Italy Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

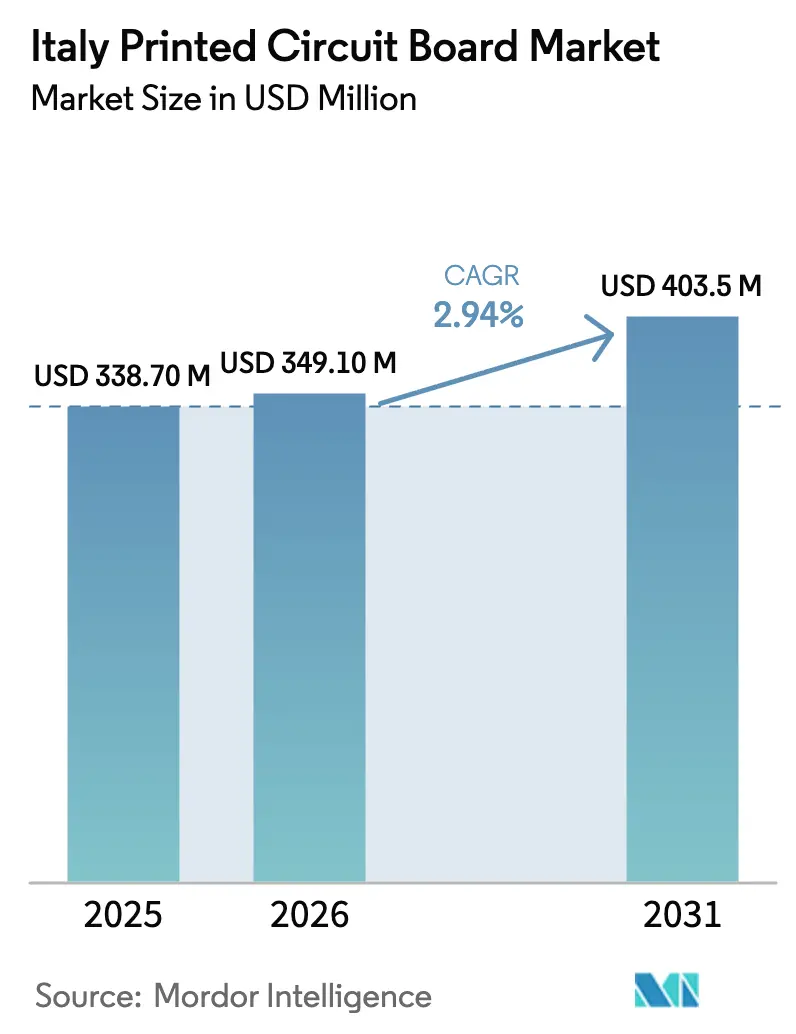

| Base Year Market Size (2025) | USD 338.70 Million |

| Market Size (2026) | USD 349.10 Million |

| Market Size (2031) | USD 403.5 Million |

| Growth Rate (2026 - 2031) | 2.94% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Printed Circuit Board Market Analysis by Mordor Intelligence

The Italy Printed Circuit Board Market is expected to grow from USD 338.70 million in 2025 to USD 349.10 million in 2026 and is forecasted to reach USD 403.5 million by 2031 at 2.94% CAGR over 2026-2031. This steady trajectory reflects a re-shoring wave in automotive and defense electronics, stronger semiconductor policy support, and widening demand for low-loss laminate solutions that align with 5G roll-outs. Domestic fabricators are capitalizing on shorter lead times, while high-speed material qualifications create cross-selling opportunities into data-center and radar platforms. Meanwhile, vertical integration around the Silicon Carbide value chain is tying silicon innovation to substrate and final-assembly demand, amplifying the linkage between wafer capacity and printed circuit board purchasing. Copper-price volatility and elevated power tariffs temper headline growth, yet they also reward process optimization and copper-weight reduction strategies that safeguard margins.

Key Report Takeaways

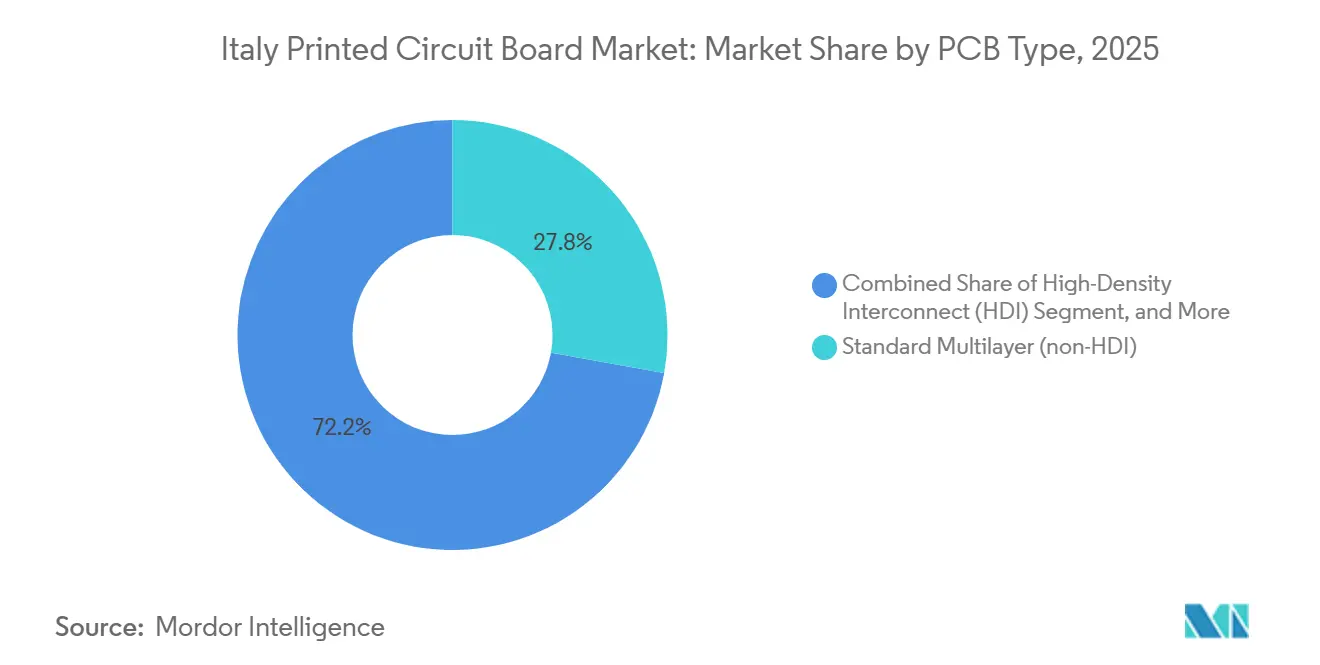

- By PCB type, standard multilayer non-HDI rigid boards led with 27.82% revenue share, of Italy printed circuit board market, in 2025, while flexible circuits are projected to expand at a 3.17% CAGR through 2031.

- By substrate material, glass-epoxy FR-4 accounted for 42.34% of the Italy printed circuit board (PCB) market share in 2025, whereas high-speed low-loss laminates are advancing at a 3.26% CAGR to 2031.

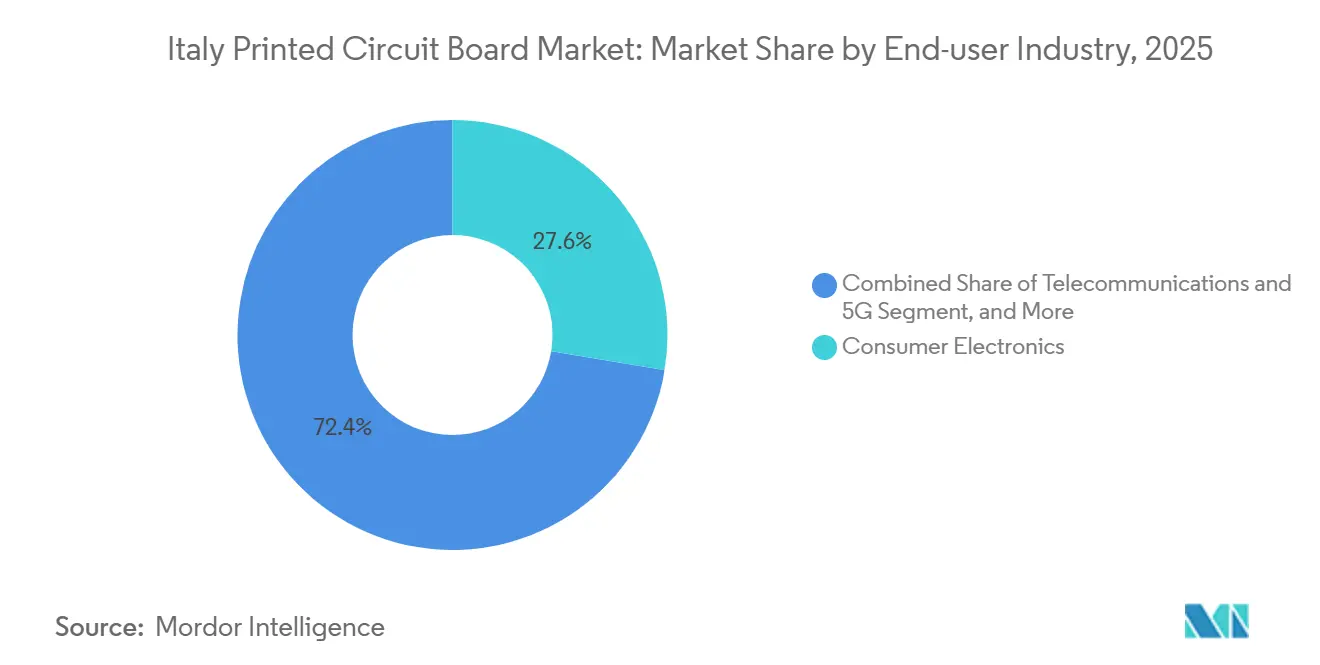

- By end-user industry, consumer electronics captured 27.61% of the Italy PCB market size in 2025, but automotive and electric-vehicle applications are growing at a 4.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Consumer Electronics and IoT Devices | +0.4% | Lombardy and Emilia-Romagna clusters | Medium term (2-4 years) |

| Growing Adoption of Electric Vehicles | +0.6% | Turin automotive corridor and Emilia Motor Valley | Long term (≥ 4 years) |

| Rapid Deployment of 5G Infrastructure | +0.5% | Milan, Rome, Naples metropolitan areas | Short term (≤ 2 years) |

| Ongoing Miniaturization and HDI Requirements | +0.4% | Medical hubs in Lombardy and Veneto | Medium term (2-4 years) |

| Reshoring of High-Tech PCB Prototyping | +0.3% | Nationwide with IPCEI Microelectronics support | Long term (≥ 4 years) |

| EU Chips Act Investments in Advanced Substrates | +0.5% | Sicily (Catania) and Lombardy (Agrate Brianza) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Electric Vehicles

Ferrari’s EUR 200 million (USD 236 million) e-building in Maranello is already sourcing flexible circuits for cylindrical battery modules and multilayer boards for 800-volt inverters, setting the tone for future sourcing preferences.[1]Ferrari N.V., “Ferrari Inaugurates E-Building in Maranello,” ferrari.com Stellantis followed in December 2025, confirming Mirafiori battery-pack output from mid-2026, which locks in high-current, high-temperature board demand across its next-generation Fiat 500 line. Vehicle electrification effectively doubles to triples the number of boards per unit, spanning battery-management, on-board chargers, and DC-DC converters. in the Italy printed circuit board market the local suppliers that match automotive qualification cycles and offer quick-turn layout support are winning prototype slots that later translate into serial volume. As platform life cycles compress, Tier-1s increasingly rely on Italian quick-turn capacity to de-risk ramp schedules.

Rapid Deployment of 5G Infrastructure

The National Recovery and Resilience Plan earmarked EUR 5.29 billion (USD 6.24 billion) for 5G, and a 2025 supply deal between Nokia and Telecom Italia triggers high-speed laminate pull-through.[2]Nokia, “Nokia and TIM Sign 3-Year 5G Supply Agreement,” nokia.com Every active antenna unit integrates up to eight multilayer PCBs, each fabricated on low-loss materials with dissipation factors below 0.004. Sub-6 GHz coverage dominates 2026 rollout, yet millimeter-wave densification after 2027 introduces a second build cycle for rigid-flex antenna boards. Domestic shops offering six-to-eight-week prototype-to-production schedules fill gaps that Asian providers cannot meet within compressed deployment timelines. Mandatory gigabit connectivity for 99.8% of households by 2026 further accelerates demand concentration in the Italy printed circuit board market.

EU Chips Act Investments in Advanced Substrates

STMicroelectronics’ EUR 5 billion (USD 5.9 billion) Silicon Carbide expansion in Catania and Agrate Brianza, alongside Silicon Box’s EUR 3.2 billion (USD 3.8 billion) packaging project, elevates thin-core IC and package substrates to strategic status.[3]STMicroelectronics, “STMicroelectronics Announces EUR 5 Billion Investment in Silicon Carbide Capacity Expansion,” st.com Ultra-fine line widths below 25 µm and via diameters under 75 µm require new build-up films such as ABF and BT resins, but European supply chains remain nascent. The Chips Act allocates EUR 3 billion (USD 3.5 billion) for substrate localization, opening space for Italian laminate producers to partner directly with back-end houses in the Italy PCB market. Early movers able to certify new resin systems on existing lamination equipment lock in preferred-supplier status long before high-volume manufacturing commences in 2027.

Ongoing Miniaturization and HDI Requirements

Medical-device companies in Lombardy and Veneto are migrating toward laser-drilled microvia designs to shrink device footprints under 20 mm × 30 mm. HDI architectures achieve 75 µm trace-and-space rules, double routing density, and sustain signal integrity for multi-gigabit data links. Premium pricing stems from ISO 13485 traceability and IEC 60601-1 safety compliance, which together impose rigorous documentation and process-control regimes. Flex and rigid-flex solutions in surgical robotics endure more than 100,000 dynamic bends, pushing copper foil thickness down to 12 µm. Suppliers that integrate computer-vision inspection and statistical-process-control analytics reach IPC Class 3 yield targets, reinforcing Italy’s reputation for high-reliability medical electronics in the Italy PCB market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Copper Prices | -0.5% | Nationwide across all fabricators | Short term (≤ 2 years) |

| Competition from Low-Cost Asian Imports | -0.4% | Nationwide, most acute for commodity board types | Medium term (2-4 years) |

| Lead Times for Semiconductor-Grade Substrates | -0.2% | IC substrate and HDI segments | Medium term (2-4 years) |

| Skilled Labor Shortage in Advanced Processing | -0.3% | Northern industrial regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Copper Prices

Spot copper climbed 34% between August 2025 and January 2026, eroding margins by 200-300 basis points for shops on quarterly contracts.[4]London Metal Exchange, “Copper Futures Prices,” lme.com Smaller players without hedging capacity absorbed the hike, prompting thinner-foil and narrower-trace design shifts that cut copper usage per panel. Unpredictable raw-material swings deter long-horizon capex planning, delaying installation of lamination presses and plating lines. Forward-contract strategies mitigate exposure, but only vertically integrated groups possess the treasury depth to lock in multi-month coverage. Until prices stabilize, board makers, in the Italy printed circuit board market, continue to prioritize material-light stack-ups and reduce work-in-process inventories.

Competition from Low-Cost Asian Imports

Imports from China, Taiwan, and South Korea covered roughly 60% of Italian demand by value in 2024, leveraging unit costs 25-35% lower on commodity multilayer and double-sided boards.[5]Eurostat, “Customs Data for PCB Imports,” ec.europa.eu While the Carbon Border Adjustment Mechanism intends to price embedded emissions, PCBs sit in a definitional gray zone, postponing protective tariffs. Italian producers are pivoting to quick-turn, HDI, and rigid-flex niches where design collaboration and two-to-three-week cycles justify premiums. Nonetheless, any delay in value-added migration risks ceding further share to import competition during the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PCB Type: Flexible Circuits Lead Miniaturization Wave

Flexible circuits command the spotlight, growing at a 3.17% CAGR and steadily lifting their portion of the Italy printed circuit board market. Demand stems from battery modules, wearable health sensors, and foldable electronics that require substrates capable of continuous bending without microcracking. In contrast, standard multilayer non-HDI rigid boards maintained 27.82% of the Italy printed circuit board market size in 2025 but face intensified price competition that limits expansion potential. High-density interconnect boards, with stacked microvias and sequential build-up layers, are migrating from smartphones into automotive radar and advanced driver-assistance systems, supporting the broader Italy printed circuit board market push toward engineering complexity. Rigid-flex architectures win aerospace adoption because foldable form factors shave mass while preserving vibration resilience. One- and two-sided boards continue a managed decline as appliance makers consolidate circuitry into integrated power modules. Throughout this shift, domestic fabricators leverage proximity to design centers, capturing prototype programs and then scaling into medium-volume lots.

The Italy printed circuit board market benefits from Ferrari, Leonardo, and medical OEMs that prioritize quick-turn partners able to iterate stack-ups within days. Such customers reward end-to-end engineering engagement, encompassing signal-integrity simulation, panel utilization, and thermal path design. Within flexible and HDI work, Italy printed circuit board industry participants integrate laser direct imaging and plasma desmear to achieve IPC Class 3 reliability. This technology mix sustains pricing power and offsets shrinking volumes in legacy rigid formats. Emerging opportunities lie in ultra-thin IC substrates once Silicon Box brings its Italian facility online, potentially spawning a local ecosystem for carrier boards and interposer supply by 2028.

By Substrate Material: High-Speed Laminates Gain on 5G and Data Centers

Glass-epoxy FR-4 dominated with 42.34% of the Italy PCB market share in 2025, yet its loss tangent above 0.02 constrains use beyond 10 GHz. High-speed low-loss materials are therefore accelerating at a 3.26% CAGR as telecom and data-center switch OEMs pursue dielectric constants below 3.5. The Italy printed circuit board (PCB) market increasingly specifies Rogers, Isola, and Panasonic laminates for macro-cell radios and optical-backplane routers, anchoring multi-year qualification roadmaps. Polyimide remains essential for flex boards because it retains mechanical integrity at 260 °C reflow temperatures. Despite costing three-to-four times more than FR-4, polyimide secures orders in battery packs, surgical robotics, and avionics where thermal cycling is severe.

Further upstream, ABF and BT resins emerge in IC packaging substrates, albeit in low volumes until domestic ABF production matures. Ceramic-filled PTFE and liquid-crystal polymer live in specialty RF front-end and satellite payload niches where extreme dielectric stability is mandatory. Supply-chain tightness around copper foil continues to affect every laminate tier, reinforcing the Italy printed circuit board market emphasis on thinner base weights and reduced panel scrap. Partnerships between local fabricators and global material houses shorten qualification loops, letting shops retool presses through software-defined temperature and pressure profiles rather than major hardware overhauls.

By End-User Industry: Automotive and EV Outpace Consumer Electronics

Consumer electronics contributed 27.61% of the Italy printed circuit board market size in 2025, covering smartphones, tablets, and white-goods controls. However, automotive and electric-vehicle demand is the momentum engine, rising at a 4.02% CAGR to 2031 as powertrain electrification multiplies board counts per vehicle. Traction inverters, battery-management systems, and on-board chargers require multilayer constructions that withstand 800-volt architectures and ambient temperatures exceeding 125 °C. The Italy printed circuit board market therefore aligns R&D spend toward heavy-copper, high-thermal-conductivity designs compatible with silicon-carbide semiconductors. Telecommunications infrastructure also drives material upgrades, but its volume plateau post-2027 moderates growth relative to the EV surge.

Industrial automation retains a stable share thanks to Italy’s Industry 4.0 incentives, funneling programmable-logic-controller and motor-drive orders into regional board shops. Medical electronics offers premium margins on modest volume, tied to ISO 13485 traceability, while aerospace and defense boards enjoy long program horizons courtesy of Leonardo’s EUR 44.2 billion (USD 52.1 billion) backlog. Data centers and AI servers contribute niche high-layer-count backplanes, yet the country’s limited hyperscale footprint tempers absolute square-meter demand when compared with Northern European clusters. Energy-storage projects and smart-grid upgrades round out emerging applications that require high-isolation, high-frequency switching layouts.

Geography Analysis

Northern Italy remains the nucleus of production and demand, stretching from Lombardy through Piedmont, Veneto, and Emilia-Romagna. The cluster’s dense network of automotive OEMs, industrial-automation suppliers, and medical-device firms underpins rapid prototype cycles, anchoring the Italy printed circuit board market in just-in-time workflows. Electricity tariffs around EUR 108 (USD 127) per megawatt-hour in 2024 exceeded the European average, nudging some high-energy lamination steps toward night-shift scheduling or partial offshoring. Still, cross-border freight from Austria and Germany keeps lead times within two days, preserving regional competitiveness.

Southern Italy’s profile is rising as STMicroelectronics expands its Silicon Carbide wafer hub in Catania and as Silicon Box builds an advanced-packaging site in the north. These projects knit front- and back-end silicon with downstream board assembly, potentially shifting substrate logistics southward after 2027. The Made in Italy Fund has earmarked EUR 700 million (USD 825 million) in grants for HDI and rigid-flex capacity upgrades, steering capex toward process automation and optical inspection. Neighboring Central and Eastern European nations offer 40-50% lower labor costs, yet they lack the dense OEM co-location that shortens design iterations, mitigating the labor gap to an extent.

Regulatory hurdles remain a drag: complex permitting adds 12-18 months to green-field expansions, and social-security contributions inflate employment overhead. Nonetheless, participation in Important Projects of Common European Interest allows Italian projects to bypass state-aid ceilings for strategic microelectronics ventures. EU Recovery and Resilience funds support digital infrastructure, indirectly sustaining demand for telecom PCBs, but disbursement bottlenecks slow contract awards. Overall, the Italy printed circuit board market leverages geographic proximity to high-value OEMs despite structural cost disadvantages.

Competitive Landscape

Domestic specialists such as Somacis, Cistelaier, Elemaster, anchor the medium-volume, high-mix segment, focusing on automotive, industrial, and medical verticals in the Italy printed circuit board (PCB) market. Bain Capital’s 2024 purchase of Somacis signals private-equity appetite for consolidating these mid-tier firms to unlock procurement scale and broaden HDI and rigid-flex portfolios. Global players such as AT&S, TTM Technologies, and Flex serve Italy through multi-site European networks, with AT&S’s Leoben plant positioned to truck boards to northern Italy in under 48 hours. Asian giants like Unimicron and Zhen Ding generally deliver commodity multilayer volumes on eight-to-twelve-week cycles, ceding prototyping business to European shops.

Technology adoption varies: leaders deploy laser direct imaging, plasma desmear, and automated optical inspection to achieve IPC Class 3 yields above 95%, while smaller facilities rely on mechanical drilling and manual screen printing that limit applications to IPC Class 2. Design-for-manufacturing collaboration is emerging as the primary battleground. Fabricators increasingly embed engineers at customer sites to co-optimize stack-ups, via structures, and thermal paths, monetizing non-recurring engineering fees rather than competing purely on unit price.

White-space opportunity lies in IC and package substrates, a segment almost entirely imported today. Silicon Box’s Italian facility may serve as the tipping point that encourages local laminate production, creating a vertically integrated ecosystem from resin synthesis to thin-core lamination. High-frequency RF boards for satellite payloads and defense radars also present margin upside, as domestic suppliers can align with Leonardo’s long program cycles and security clearances. Overall, moderate fragmentation prevails, but consolidation momentum suggests the Italy PCB market is heading toward a more concentrated landscape by the decade’s close.

Italy Printed Circuit Board Industry Leaders

Somacis S.p.A.

Cistelaier S.p.A.

Elemaster S.p.A.

TTM Technologies, Inc.

AT&S AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Scanfil completed the acquisition of MB Elettronica, adding ISO 13485 cleanroom capacity for medical PCB assembly.

- December 2025: Stellantis confirmed Mirafiori battery-pack production from mid-2026, locking in demand for high-current power-distribution boards.

- November 2025: Nokia signed a three-year agreement with Telecom Italia to supply 5G macro-cell base stations, requiring an estimated 50,000 m² of low-loss PCBs annually.

- October 2025: Ferrari inaugurated its EUR 200 million (USD 236 million) e-building, integrating battery-pack assembly and inverter production that sources 60% of PCBs locally.

Italy Printed Circuit Board Market Report Scope

The Italy Printed Circuit Board Market / Italy Printed Circuit Board (PCB) Market / Italy PCB Market Report is Segmented by PCB Type (Standard Multilayer non-HDI Rigid, 1-2 Sided, High-Density Interconnect HDI, Flexible Circuits FPC, IC Substrates Package Substrates, Rigid-Flex, Other PCB Types), Substrate Material (Glass Epoxy FR-4, High-Speed Low-Loss, Polyimide PI, Packaging Resins BT ABF, Other Substrate Materials, Parent Substrate Material), and End-user Industry (Consumer Electronics, Computing and Data Centers, Telecommunications and 5G, Automotive and EV, Industrial and Power, Healthcare Medical, Aerospace and Defense, Other End-user Industries). The Market Forecasts are Provided in Terms of Value USD.

| Standard Multilayer (non-HDI) Rigid |

| 1-2 Sided |

| High-Density Interconnect (HDI) |

| Flexible Circuits (FPC) |

| IC Substrates (Package Substrates) |

| Rigid-Flex |

| Other PCB Types |

| Glass Epoxy (FR-4) |

| High-Speed / Low-Loss |

| Polyimide (PI) |

| Packaging Resins (BT / ABF) |

| Other Substrate Materials |

| Consumer Electronics |

| Computing and Data Centers |

| Telecommunications and 5G |

| Automotive and EV |

| Industrial and Power |

| Healthcare / Medical |

| Aerospace and Defense |

| Other End-user Industries |

| By PCB Type | Standard Multilayer (non-HDI) Rigid |

| 1-2 Sided | |

| High-Density Interconnect (HDI) | |

| Flexible Circuits (FPC) | |

| IC Substrates (Package Substrates) | |

| Rigid-Flex | |

| Other PCB Types | |

| By Substrate Material | Glass Epoxy (FR-4) |

| High-Speed / Low-Loss | |

| Polyimide (PI) | |

| Packaging Resins (BT / ABF) | |

| Other Substrate Materials | |

| By End-user Industry | Consumer Electronics |

| Computing and Data Centers | |

| Telecommunications and 5G | |

| Automotive and EV | |

| Industrial and Power | |

| Healthcare / Medical | |

| Aerospace and Defense | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the current valuation of the Italy printed circuit board market?

The Italy printed circuit board market size stands at USD 349.1 million in 2026 and is projected to reach USD 403.5 million by 2031.

Which application segment is expanding the fastest?

Automotive and electric-vehicle applications are advancing at a 4.02% CAGR, outpacing all other end-use verticals.

How significant is flexible-circuit demand within Italy?

Flexible circuits are growing at a 3.17% CAGR, benefiting from battery modules, wearables, and foldable devices that need durable bending performance.

Which substrate materials are gaining share?

High-speed low-loss laminates are increasing at a 3.26% CAGR as 5G and data-center hardware require lower dielectric loss.

What policy measures support local PCB capacity?

EU Chips Act funding and the Italian Made in Italy Fund provide grants and state-aid exemptions that incentivize HDI and substrate investments.

How are copper-price swings affecting manufacturers?

A 34% upswing in copper prices compressed margins by up to 300 basis points, prompting thinner-foil designs and heightened focus on material hedging.

Page last updated on: