Indonesia Global Capability Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

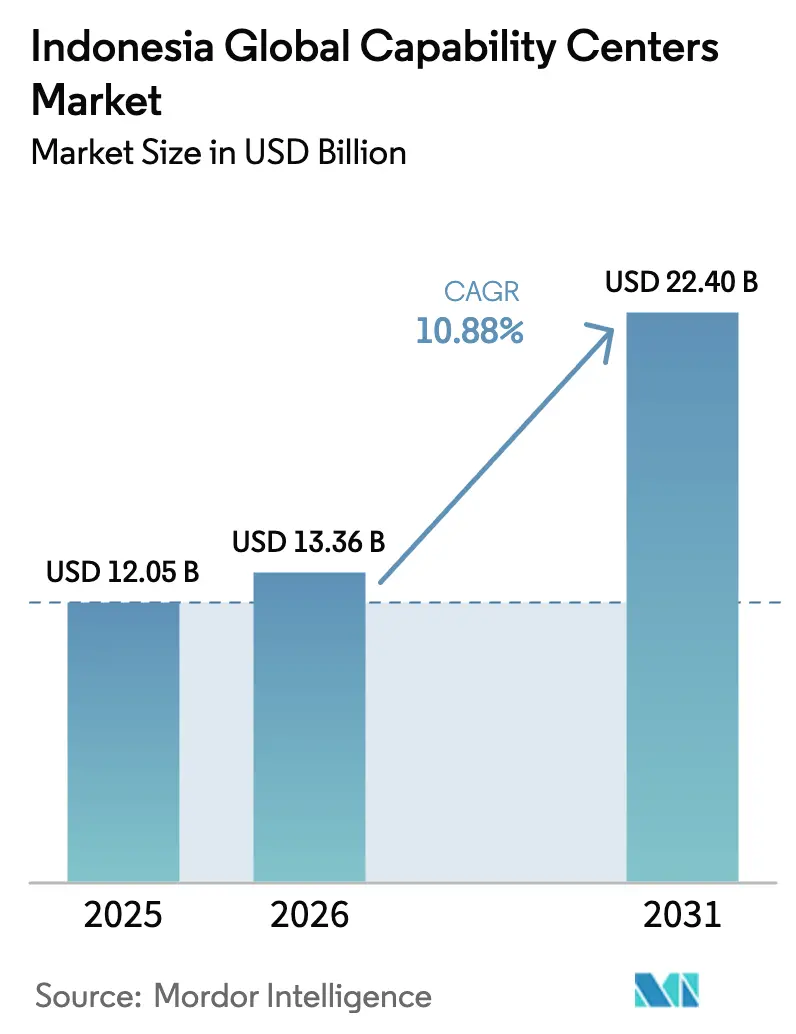

| Base Year Market Size (2025) | USD 12.05 Billion |

| Market Size (2026) | USD 13.36 Billion |

| Market Size (2031) | USD 22.4 Billion |

| Growth Rate (2026 - 2031) | 10.88% CAGR |

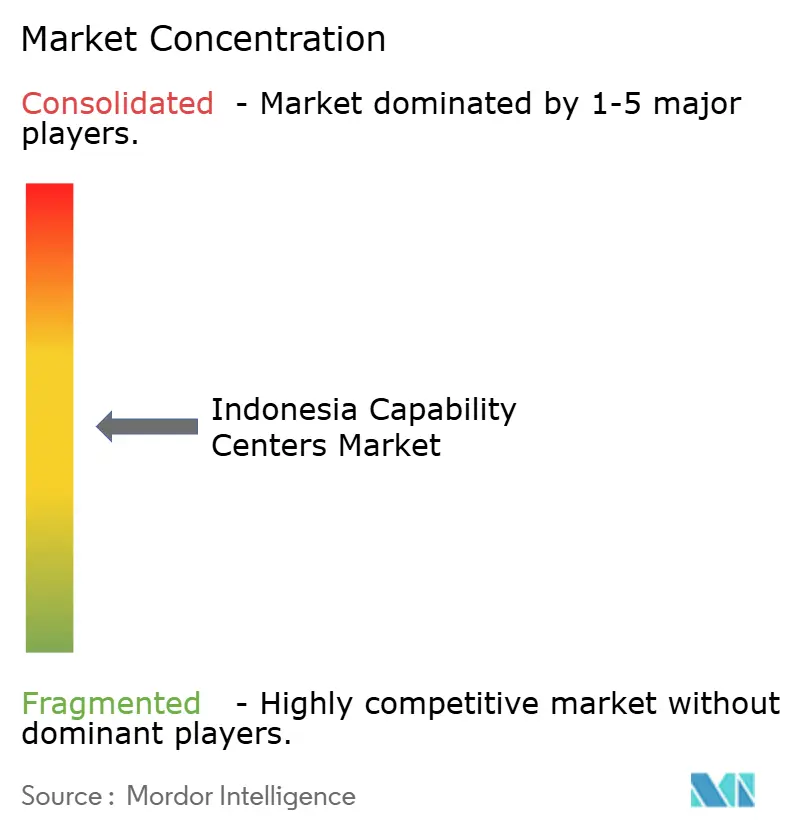

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Global Capability Centers Market Analysis by Mordor Intelligence

The Indonesia Global Capability Centers Market size was valued at USD 12.05 billion in 2025 and estimated to grow from USD 13.36 billion in 2026 to reach USD 22.4 billion by 2031, at a CAGR of 10.88% during the forecast period (2026-2031). Favorable macroeconomic fundamentals, ongoing cloud and AI infrastructure buildouts, and data residency mandates collectively drive demand for capability centers that can strike a balance between low costs and regulatory certainty. The Indonesian global capability centers market benefits from Jakarta’s stable Grade-A office rents, a multilingual mid-skill workforce graduating from universities in Java and Bali, and a rising volume of foreign direct investment earmarked for AI-ready facilities. At the same time, cybersecurity talent gaps and bureaucratic hurdles temper growth momentum, prompting operators to invest heavily in in-house training and hybrid partnership models. Competitive intensity remains moderate because no single vendor commands an outsized share, leaving room for specialized providers in high-value niches such as data governance and industry-specific analytics.

Key Report Takeaways

- By function, Business Process Management led with 44.98% revenue share in 2025; Information Technology and Digital Services are projected to expand at an 11.44% CAGR through 2031.

- By engagement model, the Captive (Self-Build) approach held 58.12% of the Indonesian global capability centers market share in 2025, while the Hybrid Build-Operate-Transfer approach is forecast to post a 12.18% CAGR from 2025 to 2031.

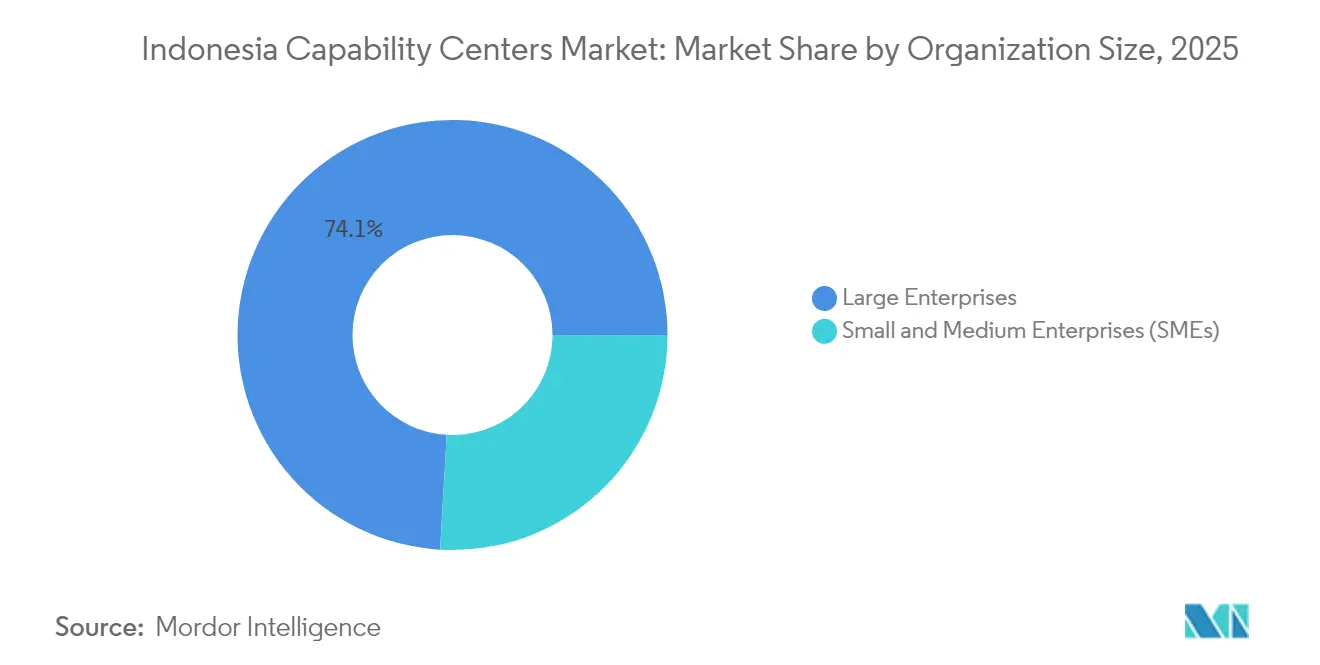

- By organization size, large enterprises accounted for a 74.08% share of the Indonesian global capability centers market size in 2025, while small and medium enterprises are expected to advance at a 13.01% CAGR through 2031.

- By industry vertical, telecom and IT captured 33.21% of the Indonesian global capability centers market in 2025; retail and consumer goods are set to lead growth with an 11.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Global Capability Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging AI-anchored digital economy investments | +2.5% | Greater Jakarta, Surabaya, Bandung | Medium term (2-4 years) |

| Accelerated cloud-first adoption by state-owned enterprises | +1.8% | National, concentrated in Java | Short term (≤ 2 years) |

| Mandatory on-shore data residency requirements | +1.2% | National, early compliance in financial services | Short term (≤ 2 years) |

| Jakarta-centric premium Grade-A office rental stagnation | +0.9% | Greater Jakarta Metropolitan Area | Long term (≥ 4 years) |

| Rising global supply-chain de-risking in Indonesia | +1.1% | Industrial corridors, SEZ locations | Medium term (2-4 years) |

| Availability of a multi-lingual mid-skill talent pool | +0.8% | Java-Bali corridor, urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging AI-Anchored Digital Economy Investments

Indonesia’s digital economy is projected to climb from USD 82 billion in 2023 to roughly double that value by 2030, triggering a surge in AI-driven workloads that flow into capability centers. Nvidia’s USD 200 million AI facility in Surakarta marks the first large-scale AI infrastructure build outside Greater Jakarta and signals geographic diversification of the Indonesian global capability centers market. Microsoft’s pledge to train 840,000 Indonesians in AI skills by 2028 directly addresses the chronic talent shortage that previously constrained large-scale deployments.[1]Satya Nadella, “Microsoft Cloud and AI Investment in Indonesia,” microsoft.com Each newly skilled AI professional significantly enhances the productive capacity of centers across data analytics, process automation, and customer experience. As corporations shift from cost arbitrage to value creation, AI capability becomes the decisive differentiator when selecting Indonesian locations. The net effect is a virtuous cycle in which infrastructure availability, talent readiness, and enterprise demand reinforce one another, lifting the trajectory of the Indonesian global capability centers market.

Accelerated Cloud-First Adoption by State-Owned Enterprises

State-owned enterprises account for a sizable share of domestic technology spend, and their cloud-first mandates generate predictable, large-volume projects for capability centers. Bank Indonesia’s Payment Systems Blueprint 2025 contains 23 deliverables, ranging from open banking to real-time retail payments, that rely heavily on specialized technical skills only Global Capability Centers can provide.[2]Perry Warjiyo, “Indonesia Payment Systems Blueprint 2025,” bi.go.id Telkom Indonesia’s IDR 1.4 trillion (USD 85 million) AI-ready data center in Batam serves as an anchor tenant model, ensuring utilization and mitigating start-up risks. Hybrid Build-Operate-Transfer arrangements thrive in this environment because they blend local compliance knowledge with multinational standards, supporting a 12.41% CAGR for the model. With each new public-private partnership, capability centers gain deeper domain knowledge in regulated sectors and strengthen their foothold in the Indonesian global market for capability centers.

Mandatory On-Shore Data Residency Requirements

Indonesia’s Personal Data Protection Law obliges firms to store personal data domestically, driving incremental demand for on-shore processing capacity. Global corporations operating high-volume customer platforms must now co-locate data-intensive functions inside Indonesia to remain compliant, effectively creating a moat around the Indonesian global capability centers market. Local data hosting yields real-time analytics advantages and eliminates latency, permitting premium pricing. Agreements such as GoTo’s collaboration with Tencent Cloud to localize workloads illustrate how hybrid cloud architectures evolve to satisfy both compliance and performance mandates. The regulation thus serves as a structural tailwind that locks multinationals into long-term Indonesian footprints and encourages further investment in in-country talent pipelines.

Jakarta-Centric Premium Grade-A Office Rental Stagnation

Contrary to many regional peers, Jakarta’s prime office rents have remained flat for four years, offering capability centers rare cost visibility in an otherwise inflationary real estate market. Stable leasing rates enable operators to secure multi-year occupancy at predictable expense levels, making total cost of ownership models more attractive than in Manila or Ho Chi Minh City. Concentration inside Indonesia’s capital deepens labor-market liquidity, enabling rapid staff redeployment across centers without relocation packages. Eastern Greater Jakarta industrial zones provide expansion space within commuting distance of core financial and telecommunications infrastructure, a combination that sustains long-term scalability. Collectively, these factors lower operating risk and contribute positively to the CAGR forecast for the Indonesian global capability centers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity talent shortfall and wage inflation | -1.4% | National, acute in Greater Jakarta | Short term (≤ 2 years) |

| Persistent bureaucratic hurdles for work permits | -0.7% | National, processing centers in Jakarta | Medium term (2-4 years) |

| Power-grid reliability gaps outside Greater Jakarta | -0.8% | Outer islands, secondary cities | Long term (≥ 4 years) |

| IP protection perception below regional peers | -0.6% | National, sector-specific variations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security Talent Shortfall and Wage Inflation

The June 2024 ransomware attack on Indonesia’s National Data Center underscored the country's limited domestic cybersecurity capabilities. Fewer than 150 CISSP-certified experts service a digital economy exceeding USD 80 billion, forcing capability centers to compete for scarce talent at premium salaries. Security headcount expanded 160% in 2024 while pay packages grew at double-digit rates, eroding Indonesia’s traditional cost advantages. Global Capability Centers processing financial or healthcare data must either absorb inflated personnel costs or extend project timelines to train internal candidates. The mismatch between demand and supply directly impacts the growth rate of Indonesia's global capability centers market, especially for workloads that require strict compliance.

Persistent Bureaucratic Hurdles for Work Permits

Indonesia’s RPTKA work-permit system imposes four-year term caps, monthly development fund fees, and a requirement to pair each foreign professional with a local “companion” worker. These stipulations introduce administrative delays and cost overheads that deter rapid staffing of niche roles. Smaller providers lacking in-house compliance units face disproportionate difficulties, which limit new entrants and constrain the competitive dynamism of the Indonesian global capability centers market. While large incumbents have learned to navigate the process, any tightening of immigration rules or fee structure could remove as much as 0.7 percentage points from the CAGR forecast by extending ramp-up timelines for new projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function / Capability: Value Creation Outpaces Labor Arbitrage

Business Process Management holds 44.98% share of the Indonesian global capability centers market, reflecting the country’s historical strength in customer support and transaction processing. Rising automation and AI adoption reconfigure these workflows, redirecting investment toward data analytics and digital customer-experience solutions. Information Technology and Digital Services, although smaller in absolute terms, is forecasted to grow at an 11.44% CAGR and is central to the repositioning of centers from cost centers to innovation hubs. The Indonesian global capability centers market size for IT and Digital Services is set to expand rapidly as enterprises deploy AI-driven tools across finance, healthcare, and e-commerce. Engineering and R&D operations, although still in their early stages, are gaining traction as vehicle electrification and battery manufacturing become established. Knowledge Process Outsourcing benefits from improving English proficiency scores and government STEM scholarship programs, enabling more advanced research and analytics assignments to be anchored locally.

Second-tier cities, such as Surabaya, attract BPM spillover due to lower wages, whereas high-skill IT work remains concentrated in Jakarta’s technology corridors. Microsoft’s new data centers extend local cloud footprints and lower latency, giving IT and Digital Services providers the compute power needed for real-time analytics. BPM vendors must therefore embed machine learning and process automation to defend their share, while entrants that can integrate AI, cybersecurity, and regulatory expertise will capture disproportionate growth in the Indonesian global capability centers market.

By Engagement Model: Hybrid Strategies Balance Control with Speed

Captive centers continue to dominate with a 58.12% share, as large multinationals seek maximum IP and process control within regulated environments. Yet the Indonesian global capability centers market increasingly rewards Hybrid Build-Operate-Transfer models, which show a 12.18% CAGR as firms leverage local partners for regulatory navigation and talent acquisition before assuming full ownership. Pure BOT structures serve cost-focused entrants willing to outsource operational management entirely; however, their relative share is declining as enterprises demand tighter integration with their parent company's innovation roadmaps.

Hybrid proponents argue that joint ventures reduce setup time by 30% and lower the risk of compliance errors. Telkom Indonesia’s partnerships demonstrate how local incumbents mitigate risk by offering a comprehensive package of real estate, connectivity, and government relations infrastructure. Traditional IT services vendors, sensing a threat, have pivoted to co-build solutions that let them retain revenue through managed services even after ownership transfers. These dynamics underscore the shift in the Indonesian global capability centers market share toward structurally flexible engagement frameworks.

By Organization Size: SMEs Unlock a New Demand Wave

Although large enterprises command 74.08% of spending, SMEs now account for the fastest growth within the Indonesian global capability centers market. Cloud standardization enables firms with limited capital to access enterprise-grade security, analytics, and customer support modules through shared-service constructs. The Indonesian global capability centers industry records a 13.01% SME CAGR as digital-native start-ups tap Jakarta’s talent pools for DevOps and product design functions. Government programs issued 7 million Business Identification Numbers in 2023 and continue to streamline online licensing, reducing onboarding friction for smaller firms. As adoption broadens, providers launch modular service catalogs that scale from pilot projects to multi-function engagements, further accelerating SME penetration.

Large multinationals, meanwhile, double down on AI and cyber-resilience upgrades, ensuring that enterprise demand remains the backbone of their revenue. The net result is a diversified customer mix that stabilizes the Indonesian global capability centers market size against cyclical shocks in any single corporate segment.

By Industry Vertical: Telecom Anchors, Retail Surges

Telecom and IT claims 33.21% of 2025 revenues, buoyed by commitments to 4G and 5G rollouts and data center buildouts by carriers. Yet, retail and consumer goods are forecast to grow at 11.62% as e-commerce spending expands beyond Java, prompting merchants to outsource logistics optimization and omnichannel customer engagement. Financial services draw strength from Bank Indonesia and OJK’s sandbox frameworks, which clear regulatory ambiguity for digital banking pilots. The Indonesian global capability centers market size attached to fintech workloads expands steadily as open-banking APIs spawn data analytics and fraud-monitoring tasks.

The electric vehicle supply chain build-up, combined with mandatory local content thresholds, drives new engineering workloads in the automotive and industrial verticals. The healthcare and life sciences sectors are adopting telemedicine and real-world evidence studies; however, progress depends on closing the cybersecurity skills gap, given the sensitivity of patient data. Together, these shifts diversify revenue streams and hedge the Indonesian global capability centers market against sector-specific downturns.

Geography Analysis

Greater Jakarta anchors a significant share of the Indonesian global capability centers market size in 2025, a position secured by superior fiber connectivity, ready access to regulators, and stable Grade-A office rents that have held flat for four years. The region’s data center inventory doubled between 2020 and 2024, providing operators with the low-latency infrastructure needed for AI workloads and real-time analytics. Concentrated talent pools enable firms to scale their headcount quickly without incurring relocation costs, while a growing base of multinational tenants continues to reinforce network effects. As a result, Greater Jakarta delivers the highest productivity per employee among domestic hubs and remains the primary landing point for most greenfield investments in Indonesia's global capability centers market.

Surabaya has emerged as the preferred secondary node, particularly for manufacturing and automotive support, thanks to its proximity to industrial corridors and a labor cost that is approximately 15% lower than the average in Jakarta. Local universities funnel engineering graduates into process automation and supply chain roles, providing multinationals with a mid-skill workforce that complements Jakarta’s more expensive specialists. Bandung plays a distinct role as an R&D satellite, leveraging a dense cluster of IT institutes that produce AI and software talent suited for high-value analytics assignments. [3]Warief Djajanto Basorie, “Indonesia's Digital Drive Gets Big Tech Backing,” Lowy Institute, lowyinstitute.org Batam, situated just 20 km from Singapore, benefits from submarine cable redundancy and houses Telkom Indonesia’s USD 85 million AI-ready data center, creating a cross-border hybrid cloud option that meets data sovereignty requirements while leveraging regional connectivity. Looking ahead, the new capital Nusantara offers 95-year land leases and up to 100% corporate income tax holidays, which could shift 10-15% of future capacity to East Kalimantan once core infrastructure is in place. Government infrastructure spending, now 12% of the budget, is upgrading toll roads and power grids across Java and Sumatra, which will gradually reduce uptime risk in secondary cities. Still, grid reliability gaps outside the Java-Bali corridor keep mission-critical workloads concentrated in established metros. Inter-provincial migration remains low at 2.3%, resulting in high talent retention; however, rapid staff scaling in outer provinces is proving to be a challenge. These geographic dynamics ensure that Jakarta maintains primacy while a concentric expansion pattern spreads the Indonesian global capability centers market share to Surabaya, Batam, and, in the longer term, Nusantara.

Competitive Landscape

The top five providers control just over half of the total revenue, giving the sector a balanced structure in which both scale and specialization confer an advantage. Global incumbents, Accenture, IBM, and Tata Consultancy Services, leverage mature delivery frameworks and deep client rosters to win complex transformation mandates. Local champions PT Telekomünikasyon Indonesia and PT Indosat Ooredoo Hutchison capitalize on their regulatory familiarity to secure state-owned enterprise contracts, particularly in the telecom and fintech verticals. Because no single vendor holds more than a low double-digit share, buyers can negotiate favorable terms, while vendors must continuously enhance their value propositions to defend their position in the Indonesian global capability centers market.

Strategic partnerships dominate current expansion moves. Microsoft collaborates with multiple local operators to accelerate cloud migration and jointly train 840,000 Indonesians in AI skills by 2028, a program that directly enlarges the addressable labor pool. Nvidia’s USD 200 million Surakarta AI hub is structured as a partnership with Indosat, creating an ecosystem in which hyperscale compute capacity is paired with telecom connectivity. Hybrid Build-Operate-Transfer contracts are increasingly popular, as they allow foreign firms to share initial regulatory risk with local partners before assuming full ownership, which explains the model’s 12.41% CAGR. Traditional IT services vendors, sensing margin erosion, now pitch joint-innovation labs rather than pure outsourcing to stay embedded in client roadmaps.

Specialization is the emerging battleground. Firms offering Islamic finance compliance, EV battery analytics, or advanced cyber resilience solutions command premium pricing and fend off commoditization pressures. Cybersecurity shortages have prompted several mid-tier providers to acquire boutique security consultancies with global certifications, a trend expected to accelerate following the 2024 National Data Center breach.[4]Otoritas Jasa Keuangan, “Peta Jalan Pengembangan dan Penguatan Inovasi Teknologi Sektor Keuangan 2024–2028,” ojk.go.id Wage inflation, especially for CISSP-certified professionals, is spurring investment in low-code automation and proprietary AI copilots that raise output per employee. Altogether, these maneuvers maintain a moderate yet dynamic competitive intensity, with sustained opportunities for entrants that can combine regulatory fluency, vertical expertise, and technological depth in the Indonesian global capability centers market.

Indonesia Global Capability Centers Industry Leaders

Accenture plc

International Business Machines Corporation (IBM)

Tata Consultancy Services Limited

Cognizant Technology Solutions Corporation

Capgemini SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Bank Indonesia issued PP 28/2025, a reform package that trims foreign-investment and payment-system license approvals to 45 days for qualified capability-center operators, easing a bottleneck that had slowed market entry.

- August 2025: Apple has revealed plans for a fifth Apple Developer Academy in Thamrin, Jakarta, set to open in 2026. The academy is expected to train 2,000 Swift and iOS developers annually, thereby extending the company’s Indonesian talent pipeline beyond Surabaya and Batam.

- July 2025: Worldvuer iByond Limited signed agreements to build a USD 400 million Quantum AI Data Center in Batam. The 50 MW facility, billed as Asia’s first quantum-ready site for AI workloads, will serve financial services and pharmaceutical research clients.

- May 2025: The Indonesian government and Oracle have agreed to create ASEAN’s largest GPU cluster and launch an Indonesian public cloud region in Q3 2025, which will support up to 100,000 concurrent AI training jobs.

Indonesia Global Capability Centers Market Report Scope

The scope of the global capability center study for the market segmentation by the Function/Capability for (i) Information Technology (IT) and Digital Services segment is limited to Software Development, Cloud and Infrastructure Management, Cybersecurity, Data Analytics and AI/ML; (ii) Engineering / ER&D segment is limited to Product Design and Testing, Embedded Systems, Digital Twin / Simulation; (iii) Business Process Management (BPM) segment is limited to Finance and Accounting, HR, Payroll and Talent Management, Procurement, Customer Service; and (iv)Knowledge Process Outsourcing (KPO) segment is limited to Market Research and Insights, Risk and Compliance, Legal and Regulatory Support, Strategy and Consulting Support. Similarly, for segmentation by the Engagement Model, scope for (i) Hybrid Build-Operate-Transfer (BOT) is limited to Joint Venture / Strategic Partnership and Virtual Captive Model. The rest of the segment scope is as specified for the listed segment.

| Information Technology (IT) and Digital Services |

| Engineering / ER&D |

| Business Process Management (BPM) |

| Knowledge Process Outsourcing (KPO) |

| Captive (Self-Build) / In-house |

| Build-Operate-Transfer (BOT) |

| Hybrid Build-Operate-Transfer (BOT) |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT |

| Healthcare and Life Sciences |

| Manufacturing, Automotive and Industrial |

| Retail and Consumer Goods |

| Other Industry Verticals |

| By Function / Capability | Information Technology (IT) and Digital Services |

| Engineering / ER&D | |

| Business Process Management (BPM) | |

| Knowledge Process Outsourcing (KPO) | |

| By Engagement Model | Captive (Self-Build) / In-house |

| Build-Operate-Transfer (BOT) | |

| Hybrid Build-Operate-Transfer (BOT) | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By Industry Vertical | Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT | |

| Healthcare and Life Sciences | |

| Manufacturing, Automotive and Industrial | |

| Retail and Consumer Goods | |

| Other Industry Verticals |

Key Questions Answered in the Report

How fast is the Indonesian global capability centers market projected to grow through 2031?

The market is expected to post a 10.88% CAGR, rising from USD 13.36 billion in 2026 to USD 22.4 billion by 2031.

Which functional segment is expanding the quickest?

Information Technology and Digital Services lead growth with an 11.44% CAGR as enterprises deploy AI-enabled solutions.

What engagement model is gaining popularity among multinationals?

The Hybrid Build-Operate-Transfer model is the fastest-growing, advancing at a 12.18% CAGR, as it strikes a balance between control and regulatory ease.

Why is Jakarta still the primary hub for capability centers?

Stable Grade-A rents, dense talent clusters, and immediate regulator access keep Jakarta at the center of 60% of all Global Capability Center activity.

What is the main supply-side challenge faced by providers?

A shortage of certified cybersecurity professionals drives up wages and hinders the deployment of high-compliance projects.

How are state-owned enterprises influencing Global Capability Center demand?

SOE cloud-first mandates and digital-payment blueprints create large, predictable workloads that anchor long-term Global Capability Center investments.

Page last updated on: