Italy Pet Veterinary Diets Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

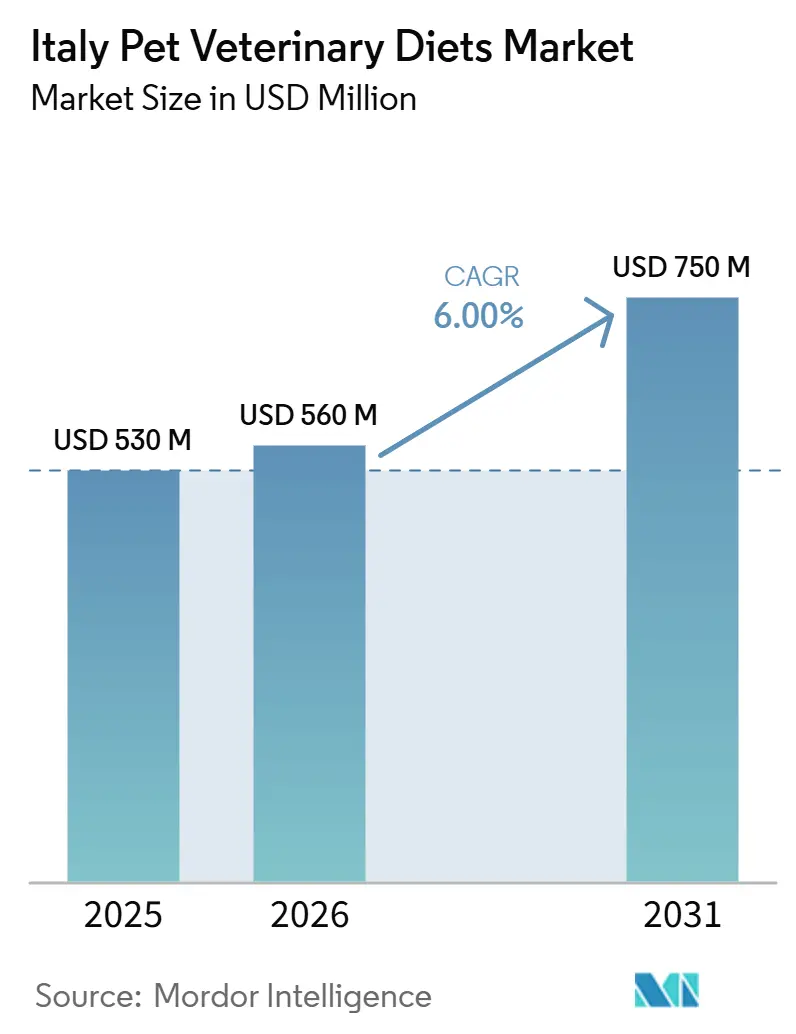

| Base Year Market Size (2025) | USD 530 Million |

| Market Size (2026) | USD 560 Million |

| Market Size (2031) | USD 750 Million |

| Growth Rate (2026 - 2031) | 6.00% CAGR |

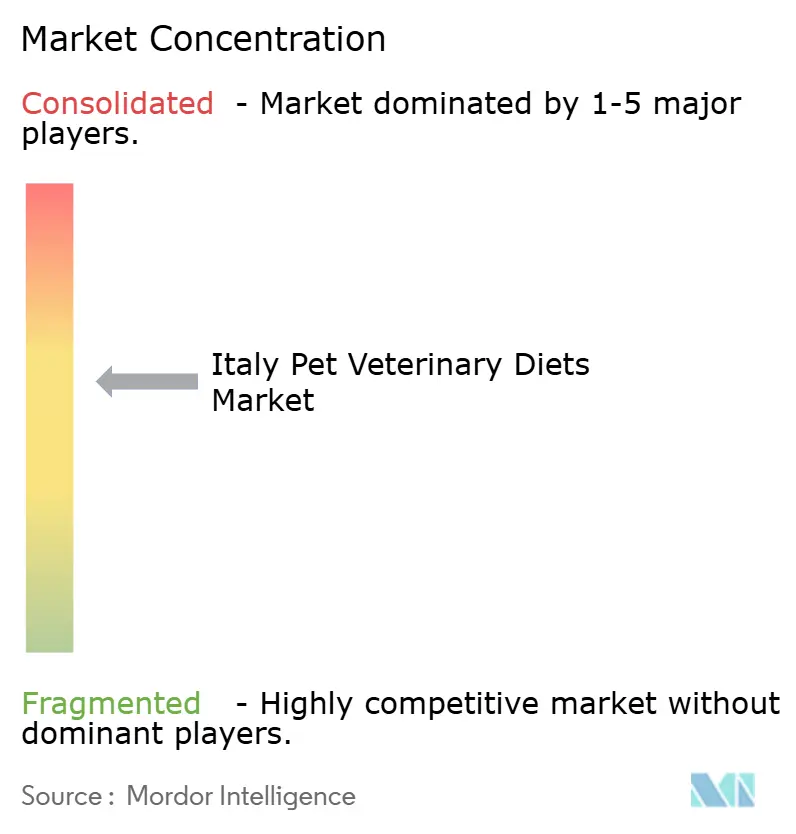

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Pet Veterinary Diets Market Analysis by Mordor Intelligence

The Italy Pet Veterinary Diets Market size is estimated to increase from USD 530 million in 2025 to USD 560 million in 2026 and reach USD 750 million by 2031, growing at a CAGR of 6% over 2026-2031. Therapeutic and specialist nutrition is capturing a growing share of total pet spending as pet owners increasingly prioritize products addressing digestive health, renal care, dermatology, mobility, and healthy aging. Italy's pet food and pet care market reached EUR 5.3 billion (USD 5.7 billion) in 2025, indicating a substantial consumer base for the continued growth of therapeutic feeding. The Italy pet veterinary diets market is further supported by stronger veterinary engagement, an aging pet population, and a rising trend among owners to view nutrition as an integral part of routine health management rather than just basic feeding. Colgate-Palmolive Company (Hill’s Pet Nutrition Inc.) reported a 23% increase in clinic-dispensed products in 2024, highlighting that veterinary recommendations remain the primary channel for adopting structured diets. Companies are responding with microbiome-focused product lines and digital tools to improve owner education, support refill adherence, and maintain the premium positioning of veterinary diet products in Italy's broader pet care market.

Key Report Takeaways

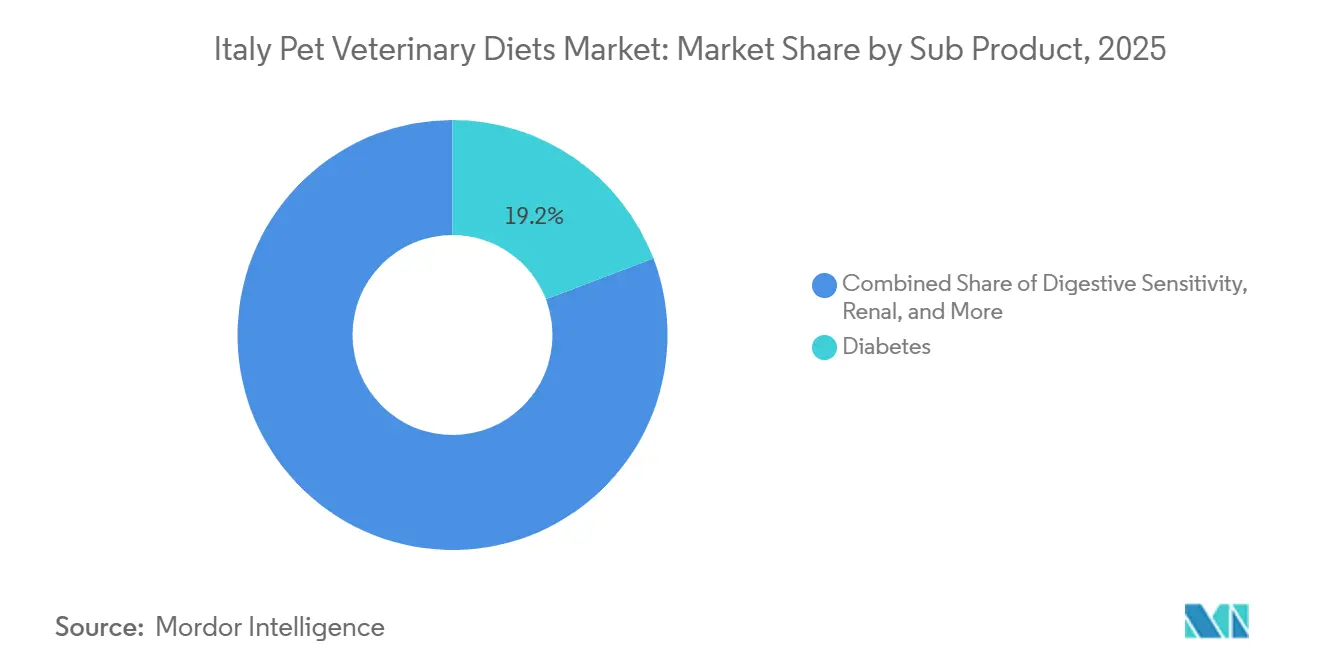

- By sub product, Diabetes was the largest segment with a market share of 19.2% in 2025, while digestive senstivity was the fastest-growing segment with 10.0% CAGR through 2031.

- By pets, dogs held 56.0% of the Italy pet veterinary diets market share in 2025, while dogs are forecast to expand at a 6.8% CAGR through 2031.

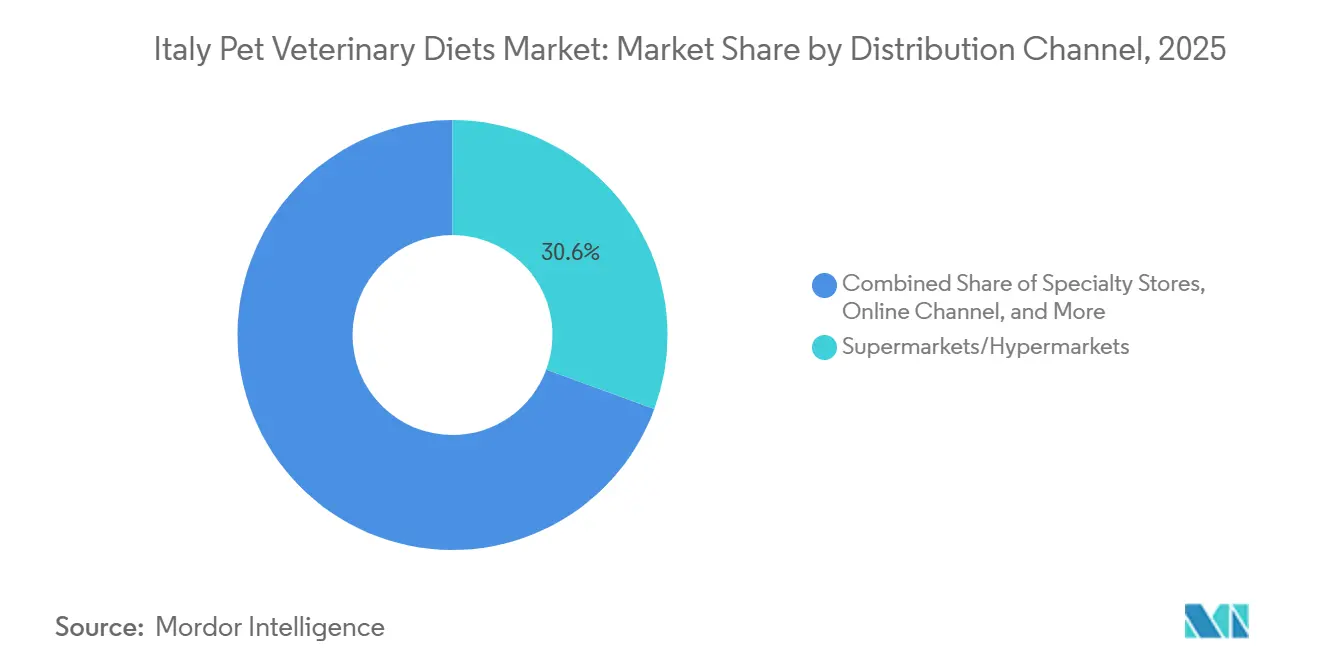

- By distribution channel, Supermarkets/Hypermarkets accounted for 30.6% of the Italy pet veterinary diets market size in 2025, while the Online Channel is projected to grow at a 6.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Pet Veterinary Diets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Veterinary Prescription Endorsement of Therapeutic Diets | +1.3% | National, with early gains in Milan, Rome, and Bologna | Short term (≤ 2 years) |

| Chronic Pet Disease Burden in Aging Pets | +1.1% | National | Medium term (2-4 years) |

| Premiumization of Condition-Specific Nutrition | +0.9% | National, strongest in northern Italian urban centers | Medium term (2-4 years) |

| E-Commerce Refill Convenience and Adherence | +0.7% | National | Short term (≤ 2 years) |

| Private Label Veterinary Diet Alternatives | +0.6% | National, with early gains in mid-tier specialty retail | Medium term (2-4 years) |

| Preventive Nutrition Adoption and Early Intervention | +0.7% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Veterinary Prescription Endorsement of Therapeutic Diets

Veterinary recommendations remain a key factor influencing purchasing decisions in the Italy pet veterinary diets market. According to the Assalco–Zoomark 2026 Report, 44.7% of Italian dog owners and 35.9% of cat owners rely on their veterinarians as their primary source for selecting pet food, underscoring the importance of veterinary-recommended therapeutic nutrition categories. For many chronic medical conditions, pet owners continue to use the recommended therapeutic diet for extended periods, supporting relatively stable repeat-purchase demand compared with conventional premium pet food categories. This dynamic reinforces the role of veterinary clinics and specialist practices, particularly in urban areas where chronic disease management and follow-up care are more developed. In May 2026, Monge & C. S.p.a. bolstered its presence in this channel with the introduction of VetSolution AN-HYDRO, supported by clinical trial research from the University of Teramo and digestibility scores reaching up to 99%, which strengthens clinician confidence in the product's therapeutic claims[1]Source: Monge and C. S.p.A., “Monge VetSolution AN-HYDRO: The Dietary Revolution in Veterinary Diets,” Monge, monge.it . Consequently, brands that maintain strong relationships with veterinarians are better positioned to sustain long-term demand in the Italy pet veterinary diets market compared to those relying solely on shelf visibility.

Chronic Pet Disease Burden in Aging Pets

The long-term growth of the Italy pet veterinary diets market is driven by the increasing prevalence of chronic diseases in aging pets. There is a rise in conditions such as diabetes, renal, urinary, and mobility-related disorders, which often necessitate nutritional support alongside clinical care. Chronic kidney disease is particularly significant in cats, affecting the majority of those aged 10 years or older, thereby sustaining demand for renal diets. The clinical benefits of phosphorus-restricted and metabolically tailored diets demonstrate extensive renal metabolic reprogramming in cats with spontaneous chronic kidney disease. This trend has commercial implications, as older pets increasingly transition from occasional specialty nutrition to routine therapeutic feeding. As this shift progresses, the Italy pet veterinary diets market is anticipated to continue attracting demand from pet owners managing conditions requiring prolonged treatment and high compliance.

Premiumization of Condition-Specific Nutrition

Premiumization in the Italy pet veterinary diets market is primarily driven by clinical trust rather than brand image. Pet owners are increasingly willing to pay for products that offer clear health benefits and are supported by veterinary recommendations. Despite economic challenges, Italy's pet food and pet care market reached EUR 5.3 billion (USD 5.7 billion) in 2025, with specialist nutrition accounting for more value than volume. Farmina Pet Food's Genius AI platform, which won the Pet Care Innovation of the Year Award in 2025, reflects the growing role of digital tools in providing personalized nutritional guidance to pet owners and supporting informed feeding decisions alongside veterinary consultation. This trend strengthens the premium segment of the Italy pet veterinary diets market, as targeted nutrition is increasingly seen as a key component of responsible pet health management. Additionally, it reduces the emphasis on price comparison, making outcome-focused products more resilient compared to standard maintenance diets.

E-Commerce Refill Convenience and Adherence

E-commerce is enhancing efficiency in the Italy pet veterinary diets market following the issuance of the initial prescription. Purina expanded its health-focused nutrition offerings through online and pet specialty channels in 2026, highlighting the growing importance of digital platforms for specialized feeding[2]Source: Purina PetCare, “Purina Pro Plan Veterinary Diets Now Available on Amazon,” Purina, purina.com . This is significant because many products in the Italy pet veterinary diets market require continuous feeding over extended periods. Subscription tools and scheduled reorder systems help minimize the risk of interruptions during the refill cycle. Additionally, online access enables households in remote areas to maintain consistent treatment. Over time, this improves adherence and reduces the market's reliance on the physical availability of specialist retail outlets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-Led Down-Trading to General Maintenance Food | -1.2% | National, more pronounced in southern Italy and lower-income households | Short term (≤ 2 years) |

| Limited Veterinary Access in Rural and Southern Italy | -0.8% | Southern Italy and rural regions | Medium term (2-4 years) |

| Ingredient and Label Compliance Costs | -0.7% | National, EU-wide | Medium term (2-4 years) |

| Custom Compounding as a Substitute in Urban Areas | -0.5% | Urban centers, including Milan, Rome, and Florence | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Inflation-Led Down-Trading to General Maintenance Food

Inflation continues to be a significant constraint on the volume growth of the Italy pet veterinary diets market. Therapeutic diets cost more than standard pet food, creating financial pressure for households managing recurring monthly expenses for chronic pet conditions. Despite these challenges, Italy's broader pet food and pet care market grew to EUR 5.3 billion (USD 5.7 billion) by 2025. However, this growth has occurred during a period of sustained economic pressure, which has not impacted all households equally. In the Italy pet veterinary diets market, down-trading does not necessarily indicate a complete withdrawal. Some pet owners retain one essential product while eliminating supplementary or secondary therapeutic items from their regimen. This behavior reduces revenue per treated pet and slows the adoption of premium products. It also limits the pace at which advanced formulations can expand beyond higher-income households.

Limited Veterinary Access in Rural and Southern Italy

Limited access to veterinary services constrains the growth potential of the Italy pet veterinary diets market. This market segment typically begins with a diagnosis, and fewer veterinary consultations are associated with lower adoption of therapeutic feeding plans. A persistent north-south disparity in veterinary infrastructure, premium retail availability, and disposable income leaves southern and rural Italy underserved compared to northern urban centers. Pet owners in these underserved areas are anticipated to continue using general maintenance food, even when therapeutic diets would be more suitable. The market experiences faster growth in regions where veterinary clinics, specialty stores, and higher spending power are concentrated. While online ordering facilitates access to therapeutic diets after diagnosis, it does not address the lack of initial clinical assessments. Without improved access to veterinary services, regional demand will remain partially untapped, leading to uneven growth across the country throughout the forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Digestive Sensitivity Leads Growth Across Therapeutic Conditions

Diabetes represents the largest individual therapeutic diet category with a market share of 19.2% in the Italy pet veterinary diets market in 2025. At VMX 2026, Royal Canin previewed a new therapeutic formulation for overweight diabetic cats, highlighting the link between diabetes management and safe weight reduction. Renal diets remain the second-largest sub-product category, as chronic kidney disease affects over 30% of cats aged 10 years or older. Dechra's January 2026 European launch of SPECIFIC Kidney Support Hydrolyzed reflects continued investment in this area. Other therapeutic diets, including those for urinary tract disease, obesity, dermatological conditions, oral care, and related indications, complete the product portfolio. These offerings reflect the Italy pet veterinary diets market's focus on long-term, indication-specific feeding rather than discretionary premium purchases.

Digestive sensitivity is the fastest-growing product in the Italy pet veterinary diets market, with the segment projected to grow at a 10.0% CAGR from 2026 to 2031. This growth reflects increased awareness of food-responsive digestive disorders and the introduction of clinically focused products that extend beyond general wellness claims. In February 2025, Virbac launched Veterinary HPM Digestive Support wet diets for both dogs and cats, using species-specific nutritional designs rather than a generalized approach[3]Source: Virbac S.A., “Virbac Veterinary HPM Digestive Support Wet Diets Launch,” Virbac, virbac.com .This development highlights the shift in digestive care within the Italy pet veterinary diets market toward microbiome-focused and clinically validated solutions.

By Pets: Dogs Drive Prescribed Volume, Cats Sustain Renal and Urinary Segments

Dogs represent the largest pet segment in the Italy pet veterinary diets market, accounting for a 56% market share in 2025. This dominance is driven by higher therapeutic spending per dog, extended treatment protocols for conditions such as obesity and digestive care, and stronger owner adherence to structured feeding plans. In March 2026, Royal Canin strengthened its focus on canine therapeutic diets by renewing its partnership with the University of Tennessee Veterinary Obesity Center, aligning product development with chronic condition research to provide improved products globally, including Italy.

Dogs are also the fastest-growing segment in the Italy pet veterinary diets market, with a projected compound annual growth rate (CAGR) of 6.8% from 2026 to 2031. This growth is supported by an increasing prevalence of lifestyle-related conditions such as diabetes, digestive sensitivity, and obesity-related complications, coupled with rising owner commitment to long-term prescribed feeding plans. Meanwhile, cats remain the primary segment for renal and urinary therapeutic demand due to the prevalence of chronic kidney disease and feline lower urinary tract disorders in older cats, which often require extended nutritional management. This gives cats a stable and high-value role in the market, even though they do not lead in total therapeutic revenue. Other pets continue to play a marginal role in the Italy pet veterinary diets market due to limited prescription formats and less structured purchasing behavior.

By Distribution Channel: Supermarkets Leads Volume, Online Channel helps in Growth of Therapeutic Diets

Supermarkets/Hypermarkets accounted for 30.6% of the Italy pet veterinary diets market share in 2025, making them the largest distribution channel. This dominance is attributed to routine household traffic, extensive brand visibility, and efforts by major suppliers to expand specialist shelf space near mainstream pet food. However, purchasing behavior in these outlets is primarily driven by diagnosis and refill needs rather than impulse buying. This results in more stable therapeutic demand compared to standard packaged pet food. Specialty stores also play a significant role, as they provide a better advisory environment for explaining prescribed nutrition choices. Physical retail continues to represent a substantial portion of the Italy pet veterinary diets market, though different channels serve the category in varying ways.

The online channel is the fastest-growing segment in the Italy pet veterinary diets market, projected to grow at a 6.5% CAGR from 2026 to 2031. Since prescribed diets often remain unchanged for extended periods, digital replenishment is particularly effective and fosters stronger customer retention compared to pet food. For instance, Dechra’s March 2025 launch of SPECIFIC in Italy began with a clinic-first rollout before expanding to broader distribution channels, highlighting the importance of veterinary credibility in building trust before scaling. Convenience stores and smaller outlets play a limited role, primarily serving as top-up options, as prescription-led nutrition requires a broader range and more specialized guidance than these formats typically offer.

Geography Analysis

Northern Italy accounts for the largest share of demand in the Italy pet veterinary diets market, driven by regions such as Lombardy, Emilia-Romagna, and Veneto. This area benefits from higher disposable incomes, a denser network of specialist veterinarians, and a well-developed specialty retail infrastructure. In May 2024, Mars, Incorporated enhanced its presence by opening the first One Mars, Incorporated's Office in Milan, integrating Royal Canin and AniCura operations to support a more cohesive pet care model in Italy's most affluent pet market.

Central Italy represents the second-largest geographic segment in the Italy pet veterinary diets market, with Rome and the Tuscany corridor serving as key demand centers. Rome's large urban pet-owning population and growing specialty retail presence drive demand, while Tuscany demonstrates a preference for premium, functional products, favoring brands with health-focused credentials and Italian production. Monge & C. S.p.a.'s participation in the World Dog Show in Bologna and its nutrition-focused professional outreach in 2026 highlight ongoing efforts to build awareness through veterinarian-focused channels in central-northern Italy. Although specialist density is lower than in Milan or Bologna, the region continues to generate steady demand due to favorable awareness and purchasing power.

Southern Italy and the islands face significant constraints in the Italy pet veterinary diets market. Regions such as Campania, Sicily, Calabria, and Sardinia have notably lower densities of specialist veterinarians, which limits the initiation of prescriptions. The adoption gap in these areas is more closely linked to healthcare access challenges rather than a lack of owner interest in pet health products. Epidemiological reporting from April 2025 highlighted ongoing disparities in healthcare surveillance across central-southern and insular regions, emphasizing this structural issue. However, in the short term, advantages in distribution and diagnosis continue to concentrate most market value in northern and central Italy.

Competitive Landscape

The Italian pet veterinary diets market is moderately concentrated in 2025, with the top five players being Nestle S.A. (Purina), Mars, Incorporated, Farmina Pet Food, Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), and Monge. Nestle S.A., through Purina PetCare, and Mars, Incorporated, through Royal Canin, maintain strong global positions due to their established veterinary science infrastructure and robust relationships with clinicians. Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)’s Prescription Diet secures a competitive position by emphasizing prescription-focused products and maintaining clear channel separation from general over-the-counter nutrition. Farmina Pet Food, Monge & C.s.p.a., and Almo Nature are significant domestic competitors, leveraging local brand recognition, regional supply chain advantages, and connections with professional communities. This competitive landscape fosters innovation while favoring companies that can support strong clinical claims and ensure reliable product availability.

Strategic developments in 2026 highlight the evolving competition within the Italy pet veterinary diets market. Colgate-Palmolive Company (Hill's Pet Nutrition Inc.) introduced k/d + Derm Complete and k/d + z/d Hydrolyzed in June 2026, advancing a multi-condition nutrition model for pets with overlapping renal, dermatological, and gastrointestinal needs. The Purina Institute published research on microbiome and antimicrobial stewardship in May 2026, reinforcing Nestle S.A. (Purina)’s focus on clinical credibility rather than solely relying on brand scale. These initiatives demonstrate that leading companies are prioritizing scientific advancements, broadening indications, and strengthening clinician engagement over mere shelf presence.

Supply-side dynamics are also shaping the Italy pet veterinary diets market, particularly for formulations that incorporate vitamins, omega-3 fatty acids, and microbiome-supporting ingredients. Italy-based manufacturers are strengthening their competitive position through clinical collaborations and the international expansion of their therapeutic nutrition portfolios. Opportunities remain in the mid-market segment between premium global brands and private-label alternatives, particularly for manufacturers that can combine regulatory compliance, scientific evidence, and competitive pricing for long-term therapeutic use.

Italy Pet Veterinary Diets Industry Leaders

Mars Incorporated

Nestle S.A. (Purina)

Farmina Pet Food

Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

Monge & C.s.p.a.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Colgate-Palmolive Company (Hill's Pet Nutrition Inc.) launched Prescription Diet k/d + Derm Complete and k/d + z/d Hydrolyzed, the first dual-indication therapeutic dry food products in its European portfolio, including Italy. These products address simultaneous renal phosphorus restriction and hydrolyzed protein management for dermatological or GI conditions, reflecting a clinical trend toward nutrition for comorbidities in aging cats.

- May 2026: Monge and C.s.p.a. launched VetSolution AN-HYDRO, combining a single protein source with XOS prebiotics, live Limosilactobacillus reuteri, and inactivated postbiotics, validated through clinical trials at the University of Teramo with digestibility scores of up to 99% and a probiotic viability shelf life of 18 months.

- January 2026: Dechra Pharmaceuticals PLC launched SPECIFIC Kidney Support Hydrolysed (FKD-HY and CKD-HY) therapeutic diets across Europe, including Italy, addressing the hydrolyzed-protein sub-segment of renal nutrition.

Italy Pet Veterinary Diets Market Report Scope

Pet veterinary diets (also known as therapeutic or prescription diets) are specialized, scientifically formulated pet foods designed to treat, prevent, or manage specific medical conditions.

The Italy Pet Veterinary Diets Market Report is segmented by sub product (Diabetes, Renal, Urinary Tract Disease, Digestive Sensitivity, Oral Care Diets, Derma Diets, Obesity Diets, and Others), by pets (Cats, Dogs, and Other Pets), and by distribution channel (Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets, and others). The market forecasts are provided in terms of value in USD and value in metric tons.

| Diabetes |

| Digestive Sensitivity |

| Oral Care Diets |

| Renal |

| Urinary Tract Disease |

| Obesity Diets |

| Derma Diets |

| Other Veterinary Diets |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| By Sub Product | Diabetes |

| Digestive Sensitivity | |

| Oral Care Diets | |

| Renal | |

| Urinary Tract Disease | |

| Obesity Diets | |

| Derma Diets | |

| Other Veterinary Diets | |

| By Pets | Cats |

| Dogs | |

| Other Pets | |

| By Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

Key Questions Answered in the Report

What is the 2026 to 2031 growth outlook for Italy pet veterinary diets?

The Italy pet veterinary diets market is forecast to rise from USD 560 million in 2026 to USD 750 million by 2031 at a 6.0% CAGR.

Which therapeutic category is expanding the fastest in Italy?

Digestive sensitivity is the fastest-growing sub product, with a projected 10.0% CAGR through 2031.

Which pet type generates the most therapeutic diet revenue in Italy?

Dogs are the largest segment, supported by higher spending per patient, longer feeding protocols, and stronger owner compliance.

Which sales channel leads and which one is growing fastest?

Supermarkets/Hypermarkets led with 30.6% of revenue in 2025, while the online channel is growing fastest at a 6.5% CAGR.

Page last updated on: