Infant Oxygen Hoods Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

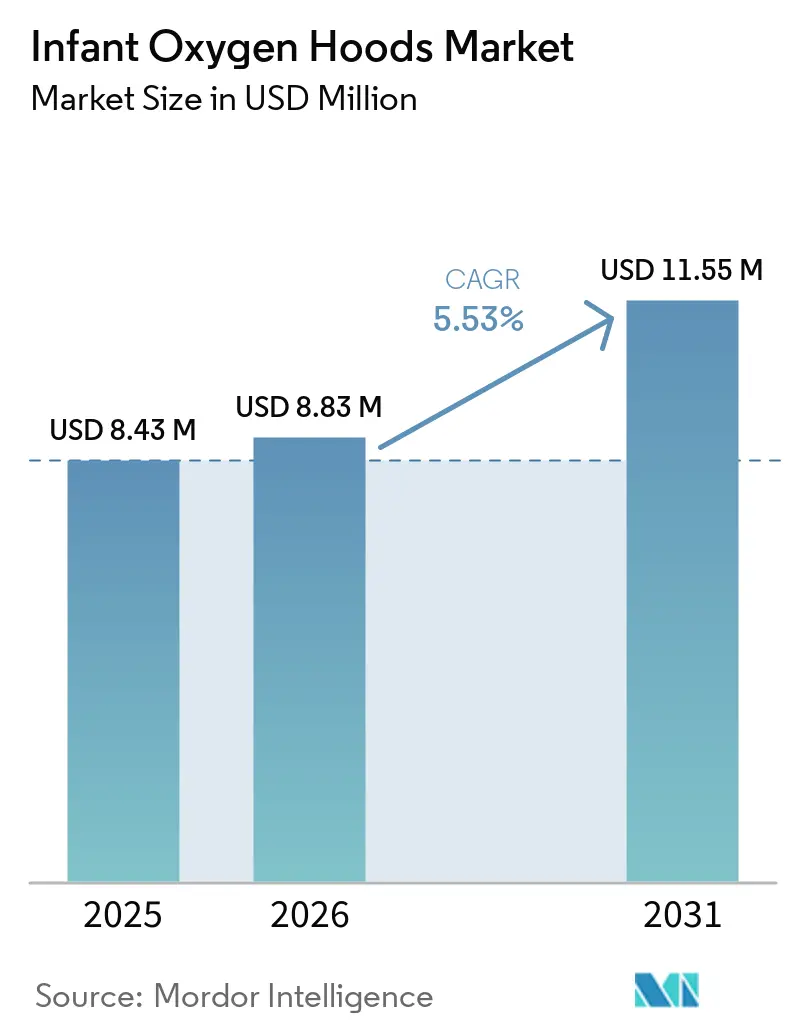

| Market Size (2026) | USD 8.83 Million |

| Market Size (2031) | USD 11.55 Million |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

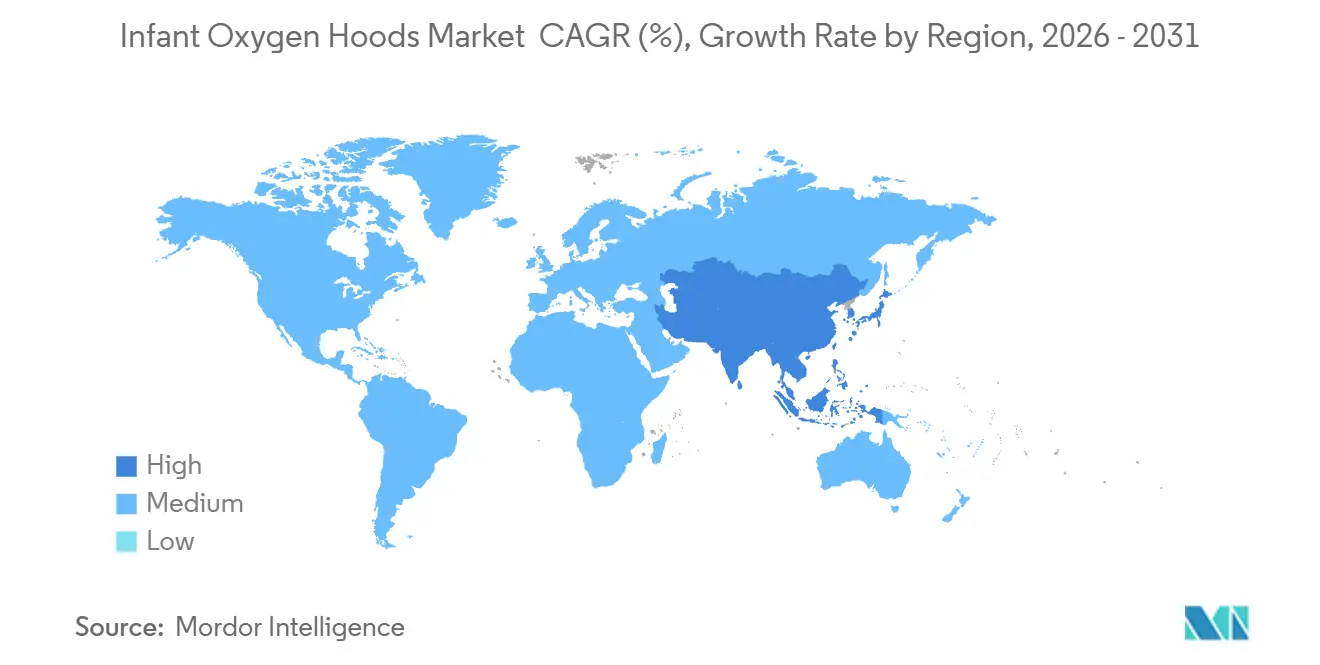

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Infant Oxygen Hoods Market Analysis by Mordor Intelligence

The Infant Oxygen Hoods Market size is projected to expand from USD 8.43 million in 2025 and USD 8.83 million in 2026 to USD 11.55 million by 2031, registering a CAGR of 5.53% between 2026 to 2031.

Uptake is supported by infection-prevention priorities that favor single-patient-use devices, along with design advances that improve CO2 washout and caregiver access during short stabilization windows. The infant oxygen hoods market is also shaped by the persistence of preterm births in high-income systems like the United States, where the 2024 preterm rate held at 10.4%, sustaining a baseline need for supplemental oxygen in immediate postnatal care. Competition from high-flow nasal cannula and CPAP defines the clinical boundary, with hoods retained for cases where nasal interfaces are not tolerated or contraindicated, and for lower-acuity or resource-limited contexts where rapid setup and minimal training are critical. Infection-control concerns that intensified during COVID-19 continue to steer procurement toward disposable options in maternity and pediatric wards, as well as emergency and transport settings that prioritize turnover and hygiene safeguards. Engineering features such as dispersed gas inlets to promote uniform oxygen distribution and CO2 washout, and ports to facilitate monitoring access, are now baseline expectations in premium products. A niche opportunity is opening for inhaled nitric oxide delivery via hood in select term neonates with mild-to-moderate pulmonary hypertension, which could gradually support premium-price devices if adoption expands within tertiary protocols.

Key Report Takeaways

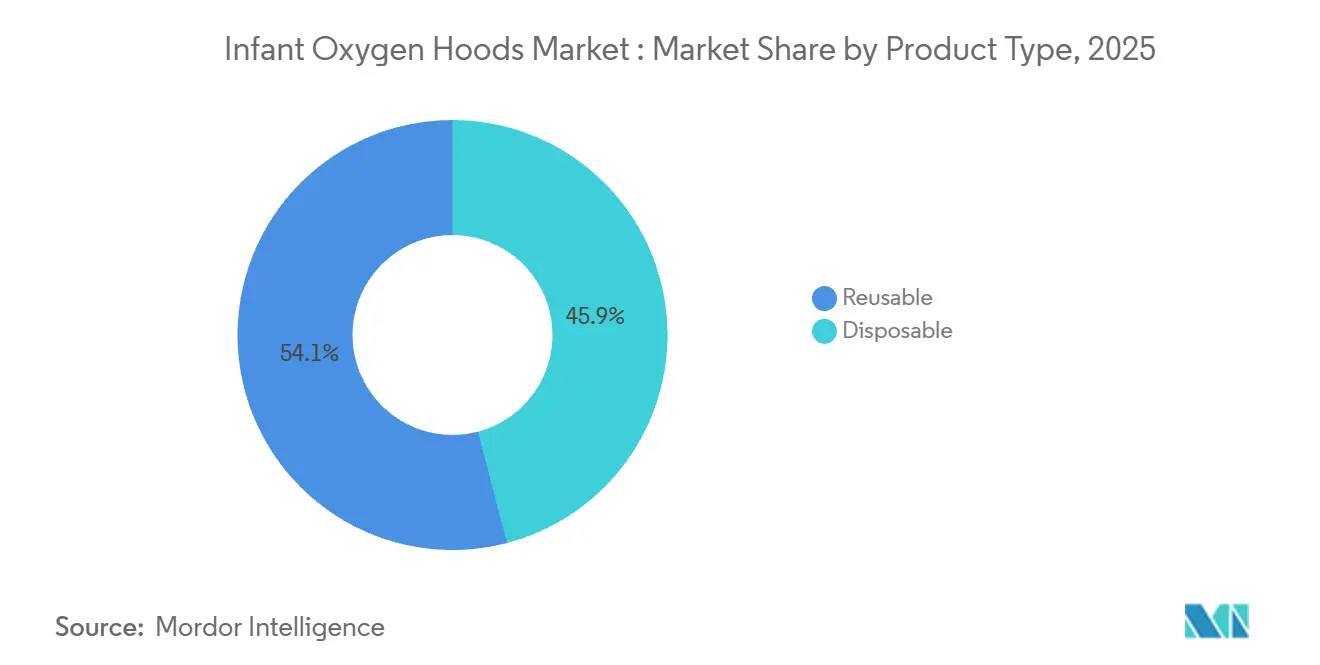

By product type, reusable oxygen hoods held 54.08% share in 2025, while disposables are projected to expand at a 6.57% CAGR to 2031.

By end user, level III/IV NICUs led with 45.24% share in 2025, while maternity or birthing centers and pediatric wards or ERs are forecast to grow at a 6.30% CAGR through 2031.

By geography, North America commanded 46.11% share in 2025, while the Asia Pacific is the fastest-growing region at a 6.24% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Infant Oxygen Hoods Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising preterm births and neonatal hypoxemia burden | +1.8% | Global, with acute pressure in Sub-Saharan Africa, South Asia | Long term (≤ 4 years) |

| NICU/SNCU capacity expansion in emerging markets | +1.2% | Asia Pacific (India, Indonesia, China), Nigeria | Medium term (2-4 years) |

| Clinical guidance formalizing oxygen hood use in defined scenarios | +0.7% | North America, Western Europe | Medium term (2-4 years) |

| Availability of disposable hoods for infection control | +1.4% | Global, spill-over to maternity care deserts in rural United States | Short term (≤ 2 years) |

| Feasibility of iNO delivery via oxygen hood in select term neonates | +0.3% | High-income markets, niche tertiary centers | Long term (≥ 4 years) |

| Design advances improving CO2 washout and caregiver access | +0.6% | North America, Asia Pacific core | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Preterm Births and Neonatal Hypoxemia Burden

Preterm births remain a stable driver of neonatal oxygen needs in high-income markets, with the United States recording a 2024 preterm rate of 10.4%, indicating steady inflows of infants at risk of hypoxemia who require carefully titrated oxygen therapy in early life[1]Brady E. Hamilton, Joyce A. Martin, and Michelle J.K. Osterman, “Births: Provisional Data for 2024"Centers for Disease Control and Prevention. Oxygen hoods offer a non-contact alternative for newborns that do not tolerate nasal prongs or CPAP interfaces during short stabilization periods, helping reduce nasal trauma when tissue integrity is fragile. Their utility is bounded by the absence of positive end-expiratory pressure, which limits application to oxygenation support rather than lung recruitment strategies that CPAP provides in surfactant-deficient or atelectatic lungs. Narrow oxygen saturation targets for preterm infants reinforce the need for tight FiO2 control and continuous monitoring, with guidelines emphasizing ranges around 90–95% in extremely low-birth-weight infants to mitigate retinopathy of prematurity and bronchopulmonary dysplasia risk. These clinical parameters preserve a targeted place for oxygen hoods in the infant oxygen hoods market, particularly for brief use cases that do not require positive pressure, while ensuring monitoring and escalation protocols are readily available.

NICU/SNCU Capacity Expansion in Emerging Markets

Government-backed neonatal-care upgrades in Asia and Africa are expanding the installed base for essential respiratory equipment, including oxygen hoods in level II and district facilities where noninvasive positive-pressure systems are not always present. Indonesia’s Sawahlunto Regional General Hospital opened a four-bed NICU and four-bed pediatric ICU in April 2026, funded by Special Allocation Funds totaling Rp 2.4 billion, with integration into SIHREN to strengthen referral alignment and standardize equipment across facilities. A WHO-supported model estimates that low and middle-income countries require 2.8 neonatal beds per 1,000 live births at 85% occupancy, exceeding current capacity in several regions, which raises demand for hygiene-focused consumables as facilities add beds and staff[2]Bireshwar Sinha, “Estimating the Number of Hospital Beds for the Care of Sick and Small Newborns: An Evidence-Based Systematic Approach,” Journal of Global Health. China’s tiered capability lists specify that county-level units should stabilize moderate acuity cases and deliver CPAP for defined durations before escalation, a framework that also accommodates oxygen hoods for cases where nasal interfaces are not tolerated during initial stabilization. As systems expand, disposable consumables are favored for infection control and fast turnover, while reusable hoods remain present where sterilization workflows are well-managed and operating budgets are tight, positioning the infant oxygen hoods market to serve distinct price and performance tiers across geographies. Funding from multilateral partners, such as the World Bank’s financing to strengthen Nigeria’s primary healthcare network with oxygen access and neonatal resuscitation equipment, further broadens the addressable base for basic respiratory consumables.

Availability of Disposable Hoods for Infection Control

Hospitals continue to prioritize single-patient-use devices to reduce hospital-acquired infection risk, a priority that intensified during the COVID-19 era and that directly benefits disposable oxygen hoods in maternity and pediatric units where turnover is high. Disposable hoods eliminate reprocessing steps and the risk that inconsistent sterilization leaves residual pathogens on internal surfaces, which aligns with staff safety protocols and environmental hygiene programs in neonatal care. Vendors emphasize design features that disperse gas inlets along the inner surface to promote uniform FiO2 distribution and facilitate CO2 washout while maintaining visualization, which reinforces the infection-control and workflow value proposition in the infant oxygen hoods market. Standardized procurement frameworks that include Indonesia’s SIHREN reinforce single-use specifications and infection-prevention criteria for NICU and pediatric equipment across both urban and rural facilities. MDR and ISO 13485 certifications further steer purchasing toward compliant disposable portfolios supplied by vendors with established quality systems and post-market surveillance, improving supply assurance for high-throughput care areas. These infection-control and compliance dynamics support steady share gains for disposables within the infant oxygen hoods market as providers seek simple, hygienic oxygenation during short stabilization windows.

Clinical Guidance Formalizing Oxygen Hood Use in Defined Scenarios

Professional guidance continues to clarify that oxygen hoods are not routinely recommended and should be reserved for cases where nasal cannulae or CPAP are contraindicated or poorly tolerated, which preserves defined stabilization roles for hoods and prevents inappropriate substitution for positive-pressure support. Narrow SpO2 targets for preterm infants require real-time monitoring and rapid FiO2 adjustments, and codified targets improve bedside decision-making when hoods are used for brief periods before escalation, supporting consistent practice in the infant oxygen hoods market. Stabilization algorithms that prioritize escalation to CPAP or HFNC when recruitment is needed, combined with explicit exceptions that allow hood use for interface intolerance, reduce variability and align care teams on when passive oxygen delivery is acceptable. Country-level capability frameworks, such as China’s tiered neonatal lists, also delineate which units handle moderate acuity cases locally and when to refer, which helps embed oxygen hoods within initial stabilization workflows at county-level facilities. This codification encourages targeted procurement, supports training, and sustains a baseline of hood use across non-tertiary and transport contexts where fast setup and minimal nasal contact are priorities. As guidance harmonizes across regions, the infant oxygen hoods market benefits from clearer indications that align with safety goals and escalation pathways in neonatal respiratory care.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to HFNC/CPAP, reducing routine hood use | -2.1% | North America, Western Europe, and tertiary centers in the Asia Pacific | Short term (≤ 2 years) |

| CO2 retention risk and variable FiO2 without analyzer | -0.8% | Global, especially resource-limited settings lacking capnography | Medium term (2-4 years) |

| Regulatory compliance burden under EU MDR and United States FDA QMSR | -0.6% | North America, Europe | Medium term (2-4 years) |

| Supply chain fragility for medical-grade polymers and components | -0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift to HFNC/CPAP Reducing Routine Hood Use

HFNC and CPAP have become first-line modalities for noninvasive neonatal respiratory support in tertiary environments, limiting oxygen hoods to defined indications such as poor tolerance of nasal interfaces or short stabilization prior to escalation. In a pediatric critical care RCT across 25 U.K. units, HFNC was non-inferior to CPAP for time to liberation from respiratory support, though post-extubation outcomes favored CPAP for key endpoints, reinforcing CPAP’s preferred role when positive-pressure support is a priority. A tertiary-center study comparing bubble CPAP to heated humidified HFNC in neonates reported shorter durations of respiratory support and ventilator days in CPAP cohorts, which strengthens the case for CPAP in acute management where pressure support is crucial. These clinical patterns confine the infant oxygen hoods market to scenarios where passive oxygen delivery suffices and where nasal contact is contraindicated or poorly tolerated, as well as to lower-acuity points of care that lack complex equipment or a respiratory therapist. In this environment, vendors emphasize ease of use and fast setup, while maintaining integration options for escalation pathways that involve CPAP and HFNC within the same care episode.

CO2 Retention Risk and Variable FiO2 Without Analyzer

Oxygen hoods do not provide closed-circuit control of FiO2, and the actual oxygen concentration at the infant’s airway varies with flow rate, hood volume, and patient ventilation, which complicates rapid titration to target saturations without real-time monitoring. Clinical guidance emphasizes narrow saturation targets for very preterm infants, which requires reliable monitoring and quick adjustments to avoid hyperoxia or hypoxia episodes that are linked to adverse outcomes. Hoods also demand vigilant CO2 washout, since inadequate outlet flow or obstructed ports can allow accumulation, especially when respiratory drive is depressed, raising the importance of good design and monitoring. Enhanced hood designs disperse gases along inner surfaces to improve CO2 clearance and promote more uniform FiO2, but these engineering refinements do not replace positive-pressure support when lung recruitment is needed. Heightened regulatory scrutiny through the United States FDA’s Quality Management System Regulation, effective February 2, 2026, and aligned to ISO 13485, reinforces expectations for robust validation of oxygen delivery performance and post-market surveillance in neonatal applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Disposables Propel Infection-Control Shift

Disposable oxygen hoods accounted for 45.92% in 2025 and are projected to grow at a 6.57% CAGR through 2031, reflecting infection-control mandates and the operational need for single-patient-use devices during rapid patient turnover in maternity and pediatric units. Reusable hoods held 54.08% of 2025 volume, supported by budget-constrained facilities with established sterilization workflows, although reprocessing complexity and the risk of suboptimal disinfection have led many providers to prioritize disposables in new tenders. The infant oxygen hoods market is seeing greater attention to materials, such as bio-based polymers and plasticizer-free resins, in line with sustainability standards that complement infection-control objectives in high-throughput care areas. Engineering choices that spread gas inlets along the hood surface, along with transparent shells that improve visualization and access for care procedures, have become differentiators as hospitals aim to reduce setup friction in busy delivery suites and pediatric emergency rooms. Infection-prevention policies influenced by COVID-19-era safeguards further entrench disposables in environments with limited sterilization capacity or where staff protection protocols prioritize filtered expiratory pathways and minimized reuse.

Disposable models align with purchasing frameworks that aim to streamline compliance with MDR, ISO 13485, and related quality standards, since single-use devices reduce the burden of validating reprocessing instructions across diverse hospital protocols and equipment fleets. In the infant oxygen hoods market, vendors with broader neonatal respiratory portfolios bundle hoods with CPAP interfaces and ventilator circuits to leverage scale in procurement, an approach that supports education and cross-training for escalation pathways within a single vendor ecosystem. For resource-limited hospitals that maintain effective sterilization departments, reusable hoods remain relevant as a cost-control measure, although recurring labor and quality assurance checks add hidden costs that are increasingly scrutinized in tenders focused on hygiene and turnaround times[3]Bradley G. Carter, “Making Respiratory Care Safe for Neonatal and Paediatric Intensive Care Unit Staff: Mitigation Strategies and Use of Filters,” Canadian Journal of Respiratory Therapy. On balance, disposables continue to gain share as the infant oxygen hoods market size for disposables is projected to expand in line with infection prevention and sustainability specifications embedded in global procurement standards.

By End User: Maternity Centers and Pediatric Wards Narrow Tertiary NICU Gap

Level III and IV NICUs held 45.24% of the 2025 share, reflecting their high-acuity case mix and comprehensive respiratory capabilities, including HFNC and CPAP that often supersede hoods for ongoing support. Protocols in these settings reserve hoods for brief stabilization or for infants who cannot tolerate nasal interfaces, consistent with guidance that prioritizes active pressure support for extubation failure prevention and lung recruitment when indicated. As capacity expands in emerging markets, more level II or county-level units are tasked with managing moderate acuity cases locally before referral, which creates a steady need for basic oxygen delivery that can be set up quickly with minimal training. These patterns anchor the infant oxygen hoods market in a clearly defined set of clinical contexts that benefit from non-contact oxygenation, simple setup, and compatibility with early stabilization workflows.

Maternity or birthing centers and pediatric wards or ERs represent the fastest-expanding end-user group at a 6.30% CAGR, supported by equipment strategies that emphasize disposables for infection control and near-continuous patient turnover. In several countries, policy-led upgrades to district and primary facilities now include oxygen concentrators, pulse oximeters, and basic neonatal resuscitation equipment, providing the foundation for supplemental oxygen delivery in the first hours of life. This tier often lacks the staff capacity for complex setup and monitoring, which elevates the value proposition of hoods for short-duration stabilization until escalation or transfer. For these end users, the infant oxygen hoods market size is projected to expand alongside standardized procurement frameworks that codify single-use consumables for hygiene and compliance reasons. Vendors emphasize clear access to the infant’s head and neck, humidity options, and monitoring ports to support workflows led by delivery and pediatric teams that may not include specialized respiratory therapists.

Geography Analysis

North America held 46.11% of 2025 revenue, driven by strong adoption of disposables in tertiary NICUs and maternity hospitals, tight infection-control standards, and payment models that accommodate single-use respiratory consumables. The region also sustains baseline demand as the United States preterm rate remained at 10.4% in 2024, which supports the need for supplemental oxygen during early stabilization despite the dominance of HFNC and CPAP in ongoing management. In this environment, hoods are most common when nasal interfaces are contraindicated, during short stabilization periods in labor and delivery, and in rural hospitals that focus on immediate postnatal care prior to transfer. Supply chain sensitivity persists, with some vendors reporting resin and silicone constraints that weighed on device shipments in 2024, underscoring the importance of diversified inputs and inventory buffering in neonatal consumables. As a result, the infant oxygen hoods market continues to track hospital purchasing policies that align hygiene, availability, and ease of use.

Europe’s procurement landscape is shaped by the Medical Device Regulation, which adds cost and time for reapproval of legacy devices and raises evidence expectations for clinical evaluations and post-market surveillance. Vendors with early MDR certification leverage that status to ensure continuity of supply across large hospital networks, including for accessory consumables that complement ventilators and CPAP. Framework agreements that prioritize comprehensive respiratory platforms influence consumable adoption paths, often bundling circuits, interfaces, and compatible hoods to streamline service and training. These dynamics keep oxygen hoods in ancillary roles for defined use cases, while procurement concentrates on multi-modality systems that deliver both positive-pressure support and passive oxygenation. Within this construct, the infant oxygen hoods market share is sustained by facilities that value disposable options for infection control and transparent shells that simplify procedures at the bedside.

Asia Pacific is the fastest-growing region at a 6.24% CAGR, reflecting significant public investment in neonatal beds and tiered capability frameworks that expand care closer to where births occur. Indonesia’s integration of new NICU capacity into its referral network is an example of how standardized procurement, including disposable oxygen hoods, can extend neonatal stabilization capabilities in both urban and rural districts. China’s modified Delphi approach for neonatal units clarifies the scope of county-level care and escalation pathways, which helps define where oxygen hoods fit within stabilization workflows alongside CPAP [4]Xing Li, “Development of Capability Lists for Neonatal Critical Care at Three Levels in China,” BMJ Paediatrics Open. In Africa and the Middle East, multilateral financing programs that upgrade primary and referral facilities with oxygen access and neonatal resuscitation equipment expand the addressable base for basic respiratory consumables.

Competitive Landscape

The infant oxygen hoods market is moderately fragmented, with a cohort of specialized neonatal device firms and integrated respiratory suppliers competing on infection-control features, regulatory credentials, and distribution reach. Established players emphasize robust quality systems to navigate MDR, MDSAP, and the United States QMSR, a posture that supports continuity for consumables that interface with ventilators and CPAP equipment. Product strategy centers on fast setup, transparent visualization, CO2 washout efficiency, and compatibility with monitoring ports to align with stabilization workflows in maternity and pediatric units. Firms with broader neonatal portfolios use bundling to consolidate procurement, while maintaining interface-level innovation to differentiate on safety and usability within defined hood use cases. These factors sustain competition on both cost and design in the infant oxygen hoods market.

Strategic partnerships are advancing multifunctional neonatal solutions that may indirectly shape oxygen hood utilization by streamlining monitoring and reducing hardware clutter near the bedside. A collaboration announced in January 2026 aims to co-develop a multifunctional feeding tube with temperature, ECG, heart rate, and internal respiratory pressure sensing, a direction that aligns with efforts to integrate monitoring capabilities and reduce the need for separate devices. Digital engagement platforms in neonatal care have attracted growth capital to accelerate product innovation and expand hospital coverage, indicating ongoing investment momentum across adjacent categories that can intersect with respiratory workflows. In parallel, companies continue to expand their regulatory scope with MDSAP certifications and MDR approvals, strengthening their credentials to supply disposable and reusable respiratory accessories at scale across regions. These moves support stable near-term access to compliant consumables, including oxygen hoods, within national tenders that emphasize vendor reliability and evidence-backed designs.

White-space opportunities concentrate in transport, field, and resource-limited contexts where non-electrical, straightforward oxygen delivery is valuable, and where CPAP or HFNC infrastructure is not always feasible. Technology that provides objective airway pressure feedback is progressing through clinical feasibility work, which could later inform pressure-sensing pathways that improve titration confidence for noninvasive modalities and adjacent accessories. Regulatory alignment to QMSR raises the bar for design validation and post-market surveillance, favoring incumbents that can document consistent performance and field support. Framework agreements in mature health systems, including those geared to neonatal ventilation platforms and associated consumables, reinforce the relevance of portfolio suppliers that can balance unit price, compliance, and service in multi-year contracts. Within this competitive context, the infant oxygen hoods market advances on infection-control value, workflow compatibility, and assured supply.

Infant Oxygen Hoods Industry Leaders

-

Utah Medical Products

-

GaleMed Corporation

-

GINEVRI srl

-

Fanem Ltda

-

Ningbo David Medical Device

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Inspiration Healthcare Group plc secured a four-year NHS framework agreement covering England and Wales as the number one neonatal ventilator supplier for 2025 or 2026, supporting revenue visibility for respiratory platforms and related consumables.

- March 2026: GaleMed achieved ISCC PLUS certification for its BioVent-Circuit series using sugarcane-derived bio-based materials, aligning infection-control consumables with lower carbon-footprint resins.

- January 2026: Imagine Devices and Neotech Products announced a partnership to co-develop a multifunctional neonatal feeding tube with integrated vital sign monitoring and internal respiratory pressure sensing.

- December 2025: AngelEye Health closed USD 9 million in Series C funding, plus a debt facility, to accelerate innovation for neonatal and pediatric services and expand its commercial footprint.

Global Infant Oxygen Hoods Market Report Scope

| Disposable oxygen hoods |

| Reusable oxygen hoods |

| Level III/IV NICUs (tertiary) |

| Level II SCBUs/step-down units |

| Maternity/birthing centers and pediatric wards/ER |

| Home care/transport use |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South and Central America |

| By Product Type | Disposable oxygen hoods | |

| Reusable oxygen hoods | ||

| By End User | Level III/IV NICUs (tertiary) | |

| Level II SCBUs/step-down units | ||

| Maternity/birthing centers and pediatric wards/ER | ||

| Home care/transport use | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South and Central America | ||

Key Questions Answered in the Report

What is the infant oxygen hoods market size in 2026 and where is it headed by 2031?

The infant oxygen hoods market size was USD 8.43 million in 2026 and is projected to reach USD 11.55 million by 2031 at a 5.53% CAGR.

Which region leads and which grows fastest through 2031?

North America led with 46.11% in 2025, while Asia Pacific is the fastest-growing region at a 6.24% CAGR through 2031.

Which product type is expanding fastest and why?

Disposables show the fastest growth at a 6.57% CAGR due to infection-control mandates and simpler workflows for rapid turnover.

Which end-user segments are most important now and over the forecast period?

Level III or IV NICUs held 45.24% in 2025, while maternity or birthing centers and pediatric wards or ERs are set to grow at 6.30% CAGR.

What clinical factors most limit oxygen hood use?

Widespread reliance on HFNC and CPAP for positive-pressure support narrows hood use to short stabilization and cases of nasal-interface intolerance.

What features do leading vendors emphasize in new oxygen hood designs?

Designs focus on uniform oxygen distribution, improved CO2 washout, transparent access for procedures, and ports that simplify monitoring and escalation.

Page last updated on: