Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

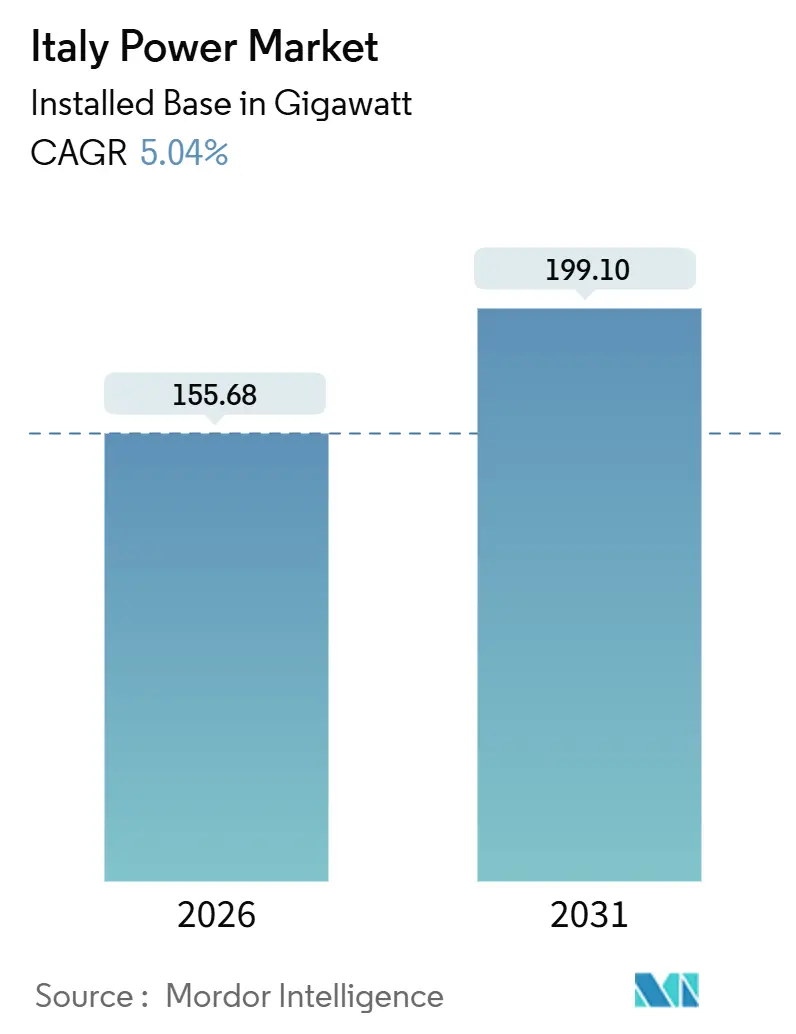

| Market Volume (2026) | 155.68 gigawatt |

| Market Volume (2031) | 199.10 gigawatt |

| Growth Rate (2026 - 2031) | 5.04% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Power Market Analysis by Mordor Intelligence

The Italy Power Market size in terms of installed base is expected to grow from 155.68 gigawatt in 2026 to 199.10 gigawatt by 2031, at a CAGR of 5.04% during the forecast period (2026-2031).

This outlook is anchored by accelerated renewable additions, the coal-fired phase-out, and a EUR 16.5 billion–23 billion transmission-upgrade plan that aims to double cross-border exchange capacity beyond 30 GW.[1]Terna S.p.A., “2024-2034 Development Plan,” terna.it Developers are racing to secure grid access in Apulia and Sicily, where streamlined permitting has shortened approval cycles to months, yet congestion risks remain high and have already triggered curtailment penalties above 8% of potential output in 2024.[2]Autorità di Regolazione per Energia Reti e Ambiente, “Annual Report 2025,” arera.it Natural gas continues to fuel roughly 50% of generation and, given 90% import exposure, creates a vulnerability to geopolitical price shocks despite new LNG terminals and pipeline diversification. Storage is scaling quickly: Terna’s inaugural MACSE auction in 2024 awarded 2.3 GW of grid-scale batteries, signaling a structural pivot from gas peakers toward lithium-ion and flow technologies that capture day-ahead spreads and supply ancillary services.

Key Report Takeaways

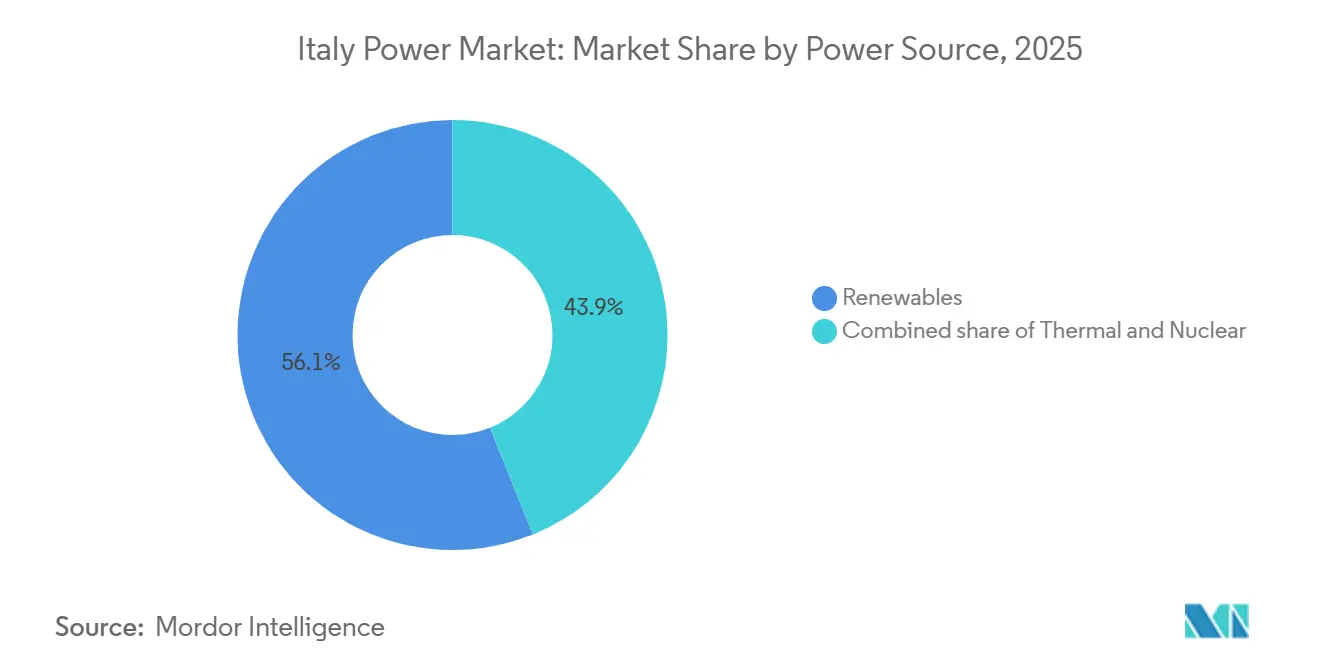

- By power source, renewables held 56.1% of Italy's power market share in 2025 and are advancing at an 8.9% CAGR through 2031.

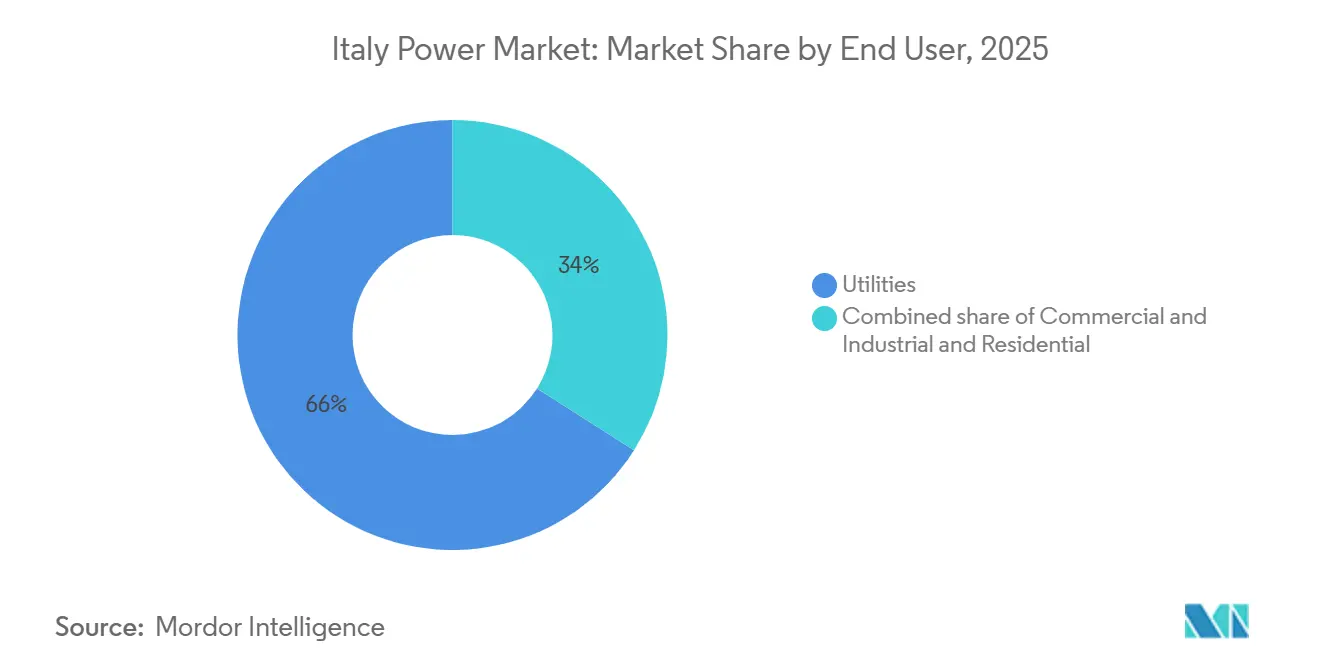

- By end user, the utility segment controlled 66% of Italy's power market share in 2025 and is expanding at a 6.7% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Permitting Reforms under Legislative Decree 199/2021 | +1.2% | National, with higher uptake in southern regions (Apulia, Sicily, Calabria) | Medium term (2-4 years) |

| Grid-scale Battery Capacity Market Auctions (Terna) | +0.8% | National, concentrated in high-congestion zones (Apulia, Sicily) | Short term (≤ 2 years) |

| Coal Phase-out by 2025 Creating Capacity Gap | +0.9% | National, acute in Sardinia and mainland coal-dependent zones | Short term (≤ 2 years) |

| REPowerEU-funded HVDC Projects (Tyrrhenian Link) | +0.6% | Sardinia-mainland corridor, spillover to Sicily-Tunisia link | Long term (≥ 4 years) |

| Corporate PPAs Surge among Luxury & FMCG Majors | +0.5% | National, concentrated in northern industrial regions (Lombardy, Veneto, Emilia-Romagna) | Medium term (2-4 years) |

| Superbonus 110% Stimulus for Rooftop PV | +0.4% | National, with highest adoption in northern homeownership zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Permitting Reforms Under Legislative Decree 199/2021

Legislative Decree 199/2021 cut solar and onshore wind approval cycles from more than two years to roughly six months for projects under 10 MW, while Decree 190/2024 extended the fast track to repowering and hybrid storage configurations. Over 15 GW of applications were filed between 2024 and early 2025, concentrated in Apulia, Sicily, and Calabria, where resource quality is strongest. Municipal veto power on landscape grounds continues to slow projects in heritage zones, creating regional disparities even as Italy aligns with its EU-wide 131 GW renewable target. Successful execution now depends on synchronized transmission upgrades that absorb intermittent inflows without driving up curtailment. Market participants who navigate local planning risks first can secure scarce grid nodes and lock in early-mover returns.

Grid-scale Battery Capacity Market Auctions (MACSE)

Terna’s 2024 MACSE auction awarded 2.3 GW of 10-year availability contracts, creating the first dedicated revenue stack for storage in the Italy power market. Winning projects, mainly 50 MW lithium-ion systems co-located with solar farms in Apulia and Sicily, address midday oversupply and evening peaks where price spreads topped EUR 100/MWh in summer 2025. The model sidelined pumped-hydro proposals that require multi-year construction and instead favored modular batteries deployable within 18 months. Terna’s 2026 auction is expected to introduce a six-to-eight-hour category, opening opportunities for flow batteries and compressed-air storage. Early project sponsors gain dual upside from arbitrage and capacity payments while shielding solar assets from curtailment, strengthening project bankability in a tight financing environment.

Coal Phase-Out by 2025 Creating Capacity Gap

Mainland coal plants totaling 5.7 GW will retire by end-2025, with Sardinian units following by 2029 once the Tyrrhenian Link is energized. The exit accelerates decarbonization: renewable generation hit 49% in 2024, but it tightens reserve margins during low-renewable spells, pushing Terna to procure 11.5 GW of capacity from Enel and others in the 2025 auction. Gas units will cover the gap, yet LNG price volatility remains a threat, underscoring the need for storage and demand-response scaling. Investors who can monetize flexibility services stand to benefit from rising peak-spread volatility until large-scale batteries reach critical mass after 2027.

REPowerEU-funded HVDC Projects (Tyrrhenian Link)

The EUR 3.7 billion, 1,000 MW Tyrrhenian Link broke ground in January 2025 with EUR 500 million in EU co-funding and is scheduled for commissioning in 2027-2028. Prysmian is manufacturing 480 km of XLPE submarine cable and will maintain the asset for 25 years, capturing long-run aftermarket revenue.[3]Prysmian Group, “Tyrrhenian Link Cable Contract,” prysmiangroup.com Once online, the link lets Sardinia import surplus mainland renewables, enabling the island’s final coal units to close and reducing diesel peaker dispatch that peaked at 15% of summer demand in 2024. Long lead times illustrate why HVDC benefits materialize only beyond 2027, yet securing social acceptance early locks in strategic interconnection capacity critical for 2030 renewable targets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid Congestion in Apulia & Sicily (≥36-month Delays) | -0.7% | Southern Italy (Apulia, Sicily, Calabria) | Short term (≤ 2 years) |

| Gas-Import Exposure to Geopolitical Shocks (≈90%) | -0.5% | National, acute during winter heating season | Medium term (2-4 years) |

| Offshore Wind Tender Under-realisation (Adriatic) | -0.3% | Adriatic Sea coastal regions (Apulia, Abruzzo, Marche) | Medium term (2-4 years) |

| Landscape-related Permit Litigation for Wind Farms | -0.4% | Heritage-sensitive zones (Tuscany, Umbria, Sicily) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid Congestion in Apulia & Sicily (≥36-Month Delays)

Apulia and Sicily host more than 40% of the renewable pipeline, yet 150 kV corridors designed for north-to-south flows now experience reverse overloads that triggered 8% curtailment in 2024, costing producers over EUR 200 million in lost revenue. Connection requests lodged in 2023 face ≥36-month delays as substations queue for reinforcement, forcing developers to accept interruptible agreements that shift curtailment risk onto project economics. Terna’s EUR 11 billion Hypergrid plan will reconductor southern lines and deploy dynamic-rating sensors by 2034, yet interim bottlenecks threaten to slow the forecast 8.9% renewable CAGR unless temporary capacity payments or grid-forming inverters mitigate risk.

Gas-Import Exposure to Geopolitical Shocks

Despite adding Algerian and Azerbaijani pipelines and floating LNG units in Piombino and Ravenna, Italy still imports about 90% of its gas, leaving power prices linked to TTF hub volatility that topped EUR 50/MWh during winter 2024-2025. Coal retirements deepen reliance on combined-cycle units, so any supply shortfall forces expensive LNG cargos into the merit order. Tariffs for unhedged households rose 15-20% in early 2025, and prolonged price spikes could dampen the 5.04% CAGR of the Italy power market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Source: Renewables Outpace Thermal Replacement

Renewables accounted for 56.1% of installed capacity in 2025, the largest slice of the Italy power market, and are projected to grow at an 8.9% CAGR through 2031. Solar capacity surged by 5.3 GW in 2023, pushing the Italy power market size for solar past 30 GW; utility-scale projects in Apulia and Sicily contributed more than 60% of that buildout. The coal retirement removes 5.7 GW by 2025, cementing solar and onshore wind as primary replacements, though grid bottlenecks could temper momentum. Offshore wind remains marginal until 2028, and hydro expansion is capped by the EU Water Framework Directives, limiting diversification options.

Hydro still contributes 19 GW of reservoir and run-of-river assets, geothermal adds about 800 MW in Tuscany, and biomass-plus-waste holds 4 GW, giving Italy one of Europe’s most diversified renewable stacks. Combined-cycle gas turbines, presently 50 GW, will increasingly swing-dispatch to cover renewable droughts. Open-cycle gas peakers are being phased into synchronous condensers, and no nuclear program is under discussion. Altogether, the renewable surge underpins long-run decarbonization but heightens the urgency of storage and HVDC delivery so that the Italy power market can accommodate variable inflows without systemic risk.

By End User: Utilities Consolidate but C&I PPAs Rise

Utilities held 66% of installed capacity and electricity off-take in 2025, the dominant share of the Italy power market. Their segment is expanding at a 6.7% CAGR as they procure grid-scale renewables and battery capacity-market contracts that stabilize cash flows. Utilities secured most of the 2.3 GW MACSE awards in 2024, pairing batteries with solar farms to mitigate the curtailment that undermines merchant revenues in southern Italy.

Commercial and industrial buyers are still a smaller slice of Italy's power market size but are growing rapidly through 10- to 50-MW corporate PPAs priced below EUR 60/MWh, outpacing retail tariffs during gas-price spikes. Luxury houses, FMCG companies, and data-center operators are anchoring multi-GW renewable pipelines and forcing utilities to evolve their retail business models. Residential demand, buoyed by the Superbonus solar-plus-storage boom, now contributes a distributed-generation layer that meets up to 70% of annual household consumption for participating homes, squeezing utility margins yet widening the pool of dispatchable virtual power plants as battery adoption spreads.

Geography Analysis

Southern regions, led by Apulia and Sicily, house more than 40% of renewable applications, reflecting superior solar irradiance and onshore-wind resource quality.[4]: Autorità di Regolazione per Energia Reti e Ambiente, “Regional Demand Statistics,” arera.it These regions also bear the brunt of curtailment, underscoring why Terna has earmarked EUR 11 billion for Hypergrid reconductoring that will raise south-to-north transfer capacity by 50% once completed after 2030. The Italy power market size attributable to southern Italy is poised to grow fastest through 2031, provided congestion relief stays on schedule.

Northern industrial hubs, Lombardy, Veneto, and Emilia-Romagna, consume over 45% of national electricity, making them fertile ground for corporate PPAs that hedge volatile tariffs. Because local solar and wind resources are weaker, corporates import green power from the south, accepting basis risk on grid fees until north-bound HVDC reinforcements emerge. Distributed rooftop-PV adoption is highest here thanks to the Superbonus, flattening midday demand, and altering load-curve dynamics that utilities must price into retail tariffs.

Islands present distinct dynamics. Sardinia’s coal exit hinges on the Tyrrhenian Link energizing by 2028; until then, derogations allow limited coal burn to maintain grid stability. Sicily, already an export-oriented renewables hub, will gain interconnection redundancy via the link, enabling higher renewable penetration and reducing curtailment risk. Together, the islands showcase how HVDC and storage are core to balancing an archipelagic portion of the Italy power market without compromising reliability.

Competitive Landscape

Italy hosts a moderately consolidated generation stack: the top five producers, Enel, Edison, A2A, ERG, and Acea, control roughly 60% of capacity, while international entrants such as RWE, Iberdrola, and ENGIE are expanding utility-scale solar portfolios in the south. Enel’s vertical integration is distinctive; its 3Sun cell plant in Sicily will reach 3 GW of annual output by 2026, capturing manufacturing margins in addition to generation and retail. This positions Enel to capitalize on EU domestic-content preferences under the Net-Zero Industry Act and adds security-of-supply leverage against Asian panel imports.

Strategic positioning revolves around capacity-market bids, battery co-location, and long-term PPAs. Enel, A2A, and ERG won most MACSE contracts, locking a stable revenue stream and mitigating solar curtailment. Edison and RWE formed a joint venture for 500 MW of onshore wind in Basilicata and Calabria, signaling a pivot away from legacy gas assets toward fast-tracked renewables that qualify under Decree 190/2024. Smaller developers like Renantis and Sonnedix pursue agrivoltaic and hybrid models that bypass congested nodes by pairing batteries and solar behind a single point of interconnection.

Equipment suppliers compete on technology differentiation. Vestas is repowering early-2000s wind fleets with 4- to 5-MW turbines that raise site output by up to 50%, while Prysmian secures long-run cable orders tied to Terna’s HVDC budget, embedding annuity income through 25-year maintenance deals. As floating offshore wind matures, Siemens Gamesa and Hexicon are trialing platform designs suited to 50-meter depths off the Tyrrhenian coast, although capex intensity still limits near-term scale.

Italy Power Industry Leaders

Enel SpA

Edison SpA

A2A SpA

ERG SpA

Terna SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: ENGIE has inked a 15-year renewable Power Purchase Agreement (PPA) with Apple, underscoring its commitment to fast-tracking the adoption of green energy solutions via a diverse range of large-scale technologies. As part of this pact, ENGIE is set to establish two wind farms (74 MW), undertake the repowering of one wind farm (11 MW), and set up two agrivoltaic plants (88 MW).

- September 2025: Italy's energy agency, Gestore dei Servizi Energetici (GSE), has kicked off the second solar auction under the transitional FER X program, the country's fresh incentive mechanism for renewable energy.

- July 2025: Italy's energy agency, Gestore dei Servizi Energetici (GSE), has initiated a tender aimed at facilitating the installation of approximately 50 MW of floating photovoltaic (PV) capacity.

- April 2025: Gestore dei Servizi Energetici (GSE), Italy's energy agency, has set aside EUR 323 million for the nation's second agrivoltaic tender, tapping into leftover funds from the inaugural round, which wrapped up in December 2024. Bidders have until June 30 to submit their proposals.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts the Italy power market as the sum of all utility-scale and captive generation assets physically located in the country; capacity is expressed in gigawatts of net installed power and covers thermal, hydro, wind, solar, geothermal, and bioenergy plants. Electricity imported through interconnectors is excluded from the baseline, yet its impact is treated in demand modeling.

Scope exclusion: Transmission and distribution hardware, retail energy services, and auxiliary backup sets below 1 MW lie outside this sizing.

Segmentation Overview

- By Power Source

- Thermal (Coal, Natural Gas, Oil and Diesel)

- Nuclear

- Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal)

- By End User

- Utilities

- Commercial and Industrial

- Residential

- By T&D Voltage Level (Qualitative Analysis only)

- High-Voltage Transmission (Above 230 kV)

- Sub-Transmission (69 to 161 kV)

- Medium-Voltage Distribution (13.2 to 34.5 kV)

- Low-Voltage Distribution (Up to 1 kV)

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed grid planners, IPP managers, OEM service engineers, and energy-policy advisors across Lombardy, Sicily, and Lazio. These conversations validated retirement dates, average heat-rate evolution, and realistic construction lead times, filling gaps that desk research alone left open.

Desk Research

We began with public datasets from Terna's monthly capacity bulletins, Eurostat energy balances, IEA Electricity Information, and ENTSO-E transparency files, which gave dependable plant-level or technology-level figures. Financial filings from listed generators, parliamentary energy bills, and reputable press pieces such as Il Sole 24 Ore helped track commissioning delays and policy inflections. D&B Hoovers and Dow Jones Factiva, two of Mordor's paid databases, supplied historical investment and outage records. The sources cited are illustrative; many more feeds were screened, tagged, and archived for cross-checks.

Market-Sizing & Forecasting

A top-down reconstruction starts with Terna-verified capacity by technology for 2024; additions and retirements are layered on through 2030 using announced project pipelines, average permitting-to-COD lags, and expected capacity-factor improvements. Target figures are then reconciled with a sampled bottom-up roll-up of large plant nameplates and channel checks to fine-tune totals. Key variables like renewable auction awards, gas-price indexed dispatch costs, and grid connection queue lengths drive scenario spreads that feed an ARIMA forecast of annual net additions, which our domain experts reviewed before lock-in.

Data Validation & Update Cycle

Outputs run through variance dashboards that flag deviations versus IEA regional means and Terna's quarterly revisions; anomalies trigger a secondary analyst review. Reports refresh each year, and material policy changes prompt interim updates so clients always receive our latest calibrated view.

Why Mordor's Italy Power Baseline Commands Reliability

Published estimates often diverge because firms choose different scope boundaries, valuation units, and refresh cadences. Our disciplined capacity-based framework, refreshed annually, minimizes those mismatches.

Key gap drivers include rivals valuing revenue rather than physical capacity, omitting pumped-storage assets, or applying static currency conversions that distort euro-to-dollar trends.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 137.53 GW (2024) | Mordor Intelligence | - |

| 136.80 GW (2024) | Regional Consultancy A | Excludes cross-border pumped storage and captive CHP |

| USD 105.6 B (2024) | Global Consultancy B | Tracks sales revenue, not installed capacity; price assumptions undisclosed |

| USD 27.6 B (2024) | Trade Journal C | Uses average wholesale price only; limited value-chain coverage |

These contrasts show that Mordor's capacity-anchored, multi-variable model delivers a balanced, transparent baseline that decision-makers can readily trace and replicate.

Key Questions Answered in the Report

What is the current size of the Italy power market?

Installed capacity is 155.68 GW in 2026 and is set to reach 199.10 GW by 2031.

Which segment holds the largest Italy power market share?

Renewables led with 56.1% of capacity in 2025 and continue to expand fastest.

How fast will the utilities segment grow?

Utility off-take is forecast to expand at a 6.7% CAGR through 2031 as capacity-market and storage revenues rise.

What role do batteries play in Italy’s power mix?

Grid-scale batteries won 2.3 GW of ten-year MACSE contracts in 2024, providing flexibility to integrate intermittent renewables.

When will Sardinia fully exit coal generation?

Final coal units are scheduled to close by 2029 once the Tyrrhenian Link HVDC cable is operational.

Page last updated on: