Iran Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

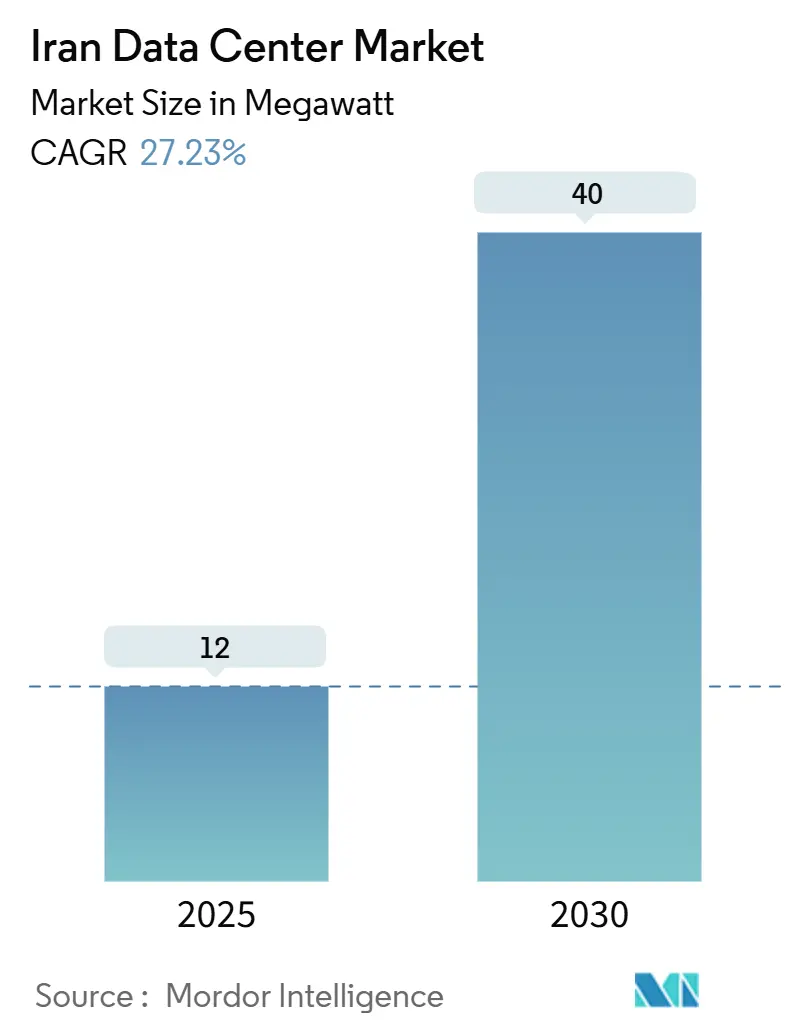

| Market Volume (2025) | 12 megawatt |

| Market Volume (2030) | 40 megawatt |

| Growth Rate (2025 - 2030) | 27.23% CAGR |

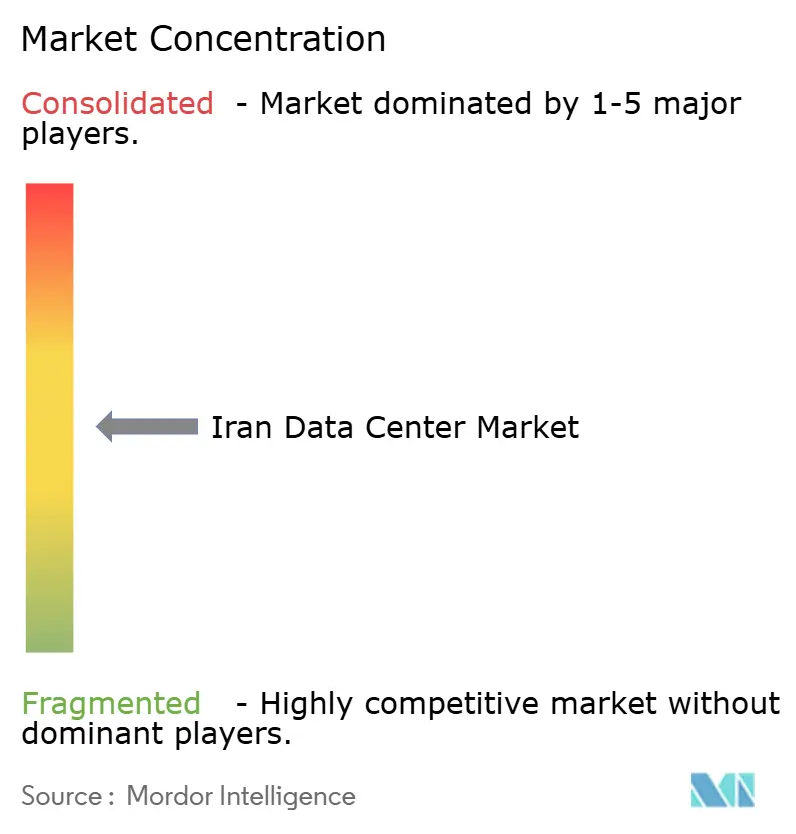

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iran Data Center Market Analysis by Mordor Intelligence

The Iran data center market size is 12 MW in 2025 and, at a forecast CAGR of 27.23%, is projected to reach 40 MW by 2030, underscoring the country’s rapid push for digital autonomy. A USD 16.6 billion public-sector investment program, tightening data-sovereignty mandates, and steadily rising enterprise cloud adoption create a supportive backdrop for hyperscale build-outs, while permitted cryptocurrency miners provide stable baseload demand. Tehran’s banking and government clusters keep the capital at the center of deal flow, yet Mashhad’s fiber gateway to Central Asia and access to low-cost renewables give it the fastest growth outlook. Mid-capacity facilities lead new supply, but domestic cloud providers are accelerating a shift toward mega-sites to replicate the scale once available only on global hyperscalers. Operators, however, confront sanctions-driven import curbs that raise equipment costs by 15-25% and a brain drain that is hollowing out experienced site engineers, forcing heavier reliance on automation and in-house training.

Key Report Takeaways

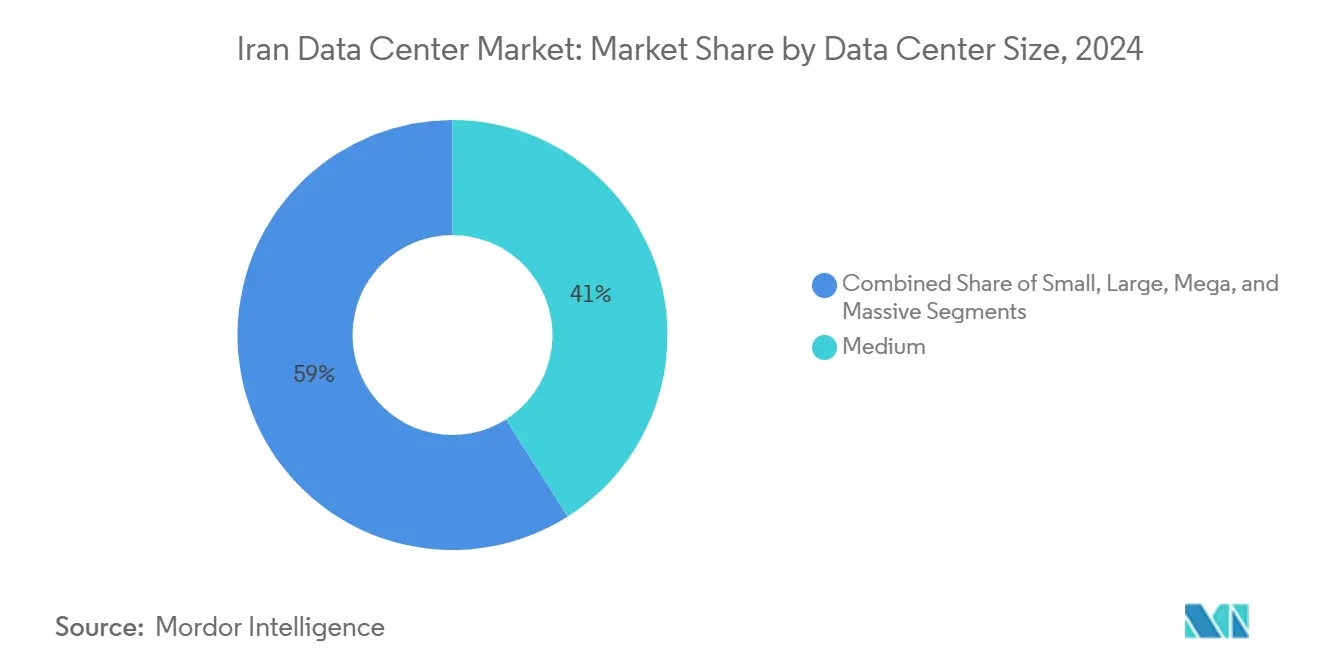

- By data-center size, medium facilities accounted for 41% of the Iranian data center market size in 2024; mega sites are forecast to expand at a 28.3% CAGR to 2030.

- By tier, Tier III captured 65% of the Iran data center market share in 2024, and Tier IV is growing at a 27.23% CAGR through 2030.

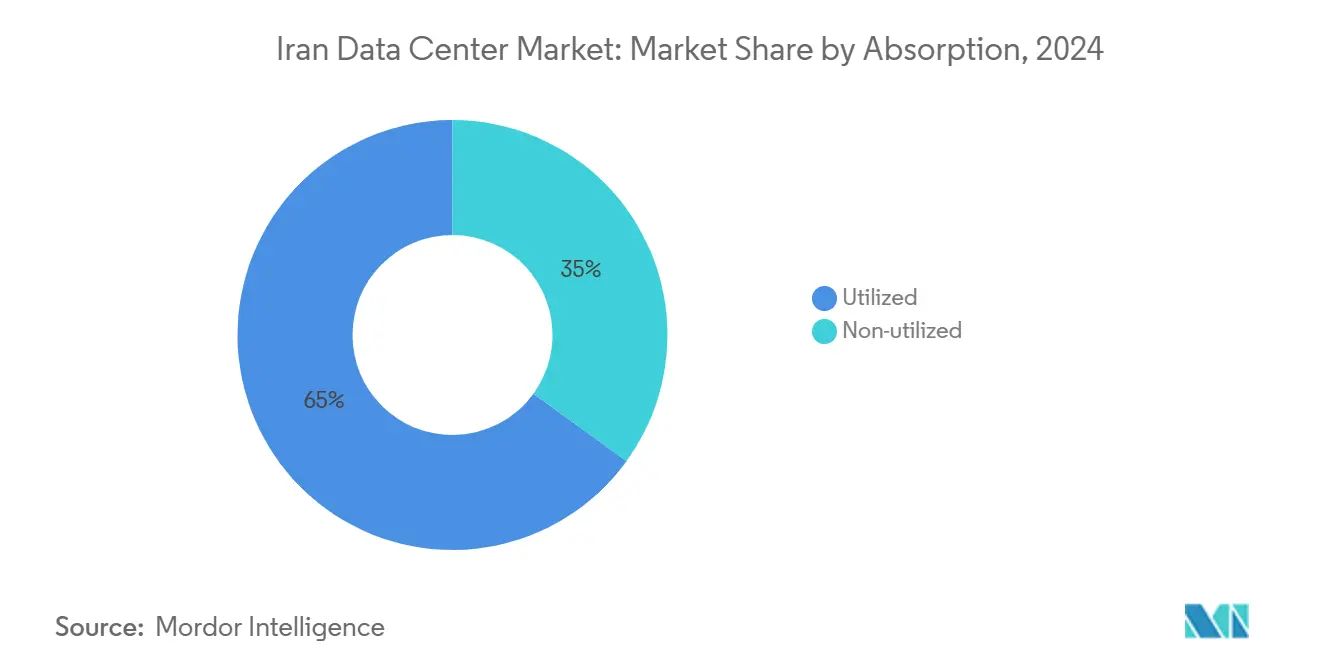

- By absorption, the utilized capacity represented 65% of the Iran data center market size in 2024, and hyperscale colocation is progressing at a 29.5% CAGR to 2030.

- By hotspot, Tehran held 47% of the Iran data center market share in 2024, while Mashhad is advancing at a 27.23% CAGR through 2030.

Iran Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-transformation funding under Iran’s 7th Five-Year Plan | +8.2% | Nationwide; strongest in Tehran | Medium term (2–4 years) |

| Expansion of domestic cloud regions (Abr Arvan, Hetra) | +6.8% | Tehran, Mashhad | Short term (≤ 2 years) |

| Growth in mobile data traffic and pilot 5G networks | +5.4% | Urban centers | Medium term (2–4 years) |

| Renewable-energy incentives in free-trade zones | +3.7% | Chabahar, Kish, Qeshm, new FTZs | Long term (≥ 4 years) |

| Licensed crypto-mining demand moving into pro facilities | +4.1% | Semnan, Alborz, Tehran | Short term (≤ 2 years) |

| China-Iran-Europe fiber corridor | +2.9% | Mashhad corridor, southern ports | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

National Digital-Transformation Funding Under Iran’s 7th Five-Year Plan

The USD 16.6 billion funding envelope redirects national priorities from petro-revenues to digital services, with six state-backed AI megaprojects focused on cutting industrial energy use by up to 25%.[1]Tehran Times, “Iran designs 6 AI megaprojects to tackle energy imbalance,” tehrantimes.com Mandatory migration of 3,000 e-government services toward centralized cloud authentication is accelerating workload placement into domestic facilities. As the National Information Network nears completion, mandatory in-country hosting rules lock enterprise and public-sector traffic inside Iranian borders, prompting roughly 15–20 MW of incremental capacity for banking modernization alone.

Expansion of Domestic Cloud Regions Replacing Hyperscalers

Sanctions that sidelined AWS and Microsoft Azure have opened a sizeable gap now filled by providers such as Abr Arvan and Hetra. Quarterly reports show Abr Arvan handling 315 abuse requests and 51 judicial oversight cases in Winter 2024, signaling enterprise-grade adoption.[2]ArvanCloud, “Cultivating Trust with Our Quarterly Transparency Reports,” arvancloud.ir Forced localization has turbo-charged cloud maturity by an estimated three to five years, with providers rolling out multi-region redundancy and compliance toolsets once sourced abroad. Financial institutions previously wary of offshore hosting are mandating local cloud deployment, creating a captive demand base.

Rapid Growth in Mobile Data Traffic and Pilot 5G Networks

Nationwide 5G activation is scheduled for March 2025 on 3.6–3.7 GHz spectrum, following auctions that secured handset interoperability.[3]Iran Daily, “5G mobile Internet to launch countrywide by year end,” irandaily.ir Seventy million users now consume high-speed mobile data, straining metropolitan backhaul capacity and prompting carriers to build edge nodes within a 10 millisecond latency envelope. Government targets to double household broadband to 14 million connections further lift colocation requirements for caching, analytics, and content delivery.

Licensed Crypto-Mining Demand Shifting Into Professional Data Centers

Thirty authorized mining operations, each exceeding 200 kWh monthly consumption, now collocate hardware in purpose-built facilities, stabilizing utilization above 90% far higher than the 60–70% traditional enterprise average. Regulatory guidance channels miners toward sites with robust power and cooling, providing operators with predictable base-load revenue even as tariff regimes fluctuate seasonally.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| U.S. sanctions limiting advanced IT imports and financing | -7.3% | Nationwide | Short term (≤ 2 years) |

| Seasonal electricity shortages and tariff volatility | -4.8% | Nationwide; peak in summer | Short term (≤ 2 years) |

| Seismic-zone construction cost premium | -2.1% | Tehran, Mashhad, Bandar Abbas | Long term (≥ 4 years) |

| Brain drain of certified facility engineers | -3.4% | Large urban centers | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

U.S. Sanctions Limiting Advanced IT Imports and Financing

A ban on 2,500 high-tech items pushes capex 15–25% above pre-sanction baselines and stretches build schedules by up to a year. Exclusion from global payment rails forces reliance on local lenders, whose ticket sizes rarely exceed USD 50 million. Older, less efficient hardware raises power overhead 20–30%, while restricted cooling technologies complicate Tier IV ambitions for banks and the public sector.

Seasonal Electricity Shortages and Tariff Volatility

National demand climbs past 72,000 MW each summer, exposing data-center operators to brownouts and penalty tariffs pegged to temperature and system load. Policymakers have singled out cryptocurrency miners, threatening higher rates when air-conditioning drives 40% of consumption. Operators now budget an extra 10–15% capex for on-site storage and generation to mitigate volatility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Size: Medium Facilities Lead, Mega Segment Accelerates

Medium-capacity halls, typically 1–5 MW, held 41% of the Iran data center market share in 2024 by catering to regional banks and ministries that need dedicated infrastructure without hyperscale complexity. Domestic cloud providers, however, are catalyzing a surge in 10 MW-plus builds. The mega category is forecast to post 28.3% CAGR as Abr Arvan and Hetra pursue economies of scale to rival global peers.

Legacy small sites cling to ISP and SME customers, while large footprints serve telco trunks and industrial groups. Financing constraints and import bottlenecks cap the pace of massive (over 20 MW) campuses, but crypto-miner co-location is nudging demand toward larger contiguous blocks that optimize PUE and staffing ratios.

By Tier Type: Tier III Dominance With Tier IV Acceleration

Tier III captured 65% of the Iran data center market size in 2024, offering 99.982% uptime through N+1 redundancy at a tolerable price point. Seismic codes effectively make Tier I non-viable for new projects, establishing Tier III as the default floor. Financial institutions and national service portals are pushing Tier IV adoption at a 27.23% CAGR to secure 99.995% uptime and dual-power paths.

Supply, however, lags demand because sanctions complicate sourcing high-efficiency UPS and redundant cooling hardware. Operators able to demonstrate Tier IV certification enjoy premium pricing and long-tenor contracts, particularly in Tehran’s banking district and Mashhad’s carrier hotels.

By Absorption: High Utilization Rates Signal Healthy Demand

Utilized racks constituted 65% of total area in 2024, reflecting a tight supply environment rare in regional peers. Domestic cloud expansion fuels a 29.5% CAGR in hyperscale colocation, where tenants lease entire data halls under long-term deals. Retail cabinets continue to serve SMEs, while wholesale suites address large enterprise and public-sector needs for compliance-ready environments.

Non-utilized capacity sits mostly in freshly commissioned halls undergoing ramp-up rather than systemic oversupply. The Iran data center market size tied to BFSI workloads is growing steadily, driven by core banking modernization, whereas e-commerce giants seek edge nodes near major population centers to trim last-mile latency.

By Hotspot: Tehran Dominance Faces Mashhad Challenge

Tehran accounts for 47% of the Iran data center market size in 2024, underpinned by dense banking and governmental demand. Stringent data-residency rules keep mission-critical workloads inside the capital despite higher land prices and seismic premiums. Mashhad, however, is projected to grow at a 27.23% CAGR, helped by the China-Iran-Europe fiber corridor, which offers 540 Gbps and is scalable to 3.2 Tbps. Renewable-powered sites in the northeast trim power costs by up to 20%, attracting both carriers and domestic cloud nodes.

Competition from emerging free-trade zones is set to diversify footprints beyond the two hubs. Chabahar’s 30-year tax holiday and duty-free machinery imports bode well for operators pursuing large campuses, though skills scarcity outside major cities remains a drag. The Iran data center market share attributable to secondary cities is therefore poised to climb, yet will not displace the strategic relevance of Tehran for regulated workloads.

Geography Analysis

Tehran retains 47% share of installed capacity, sustained by unparalleled fiber density and immediate access to regulators and C-suite buyers. High real-estate costs and seismic complexity raise development expenses, yet the capital’s role as nerve center of the National Information Network preserves its primacy. Operators nonetheless face peak-season grid strain, prompting heavier investment in diesel or gas-fired backup.

Mashhad is the standout growth node, clocking 27.23% CAGR through 2030 thanks to international fiber transit, renewable energy availability, and proximity to Afghan and Central Asian end markets. The Europe-Persia Express Gateway positions the city as Iran’s eastern traffic aggregation point, while moderate land prices and lower seismicity aid large-campus economics.

Free-trade zones from Kish to Chabahar round out the map. Thirty-year tax relief, duty-free imports, and preferential energy tariffs are luring pilot builds that, over time, could dilute Tehran’s concentration risk. Renewable capacity touching 4,800 MW by March 2025 gives southern and southeastern provinces a sustainability edge. Still, talent scarcity and route diversity remain gating factors for hyperscale entrants evaluating green-field options.

Competitive Landscape

Market structure is moderately fragmented. Telco incumbents Iran Telecommunication Company (TCI) and Mobile Telecommunication Company of Iran (MCI) wield extensive metro fiber and established enterprise accounts. Pure-play operators such as Fanap Infrastructure leverage agility to win high-spec contracts, while Abr Arvan and Hetra scale out cloud regions that absorb sizeable white-space in mega-campuses. Regulatory favor toward local hosting further cements their pipelines.

Energy strategy is a core differentiator. Sites tapping subsidized renewables in FTZs cut OPEX and appeal to ESG-focused tenants. Sanctions create entry barriers that reward players with diversified sourcing and engineering depth; the Iranian seismic code demands premium construction know-how that only well-capitalized actors can meet. Meanwhile, crypto-mining specialists sign multi-year PPAs that stabilize occupancy, giving host operators financial cushioning amid tariff swings.

Competitive intensity spikes in hyperscale deals, with price points squeezing as domestic clouds jockey to land fintech and public-sector workloads formerly on foreign clouds. Yet, capacity scarcity lets established facilities in Tehran still command premium rates, especially for Tier IV suites tailored to banking and real-time payment workloads.

Iran Data Center Industry Leaders

Iran Telecommunication Co. (TCI)

Mobile Telecommunication Co. of Iran (MCI)

Shatel Group

Asiatech

Abr Arvan

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Countrywide 5G activation scheduled by March 2025 after 3.6–3.7 GHz spectrum auctions, elevating edge-computing demand across population centers.

- May 2025: The IT Organization of Iran launched six AI megaprojects targeting industrial energy management, signaling a rising need for HPC-grade data-center capacity.

- April 2025: The Communications Ministry confirmed plans to unveil new satellites and double household broadband connections to 14 million, amplifying backhaul requirements.

- March 2025: National renewable energy portfolio hit 4,800 MW, opening avenues for sustainable data-center power procurement in FTZs.

Iran Data Center Market Report Scope

The Iran Data Center Market Report is Segmented by Data Center Size (Small, Medium, Large, Mega, Massive), Tier Standard (Tier I and II, Tier III, and Tier IV), Absorption (Non-Utilized, Utilized (Colocation Type (Hyperscale, Retail, Wholesale), End-User (BFSI, Cloud Service Providers, E-Commerce, Government, Manufacturing, Media and Entertainment, Telecom, and Other End-Users)), and Hotspot (Tehran, Mashhad, Rest of Iran). The Market Forecasts are Provided in Terms of Volume (MW Capacity).

| Tehran |

| Mashhad |

| Rest of Iran |

| Small |

| Medium |

| Large |

| Mega |

| Massive |

| Tier I and II |

| Tier III |

| Tier IV |

| Non-utilized | ||

| Utilized | By Colocation Type | Hyperscale |

| Retail | ||

| Wholesale | ||

| By End-User | BFSI | |

| Cloud Service Providers | ||

| E-Commerce | ||

| Government | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Telecom | ||

| Other End-Users | ||

| By Hotspot | Tehran | ||

| Mashhad | |||

| Rest of Iran | |||

| By Data-Center Size | Small | ||

| Medium | |||

| Large | |||

| Mega | |||

| Massive | |||

| By Tier Type | Tier I and II | ||

| Tier III | |||

| Tier IV | |||

| By Absorption | Non-utilized | ||

| Utilized | By Colocation Type | Hyperscale | |

| Retail | |||

| Wholesale | |||

| By End-User | BFSI | ||

| Cloud Service Providers | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End-Users | |||

Key Questions Answered in the Report

What is the installed data-center capacity in Iran today and its growth outlook to 2030?

Installed capacity stands at 12 MW in 2025 and is projected to rise to 40 MW by 2030, reflecting a 27.23% CAGR.

Which Iranian city holds the largest share of operational data-center space?

Tehran commands 47% of national capacity, driven by its concentration of banks, ministries, and carrier interconnects.

Why is Mashhad viewed as the fastest-expanding data-center hub?

Its position on the China–Iran–Europe fiber corridor and access to low-cost renewables support a 27.23% CAGR through 2030.

How do U.S. sanctions affect data-center construction economics in Iran?

Restrictions on 2,500 high-tech imports inflate capital costs by 15-25% and add 6–12 months to typical build schedules.

What impact do licensed cryptocurrency miners have on facility utilization?

Their high-density workloads lift average utilization above 90%, providing predictable base-load revenue for operators.

What portion of Iranian facilities are Tier III and what drives this preference?

Tier III sites account for 65% of capacity because they deliver 99.982% uptime with N+1 redundancy at a cost most enterprises can absorb.

Page last updated on: