Industrial Exhaust System Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 3.85 Billion |

| Market Size (2030) | USD 4.76 Billion |

| Growth Rate (2025 - 2030) | 4.33% CAGR |

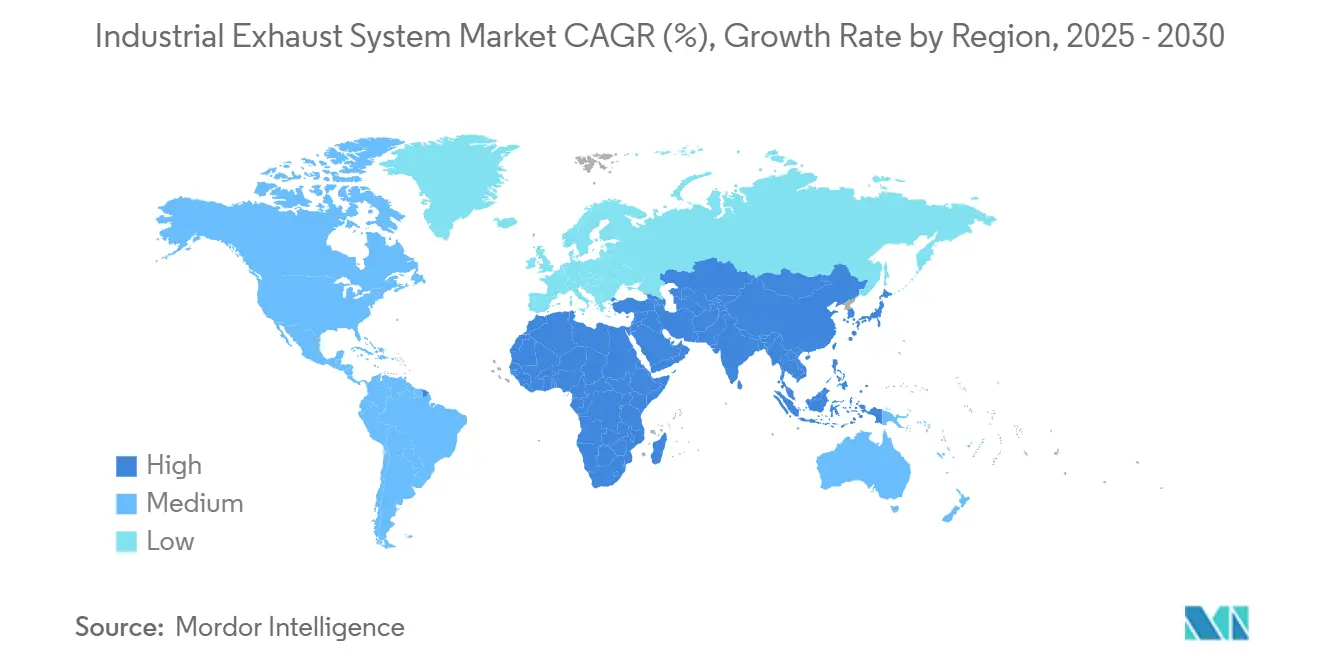

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

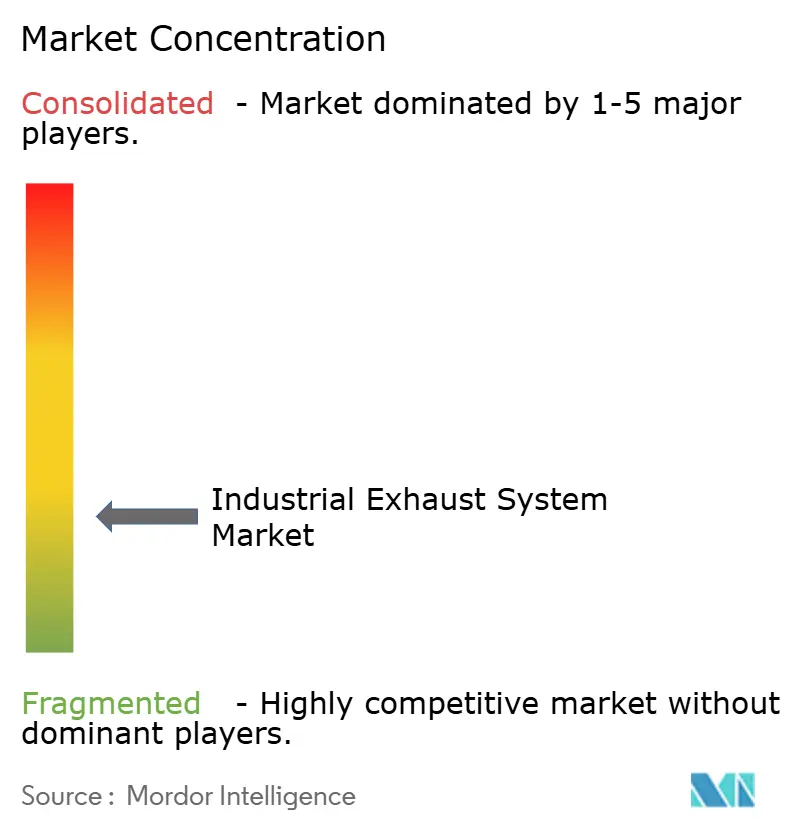

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Exhaust System Market Analysis by Mordor Intelligence

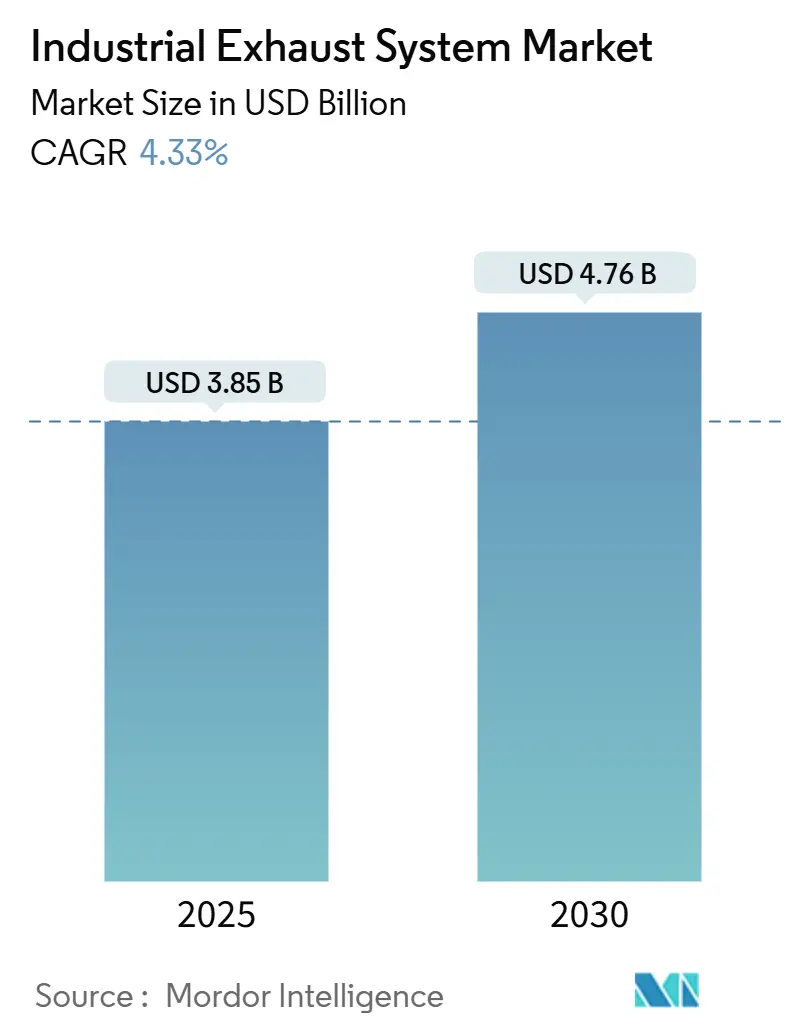

The Industrial Exhaust System Market size is estimated at USD 3.85 billion in 2025, and is expected to reach USD 4.76 billion by 2030, at a CAGR of 4.33% during the forecast period (2025-2030).

The industrial exhaust systems market is realigning as stationary power generation shifts from diesel to natural gas, pushing selective catalytic reduction (SCR) demand into double-digit territory while muffler orders level off. Tightening United States Environmental Protection Agency (EPA) Tier 4 Final rules, European Union Stage V directives, and China’s National VI norms are compelling operators to weigh costly retrofits against outright generator replacement.[1]U.S. Environmental Protection Agency, “Standards of Performance for Stationary Compression Ignition and Spark Ignition Internal Combustion Engines,” epa.gov Asia-Pacific dominates current global revenue, driven by manufacturing growth in India, Vietnam, and Indonesia that favors on-site combined heat and power (CHP) over grid reliance. Precious-metal pricing volatility and material innovations in composites are reshaping supplier margins, and Tier 1 engine manufacturers are vertically integrating aftertreatment to secure emissions warranties.

Key Report Takeaways

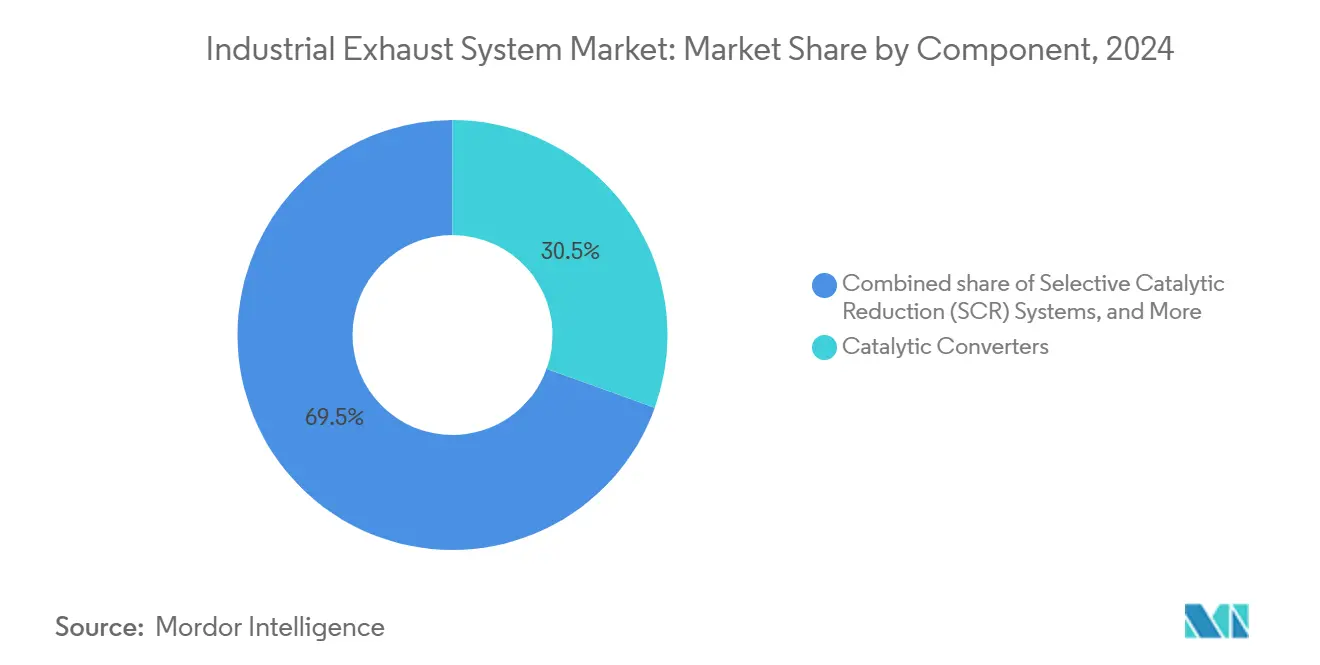

- By component, catalytic converters held 30.5% of 2024 revenue, while SCR modules are projected to expand at an 8.6% CAGR through 2030.

- By material, stainless steel commanded 41.8% of the industrial exhaust systems market share in 2024; composite and ceramic demand is advancing at a 9.1% CAGR.

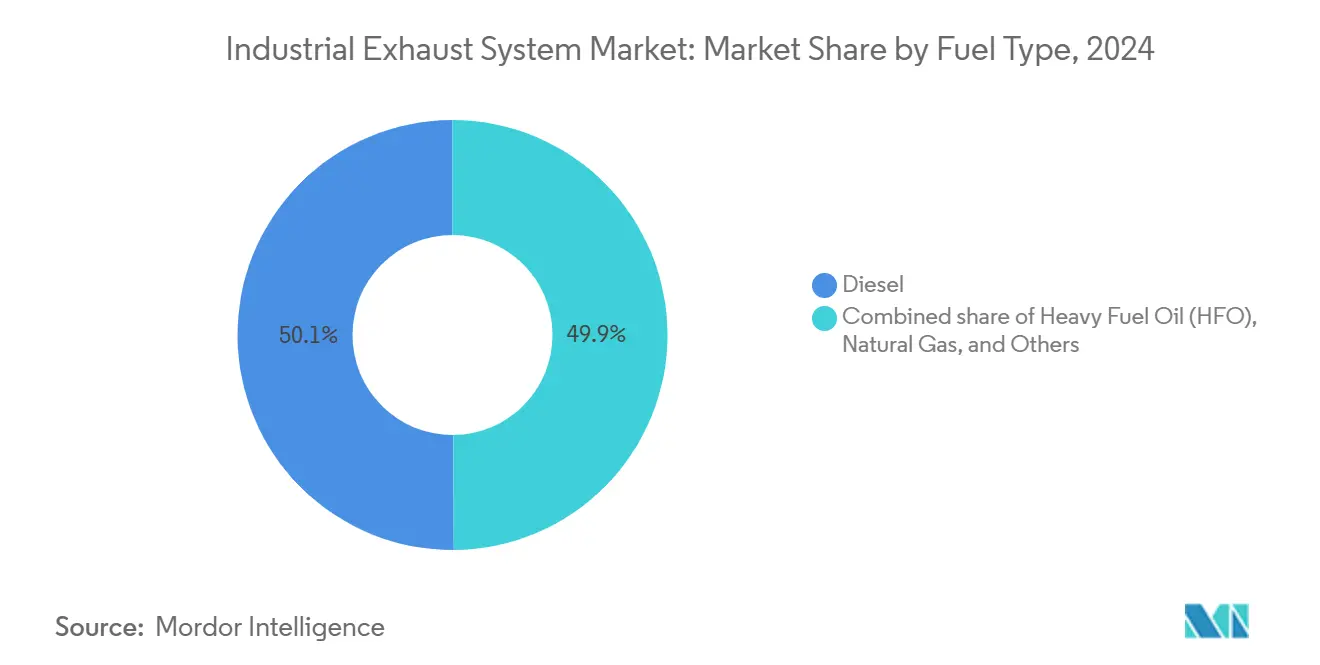

- By fuel type, diesel represented 50.1% of installations in 2024, yet natural-gas units are expanding at a 7.0% CAGR and rapidly closing the gap.

- By application, commercial facilities accounted for 36.7% of 2024 revenue and are growing at a 7.3% CAGR as resilience mandates broaden.

- By geography, Asia-Pacific commanded 41.4% of the industrial exhaust system market share in 2024, and the same is expected to log the highest 6.7% CAGR through 2030.

Global Industrial Exhaust System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening global NOx/PM regulations for stationary engines | 1.2% | Global, with early enforcement in North America, EU, and China | Medium term (2-4 years) |

| Rapid growth of on-site CHP installations in commercial facilities | 0.9% | North America and EU core, expanding to APAC urban centers | Medium term (2-4 years) |

| Industrial expansion and generator replacement cycles in APAC | 1.5% | APAC core (China, India, ASEAN), spill-over to Middle East | Long term (≥ 4 years) |

| Shift from diesel to natural-gas generators boosting SCR uptake | 1.1% | Global, led by North America and Europe | Medium term (2-4 years) |

| Edge-data-center demand for ultra-low-noise exhaust solutions | 0.6% | North America, Western Europe, select APAC metros | Short term (≤ 2 years) |

| Growing deployment of IoT-enabled exhaust sensors | 0.4% | Global, with faster adoption in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Global NOx/PM Regulations for Stationary Engines

Convergence between stationary-engine and on-road emission ceilings has erased the compliance gap that once favored standby gensets. EPA Tier 4 Final caps NOx at 0.67 g/kWh for engines above 560 kW, while EU Stage V adds particle-number limits alongside mass-based thresholds. China’s National VI rules, enforced since December 2022, extend in-use testing to backup generators in industrial parks, capturing units that formerly skirted oversight. India’s Central Pollution Control Board draft norms released in 2024 would mandate continuous-emissions monitoring on gensets above 500 kW in non-attainment cities, accelerating SCR deployment in Delhi and Maharashtra. Maritime sulfur caps introduced by the International Maritime Organization have indirectly tightened land-based heavy-fuel-oil use, as port authorities now scrutinize shore-power exhaust to avoid berth violations.

Rapid Growth of On-Site CHP Installations in Commercial Facilities

Unbundled utility tariffs, reliability concerns, and net-zero targets are steering hospitals, universities, and mixed-use campuses toward natural-gas CHP. The United States added 267 MW of new CHP in 2024, 38% of which served healthcare and institutional users.[2]Department of Energy, “Combined Heat and Power Installation Database 2025,” energy.gov EU members added 1.2 GW of commercial CHP the same year, helped by feed-in premiums under the Energy Efficiency Directive.[3]European Commission, “Energy Efficiency Directive Implementation Report 2024,” europa.eu Typical configurations employ 500 kW–2 MW gas engines that harvest exhaust heat while meeting local NOx ceilings below 9 ppm through SCR or lean-burn tuning. Edge data centers exemplify premium demand: a 5 MW Italian site specified 24 acoustic enclosures integrating SCR to satisfy Milan’s 85 dB daytime ordinance. These requirements raise content value per kilowatt, strengthening the industrial exhaust systems market.

Industrial Expansion and Generator Replacement Cycles in APAC

Factory growth in Southeast Asia and the Indian subcontinent is outpacing grid upgrades, compelling manufacturers to install captive power that must still honor emerging air-quality rules. India’s captive-industrial generation reached 89 GW in 2024, with diesel and gas gensets forming 62% of the total. Vietnam’s Power Development Plan VIII anticipates dual-fuel engines that switch between liquefied natural gas and diesel, each mode requiring distinct aftertreatment. China’s 14th Five-Year Plan mandates ultra-low-emission retrofits for existing diesel units in priority regions, nudging owners toward factory-integrated Tier 4-equivalent gas sets. Indonesia retains emission caps aligned with regional ASEAN standards, creating a window for turnkey exhaust solutions bundled with multiyear service contracts.

Shift from Diesel to Natural-Gas Generators Boosting SCR Uptake

Natural gas traded 40–50% cheaper than diesel on an energy-equivalent basis in 2024, underscoring economic drivers behind the fuel switch. Spark-ignition platforms comply with NOx rules via SCR yet avoid diesel particulate filter (DPF) regeneration, reducing downtime in mission-critical settings. Cummins launched its X15N natural-gas engine in late 2023, pairing 500 hp output with an integrated SCR that achieves EPA optional low-NOx limits of 0.02 g/bhp-hr. Caterpillar’s lean-burn G3500 family similarly dominates CHP installations, utilizing ammonia-slip catalysts to maintain sub-0.5 g/bhp-hr NOx without urea in remote zones. European cities now plan to phase out diesel backup sets by 2030, compelling hospitals and telecom operators to retrofit enclosures around larger SCR modules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex for multi-stage aftertreatment retrofits | -0.8% | Global, acute in North America and EU retrofit markets | Short term (≤ 2 years) |

| Volatile precious-metal catalyst prices | -0.6% | Global, affecting all catalyst-intensive segments | Medium term (2-4 years) |

| Lengthy local certification for custom silencers in EMEA | -0.3% | Europe, Middle East, select African markets | Medium term (2-4 years) |

| Low awareness of digital O&M savings among SME plant owners | -0.2% | Global, most pronounced in APAC and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex for Multi-Stage Aftertreatment Retrofits

Bringing pre-Tier 4 diesel generators up to current codes often demands a full stack of SCR, diesel oxidation catalyst, and DPF hardware that costs 40-60% of a new power unit. A 1 MW standby genset retrofit in the United States typically runs USD 150,000-200,000 when accounting for urea tanks, control integration, and structural reinforcement, based on CECO Environmental project data.[4]CECO Environmental, “Stationary Engine Retrofit Cost Index 2024,” cecoenviro.com European operators also absorb CE-marking expenses and fragmented municipal permitting that can stretch timelines by up to 12 months, particularly in Germany and France. Arctic and high-altitude oil sites face added costs for heated urea storage that siphons 2–3% of net generation capacity.

Volatile Precious-Metal Catalyst Prices

Platinum, palladium, and rhodium remain indispensable for three-way and oxidation catalysts, yet their pricing swung 30–50% during 2024, compressing converter margins. Palladium averaged USD 1,020/oz while rhodium peaked near USD 4,800/oz amid constrained South African mine output. The World Platinum Investment Council logged a 450,000-oz supply deficit the same year, spotlighting recycling shortfalls. Suppliers are investing in copper-zeolite SCR and perovskite oxidation catalysts to cut noble-metal exposure, yet thermal durability beyond 5,000 hours remains unproven.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: SCR Modules Outpace Legacy Mufflers

Selective Catalytic Reduction (SCR) systems are expanding at an 8.6% CAGR, nearly twice the industrial exhaust systems market pace, because natural-gas generators rely on ammonia-fed catalysis rather than passive mufflers for NOx compliance. Catalytic converters captured 30.5% of 2024 revenue, yet growth is moderating as price competition intensifies and automotive-style formulations mature. Mufflers and silencers remain essential for legacy installations but face stagnation in markets with established noise ordinances, whereas Asia-Pacific industrial parks lacking strict acoustic codes sustain baseline demand. DPFs stay diesel-centric, and their adoption has plateaued as fleet owners pivot to gas to avoid soot regeneration downtime. Exhaust gas recirculation equipment occupies a niche for large reciprocating engines operating in water-constrained oil fields. Sensors, temperature, backpressure, oxygen, and ammonia-slip form the fastest-growing subsegment because predictive maintenance is gaining traction. Combination modules that package SCR, oxidation catalyst, and electronic dosing in a single housing suit tight retrofit envelopes, exemplified by Cummins’ 400-lb assembly for the X15N platform.

By Material: Composites Challenge Stainless Steel Dominance

Stainless steel held 41.8% of 2024 demand, yet its 650 °C service ceiling limits applicability in high-temperature combined-cycle plants and hydrogen trials. Silicon-carbide ceramic matrix composites maintain integrity at 1,200 °C and cut thermal expansion by 40% versus nickel superalloys, permitting more compact exhaust heat exchangers. Composite and ceramic demand is therefore advancing at a 9.1% CAGR, reshaping procurement specifications in new-build gas-turbine projects. Mild steel persists in cost-sensitive portable sets where operating hours stay below 5,000. Titanium grades resist seawater-induced chloride cracking, supporting longer inspection intervals on offshore platforms despite a 300% cost premium. Nickel alloys, Inconel 625 and Hastelloy C-276, dominate chemical-plant exhaust exposed to acid condensates, although volatile nickel pricing is encouraging trials of duplex stainless alternatives.

By Fuel Type: Natural Gas Narrows Diesel’s Lead

Diesel retained 50.1% of 2024 installations, but natural-gas capacity is growing 7.0% annually as operators leverage fuel-cost arbitrage and avoid DPF maintenance. EPA optional low-NOx certification at 0.02 g/bhp-hr is achievable on gas engines with single-stage SCR, giving them a compliance edge. Heavy-fuel-oil gensets plunged below 8% share after the International Maritime Organization’s sulfur cap, driving marine and island grids toward marine gas oil or scrubber retrofits. Biogas, hydrogen blends, and dual-fuel engines remain nascent but benefit from Horizon Europe’s EUR 120 million research allocation for hydrogen combustion exhaust materials. Dual-fuel units that toggle between liquefied natural gas and diesel increase aftertreatment complexity, lifting system cost by up to 30%.

By Application: Commercial Facilities Outpace Industrial Base

Commercial facilities, hospitals, data centers, and mixed-use developments collectively grew to 36.7% of 2024 revenue and will expand at a 7.3% CAGR as backup-power codes harden. Joint Commission accreditation in U.S. healthcare mandates 96-hour power autonomy, incentivizing CHP that recovers waste heat and lowers energy bills. Edge data centers elevate acoustic standards, specifying 85 dB at 1 m daytime and 75 dB at night, which raises exhaust content by 15–20%. Industrial facilities still anchor the installed base but face slower growth where renewable penetration reduces diesel baseload economics. Power-generation peakers are migrating to large-frame gas turbines with SCR, concentrating demand among catalyst majors. Oil and gas upstream sites continue modular SCR retrofits to comply without sacrificing engine lifetimes.

Geography Analysis

Asia-Pacific generated 41.4% of global revenue in 2024 and is projected to grow at 6.7% through 2030, lifted by factory build-outs that outstrip grid capacity. India’s 89 GW captive-industrial fleet depends heavily on diesel and gas, and draft emissions-monitoring rules for >500 kW gensets in non-attainment zones will hasten SCR adoption. China’s ultra-low-emission retrofit mandate in key industrial clusters is steering owners toward Tier 4-level natural-gas generators integrated with SCR. Vietnam’s power roadmap confirms a 15-year reliance on dual-fuel units, raising demand for flexible aftertreatment designs. Japan and South Korea focus on predictive-maintenance upgrades, benefiting sensor suppliers. Southeast Asian nations retain diesel dominance but are starting to specify acoustic and emissions packages for export-oriented industrial parks.

North America and Europe jointly captured 38% of 2024 sales, driven by retrofit-heavy spending. U.S. enforcement of the 0.67 g/kWh NOx limit for >560 kW stationary engines sparked a wave of SCR installations in hospitals and data centers, with project budgets averaging USD 150,000–200,000 per. Europe’s Ambient Air Quality Directive supports municipal diesel-phase-out plans by 2030, propelling natural-gas conversions that often require custom exhaust routing inside legacy enclosures. Germany’s TA Lärm and the United Kingdom’s Building Regulations Document F stretch silencer certification timelines by up to six months, rewarding suppliers that maintain in-house acoustic labs.

South America, the Middle East, and Africa together accounted for 20.6% of 2024 demand. Brazil’s grid volatility sustains diesel use, although draft NOx limits for stationary engines are under review. Middle-Eastern oil and gas projects specify titanium and nickel exhaust stacks to extend offshore inspection cycles, offsetting higher material costs. South African mines require ruggedized systems capable of high-dust, high-altitude service, with electrification expected only in the long term.

Competitive Landscape

The industrial exhaust systems market is moderately fragmented. Cummins, Caterpillar, and Perkins are vertically integrating aftertreatment to solidify emissions warranties and capture margin. Cummins’ X15N gas engine embeds SCR, oxidation catalyst, and dosing controls in a 400-lb module that meets 0.02 g/bhp-hr NOx, binding customers to factory service contracts. Caterpillar bundles closed-loop urea dosing with proprietary algorithms, creating competitive barriers for independent suppliers. Johnson Matthey and BASF dominate precious-metal catalysts yet face thinner spreads amid palladium and rhodium volatility, prompting investment in copper-zeolite alternatives. ADE Power commands edge-data-center acoustics, delivering 85 dB enclosures that integrate heat recovery; its 2024 Italian deployment highlights premium pricing power. NETL research into 1,200 °C ceramic matrix composites is opening high-temperature niches unreachable by stainless steel. Smaller firms such as Schock Manufacturing and Eldridge Sales are embedding IoT sensors to shift revenue toward predictive diagnostics; Donaldson’s wireless pressure-sensor DPF kit exemplifies this service pivot.

Industrial Exhaust System Industry Leaders

Cummins Inc.

Caterpillar Inc. (Solar Turbines & Progress Rail)

Johnson Matthey PLC

Donaldson Company Inc.

Tenneco Inc. (Walker Exhaust)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Tenaris completed the installation of a USD 85 million fume exhaust system at its Koppel, Pennsylvania, steel mill. This advanced exhaust system is designed to efficiently collect, capture, and separate dust and particulates produced during steel production, and it also aims to curb carbon monoxide emissions.

- December 2024: SSE and Siemens Energy have unveiled “Mission H2 Power.” This collaboration is set to pioneer gas turbine technology that operates solely on hydrogen. Building upon their established partnership, the initiative seeks to further the decarbonisation efforts at SSE’s Keadby 2 Power Station in North Lincolnshire, which currently utilizes Siemens Energy’s SGT5-9000HL gas turbine.

- August 2024: Donaldson acquired Solaris Biotechnology’s filtration arm for USD 65 million, adding biogas exhaust-cleaning technology to its DPF lineup.

Global Industrial Exhaust System Market Report Scope

Engineered to purify industrial environments, an industrial exhaust system effectively eliminates contaminated air, fumes, smoke, and particles. Utilizing components such as hoods, fans, and ducts, the system captures pollutants at their source, transports them, and either filters or directly discharges them.

The global industrial exhaust systems market is segmented by component, material, fuel type, application, and geography. By component, the market is segmented into mufflers, catalytic converters, particulate filters, SCR systems, EGR systems, sensors, and others. By material, the market is segmented into stainless steel, mild steel, titanium, nickel alloys, composite, and ceramic materials. By fuel type, the market is segmented into heavy fuel oil, diesel, natural gas, and others. By application, the market is segmented into power generation (including CHP systems), oil and gas, industrial facilities, commercial facilities (hospitals, data centers, etc.), and others. The market forecasts are provided in terms of value (USD).

| Mufflers |

| Catalytic Converters |

| Particulate Filters |

| Selective Catalytic Reduction (SCR) Systems |

| Exhaust Gas Recirculation (EGR) Systems |

| Sensors |

| Others (Combination and Control Modules) |

| Stainless Steel |

| Mild Steel |

| Titanium |

| Nickel Alloys |

| Composite and Ceramic Materials |

| Heavy Fuel Oil (HFO) |

| Diesel |

| Natural Gas |

| Others |

| Power Generation (incl CHP systems) |

| Oil and Gas |

| Industrial Facilities |

| Commercial Facilities (Hospitals, Datacenters, etc.) |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Component | Mufflers | |

| Catalytic Converters | ||

| Particulate Filters | ||

| Selective Catalytic Reduction (SCR) Systems | ||

| Exhaust Gas Recirculation (EGR) Systems | ||

| Sensors | ||

| Others (Combination and Control Modules) | ||

| By Material | Stainless Steel | |

| Mild Steel | ||

| Titanium | ||

| Nickel Alloys | ||

| Composite and Ceramic Materials | ||

| By Fuel Type | Heavy Fuel Oil (HFO) | |

| Diesel | ||

| Natural Gas | ||

| Others | ||

| By Application | Power Generation (incl CHP systems) | |

| Oil and Gas | ||

| Industrial Facilities | ||

| Commercial Facilities (Hospitals, Datacenters, etc.) | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the industrial exhaust systems market in 2030?

The industrial exhaust systems market size is forecast to reach USD 4.76 billion by 2030, growing at a 4.33% CAGR.

Which component is expanding fastest?

SCR modules are advancing at an 8.6% CAGR, almost double the overall market pace due to stricter NOx rules on natural-gas generators.

Why are composites gaining share in exhaust systems?

Silicon-carbide and other composites tolerate temperatures above 1,000 °C and reduce thermal expansion, supporting hydrogen-blend and high-turbine-inlet projects.

How are regulations influencing generator fuel choice?

Tight NOx and particulate limits plus lower gas prices are moving buyers from diesel to natural-gas gensets that meet compliance with single-stage SCR.

Which region will see the strongest growth through 2030?

Asia-Pacific leads, with a 6.7% CAGR driven by industrial expansion in India, Vietnam, and Indonesia that necessitates captive power and compliant exhaust systems.

Page last updated on: