Intermittent Catheters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

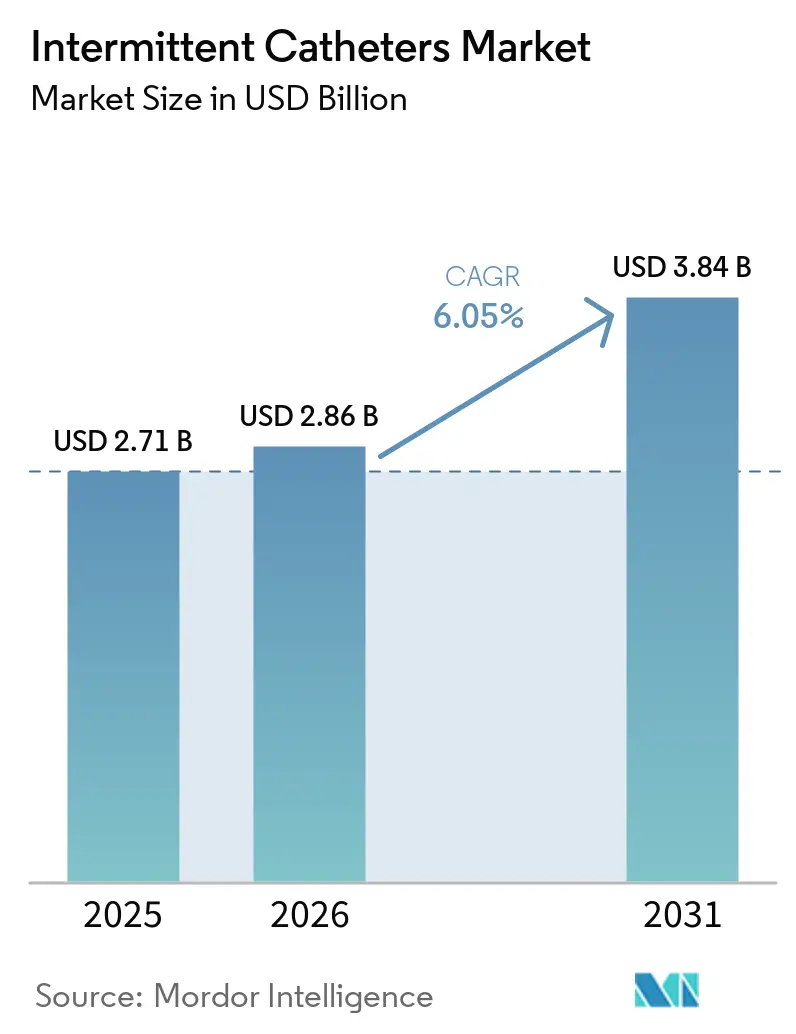

| Market Size (2026) | USD 2.86 Billion |

| Market Size (2031) | USD 3.84 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

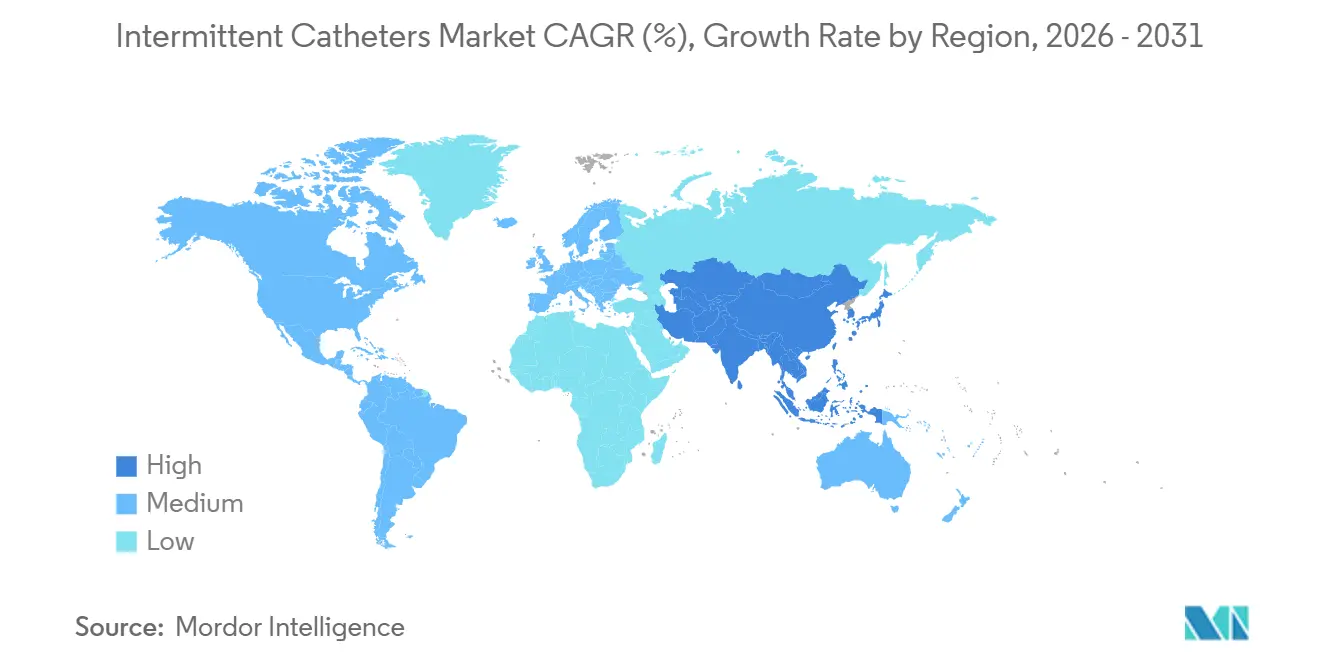

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intermittent Catheters Market Analysis by Mordor Intelligence

The Intermittent Catheters Market size is projected to expand from USD 2.71 billion in 2025 and USD 2.86 billion in 2026 to USD 3.84 billion by 2031, registering a CAGR of 6.05% between 2026 to 2031.

The intermittent catheters market is expanding as clean intermittent catheterization remains the preferred bladder management approach for many patients with spinal cord injury, multiple sclerosis, and other neurogenic conditions because it is associated with lower long-term complication risk than indwelling use. The January 2026 rollout of dedicated HCPCS codes for hydrophilic-coated devices is also changing commercial behavior in the United States by improving reimbursement clarity for premium products and by making direct-to-patient fulfillment simpler for suppliers. The intermittent catheters market is also being shaped by user behavior, as compact packaging and discreet formats support routine adherence and reduce avoidance among patients who self-catheterize outside institutional settings. Clinical guideline updates in Europe and infection control pressure in North America continue to favor single-use, coated, and closed-system formats, which keeps premium innovation relevant even as lower-cost devices remain important in price-sensitive countries. Competition in the intermittent catheters market therefore reflects a split between companies building coated technology, compact designs, and reimbursement readiness in developed regions, and suppliers serving lower-cost demand where reuse and supply inconsistency still limit full clinical adoption.

Key Report Takeaways

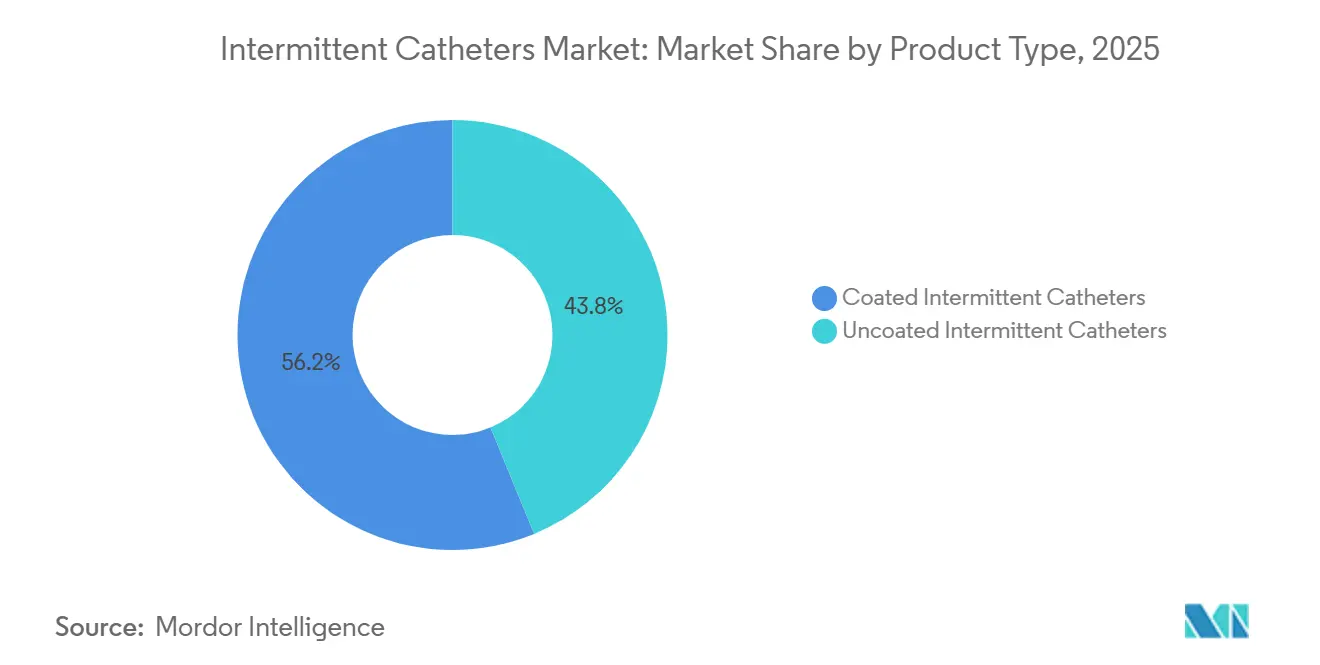

- By product type, coated catheters led with 56.21% revenue share in 2025, while uncoated catheters are forecast to expand at a 6.81% CAGR through 2031.

- By category, male length catheters held 42.83% share in 2025, while pediatric length catheters recorded the highest projected CAGR at 7.94% through 2031.

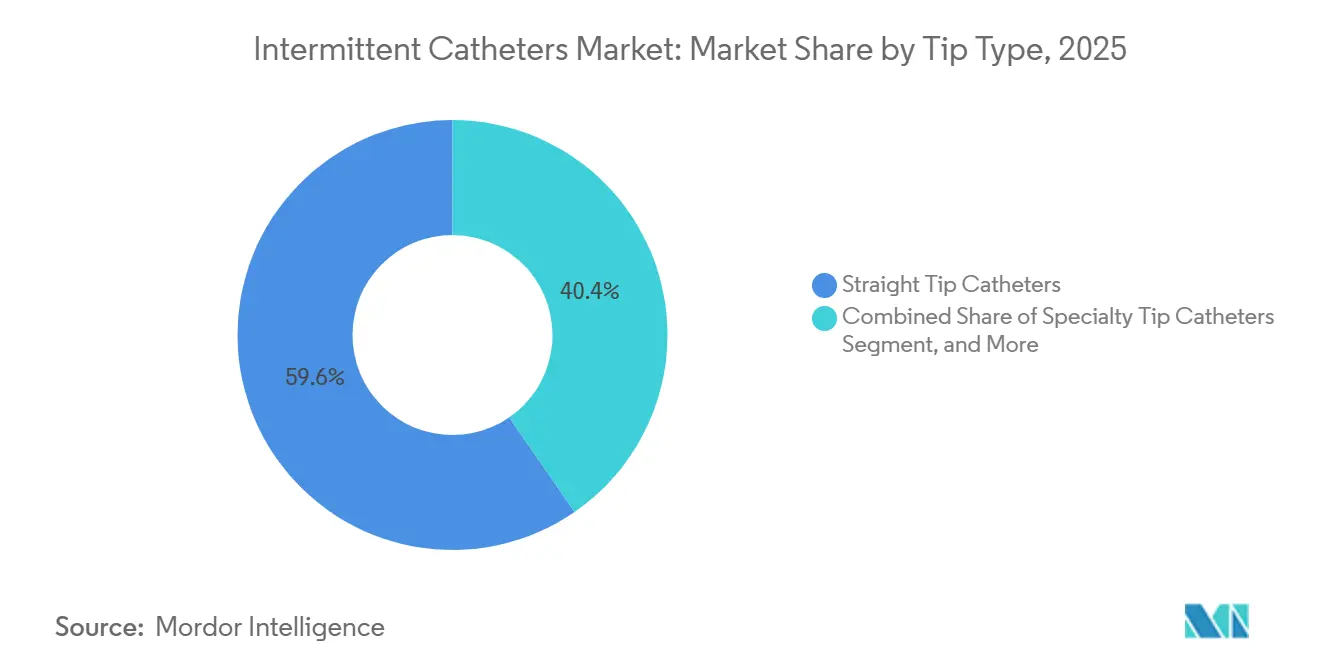

- By tip type, straight tip catheters accounted for 59.64% share in 2025, while coudé tip catheters are advancing at a 7.33% CAGR through 2031.

- By material, PVC commanded 53.2% share in 2025, while silicone is projected to grow at an 8.6% CAGR through 2031.

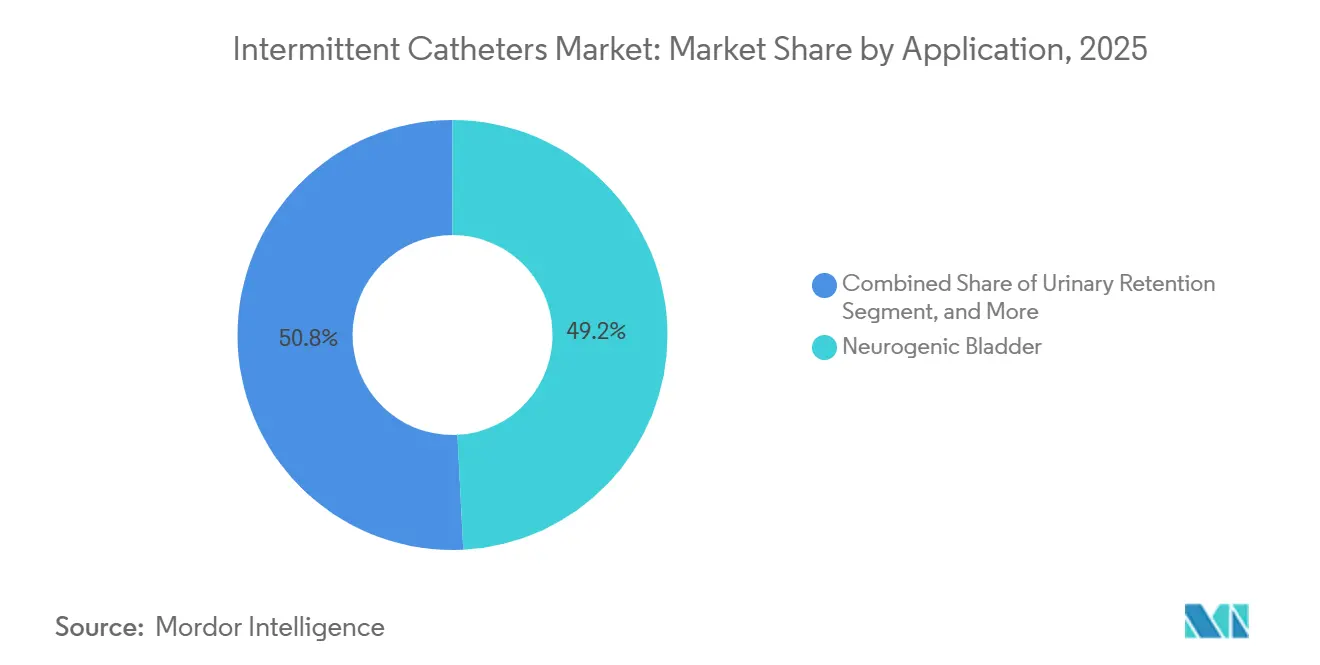

- By application, neurogenic bladder represented 49.2% share in 2025, while urinary incontinence is projected to rise at a 6.7% CAGR through 2031.

- By end user, hospitals held 39.2% share in 2025, while long-term care facilities are forecast to expand at a 7.6% CAGR through 2031.

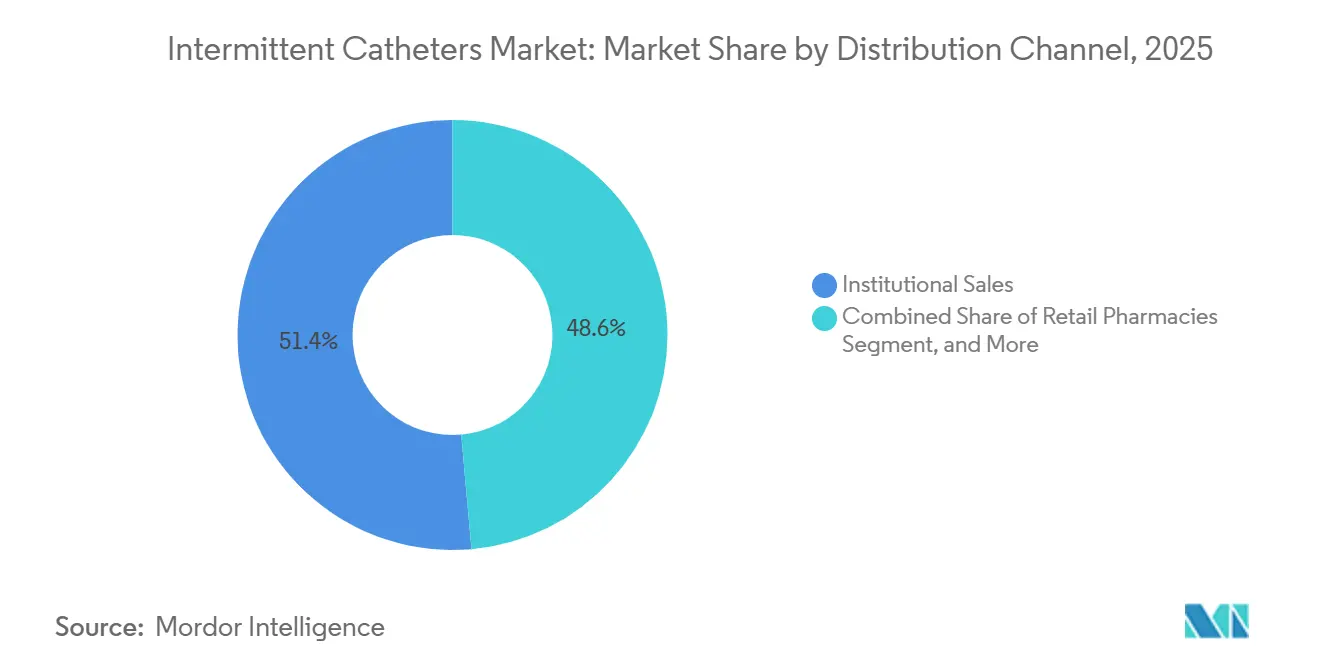

- By distribution channel, institutional sales led with 51.41% share in 2025, while online and direct-to-patient channels are projected to grow at a 6.56% CAGR through 2031.

- By geography, North America held 33.41% share in 2025, while Asia-Pacific recorded the highest projected CAGR at 7.82% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Intermittent Catheters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Neurogenic Bladder Burden | +1.6% | Global, with North America, Europe, and Asia-Pacific as core demand centers | Long term (≥ 4 years) |

| Shift Toward Hydrophilic And Pre-Lubricated Catheters | +1.4% | North America, Northern Europe, and premium Asia-Pacific markets | Medium term (2-4 years) |

| Expansion Of Home-Based Self-Catheterization | +0.9% | North America, Western Europe, and Australia | Medium term (2-4 years) |

| Reimbursement Support For Disposable Intermittent Catheters | +1.1% | United States first, with spillover relevance across Europe | Short term (≤ 2 years) |

| Closed System Adoption In Infection-Sensitive Care Pathways | +0.6% | North America, Europe, and GCC markets | Medium term (2-4 years) |

| Data-Driven Training And Remote Support Improves Adherence | +0.3% | North America, Australia, and Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Neurogenic Bladder Burden

The intermittent catheters market draws durable demand from neurogenic bladder management because bladder dysfunction affects a large share of people with spinal cord injury and a meaningful share of those living with multiple sclerosis. A 2025 study from China showed that intermittent catheterization was the leading bladder management method among chronic spinal cord injury patients, and those using it had fewer urological hospitalizations than those relying on indwelling devices.[1]K. Suda et al., “Quantifying Guideline-Discordant Intermittent Catheterization in Adults Hospitalized With Spinal Cord Injury,” Spinal Cord, nature.com The same clinical pattern supports recurring demand because the patient base does not use catheters occasionally, but over long periods and often across several care settings. The intermittent catheters market is also influenced by the fact that guideline-discordant measurement practices remain common in hospitalized spinal cord injury care, which leaves room for training support, nurse-led education, and adherence tools from manufacturers. Pediatric demand adds to this base because congenital neurological conditions create a long lifetime of catheter use, which supports steady replacement volume rather than short-cycle treatment demand.

Shift Toward Hydrophilic and Pre-Lubricated Catheters

The intermittent catheters market continues to move toward hydrophilic and pre-lubricated devices because these products are associated with lower urethral trauma and better ease of use in routine self-catheterization. Wellspect expands this direction in 2026 with the LoFric Elle Pro and LoFric Origo Pro launches, both built around 12 smooth eyelets intended to support complete bladder emptying in one flow.[2]Wellspect HealthCare, “Wellspect HealthCare Introduces LoFric Elle Pro,” Wellspect Press Release, cision.com Coloplast also reported that its Luja catheter platform was a main contributor to continence care growth, which shows that premium product performance is translating into commercial results rather than remaining only a clinical discussion. The January 2026 CMS coding revision strengthens this shift because coated and non-coated products are no longer treated as one bundled reimbursement category in Medicare billing. The intermittent catheters market is therefore seeing premium conversion supported by both clinical evidence and payment clarity, which is a stronger combination than either factor alone.

Reimbursement Support for Disposable Intermittent Catheters

The intermittent catheters market receives an immediate boost from the new HCPCS codes A4295, A4296, and A4297, which became effective on January 1 2026, for hydrophilic-coated intermittent catheters. This change removes an important commercial barrier because premium devices can now be billed more clearly instead of being compressed inside broader composite categories. The reform also matters operationally because suppliers serving home users can process claims with less ambiguity, which improves the economics of direct-to-patient delivery and recurring supply models. Large manufacturers were already organized around this shift through the Intermittent Catheter Coding Reform Coalition, which shows that reimbursement policy is now a central competitive variable in this category. At the same time, the 2025 OIG audit on improper payments shows that access will remain tied to compliance discipline, so better reimbursement does not remove scrutiny from the intermittent catheters market.[3]U.S. Department of Health and Human Services Office of Inspector General, “Medicare Improperly Paid Suppliers for Intermittent Urinary Catheters,” OIG, oig.hhs.gov

Closed System Adoption in Infection-Sensitive Care Pathways

The intermittent catheters market is also benefiting from the spread of closed-system formats in settings where infection prevention is a purchasing priority. APIC reported 21,525 catheter-associated urinary tract infections across U.S. healthcare facilities in 2023, with an average incremental cost of USD 9,807 per event, which keeps infection control committees focused on avoidable catheter-related harm. This cost burden supports procurement of products that add microbial barriers and cleaner handling during use, especially where quality reporting and facility performance metrics are closely tracked. Hollister responded to this need with its Sleeved IC 3 family, which received FDA 510(k) clearance in October 2025 and uses an integrated sleeve barrier design. The intermittent catheters market is likely to see this driver stay strongest in hospitals and long-term care settings, where infection-sensitive pathways affect both cost and compliance outcomes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Out-Of-Pocket Cost For Premium Catheters | -0.7% | Asia-Pacific, Latin America, Middle East and Africa, and uninsured cohorts in North America | Long term (≥ 4 years) |

| Reuse Behavior And Supply Inconsistency In Price-Sensitive Markets | -0.5% | South Asia, Sub-Saharan Africa, and Latin America | Long term (≥ 4 years) |

| Limited Urology Training And Patient Technique Variability | -0.3% | Global, with stronger concentration in emerging and rural settings | Medium term (2-4 years) |

| Material And Biocompatibility Compliance Burden | -0.2% | Europe and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Cost for Premium Catheters

The intermittent catheters market still faces a meaningful affordability barrier because premium hydrophilic devices cost far more than standard uncoated alternatives in systems with weak reimbursement. This price gap matters most where patients buy supplies directly, because the daily and long-duration nature of use turns a product choice into a sustained financial burden. The OIG audit on improper payments also suggests that tighter compliance reviews can narrow reimbursement access for some U.S. beneficiaries, which may indirectly slow premium mix expansion even in a well-funded system. The result is a structural tradeoff in which some patients reuse catheters to control cost, even though reuse weakens the hygiene advantage that supports single-use intermittent protocols. This restraint remains important for the intermittent catheters market because it limits conversion toward higher-value products and keeps lower-cost formats relevant in large patient populations.

Reuse Behavior and Supply Inconsistency in Price-Sensitive Markets

The intermittent catheters market is also constrained by catheter reuse and by inconsistent product availability in lower-income settings, where clean single-use routines are harder to sustain. A 2025 study from Brazil's SARAH rehabilitation network found strong initial use of clean intermittent catheterization, but lower follow-up adherence because cost, access barriers, and supply reliability remained difficult for many patients. When formal supply channels are weak, patients may delay replacement, reuse devices, or substitute with lower-tier products, which reduces the clinical value of intermittent care in practice. These conditions also push demand back toward basic PVC devices because silicone and polyurethane products are not always available across secondary cities or public systems. The intermittent catheters market, therefore, remains uneven across regions, with clinical guidance supporting best practice more broadly than local supply conditions allow.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Coated Catheters Anchor Premium Revenue

Coated intermittent catheters held 56.21% of the intermittent catheters market share in 2025, which shows how strongly reimbursement support and clinical guidance favor premium formats in established healthcare systems. In the intermittent catheters market, hydrophilic products remain the main volume engine inside coated devices because they are positioned around easier insertion, lower trauma, and cleaner daily use. This is especially visible in North America and Northern Europe, where single-use protocols are more established and where procurement decisions increasingly reflect quality metrics as well as product price. Antimicrobial-coated devices remain a smaller tier, but they are gaining relevance where infection-sensitive care pathways require stronger contamination control during catheter handling and use. The intermittent catheters market also gives coated products a commercial advantage because January 2026 Medicare coding changes now differentiate hydrophilic reimbursement from standard billing categories in a more direct way.

Uncoated catheters are projected to grow at a 6.81% CAGR through 2031, which makes them the fastest-moving product type even though their share base is smaller. That pattern reflects cost substitution in Asia-Pacific, the Middle East and Africa, and Latin America, where affordability still determines much of product choice across hospitals, clinics, and out-of-pocket users. In the intermittent catheters industry, this creates a split between premium innovation in coated devices and steady volume resilience in basic PVC-based products. EU MDR documentation also needs to weigh more heavily on smaller suppliers of uncoated products because compliance costs are harder to absorb in lower-margin categories. As a result, the intermittent catheters market is likely to keep coated devices at the center of premium revenue while uncoated products remain essential for access and volume growth in price-sensitive settings.

By Category: Pediatric Demand Gains Strategic Weight

Male length catheters accounted for 42.83% share of the intermittent catheters market size in 2025, reflecting the strong male skew in spinal cord injury prevalence and the large installed base of adult male self-catheterization users. This leading position is supported by the fact that spinal cord injury cohorts in large clinical datasets continue to show a high male representation, which feeds long-term demand for standard male length products. Female length products remain strategically important because manufacturers are using compact designs, discreet packaging, and easier handling features to improve adoption among daily users outside institutional settings. Coloplast reported strong uptake for the Luja female catheter in France and the United Kingdom during Q2 2025/26, which suggests that user-centered product design is translating into sales momentum in mature European markets. The intermittent catheters market is therefore seeing category development shaped by anatomy, daily routine, and packaging expectations rather than by length alone.

Pediatric length catheters are projected to rise at a 7.94% CAGR through 2031, which makes them the fastest-growing category in the intermittent catheters market. This growth is supported by expanding pediatric neurology and rehabilitation services, particularly in developing countries where congenital neurological conditions continue to create long-duration catheter users. Children diagnosed with spina bifida or neurogenic bladder often continue catheter use into adulthood, so early diagnosis supports many years of recurring demand rather than a short treatment cycle. The intermittent catheters market also benefits when pediatric lines incorporate smaller diameters, gentler insertion features, and child-friendly packaging, because long-term adherence depends on routine acceptability as much as clinical need. That combination keeps the pediatric segment under stronger strategic focus than its current size alone would suggest.

By Tip Type: Straight Tip Products Hold the Core Base

Straight tip catheters commanded 59.64% share in 2025, which reflects their broad suitability across standard urethral anatomies and their role as the default option in many training protocols. In the intermittent catheters market, straight tip formats remain the main entry point because clinicians commonly begin patients on simpler devices before considering more specialized configurations. Their leadership is also helped by scale, since large hospital and institutional purchasing programs often prefer products that cover a wide range of routine needs with less complexity. This keeps straight tip products central to the recurring demand base across both initial prescriptions and repeat supply cycles. The intermittent catheters market therefore continues to rely on straight tip devices as its broadest-volume tip category.

Coudé tip catheters are projected to expand at a 7.33% CAGR through 2031, driven by patients with benign prostatic hyperplasia, urethral strictures, and post-surgical anatomical difficulty. CMS requires explicit medical necessity documentation for coudé use under the relevant hydrophilic code, which supports tip-specific reimbursement discipline and clearer clinical justification in the U.S. system. Specialty tip products remain smaller, but they are building a place in pediatric and complex neurological care where softer or more tailored designs can reduce insertion difficulty. Remote consultations also support this segment because patients with anatomy-related challenges can reach specialists faster and move to more suitable tip types without as many in-person visits. In the intermittent catheters industry, that gives coudé and specialty formats a narrower but steadily deepening role within premium and clinically differentiated product lines.

By Material: Silicone Builds Momentum in Sensitive Use Cases

PVC held 53.23% share in 2025, which kept it as the leading material in the intermittent catheters market because of its cost advantage, long manufacturing history, and wide availability. PVC remains important in institutional and lower-cost settings where affordability shapes the first product decision and where supply networks are built around established high-volume formats. Latex still retains some volume in developing regions for the same cost reason, but it faces increasing replacement pressure as allergy awareness and facility policies become stricter. Polyurethane and polyethylene are developing smaller positions in specialty applications where flexibility and tighter design control matter. The intermittent catheters market therefore still depends on PVC for scale, even as the premium mix shifts elsewhere.

Silicone is projected to grow at an 8.62% CAGR through 2031, the fastest pace among material categories in the intermittent catheters market. Its rise is linked to stronger awareness of latex allergy, concern around biocompatibility, and user preference for softer materials in repeated daily catheterization routines. This matters especially in home care, where comfort, ease of insertion, and body compatibility influence whether patients stay consistent with prescribed use over time. Regulatory frameworks also reinforce the shift because EU MDR and ISO 10993 expectations favor material evidence, post-market follow-up, and documentation discipline that premium suppliers are better positioned to provide. As a result, the intermittent catheters market is gradually moving toward silicone and other higher-specification materials in its premium tiers while PVC retains its volume base.

By Application: Neurogenic Bladder Keeps Its Lead While Use Broadens

Neurogenic bladder represented 49.19% share in 2025, which confirms that it remains the central demand pool in the intermittent catheters market. This position is structurally stable because spinal cord injury and multiple sclerosis management often requires repeated catheterization over long periods, making usage less discretionary than in several other application areas. Germany's revised 2026 guidance also reinforces clean intermittent catheterization as the preferred option for neurogenic lower urinary tract dysfunction, which supports procurement and physician confidence across institutional care in Europe. The intermittent catheters market continues to derive much of its recurring replacement volume from this application because many users remain in long-term care pathways rather than short procedure-based episodes. That keeps neurogenic bladder at the center of portfolio planning for leading manufacturers.

Urinary incontinence is forecast to grow at a 6.73% CAGR through 2031, making it the fastest-rising application in the intermittent catheters market. Its rise points to demand broadening beyond spinal injury and into age-related lower urinary tract dysfunction, ambulatory recovery, and quality-of-life-driven use cases. Prostate surgery, urinary retention, and procedure-related needs also support this expansion because more patients now move through recovery with an expectation of cleaner, more discreet, single-use bladder management. In older male populations, post-prostatectomy and post-intervention care are creating a more visible bridge between urology procedures and intermittent catheter adoption. This means the intermittent catheters market is not losing its neurological core, but it is widening its application base in ways that create new room for compact and patient-managed product formats.

By End User: Long-Term Care Becomes the Fastest-Moving Setting

Hospitals held 39.23% share in 2025, which kept them as the largest end-user group in the intermittent catheters market because they remain the main point of diagnosis, first prescription, and patient training. Hospital settings also concentrate nurse specialists and urology care teams, which gives them a lasting role in selecting product type, coating format, tip configuration, and user education. This influence extends beyond the inpatient episode because the first product experience often shapes later refill behavior in home use. Hospitals also manage high-acuity patients who require closer monitoring before transitioning to self-care or lower-intensity environments. The intermittent catheters market therefore still depends on hospitals as the main channel through which product choice is established.

The intermittent catheters market size for long-term care facilities is projected to expand at 7.58% CAGR between 2026 and 2031, the fastest rate among end users. This reflects the aging of chronic care populations and the stronger emphasis on catheter-associated infection prevention inside nursing and residential care settings. Home care is also becoming strategically central because the recurring demand base increasingly comes from self-catheterizing users who want portable formats and reliable refill pathways. Ambulatory surgical centers and specialty clinics add to this shift by supporting post-procedural use and chronic neurological management outside traditional hospital beds. As a result, the intermittent catheters market is moving toward a more distributed care model, even though hospitals still anchor the largest single end-user share.

By Distribution Channel: Direct Fulfillment Gains Ground

Institutional sales held 51.41% share in 2025, which kept them as the largest distribution route in the intermittent catheters market because hospital systems and long-term care facilities still buy in large contracted volumes. This channel benefits from predictable ordering, formal supplier relationships, and a strong fit with first-use prescription environments. Institutional procurement also favors companies that can meet compliance, training, and documentation expectations across large care networks. That gives scale suppliers an advantage, especially in developed markets where reimbursement and product differentiation increasingly intersect. The intermittent catheters market therefore remains anchored by institutional demand even as purchasing behavior begins to diversify.

Online and direct-to-patient channels are projected to grow at a 6.56% CAGR through 2031, which makes them the fastest-rising path in the intermittent catheters market. The change is closely linked to home self-catheterization, subscription supply models, and clearer Medicare coding that helps hydrophilic claims move through direct fulfillment more smoothly from 2026 onward. Manufacturers are also investing in refill reminders, remote nurse support, and adherence tools, which strengthens retention in channels that are built around recurring reorder behavior rather than one-time institutional contracts. Retail pharmacies still matter for out-of-pocket users, especially in developing countries, but they face pressure from online convenience and price comparison. This leaves the intermittent catheters market with a mixed channel structure where institutional sales lead today while direct-to-patient delivery becomes more strategically important.

Geography Analysis

North America held 33.41% of intermittent catheters market share in 2025, which made it the largest regional block by value. The region leads because the United States combines established reimbursement, high single-use adoption, and a large diagnosed base of neurogenic bladder patients who use intermittent devices over long periods. The January 2026 HCPCS reform is especially important because it gives hydrophilic-coated products clearer billing pathways through codes A4295, A4296, and A4297, which supports coated conversion and direct-to-patient supply. Canada adds stability through structured provincial reimbursement for spinal cord injury and neurogenic bladder care, while Mexico adds a smaller but growing private healthcare demand base. The intermittent catheters market in North America also benefits from earlier adoption of digital support tools that help younger and active self-catheterizing patients stay on routine supply schedules.

Europe was the second-largest regional cluster in the intermittent catheters market in 2025, led by Germany, the United Kingdom, and France. Coloplast identified these countries as key contributors to continence care growth in its H1 2025/26 reporting, which underlines the purchasing strength of their major health systems. Germany's revised 2026 clinical guidance gives the region added institutional support by positioning clean intermittent catheterization as the preferred standard for neurogenic lower urinary tract dysfunction. At the same time, the EU MDR transition is raising documentation and follow-up demands, which gradually favors large suppliers with stronger regulatory infrastructure. Southern and Eastern Europe still offer room for expansion, especially where physician training and patient education remain less developed than in Northern Europe.

The intermittent catheters market size for Asia-Pacific is projected to expand at 7.82% CAGR through 2031, the fastest regional pace in this study. China remains central to that growth because 2025 clinical evidence showed intermittent catheterization as the leading bladder management method among chronic spinal cord injury patients, with fewer urological hospitalizations than indwelling use. India adds momentum through a combination of spina bifida-linked need, broader urology service availability, and rehabilitation access beyond the largest metro centers. Japan supports steady demand through its aging population and its established use base in urinary incontinence and post-prostatectomy care. South Korea and Australia represent premium regional pockets where hydrophilic and compact formats fit well with higher healthcare standards and greater acceptance of self-managed use. Middle East and Africa and South America remain smaller overall, but the GCC shows premium demand growth while Brazil provides a strong clinical adoption base for recurring CIC volume through rehabilitation and public hospital channels.

Competitive Landscape

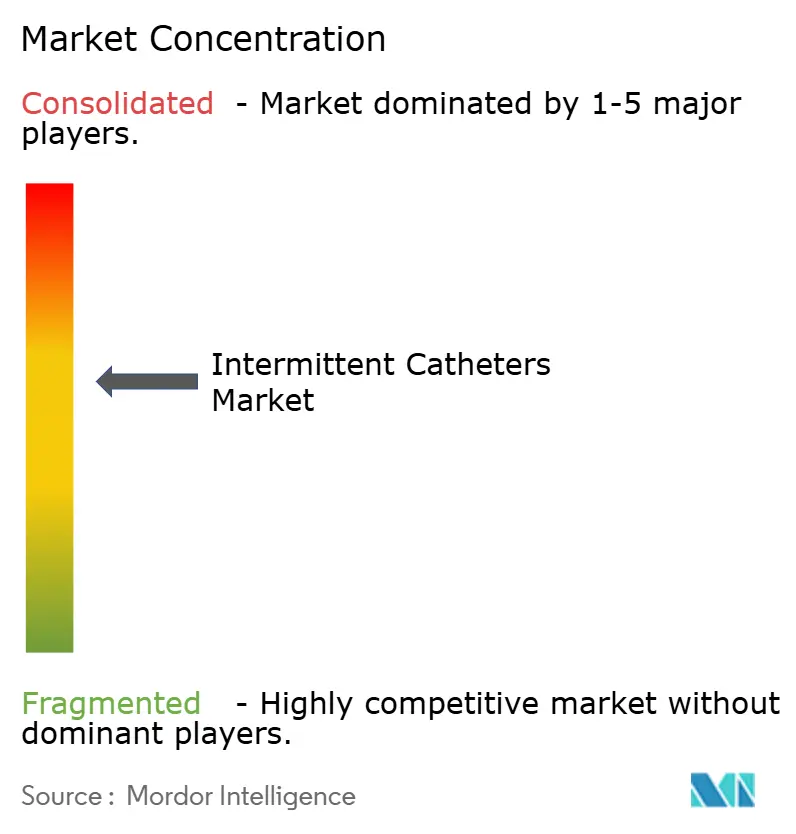

The intermittent catheters market is moderately consolidated, with Coloplast, ConvaTec, Hollister, Becton Dickinson, and Wellspect forming the most visible group in premium coating technology, reimbursement engagement, and product innovation. Their position is reinforced by the fact that they were aligned around the U.S. coding transition through the Intermittent Catheter Coding Reform Coalition, which shows coordinated attention to reimbursement architecture as a competitive tool. Even so, the intermittent catheters market is not closed, because lower-cost regional suppliers still serve a wide installed base in Asia-Pacific, Latin America, and parts of the Middle East and Africa where price matters more than premium features. This creates a dual structure in which premium players compete on coating performance, complete emptying design, compact packaging, and evidence generation, while volume-focused suppliers compete on affordability and reach. The result is a market where leadership is strongest in the high-value segments, but fragmentation remains visible in lower-cost and less reimbursed product tiers.

Coloplast continues to set the pace in premium continence care, with 7% organic growth in H1 2025/26 supported by its Luja platform and its Micro-hole Zone Technology rollout across 13 markets. Wellspect is also active, as it launches LoFric Elle Pro in March 2026 and LoFric Origo Pro in June 2026, both designed around 12 smooth eyelets for complete bladder emptying in one flow. ConvaTec is reshaping its position through the Accelerate strategy announced in April 2026, with an active launch pipeline that includes GentleCath Air Pocket, GentleCath Air Set, and male compact formats for the second half of 2026. Hollister adds a different angle through the Sleeved IC 3 family, which received FDA clearance in October 2025 and brings a sleeve barrier concept into home intermittent use. These moves show that the intermittent catheters market is being shaped by differentiated product design rather than by price competition alone at the leading edge.

Bactiguard adds a further layer through coating intellectual property and partnership-based commercialization, which points to licensing as a viable route in adjacent catheter technologies. Becton Dickinson remains relevant through manufacturing scale and broader catheter capabilities, supported by its January 2025 investment in U.S. production capacity. The intermittent catheters market still has open space in adherence support platforms and in home-use antimicrobial concepts, where no single model has become dominant. Regulatory demands under FDA device rules, ISO biocompatibility expectations, and European compliance standards continue to favor companies with strong quality systems and the ability to document performance over time. That keeps competition active, but it also means the intermittent catheters market rewards scale, evidence, and reimbursement readiness more than simple product availability.

Intermittent Catheters Industry Leaders

B. Braun SE

Becton, Dickinson and Company

Boston Scientific Corporation

Cardinal Health, Inc.

Teleflex Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Wellspect HealthCare launched LoFric Origo Pro, a single-use hydrophilic intermittent catheter for men featuring 12 smooth Pro eyelets engineered for complete bladder emptying in one uninterrupted flow, directly targeting residual urine as a primary UTI risk factor. The product is being gradually introduced across markets through 2026.

- May 2026: Coloplast A/S reported H1 2025/26 interim results, with Continence Care delivering 7% organic growth driven by the Luja catheter portfolio in Europe, including the UK, France, and Germany, and the United States. Full-year guidance remained at 5-6% organic revenue growth.

- April 2026: ConvaTec announced its Accelerate strategy at its Capital Markets Day, targeting 6-8% organic revenue growth from 2027 and committing to an active launch pipeline including GentleCath Air Pocket, GentleCath Air Set, and male compact catheter formats expected in H2 2026.

- March 2026: Wellspect HealthCare introduced LoFric Elle Pro, a hydrophilic, ready-to-use intermittent catheter for women with 12 smooth Pro eyelets designed for complete bladder emptying in a single free flow, extending multi-eyelet technology to the female catheter segment.

Global Intermittent Catheters Market Report Scope

An intermittent catheter is a temporary, flexible medical tube inserted into the bladder through the urethra to drain urine and removed immediately afterward. Primarily used by individuals with spinal cord injuries, urinary incontinence, or neurogenic bladder dysfunction, these catheters allow patients to self-catheterize multiple times a day to maintain bladder health.

The Intermittent Catheters Market is segmented across multiple dimensions. By product type, the market includes Coated Intermittent Catheters, such as Hydrophilic Coated Catheters and Antimicrobial Coated Catheters, and Uncoated Intermittent Catheters, which comprise PVC Intermittent Catheters and Latex Intermittent Catheters. By category, the market is divided into Male Length Catheters, Female Length Catheters, and Pediatric Length Catheters. Based on tip type, products include Straight Tip Catheters, Coudé Tip Catheters, and Specialty Tip Catheters. By material, the market spans PVC, Silicone, Latex, Polyurethane, and Polyethylene. In terms of application, intermittent catheters are used for conditions such as Neurogenic Bladder, Urinary Retention, Urinary Incontinence, Spinal Cord Injury, Prostate Surgery, and Multiple Sclerosis. By end user, the market serves Hospitals, Home Care Settings, Ambulatory Surgical Centers, Long-Term Care Facilities, and Specialty Clinics. By distribution channel, products are supplied through Institutional Sales, Retail Pharmacies, and Online and Direct-To-Patient platforms. Geographically, the market spans North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East & Africa (GCC, South Africa, Rest of Middle East & Africa), and South America (Brazil, Argentina, Rest of South America).

| Coated Intermittent Catheters | Hydrophilic Coated Catheters |

| Antimicrobial Coated Catheters | |

| Uncoated Intermittent Catheters | PVC Intermittent Catheters |

| Latex Intermittent Catheters |

| Male Length Catheters |

| Female Length Catheters |

| Pediatric Length Catheters |

| Straight Tip Catheters |

| Coudé Tip Catheters |

| Specialty Tip Catheters |

| PVC |

| Silicone |

| Latex |

| Polyurethane |

| Polyethylene |

| Neurogenic Bladder |

| Urinary Retention |

| Urinary Incontinence |

| Spinal Cord Injury |

| Prostate Surgery |

| Multiple Sclerosis |

| Hospitals |

| Home Care Settings |

| Ambulatory Surgical Centers |

| Long-Term Care Facilities |

| Specialty Clinics |

| Institutional Sales |

| Retail Pharmacies |

| Online and Direct-To-Patient |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Coated Intermittent Catheters | Hydrophilic Coated Catheters |

| Antimicrobial Coated Catheters | ||

| Uncoated Intermittent Catheters | PVC Intermittent Catheters | |

| Latex Intermittent Catheters | ||

| By Category | Male Length Catheters | |

| Female Length Catheters | ||

| Pediatric Length Catheters | ||

| By Tip Type | Straight Tip Catheters | |

| Coudé Tip Catheters | ||

| Specialty Tip Catheters | ||

| By Material | PVC | |

| Silicone | ||

| Latex | ||

| Polyurethane | ||

| Polyethylene | ||

| By Application | Neurogenic Bladder | |

| Urinary Retention | ||

| Urinary Incontinence | ||

| Spinal Cord Injury | ||

| Prostate Surgery | ||

| Multiple Sclerosis | ||

| By End User | Hospitals | |

| Home Care Settings | ||

| Ambulatory Surgical Centers | ||

| Long-Term Care Facilities | ||

| Specialty Clinics | ||

| By Distribution Channel | Institutional Sales | |

| Retail Pharmacies | ||

| Online and Direct-To-Patient | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in intermittent catheters through 2031?

Growth is being supported by the rise in neurogenic bladder cases, wider use of clean intermittent catheterization, stronger adoption of hydrophilic products, and clearer U.S. reimbursement from the January 2026 HCPCS coding update.

How large is the intermittent catheters space expected to become by 2031?

The intermittent catheters market is forecast to reach USD 3.84 billion by 2031, rising from USD 2.86 billion in 2026 at a 6.05% CAGR over 2026-2031.

Which product category leads revenue today?

Coated catheters led the intermittent catheters market in 2025 with a 56.21% share, supported by premium positioning, clinical preference, and reimbursement support in developed markets.

Which end-user setting is growing the fastest?

Long-term care facilities are projected to grow the fastest at a 7.58% CAGR through 2031 as aging care populations and infection prevention requirements push higher single-use adoption.

Which region is growing the fastest for intermittent catheters?

Asia-Pacific is projected to post the fastest growth at a 7.82% CAGR through 2031, supported by expanding rehabilitation access, rising urology services, and a broadening patient base.

Page last updated on: