Inhalation CDMO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.41 Billion |

| Market Size (2031) | USD 3.44 Billion |

| Growth Rate (2026 - 2031) | 7.54% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Inhalation CDMO Market Analysis by Mordor Intelligence

The Inhalation CDMO Market is expected to grow from USD 2.23 billion in 2025 to USD 2.41 billion in 2026 and is forecasted to reach USD 3.44 billion by 2031 at 7.54% CAGR over 2026-2031.

The rising prevalence of chronic respiratory diseases, expanding pipelines of inhalable biologics, and sponsors’ preference for outsourcing highly specialized aerosol manufacturing are the chief forces driving this double-digit growth trajectory. Sponsors are shifting capital away from in-house device lines because ISO 14644 clean rooms, multi-region regulatory expertise, and propellant-handling infrastructure require steep, recurring investments. At the same time, CDMOs have industrialized aerosol particle-size testing, dose-uniformity validation, and plume-geometry characterization at scale, giving them a defensible service advantage. Competitive strategies now center on full-service integration, propellant-free device innovation, and early adoption of low-GWP propellants, each of which widens the opportunity set for CDMOs able to execute across development, clinical, and commercial stages.

Key Report Takeaways

- By service type, contract development accounted for 37.09% of the inhalation CDMO market share in 2025, while clinical manufacturing is on track for the fastest CAGR of 10.23% to 2031.

- By product type, metered-dose inhalers led revenue with 35.21% in 2025; soft-mist and nebulized formats are projected to expand at a 10.67% CAGR through 2031.

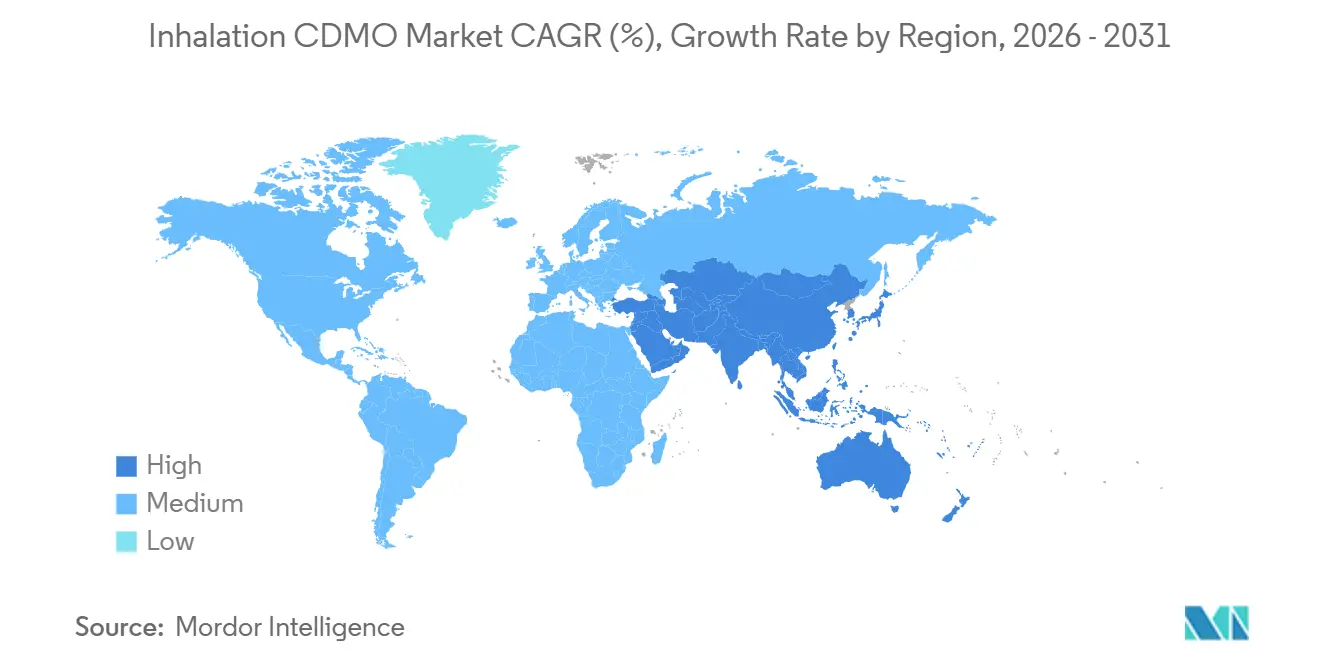

- By geography, North America held 44.25% of the revenue share in 2025; Asia-Pacific is the fastest-growing region, with a 11.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Inhalation CDMO Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increasing prevalence of chronic respiratory diseases | +1.2% | Global with acute burden in South Asia and Sub-Saharan Africa | Long term (≥ 4 years) |

| Pharmaceutical outsourcing of specialized inhalation manufacturing | +1.0% | North America and Europe, expanding in the Asia-Pacific | Medium term (2-4 years) |

| Technological advances in particle engineering and smart devices | +0.8% | North America and Europe, early adoption in Japan and South Korea | Medium term (2-4 years) |

| Growing adoption of combination and smart inhalers | +0.7% | Global, led by North America and Western Europe | Short term (≤ 2 years) |

| Low-GWP propellant transition favoring equipped CDMOs | +0.6% | Global, the strongest regulatory pressure in the EU and North America | Long term (≥ 4 years) |

| Surge in inhalable biologics and peptides pipelines | +0.9% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Chronic Respiratory Diseases

WHO’s 2024 update recorded 569.2 million prevalent asthma, COPD, and interstitial lung disease cases and 4.2 million related deaths worldwide.[1]World Health Organization, “Global Burden of Disease 2023,” who.int Incidence is rising fastest in low-income regions where rapid urbanization degrades air quality, so sponsors are broadening inhaled portfolios beyond bronchodilators into anti-inflammatory biologics and targeted small molecules. CDMOs holding sub-5-micron particle-size capability and high-potency API containment win disproportionate contracts because these exacting specifications exceed many sponsors’ internal skill sets. Device penetration remains low in several high-burden countries, indicating underserved demand that could unlock downstream volume as reimbursement schemes mature. Regulators reinforce higher technical standards, which consolidate work among CDMOs with validated analytical methods and multi-jurisdictional dossiers.

Pharmaceutical Outsourcing of Specialized Inhalation Manufacturing

Internal aerosol groups at several large pharmaceutical companies were redeployed toward higher-margin cell and gene therapy programs in 2025, redirecting inhalation budgets to external partners. Maintaining propellant lines, laser-diffraction suites, and aerosol talent for sporadic launches no longer passes internal hurdle rates, especially for mid-sized biotechs. CDMOs in North America and Western Europe capture the bulk of late-stage work because proximity and regulatory familiarity shorten oversight cycles. At the same time, Asia-Pacific providers pick up early-stage studies through cost leadership. Compliance with ISO 13485 and GMP annexes remains the entry ticket, so qualified capacity stays tight, and pricing power remains with established providers.

Technological Advances in Particle Engineering and Smart Devices

Spray-drying and supercritical-fluid platforms enable CDMOs to tune morphology, surface area, and dissolution, allowing sponsors to repurpose legacy molecules for improved lung deposition. Lonza’s PulmoSphere technology demonstrates how precision particle engineering enables controlled aerosol release profiles. Parallel progress in connected inhalers provides sponsors with real-time adherence data, enabling value-based contracts that reward outcomes. CDMOs that integrate electronics assembly, firmware validation, and post-market data analysis into existing fill-finish lines offer a complete solution under one quality system. FDA’s Office of Combination Products and EMA’s cross-disciplinary working parties have clarified approval expectations, raising barriers but giving compliant providers a durable edge.[2]U.S. Food and Drug Administration, “Chemistry, Manufacturing, and Controls Guidance for Metered-Dose and Dry-Powder Inhalers,” fda.gov

Growing Adoption of Combination and Smart Inhalers

GSK’s Trelegy and AstraZeneca’s Breztri drove single-inhaler triple therapy uptake to more than 5.5 million global patients by 2024. Co-suspension formulations require dose uniformity across APIs with divergent solubilities, elevating the strategic weight of contract development. CMS is adding a new product category to the CMS-855S DMEPOS Enrollment Form for multi-function respiratory devices (excluding ventilators). This formalizes the inclusion of advanced, connected devices into Medicare reimbursement pathways.[3]Centers for Medicare & Medicaid Services. "Value-Based Care Models." CMS. https://www.cms.gov CDMOs that can align ISO 62304 software processes with GMP production attract sponsors seeking one-stop drug-device programs that compress timelines while satisfying regulators.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent, multi-region regulatory compliance burden | -1.3% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| High CAPEX for aerosol facilities and clean-room integration | -0.9% | Global, strongest barrier in emerging markets | Long term (≥ 4 years) |

| Supply risk for medical-grade propellants during HFC phase-out | -0.5% | Global, supply is concentrated in North America and Europe | Short term (≤ 2 years) |

| Scarcity of aerosol characterization talent and test capacity | -0.6% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent, Multi-Region Regulatory Compliance Burden

FDA’s 2024 draft guidance layered real-time stability and multi-flow aerodynamic testing across all inhaled products, adding 12-18 months and boosting pre-approval costs by up to 30%. EMA tightened dissolution and pharmacokinetic bridging requirements for device changes, forcing sponsors pursuing global launches to comply with divergent yet overlapping rules. CDMOs maintain parallel quality systems across FDA 21 CFR Part 211, EMA Annex 1, and PMDA, which raise overhead and constrain margins. Smaller providers without dedicated regulatory teams struggle, leading to market consolidation among larger firms that can shoulder evolving compliance demands.

High CAPEX for Aerosol Facilities and Clean-Room Integration

New ISO Class 7 inhalation facilities cost USD 50–150 million and include clean rooms, propellant bunkers, and a laser-diffraction suite. Kindeva’s USD 200 million Kansas City expansion highlighted the capital intensity needed to compete for commercial-scale MDI contracts. Emerging markets face even higher financing costs, which slow capacity growth in regions with the fastest increase in disease burden. High depreciation forces CDMOs to seek multi-year, high-volume contracts to recover investment, restricting price flexibility and raising entry barriers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Development Contracts Anchor Revenue, Clinical Scale Drives Growth

In 2025, contract development accounted for 37.09% of the inhalation CDMO market revenue, as sponsors prioritized risk reduction during formulation screening and device selection. Clinical manufacturing, however, is registering a 10.23% CAGR to 2031 on the back of an expanding cohort of Phase II and Phase III biologics programs. The inhalation CDMO market size allocated to development services has a higher gross margin profile than routine commercial production, as feasibility studies, analytical method development, and regulatory consulting command 50–60% gross margins.

The inhalation CDMO market sees service-mix value migrating upstream. CDMOs with earlier investments in spray-drying, lyophilization, and single-use bioreactors, such as Lonza, Catalent, and Hovione, capitalize on complex biologic demand. Lower-margin commercial campaigns are increasingly price-pressured by Asian plants offering 20–30% savings, which pushes Western providers to bundle packaging, labeling, and stability into single contracts. Ancillary services, such as post-approval change management, are expanding as sponsors seek to house lifecycle updates with partners who already hold validated dossiers.

By Product Type: MDI Dominance Persists, SMI Innovation Accelerates

Metered-Dose Inhalers retained 35.21% of 2025 revenue due to clinical familiarity and decades of manufacturing optimization that achieve fill-weight precision within ±3%. However, propellant scarcity and environmental pressure weigh on future growth, so sponsors are reassessing MDI life-cycle economics. Dry-Powder Inhalers hold about 30% share but confront performance variability across humidity and inspiratory flow. The inhalation CDMO market for soft-mist and nebulized systems is expected to grow at a 10.67% CAGR through 2031, driven by demand for propellant-free devices compatible with biologics.

Vibrating-mesh nebulizers entering hospital and home settings permit high-dose or large-molecule delivery without thermal degradation, opening specialty indications such as cystic fibrosis and pulmonary arterial hypertension. Sponsors pursuing personalized medicine increasingly request connected inhalers that feed real-time usage data into payer portals, which further elevates the technical bar for CDMOs.

Geography Analysis

North America held 44.25% of the inhalation CDMO market revenue in 2025 on the strength of the FDA’s streamlined 505(b)(2) pathway, a dense cluster of respiratory biotechs, and mature reimbursement that supports premium triple therapies. Europe remains fragmented yet sizable because EMA’s centralized procedure allows multi-country launches. Mexico is emerging as a nearshore commercial hub for Latin American distributors.

Asia-Pacific is projected to post an 11.14% CAGR through 2031, making it the fastest-rising regional contributor to Inhalation CDMO market growth. China’s NMPA has accelerated generic inhaler reviews, and India’s production-linked incentives now refund up to 8% of incremental sales to qualifying manufacturers. Japan’s aging population keeps demand steady, but local sourcing preferences limit foreign CDMO penetration. South Korea and Australia are growing as clinical trial hubs, while the Middle East, Africa, and South America present latent expansion opportunities that hinge on reimbursement modernization and currency stability.

Competitive Landscape

The inhalation CDMO market is moderately concentrated; the top five providers, Hovione, Lonza Group AG, Recipharm AB (EQT AB), Kindeva, and Iconovo, collectively hold significant shares. No single firm dominates because sponsors deliberately source from multiple suppliers to hedge supply risk, and technical diversity across formulation, device, and analytics keeps entry points varied. Novo Holdings’ USD 16.5 billion Catalent purchase in 2024 created a full-service entity spanning sterile fill, biologics, and inhalation, pressuring mid-tier players to niche up or scale out.

Competitive strategies cluster in three groups. Full-service integrators bundle development through commercial supply. Device specialists focus on proprietary actuators, valves, and, now, Bluetooth-enabled dose counters, with Aptar’s recent digital sensor acquisitions as a case in point. Formulation innovators focus on particle engineering IP and agile pilot suites; Bend Bioscience’s spray-drying patents underscore this model. White-space remains in nebulized biologics where cold chain, lyophilization, and single-use bioreactors intersect, and in propellant retrofits where validated HFO-1234ze lines are scarce.

Technology deployment continues to redraw competitive borders. Iconovo’s single-use DPI platform cuts tooling and time-to-clinic for early-stage programs. HCmed Innovations offers modular mesh nebulizers that adapt to multiple APIs without full revalidation. Patent filings in spray-drying nozzle geometry, electrostatic powder coating, and breath-actuated valves accelerated during 2025, suggesting that know-how, rather than pure capacity, will decide future market share.

Inhalation CDMO Industry Leaders

-

Hovione

-

Lonza Group AG

-

Recipharm AB (EQT AB)

-

Kindeva

-

Iconovo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Chiesi Group, a certified B Corp, expanded its long-standing partnership with Bespak, a specialist CDMO in pulmonary and nasal drug delivery. The collaboration increased pressurized metered dose inhaler (pMDI) manufacturing capacity at Bespak’s Holmes Chapel site to support the next phase of Chiesi’s Carbon Minimal Inhaler (CMI) program.

- July 2025: Hovione, a fully-integrated global CDMO, today announced the completion of an initial multi-million-dollar investment cycle to expand its manufacturing site in East Windsor, New Jersey. Upon completion, this world-class campus will cover more than 200,000 square feet and integrate the latest technologies into sustainably designed facilities. The initiative advances Hovione’s long-term strategy to grow its U.S. operations and enhance its integrated capabilities in drug substance, drug product intermediates, and drug products.

- July 2025: Transpire Bio announced a definitive agreement with Recipharm to develop TRB-1 and TRB-2, inhaled medicines for the treatment of asthma and Chronic Obstructive Pulmonary Disease (COPD). TRB-1 and TRB-2, the first products developed by Transpire Bio, will be indicated for the treatment of asthma and COPD and will be intended for advanced markets.

Global Inhalation CDMO Market Report Scope

As per the scope of the report, an inhalational CDMO is a contract development and manufacturing organization specializing in the formulation, testing, and production of inhalable drug products, including metered-dose inhalers (MDIs), dry powder inhalers (DPIs), nebulizers, and soft mist inhalers.

The inhalation CDMO market is segmented into service type, product type, and geography. By service type, the market is segmented into contract development, clinical manufacturing, commercial manufacturing, packaging & labelling, and other services. By product type, the market is segmented into metered-dose inhalers (MDI), dry-powder inhalers (DPI), nebulized formulations, soft-mist inhalers (SMI) & and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and trends for 17 countries across major regions worldwide. The report offers market size and forecasts in value (USD) for the above segments.

| Contract Development |

| Clinical Manufacturing |

| Commercial Manufacturing |

| Packaging & Labelling |

| Other Services |

| Metered-Dose Inhalers (MDI) |

| Dry-Powder Inhalers (DPI) |

| Nebulized Formulations |

| Soft-Mist Inhalers (SMI) & Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Contract Development | |

| Clinical Manufacturing | ||

| Commercial Manufacturing | ||

| Packaging & Labelling | ||

| Other Services | ||

| By Product Type | Metered-Dose Inhalers (MDI) | |

| Dry-Powder Inhalers (DPI) | ||

| Nebulized Formulations | ||

| Soft-Mist Inhalers (SMI) & Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Inhalation CDMO market?

The market reached USD 2.41 billion in 2026 and is forecast to hit USD 3.44 billion by 2031.

Which service line is growing fastest?

Clinical Manufacturing is increasing at a 10.23% CAGR as more inhalable biologics enter late-stage trials.

Why are sponsors outsourcing inhalation manufacturing?

ISO-class clean rooms, propellant storage, and specialized aerosol analytics carry high fixed costs that CDMOs have already absorbed.

Which region leads demand today?

North America holds 44.25% revenue share thanks to a dense biotech ecosystem and supportive regulatory pathways.

How will low-GWP propellant rules affect the sector?

CDMOs that have validated HFO-1234ze lines are poised to win reformulation contracts as HFC-134a supply tightens before 2030.

Who are the dominant market players?

Catalent (Novo Holdings), Lonza, Kindeva, Hovione, and Recipharm collectively command about half of global revenue.

Page last updated on: