Indoor Location Solutions Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 14.88 Billion |

| Market Size (2030) | USD 43.32 Billion |

| Growth Rate (2025 - 2030) | 24.00% CAGR |

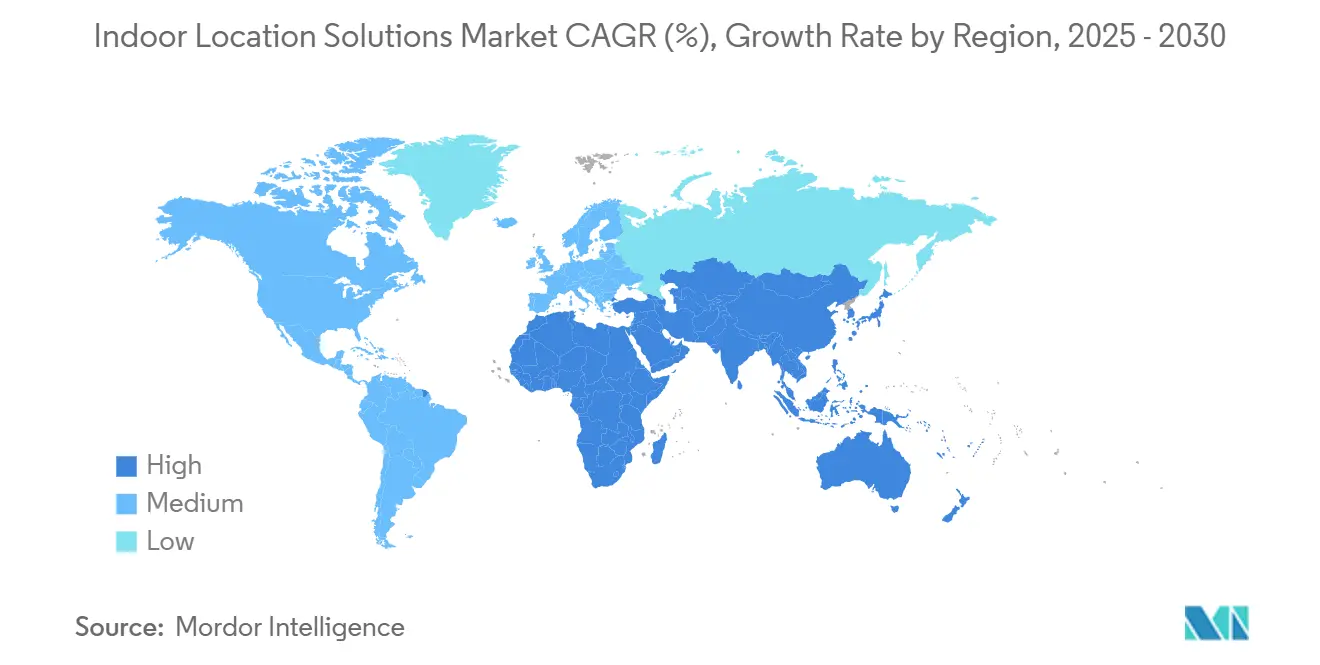

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

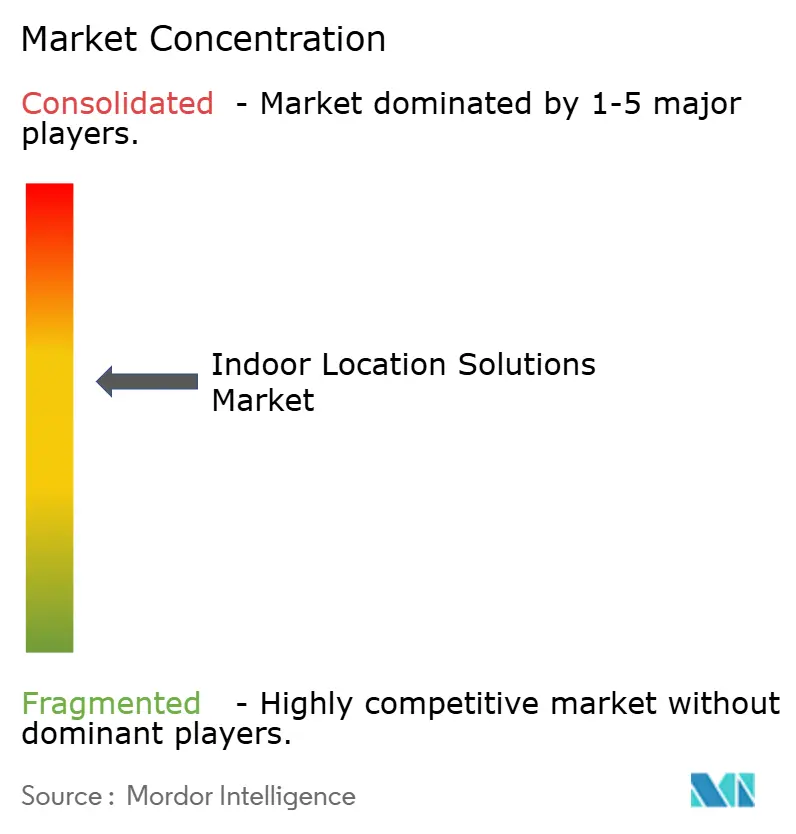

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indoor Location Solutions Market Analysis by Mordor Intelligence

The indoor location solutions market size reached a value of USD 14.88 billion in 2025 and is forecast to post a 24% CAGR, lifting revenue to USD 43.32 billion by 2030. Uptake is accelerating as enterprises pair next-generation wireless technologies with analytics-rich software to digitalize warehouses, hospitals, campuses, and transportation hubs. Widespread 5G-Advanced and Wi-Fi 7 rollouts, regulator-led real-time-location-system (RTLS) mandates in healthcare, and consumer familiarity with smartphone-centric positioning are converging to reshape indoor navigation, asset tracking, and proximity marketing. Bluetooth Low Energy (BLE) anchors today’s installed base, yet ultra-wideband (UWB) is converting consumer demand for centimetre-level accuracy into enterprise spending. Bundled software-hardware offerings now command a clear majority of new contracts, while managed and professional services grow in step with customer need for RF planning and ongoing optimisation. Although North America currently heads adoption, Asia-Pacific’s smart-factory programmes and Middle-East megaprojects are expanding total addressable opportunity across all segments of the indoor location solutions market.

Key Report Takeaways

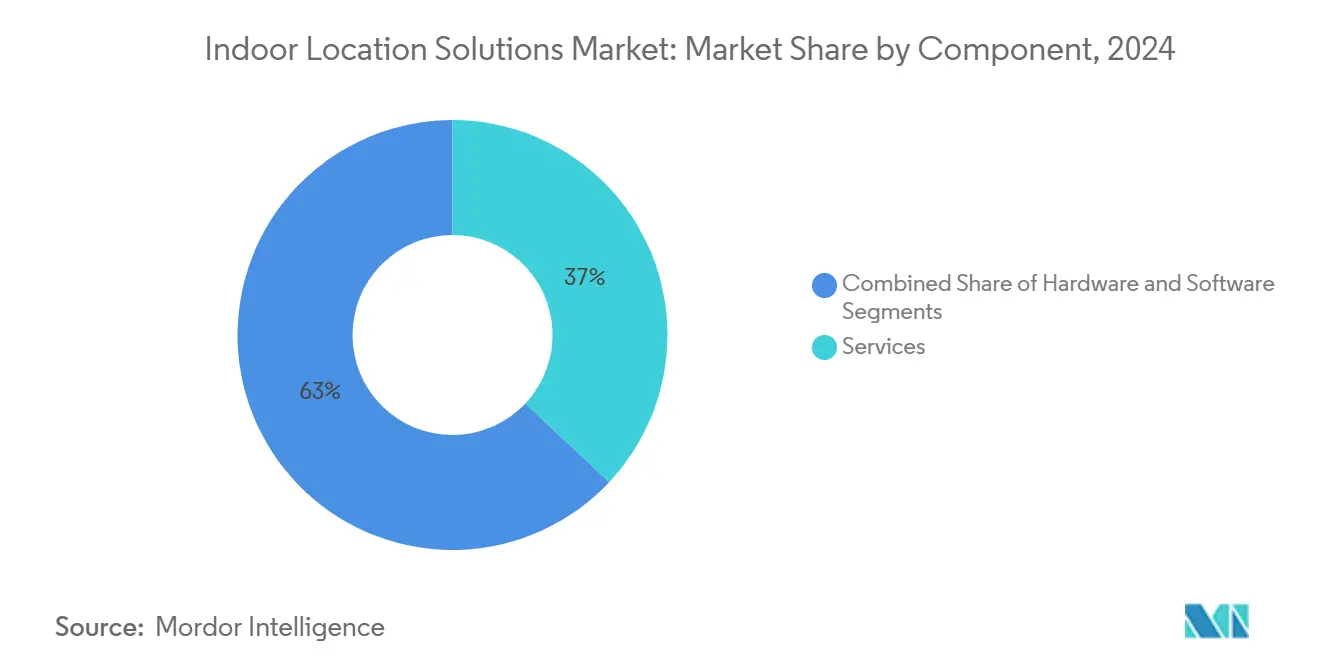

- By component, software captured 63% of the indoor location solutions market size in 2024; services are projected to advance at a 24.81% CAGR through 2030.

- By technology, Bluetooth low energy held 22% of the indoor location solutions market size in 2024, while Ultra-Wideband is projected to expand at a 25.87% CAGR to 2030.

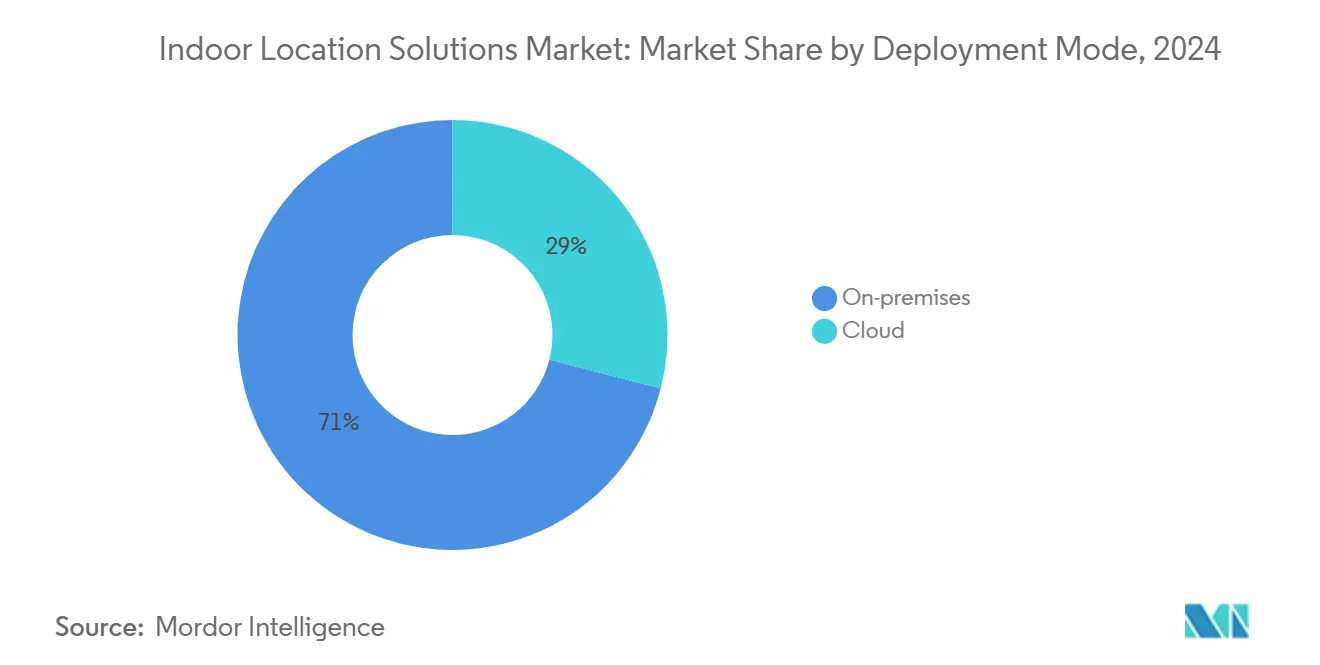

- By deployment mode, on-premises accounted for 71% of the indoor location solutions market size in 2024; cloud-based deployments are forecast to grow at a 24.69% annual rate to 2030.

- By application, navigation and maps represented 31% of the indoor location solutions market size in 2024, whereas asset tracking and management are projected to grow at a 25.79% CAGR for the forecast period.

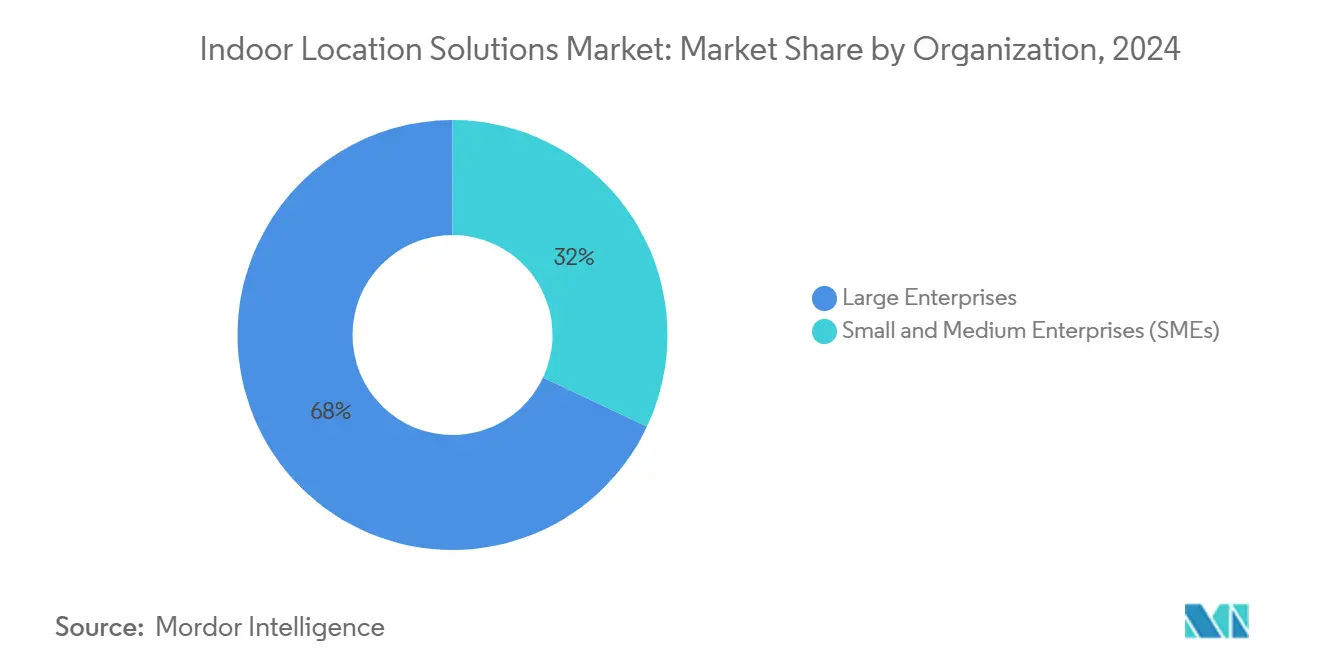

- By organization size, large enterprises commanded 42.7% of the indoor location solutions market size in 2024, while small and medium enterprises are expected to register the fastest growth at a 24.64% CAGR through 2030.

- By end-user industry, retail and e-commerce accounted for 28% of the indoor location solutions market size in 2024; healthcare is expected to register the fastest growth at a 26.17% CAGR through 2030.

- By geography, North America commanded 42.7% of the indoor location solutions market size in 2024, while the Asia-Pacific region is expected to register the fastest growth at a 26.89% CAGR through 2030.

Global Indoor Location Solutions Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surge in UWB-Enabled Consumer Devices (North America and Europe) | +4.2% | North America and Europe, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Mandates for RTLS Compliance in US Healthcare Facilities | +3.8% | North America, early adoption in Canada | Short term (≤ 2 years) |

| 5G-Advanced and Wi-Fi 7 Roll-outs Driving Asian Smart-Factory Adoption | +5.1% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Digital-Twin Wayfinding in Middle-East Mega Airports and Metros | +2.9% | Middle East, UAE and Saudi Arabia focus | Long term (≥ 4 years) |

| EU Green-Deal Retrofit Push for Occupancy-Aware Smart Buildings | +3.4% | Europe, Germany and France leading | Medium term (2-4 years) |

| Micro-Fulfillment "Last-50 m" Geofencing for e-Commerce Dark Stores | +2.7% | Global, concentrated in urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in UWB-enabled consumer devices

Samsung’s release of centimetre-precision UWB chipsets for smartphones and cars, coupled with Apple’s U1 ecosystem and the FiRa Consortium’s certification programme, has normalised device-to-device ranging. Mass-market visibility is pushing enterprises to pilot UWB badges, tags, and access-control solutions that outperform Wi-Fi RTT in dense interiors. As chipset costs fall, integrators are using the same radios to serve asset-tracking, wayfinding, and secure-entry scenarios, reducing bill-of-material complexity across the indoor location solutions market.[1]Samsung Semiconductor, “Samsung Announces Ultra-Wideband Chipset with Centimeter-Level Accuracy for Mobile and Automotive Devices,” semiconductor.samsung.com

Mandates for RTLS compliance in US healthcare facilities

The US Department of Veterans Affairs now requires continuous visibility of equipment, pharmaceuticals, and personnel, driving large-scale RTLS installations. Vendors such as CenTrak respond with HIPAA-compliant, sub-metre BLE systems that integrate seamlessly with existing clinical workflows. Joint Commission accreditation audits increasingly verify location-aware safety procedures, making RTLS a non--optional budget line for hospital operators. Demand resilience is therefore less exposed to discretionary IT cycles than other verticals in the indoor location solutions market industry.

5G-Advanced and Wi-Fi 7 rollouts driving Asian smart-factory adoption

China Mobile’s partnership with Huawei demonstrates that industrial 5G positioning has moved from pilot to production, achieving double-digit productivity gains in automotive and electronics plants. Broadcom’s second-generation Wi-Fi 7 chipsets combine 320 MHz channels with multi-link operation, allowing simultaneous data and centimetre-scale ranging. Vendors offering hybrid BLE/UWB/Wi-Fi stacks are winning contracts as manufacturers demand accuracy and bandwidth within a single infrastructure spend.

Digital-twin wayfinding in Middle East mega-airports and metros

Dubai’s Al Maktoum International Airport and Riyadh Metro are embedding indoor mapping and digital-twin functionality during construction, ensuring that passenger-facing apps launch on day one. Centimetre-level positioning feeds operational analytics for resource scheduling and crowd management, while premium retail tenants gain proximity-marketing capabilities. The projects’ scale is setting reference architectures that neighbouring airports, malls, and exhibition centres are beginning to replicate, expanding regional relevance of the indoor location solutions market.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Multipath Interference in Dense-Metal Manufacturing Environments | -2.8% | Global, concentrated in industrial regions | Medium term (2-4 years) |

| Fragmented BLE / UWB / Wi-Fi RTT Standards Elevating Integration Cost | -3.2% | Global, particularly affecting SME adoption | Long term (≥ 4 years) |

| GDPR-Led Privacy Litigations Against In-Store Tracking in EU | -1.9% | Europe, with regulatory spillover effects | Short term (≤ 2 years) |

| Capex Freeze at Tier-2 Airports Post-COVID Delaying Indoor Mapping | -1.4% | Global, concentrated in secondary markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Multipath interference in dense-metal manufacturing environments

IEEE research confirms that Wi-Fi RTT and BLE accuracy degrades in reflective surroundings, while UWB maintains 10 cm precision but at 2-3 times the infrastructure cost. Manufacturers therefore face a trade-off between capital expenditure and accuracy, often deploying hybrid sensors that layer inertial data or machine-learning multipath mitigation. Solution complexity favours vendors with deep RF engineering capabilities, limiting choices for cost-sensitive buyers and mildly dampening the indoor location solutions market growth.[2]arXiv, “Ultra-Wideband Positioning System Based on ESP32 and DWM3000 Modules,” arxiv.org

Fragmented BLE / UWB / Wi-Fi RTT standards elevating integration cost

Bluetooth 5.4 direction-finding, IEEE 802.11az, and FiRa UWB profiles each promise high precision, yet coexistence remains immature, forcing enterprises to support multiple radio stacks. Keysight’s field-testing shows that multi-technology back-end integration can raise total cost of ownership by up to 40% versus single-stack deployments. Small and medium enterprises, lacking large in-house IT teams, postpone projects until unifying chipsets and reference designs emerge, slowing diffusion across lower-tier customer segments of the indoor location solutions market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Integrated platforms dominate yet services accelerate

Software held 63% revenue in 2024. This segment’s scale stems from buyers’ preference for turnkey deployment that removes multi-vendor coordination. Services represent the fastest-rising share of the indoor location solutions market, growing at 24.81% annually as customers outsource RF design, installation, and lifecycle optimisation.

Managed-service contracts convert upfront capex into predictable opex, aligning with Industry 4.0 outcome-based models. Vendors now attach service-level agreements for accuracy and uptime, deepening recurring revenue streams and making services an essential driver of the indoor location solutions industry.[3]Kontakt.io, “Indoor Navigation with Bluetooth Beacons Whitepaper,” kontakt.io

By Technology: BLE rules incumbency while UWB captures momentum

BLE accounted for 22% of the indoor location solutions market size in 2024, reflecting ubiquity in smartphones and low-cost beacons. UWB, however, is scaling at 25.87% CAGR to 2030 as handset makers include native radios and as the FiRa Consortium certifies interoperable modules.

UWB’s resilience to multipath and near-instant ranging has led carmakers to adopt digital keys and factories to specify high-accuracy asset tracking. Meanwhile, Wi-Fi 7’s channel-sounding narrows the performance gap but still depends on dense access-point grids. Hybrid BLE/UWB tags balance cost and accuracy, signalling a multi-radio future for the indoor location solutions market.

By Deployment Mode: On-premises retains control while cloud accelerates analytics

Data-sovereignty and latency dictated that 71% of installations remained on-site in 2024. Hospitals, financial institutions, and defence facilities continue to mandate local data processing for compliance and security reasons. Yet cloud-native platforms are growing 24.69% annually because they avoid upfront server costs and unleash machine-learning analytics.

Vendors are shipping edge gateways that anonymise coordinates before off-premises export, allowing customers to satisfy GDPR while still benefitting from cloud-driven insight. Hybrid architecture is thus emerging as the de-facto blueprint across the indoor location solutions market.

By Application: Navigation leads, asset tracking surges

Mapping and wayfinding held 31% of the indoor location solutions market size in 2024 as airports, malls, and hospitals prioritised visitor experience. Asset-tracking solutions are advancing at a matching 25.79% CAGR because industrial, healthcare, and logistics operators quantify rapid ROI by cutting search times and preventing loss.

Integration platforms now converge navigation, tracking, and proximity-marketing functions into a single data layer, unlocking cross-departmental value and fuelling software subscription growth within the wider indoor location solutions market.

By Organisation Size: Enterprises dominate revenue, SMEs unlock next-wave growth

In 2024, large enterprises held a dominant 42.7% share of the indoor location solutions market. Meanwhile, small and medium enterprises are poised for rapid expansion, projected to grow at an impressive 24.64% CAGR through 2030. Global brands with multi-site campuses, distribution centres, and retail footprints continue to account for the bulk of spend, leveraging dedicated IT and facilities teams for complex deployments. However, SaaS pricing, battery-free tags, and low-code integration tools are lowering barriers for SMEs, opening a sizeable greenfield across the indoor location solutions industry.

Solution vendors are therefore packaging starter kits that combine plug-and-play beacons with cloud dashboards, shortening proofs-of-concept from months to days and translating best practice developed for large enterprises into SME budgets.

By End-User Industry: Retail commands share, healthcare accelerates

Retail and e-commerce secured 28% revenue in 2024 by blending in-store navigation, pick-to-light, and click-and-collect optimisation. Healthcare is climbing fastest, clocking a 26.17% CAGR as RTLS becomes a compliance necessity for asset and patient safety.

Beyond these anchors, manufacturing, logistics, and smart buildings deploy indoor positioning to drive efficiencies from automated guided vehicles to occupancy-based HVAC, broadening vertical diversification and stabilising the indoor location solutions market against sector-specific slowdowns.

Geography Analysis

In 2024, North America held a dominant 42.7% share of the indoor location solutions market, while the Asia-Pacific region is poised for rapid expansion, projected to grow at a robust 26.89% CAGR through 2030. Federal mandates, such as the Department of Veterans Affairs RTLS rollout, are translating policy into predictable project pipelines. Canada complements with smart-building retrofits, while Mexico begins shifting from pilot to production in automotive plants.

The Asia-Pacific region is expanding the fastest as public-private initiatives deploy 5G and Wi-Fi 7 infrastructure across industrial parks and transportation corridors. China leads in smart-factory retrofits, South Korea pioneers elder-care tracking, and India’s digital-industrial corridors fuel greenfield installations that sidestep legacy constraints.

Europe leverages stringent data privacy and energy efficiency regulations to drive demand for occupancy-aware solutions. Germany and France retrofit commercial real estate to align with the EU Green Deal, while the United Kingdom emphasises patient-centric RTLS post-Brexit. The Middle East and Africa, though smaller in absolute value, are seeing outsized growth as airports and metros embed digital twins at the build stage, ensuring the region becomes a high-visibility use-case showcase for the indoor location solutions market.

Competitive Landscape

The indoor location solutions market remains moderately fragmented. Major players like Cisco, HPE Aruba, and Zebra Technologies, known for their networking prowess, bundle Wi-Fi and BLE into cohesive portfolios, leveraging established ties with enterprises. Meanwhile, specialists such as HID Global, CenTrak, and Sonitor secure contracts by customizing solutions to enhance accuracy and workflow integration for sectors like healthcare, manufacturing, and mining.

Technology platforms from Apple, Google, and Microsoft embed location APIs within mobile and cloud ecosystems, creating high switching costs for developers. Acquisition activity is rising: CoStar’s USD 1.6 billion purchase of Matterport and Viavi’s USD 150 million buy-in of inertial-sensor specialist Inertial Labs illustrate cross-industry demand for spatial-data capabilities.

Competitive advantage is shifting toward vendors that can supply end-to-end accuracy guarantees, integrate multi-radio stacks, and deliver outcome-based service agreements. Ecosystem openness, rather than proprietary lock-in, is increasingly a selection criterion as buyers aim to future-proof investments amidst rapid standards evolution.

Indoor Location Solutions Industry Leaders

Cisco Systems Inc.

Hewlett Packard Enterprise Development LP (Aruba Networks)

Zebra Technologies Corporation

Google LLC

Apple Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Broadcom announced availability of second-generation Wi-Fi 7 wireless connectivity chips, including BCM47722 and BCM4390 models supporting Bluetooth 5.4 and Channel Sounding specifications for enhanced location services, targeting smartphone, access point, and IoT applications with improved accuracy and reduced latency capabilities.

- December 2024: CoStar Group completed its $1.6 billion acquisition of Matterport, integrating 3D spatial data and digital twin capabilities with commercial real estate services to create comprehensive indoor mapping and location intelligence platforms for property management and tenant experience applications.

- November 2024: Kontakt.io received two 2024 Merit Awards for HealthTech innovation, recognizing the company's contributions to indoor location solutions and RTLS solutions specifically designed for healthcare environments, highlighting the growing importance of compliance-driven market segments.

- October 2024: STMicroelectronics and Qualcomm announced strategic collaboration in wireless IoT, integrating Qualcomm's AI-powered connectivity technologies with ST's STM32 microcontroller ecosystem to accelerate development of next-generation industrial and consumer IoT applications with enhanced positioning capabilities.

Global Indoor Location Solutions Market Report Scope

The Indoor Location Solutions Market Report Segments the Industry into Component (Hardware, Software, Services), Technology (Bluetooth Low Energy (BLE), Ultra-Wideband (UWB), RFID, Wi-Fi / Wi-Fi RTT, Magnetic Positioning, Other Technology), Deployment Mode (On-premises, and Cloud), Application (Navigation and Maps, Asset Tracking and Management, Proximity Marketing and Customer Engagement, Emergency Management and Remote Monitoring, Industrial Automation and Control, Other Application), Organization Size (Large Enterprises, and Small and Medium Enterprises (SMEs)), End-User Industry (Retail and E-commerce, Healthcare and Life Sciences, Transportation and Logistics, Manufacturing and Warehousing, Smart Buildings and Real Estate, Government, Defense and Public Sector, Oil, Gas and Mining, Telecom and IT, Entertainment, Events and Hospitality, Other End-User Industry), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Services |

| Bluetooth Low Energy (BLE) |

| Ultra-Wideband (UWB) |

| Wi-Fi / Wi-Fi RTT |

| RFID |

| Magnetic Positioning |

| Other Technology |

| On-premises |

| Cloud |

| Navigation and Maps |

| Asset Tracking and Management |

| Proximity Marketing and Customer Engagement |

| Emergency Management and Remote Monitoring |

| Industrial Automation and Control |

| Other Application |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Retail and E-commerce |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Manufacturing and Warehousing |

| Smart Buildings and Real Estate |

| Government, Defense and Public Sector |

| Oil, Gas and Mining |

| Telecom and IT |

| Entertainment, Events and Hospitality |

| Other End-User Industry |

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | Japan | |

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Technology | Bluetooth Low Energy (BLE) | ||

| Ultra-Wideband (UWB) | |||

| Wi-Fi / Wi-Fi RTT | |||

| RFID | |||

| Magnetic Positioning | |||

| Other Technology | |||

| By Deployment Mode | On-premises | ||

| Cloud | |||

| By Application | Navigation and Maps | ||

| Asset Tracking and Management | |||

| Proximity Marketing and Customer Engagement | |||

| Emergency Management and Remote Monitoring | |||

| Industrial Automation and Control | |||

| Other Application | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By End-User Industry | Retail and E-commerce | ||

| Healthcare and Life Sciences | |||

| Transportation and Logistics | |||

| Manufacturing and Warehousing | |||

| Smart Buildings and Real Estate | |||

| Government, Defense and Public Sector | |||

| Oil, Gas and Mining | |||

| Telecom and IT | |||

| Entertainment, Events and Hospitality | |||

| Other End-User Industry | |||

| By Geography | Europe | United Kingdom | |

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | Japan | ||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the indoor location services market and how fast is it growing?

The market generated USD 14.88 billion in 2025 and is projected to advance at a 24% CAGR to USD 43.32 billion by 2030.

Which technology segment is expanding the quickest in this market?

Ultra-wideband solutions are pacing at a 25.87% CAGR through 2030 as handset makers embed native UWB radios and enterprises demand centimetre-level accuracy.

Why are hospitals and clinics accelerating RTLS deployments?

U.S. Department of Veterans Affairs standards and Joint Commission audits require continuous asset and patient visibility, making RTLS a compliance-driven necessity that also boosts operational efficiency.

How do 5G-Advanced and Wi-Fi 7 upgrades influence adoption?

Next-gen wireless networks deliver multi-gigabit bandwidth and precise channel-sounding, enabling smart-factory positioning and simultaneous data transmission that lift ROI for new installations.

What restrains adoption in dense-metal manufacturing environments?

Multipath interference degrades Wi-Fi RTT and BLE accuracy; while UWB mitigates the issue, its higher infrastructure cost forces factories to weigh capital outlays against precision gains.

Which region is forecast to record the highest growth rate?

The Asia-Pacific region is expected to expand the fastest at 26.89% CAGR on the back of mega-airport, metro, and smart-city projects that embed digital-twin wayfinding from the ground up.

Page last updated on: