Integrated Voltage Regulator Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

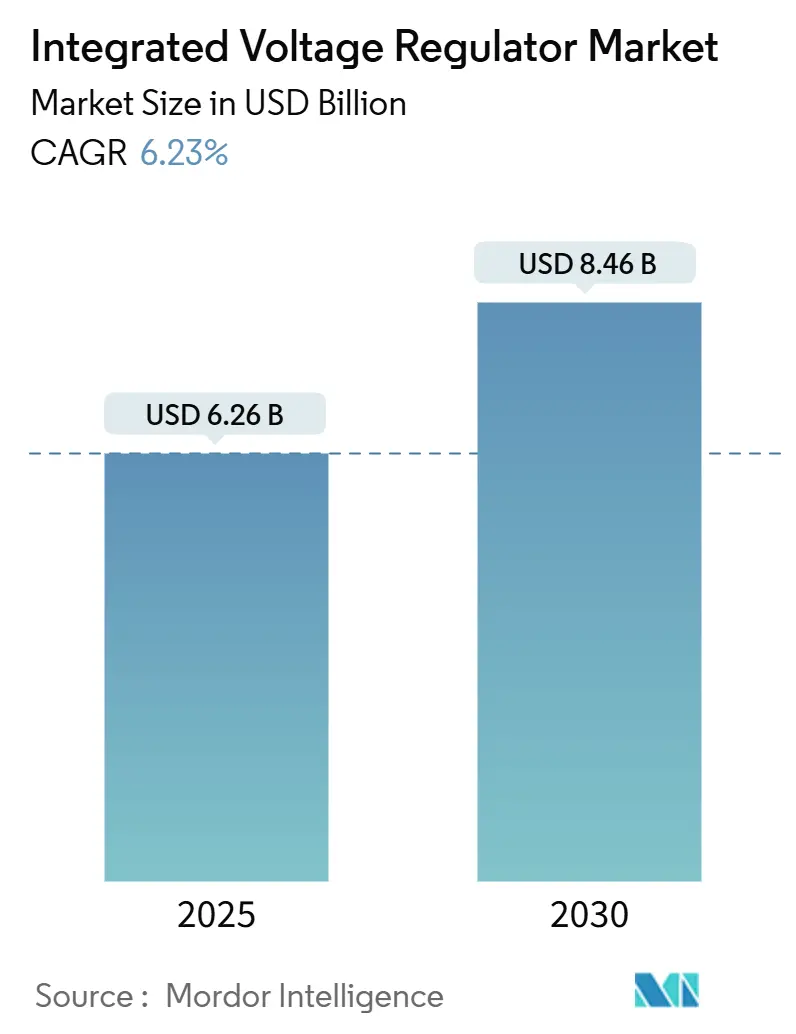

| Market Size (2025) | USD 6.26 Billion |

| Market Size (2030) | USD 8.46 Billion |

| Growth Rate (2025 - 2030) | 6.23% CAGR |

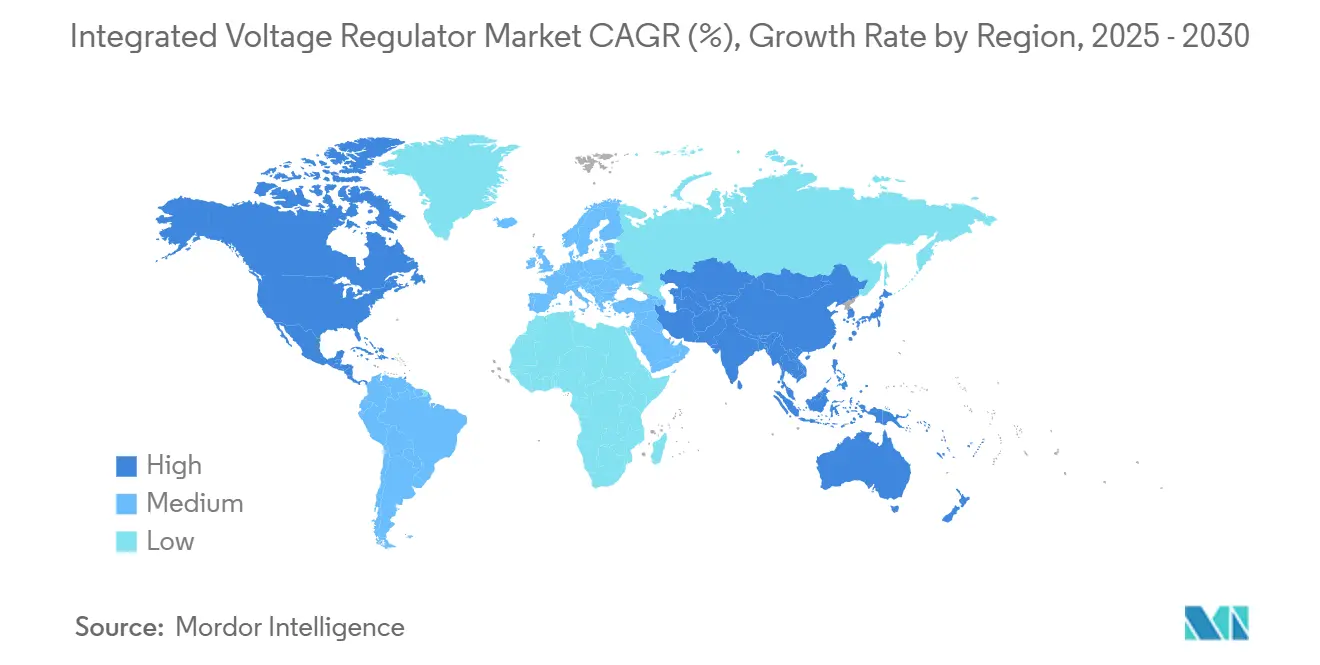

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

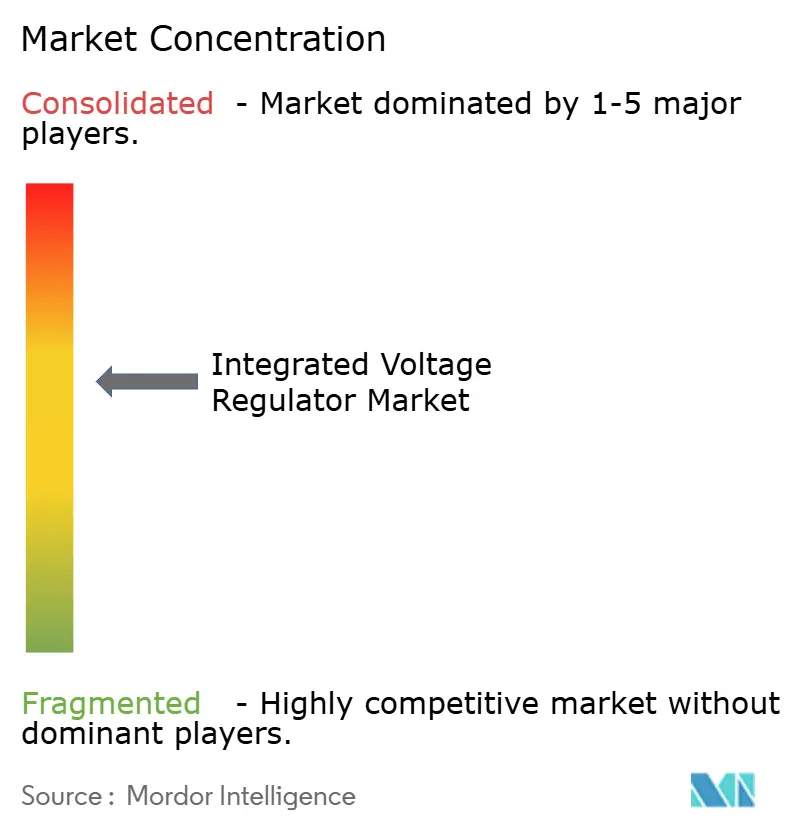

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Integrated Voltage Regulator Market Analysis by Mordor Intelligence

The integrated voltage regulator market size is valued at USD 6.26 billion in 2025 and is projected to reach USD 8.46 billion by 2030, advancing at a 6.23% CAGR over the forecast period. Adoption is accelerating as traditional off-chip conversion cannot meet the sub-nanosecond transient response required by advanced 3nm and 2nm logic. Fully integrated solutions improve power-delivery network impedance, reclaim die area once reserved for thick on-chip metals, and enable higher clock frequencies for AI accelerators. Data center operators, automotive OEMs, and sovereign AI programs are setting stricter energy-efficiency targets that elevate integrated voltage regulation from a cost decision to a strategic imperative. Competitive intensity is rising as analog incumbents, fabless specialists, and foundries rush to integrate turnkey voltage-regulator IP blocks into front-end design kits.

Key Report Takeaways

- By product type, digital fully integrated voltage regulators led with 42.31% revenue share in 2024, while switched-capacitor designs are forecast to expand at a 6.92% CAGR through 2030.

- By process node, 7-9 nm devices held 38.79% of the 2024 demand, and 3-4 nm nodes are expected to grow at a 7.31% CAGR through 2030.

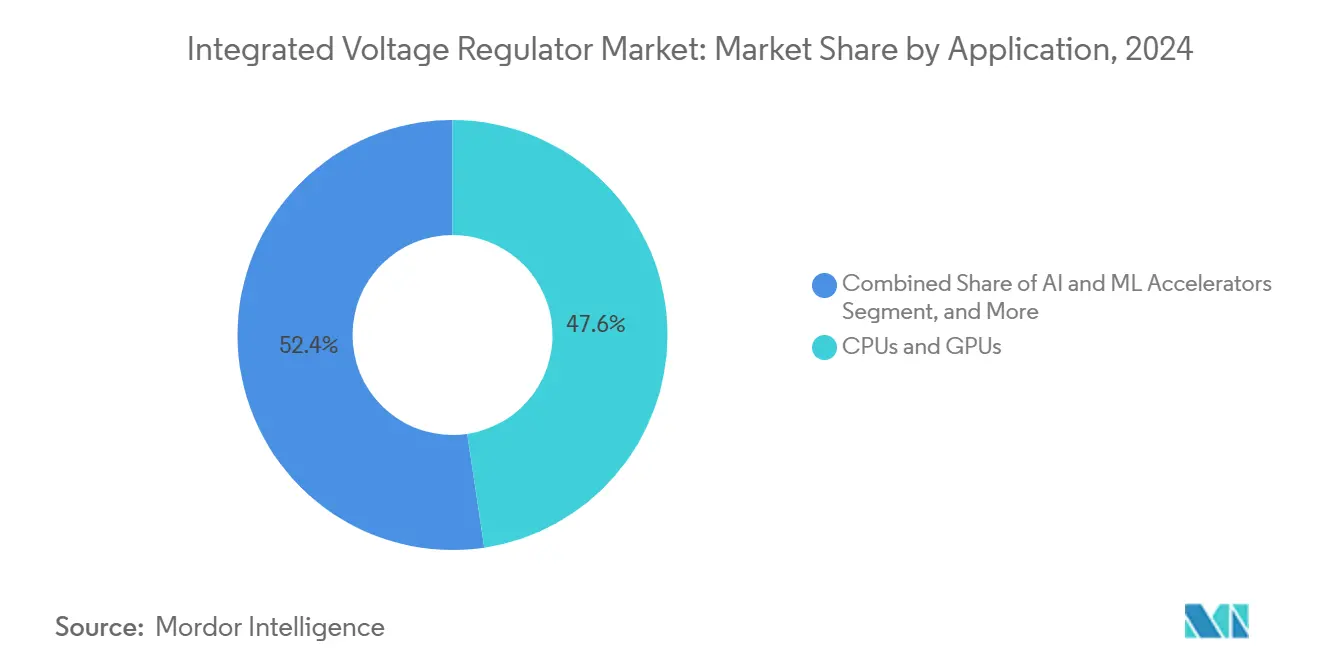

- By application, CPUs and GPUs accounted for a 47.64% share in 2024, whereas AI and ML accelerators are poised for a 7.17% CAGR over the same horizon.

- By end-user industry, data centers represented 43.89% of 2024 volumes, but automotive electronics is projected to register a 7.29% CAGR through 2030.

- By geography, the Asia-Pacific region dominated with 35.66% of 2024 revenue, while the Middle East is set to achieve a 7.24% CAGR as hyperscale data center builds ramp up.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Integrated Voltage Regulator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Integration of Power Management On-Chip | +1.2% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Rising Demand for Energy Efficient Data Centers | +1.4% | Global, led by North America, Europe, and Middle East | Short term (≤ 2 years) |

| Proliferation of AI Accelerators Requiring Fine-Grained Power Domains | +1.6% | North America and Asia-Pacific, spillover to Europe | Short term (≤ 2 years) |

| Shift to Advanced 3 nm and Below Nodes Enabling On-Die Power Conversion | +1.1% | Asia-Pacific core (Taiwan, South Korea), North America | Long term (≥ 4 years) |

| Growing Adoption in Automotive ADAS and EV Powertrains | +0.9% | Europe and Asia-Pacific, emerging in North America | Medium term (2-4 years) |

| Government Incentives for Semiconductor Power Efficiency Compliance | +0.7% | Europe (EU regulations), Asia-Pacific (China standards), North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Integration of Power Management On-Chip

Migrating voltage regulation onto the die eliminates motherboard-level inductance that once caused voltage droop exceeding 10% during transient loads, allowing designers to drop nominal core voltages and shrink energy budgets. IBM’s 2024 study showed an 87% reduction in parasitic inductance when regulators sit within 50 µm of logic, enabling sub-microsecond dynamic voltage and frequency scaling cycles. Foundries now bundle backside power rails with standard cell libraries, making proximity regulation unavoidable at 3 nm, where impedance budgets fall below single-digit milliohms.[1]TSMC, “N3E Process Technology and Design Infrastructure,” tsmc.com Smartphone vendors are following a similar path to achieve 24-hour mixed-use battery life targets, which require 15% efficiency gains compared to 2023 flagships.

Rising Demand for Energy-Efficient Data Centers

Hyperscalers consumed 21.3 TWh in 2024 and lost 8% of that energy in multi-stage power conversion alone.[2]Google, “Environmental Report 2024,” google.com Integrated regulators eliminate intermediate 12 V to 1 V steps, increasing end-to-end efficiency above 92% and enabling facilities to meet sub-1.3 power-usage-effectiveness metrics imposed on U.S. federal sites. In hot-climate regions such as the United Arab Emirates, sovereign investors mandate integrated power-delivery topologies to control cooling overheads, driving new orders for high-current on-die regulators that guarantee chip-level conversion efficiency exceeding 95%.

Proliferation of AI Accelerators Requiring Fine-Grained Power Domains

AI chips, such as NVIDIA’s H100, expose a dozen rails that shift from idle to 400W loads in microseconds, forcing regulators to supply 100A bursts without overshoot.[3]NVIDIA Corporation, “H100 Tensor Core GPU Architecture,” nvidia.com Integrated solutions enable 10-µs rail switching and deliver 12 TOPS per watt in Qualcomm’s 2024 mobile AI engine, a 34% lift over discrete power-management ICs. As edge devices host ever-larger language models, Apple’s M4 neural engine now modulates rail voltage every 10 µs, driving universal adoption of near-die regulation across consumer, automotive, and industrial edge silicon.

Shift to Advanced 3 nm and Below Nodes Enabling On-Die Power Conversion

At 3 nm, a 50 mV swing can shift critical-path delay by 15%, making millivolt-level line regulation mandatory. Samsung’s 2 nm gate-all-around PDK therefore ships with turnkey regulator IP, and TSMC pegs integration overhead at just 4% of the die cost for gains that allow 20% higher clock speeds. In the long run, backside power-delivery networks will pull current through dedicated buried rails, reducing IR drop by 45% and solidifying regulators as a baseline feature on every leading-edge design.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thermal Management Challenges at High Current Densities | -0.8% | Global, particularly acute in automotive and industrial applications | Short term (≤ 2 years) |

| Complex Co-Design Requirements Between Analog and Digital Teams | -0.5% | Global, more pronounced in regions with fragmented design ecosystems | Medium term (2-4 years) |

| Reliability Concerns Over Electromigration in Advanced Packaging | -0.6% | Asia-Pacific and North America leading-edge fabs | Long term (≥ 4 years) |

| Limited Foundry IP Availability for High Current Inductors | -0.4% | Global, except Intel's captive foundry operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Thermal Management Challenges at High Current Densities

Regulators delivering 200 A on die can drive hotspots past 120 °C, and heat fluxes above 500 W cm-2 shorten via lifetime by 40%. Automotive junctions that already reach temperatures of 150 °C often require designers to derate the regulator current by 30% or add costly active cooling, which hampers adoption in powertrain controllers. Fanless industrial PCs abandon nearly one-quarter of qualification attempts because integrated solutions exceed thermal headroom, limiting early revenue capture.

Reliability Concerns Over Electromigration in Advanced Packaging

As current density approaches 2 mA µm-2 in 3 nm copper traces, predicted lifetimes fall below five years unless metallization stacks are re-engineered. Foundry-qualified inductor IP remains scarce, preventing many fabless designers from bringing full-scale digital regulators to tapeout. The lingering mismatch between available packaging materials and next-generation current loads weighs on long-term confidence, especially for mission-critical aerospace and medical designs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Dominance With Switched-Capacitor Momentum

Digital architectures commanded the largest integrated voltage regulator market share at 42.31% in 2024, reflecting seamless compatibility with standard CMOS flows that ease porting down to 3 nm nodes. Intel’s Raptor Lake family utilizes 256-step digital rails to reduce idle power by 23%. The segment benefits from scalable control logic, but it also incurs die-area penalties due to on-chip inductors. The integrated voltage regulator market size for digital solutions is projected to grow steadily as foundries pre-qualify turnkey IP in every advanced design kit.

Switched-capacitor regulators are expected to post the fastest growth at 6.92% as mobile and edge devices seek slimmer profiles. Qualcomm’s Snapdragon 8 Gen 3 reduced the die area by 35% and achieved an 88% efficiency without the use of magnetic components. Upcoming GaN-on-Si switches push operation above 100 MHz, shrinking capacitor footprints by 60%. Vendors see room to hybridize digital control with capacitor-only power stages, blurring architectural lines while expanding total addressable opportunity.

By Process Node: Mainstream 7-9 nm Today, 3-4 nm Tomorrow

The 7-9 nm bracket led demand with a 38.79% integrated voltage regulator market share in 2024, thanks to high tape-out success rates and proven reliability. Automotive ASIC vendors rely on their mature defectivity curves to hit stringent zero-defect targets, underpinning stable design-win volume. Nevertheless, the integrated voltage regulator market size for 3-4 nm designs is expected to accelerate at a 7.31% CAGR as AI accelerators and flagship smartphones migrate to leading-edge nodes that require on-die power conversion.

Apple’s A18, fabbed on N3E, realized 18% higher performance and 12% lower energy by exploiting 14 discrete voltage domains. Backside power rails debut at 5-6 nm and become mainstream at 3-4 nm, cutting IR drop by 45% and guaranteeing supply-voltage headroom for 20% clock boosts. Mature 28 nm FD-SOI remains relevant for safety-critical power management, but its share will erode as the cost per transistor falls at newer nodes.

By Application: AI Accelerators Overtake General Compute

CPUs and GPUs accounted for 47.64% of 2024 unit shipments, driven by data-center refresh cycles and desktop gaming demand. AMD’s Ryzen 9000 cores each receive 50 A of regulated current to sustain 5.7 GHz boost clocks without exceeding the 170 W thermal envelope. While large today, this slice of the integrated voltage regulator market will cede share to AI accelerators, which are projected to post a 7.17% CAGR, driven by inference workloads that spike power in microseconds.

Google’s TPU v5 tiled architecture cut idle power 41% through per-tile gating. Edge AI silicon in smartphones, cameras, and smart speakers broadens the customer base, inserting integrated regulation into low-cost SoCs by 2027. Networking ASICs and sensor-fusion processors add incremental volume as 800G Ethernet and Level 3 autonomy spread through data-center and automotive ecosystems.

By End-User Industry: Automotive Outpaces All Others

Data centers accounted for 43.89% of shipments in 2024, but capex discipline and software-level power tuning will moderate growth through 2030. Hyperscalers increasingly extend server life by optimizing firmware-level idle states rather than refreshing motherboards. In contrast, the automotive segment is expected to rise at 7.29%, making it the fastest-growing segment of the integrated voltage regulator market. Euro 7 mandates require tighter real-time efficiency monitoring, which depends on low-noise voltage rails. The content value per vehicle already exceeds USD 720 at Continental.

Consumer electronics and telecom equipment contribute steadily to volumes: every premium handset now embeds at least six on-die regulators, and 5G massive-MIMO radios require point-of-load conversion to meet the 3% energy-efficiency improvement targets set by operators. Industrial automation represents an emerging frontier, although higher ambient temperatures and noise immunity demands will slow adoption until regulators achieve better thermal headroom.

Geography Analysis

Asia-Pacific retained the lead with 35.66% of 2024 revenue as China’s self-sufficiency plan funneled RMB 143 billion (USD 20 billion) into domestic power-management IC development. TSMC’s 3 nm rollout and SMIC’s 28 nm volume ramp together underpin a dense ecosystem of fabless designers adopting integrated regulation IP. Japan’s EV supply chain added upside: Renesas recorded JPY 180 billion (USD 1.2 billion) in automotive-power revenue during 2024, largely from 800 V platforms.

North America’s outlook is buoyed by CHIPS-Act incentives that reward power-efficient silicon. Intel’s 18A Ohio mega-fab aims to serve both Intel and foundry clients with backside-power technology, guaranteeing local access to advanced regulator IP. European growth is tethered to automotive electrification programs backed by EUR 20 billion (USD 22 billion) in German research grants that target 800 V inverter ICs.

The Middle East, currently modest in size, will expand at 7.24% CAGR as sovereign funds build AI data centers in heat-intensive climates. Mubadala earmarked USD 3.2 billion, and Saudi Arabia’s NEOM smart-city initiative reserved USD 500 million for energy-optimized processors that require integrated regulation. Latin America and Africa remain nascent, yet Brazil’s USD 1.1 billion Stellantis EV plant will spark local demand for automotive-grade regulators by 2026.

Competitive Landscape

The top five suppliers accounted for 58% of 2024 revenue, resulting in a moderately concentrated sector profile. Texas Instruments and Analog Devices defend their shares through broad catalogs and domestic fabrication expansions, including TI’s USD 900 million Lehi-fab acquisition, slated for analog conversion. Renesas bolstered its arsenal through the acquisitions of Dialog and IDT, enabling single-vendor power subsystems that reduce automotive design cycles by nine months.

Fabless disruptors combine GaN switches and switched-capacitor topologies to reach 95% efficiency at 100 A, delaying hyperscaler grid upgrades. Empower Semiconductor and other startups filed 47 patents on capacitor networks in 2024, illustrating an intellectual-property arms race. Foundries threaten to commoditize discrete power-IC value by bundling regulator IP in their process design kits; yet, this move opens up novel territory for algorithm-rich control firmware that remains vendor-differentiated.

Chiplet-based 3D packaging is another battleground. Intel’s Foveros stack requires high-density regulators that supply vertically arranged compute tiles, a niche currently served by only a handful of suppliers. ON Semiconductor and Infineon push further into silicon-carbide driver integration, extending the reach of on-die regulation from logic rails into traction inverters and industrial drives.

Integrated Voltage Regulator Industry Leaders

Analog Devices, Inc.

Empower Semiconductor, Inc.

Enpirion Technologies, Inc. (Intel Corporation)

Infineon Technologies AG

Integrated Device Technology, Inc. (Renesas Electronics Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: TSMC debuted a 2 nm design-kit update that bundles backside-power integrated voltage-regulator IP blocks as standard cells, enabling customers to reduce power-delivery IR drop by 45% and reclaim up to 6% die area previously devoted to on-chip metal routing.

- June 2025: Texas Instruments completed tool installation at the newly acquired Lehi, Utah 300 mm facility and initiated pilot runs of analog and power-management wafers, including next-generation integrated voltage regulators for industrial and automotive customers.

- March 2025: Continental AG disclosed a 27% year-over-year jump in automotive power-management IC purchases, earmarking an additional USD 180 million for integrated voltage regulators to support upcoming 800 V electric-vehicle platforms.

- January 2025: Infineon Technologies committed USD 2.1 billion to expand its Kulim, Malaysia fab, adding 70,000 300 mm wafers per month dedicated to automotive-grade integrated voltage regulators.

Global Integrated Voltage Regulator Market Report Scope

The Integrated Voltage Regulator Market Report is Segmented by Product Type (Digital Fully Integrated Voltage Regulators, Analog Point-of-Load IVRs, Switched-Capacitor IVRs, Hybrid Multiphase IVRs), Process Node (greater than or equal to 16 nm, 10-14 nm, 7-9 nm, 5-6 nm, 3-4 nm), Application (CPUs and GPUs, AI and ML Accelerators, Mobile SoCs, Networking ASICs, Automotive ASICs), End-User Industry (Data Centers, Consumer Electronics, Automotive, Telecommunications, Industrial Automation), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Digital Fully Integrated Voltage Regulators (FIVR) |

| Analog Point-of-Load IVRs |

| Switched-Capacitor IVRs |

| Hybrid Multiphase IVRs |

| greater than or equal to 16 nm |

| 10-14 nm |

| 7-9 nm |

| 5-6 nm |

| 3-4 nm |

| CPUs and GPUs |

| AI and ML Accelerators |

| Mobile SoCs |

| Networking ASICs |

| Automotive ASICs |

| Data Centers |

| Consumer Electronics |

| Automotive |

| Telecommunications |

| Industrial Automation |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product Type | Digital Fully Integrated Voltage Regulators (FIVR) | ||

| Analog Point-of-Load IVRs | |||

| Switched-Capacitor IVRs | |||

| Hybrid Multiphase IVRs | |||

| By Process Node | greater than or equal to 16 nm | ||

| 10-14 nm | |||

| 7-9 nm | |||

| 5-6 nm | |||

| 3-4 nm | |||

| By Application | CPUs and GPUs | ||

| AI and ML Accelerators | |||

| Mobile SoCs | |||

| Networking ASICs | |||

| Automotive ASICs | |||

| By End-User Industry | Data Centers | ||

| Consumer Electronics | |||

| Automotive | |||

| Telecommunications | |||

| Industrial Automation | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the integrated voltage regulator market in 2025?

The integrated voltage regulator market size stands at USD 6.26 billion in 2025.

What is the projected CAGR for integrated voltage regulators through 2030?

The market is forecast to grow at a 6.23% CAGR between 2025 and 2030.

Which product type currently leads adoption?

Digital fully integrated voltage regulators hold the highest 2024 share at 42.31%.

Which application area is expected to grow the fastest?

AI and ML accelerators are projected to record the highest CAGR at 7.17% through 2030.

Why are integrated voltage regulators critical for 3 nm nodes?

At 3 nm, millivolt-level supply variation can shift circuit timing by 15%, so on-die regulation is essential to maintain performance and yield.

Which region will experience the highest growth?

The Middle East is expected to post the fastest regional CAGR at 7.24% thanks to sovereign AI-data-center investments.

Page last updated on: