Intravascular Warming Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

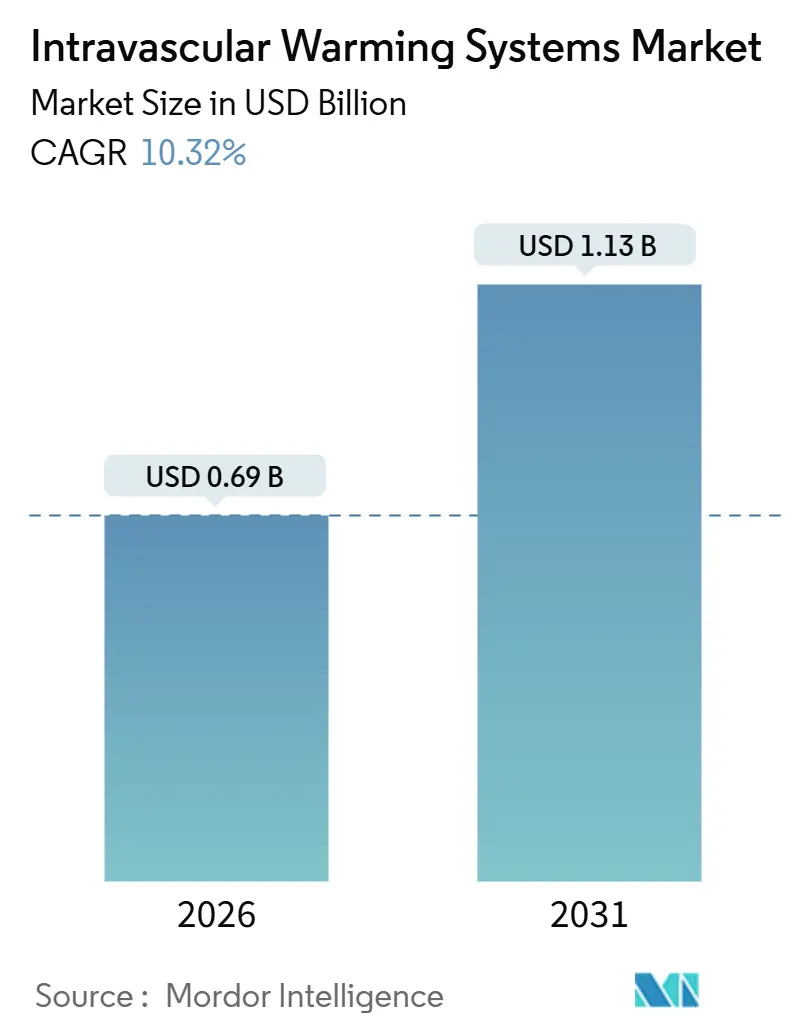

| Market Size (2026) | USD 0.69 Billion |

| Market Size (2031) | USD 1.13 Billion |

| Growth Rate (2026 - 2031) | 10.32% CAGR |

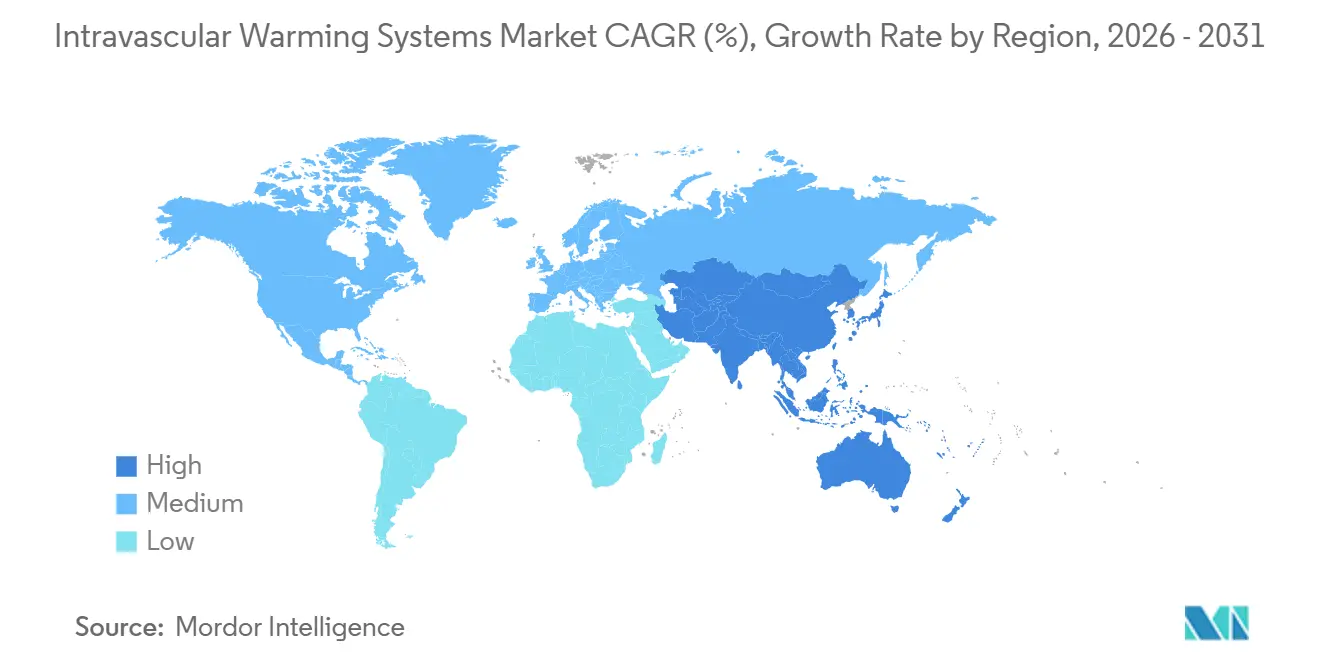

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intravascular Warming Systems Market Analysis by Mordor Intelligence

The Intravascular Warming Systems Market size is estimated at USD 0.69 billion in 2026, and is expected to reach USD 1.13 billion by 2031, at a CAGR of 10.32% during the forecast period (2026-2031).

Clinical evidence tying even mild peri-operative hypothermia to longer hospital stays and higher infection rates is prompting health-system administrators to shift capital budgets toward active core-temperature technology, especially in operating rooms that already report near-saturation for standard fluid warmers. Vendors are also benefiting from hospital infection-prevention policies that favor single-use disposables, a trend that has transformed accessories into the fastest-growing revenue stream across the intravascular warming systems market. On the demand side, emergency departments and trauma centers are rolling out rapid-rewarming protocols for sepsis and hemorrhagic shock, widening the addressable base beyond traditional cardiac and transplant suites. Meanwhile, the integration of closed-loop algorithms guided by artificial intelligence is recasting consoles from static hardware into software-enabled platforms that reduce the workload for anesthesiologists and critical-care nurses. Consolidation among leading manufacturers is underway as incumbents acquire catheter, monitoring, and vascular-access assets to deliver “one-stop” peri-operative suites and defend share.

Key Report Takeaways

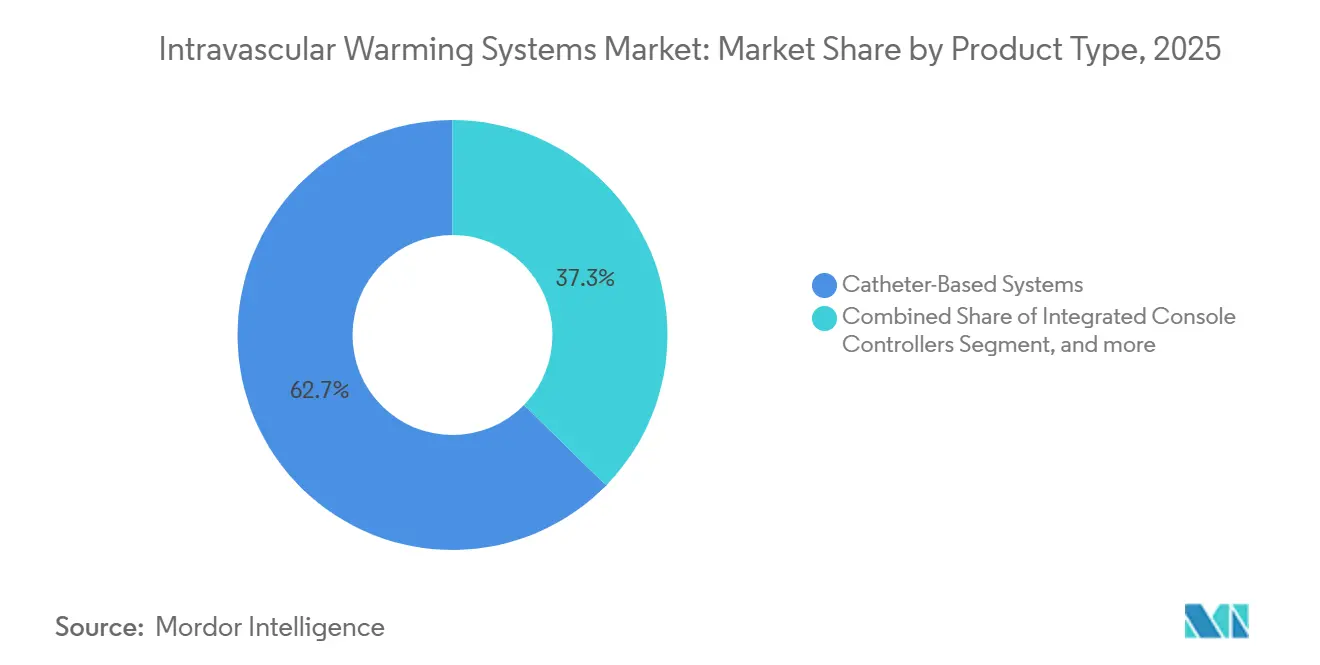

- By product type, catheter-based systems captured 62.67% of the intravascular warming systems market share in 2025; accessories and disposables are forecast to grow at a 12.54% CAGR through 2031.

- By application, peri-operative care accounted for 48.65% of revenue in 2025, while acute-care adoption is projected to grow at a 12.66% CAGR through 2031.

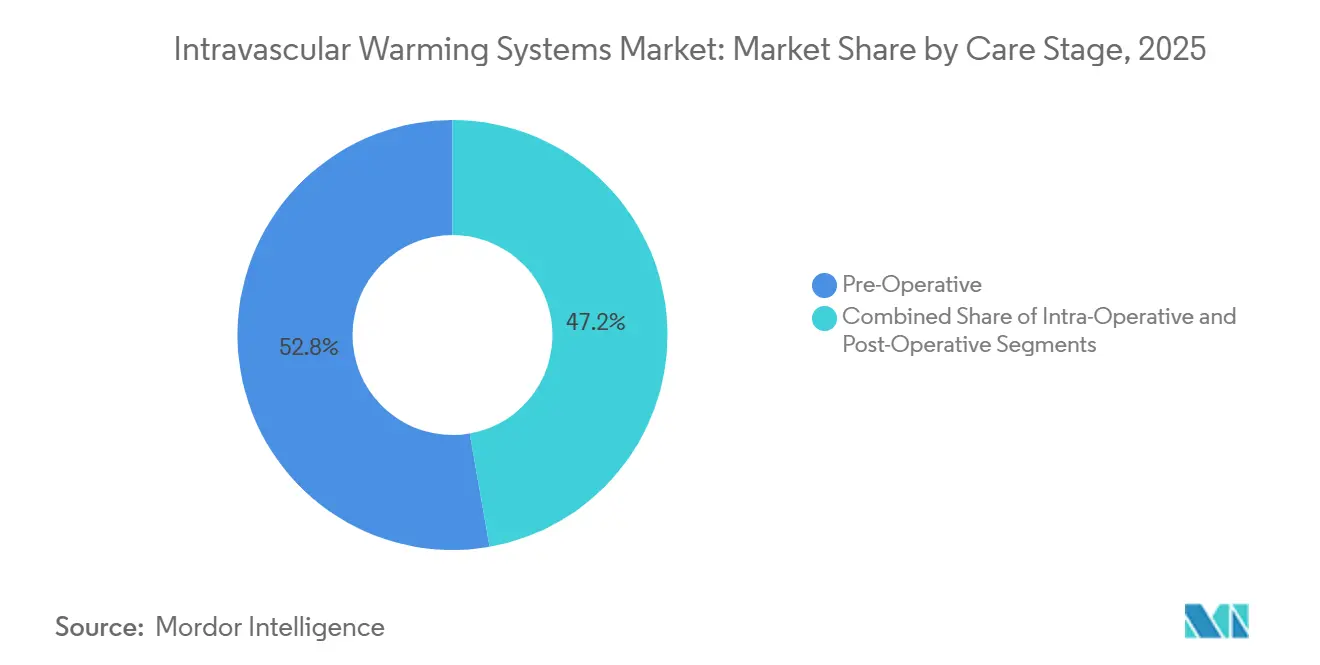

- By care stage, pre-operative warming held 52.76% share in 2025; post-operative usage is poised to climb at a 13.76% CAGR through 2031 as recovery units implement closed-loop algorithms.

- By end user, intensive care units generated 42.87% of revenue in 2025, yet emergency rooms are expected to register the fastest 13.54% CAGR as triage protocols formalize active warming for unstable patients.

- By geography, North America led with 42.56% revenue share in 2025; Asia-Pacific is projected to expand at an 11.43% CAGR through 2031 on the back of large-scale hospital-bed additions in China and India.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Intravascular Warming Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Surgical Procedure Volumes | +2.8% | Global, with concentration in North America & APAC | Medium term (2-4 years) |

| Rising Geriatric Population and Chronic Disease Burden | +2.3% | Global, particularly Europe & North America | Long term (≥ 4 years) |

| Stringent Patient Safety and Quality Mandates | +1.9% | North America & EU | Short term (≤ 2 years) |

| Technological Advancements in Catheter-Based Thermal Control | +1.7% | Global, early adoption in North America & EU | Medium term (2-4 years) |

| Expansion of Military and Emergency Medical Services Procurement | +1.1% | North America, Middle East, APAC | Medium term (2-4 years) |

| Integration of AI-Enabled Closed-Loop Temperature Algorithms | +0.5% | North America & EU, pilot programs in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Surgical Procedure Volumes

Worldwide surgical procedures climbed to 313 million in 2024, up 6.1% year over year, and orthopedic, cardiovascular, and oncologic cases represented almost two-thirds of the incremental volume[1]World Bank, “Global Surgical Procedures Database 2024,” worldbank.org. Outpatient centers in the United States added 28.3 million cases in 2024 after Medicare approved total knee arthroplasty for ambulatory reimbursement, forcing clinicians to manage hypothermia risk within shorter turnover windows. Every hour under anesthesia lifts hypothermia odds by 18%, so anesthesiologists are standardizing routine intravascular warming even in 90-minute procedures. Japan reported an 11% surge in laparoscopic surgeries in 2024, a modality that depresses core temperature due to insufflation with chilled carbon dioxide, heightening demand for catheter-based warming that does not impede the operative field. Hospitals that prevent hypothermia shorten the average length of stay and unlock additional OR capacity, reinforcing device utilization across the intravascular warming systems market.

Rising Geriatric Population and Chronic Disease Burden

Global citizens aged 65 plus will reach 831 million in 2026, swelling by 70 million in just five years. Elderly patients possess less subcutaneous insulation and slower shivering reflexes, making them 2.4 times more likely to drop 35 °C below during surgery. Diabetes and peripheral vascular disease affect 537 million adults and hinder microcirculation, delaying passive rewarming and making active intravascular therapy clinically necessary[2]World Health Organization, “Global Diabetes Statistics 2024,” who.int. A German cohort study of 1,840 hip-fracture patients warmed with intravascular catheters reported 31% fewer infections and EUR 4,200 lower per-patient costs, a data point payer are starting to embed in bundled-payment models. The demographic swell, therefore, directly expands the intravascular warming systems market as hospitals upgrade temperature control to protect frail patients.

Stringent Patient Safety and Quality Mandates

The CMS Hospital-Acquired Condition Reduction Program has penalized peri-operative hypothermia since January 2025, cutting up to 1% of Medicare revenue for outlier hospitals. The Joint Commission now demands core-temperature documentation every thirty minutes from induction through recovery, steering procurement toward consoles that integrate continuous telemetry with electronic health records. Europe’s Medical Device Regulation requires ±0.3 °C thermal stability, favoring established vendors that can validate precision circuitry and maintain rigorous post-market surveillance. Compliance pressure, therefore, funnels capital toward high-reliability consoles and disposables, strengthening volume growth across the intravascular warming systems market.

Technological Advancements in Catheter-Based Thermal Control

ZOLL’s FDA-cleared Thermogard XP console delivers 400 watts of heat transfer, doubling the output of previous models and reducing time-to-normothermia by 40% in obese patients. Smiths Medical’s dual-lumen catheter, introduced in 2025, reduces turbulence so efficiently that heat-exchange performance jumps 22% against single-lumen designs. Material science matters as well; Belmont’s polyurethane-silicone coating averts fibrin buildup for 14 days, limiting catheter swaps and lowering infection risk. Faster normothermia translates to fewer ventilator hours and lower nosocomial infections, a value narrative that accelerates unit placements in the intravascular warming systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital and Consumable Expenditure | -1.4% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Variable Reimbursement and Budget Constraints | -1.1% | North America, Europe, select APAC markets | Medium term (2-4 years) |

| Regulatory Re-Certification Delays Under EU-MDR | -0.8% | Europe, spillover to exporters in North America | Short term (≤ 2 years) |

| Supply Chain Vulnerabilities in Specialized Polymer Coatings | -0.6% | Global, concentrated in North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Consumable Expenditure

Consoles list between USD 25,000 and USD 45,000, and single-use catheters cost USD 180–320, pushing per-case spend above USD 400 after tubing and saline are added[3]American Hospital Association, “Hospital Capital Equipment Survey 2025,” aha.org. A 300-bed hospital that performs 8,000 surgeries annually must commit USD 180,000 in year one for two consoles and consumables, crowding the wish list for robotic platforms and hybrid suites. In India’s public facilities, where per-bed budgets average USD 12,000, only 14% possess intravascular warming capability. Vendors have begun offering pay-per-use contracts to convert capital cost into operating expense, but adoption funnels mostly into private chains, limiting volume lift in the intravascular warming systems market.

Variable Reimbursement and Budget Constraints

CMS bundles warming costs into DRG payments, providing no incremental revenue when hospitals deploy intravascular devices rather than cheaper forced-air blankets. German authorities reimburse only for cardiac or vascular surgeries lasting more than 3 hours, leaving hospitals to self-fund consoles for shorter cases. Japan added a JPY 8,500 (USD 57) fees for ICU warming in 2025, yet the offset barely covers the catheter expense. Documentation hurdles and fragmented payer policies slow diffusion, especially in ambulatory centers operating on thin margins, dampening the trajectory of the intravascular warming systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Consoles Drive Infrastructure, Disposables Fuel Recurring Revenue

Catheter-based systems accounted for 62.67% intravascular warming systems market share in 2025 and remained the clinical mainstay for rapid core-temperature modulation. Integrated console controllers, though fewer in unit shipments, command premium pricing thanks to embedded processors and sophisticated user interfaces. Accessories and disposables are projected to expand at a 12.54% CAGR through 2031, outpacing consoles as hospitals embrace single-use sets that eliminate reprocessing costs and cross-contamination risks. Clinical data support the pivot; a 2025 meta-analysis of 3,200 patients found that disposable catheter kits reduced bloodstream infections by 41%, prompting infection-control bodies to advocate for exclusive single-use adoption. Gentherm’s Blanketrol III console pairs with proprietary pads that remove external water circulation, trimming setup time by 60% and appealing to ambulatory surgical centers focused on quick turnover. Subscription bundling—consoles, disposables, analytics—now shifts capital outlay into predictable operating budgets, a model likely to widen customer reach across the intravascular warming systems market.

The product mix is also evolving technologically. ZOLL and Medtronic embed wireless connectivity that streams real-time metrics to anesthesia dashboards, letting one clinician supervise multiple rooms simultaneously. Belmont’s 14-day dwell-time catheter aligns with prolonged ICU care, where device exchanges drive cost and infection risk. As disposables rise faster than console placements, revenue recurrence strengthens, improving visibility for suppliers and investors tracking the intravascular warming systems market size at the SKU level.

By Application: Acute Care Gains as Emergency Protocols Mandate Active Warming

Peri-operative care generated 48.65% of 2025 application revenue, a testament to embedded protocols that require normothermia from pre-incision through recovery. Yet acute-care settings are expected to log a 12.66% CAGR to 2031 as emergency rooms adopt intravascular systems for trauma resuscitation, septic shock, and targeted temperature management after cardiac arrest. The Surviving Sepsis Campaign’s 2025 update elevated active warming to a Grade 1B recommendation for hypotensive sepsis cases under 36 °C, a scenario now present in one-third of emergency presentations. Level I trauma centers that implemented rapid-rewarming protocols reported a 19% reduction in mortality among patients with Injury Severity Scores above 25. Peri-operative rooms remain the dominant install base, but protocol-driven demand in emergency departments is expanding the intravascular warming systems market into 24-hour environments where speed directly impacts survival.

Growth in acute care is reinforced by portable consoles that plug into standard wall outlets and reach therapeutic flow rates within two minutes. Vendor clinical support teams now train ED nurses to place femoral catheters under ultrasound guidance, avoiding delays that once limited their use to anesthesiologists. As sepsis bundle compliance links to reimbursement, hospitals view rapid-rewarming capability as both a quality metric and a revenue safeguard, further expanding the intravascular warming systems market tied to unscheduled admissions.

By Care Stage: Post-Operative Segment Surges on Recovery-Unit Protocols

Pre-operative warming retained a 52.76% share in 2025, thanks to ubiquitous forced-air blankets and fluid warmers stationed in holding bays. Yet post-operative adoption is set to accelerate at a 13.76% CAGR through 2031, fueled by recovery-unit algorithms that use intravascular feedback loops to curb shivering and lower opioid need. A 2025 randomized trial involving 520 abdominal-surgery patients cut shivering from 48% to 12% and enabled 23% of cases to bypass the post-anesthesia care unit, freeing scarce beds for subsequent procedures. The American Society of PeriAnesthesia Nurses guidelines now require active rewarming for any patient arriving at 36 °C or lower, a threshold met by 41% of 2024 discharges from 87 hospitals. As operating-room throughput tightens, administrators see post-operative warming as an operational lever, embedding consoles in Phase I and II bays and widening the intravascular warming systems market.

Intra-operative settings still consume a sizeable piece of the intravascular warming systems industry, especially during cardiothoracic and transplant cases that last four hours or more. However, surface devices often suffice for shorter orthopedic or general procedures, capping intra-operative growth. Post-operative segments, therefore, capture incremental share by addressing pain management, respiratory function, and discharge readiness, three metrics that strain hospital capacity and cost each day they extend.

By End-User: Emergency Rooms Accelerate Adoption for Time-Sensitive Protocols

Intensive-care units held 42.87% of end-user revenue in 2025, leveraging intravascular systems for targeted temperature management in cardiac arrest, traumatic brain injury, and refractory fever. Operating rooms follow closely, yet emergency departments are on track for a 13.54% CAGR through 2031 as clinical policies mandate active warming for hemodynamically unstable patients. The American College of Emergency Physicians recommends intravascular warming for any arrival below 32 °C or septic shock unresponsive to passive warming within thirty minutes. Cleveland Clinic documented a 27% reduction in time-to-normothermia after installing dedicated consoles in its Level I trauma bay in 2024. Ambulatory surgical centers, which performed 28.3 million U.S. procedures in 2024, are now adopting compact consoles as accreditation bodies raise temperature-management standards, providing another growth vector for the intravascular warming systems market.

High-acuity adoption is also spilling into pre-hospital care. Air-ambulance operators in Germany and the Gulf now carry battery-powered consoles that attach to standard 14-gauge IVs, improving thermal control before arrival at the hospital. Such use cases extend the technology’s reach beyond fixed facilities, broadening revenue opportunities across the intravascular warming systems market spectrum.

Geography Analysis

North America generated 42.56% of 2025 revenue, anchored by 6,090 U.S. hospitals and 5,900 ambulatory centers that together performed more than 51 million procedures in 2024. CMS hypothermia penalties enacted in 2025 have catalyzed widespread console upgrades, while Canada’s CAD 1.2 billion surgical backlog fund favors equipment that shortens length of stay. Mexico added 14 high-specialty units in 2024, each outfitted with warming systems for complex cancer and cardiovascular care. Although penetration in U.S. tertiary centers is nearing maturity, rising adoption in emergency departments and ambulatory centers is driving steady expansion of the intravascular warming systems market across the region.

Europe ranked second in revenue in 2025, with Germany, the United Kingdom, and France accounting for 58% of regional sales. Germany’s quality directive now requires continuous temperature monitoring in surgeries lasting more than 60 minutes, forcing hospitals to integrate console data with anesthesia records (G-BA.DE). The United Kingdom earmarked GBP 340 million for peri-operative infrastructure in 2024, placing warming consoles in 180 trauma centers. EU-MDR recertification delays lengthened launch timelines, temporarily tightening supply and raising unit prices, yet the emphasis on patient-safety metrics ensures sustained demand across the intravascular warming systems market. Southern Europe lags due to budget limits, relying on forced-air blankets except in flagship tertiary hospitals.

Asia-Pacific will post an 11.43% CAGR through 2031, the highest globally, stimulated by China’s 1.2 million new hospital beds between 2024 and 2025 and India’s USD 9.8 billion tertiary-care investment. China’s centralized procurement cut catheter prices 32% in 2024, unlocking adoption in tier-2 cities. Japan’s 29.1% geriatric population is boosting laparoscopic volumes, pressing hospitals to adopt closed-loop temperature control. Australia trimmed device-approval timelines to 180 days in 2024, and South Korea expanded insurance coverage for intravascular warming in neurosurgery in 2025. Price sensitivity still shapes configurations—many facilities start with one console per operating theater—but the sheer procedural volume will sustain rapid growth across the intravascular warming systems market.

The Middle East and Africa remain smaller in absolute terms but show infrastructure-led spikes. GCC nations invested USD 18.4 billion in 2024 healthcare builds; Saudi Arabia plans to build 50 new hospitals by 2028, with full peri-operative suites that require active warming. The UAE’s updated surgical guidelines in 2024 require active warming in all operations exceeding 90 minutes, driving console tenders for public and private chains. South Africa set aside ZAR 2.1 billion to modernize operating theaters in Gauteng and Western Cape, although broader adoption is hindered by reimbursement gaps. Sub-Saharan penetration will likely depend on donor funding and private-sector growth, moderating overall contribution to the intravascular warming systems market size.

South America is the smallest region, with Brazil and Argentina providing 71% of 2025 revenue. Brazil opened 22 high-complexity hospitals in 2024 that require intravascular warming for cardiac and trauma care. Argentina’s 2024 guideline endorses intravascular warming for high-risk surgeries, but currency volatility and device import tariffs slow procurement. Private chains in Chile and Colombia are adopting consoles to attract international bariatric and orthopedic clients, signaling a gradual yet steady expansion path for the intravascular warming systems market.

Competitive Landscape

The intravascular warming systems market remains moderately concentrated, with the top five suppliers—Medtronic, 3M, BD, Stryker, and ZOLL—capturing roughly 55% of global 2025 revenue. Incumbents pursue vertical integration to cement share; Medtronic’s USD 1 billion Affera purchase brings cardiac mapping and ablation under the same roof as the Arctic Sun platform, creating an electrophysiology bundle that leverages shared console architectures. BD’s USD 4.2 billion bid for Edwards Lifesciences’ critical-care unit aims to unite hemodynamic sensors with warming catheters, a pairing designed to lock ICUs into single-vendor procurement cycles. Stryker’s 2024 acquisition of Inari Medical extends reach into interventional suites, another high-temperature-required domain. Such moves illustrate a strategic pivot toward complete peri-operative ecosystems that raise switching costs and defend intravascular warming systems' market positions.

Technology differentiation is escalating. Medtronic’s Arctic Sun 5000 leverages predictive analytics to maintain ±0.2 °C stability in almost nine of ten monitored minutes, a software edge that amplifies clinical value beyond raw heating capacity. ZOLL’s Thermogard XP doubles power output while cutting setup time by 25%, a feature set tailored to emergency and bariatric units with urgent thermal needs. Belmont’s Allon2 and Smiths Medical’s dual-lumen catheter address infection control and dwell-time pain points, carving space for mid-tier competitors to win niche contracts. Regulatory compliance with ISO 13485 and the EU MDR creates barriers, limiting new entrants while also shielding incumbents from price-led disruptions in the intravascular warming systems market.

Price pressure persists, especially in APAC and Latin America, where public tenders dominate. Vendors respond by offering lease-to-own models and bundled disposables that spread expenditure over procedure volume. Cloud-based analytics and remote console diagnostics now feature in proposal decks, adding sticky service revenue. The military and pre-hospital segments present greenfield opportunities, and multiple suppliers have launched ruggedized, battery-ready devices suited to austere environments, underscoring the continued white-space potential in the intravascular warming systems market.

Intravascular Warming Systems Industry Leaders

ZOLL Medical Corporation

Stryker Corporation

Medtronic plc

Smiths Group plc (Smiths Medical)

3M Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Stryker completed a USD 4.9 billion takeover of Inari Medical, enhancing its vascular-intervention footprint.

- June 2024: BD agreed to buy Edwards Lifesciences’ critical-care division for USD 4.2 billion, with closing targeted for mid-2026.

Global Intravascular Warming Systems Market Report Scope

As per the scope of the report, intravascular warming systems are medical devices used to maintain or raise a patient's core body temperature during surgery or critical care. They work by warming blood directly through catheters inserted into blood vessels. These systems help prevent hypothermia and improve patient outcomes.

The Intravascular Warming Systems Market is Segmented by Product Type (Catheter-Based Systems, Integrated Console Controllers, and Accessories & Disposables), Application (Acute Care and Peri-Operative Care), Care Stage (Pre-Operative, Intra-Operative, and Post-Operative), End-User (Ambulatory Surgical Centers, Emergency Rooms, ICUs, and Operating Rooms), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Catheter-Based Systems |

| Integrated Console Controllers |

| Accessories & Disposables |

| Acute Care |

| Peri-Operative Care |

| Pre-Operative |

| Intra-Operative |

| Post-Operative |

| Ambulatory Surgical Centers |

| Emergency Rooms |

| Intensive Care Units (ICUs) |

| Operating Rooms |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | GCC | |

| By Product Type | Catheter-Based Systems | ||

| Integrated Console Controllers | |||

| Accessories & Disposables | |||

| By Application | Acute Care | ||

| Peri-Operative Care | |||

| By Care Stage | Pre-Operative | ||

| Intra-Operative | |||

| Post-Operative | |||

| By End-User | Ambulatory Surgical Centers | ||

| Emergency Rooms | |||

| Intensive Care Units (ICUs) | |||

| Operating Rooms | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest Of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest Of Asia-Pacific | |||

| Middle East & Africa | GCC | ||

| South Africa | |||

| Rest Of Middle East & Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest Of South America | GCC | ||

Key Questions Answered in the Report

How large is the intravascular warming systems market in 2026?

The intravascular warming systems market size was USD 0.69 billion in 2026 and is projected to reach USD 1.13 billion by 2031.

Which product type holds the leading share?

Catheter-based systems captured 62.67% intravascular warming systems market share in 2025 and continue to anchor most console placements.

What is driving rapid adoption in emergency departments?

Updated sepsis and trauma protocols mandate active core-temperature control, pushing emergency rooms toward intravascular warming for faster normothermia and improved survival.

Which region will grow fastest through 2031?

Asia-Pacific is forecast to expand at an 11.43% CAGR thanks to large-scale hospital-bed additions in China and India and broader reimbursement in Japan and South Korea.

How are vendors differentiating their platforms?

Manufacturers are embedding AI-based closed-loop algorithms, higher-power heat exchangers, and wireless connectivity to reduce clinician workload and optimize temperature precision.

What challenges limit uptake in emerging markets?

High console prices, per-case disposable costs, and fragmented reimbursement frameworks slow adoption despite rising surgical volumes and government infrastructure investments.

Page last updated on: