Italy Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

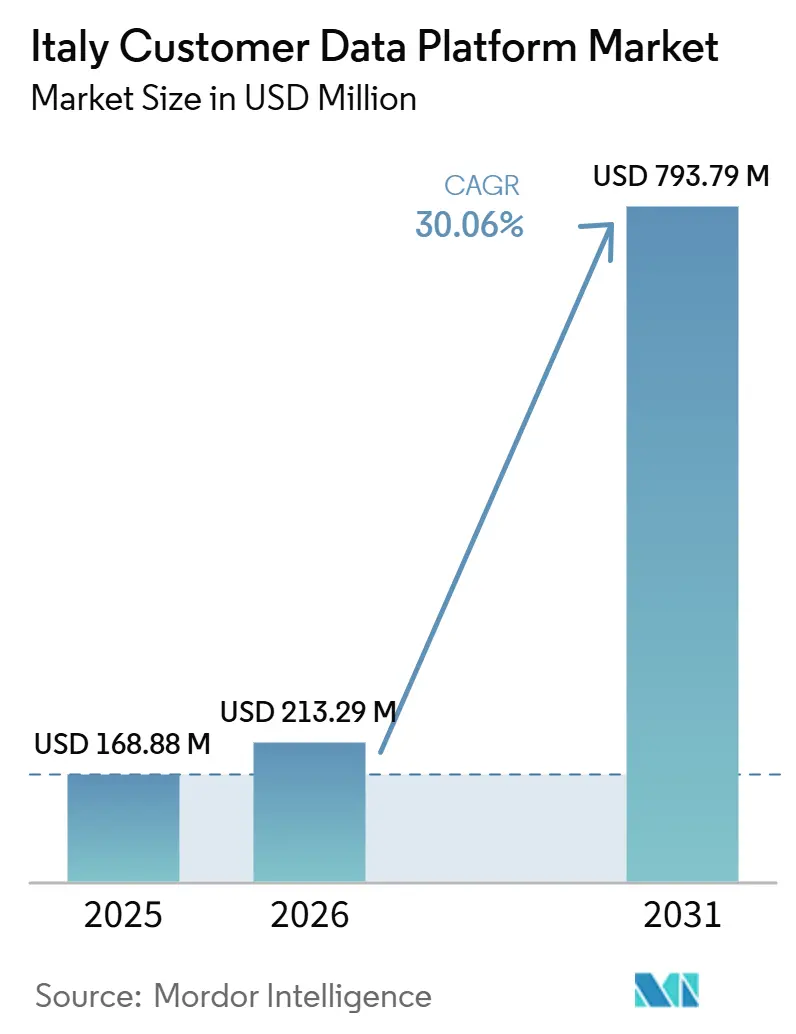

| Base Year Market Size (2025) | USD 168.88 Million |

| Market Size (2026) | USD 213.29 Million |

| Market Size (2031) | USD 793.79 Million |

| Growth Rate (2026 - 2031) | 30.06% CAGR |

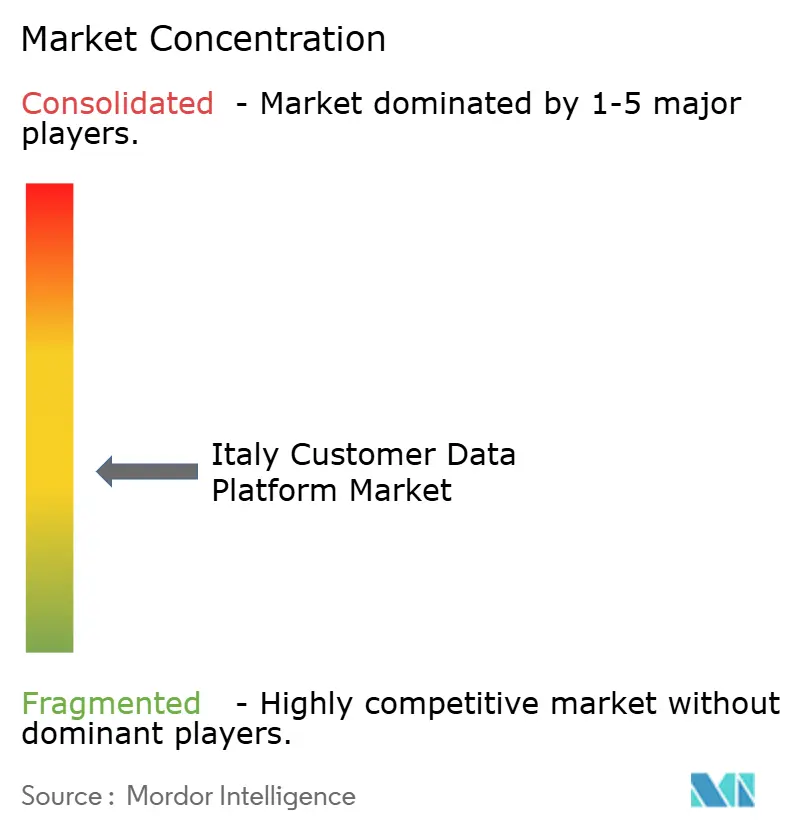

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Customer Data Platform Market Analysis by Mordor Intelligence

The Italy customer data platform market size was valued at USD 168.88 million in 2025 and is forecast to reach USD 793.79 million by 2031 at a CAGR of 30.06% from 2026 to 2031. The market is moving ahead of Italy’s broader digital expansion because customer data has become central to compliance, customer retention, and revenue execution across digital channels. Buyers are no longer treating these platforms as optional marketing systems, since the need to manage consent, unify identities, and activate first-party data is now tied to day-to-day operating requirements. Demand is also shifting toward platforms that can support real-time decisioning and stronger analytics, because unified data alone is becoming less valuable than the ability to act on it quickly. Competitive activity is therefore favoring vendors that combine strong platform depth with local delivery capacity, sector knowledge, and simpler deployment models for buyers with limited specialist resources. The clearest opening now lies in deployments that reduce implementation effort, connect fragmented systems, and help organizations move from isolated customer records to a usable cross-channel view.

Key Report Takeaways

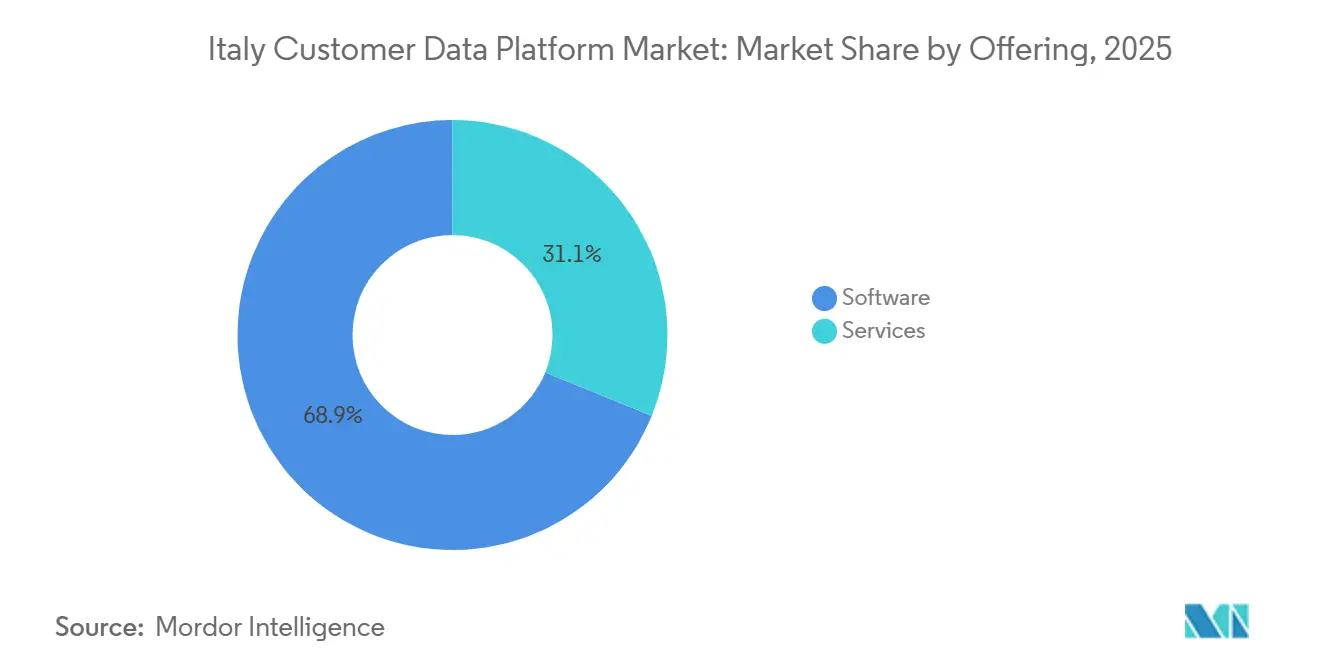

- By offering, software held 68.87% of the Italy customer data platform market share in 2025, while services are projected to expand at a 32.76% CAGR through 2031.

- By deployment mode, cloud accounted for 65.11% share in 2025 and is projected to remain the fastest-growing model at a 32.12% CAGR through 2031 in the Italy customer data platform market.

- By organization size, large enterprises held 70.24% of the Italy customer data platform market share in 2025, while small and medium enterprises are projected to expand at a 31.45% CAGR through 2031.

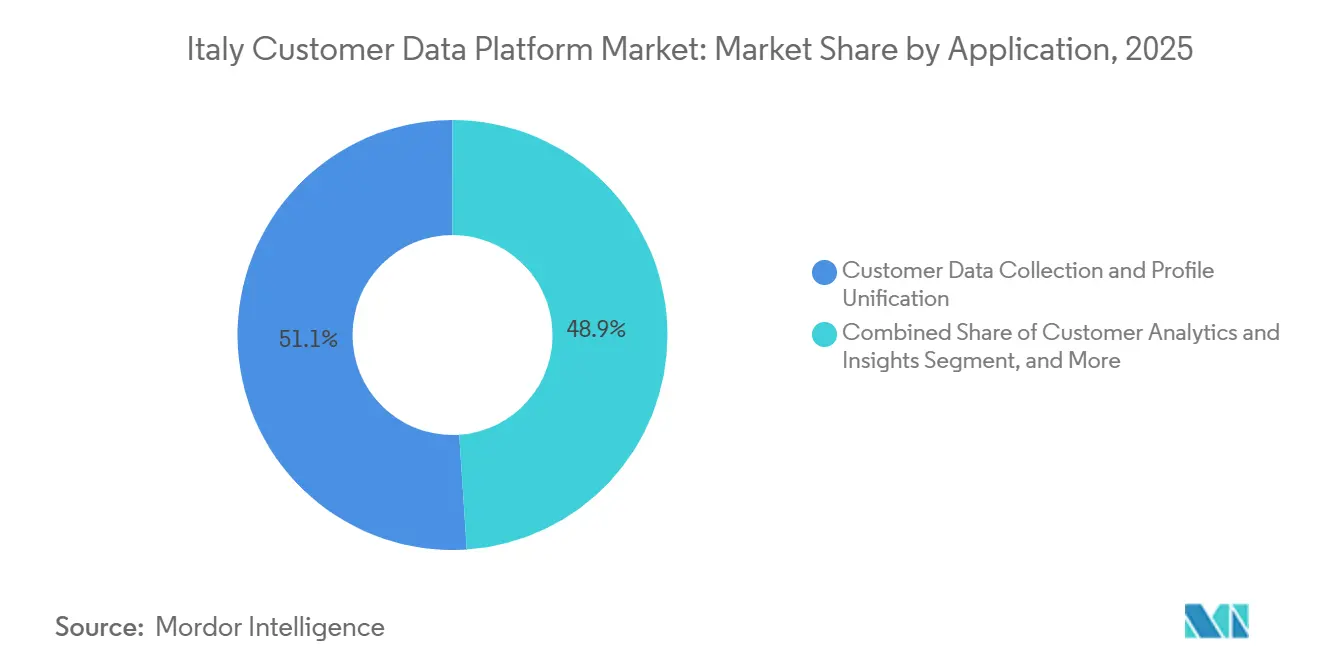

- By application, customer data collection and profile unification accounted for 51.06% of the Italy customer data platform market share in 2025, while customer analytics and insights are projected to grow at a 31.88% CAGR through 2031.

- By end-user industry, retail and e-commerce held 28.14% share in 2025, while BFSI is projected to record the highest CAGR at 31.56% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR-Driven First-Party Data Shift | +5.8% | National, with early gains in Milan and Rome enterprise clusters | Short term (≤ 2 years) |

| Customer Journey Unification Across Fragmented Channels | +4.9% | National, concentrated in retail and BFSI verticals | Medium term (2-4 years) |

| AI-Led Real-Time Personalization Demand | +5.2% | National, with tech-intensive sectors concentrated in North Italy | Medium term (2-4 years) |

| Cloud Migration of MarTech Stacks | +4.3% | National, accelerated by digital transformation programs across regions | Short term (≤ 2 years) |

| Retail Media and Commerce Activation Use Cases | +3.4% | National, with concentration in northern retail corridors and major digital marketplaces | Medium term (2-4 years) |

| Consent-Oriented Identity Resolution Demand | +2.8% | National, shaped by European privacy rules and local enforcement expectations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

GDPR-Driven First-Party Data Shift

The Italy customer data platform market is being shaped by a stronger preference for first-party data models, as organizations are under greater pressure to demonstrate that customer information is collected, governed, and activated in a controlled manner. Italy’s digital policy environment is becoming more structured through the national AI strategy for 2024-2026 and Law n. 132/2025, which adds weight to governance, auditability, and responsible data handling in customer-facing systems.[1]European Commission and Dipartimento per la Trasformazione Digitale, “Digital Decade 2026 Report, Italy,” European Commission This is changing how platforms are evaluated, since consent controls, data lineage, and traceable workflows now matter alongside campaign execution and analytics quality. Procurement is therefore moving beyond the marketing function, with IT, legal, and security teams becoming more active in platform selection when customer data flows across multiple channels and automated processes. The result is that the Italy customer data platform market is increasingly tied to compliance readiness, which gives an advantage to vendors that can support both activation and governance in the same environment.

Customer Journey Unification Across Fragmented Channels

The Italy customer data platform market is also gaining momentum because consumer journeys span multiple touchpoints, while many organizations still manage disconnected systems for commerce, loyalty, service, and CRM. In 2026, Italy’s online consumers consulted an average of 4 touchpoints before completing a purchase, underscoring fragmented identity and event data as a direct barrier to conversion and retention. Once this fragmentation begins to affect both acquisition efficiency and service quality, profile unification becomes a core business requirement rather than a technical enhancement. The same pattern is visible in large enterprise deployments, where unified profiles support more consistent cross-sell activity, better service continuity, and stronger orchestration across digital and assisted channels. This is why the Italy customer data platform market is drawing budget from broader customer experience programs, not only from traditional campaign technology lines.

AI-Led Real-Time Personalization Demand

The Italy customer data platform market is moving toward platforms that do more than store and organize data, because buyers increasingly want immediate analysis, prediction, and action. Around 50% of Italian financial institutions were already using traditional AI in marketing and customer-facing functions in early 2026, indicating that the shift toward data-driven personalization is underway among one of the country’s most important buyer groups. Crédit Agricole Italia reported a 25% increase in overall engagement, a 20% lift in cross-sell campaign effectiveness, a 15% decrease in churn, and a 30% improvement in team productivity after deploying Adobe Experience Platform, demonstrating how quickly a unified data environment can deliver measurable operating gains. As more buyers seek real-time inference and next-best-action capabilities, platforms without embedded intelligence are more likely to be treated as support layers for external tools rather than as primary decision systems. This keeps the Italy customer data platform market focused on vendors that can demonstrate execution results in regulated, high-volume environments, rather than on generic claims of AI readiness.

Cloud Migration of MarTech Stacks

Cloud adoption remains a strong growth force for the Italy customer data platform market, because flexible deployment is becoming easier to justify than building new customer infrastructure around older fixed environments. Italy’s digital economy reached EUR 84.4 billion (USD 91.2 billion) in 2025, up 3.4%, with cloud among the main areas supporting that growth. The logic behind this shift is practical: cloud-based customer data layers are easier to scale across channels and to connect with commerce, analytics, service, and personalization tools. At the same time, buyers in regulated fields are not moving uniformly, which is why hybrid approaches remain relevant when sensitive data and activation workflows are separated across environments. Even so, the broader direction still favors cloud-led deployment, keeping the Italy customer data platform market aligned with organizations that want faster activation without waiting for full legacy replacement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy CRM and Data Warehouse Lock-In | -2.5% | National, most acute in large enterprises and BFSI | Medium term (2-4 years) |

| Shortage of CDP Integration Talent | -2.1% | National, most severe outside Milan and Rome metropolitan areas | Long term (≥ 4 years) |

| Privacy Risk and Consent Governance Complexity | -1.7% | National, most visible in regulated customer-facing sectors | Short term (≤ 2 years) |

| Attribution Uncertainty Across Walled Gardens | -1.3% | National, concentrated in performance marketing-heavy retail and media sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy CRM and Data Warehouse Lock-In

The Italy customer data platform market still faces slow decision cycles in organizations where customer information is tied to older CRM systems, data warehouses, and custom interfaces that were not designed for real-time activation. In the Italian finance sector, 55% of institutions still relied on on-premises architectures for core systems, and more than 60% cited technical debt as a major barrier to cloud migration. That creates a clear mismatch, because many of the buyers with the richest customer records also face the longest and most complex implementation paths. Platform selection, therefore, depends as much on connector depth and migration practicality as it does on feature strength, especially when legacy estates need to remain active during phased deployment. This slows the Italy customer data platform market where the value case is strong but the operating environment still resists fast change.

Shortage of CDP Integration Talent

The Italy customer data platform market is also held back by a shortage of teams capable of configuring identity logic, event pipelines, consent frameworks, and cross-system orchestration without heavy external support. This affects small and mid-sized buyers most directly, because they often need the same governance and integration outcomes as larger enterprises but have fewer internal specialists to manage deployment and maintenance. The challenge is more visible outside the main metropolitan centers, where digital demand is rising but access to experienced delivery talent remains thinner than in Milan or Rome. That is one reason services are growing faster than software, and it also explains why low-code configuration and AI-assisted setup are becoming more important in vendor positioning. The Italy customer data platform market therefore rewards platforms that reduce operational dependence on scarce specialist labor, since complexity itself can delay adoption even when budget intent is present.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Rising Services Demand Reflects Ongoing Implementation Gaps

Software held 68.87% of the Italy customer data platform market share in 2025, which kept core licensing, analytics modules, and platform subscriptions at the center of vendor revenue. This base shows that most organizations still begin their commitment with the platform layer itself before expanding into deeper operational support. It also gives larger vendors a stable foundation in enterprise accounts, where contract duration and platform standardization matter more than short-term price differences. In the Italy customer data platform market, software remains the anchor because buyers still need a single environment for identity, profile, and activation workflows.

Services are projected to grow at a 32.76% CAGR through 2031, making them the fastest-growing part of the offering mix. The Italy customer data platform industry is showing this pattern because implementation, governance design, training, and integration work continue well after the initial platform decision. Buyers often need help translating fragmented source systems into usable customer models, and that requirement stretches beyond technical setup into operating process design. The result is that vendors with strong partner networks, sector delivery depth, and managed support capability are better placed to expand account value over time.

By Deployment Mode: Cloud Leads While Hybrid Stays Relevant in Regulated Fields

Cloud accounted for 65.11% of the market in 2025 and is projected to expand at a 32.12% CAGR through 2031, giving it both the largest installed base and the fastest growth rate. This pairing matters because it shows that the preferred deployment model is not only established but still gaining momentum. In the Italy customer data platform market, cloud appeals to organizations that want easier scalability, faster rollout across channels, and better alignment with modern analytics and personalization tools. It also reduces the need to build new activation capability around fixed internal infrastructure.

Hybrid still holds an important place, especially in banking and insurance, where sensitive data handling and existing operational structures continue to shape deployment choices. Many financial institutions in Italy still run core environments on-premises and identify technical debt as a significant obstacle to migration, underscoring the continued relevance of mixed architectures. That means the Italy customer data platform market is not moving through a simple replacement cycle, since many buyers are connecting cloud activation to older system estates rather than removing those estates immediately. Vendors that support phased deployment and strong interoperability are therefore more likely to succeed than those that assume full migration at the start.

By Organization Size: SME Adoption is Broadening the Buyer Base

Large enterprises held 70.24% of the market in 2025, which reflects the long-standing presence of major banks, telcos, and retail chains in customer data infrastructure programs. These organizations usually have the data volume, budget scale, and cross-channel complexity that make customer data platforms a practical enterprise requirement. Their early lead also means the Italy customer data platform market has been shaped first by buyers that can sustain multi-year platform and services spending. This keeps enterprise-grade governance, security, and integration depth central to vendor competition.

Small and medium enterprises are projected to grow at a 31.45% CAGR through 2031, suggesting a wider addressable base rather than a shift away from enterprise demand. That growth matters because it expands the Italy customer data platform market into organizations that need more practical deployment models, lower operating burden, and clearer time-to-value. Adoption is unlikely to be uniform across the country, since digital maturity varies by region and by sector, with stronger momentum typically concentrated in more digitally advanced northern clusters. Vendors that simplify onboarding and reduce dependence on specialist teams are, therefore, better placed to capture this next layer of demand.

By Application: Data Unification Anchors Spend While Analytics Gains Speed

Customer data collection and profile unification accounted for 51.06% of the market in 2025, confirming that most buyers still begin with the basic need to consolidate records, identifiers, and behavioral signals into a single usable structure. This is the enabling layer behind nearly every later use case, including personalization, segmentation, journey coordination, and consent tracking. In the Italy customer data platform market, investment continues to center on this foundation because organizations cannot scale cross-channel actions while customer data remains split across systems. The persistence of this lead also shows that many deployments are still solving core data readiness before moving deeper into intelligence-led activation.

Customer analytics and insights in the Italy customer data platform market are projected to expand at a 31.88% CAGR through 2031, making this the fastest-growing application area. The shift reflects demand for predictive modeling, churn detection, and better decision support, especially in sectors where customer timing and relevance directly affect conversion and retention. Around 50% of Italian financial institutions were already using traditional AI in marketing and customer-facing functions in 2026, which supports the move toward analytics-led deployment priorities. Platforms that can connect unified profiles to explainable analysis are therefore better aligned with how application demand is evolving across the Italy customer data platform market.

By End-User Industry: Retail and E-Commerce Lead While BFSI Sets the Pace

Retail and e-commerce accounted for 28.14% of the Italy customer data platform market in 2025, making it the largest end-user segment. Italy’s B2C e-commerce value exceeded EUR 66.6 billion (USD 75.1 billion) in 2026, and the country had 35 million digital consumers, underscoring the scale of customer data activity through commerce channels. This gives retailers a clear reason to invest in better identity continuity, more relevant offers, and stronger measurement across browsing, purchase, and service interactions. In the Italy customer data platform market, retail remains the volume anchor because customer data is directly linked to both demand generation and repeat purchase performance.

BFSI is projected to grow at a 31.56% CAGR through 2031, making it the fastest-expanding end-user group. In Italy, 65% of financial institutions treated IT as a structural strategy lever in 2026, and many were prioritizing omnichannel customer journeys and personalization more directly than before. Crédit Agricole Italia’s Adobe deployment improved engagement, cross-sell effectiveness, churn outcomes, and team productivity, which shows why the banking use case is moving beyond data storage toward measurable operating value.[2]Adobe, “Crédit Agricole Italia Transforms Customer Experiences with Adobe,” Adobe Business This makes BFSI one of the most important growth engines in the Italy customer data platform market, even though retail still contributes the largest current share.

Geography Analysis

The Italy customer data platform market was valued at USD 168.88 million in 2025 and is projected to reach USD 793.79 million by 2031, indicating that all geographic demand in this report is concentrated within a single national market. Italy’s digital economy reached EUR 84.4 billion (USD 91.2 billion) in 2025, up 3.4%, providing the broader digital context for customer data platform adoption. Within that setting, the Italy customer data platform market is not evenly distributed, because the strongest enterprise demand is concentrated in northern metropolitan clusters with deeper financial, retail, manufacturing, and technology activity. Milan remains especially important because large vendors, service partners, and enterprise buyers are more densely concentrated there than in most other parts of the country. Salesforce’s June 2026 decision to commit USD 1 billion over five years to Italy, including a new Milan office and added hiring in data science and agentic AI, reinforces that location advantage and strengthens Milan’s role as a focal point for enterprise platform investment.

The Italy customer data platform market is also shaped by sector concentration, since BFSI and large retail organizations are clustered most heavily around Milan, Rome, and Turin. That matters because the buyer groups with the largest data estates and the highest customer interaction volumes are also the ones most likely to push more advanced platform adoption. The geography is therefore less about national spread and more about where digitally mature demand already exists, which keeps the near-term revenue base concentrated in a relatively small number of urban enterprise hubs. At the same time, the country’s broader digital agenda is creating conditions for later expansion outside those core centers. Italia Digitale 2026 continues to support citizen-facing digital services and broader digital transformation, helping build process discipline and data awareness that can support future customer data platform demand in less mature areas.

This means the Italy customer data platform market has a clear internal imbalance, with stronger short-term commercialization in the north and a longer runway in central and southern regions. The national AI strategy for 2024-2026 and Law n. 132/2025 place customer data governance within a broader modernization effort that supports more consistent enterprise attention to controlled data use and automated decision-making processes. Compared with larger European markets, where deployment is already more mature, Italy still looks like a catch-up market with strong regulatory and operational reasons to accelerate. That combination keeps the Italy customer data platform market concentrated in a few leading business corridors today, while still leaving room for broader regional diffusion over the forecast period.

Competitive Landscape

The Italy customer data platform market is moderately consolidated in the enterprise tier, where global platforms such as Salesforce, Adobe, Oracle, SAP, and Tealium compete for large multi-year contracts, while smaller European and specialized vendors remain active in mid-market and SME opportunities. The structure is not fully concentrated, as vendor choice still depends on deployment model, regulatory comfort, sector specialization, and partner delivery capacity rather than on a single dominant supplier. In practical terms, the Italy customer data platform market rewards vendors that can combine platform depth with local execution and simpler adoption paths for buyers managing fragmented system estates. This is one reason the competitive field still includes both large software platforms and more focused players that emphasize identity resolution, interoperability, or sovereignty positioning. The result is a market where leadership is visible at the top end, but substitution and competition remain active across a broad middle layer.

Salesforce’s USD 1 billion five-year investment in Italy is one of the clearest strategic moves in the current period, because it strengthens local presence while also signaling a long-term commitment to enterprise AI and data workloads in the country.[3]Salesforce, “Salesforce Announces USD 1 Billion Investment in Italy to Accelerate Agentic AI,” Salesforce Newsroom Zeotap’s work with Sky Italia shows a different strategic route, where European data governance credentials and real-time personalization capability are used to compete against larger global platforms on a more focused value proposition. Treasure Data’s April 2026 rebrand to Treasure AI signals another important shift, as it frames competitive value around an ongoing AI-led operation rather than data storage alone. Amperity also moved further into governed AI activation through its Customer Data Agent and the Spring 2026 release, suggesting that real-time customer context is becoming a central battleground for platform differentiation.

The Italy customer data platform market is therefore moving toward competition based less on raw data ingestion and more on activation quality, intelligence, and operational ease. Buyers increasingly want proof that a vendor can help them connect data, reduce manual effort, and support compliant personalization across channels without adding excessive system burden. That favors platforms that can demonstrate operational enterprise deployments in Italy or comparable regulated European markets, rather than relying solely on broad global messaging. It also supports a continued role for challengers that can serve mid-sized Italian organizations with lower delivery complexity and stronger local fit, even while the largest enterprise contracts remain concentrated among a smaller group of global players.

Italy Customer Data Platform Industry Leaders

Twilio Inc.

Adobe Inc.

Salesforce, Inc.

Oracle Corporation

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Tealium launched the Context API, a real-time context layer uniting data-cloud depth with live customer behavioral signals for AI agents, enterprise applications, and CDP activation. The product extends Tealium's Moments API and serves the platform's 850+ global enterprise customers.

- June 2026: Salesforce announced a USD 1 billion five-year investment in Italy, including a new Milan office at Palazzo Missori, expanded hiring in data science and agentic AI, and the launch of the Enterprise Architecture Academy targeting more than 70 initial participants across enterprise and public sector organizations.

- June 2026: BlueConic acquired Blueshift, an AI-powered cross-channel marketing and decisioning platform, closing the gap between real-time customer context and multi-channel execution, email, push, in-app, SMS, and web. The combined platform serves more than 600 customers across consumer packaged goods, retail, direct-to-consumer, and travel and hospitality verticals.

- May 2026: Amperity launched its Spring 2026 release, addressing the "Customer Decision Gap," including the Amperity Model Context Protocol Server connecting AI tools, Microsoft Copilot, Braze AI, and Salesforce AgentForce, to a governed customer context layer without custom integration pipelines.

Italy Customer Data Platform Market Report Scope

The Italy Customer Data Platform Market comprises technology solutions that consolidate customer data from various digital and physical channels into unified customer profiles for analytics and engagement. These platforms enable organizations to improve audience targeting, customer insights, marketing automation, and privacy-compliant customer data management. Increasing adoption of data-driven marketing, omnichannel customer engagement strategies, and regulatory requirements related to data privacy drive the market. CDPs help businesses enhance customer experiences and maximize the value of customer data assets.

The Italy Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), and End-User Industry (Retail and E-Commerce, Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, Information Technology and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) | |

| Healthcare and Life Sciences | |

| Information Technology and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

How large is the Italy customer data platform market and what is the growth outlook?

The Italy customer data platform market was valued at USD 168.88 million in 2025 and is forecast to reach USD 793.79 million by 2031 at a 30.06% CAGR.

Which offering category leads demand in Italy?

Software led with 68.87% share in 2025, showing that most buyers still begin with the core platform, while services are growing faster at 32.76% CAGR through 2031.

Why are cloud deployments gaining so much traction?

Cloud held 65.11% share in 2025 and is also the fastest-growing deployment mode at 32.12% CAGR, because buyers want scalable activation and easier integration with modern customer systems.

Which application area is growing fastest in Italy customer data platforms?

Customer analytics and insights are projected to grow at 31.88% CAGR through 2031, while customer data collection and profile unification remained the largest application area in 2025 at 51.06%.

Which end-user group is creating the strongest demand?

Retail and e-commerce held the largest share at 28.14% in 2025, while BFSI is projected to grow fastest at 31.56% CAGR through 2031.

What is shaping vendor competition in Italy right now?

Competition is moving toward AI-enabled activation, stronger governance, and lower implementation burden, with moves such as Salesforce’s USD 1 billion Italy investment and Treasure Data’s shift to Treasure AI highlighting that direction.

Page last updated on: