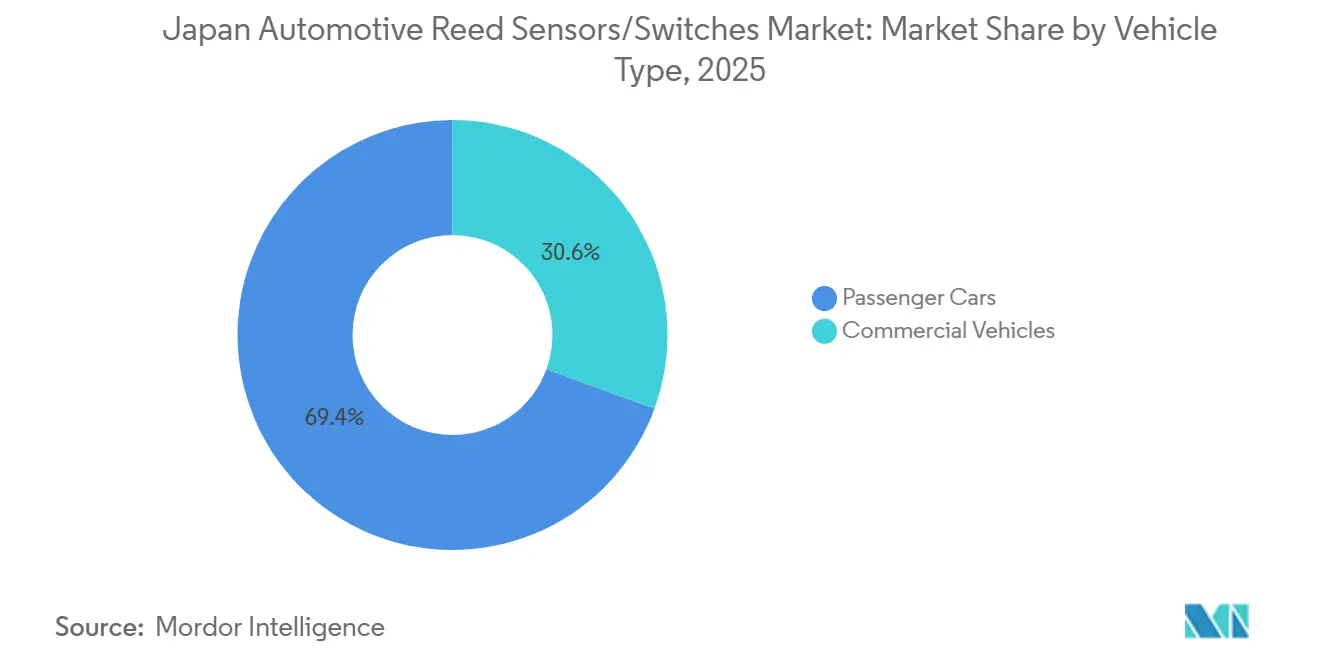

- By vehicle type, passenger cars accounted for 69.44% of the market in 2025 and are projected to grow at a CAGR of 7.08% during 2026–2031.

- By sales channel, OEMs dominated with an 86.35% share in 2025 and are projected to grow at a CAGR of 6.88% over the forecast period.

- By propulsion type, hybrid vehicles accounted for 43.16% of the market in 2025, while battery electric vehicles are projected to be the fastest-growing propulsion type, registering a CAGR of 11.58% during 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Automotive Reed Sensors/Switches Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid-Led Electrification Scale | +1.2% | National | Medium term (2-4 years) |

| Charging Ecosystem Upgrades | +1.0% | Urban + Intercity Corridors | Medium term (2-4 years) |

| OEM Design-In Dominance | +0.9% | National | Short term (≤ 2 years) |

| Passenger Car Electronics Content | +0.8% | National | Medium term (2-4 years) |

| Large Parc Replacement Demand | +0.7% | National | Medium term (2-4 years) |

| SMD Miniaturization Adoption | +0.4% | OEM/Tier Programs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hybrid-Led Electrification Keeps Electronics Content High

Japan’s electrification pathway remains strongly hybrid-centric, with hybrids accounting for a significant share of new passenger vehicle sales. Hybrid platforms typically retain high electronics content across body control, safety, and comfort systems, while also adding electrified subsystems. This combination sustains demand for reed sensors and switches in compact modules where binary state detection, low standby power, and stable performance are required.

Reed-based solutions continue to be specified in closures, position and status sensing, and sealed assemblies across hybrid and advanced internal combustion engine platforms. These use cases align with OEM preferences in Japan for proven reliability under vibration, temperature cycling, and environmental exposure, supporting continued reed adoption even as powertrains evolve[2]"Japan could lose $17 billion in car exports due to US tariffs…," Reuters, reuters.com..

Battery and Charging Subsystem Growth Is Structurally Supported by Ecosystem Upgrades

Battery and charging systems represent the fastest-growing application segment in the Japanese market. Growth is driven by ongoing upgrades to the charging ecosystem, including higher-power charging capabilities and expanded fast-charging deployments. As charging infrastructure evolves, both vehicle-side and charging-side systems require additional sensing points for access detection, interlocks, and safety-state monitoring.

These developments increase demand for sensing solutions used in charging interfaces, pack-related enclosures, and high-voltage safety architectures. As a result, battery and charging-related applications account for a growing share of incremental demand for reed sensors and switches over the forecast period.

Government Incentives Improve Electrified Vehicle Economics and Expand Sensing Points

Government support programs aimed at improving the affordability of electrified vehicles continue to influence adoption trends in Japan. Incentives for electric and plug-in hybrid vehicles support the gradual expansion of electrified platforms within the national vehicle mix. As electrified vehicle volumes increase, the number of battery, charging, and high-voltage interlock sensing points per vehicle also rises.

This dynamic indirectly supports demand for reed sensors and switches specified within electrified subsystems. While adoption remains hybrid-led, continued policy support improves demand visibility for EV- and PHV-associated sensing applications.

Large In-Use Vehicle Parc and Long Service Life Support Aftermarket Stability

Japan's large in-use vehicle parc and long average vehicle service life support a resilient aftermarket demand base. Vehicles remain in operation for extended periods, increasing the likelihood of replacement and servicing of body-electronics components, including closures, position- and status-sensing modules, and fluid-level assemblies.

This installed-base effect provides stability to market demand even when new vehicle sales fluctuate. As a result, aftermarket replacement remains an important contributor to overall consumption of reed sensors and switches alongside OEM fitment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Solid-State Sensor Substitution | -1.1% | National | Medium term (2-4 years) |

| Slower BEV Penetration | -0.8% | National | Medium term (2-4 years) |

| OEM Qualification Cycle Delays | -0.6% | OEM/Tier Programs | Short term (≤ 2 years) |

| Cost-Down Roadmap Pressure | -0.4% | Tier Supply Chain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Solid-State Magnetic Sensing Technologies

Solid-state magnetic sensing technologies, including Hall-effect and tunneling magnetoresistance solutions, continue to compete with reed-based sensing in several automotive applications. These technologies are increasingly adopted for use cases that prioritize continuous measurement, tighter ECU integration, or programmable outputs.

As OEMs consolidate electronics architectures and standardize sensor platforms, reed sensors and switches face substitution pressure in selected modules. This competitive dynamic can cap reed penetration in applications where semiconductor-based sensing offers perceived system-level advantages.

Slower Battery Electric Vehicle Penetration Limits EV-Only Demand Acceleration

Battery electric vehicle adoption in Japan is improving, but remains slower compared to leading global EV markets. OEM strategies continue to emphasize hybrids alongside selective BEV expansion, which can temper near-term growth in EV-only sensing demand.

This dynamic limits the ceiling for rapid expansion of sensing points tied exclusively to BEV architectures. While long-term electrification trends remain positive, the pace of BEV penetration can moderate the acceleration of battery and charging-related sensing demand in the short to medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reed Switches Retain Scale; Reed Sensors Gain Faster Traction

Reed switches remained the largest product type in Japan in 2025, with a market share of 56.29%. Their scale reflects cost-effective deployment across a wide range of discrete switching and state-detection functions, particularly in body electronics and safety-related applications. Reed switches continue to be specified for simple on/off detection, sealed magnetic actuation, and long-life reliability across high-volume vehicle platforms.

Reed sensors are expanding at a 7.78% rate as OEMs and Tier-1 suppliers increasingly adopt packaged, engineered sensing devices suited to dense ECUs and space-constrained modules. Growth is supported by continued innovation in surface-mount reed designs that improve manufacturability and placement stability. Developments such as low-profile SMD reed formats aligned with automated pick-and-place assembly support broader adoption of sensorized reed solutions, moving beyond bare switches toward integration-ready components.

By Application: Body Electronics Dominate; Battery and Charging Systems Accelerate

Body electronics represented the largest application segment in 2025, with a market share of 28.14%. This segment covers a wide range of high-volume sensing points per vehicle, including closures, latches, seat modules, and position or status detection across comfort and convenience systems. These applications are pervasive across passenger vehicles and sustain both OEM fitment and replacement-driven demand.

Battery and charging systems are projected to grow at the fastest rate, registering a CAGR of 10.58% during the forecast period. Growth is consistent with continued enablement of electrification in Japan, including upgrades to the charging ecosystem and vehicle incentive frameworks. As electrified subsystems expand, additional sensing points are introduced around charging interfaces, enclosures, and safety-state monitoring, supporting faster growth relative to traditional body electronics.

By Vehicle Type: Passenger Cars Drive Both Scale and Growth

Passenger cars accounted for the largest vehicle type segment in 2025, with a market share of 69.44%, and are projected to grow at a CAGR of 7.08% through 2031. This reflects Japan’s market structure, where passenger vehicles dominate both the installed base and new registrations.

As passenger vehicle platforms continue to incorporate higher electronics content and a growing mix of electrified variants, reed-based sensing points remain broadly distributed across body electronics and electrified subsystems. This sustains passenger cars as the core contributor to overall market demand.

By Sales Channel: OEMs Lead Shipments; Aftermarket Supported by Long Service Life

OEMs represented the largest and fastest-growing sales channel in 2025, with a market share of 86.35% and a projected CAGR of 6.88%. This reflects design-in requirements, qualification-driven sourcing, and long platform lifecycles typical of Japan’s automotive programs.

The aftermarket remains a meaningful contributor to demand, supported by Japan’s large in-use vehicle parc and long average service life. Replacement demand persists across common sensing points such as door, hood, and trunk systems, supporting steady aftermarket consumption alongside OEM growth.

By Propulsion Type: Hybrids Lead Today; BEVs Post the Strongest Growth

Hybrid vehicles accounted for the largest propulsion segment in 2025, with a market share of 43.16%, reflecting Japan’s hybrid-heavy new-vehicle mix. Hybrid platforms sustain high electronics density across body control and safety systems while adding electrified subsystems that increase sensing requirements.

Battery electric vehicles are projected to be the fastest-growing propulsion segment, registering a 11.58% CAGR during the forecast period. Growth is supported by policy incentives and improvements in the charging ecosystem, even as BEV volumes expand from a smaller base than hybrids.

Geography Analysis

The Japanese automotive reed sensors and switches market is mature and technology-driven, experiencing stable growth, supported by the country's shift toward electric vehicles (EVs) and advanced hybrid powertrains. As a global hub for automotive engineering, Japanese manufacturers increasingly rely on reed technology due to its zero-power consumption in standby modes, high reliability under extreme temperatures, and effective hermetic sealing.

Market activity is concentrated within Japan's established industrial regions, particularly the Chubu region. Aichi Prefecture is the primary hub, hosting major global OEMs such as Toyota and a broad network of Tier-1 suppliers, which supports localized sensor integration and rapid prototyping. The Kanto and Kansai regions serve as secondary hubs, housing corporate headquarters, R&D laboratories, and semiconductor fabrication facilities of major electronic component manufacturers.

The competitive landscape in Japan is shaped by a balance between established domestic electronics companies and specialized global players expanding their regional presence. Companies such as Omron Corporation and Alps Alpine hold strong positions by integrating reed switches into multi-functional automotive modules, while global specialists like Standex Electronics compete through high-precision, miniaturized component offerings. The market has also seen cross-border consolidation, including Standex's acquisition of Sanyu Switch Co., which allowed the acquirer to gain localized engineering expertise.

Competitive Landscape

Japan’s automotive reed sensors and switches market is served by a mix of global reed-technology specialists and suppliers with established manufacturing and engineering footprints in Japan. Competitive positioning increasingly depends on automotive-grade qualification depth, reliability validation under harsh operating conditions, and the ability to support long platform lifecycles with stable supply.

Miniaturized SMD packaging and manufacturing friendliness are central competitive differentiators. Suppliers that offer tape-and-reel formats, stable coplanarity, and pick-and-place compatibility are better aligned with Japan’s electronics manufacturing practices. Cost-down roadmaps must be balanced against consistent performance under vibration, temperature cycling, and exposure to contamination.

Competitive pressure from solid-state magnetic sensing technologies persists in select applications, particularly where tighter ECU integration or alternative diagnostics are prioritized. Overall, suppliers with local engineering support, strong quality assurance processes, and proven automotive reference designs are better positioned to secure platform-level design-ins. Notably, Standex Electronics has strengthened its regional presence through acquisitions and the integration of Japan-based capabilities, expanding switching depth and customer access in the market.

Japan Automotive Reed Sensors/Switches Industry Leaders

-

Standex Electronics

-

Littelfuse

-

Coto Technology

-

Aleph

-

PIC GmbH (PIC Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Toyota and partners accelerated deployments of high-speed EV chargers with a stated rollout plan (including a fast-charger count target within the plan horizon).

- May 2024: Standex Electronics Japan announced the MK33 SMD reed switch series, reflecting continued innovation for compact, space-constrained electronics modules.

- February 2024: Standex announced the closing of its Sanyu Switch acquisition, strengthening relay/switching capabilities and Japan-based customer access.

Japan Automotive Reed Sensors/Switches Market Report Scope

Automotive reed sensors/switches are magnetically actuated switching/sensing devices used to detect position, proximity, or open/close states in vehicle systems. A reed switch uses sealed ferromagnetic contacts actuated by a magnetic field; reed sensors typically package the reed element (and sometimes magnets/housings) for specific automotive sensing applications.

The scope of the market includes segmentation by product type (reed switches and reed sensors), application (body electronics, battery and charging systems, and others), vehicle type (passenger cars and commercial vehicles), sales channel (OEMs and aftermarket), and propulsion type (internal combustion engine vehicles, battery electric vehicles, and others). Market sizing and forecasts are provided in terms of value, expressed in USD

| Reed Sensors |

| Reed Switches |

| Engine and Powertrain Systems |

| Body Electronics |

| Safety and Security Systems |

| Infotainment and Comfort Systems |

| Transmission and Braking Systems |

| Battery and Charging Systems |

| Other Applications |

| Passenger Cars |

| Commercial Vehicles |

| OEMs |

| Aftermarket |

| Internal Combustion Engine Vehicles |

| Hybrid Vehicles |

| Plug-in Hybrid Electric Vehicle |

| Battery Electric Vehicles |

| Fuel Cell Electric Vehicle |

| By Product Type (Value, USD) | Reed Sensors |

| Reed Switches | |

| By Application (Value, USD) | Engine and Powertrain Systems |

| Body Electronics | |

| Safety and Security Systems | |

| Infotainment and Comfort Systems | |

| Transmission and Braking Systems | |

| Battery and Charging Systems | |

| Other Applications | |

| By Vehicle Type (Value, USD) | Passenger Cars |

| Commercial Vehicles | |

| By Sales Channel (Value, USD) | OEMs |

| Aftermarket | |

| By Propulsion Type (Value, USD) | Internal Combustion Engine Vehicles |

| Hybrid Vehicles | |

| Plug-in Hybrid Electric Vehicle | |

| Battery Electric Vehicles | |

| Fuel Cell Electric Vehicle |

Key Questions Answered in the Report

What is the current value of the Japan automotive reed sensors/switches market?

It stands at USD 130.75 million in 2025 and is projected to reach USD 191.96 million by 2031 (6.61% CAGR).

Which product type leads the Japan market today?

Reed switches lead with 56.29% in 2025 due to extensive use in electronics-rich vehicle architectures.

Which application is growing the fastest and why?

Battery and charging systems are growing fastest (10.58% CAGR, 2026–2031) as EV/charging subsystems scale up.

Which propulsion type contributes most to today’s demand in Japan?

Hybrid vehicles lead with 43.16% in 2025, reflecting Japan’s hybrid-heavy market structure.

Which propulsion type will expand the quickest through 2031?

Battery electric vehicles grow fastest (11.58% CAGR, 2026–2031) as BEV adoption rises from a smaller base.

Page last updated on: