Italy Automotive Reed Sensors/Switches Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 8.45 Million |

| Market Size (2026) | USD 8.97 Million |

| Market Size (2031) | USD 12.11 Million |

| Growth Rate (2026 - 2031) | 6.19% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Italy Automotive Reed Sensors/Switches Market Analysis by Mordor Intelligence

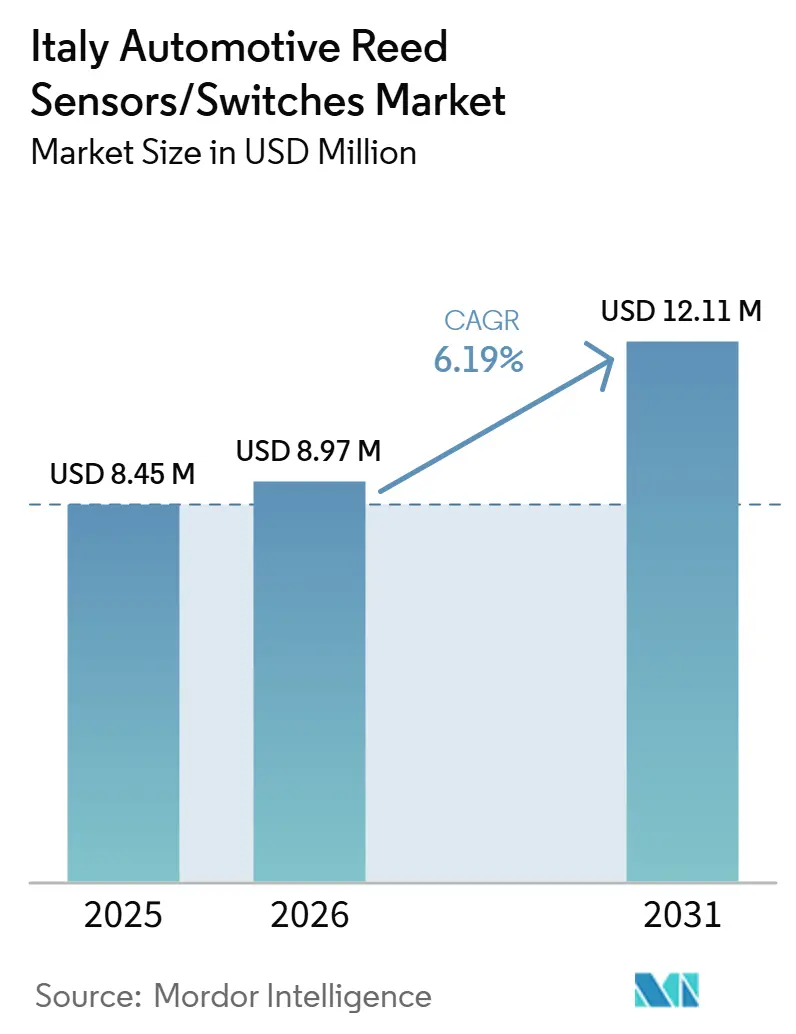

The Italian Automotive Reed Sensors/Switches Market size was valued at USD 8.45 million in 2025, USD 8.97 million in 2026, and is estimated to reach USD 12.11 million by 2031, at a CAGR of 6.19% during the forecast period (2026-2031). Italy’s automotive reed sensors and switches market is supported by two demand drivers operating in parallel. The first is a large and aging vehicle parc, which sustains steady replacement demand for position and proximity sensing in body-electronics applications such as closures, latches, access modules, and position-detection functions. These use cases are present across a large share of the in-use fleet, supporting recurring aftermarket consumption even during periods of muted new-vehicle production.

The second driver is the gradual strengthening of Italy’s electrification ecosystem, encompassing both vehicles and charging infrastructure. Public charging deployment has expanded steadily, with the installed base of charging points increasing materially over the past year and high-power charging accounting for a growing share of additions. On the vehicle side, the battery electric vehicle parc continues to expand, and BEV registrations are rising year-on-year from a low base. Together, these trends increase the number of battery- and charging-related sensing nodes, including charge-port detection, access-panel monitoring, and high-voltage safety interlock functions, supporting incremental demand for reed sensors and switches.

In contrast, Italy’s domestic automotive production remains weak, which constrains locally manufactured OEM module volumes. Passenger car and total motor vehicle output declined sharply year-on-year in 2025, limiting factory-fit demand for Italy-assembled platforms. As a result, the market structure increasingly reflects reliance on imported vehicles and cross-border OEM programs to meet factory-fit demand, while aftermarket replacement remains structurally important for body-electronics sensing applications linked to the aging vehicle fleet[1]"Ecobonus – Mobilità sostenibile," Ministry of Enterprises and Made in Italy (MIMIT), mimit.gov.it..

Key Report Takeaways

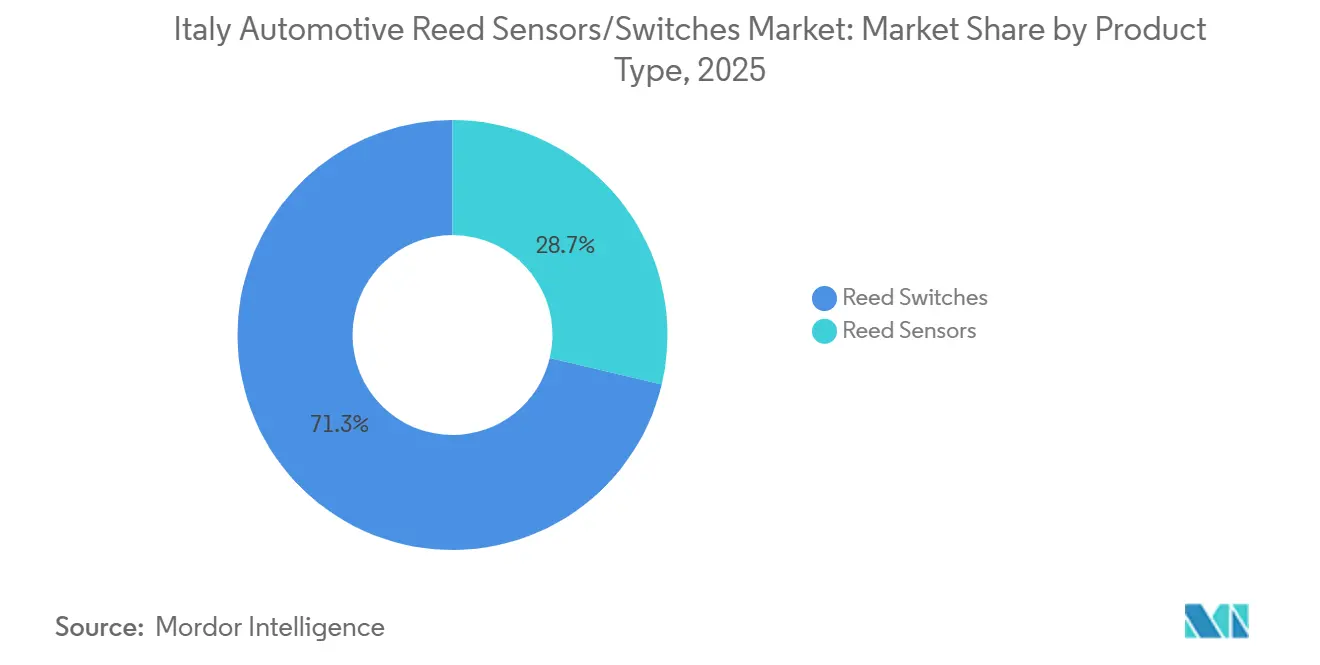

- By product type, reed switches represented the largest product type in 2025 with a market share of 71.25%, while reed sensors are projected to be the fastest-growing segment during 2026–2031, registering a CAGR of 7.48%.

- By application, body electronics accounted for the largest application segment in 2025 at 48.17%, whereas battery and charging systems are expected to record the highest growth rate over the forecast period, with a CAGR of 10.68%.

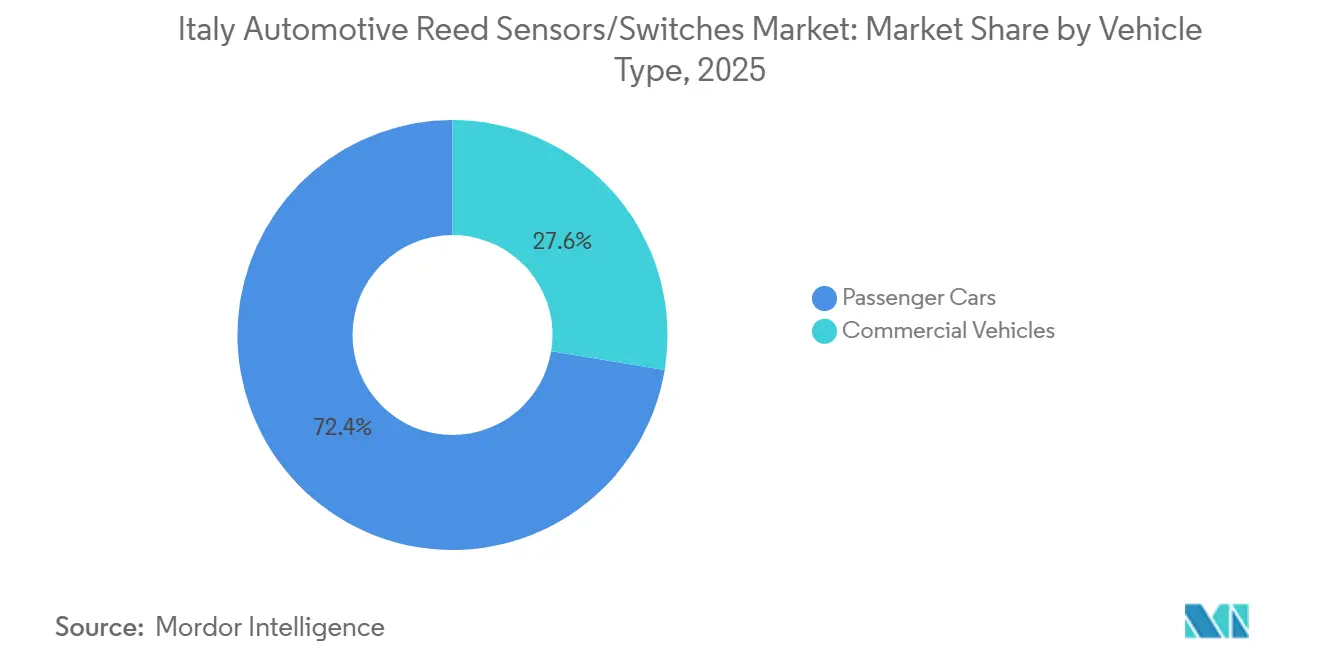

- By vehicle type, passenger cars dominated the market in 2025 with a share of 72.35% and are also projected to remain the fastest-growing vehicle type, expanding at a CAGR of 6.38% during 2026–2031.

- By sales channel, OEMs constituted the largest sales channel in 2025 with 77.54%, while the aftermarket is expected to grow slightly faster over the forecast period, registering a CAGR of 6.78%.

- By propulsion type, internal combustion engine vehicles formed the largest propulsion segment in 2025 with a market share of 61.35%, while battery electric vehicles are projected to be the fastest-growing propulsion type, recording a CAGR of 12.18% during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Automotive Reed Sensors/Switches Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-Power Charging Expansion | +1.2% | Higher impact in metro regions and highway corridors | Medium term (2-4 years) |

| Rising BEV Parc And Share | +1.0% | National; strongest in high-adoption regions | Medium term (2-4 years) |

| BEV Incentives And Fleet Renewal | +0.9% | National (scheme design influences uptake) | Short term (≤ 2 years) |

| Large Installed Vehicle Base | +0.6% | Broad-based; higher in older parc regions | Long term (≥ 4 years) |

| OEM/Tier Module Electrification | +0.5% | National; strongest where OEM/Tier activity is concentrated | Medium term (2-4 years) |

| Miniaturized Sensing Integration | +0.4% | OEM/Tier programs across Italy/EU platforms | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Charging Infrastructure Expansion Supporting EV Subsystem Build-Out

Italy's public charging infrastructure has expanded steadily over the past year, with notable growth in both total charging points and high-power charging installations. The expansion of high-power charging improves EV usability and reduces charging time, supporting higher utilization of electric vehicles. As charging infrastructure scales, the deployment of charging-related interfaces and associated vehicle-side subsystems also increases, raising demand for state detection and safety-switching solutions within charging ports, connectors, and access panels.

This infrastructure build-out strengthens downstream demand for EV subsystem components, including reed sensors and switches used in charging interlocks and safety-state verification. As charging networks expand geographically and in capacity, the number of charging-related sensing nodes increases, supporting incremental demand growth beyond conventional body electronics applications[2]"Auto elettriche: l’Italia supera i 64.391 punti di ricarica a uso pubblico…," Motus-E, motus-e.org..

Rising BEV Parc Increasing EV-Associated Sensing Points

Italy's battery electric vehicle (BEV) parc continues to expand from a low base, increasing the population of vehicles that rely on electrified architectures. Each BEV requires more sensing points than internal combustion engine vehicles, particularly across battery systems, charging interfaces, and high-voltage safety circuits. These architectures require multiple sensing nodes for access detection, interlock confirmation, and subsystem monitoring.

As the BEV parc grows, demand for EV-associated sensing points increases cumulatively. This supports sustained growth in battery- and charging-related applications for reed sensors and switches, as OEMs and Tier-1 suppliers incorporate safety and state-detection functions into EV subsystem designs.

National Incentives Supporting BEV Demand and Fleet Renewal

National incentive programs supporting battery electric vehicle adoption and fleet renewal improve demand visibility for electrified vehicles. Incentives that combine purchase support with scrappage conditions encourage the replacement of older vehicles and accelerate turnover toward newer, electrified platforms. This supports higher near-term BEV registrations and strengthens the demand outlook for EV-related components.

Improved demand visibility also supports OEM and supplier planning for electrified platforms. As incentive-backed adoption increases, component suppliers benefit from more predictable sourcing volumes for battery- and charging-related sensing solutions integrated into new vehicle programs.

Replacement-Driven Demand in Body Electronics

Body electronics remains the largest application segment in Italy's automotive reed sensors and switches market. The country's aging vehicle fleet and extended vehicle ownership cycles support recurring demand for replacement of closure, access, and position-detection components. These systems experience wear over time, leading to a higher replacement frequency compared to other vehicle subsystems.

This replacement-driven demand stabilizes the market, supporting baseline consumption even during periods of weak new vehicle production. As a result, body electronics applications continue to anchor overall market demand and reduce volatility linked to OEM production cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weak Domestic Vehicle Production Base | -1.0% | Italy-Specific | Medium term (2-4 years) |

| EU Emissions Policy Uncertainty | -0.7% | EU-Wide (Italy Impacted) | Short term (≤ 2 years) |

| Solid-State Sensor Substitution | -0.6% | EU-Wide | Medium term (2-4 years) |

| OEM Cost-Down And Consolidation | -0.4% | EU OEM Platforms | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Domestic Production Weakness Constraining Factory-Fit Volumes Tied to Italy Assembly

Italy's domestic automotive production has remained weak, resulting in lower volumes of vehicles assembled locally. Reduced production output limits factory-fit demand for reed sensors and switches used in Italy-assembled vehicles and modules. This can constrain near-term scale benefits for suppliers primarily aligned with domestic OEM programs.

Lower local assembly volumes shift the demand mix toward imported vehicles and cross-border platform programs. While overall consumption remains supported by vehicle registrations and the in-use fleet, weak domestic production can slow growth in locally sourced OEM demand during the forecast period.

Emissions-Policy Uncertainty Affecting Long-Term Platform Planning

While European emissions standards continue to set clear near-term compliance targets, uncertainty around the longer-term regulatory pathway introduces planning challenges for OEMs and Tier-1 suppliers. Proposed adjustments to post-2035 regulatory frameworks can delay or re-sequence platform investments, particularly for programs with long development cycles.

This uncertainty can affect sourcing cadence for electrified platforms and associated components. Delays in platform finalization or shifts in technology roadmaps may temporarily slow decision-making for suppliers of EV-related sensing solutions, impacting the timing of demand realization rather than the long-term direction of electrification.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reed Switches Lead; Reed Sensors Expand Faster

Reed switches led the Italian automotive reed sensors/switches market in 2025, with a market share of 71.25%. Their leadership reflects continued use as robust and cost-effective binary switching elements in applications where magnetic actuation and sealed contacts are valued. Reed switches remain widely deployed in body-electronics state-detection functions and other modules where reliability, durability, and predictable switching behavior are prioritized.

Reed sensors are projected to grow faster, registering a CAGR of 7.48% during 2026–2031. This growth reflects increasing OEM and Tier-1 preference for packaged and integration-ready sensing formats, including overmolded, surface-mount, and assembly-level sensor solutions. These formats improve mounting repeatability and simplify module manufacturing, which becomes increasingly relevant as electrification drives higher subsystem integration and tighter packaging requirements.

By Application: Body Electronics Anchor Demand; Battery and Charging Systems Drive Growth

Body electronics represented the largest application segment in 2025 at 48.17%. Demand is supported by the size of the installed vehicle base and continued feature penetration in closures, access modules, latches, and cabin mechanisms. These components are also serviceable throughout the vehicle lifecycle, supporting recurring replacement demand through the aftermarket channel.

Battery and charging systems are projected to be the fastest-growing application segment, registering a CAGR of 10.68% over the forecast period. Growth is supported by the rapid expansion of the public charging network and a rising battery electric vehicle parc. These trends increase the deployment of EV-associated modules and charging interfaces, raising demand for sensing solutions for access detection, interlocks, and safety-state monitoring within charging and battery subsystems.

By Vehicle Type: Passenger Cars Remain the Core Demand Base

Passenger cars dominated the market in 2025, with a share of 72.35%, and are projected to remain the fastest-growing vehicle type, registering a CAGR of 6.38%. This reflects where electronics feature content and electrification adoption are most concentrated within Italy’s automotive market. Passenger vehicles have a higher density of body electronics and EV-related subsystems than most other commercial vehicle categories.

Electrification adoption, new feature rollouts, and charging-enabled consumer usage patterns are primarily concentrated in passenger vehicles. As a result, passenger cars continue to drive both baseline volumes and incremental growth for reed sensors and switches across conventional body electronics and EV-adjacent applications.

By Sales Channel: OEMs Lead; Aftermarket Growth Reflects Fleet Aging

OEMs represented the largest sales channel in 2025, with a market share of 77.54%. Reed sensors and switches are typically specified during the design and validation stages of vehicle platforms and integrated into modules sourced through Tier-1 suppliers. This makes factory-fit demand the primary contributor to overall market value.

The aftermarket is projected to grow slightly faster, registering a CAGR of 6.78% during the forecast period. Growth is supported by Italy’s aging vehicle fleet and replacement-driven demand for body-electronics components. When domestic production cycles are weak, service and repair activity supports a higher share of incremental demand, reinforcing the importance of the aftermarket channel.

By Propulsion Type: ICE Dominates Today; BEVs Drive Incremental Growth

Internal combustion engine vehicles remained the largest propulsion segment in 2025, with a market share of 61.35%. This reflects the dominance of ICE vehicles within Italy’s installed vehicle parc and their continued reliance on reed sensors and switches for body electronics and conventional control applications.

Battery electric vehicles are projected to grow at the fastest rate, registering a CAGR of 12.18% during 2026–2031. Growth is supported by rising BEV parc levels, rapid expansion of public charging infrastructure, and incentives aimed at fleet renewal and BEV adoption. BEV architectures introduce additional sensing requirements in battery packs, charging systems, and high-voltage safety circuits, increasing sensing density per vehicle and across the charging ecosystem.

Geography Analysis

Demand for automotive reed sensors and switches in Italy is concentrated in regions with the largest vehicle parc, highest service density, and the strongest concentration of repair and maintenance activity. Northern and central provinces account for a significant share of vehicle ownership and workshop networks, which support recurring replacement demand for body-electronics sensing points such as closures, access modules, and latch-related detection. This geographic concentration reinforces the importance of the aftermarket channel, as replacement cycles are longer in areas with high vehicle density and high annual mileage.

Factory-fit demand is influenced by Italy’s limited domestic production footprint and the country’s reliance on imported vehicles and pan-European platform sourcing. As a result, OEM-driven demand is less dependent on localized assembly clusters and more linked to national registration patterns and the model mix entering the parc.

Growth in EV-associated sensing demand is more pronounced in metropolitan areas and corridors where public charging infrastructure deployment is denser and BEV adoption is higher, supporting faster expansion of battery- and charging-related sensing applications relative to conventional body electronics in these regions.

Competitive Landscape

Competition in Italy’s automotive reed sensors and switches market is shaped by European OEM and Tier-1 qualification requirements, ongoing cost-down pressures, and a gradual shift toward higher integration in electrified vehicle modules.

Suppliers compete on reliability, compact form factors, manufacturability, and the ability to support both the large body-electronics demand base and the faster-growing battery and charging subsystem opportunity.

Italy’s weak domestic vehicle production increases the importance of alignment with pan-European vehicle platforms, including imported models, for factory-fit demand. At the same time, replacement-driven aftermarket channels remain structurally resilient. Suppliers that can balance OEM platform participation with strong aftermarket coverage are better positioned to sustain volumes and capture incremental growth over the forecast period.

Italy Automotive Reed Sensors/Switches Industry Leaders

-

Standex Electronics

-

Coto Technology

-

Littelfuse Inc.

-

PIC GmbH

-

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Standex Detect announced the MK33 SMD Reed Switch Series, designed for compact assemblies / sensor packaging.

- January 2024: Littelfuse (Hamlin) announced availability of the MITI-7L ultra-miniature 7 mm reed switch series.

Italy Automotive Reed Sensors/Switches Market Report Scope

Automotive reed sensors and reed switches are magnetically actuated switching/sensing components used to detect position, proximity, presence, or limit states in vehicle systems. Reed switches typically use hermetically sealed contacts actuated by a magnetic field, while reed sensors generally package the reed element into application-ready formats (e.g., molded housings or SMD-friendly packages) suited to module integration.

The scope includes segmentation by Product Type (Reed Switches and Reed Sensors), Application (Body Electronics, Battery and Charging Systems, Powertrain & Drivetrain, Safety & Security Systems, and Others), Vehicle Type (Passenger Cars and Commercial Vehicles), Sales Channel (OEMs and Aftermarket), Propulsion Type (Internal Combustion Engine (ICE) Vehicles, Hybrid Electric Vehicles (HEV), Plug-in Hybrid Electric Vehicle (PHEV), Battery Electric Vehicles (BEV), and Fuel Cell Electric Vehicles (FCEV)). The market forecasts are provided in terms of value (USD).

| Reed Sensors |

| Reed Switches |

| Engine and Powertrain Systems |

| Body Electronics |

| Safety and Security Systems |

| Infotainment and Comfort Systems |

| Transmission and Braking Systems |

| Battery and Charging Systems |

| Other Applications |

| Passenger Cars |

| Commercial Vehicles |

| OEMs |

| Aftermarket |

| Internal Combustion Engine (ICE) Vehicles |

| Hybrid Electric Vehicles (HEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Battery Electric Vehicles (BEV) |

| Fuel Cell Electric Vehicles (FCEV) |

| By Product Type | Reed Sensors |

| Reed Switches | |

| By Application | Engine and Powertrain Systems |

| Body Electronics | |

| Safety and Security Systems | |

| Infotainment and Comfort Systems | |

| Transmission and Braking Systems | |

| Battery and Charging Systems | |

| Other Applications | |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| By Sales Channel | OEMs |

| Aftermarket | |

| By Propulsion Type | Internal Combustion Engine (ICE) Vehicles |

| Hybrid Electric Vehicles (HEV) | |

| Plug-in Hybrid Electric Vehicle (PHEV) | |

| Battery Electric Vehicles (BEV) | |

| Fuel Cell Electric Vehicles (FCEV) |

Key Questions Answered in the Report

What is the current value of the Italy automotive reed sensors/switches market?

It stands at USD 8.45 million in 2025 and is projected to reach USD 12.11 million by 2031 (6.19% CAGR).

Which product type leads the Italy market today?

Reed switches lead with 71.25% in 2025 because they are widely used in body and convenience modules requiring reliable on/off sensing.

Which application is growing the fastest and why?

Battery and charging systems are growing fastest (10.68% CAGR, 2026–2031) as EV adoption and charging ecosystem expansion increase EV-associated sensing points.

Which sales channel is scaling quickest in Italy?

Aftermarket grows fastest (6.78% CAGR, 2026–2031) supported by replacement demand from the in-use vehicle base.

Which propulsion type will expand the quickest through 2031?

Battery electric vehicles grow fastest (12.18% CAGR, 2026–2031) as BEVs scale and add more battery/charging-related sensing nodes.

Page last updated on: