Interactive Voice Response Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 5.39 Billion |

| Market Size (2030) | USD 7.07 Billion |

| Growth Rate (2025 - 2030) | 5.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Interactive Voice Response Market Analysis by Mordor Intelligence

The interactive voice response market or the IVR market size stands at USD 5.39 billion in 2025 and is forecast to reach USD 7.07 billion by 2030, reflecting a 5.56% CAGR over the period. Demand expands as cloud-native contact center architectures converge with conversational artificial intelligence and voice biometrics, delivering lower total cost of ownership and stronger fraud prevention. Large enterprises drive early adoption, yet small and medium enterprises accelerate growth through subscription-based platforms that remove infrastructure barriers. Vertical specialization intensifies particularly in healthcare remote triage and banking fraud mitigation, fueling solution upgrades and service contracts. Competitive dynamics remain moderate as incumbents defend installed bases while cloud-first challengers introduce API-centric offerings and predictive analytics capabilities.

Key Report Takeaways

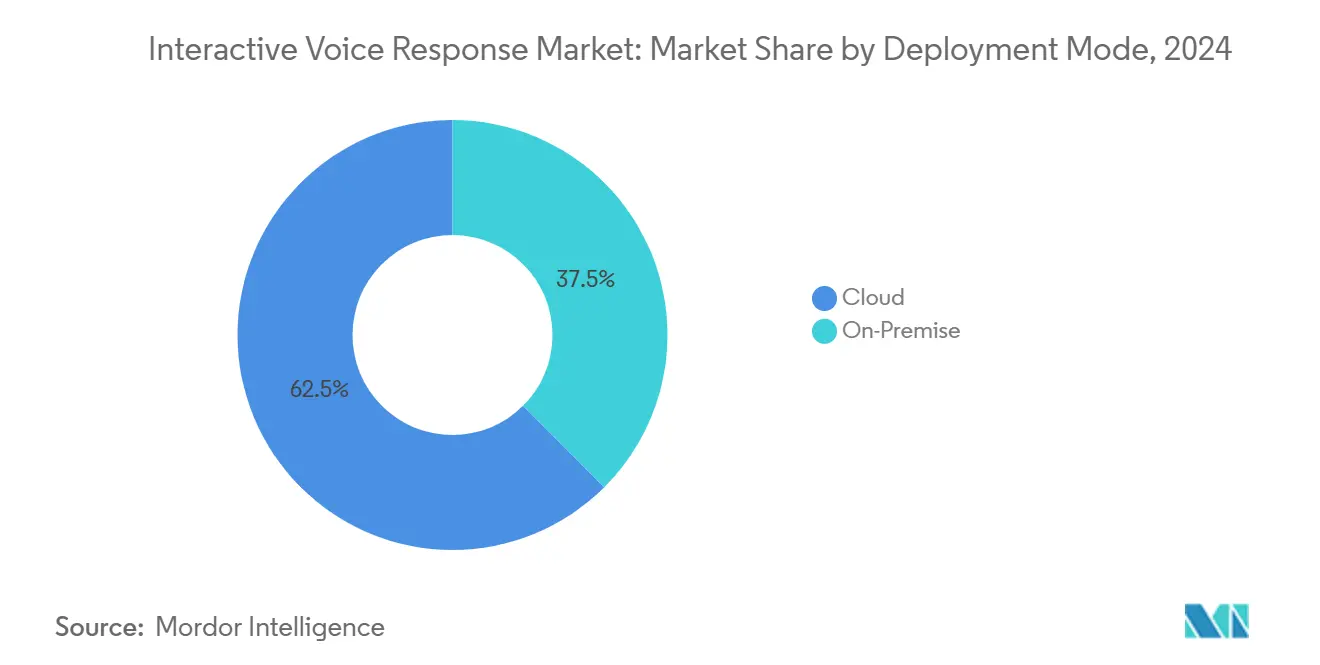

- By deployment mode, cloud captured 62.48% of the interactive voice response market share in 2024 and is projected to advance at a 5.97% CAGR through 2030.

- By enterprise size, large enterprises captured 57.91% of the interactive voice response market share in 2024; small and medium-sized enterprises are projected to expand at a 5.89% CAGR to 2030, outpacing the growth of large enterprises.

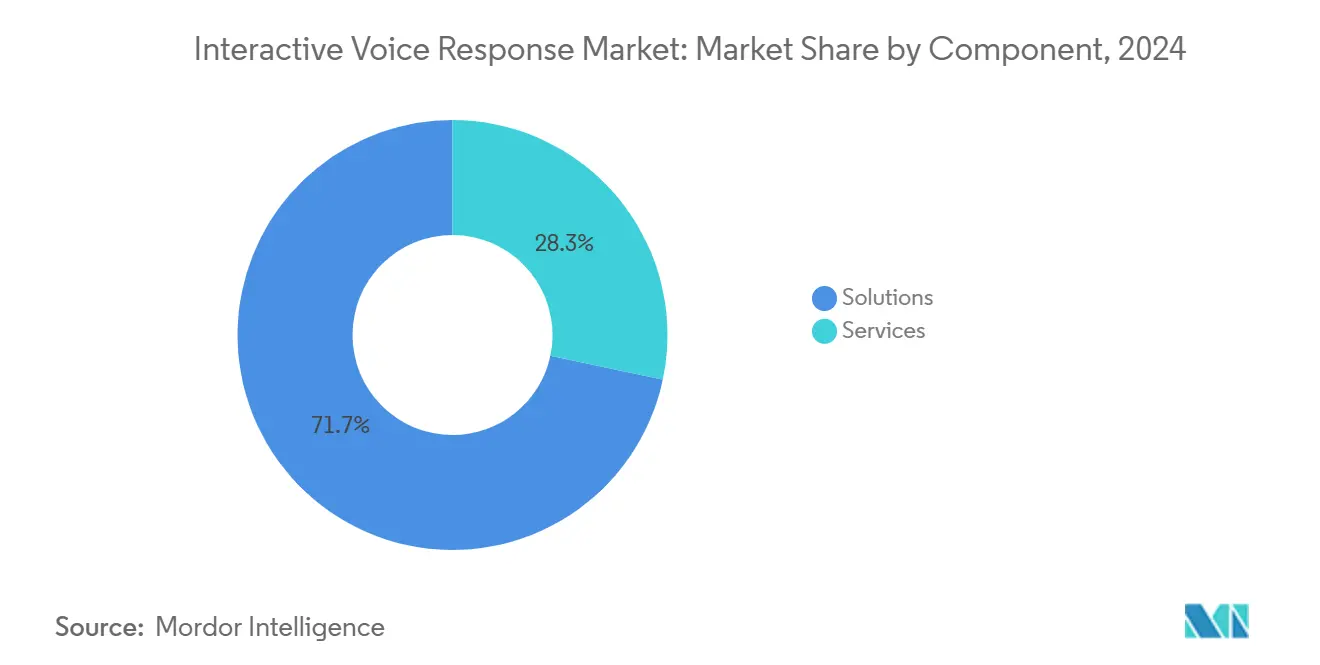

- By component, solutions captured 71.68% of the interactive voice response market share in 2024; services are expected to grow at a 6.11% CAGR through 2030, reflecting rising demand for integration expertise.

- By end-user industry, Banking, Financial Services, and Insurance captured 29.68% of the interactive voice response market share in 2024; healthcare and life sciences are forecast to record a 6.73% CAGR and emerge as the fastest-growing vertical through 2030.

- By end-user industry, North America captured 38.17% of the interactive voice response market share in 2024; Asia Pacific is projected to advance at a 6.44% CAGR through 2030.

Global Interactive Voice Response Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cloud-Based Contact Centers Adoption | +1.2% | Global, North America and Europe acceleration | Medium term (2-4 years) |

| Shift Toward Conversational AI-Enabled IVR | +0.8% | North America and Asia-Pacific core | Long term (≥ 4 years) |

| Demand for 24x7 Customer Self-Service | +0.9% | Global | Short term (≤ 2 years) |

| Integration With Omnichannel CX Platforms | +1.1% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Adoption of Voice Biometrics for Authentication | +0.7% | Global, early gains in banking sectors | Medium term (2-4 years) |

| Growing Usage in Healthcare Remote Triage | +0.6% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Cloud-Based Contact Centers Adoption

Enterprises continue to migrate IVR workloads to cloud platforms because subscription pricing removes capital-expenditure barriers and allows for elastic scaling during demand spikes. Organizations report 25-40% lower total cost of ownership and faster access to AI speech analytics after switching from on-premise systems. Cloud vendors also deliver built-in compliance certifications that shorten procurement cycles for regulated industries and support remote administration that proved resilient during recent disruptions.[1]RingCentral Investor Relations, “RingCentral Investor Presentation Q3 2024,” investors.ringcentral.com Smaller enterprises benefit the most, as they can deploy enterprise-grade IVR within days rather than months. The migration trend accelerates in North America and Western Europe, where broadband reliability and cloud maturity are highest. As a result, cloud adoption contributes the largest positive impact to the forecasted CAGR.

Shift Toward Conversational AI-Enabled IVR

Natural-language engines now achieve intent-recognition accuracy of nearly 95% for domain-trained applications, allowing callers to speak in everyday language instead of using rigid menus. Financial institutions using conversational IVR deflect up to 60% of inquiries from agents and reduce the average handle time by 35%, resulting in measurable cost savings.[2]MIT Computer Science and Artificial Intelligence Laboratory, “Conversational AI in Healthcare Applications,” csail.mit.edu Continuous-learning loops refine responses without disruptive re-programming, supporting agile iteration of call flows. Enterprises overlay emotion detection to route frustrated callers to live agents, preserving satisfaction scores. These capabilities spur long-term demand across North America and the Asia Pacific.

Demand for 24x7 Customer Self-Service

Customer expectations for instant resolution drive organizations to keep voice self-service available around the clock. Companies that extend IVR beyond business hours report 40% reductions in after-hours staffing while maintaining service levels.[3]Salesforce, “State of Service Report 2024,” salesforce.com Global brands utilize follow-the-sun models, enabling callers in any time zone to reach automated assistance without incurring premium labor costs. Healthcare providers leverage an always-on IVR for appointment scheduling and prescription refills, freeing clinicians to focus on higher-value care. Persistent availability also strengthens business continuity plans because automated workflows continue to function during local outages. The driver exerts near-term influence as enterprises race to meet rising service benchmarks.

Integration With Omnichannel CX Platforms

Modern IVR operates as a node in unified customer-experience stacks that include chat, email, and social messaging. Seamless context transfer between channels increases first-call-resolution rates by approximately 25% and reduces customer effort scores by 30%. Integrations with customer-relationship-management systems provide agents with full interaction histories, enabling personalized routing. Analytics correlate voice patterns with digital behavior to guide proactive outreach campaigns. North American and European enterprises lead adoption, with Asia Pacific deployments growing as omnichannel maturity increases. This integration driver materially expands software and services revenue tied to optimization projects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complexity in Multilingual Natural Language Processing | -0.7% | Global, notably Asia-Pacific and Europe | Long term (≥ 4 years) |

| Rising Consumer Preference for Digital-First Support | -0.9% | North America and Europe, expanding globally | Medium term (2-4 years) |

| Data Privacy and Sovereignty Regulations | -0.5% | Europe and North America, spillover globally | Short term (≤ 2 years) |

| Legacy On-Premise Capex Lock-In for Large Enterprises | -0.4% | Global, concentrated in established markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complexity in Multilingual Natural Language Processing

Code-switching and dialectal variance degrade speech recognition performance, forcing service providers to maintain separate language models that increase costs. Performance gaps lead to inconsistent experiences, particularly in Southeast Asia and parts of Europe, where callers often mix languages within a single interaction. Enterprises often rely on keypad inputs, thereby diluting the value of conversational AI. Data collection for underrepresented dialects is resource-intensive and subject to privacy regulations. The technical hurdle slows long-term IVR expansion into linguistically diverse markets.

Rising Consumer Preference for Digital-First Support

Millennials and Generation Z customers prefer chat, messaging, and self-service portals over voice calls, challenging the traditional use of IVRs. Surveys show 73% of millennials opt for non-voice channels when solving issues, prompting companies to divert budgets toward chatbots. Reduced call volumes can weaken ROI for new IVR deployments. Firms must balance investments across channels to avoid alienating older demographics who still rely on voice. This restraint exerts medium-term pressure on market growth trajectories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Infrastructure Drives Market Evolution

Cloud models captured 62.48% of the interactive voice response market in 2024 as enterprises prioritized operational flexibility and opex funding. This dominance reflects the economic attractiveness of subscription pricing, reduced hardware maintenance, and rapid feature rollouts delivered via software-as-a-service. Retailers, broadcasters, and online education platforms appreciate the ability to scale ports dynamically during promotions or live events, ensuring service continuity without the need for costly over-provisioning. Vendors bundle compliance certifications such as SOC 2 and ISO 27001, accelerating procurement cycles for regulated industries that would otherwise confront lengthy audits.

On-premise deployments persist in heavily regulated sectors where data sovereignty or legacy integrations require local control. Banks and government agencies often retain existing telephony equipment, layering secure gateways that interface with cloud analytics engines for speech recognition and call classification. Hybrid models emerge as pragmatic compromises, keeping sensitive data on-site while offloading less regulated traffic to cloud nodes. This architecture supports phased migration strategies that minimize downtime and protect sunk investments, explaining the continued, though declining, share for on-premise solutions within the Interactive Voice Response market.

By Enterprise Size: SME Adoption Accelerates Through Cloud Accessibility

Large enterprises held a 57.91% market share in 2024, leveraging dedicated IT teams to customize complex call flows, deploy voice biometrics, and integrate customer relationship management databases. Multinational businesses often operate multi-tenant deployments that support language localization and regulatory segmentation across jurisdictions. Sizeable contact-center headcounts also justify investment in advanced workforce-management analytics embedded in premium IVR suites.

Small and medium enterprises gain momentum with a projected 5.89% CAGR to 2030, buoyed by no-code configuration panels and rapid provisioning through web portals. Subscription tiers align capacity with seasonal demand, eliminating the need for over-provisioning costs. Pre-built templates for appointment booking or order tracking allow non-technical staff to deploy within days, democratizing access to enterprise-class functionality. Community clinics, boutique financial advisers, and niche ecommerce stores leverage these capabilities to compete on customer experience without incurring heavyweight infrastructure costs, widening the addressable interactive voice response market.

By Component: Services Growth Reflects Implementation Complexity

Software solutions accounted for 71.68% of 2024 revenue as natural-language engines, routing algorithms, and analytics dashboards form the core of modern IVR capabilities. Continuous software innovation, particularly in conversational AI modules, drives recurring license and upgrade revenue, maintaining the solutions segment's dominance within the interactive voice response market. Vendors emphasize developer APIs and microservices architectures that allow incremental feature activation, facilitating agile change management for enterprises that wish to pilot new use cases before full rollout.

Services revenue is expected to expand at a 6.11% CAGR to 2030 as integration complexity deepens with omnichannel frameworks, robotic process automation, and security layers. Professional services teams map call-flow logic to business processes, ensuring regulatory compliance and optimizing containment rates. Managed services provide round-the-clock monitoring, speech-model retraining, and capacity scaling, offering resource-constrained enterprises predictable cost structures. Mid-market customers, in particular, rely on managed offerings to offset their scarce IT talent, thereby reinforcing demand for services across all regions of the interactive voice response market.

By End-User Industry: Healthcare Emerges as Growth Leader

The banking, financial services, and insurance sectors retained 29.68% of theinteractive voice response (IVR) market in 2024, as institutions utilized IVR for balance inquiries, transaction authentication, and fraud alerts. Voice biometrics combat roughly USD 11 billion in annual voice fraud, reducing manual verification steps and streamlining customer journeys. Regulatory mandates for accessible service channels further solidify IVR's role within core banking operations.

The healthcare and life sciences sector is forecast to grow at a 6.73% CAGR through 2030, propelled by the expansion of telehealth and remote patient monitoring. IVR lines conduct preliminary symptom assessments, triage calls, and coordinate prescription refills, alleviating clinician workload and extending reach into rural areas. Hospitals integrate IVR with electronic health record platforms to update appointment calendars in real time, minimizing no-show rates. The pandemic’s push toward virtual care solidified funding for such initiatives, positioning healthcare as the fastest-expanding vertical in the interactive voice response market.

Geography Analysis

North America commanded 38.17% of 2024 revenue, benefitting from mature contact-center ecosystems and codified regulations that prescribe accessible communication. U.S. enterprises leverage advanced natural-language frameworks and voice biometric security, achieving high containment rates while adhering to Americans with Disabilities Act requirements. Canadian institutions deploy bilingual English-French IVR systems to comply with federal language laws, demonstrating regional customization within the interactive voice response market. Regulatory clarity fosters confidence in cloud migration, accelerating the adoption of AI-enhanced platforms.

The Asia Pacific region exhibits the highest regional CAGR of 6.44% through 2030, driven by digital government mandates and widespread mobile penetration. Enterprises in India and Indonesia deploy multilingual IVR to handle diverse dialects at scale, although linguistic variation tests current speech models. China’s financial sector integrates IVR with super-app ecosystems, allowing callers to navigate from voice menus to in-app chat without losing context. Government agencies across Southeast Asia roll out citizen hotlines for social services, further expanding the interactive voice response market base.

Europe experiences moderate growth as the General Data Protection Regulation and forthcoming AI Act impose stringent data governance obligations. Enterprises select vendors with demonstrable compliance credentials, tilting procurement toward established providers with robust privacy controls. Germany and the United Kingdom lead adoption in manufacturing and finance, respectively, while Scandinavian utilities deploy IVR to automate outage updates in remote regions. Southern European markets rely on cloud deployments to circumvent capital constraints, while maintaining local data centers to comply with sovereignty requirements.

Competitive Landscape

The Iinteractive voice response market is moderately concentrated. Genesys, Avaya, and Cisco maintain significant installed bases through broad portfolios that span telephony hardware and cloud software, creating high switching costs. Twilio, Five9, and RingCentral challenge incumbents by offering developer-centric APIs and usage-based billing that resonate with digitally native firms and small businesses alike. Differentiation hinges on the quality of conversational AI, platform openness, and vertical compliance toolkits, rather than basic call routing.

Mergers and acquisitions are demonstrating a shift toward workflow automation and analytics. Five9’s 2024 acquisition of Acqueon added proactive engagement and journey orchestration, while NICE’s purchase of LiveVox broadened mid-market reach. Partnerships such as Avaya’s alignment with Microsoft Azure infuse additional AI capabilities, signaling ecosystem collaboration as a hedge against rapid technological change. Patent filings in voice biometric authentication and emotional-sentiment scoring underscore ongoing investment in security and experience optimization.

Start-ups leveraging large language models introduce competitive tension by delivering turnkey conversational IVR that can be trained on enterprise data within hours. However, they face hurdles in obtaining regulatory certifications and integrating large-scale telephony. As a result, market participants pursue cooperative models-integrating emergent AI engines into established platforms-to balance innovation speed with enterprise-grade reliability. The landscape is thus characterized by a blend of consolidation and partnership aimed at sustaining relevance across diverse interactive voice response market segments.

Interactive Voice Response Industry Leaders

Genesys Telecommunications Laboratories Inc.

Avaya LLC

Cisco Systems Inc.

NICE Ltd.

Five9 Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: NICE formed a strategic alliance with Amazon Web Services to co-develop multilingual IVR speech models optimized for low-resource languages, targeting expansion across Asia Pacific and Africa.

- July 2025: Avaya launched its Generative CX Suite, integrating large language models into IVR to deliver dynamic responses and automated call-summary transcripts directly into customer-relationship-management records.

- March 2025: Twilio completed the acquisition of LumenVox for USD 95 million, adding advanced voice biometric authentication and real-time fraud detection to its programmable voice platform.

- January 2025: Genesys introduced its cloud-native IVR Composer 2.0, enabling drag-and-drop conversational design and live testing that reduces deployment time for new call flows by 40%.

Global Interactive Voice Response Market Report Scope

The Interactive Voice Response Market / IVR Market Report is Segmented by Deployment Mode (On-Premise, and Cloud), Enterprise Size (Small and Medium Enterprises, and Large Enterprises), Component (Solutions, and Services), End-User Industry (Banking Financial Services and Insurance, Telecommunications, Healthcare and Life Sciences, Retail and E-Commerce, Utilities and Energy, Public Sector), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| On-Premise |

| Cloud |

| Small and Medium Enterprises |

| Large Enterprises |

| Solutions |

| Services |

| Banking, Financial Services And Insurance |

| Telecommunications |

| Healthcare And Life Sciences |

| Retail And E-Commerce |

| Utilities And Energy |

| Public Sector |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Deployment Mode | On-Premise | ||

| Cloud | |||

| By Enterprise Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By Component | Solutions | ||

| Services | |||

| By End-User Industry | Banking, Financial Services And Insurance | ||

| Telecommunications | |||

| Healthcare And Life Sciences | |||

| Retail And E-Commerce | |||

| Utilities And Energy | |||

| Public Sector | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the Interactive Voice Response market by 2030?

It is forecast to reach USD 7.07 billion, supported by a 5.56% CAGR.

Which deployment mode is expanding fastest within Interactive Voice Response solutions?

Cloud deployments are growing rapidly, capturing 62.48% share in 2024 and advancing at 5.97% CAGR.

Why are healthcare providers investing in Interactive Voice Response?

They use IVR for appointment scheduling, prescription refills and remote symptom assessment, driving a 6.73% CAGR in the vertical.

What regional market is growing most quickly?

Asia Pacific leads with a 6.44% CAGR, fueled by digital-government programs and multilingual service requirements.

How are vendors differentiating their IVR offerings?

Providers focus on conversational AI accuracy, voice biometric security and vertical compliance modules to stand out in a moderately concentrated landscape.

What primary challenge limits multilingual IVR adoption?

Accuracy drops when handling code-switching and regional dialects, increasing deployment complexity and maintenance costs.

Page last updated on: