Injectable Contraceptives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

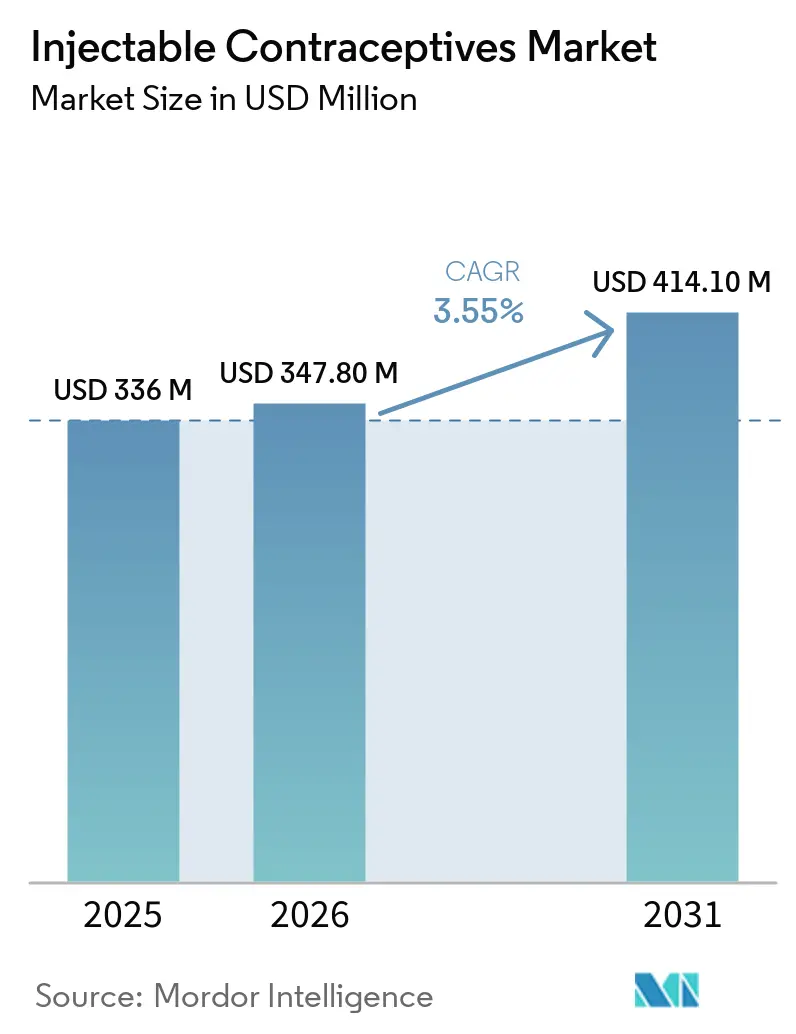

| Market Size (2026) | USD 347.80 Million |

| Market Size (2031) | USD 414.10 Million |

| Growth Rate (2026 - 2031) | 3.55% CAGR |

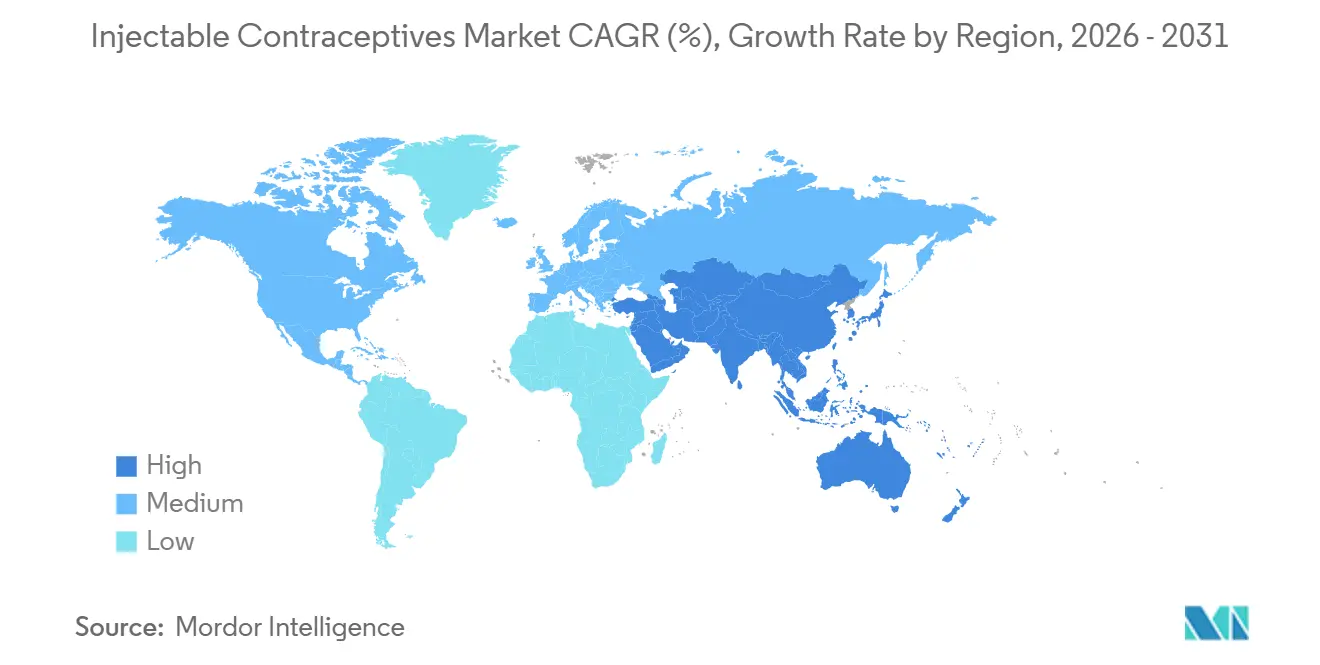

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Injectable Contraceptives Market Analysis by Mordor Intelligence

The Injectable Contraceptives Market size is projected to expand from USD 336 million in 2025 and USD 347.80 million in 2026 to USD 414.10 million by 2031, registering a CAGR of 3.55% between 2026 to 2031.

Growing acceptance of subcutaneous self-injection is shifting volumes from hospital settings to direct-to-consumer platforms, prompting distributors to diversify away from clinic-driven models [1]PATH, “Access Collaborative Self-Injection Data,” path.org. Demand is reinforced by public procurement programs that lock in multi-year supply agreements, helping manufacturers hedge against private-sector volatility. Competitive pressure centers on pricing inside global tenders rather than product branding, creating space for biosimilar entrants that can navigate WHO prequalification at lower cost. Meanwhile, social-media discourse on hormonal safety continues to weigh on continuation rates, adding uncertainty to short-term demand modeling.

Key Report Takeaways

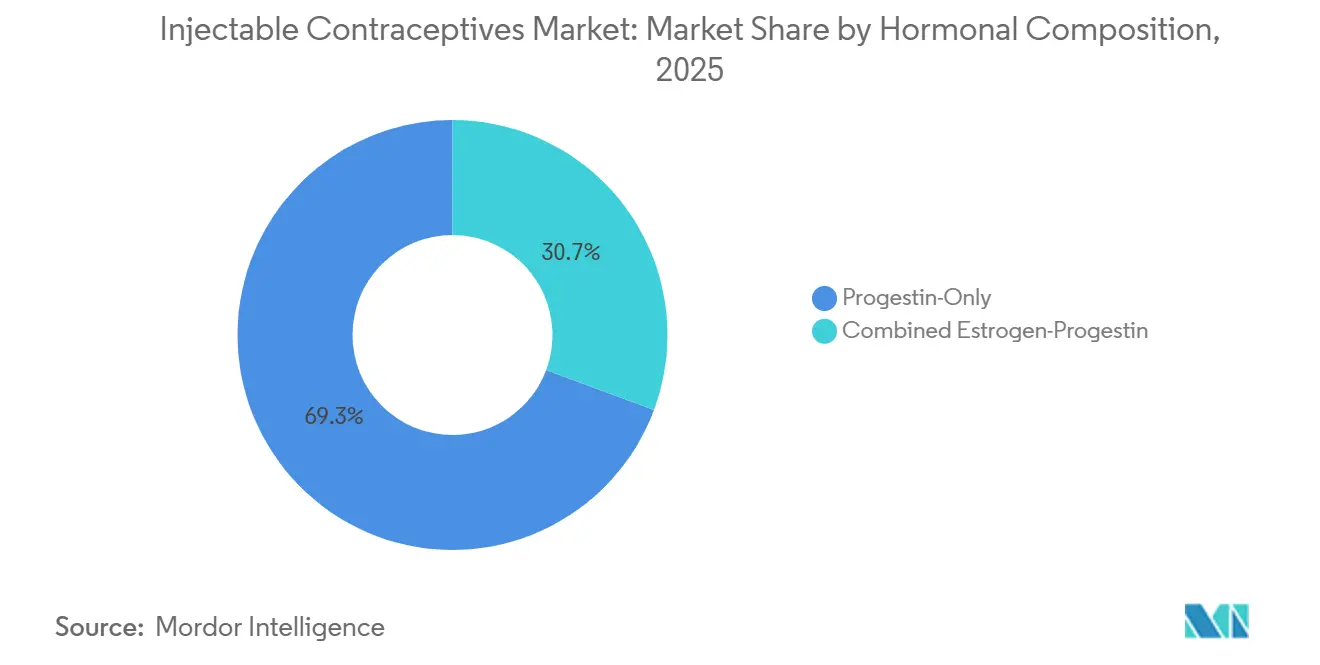

- By hormonal composition, progestin-only formulations led with 61.32% of the injectable contraceptives market share in 2025, while dual-mechanism formulations are forecast to expand at a 6.76% CAGR through 2031.

- By dosage schedule, 3-month products commanded 49.54% of the injectable contraceptives market size in 2025, but 6-month formulations are set to grow at 5.54% CAGR between 2026 and 2031.

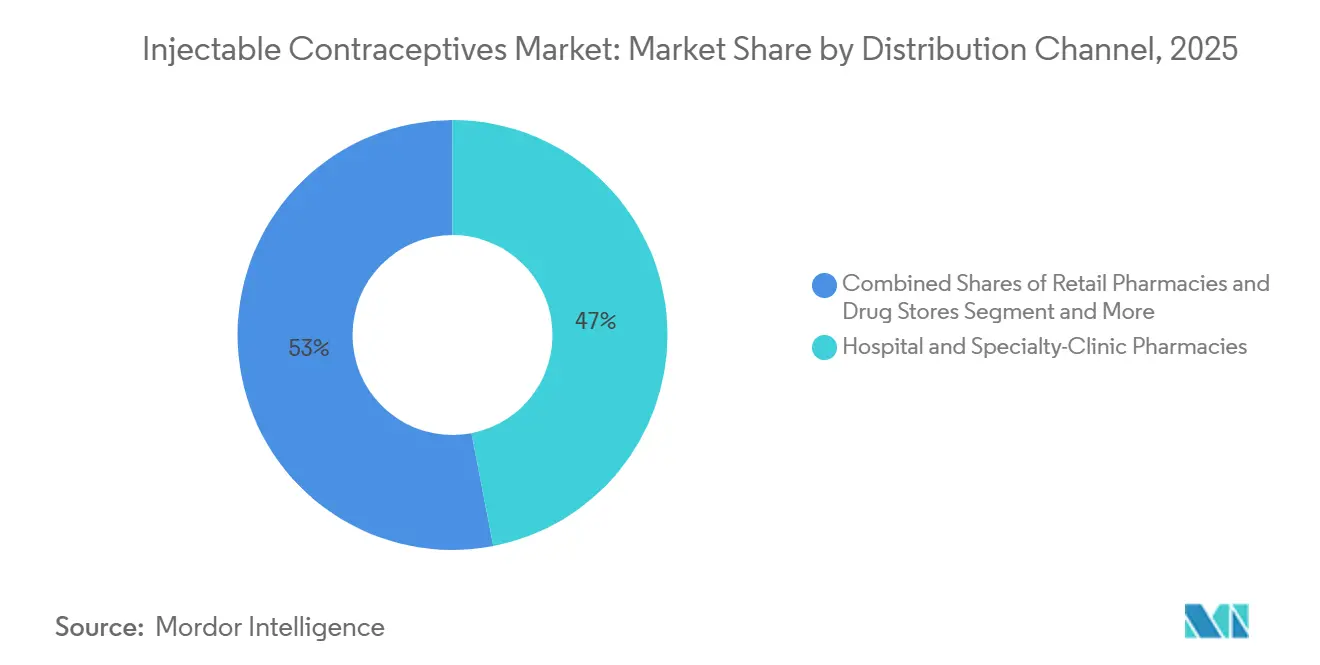

- By distribution channel, hospital and specialty-clinic pharmacies held 46.97% revenue share in 2025, whereas online and direct-to-consumer platforms are advancing at 5.43% CAGR over 2026-2031.

- By end user, women aged 25-34 accounted for 39.65% of 2025 volume, yet the 15-24 segment is projected to post a 6.11% CAGR to 2031.

- By geography, North America contributed 42.43% of the 2025 value, but Asia-Pacific is expected to register a 5.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Injectable Contraceptives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising unmet need for long-acting reversible contraception in LMICs | +1.2% | Sub-Saharan Africa, South Asia | Long term (≥ 4 years) |

| Favorable government family-planning initiatives & donor funding | +0.9% | USAID priority countries | Medium term (2-4 years) |

| Higher adherence & cost-effectiveness versus daily oral pills | +0.7% | North America, Western Europe, urban APAC | Short term (≤ 2 years) |

| Sub-cutaneous products enabling task-shifting | +0.8% | India, Indonesia, East Africa | Medium term (2-4 years) |

| Pipeline of heat-stable depot injectables | +0.5% | Rural Sub-Saharan Africa, Southeast Asia | Long term (≥ 4 years) |

| Telemedicine-driven prescription fulfilment | +0.4% | North America, Western Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Unmet Need for Long-Acting Reversible Contraception in LMICs

Low- and middle-income countries account for the majority of the 218 million women with unmet contraceptive need, yet depot injectables make up only a modest portion of the method mix in these markets, leaving a sizable demand gap that procurement agencies are beginning to close through larger framework agreements. PATH documented 1.7 million self-injection visits across 14 countries between 2020 and 2024, achieving 65-72% continuation at 12 months, well above the 55-60% typical for clinic-administered injections. Eliminating long travel and wait times helps women avoid losing up to two days of agricultural wages per visit, reinforcing the economic case for self-injection programs [2]World Health Organization, “Global Family Planning Initiatives,” who.int. Supply disruptions in Nigeria illustrated how stock-outs quickly translate to discontinuation and unintended pregnancies, adding urgency to diversifying suppliers. Manufacturers holding WHO prequalification are best placed to scale because 70% of LMIC volumes flow through UN channels rather than commercial trade.

Favorable Government Family-Planning Initiatives & Donor Funding

Family-planning budgets in 69 FP2030 focus countries climbed 57% between 2019 and 2024, underpinning procurement stability even as U.S. bilateral funding fell 41% in early 2025. Domestic allocations rose significantly in the Democratic Republic of Congo, Zambia, and Zimbabwe during 2025, signaling a pivot toward self-reliance that reduces donor exposure. UNFPA’s 2026-2030 plan dedicates 35% of its commodity basket to injectables and implants versus 28% previously, directing incremental spend toward depot formulations. Countries with stronger fiscal capacity, such as India and South Africa, maintain notable annual volume growth, whereas donor-heavy markets like Niger remain flat until alternate funding emerges. Suppliers diversified across public and private channels stand to capture outsized gains as funding sources rebalance.

Higher Adherence & Cost-Effectiveness Versus Daily Oral Pills

Depot injectables remove the daily pill burden that drives 30-40% discontinuation for orals within a year, sustaining user protection with only four contacts annually [3]BMJ Open, “Telemedicine for Contraceptive Services,” bmj.com. A 2025 BMJ Open review found prescribers increasingly recommend self-injected formulations for 18-24-year-olds who struggle with routine adherence. In systems where wasted oral packs reach 30%, injectables become 20-25% cheaper per protected year despite a higher unit price, strengthening the payer incentive to favor depots. As generic pill prices fall to USD 1-2 per cycle, the economic advantage narrows, but privacy and autonomy tilt patient choice back to injectables, especially where digital refills are seamless.

Sub-Cutaneous Products Enabling Task-Shifting to Community Health Workers

Prefilled Uniject devices cut training time from 40 hours to 4-6 hours, allowing community workers to deliver injections legally in 35 countries that amended scope-of-practice rules between 2020 and 2025. Uganda recorded a 28% coverage jump in rural districts once village teams began administering depot injections during 2024-2025, with no rise in adverse events. Doubling the provider base where physician density is below 1 per 10,000 unlocks latent demand that clinics cannot serve. Barriers around volunteer compensation and gender norms still limit uptake, especially where male workers face resistance from female clients. Even so, the policy shift contributes 0.8 percentage points to the injectable contraceptives market CAGR across 15-20 high-priority countries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Side-effect profile driving discontinuation | -0.6% | North America, Western Europe | Short term (≤ 2 years) |

| Competition from implants & intra-uterine devices | -0.4% | North America, Europe, urban APAC | Medium term (2-4 years) |

| API shortages disrupting medroxyprogesterone supply | -0.3% | Markets reliant on single-source suppliers | Short term (≤ 2 years) |

| Social-media misinformation on hormonal safety | -0.2% | North America, Western Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Side-Effect Profile Driving Discontinuation Rates

Up to 70% of depot users experience irregular bleeding, and the FDA has required a bone-density warning since 2004, creating a perception hurdle among adolescents who are otherwise ideal candidates. A 2024 French review linked long-term use to meningioma, prompting new contraindications and sparking social-media amplification that drives a 35-40% first-year drop-out. Although bone density rebounds within three years of stopping, the black-box labeling remains a deterrent. Manufacturers are testing dual-mechanism agents designed to reduce bleeding, but no option will reach the market before 2028, keeping the restraint in place in the short term.

Competition from Implants & Intra-Uterine Devices

Nexplanon won FDA approval in January 2026 to extend its labeled use from three to five years, improving its cost per protected year by 35-40% relative to quarterly depots. Implants already have notable adoption of the long-acting market in high-income countries and are expanding rapidly, directly cannibalizing injectable volumes among convenience-seeking users. IUDs also offer five-to-ten-year efficacy with a one-time procedure, although insertion requirements limit scale in low-resource areas. Where trained providers and reimbursement converge, clinics lean toward longer-duration devices, negatively affecting their growth. Injectable makers retain an edge where implant removal is unavailable, but that advantage is eroding as training programs proliferate

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Hormonal Composition: Progestin-Only Formulations Remain Mainstay While Dual-Mechanism Prospects Rise

Progestin-only injectables are expanding their lead over combined estrogen-progestin alternatives, building on the 69.32% share they commanded in 2025. Their appeal comes from breastfeeding compatibility, broad use across age groups, and the absence of estrogen-linked risks that limit combined products to roughly one-third of women of reproductive age. The 2025 update to WHO’s Medical Eligibility Criteria classified progestin-only methods as Category 1 for lactating women and for users with cardiovascular risk, while combined injectables received Category 3-4 ratings for women older than 35 who smoke, those with hypertension, or anyone with a history of venous thromboembolism. This guidance now channels about the majority of new adopters toward depot medroxyprogesterone acetate and similar formulations, especially in low- and middle-income countries where cardiovascular screening is scarce.

Combined formulations hold the remaining share and cater mainly to younger, non-smoking women who value predictable bleeding over the amenorrhea that affects more than half of progestin-only users within a year. Their growth outlook is constrained by rising obesity and population aging, factors that prompt groups such as the American College of Obstetricians and Gynecologists to steer women with a body-mass index above 35 kg/m² away from estrogen-containing methods because of clotting risk.

By Dosage Schedule: Six-Month Formulations Poised to Reduce Clinic Touchpoints

Three-month depots held 49.54% share in 2025 thanks to the legacy of DMPA, yet payer push-back over visit costs fuels interest in extended intervals that halve clinic traffic. A single family-planning encounter costs public systems USD 15-25, so six-month injectables cut annual service expenditure by roughly 20-25%, appealing especially to under-funded programs.

The six-month pipeline is forecast to grow at 5.54% CAGR, contingent on timely Phase III success and WHO prequalification by 2028. Monthly injectables, once favored for mimicking natural cycles, are receding at -1 to -1.5% CAGR because self-administered three-month depots already deliver similar bleeding patterns without clinic visits. The injectable contraceptives market size could shift toward a barbell distribution, with self-injected quarterly doses on one end and six-month provider-administered shots on the other, squeezing mid-frequency formats. Pricing strategies will matter: if manufacturers peg six-month wholesale prices at less than double three-month vials, payers may transition rapidly to longer intervals for cost savings. Regulators have already updated labeling guidance to accommodate extended intervals, clearing a path for commercialization once efficacy thresholds are met.

By Distribution Channel: Digital Platforms Capture Momentum from Self-Injection Trends

Hospital and specialty clinics owned 46.97% of the 2025 value but face a structural decline as patients pivot to self-injection models enabled by telemedicine. Online pharmacies recorded a 5.43% CAGR projection through 2031, propelled by same-day delivery, refill reminders, and discreet shipping that appeal to privacy-conscious buyers in urban corridors.

Retail drug stores, holding a near-significant share, risk losing foot traffic as app-based providers integrate prescription generation, payment, and logistics in a single click. In low-resource settings, NGO clinics and public facilities will remain indispensable as they route a notable portion of the total volume financed by donors and domestic schemes. The injectable contraceptives market size could reallocate 3-4 percentage points from brick-and-mortar outlets to digital suppliers by 2031 if reimbursement rules expand telehealth coverage.

By End User: Social-Media-Savvy Young Adults Accelerate Early Adoption

Women aged 25-34 generated the largest revenue slice at 39.65% in 2025, consistent with peak fertility years. Yet the 15-24 group is posting 6.11% CAGR, enlarged by social-media campaigns normalizing long-acting methods among first-time contraceptive users.

CDC’s 2024 U.S. guidance removed age-based restrictions, further widening adolescent eligibility. Meanwhile, the 35-44 cohort grows with a modest share as permanent methods rise, and the 45+ segment remains negligible outside niche perimenopausal applications. Brands that tailor messaging and device ergonomics for smaller hands have gained traction with younger users, highlighting the importance of user-centered design.

Geography Analysis

North America generated 42.43% of global value in 2025, buoyed by reimbursement and high per-capita spending, but growth is expected to soften as market saturation meets competition from five-year implants. Social-media safety debates further temper new-user acquisition even as telemedicine channels expand prescription volume. The injectable contraceptives market size in the region may plateau if switching outpaces new initiations, despite rising self-administration adoption.

Asia-Pacific is forecast to lead growth at 5.76% CAGR on the back of policy reforms that authorize auxiliary nurse midwives to give depots, effectively trebling provider density in rural India and Indonesia. Population momentum and urban income gains also lift private-sector uptake, while donor programs focus on hard-to-reach provinces across the Philippines and Vietnam. By 2031, the region could close half the dollar-value gap with North America, reflecting both volume and mix shifts in the injectable contraceptives market.

Europe captures a significant share but trends sideways because of low fertility rates and high contraceptive prevalence that offer limited headroom for expansion. The Middle East and Africa hold a notable share yet promise a high CAGR, provided donor-funded procurement remains intact. South America, at modest share, is projected to advance as regulatory barriers to telemedicine ease and community health worker programs proliferate, particularly in Brazil and Uruguay.

Competitive Landscape

The top five players command significant volume, placing the injectable contraceptives market in a moderately concentrated tier where tender pricing, not branding, dictates share movement. Pfizer’s Sayana Press obtained WHO prequalification in 2026, enabling rapid expansion across 14 self-injection pilot countries with documented 65-72% continuation rates. Incepta Pharmaceuticals broke price ceilings by 30-40% after winning prequalification in 2025, signaling the disruptive impact regional manufacturers can exert in donor-funded tenders.

White-space exists in dual-mechanism agents, heat-stable depots, and six-month dosing, areas where no incumbent yet wields a first-mover advantage. Technology upgrades include digital adherence apps bundled with product packs and auto-disable syringes to curb needlestick injury, each offering marginal but marketable differentiation. Competition bifurcates: multinationals chase high-margin convenience features in wealthy markets while regional firms focus on low-cost supply in LMIC tenders. Regulatory dynamics favor suppliers that align pipeline milestones with WHO guideline revisions, such as the 2025 Medical Eligibility Criteria that clarified self-injection safety.

Injectable Contraceptives Industry Leaders

Pfizer Inc.

Incepta Pharmaceuticals Ltd.

Bayer AG

Merck & Co., Inc.

Teva Pharmaceutical Industries Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: UK law firms started evaluating potential legal action on behalf of women who developed brain tumors after using the contraceptive injection Depo-Provera.

- December 2025: Incepta Pharmaceuticals received WHO prequalification for medroxyprogesterone acetate, allowing the Bangladeshi firm to compete in African tenders at a 30-40% discount.

Global Injectable Contraceptives Market Report Scope

As per the scope of the report, Injectable contraceptives are highly effective, long-acting hormonal birth control methods primarily available in progestin-only or combined formulations.

The injectable contraceptives market is segmented by hormonal composition, dosage schedule, distribution channel, end users, and geography. Based on hormonal composition, the market is segmented into combined formulation and progestin-only. Based on the dosage schedule, the market is segmented into Monthly Injectable, 3-Month Injectable, and 6-Month Long-Acting Injectable. By distribution channel, the market is segmented into hospital & specialty-clinic pharmacies, retail pharmacies & drug stores, online & D2C platforms, NGO & public-health facilities. By end users, the market is segmented into women aged 15-24 years, women 25-34 years, women 35-44 years, and women 45+ years. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Combined Formulation |

| Progestin-Only |

| Monthly Injectable |

| 3-Month Injectable |

| 6-Month Long-Acting Injectable |

| Hospital & Specialty-Clinic Pharmacies |

| Retail Pharmacies |

| Online Platforms |

| NGO & Public-Health Facilities |

| Women 15-24 Years |

| Women 25-34 Years |

| Women 35-44 Years |

| Women 45+ Years |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Hormonal Composition | Combined Formulation | |

| Progestin-Only | ||

| By Dosage Schedule | Monthly Injectable | |

| 3-Month Injectable | ||

| 6-Month Long-Acting Injectable | ||

| By Distribution Channel | Hospital & Specialty-Clinic Pharmacies | |

| Retail Pharmacies | ||

| Online Platforms | ||

| NGO & Public-Health Facilities | ||

| By End User | Women 15-24 Years | |

| Women 25-34 Years | ||

| Women 35-44 Years | ||

| Women 45+ Years | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the injectable contraceptives market?

The injectable contraceptives market size was USD 347.8 million in 2026 and is expected to reach USD 414.1 million by 2031, according to Mordor Intelligence.

Which hormonal composition dominates sales?

Progestin-only formulations led with 61.32% market share in 2025 and are projected to maintain leadership through 2031, though their growth will slow as dual-mechanism products enter.

How fast is Asia-Pacific expanding?

Asia-Pacific is forecast to register a 5.76% CAGR between 2026-2031, the fastest among all regions, driven by policy shifts that let community health workers administer depots.

What segment is growing quickest by dosage schedule?

Six-month long-acting injectables are expected to post a 5.54% CAGR through 2031 because they halve clinic visits and lower program costs in resource-constrained settings.

Page last updated on: