IV Flush Syringe Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

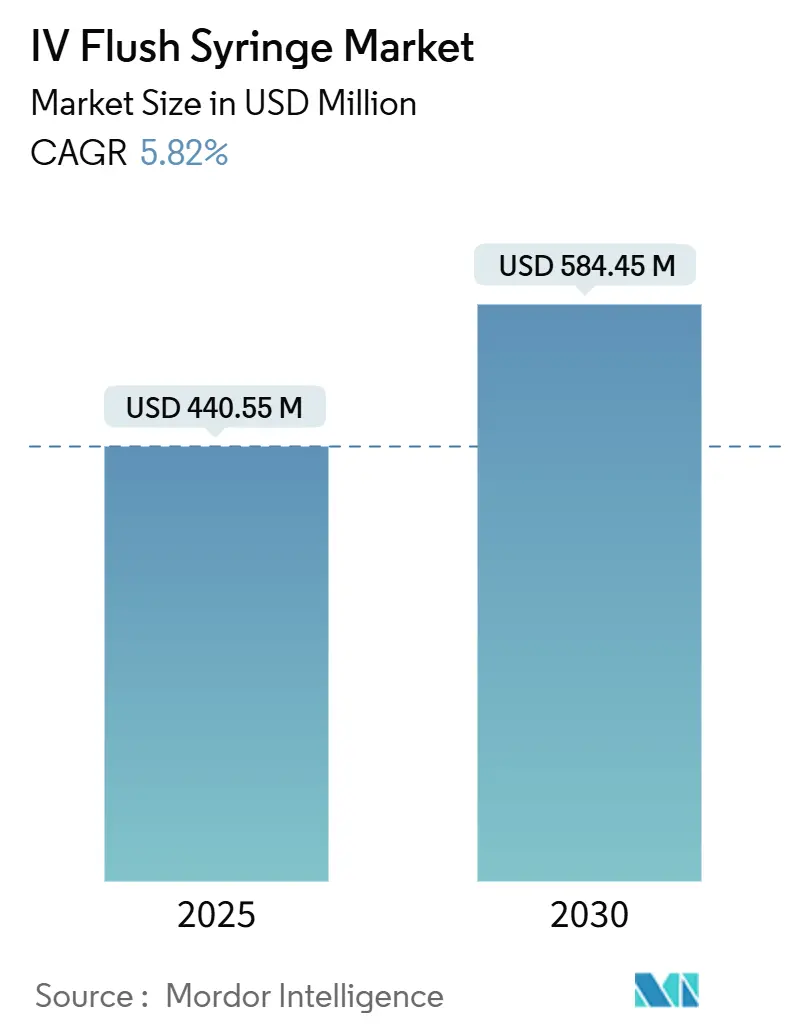

| Market Size (2025) | USD 440.55 Million |

| Market Size (2030) | USD 584.45 Million |

| Growth Rate (2025 - 2030) | 5.82% CAGR |

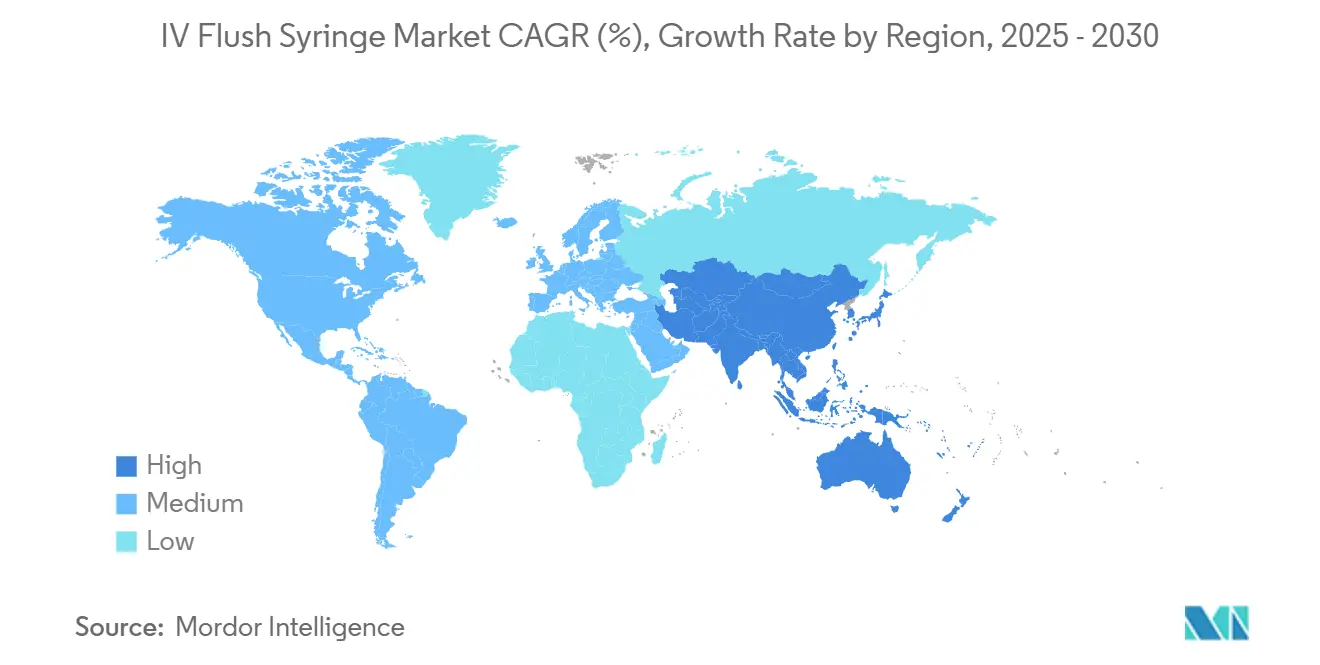

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

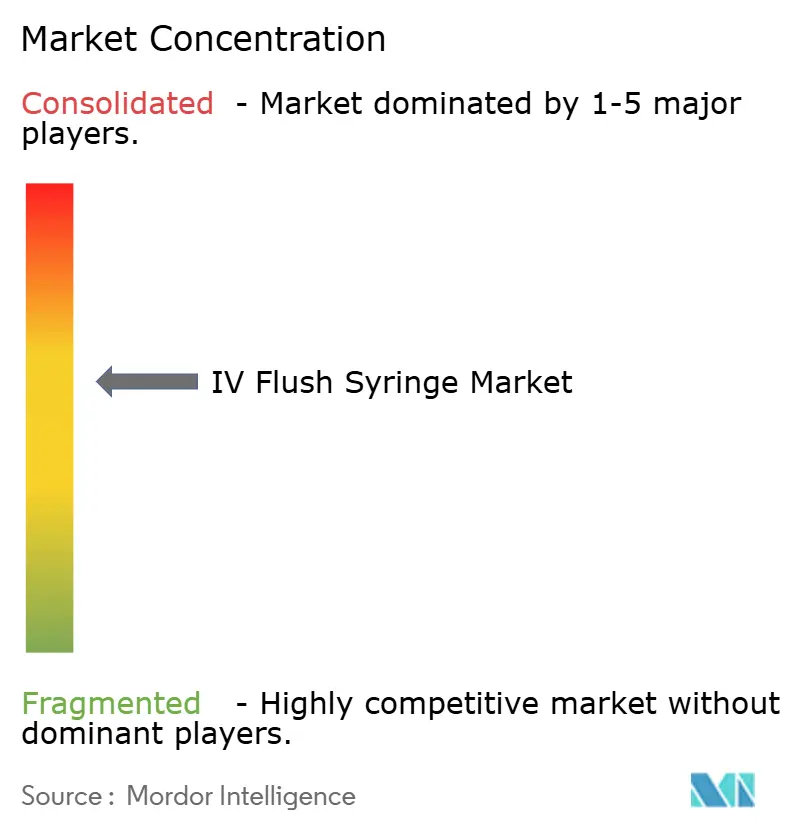

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

IV Flush Syringe Market Analysis by Mordor Intelligence

The IV flush syringe market stands at USD 440.55 million in 2025 and is forecast to reach USD 584.45 million in 2030, advancing at a 5.82% CAGR. Adoption continues to accelerate despite the 2024 supply-chain shock that exposed the risks of concentrated manufacturing. Healthcare providers responded by tightening inventory controls and favoring standardized pre-filled options, a shift that has already improved compliance with infection-control protocols. Demand is also supported by chronic-disease prevalence, wider home-infusion reimbursement, and broader regulatory convergence that smooths market entry for validated products. At the same time, manufacturers face intensified scrutiny after a series of Class I recalls, prompting large capital outlays for quality-system upgrades.

Key Report Takeaways

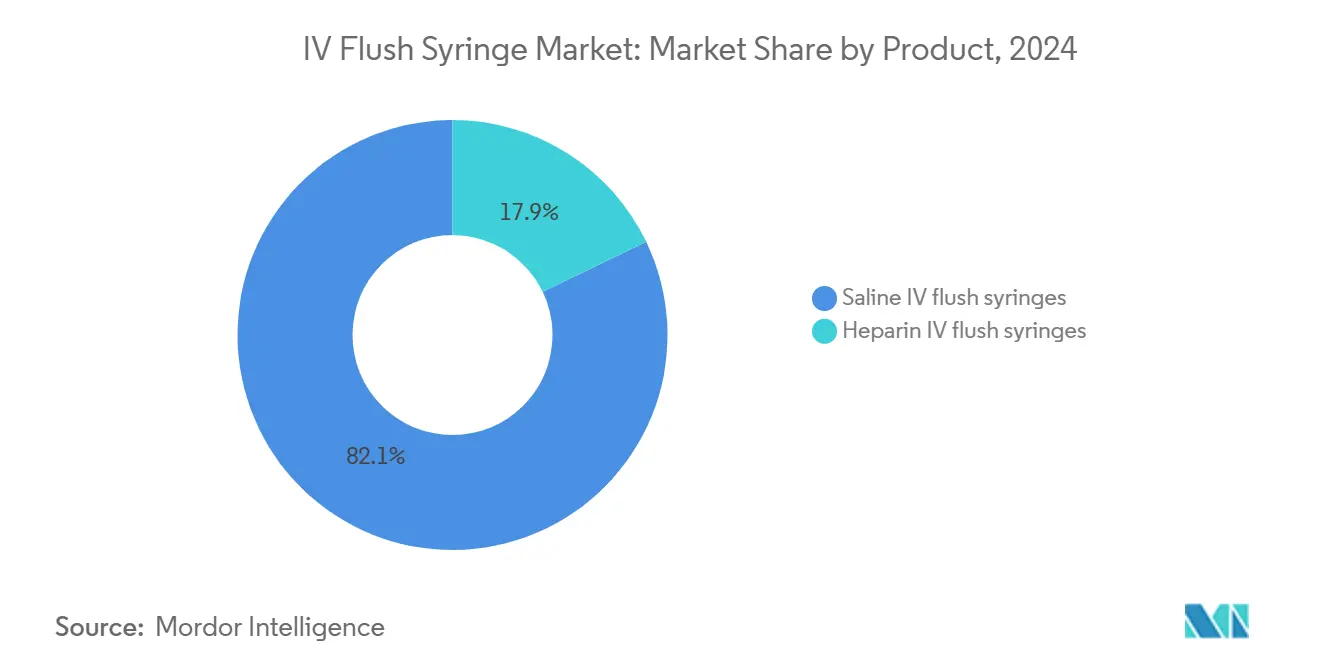

- By product, saline IV flush syringes led with 82.13% revenue share in 2024, while heparin IV flush syringes are advancing at a 6.43% CAGR to 2030.

- By volume, 10 mL units captured 62.34% of the IV flush syringe market share in 2024; 3 mL formats are projected to grow at 6.54% CAGR.

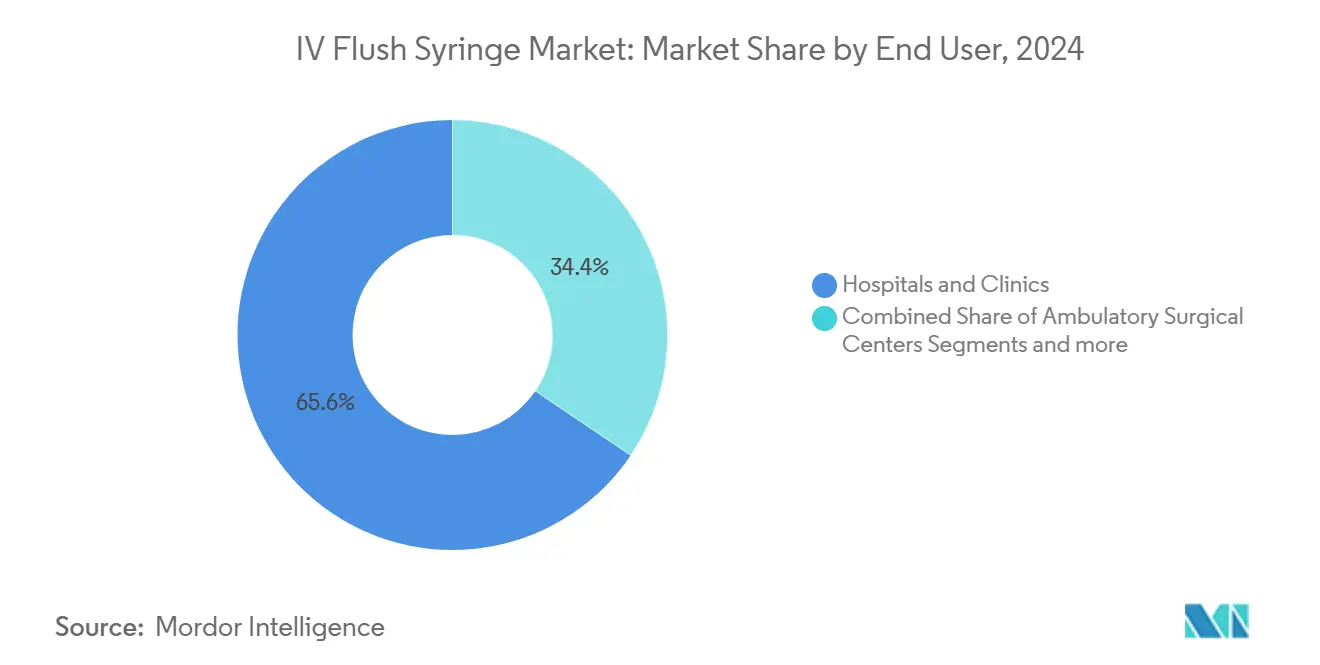

- By end-user, hospitals and clinics held 65.56% of the IV flush syringe market size in 2024; home-care settings record the highest projected CAGR at 6.58% through 2030.

- By patient age group, adults accounted for 61.19% of market revenue in 2024, while the geriatric segment is expected to expand at 6.49% CAGR.

- By geography, North America commanded 41.49% of revenue in 2024; Asia-Pacific is forecast to post the fastest regional CAGR at 6.69% to 2030.

Global IV Flush Syringe Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in awareness & global guidelines for single-use flush syringes | +1.2% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Rising incidence of chronic & infectious diseases driving IV therapy | +1.8% | Global, concentrated in aging populations | Long term (≥ 4 years) |

| Rapid switch to pre-filled flush formats to curb CLABSI and save nursing time | +1.5% | North America & EU core, expanding to APAC | Short term (≤ 2 years) |

| Expansion of home-infusion & outpatient care settings | +0.9% | North America lead, APAC emerging markets following | Medium term (2-4 years) |

| Growing focus on sterility and safety features | +0.7% | Global, with premium adoption in developed markets | Medium term (2-4 years) |

| Real-time supply-chain platforms enabling just-in-time sterile inventory | +0.5% | North America & EU primary, selective APAC adoption | Long term (≥ 4 years) |

Source: Mordor Intelligence

Rise in Awareness & Global Guidelines for Single-Use Flush Syringes

Updated infection-control directives call for single-patient flush devices to eliminate cross-contamination. The 2024 CDC guidance on central-line care placed pre-filled saline syringes at the center of CLABSI-prevention bundles [1]Centers for Disease Control and Prevention, “Strategies to Prevent CLABSI in Acute-Care Hospitals,” cdc.gov . European regulators embedded similar requirements in the Medical Device Regulation, pushing hospitals toward validated supplies. Manufacturers that combine flush and hub disinfection in one unit, such as BD’s PosiFlush SafeScrub, now enjoy preferential tender status. Consistent rules across regions lower administrative costs for multinational hospital chains. As a result, the IV flush syringe market is benefiting from synchronized demand curves rather than region-specific spikes.

Rising Incidence of Chronic & Infectious Diseases Driving IV Therapy

The aging world population raises long-term catheter use, which in turn boosts flush-syringe volume. Diabetes, cancer, and cardiovascular conditions demand maintenance of patent lines for repeated infusions, increasing daily flushing frequency. Medicare’s 2025 expansion of the home-infusion benefit cuts patient out-of-pocket costs, supporting durable demand in the United States. Similar schemes in Japan and South Korea now cover professional nursing visits, expanding product throughput outside hospitals. Persistent infection-control vigilance keeps saline the default, yet specialty heparin formulations are gaining share in oncology suites where thrombosis risk is high.

Rapid Switch to Pre-Filled Formats to Curb CLABSI and Save Nursing Time

Staff shortages intensified after the pandemic, and hospitals now seek workflow tools that reduce manual draws. Clinical studies from B. Braun show pre-filled units shave nearly four minutes off each flush cycle while cutting preparation errors by 54% [2]B. Braun Medical Inc., “Time Savings with Pre-Filled Syringes,” bbraun.com. The productivity gain allows facilities to redeploy scarce nurses toward higher-acuity tasks. Automation is extending further through RFID-tagged syringes that report stock levels in real time and lock expirations into electronic health-record alerts. These features lower waste and provide audit trails during FDA inspections, supporting premiums on quality-assured lines. The IV flush syringe market therefore moves steadily toward intelligent, ready-to-administer products.

Expansion of Home-Infusion & Outpatient Care Settings

Payers are steering low-acuity infusions away from inpatient wards to cut costs. Proposed US legislation, the Preserving Patient Access to Home Infusion Act, would widen reimbursement, potentially shifting thousands of catheter days into private residences. Ambulatory surgery centers are following suit, negotiating bundled deals for flush kits that arrive alongside custom procedure packs. Telehealth platforms now integrate connected syringes that alert nurses when patency checks are overdue, increasing caregiver confidence. Asia-Pacific governments back similar decentralization to meet rural-care gaps, fueling double-digit volume growth of small-size syringes appropriate for self-administration.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent FDA/EMA scrutiny & spike in product recalls | -0.8% | North America & EU primary, global spillover effects | Short term (≤ 2 years) |

| Limited nurse training on negative-pressure flushing technique | -0.4% | Global, more pronounced in emerging markets | Medium term (2-4 years) |

| Saline API shortages in US & EU causing intermittent supply gaps | -0.6% | North America & EU core, limited APAC impact | Medium term (2-4 years) |

| Low awareness and adoption in developing regions | -0.5% | APAC emerging markets, MEA, Latin America | Long term (≥ 4 years) |

Source: Mordor Intelligence

Stringent FDA and EMA Scrutiny with Spike in Product Recalls

Multiple Class I recalls between 2024 and 2025 exposed defects ranging from syringe-pump incompatibility to particulate contamination. The FDA now requests expanded human-factors data and longer real-time aging studies before clearance [3]U.S. Food and Drug Administration, “Medical Device Recalls 2024-2025,” fda.gov . Europe’s postmarket surveillance rules raise reporting overhead, prompting small suppliers to exit. Established firms respond with enterprise-wide quality-management upgrades, slowing new product timelines but solidifying brand trust. Although the stricter climate constrains near-term supply, it also sets a higher entry bar that protects incumbents once compliance costs are absorbed.

Saline API Shortages in US & EU Causing Intermittent Supply Gaps

Storm damage at a major Baxter facility in 2024 demonstrated the fragility of single-site production, removing a majority of US saline capacity overnight. Hospitals rationed IV solutions and postponed elective surgeries. Regulators issued temporary import waivers, yet freight bottlenecks limited relief. Manufacturers now invest in distributed plants and dual-sourcing agreements to guard against similar shocks. In the interim, patchy input availability still disrupts production plans, forcing buyers to hold more safety stock and dampening market growth until redundant capacity comes online.

Segment Analysis

By Product: Saline Dominance Faces Heparin Innovation

Saline syringes captured 82.13% of the IV flush syringe market in 2024 thanks to universal protocol alignment and competitive pricing. Clinicians regard normal saline as the safest default for most peripheral and central lines, a stance codified in multiple infection-control guidelines. However, specialty therapy growth is tilting incremental volume toward anticoagulant variants. Heparin syringes exhibit the fastest 6.43% CAGR as oncology centers rely on extended patency for implanted ports. Combination formats that hold saline and heparin in adjacent chambers let caregivers tailor flush regimens while minimizing waste.

Heparin uptake also benefits from rising use of peripherally inserted central catheters in ambulatory settings. Evidence suggests timely anticoagulant flushing reduces device replacement frequency, cutting total cost of care despite higher unit pricing. The regulatory environment remains exacting due to systemic anticoagulation risk, yet large suppliers with pharmacovigilance infrastructure win approvals and capture emerging share. Consequently, product-line breadth has become a differentiator, reinforcing consolidation trends within the IV flush syringe market.

Note: Segment shares of all individual segments available upon report purchase

By Volume Capacity: 10 mL Leadership Challenged by Pediatric Demand

The 10 mL category held 62.34% of the IV flush syringe market size in 2024, mirroring adult catheter flushing guidelines that recommend larger volumes for full lumen clearance. Hospitals value reduced procedure counts, so bulk purchasing favors this volume for central-line routines. Nevertheless, 3 mL formats post a 6.54% CAGR, propelled by pediatric and home-infusion use where smaller fluid loads are critical. Parents administering therapy at home appreciate manageable plunger resistance and minimal liquid waste.

Product developers respond with ergonomic grips and color-coded barrels that distinguish pediatric doses. Intermediate 5 mL syringes maintain relevance for mid-bore catheters, yet the fastest expansion remains at the low end. Smart pump integration now requires precise barrel geometry recognition, encouraging manufacturers to align dimensions across capacities in order to streamline device libraries and lower training time. These design harmonizations tighten customer lock-in and support long-term revenue visibility within the IV flush syringe market.

By End-User: Hospital Dominance Yields to Home-Care Innovation

Hospitals and clinics represented 65.56% of revenue in 2024, underscoring their role as the primary site for complex IV therapy. Procurement teams negotiate multi-year contracts that bundle flush kits with catheters and pumps, giving incumbents scale advantages. Rising staffing pressures, however, compel earlier patient discharge, and home-care entities now post the fastest 6.58% CAGR. The broadened US reimbursement that took effect in 2025 reimburses nursing visits and supplies, boosting adoption.

Home-infusion growth requires intuitive packaging, tamper-evident seals, and clear labeling that supports caregivers with varied skill levels. Vendors are piloting telemetric caps that confirm dose delivery and transmit data to virtual-care platforms. Ambulatory surgery centers, classed under the “Others” segment, also expand bulk ordering of pre-filled flush products to synchronize postoperative protocols. The diversification of care locations therefore spreads risk and broadens the demand base for the IV flush syringe market.

Note: Segment shares of all individual segments available upon report purchase

By Patient Age Group: Adult Market Stability Meets Geriatric Growth

Adults delivered 61.19% of sales in 2024, reflecting stable utilization across emergency, surgical, and chronic-care pathways. Usage intensity is highest in oncology and autoimmune infusion clinics. In contrast, the geriatric segment records the strongest 6.49% CAGR because older populations experience higher catheter-related complication rates and require longer treatment duration. Clinicians increasingly adopt flush devices with larger finger flanges and low-force plungers to accommodate diminished hand strength.

Pediatric demand remains consistent but specialized, emphasizing weight-based flush volumes and minimal dead-space syringes to avert fluid overload. Manufacturers supply distinct labeling to prevent errors during rapid code handoffs. Expanded caregiver education programs reinforce correct negative-pressure technique, reducing occlusion events. Collectively, these age-specific adaptations enlarge total addressable volume and sustain growth momentum for the IV flush syringe market.

Geography Analysis

North America contributed 41.49% of global revenue in 2024, supported by robust hospital infrastructure, broad insurance coverage, and rigorous safety mandates. The 2024 saline shortage accelerated substitution toward pre-filled flushes that optimize stock and reduce waste, reinforcing domestic demand. US regulatory vigilance prompts suppliers to maintain real-time traceability, a capability that commands pricing premiums. Canada mirrors these standards, while Mexico’s public-health investment upgrades infusion protocols in tertiary centers.

Europe presents a mature yet opportunity-rich environment. Implementation of the Medical Device Regulation in 2025 harmonized reporting and accelerated mutual recognition, simplifying cross-border procurement. Sustainability directives encourage lighter barrels and recyclable packaging, steering incremental innovation. Continued emphasis on infection-prevention targets sustains steady purchasing, and digital inventory platforms adopted by leading hospital trusts further standardize flush volumes.

Asia-Pacific records the fastest 6.69% CAGR and steadily raises its share of the IV flush syringe market. Health-system expansion and insurance reform in China and India unlock new patient cohorts. Japan’s super-aged society drives home-infusion uptake, while South Korea’s health-tech ecosystem spurs early adoption of connected syringes. Regulatory convergence under the APEC framework cuts dossier review times and encourages technology transfer partnerships, enabling local facilities to scale output faster. Government incentives for domestic medical-device production reduce import reliance and lower landed costs, further accelerating regional uptake.

Competitive Landscape

The IV flush syringe market remains moderately consolidated, with economies of scale, regulatory sophistication, and branded credibility separating leaders from niche suppliers. BD fortified its portfolio by absorbing Edwards Lifesciences’ Critical Care unit in 2024, adding smart-pump connectivity that dovetails with its PosiFlush suite. The planned 2025 spin-off of diagnostics will allow BD to direct more capital toward medication-delivery growth. B. Braun secured FDA clearance for its DUPLEX dual-chamber system, offering combined therapy and flush delivery in one sterile unit.

ICU Medical teamed with Otsuka Pharmaceutical Factory in a USD 200 million venture that establishes a distributed network able to produce 1.4 billion IV units yearly, mitigating regional supply shocks. Cardinal Health retains scale in distribution, yet recent syringe recalls underscore the cost of compliance lapses. Quality-assurance investments, including expanded automated vision systems, are restoring confidence. Smaller regional players focus on private-label production for group purchasing organizations but face higher per-unit regulatory overhead, nudging the competitive center toward the top five firms.

Technology differentiation now extends beyond sterility into data analytics. RFID-enabled barrels, near-field communication chips, and color-changing hubs that verify antiseptic contact time gain acceptance in North America and Western Europe. Suppliers with patent estates covering these features negotiate multiyear preferred-supplier agreements. In Asia-Pacific, joint ventures that transfer know-how and satisfy localization quotas open fresh volume channels, allowing incumbent multinationals to reinforce share while adhering to local content rules. Consolidation momentum is therefore likely to continue through the forecast horizon.

IV Flush Syringe Industry Leaders

-

BD (Becton, Dickinson and Company)

-

B. Braun Melsungen AG

-

Cardinal Health

-

Nipro Corporation

-

Medline Industries, LP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BD announced intent to separate its Biosciences and Diagnostic Solutions business to create a focused medical-technology company with USD 17.8 billion in revenue that will prioritize medication-delivery platforms including flush syringes.

- November 2024: ICU Medical and Otsuka Pharmaceutical Factory formed a USD 200 million joint venture to build one of the world’s largest IV-solution manufacturing networks, targeting annual output of 1.4 billion units.

- April 2024: The FDA issued a safety communication advising health-care facilities not to use recalled saline and sterile-water products, including certain flush syringes produced by Nurse Assist.

Global IV Flush Syringe Market Report Scope

As per the scope of the report, IV flush syringes are medical devices utilized to clear intravenous lines. When utilized correctly, saline flushes are generally safe and well tolerated by patients, but complications could occur. Although rare, IV flush syringes could introduce air embolisms into a vein, that could lead to heart attacks, strokes, and respiratory failure. Contaminated syringes have been linked to serious bacterial infections in patients. In rare cases, a serious allergic reaction may occur. The IV Flush Syringe market is segmented by Product (Saline IV Flush Syringe and Heparin IV Flush Syringe), End-User (Hospital & Clinics, Ambulatory Surgical centers, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers the value (in USD million) for the above segments.

| By Product | Saline IV flush syringes | ||

| Heparin IV flush syringes | |||

| By Volume Capacity | 3 mL | ||

| 5 mL | |||

| 10 mL | |||

| Others | |||

| By End-User | Hospitals and Clinics | ||

| Ambulatory Surgical Centers | |||

| Home-care Settings | |||

| Others | |||

| By Patient Age Group | Adults | ||

| Pediatric | |||

| Geriatric | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Saline IV flush syringes |

| Heparin IV flush syringes |

| 3 mL |

| 5 mL |

| 10 mL |

| Others |

| Hospitals and Clinics |

| Ambulatory Surgical Centers |

| Home-care Settings |

| Others |

| Adults |

| Pediatric |

| Geriatric |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is the current size of the IV flush syringe market?

The IV flush syringe market is valued at USD 440.55 million in 2025.

How fast is the IV flush syringe market expected to grow?

From 2025 to 2030 the market is projected to expand at a 5.82% CAGR.

Which product type dominates the IV flush syringe market?

Saline syringes dominated with an 82.13% revenue share in 2024.

Why are 3 mL syringes gaining popularity?

They post the fastest 6.54% CAGR because pediatric and home-infusion protocols often prefer smaller flush volumes for safety and comfort.

Which region will grow the quickest through 2030?

Asia-Pacific is forecast to record the highest regional CAGR at 6.69% as healthcare infrastructure and regulatory convergence improve access.

Page last updated on: June 25, 2025