Inhalable Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 31.70 Billion |

| Market Size (2031) | USD 41.30 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

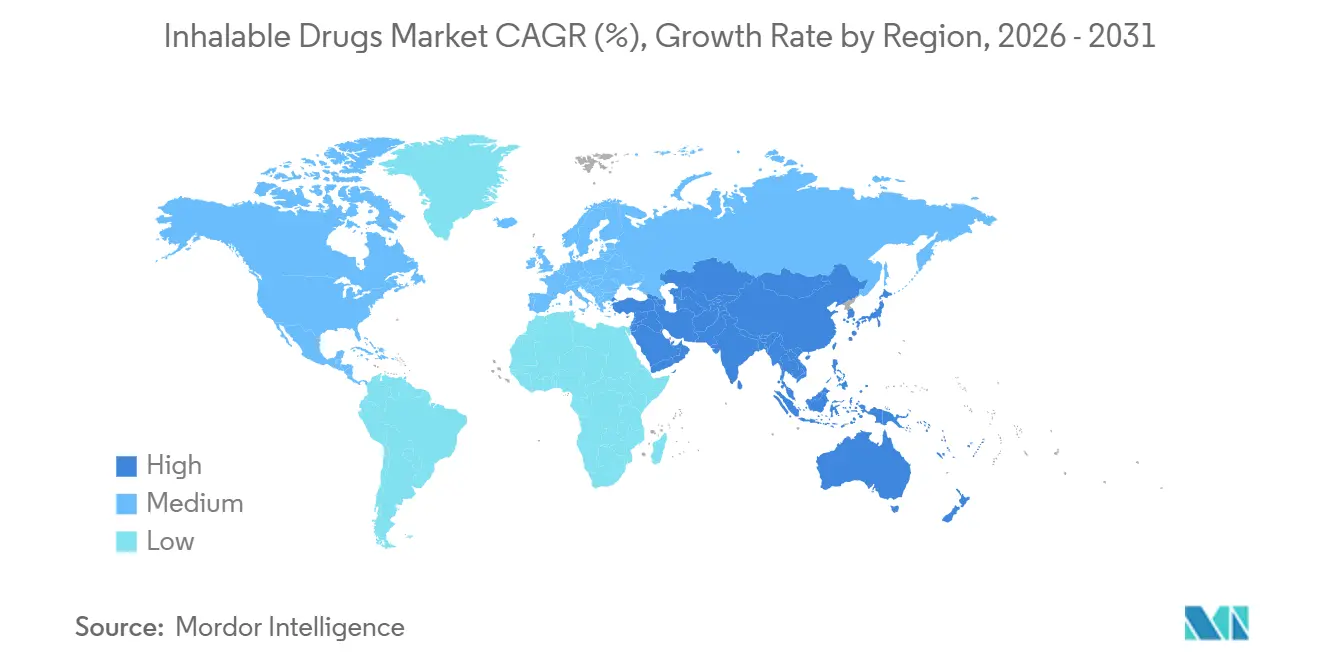

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Inhalable Drugs Market Analysis by Mordor Intelligence

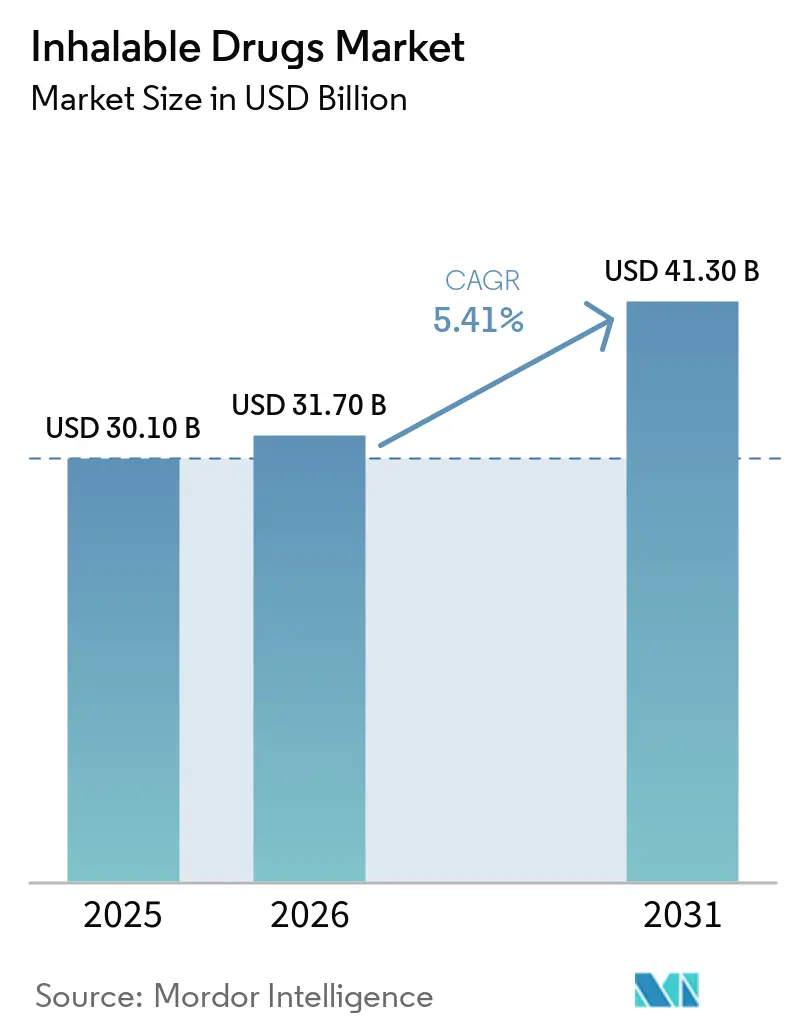

The Inhalable Drugs Market size is projected to expand from USD 30.10 billion in 2025 and USD 31.70 billion in 2026 to USD 41.30 billion by 2031, registering a CAGR of 5.41% between 2026 to 2031.

Demand is advancing as home-based respiratory care gains payer support, connected devices close adherence gaps, and manufacturers refresh metered-dose portfolios with low global warming potential propellants [1]World Health Organization, “Chronic Respiratory Diseases,” who.int. Rising prevalence of chronic respiratory conditions, generics that broaden access, and device-centric innovation are sustaining competitive momentum. Authorized generics have begun to erode branded prices, yet innovators offset margin pressure by layering device patents and digital ecosystems. Online pharmacies are reshaping distribution economics, while Asia-Pacific reimbursement expansions inject incremental volume. Manufacturers are also capturing niche systemic uses from pulmonary arterial hypertension to inhaled insulin, where rapid onset and reduced systemic exposure create clinical value.

Key Report Takeaways

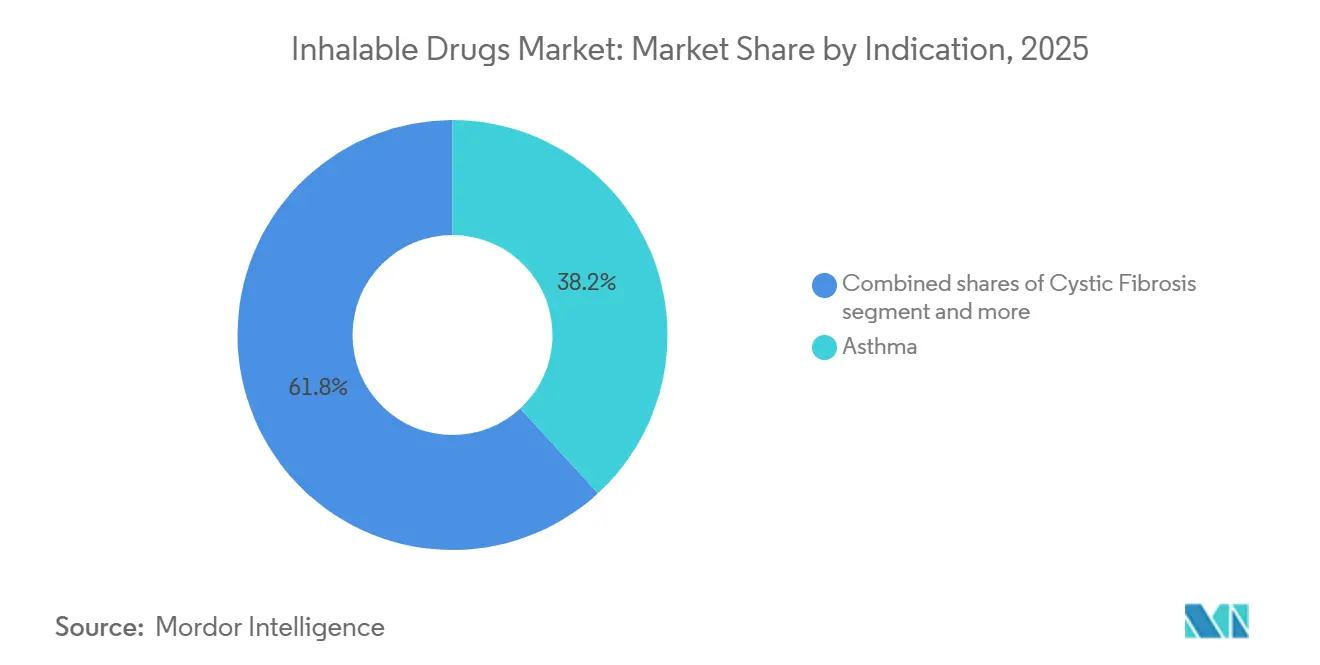

- By indication, asthma led the inhalable drugs market with 38.16% market share in 2025, whereas chronic obstructive pulmonary disease is forecast to advance at a 5.83% CAGR through 2031.

- By dosage form, metered-dose inhalers commanded 43.16% of the inhalable drugs market in 2025 and are the fastest-growing dosage form, with a 5.91% CAGR.

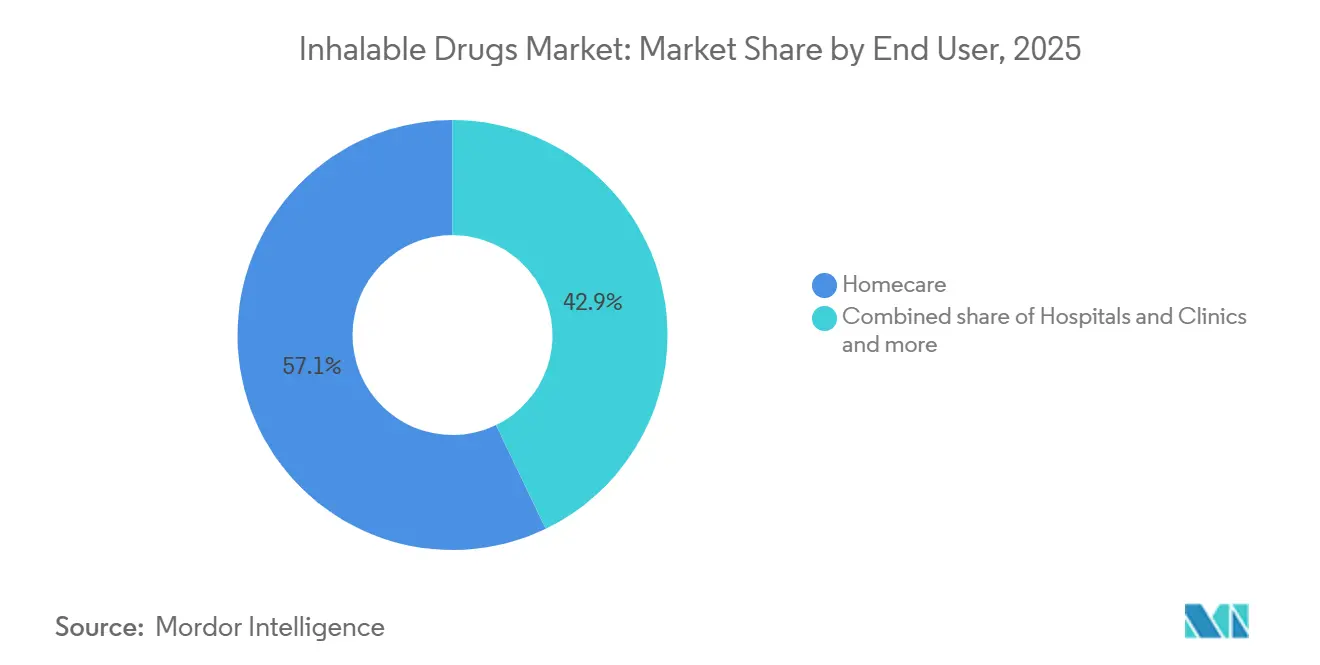

- By end user, home care settings accounted for 57.18% of revenue in 2025 and are expected to register a 5.87% CAGR through 2031.

- By distribution channel, retail pharmacies held 61.39% of the inhalable drugs market in 2025, while online pharmacies posted the highest growth rate at 6.01% through 2031.

- By geography, North America secured a 46.18% share in 2025; Asia-Pacific is expected to be the fastest-growing region at a 6.10% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Inhalable Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing global burden of asthma and COPD | +1.2% | Global, with the highest absolute growth in APAC and MEA | Long term (≥ 4 years) |

| Uptake of fixed-dose dual/triple inhalers improving outcomes | +0.9% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Expansion of home care and digital/smart inhalers | +1.1% | North America & Europe core, early adoption in urban APAC | Medium term (2-4 years) |

| Broadening access via generics and authorized generics | +0.7% | Global, with price-sensitive gains in APAC, Latin America, MEA | Short term (≤ 2 years) |

| Propellant transition (low-GWP MDIs) catalyzing portfolio refresh | +0.6% | North America & Europe are regulatory-driven, voluntary in APAC | Long term (≥ 4 years) |

| Non-respiratory systemic uses via inhalation (e.g., PAH DPI) | +0.3% | North America & Europe, niche expansion to Japan, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Global Burden of Asthma and COPD

According to a 2025 article by the National Library of Medicine, by 2050, it is projected that 15.58 billion cumulative COPD-related exacerbations will occur globally, a relative growth of 584% compared with 2025 [2]National Library of Medicine, “Forecasting the Global Economic and Health Burden of COPD From 2025 Through 2050,” nlm.nih.gov. Indoor biomass combustion still accounts for 40% of COPD cases in low-income regions, even as LPG subsidies scale. Aging populations in Japan, South Korea, and Southern Europe are increasing multimorbidity, boosting demand for combination inhalers. COPD incidence is climbing 2.1% annually in Asia-Pacific, outpacing available pulmonology capacity. Together, these forces underpin sustained volume growth for maintenance therapies that command premium pricing relative to short-acting agents.

Uptake of Fixed-Dose Dual/Triple Inhalers Improving Outcomes

AstraZeneca’s KALOS and LOGOS trials showed 24% fewer COPD-related hospitalizations with a single inhaler combining three active agents compared with dual therapy, prompting payer upgrades in Germany and the UK [3]AstraZeneca, “KALOS and LOGOS Phase III Results,” astrazeneca.com. Chiesi’s triple MDI filing under the 505(b)(2) pathway targets U.S. approval in 2026 and a cohort of 1.2 million patients currently juggling multiple devices. Prescribers increasingly prefer integrated regimens that reduce pharmacy errors and improve six-month persistence, cannibalizing standalone LABA-ICS revenue but reinforcing branded leadership in severe disease.

Expansion of Homecare and Digital/Smart Inhalers

The ACCEPTANCE RCT recorded a significant increase in adherence and a notable reduction in rescue inhaler use when Bluetooth sensors were paired with mobile coaching. Propeller Health’s Hailie platform streams dose-time-stamp data to clinicians, while Teva’s ProAir Digihaler measures inspiratory flow and flags technique errors. CMS added connected inhalers to durable medical equipment codes in 2025, accelerating Medicare Advantage uptake. Europe reimburses only when cost-effectiveness files demonstrate savings from avoided exacerbations. Urban APAC adoption is rising, yet rural connectivity barriers temper progress.

Broadening Access via Generics and Authorized Generics

Teva’s U.S. generic Advair captured notable share within nine months, compressing reference-product prices by 35%. Viatris and Mylan deploy authorized generics to defend volume, especially where substitution laws bypass prescriber consent, but revenue still fragments. Cipla and Glenmark export WHO-prequalified devices to Africa and Southeast Asia, cutting prices to levels affordable for low-income households. FDA draft guidance on plume geometry and APSD matching lengthens time-to-market, yet generic penetration in U.S. MDIs reached a significant portion of prescriptions in 2025, steering originators toward digital services for differentiation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying generic competition and price pressure | -0.8% | North America & Europe, spreading to APAC tender markets | Short term (≤ 2 years) |

| Inhaler technique errors and adherence gaps | -0.6% | Global, with highest clinical impact in low-resource settings | Medium term (2-4 years) |

| Complex-generic/device regulatory hurdles slowing launches | -0.4% | North America & Europe, less pronounced in APAC | Medium term (2-4 years) |

| Propellant supply/transition constraints elevating COGS | -0.3% | Global manufacturing, acute in North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intensifying Generic Competition and Price Pressure

Generic share of U.S. MDI scripts jumped significantly from 2022 to 2025 as multiple bioequivalents launched, slashing branded ASPs by one-third. Tender systems in Europe and Latin America now benchmark inhaler prices to generic levels, even in the absence of direct substitutes, while PBMs in the U.S. enforce lowest-acquisition-cost formulas. Shrinking margins shift R&D toward high-barrier biologic-device combinations, leaving incremental small-molecule improvements underfunded.

Inhaler Technique Errors and Adherence Gaps

Clinical audits reveal that majority of patients commit critical inhalation errors, driving poor lung deposition and a significant rise in exacerbations. Dry powders demand inspiratory flow rates that elderly COPD patients cannot reach, whereas MDIs require hand–breath coordination that children often miss. Valved holding chambers help, but add cleaning burdens that deter use. Digital tutorials and pharmacy demonstrations improve outcomes but remain unscalable in settings with low clinician-to-patient ratios and limited broadband access.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Indication: COPD Momentum Reshaping the Mix

COPD revenue is expanding at a 5.83% CAGR and is closing the gap with asthma, which retained 38.16% inhalable drugs market share in 2025. Late diagnoses in emerging markets push patients onto higher-priced triple regimens, and smoke exposure keeps incidence climbing. Cystic fibrosis therapies serve roughly 100,000 patients yet enjoy chronic daily dosing, while pulmonary arterial hypertension inhalables captured a modest share of 2025 revenue following treprostinil DPI approval. Non-tuberculous mycobacterial lung disease is advancing annually due to environmental aerosol exposure, widening the niche for liposomal amikacin. Diabetes inhalation therapy remains a sub-0.5% sliver because payers mandate failure on injections first.

COPD’s acceleration realigns product strategy toward long-acting bronchodilators with anti-inflammatory co-formulation. United Therapeutics’ treprostinil DPI and Insmed’s liposomal antibiotic illustrate movement into systemic or orphan realms where robust pricing offsets small populations. As incidence skews older, developers bundle telemonitoring and technique-coaching services to bolster persistence, creating barriers to pure-price generics.

By Dosage Form: Low-GWP Mandates Reinforce MDI Supremacy

Metered-dose inhalation led with a 43.16% share of the inhalable drugs market in 2025 and will grow at 5.91% through 2031 as HFO-1234ze propellant conversions reset patent life. Dry-powder devices hold a significant share of volume and appeal to eco-conscious prescribers, yet inspiratory-flow demands limit pediatrics and severe COPD use. Nebulizers remain critical in hospital settings where coordination is impossible, and mesh technology reduces treatment time to 5 minutes. Soft-mist platforms achieve 50% lung deposition, supporting once-daily dosing.

Portfolio refresh costs and propellant supply constraints incentivize companies to pivot toward connected MDIs that capture real-world use data. Dry-powder entrants counter with breath-actuated simplicity and zero propellant footprint. Competitive positioning thus hinges on device ergonomics, digital overlays, and carbon-label disclosures rather than chemistry alone.

By End User: Payers Propel Homecare Dominance

Homecare accounted for 57.18% of 2025 revenue and posted a 5.87% CAGR to 2031 as connected devices slash acute-care spending. Hospitals and clinics remain initiation settings for complex therapies like treprostinil DPI, but patients transition to maintenance volume at home within weeks. Specialty clinics, especially cystic fibrosis centers, anchor dosage optimization and training but represent a modest share of revenue.

Remote coaching, auto-refill logistics, and data-sharing dashboards entice payers eager to meet value-based-care targets. ISO 20072 standardization enables firms to market a single configuration for both hospital and home use, reducing SKU complexity. Asia-Pacific uptake is uneven—urban telehealth thrives, rural regions still rely on in-person dispensing.

By Distribution Channel: E-Commerce Outpaces Brick-and-Mortar

Online pharmacies are scaling at 6.01% per year, propelled by telehealth workflows that persisted post-pandemic. Retail pharmacies keep 61.39% share but face reimbursement clawbacks and a generic-induced margin squeeze. Hospital pharmacies accounted for a notable market share and remain gatekeepers for inpatient formularies negotiated via GPOs.

E-commerce vendors bundle adherence coaching and digital coupons, winning refill loyalty. U.S. DEA prescription-validation rules and the EU’s serialization mandate add compliance cost, but also curb counterfeit risk. Retail giants now acquire tech startups to defend volume, while manufacturers build direct-to-patient portals that bypass traditional wholesalers, redrawing the channel power balance.

Geography Analysis

North America held a 46.18% share in 2025, as patent cliffs invite generic erosion and PBMs press for discounts. CMS reimbursement for connected devices accelerates adoption of Hailie and Digihaler platforms, partially offsetting price deflation. Canada’s pricing alliance cut branded combination inhaler costs by up to 50%, while Mexico’s expanded coverage lifts generic DPI volume.

Asia-Pacific is the fastest-growing region at a 6.10% CAGR. China added 18 inhalers to its 2025 reimbursement list, significantly slashing patients' out-of-pocket expenses. India’s Ayushman Bharat covers 500 million people, but rural distribution gaps hamper uptake. Persistent PM2.5 exposure increases COPD incidence by 2.1% annually, expanding the addressable demand. Japan approved liposomal amikacin for NTM lung disease, while Australia struck risk-sharing deals to cap government spending on triple therapies.

Europe commands a significant share, tempered by tenders that pull branded prices within 15% of generics. NHS carbon footprint data motivates prescribers to switch to dry-powder devices. EMA low-GWP guidance spurs rapid MDI reformulations, absorbing capital. Germany reimburses digital inhalers under DiGA rules, paying EUR 250–400 annually when apps document savings. Middle East and Africa grow notabaly driven by Saudi Vision 2030 spending, while South America’s rise follows Brazil’s inhaler subsidies and Argentina’s domestic DPI approval.

Competitive Landscape

Competition is moderately concentrated: the top players controlled significant share of 2025 revenue. AstraZeneca leverages Cognita Labs AI coaching on Symbicort, transforming drug-device pairs into software-anchored services. GSK extends exclusivity for Trelegy via 37 device patents, while Boehringer Ingelheim invests EUR 150 million to expand soft-mist capacity that meets EU climate rules.

Smaller innovators target orphan or systemic niches: United Therapeutics’ treprostinil DPI hit USD 180 million in first-year sales as patients abandoned nebulizers, and Insmed’s liposomal antibiotic reached USD 450 million from a base of under 15,000 patients. Device and regulatory hurdles raise entry barriers; ISO 20072 and FDA plume-geometry tests complicate generic replication, favoring incumbents who marry manufacturing know-how with digital ecosystems.

Strategic moves in 2025-2026 include Merck’s USD 10 billion acquisition of Verona Pharma for ensifentrine, Cipla’s purchase of South Africa’s Pharma Dynamics for capacity and access, and Novartis' divestiture of Xolair auto-injectors to fund inhaled biologics. Authorized generics protect volume but self-cannibalize revenues, while online pharmacy partnerships secure data visibility and reduce rebate leakage.

Inhalable Drugs Industry Leaders

Boehringer Ingelheim International GmbH

Chiesi Farmaceutici S.p.A.

Novartis AG

GSK plc

AstraZeneca plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Qnovia, Inc., a pharmaceutical and medtech company specializing in inhaled therapeutics, announced favorable results from its Phase 1 clinical trial for RespiRx, a handheld inhalable nicotine replacement therapy (NRT).

- October 2025: Merck & Co. completed a USD 10 billion acquisition of Verona Pharma, adding Ohtuvayre, a first-in-class inhaled maintenance therapy for COPD, to its cardiopulmonary portfolio.

Global Inhalable Drugs Market Report Scope

As per the scope of the report, inhalable drugs are medications or substances delivered directly to the respiratory system through the nose or mouth, typically used to treat lung conditions or achieve rapid systemic effects. This administration route is highly effective because it targets the site of action, such as the airways in asthma or chronic obstructive pulmonary disease (COPD), allowing for a faster onset of action and lower required doses compared to oral or injectable methods.

The inhalable drugs market is segmented by indication, dosage form, end users, distribution channel, and geography. By indication, the market is segmented into asthma, chronic obstructive pulmonary disease, cystic fibrosis, pulmonary arterial hypertension / PH-ILD, non-tuberculous mycobacterial (NTM) lung disease, and diabetes. By dosage form, the market is segmented into metered-dose inhalers, dry powder inhalers, nebulized solutions, and soft mist inhalers. By end users, the market is segmented into home care, hospitals & clinics, and specialty clinics. By distribution channel, the market is segmented into retail pharmacies, hospital pharmacies, and online pharmacies. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Asthma |

| Chronic Obstructive Pulmonary Disease (COPD) |

| Cystic Fibrosis |

| Pulmonary Arterial Hypertension / PH-ILD |

| Non-tuberculous Mycobacterial (NTM) Lung Disease |

| Diabetes |

| Metered-Dose Inhalation |

| Dry Powder Inhalation |

| Nebulized Solutions |

| Soft Mist Inhalation |

| Homecare / Self-administration |

| Hospitals & Clinics |

| Specialty Clinics |

| Retail Pharmacies |

| Hospital Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Indication | Asthma | |

| Chronic Obstructive Pulmonary Disease (COPD) | ||

| Cystic Fibrosis | ||

| Pulmonary Arterial Hypertension / PH-ILD | ||

| Non-tuberculous Mycobacterial (NTM) Lung Disease | ||

| Diabetes | ||

| By Dosage Form | Metered-Dose Inhalation | |

| Dry Powder Inhalation | ||

| Nebulized Solutions | ||

| Soft Mist Inhalation | ||

| By End User | Homecare / Self-administration | |

| Hospitals & Clinics | ||

| Specialty Clinics | ||

| By Distribution Channel | Retail Pharmacies | |

| Hospital Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What growth rate is the inhalable drugs market projected to post through 2031?

The inhalable drugs market is expected to record a 5.41% CAGR from 2026 to 2031.

Which therapeutic area is growing the fastest in inhalable treatments?

COPD therapies are growing at 5.83% per year, outpacing asthma therapies.

What is the market size for Inhalable Drugs Market

The Inhalable Drugs Market size is projected to expand from USD 30.10 billion in 2025 and USD 31.70 billion in 2026 to USD 41.30 billion by 2031, registering a CAGR of 5.41% between 2026 to 2031.

How are connected inhalers influencing payer strategies?

Real-time adherence data lowers exacerbation-related hospital visits by about 30%, prompting CMS and European insurers to reimburse smart devices.

Page last updated on: