Indonesia E-cigarette Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

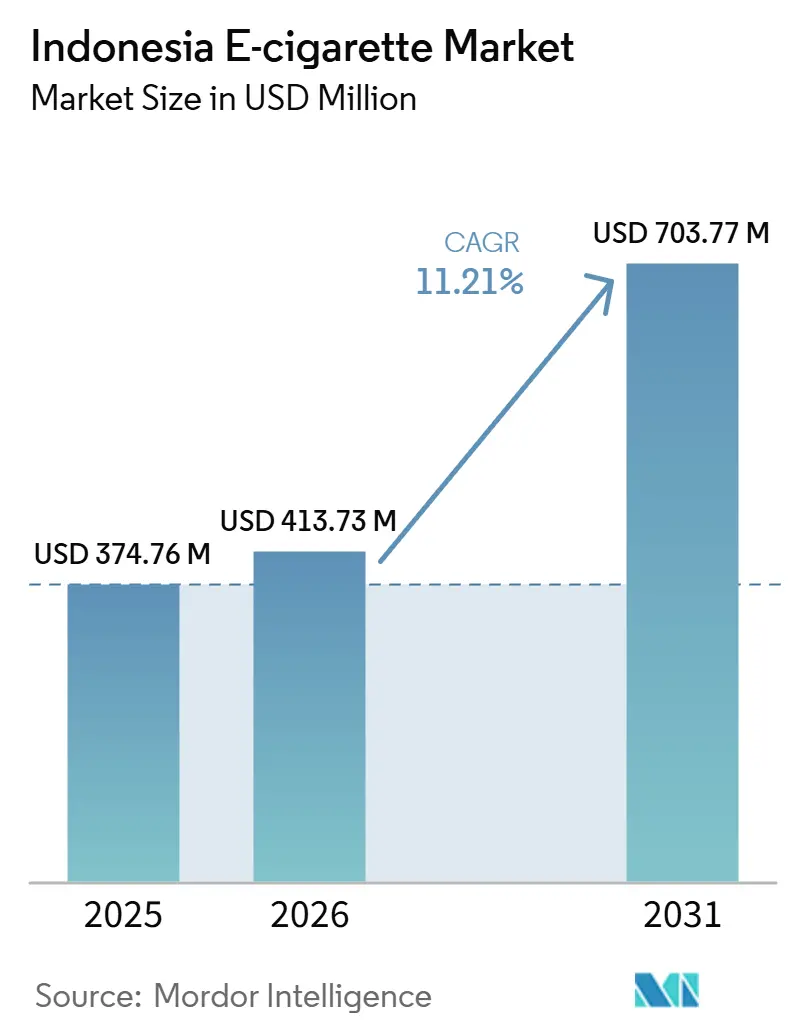

| Base Year Market Size (2025) | USD 374.76 Million |

| Market Size (2026) | USD 413.73 Million |

| Market Size (2031) | USD 703.77 Million |

| Growth Rate (2026 - 2031) | 11.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia E-cigarette Market Analysis by Mordor Intelligence

The Indonesia E-cigarette Market size is projected to be USD 374.76 million in 2025, USD 413.73 million in 2026, and reach USD 703.77 million by 2031, growing at a CAGR of 11.21% from 2026 to 2031. A large smoker base supports demand, as 30.8% of Indonesians aged 15 and above smoked in 2023. Younger adults also drive adoption, with e-cigarette use among those aged 15 to 24 reaching 7.5% in 2021. In 2024, APVI reported over 4 million active users, while excise stamp purchases rose 50% year-on-year to IDR 2.8 trillion, or USD 171 million. The market is shifting toward formal retail, differentiated products, and stricter compliance, favoring brands with broad distribution, testing capability, and product registration. However, tighter packaging, advertising, testing, and retail distance rules may raise costs and limit formal sellers over the forecast period.

Key Report Takeaways

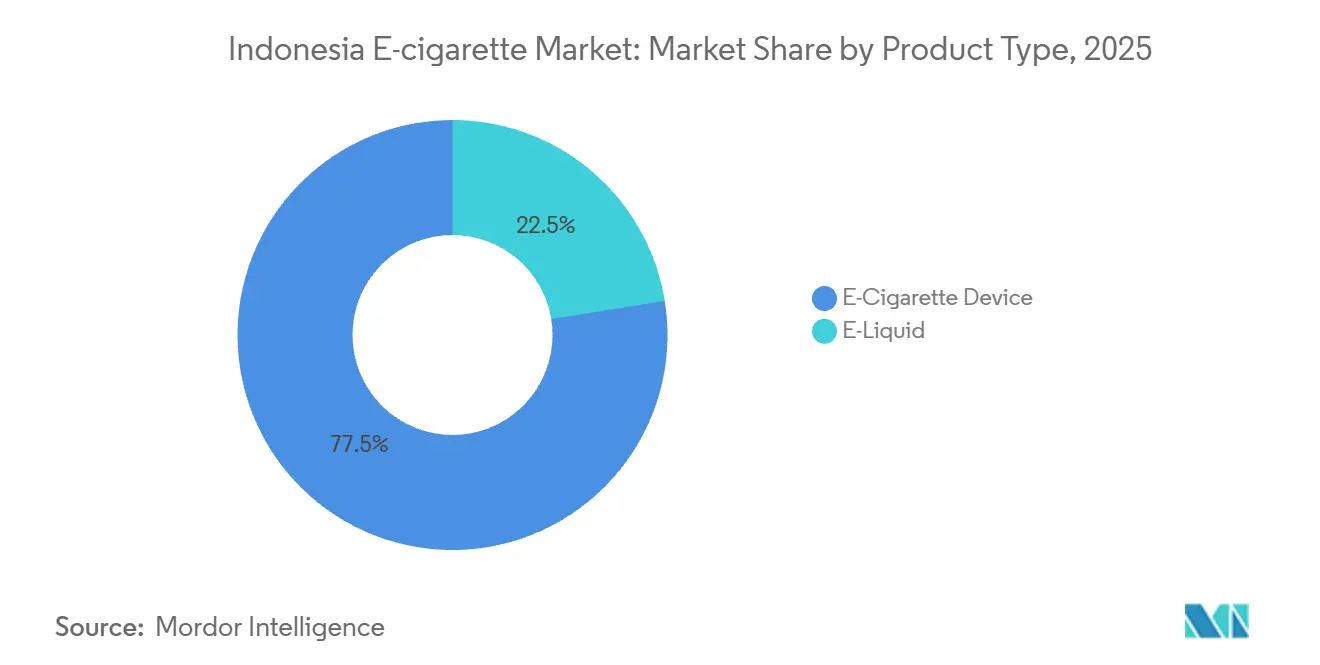

- By product type, e-cigarette devices led with a 77.54% share in 2025, while e-liquid is forecast to expand at 13.23% CAGR through 2031.

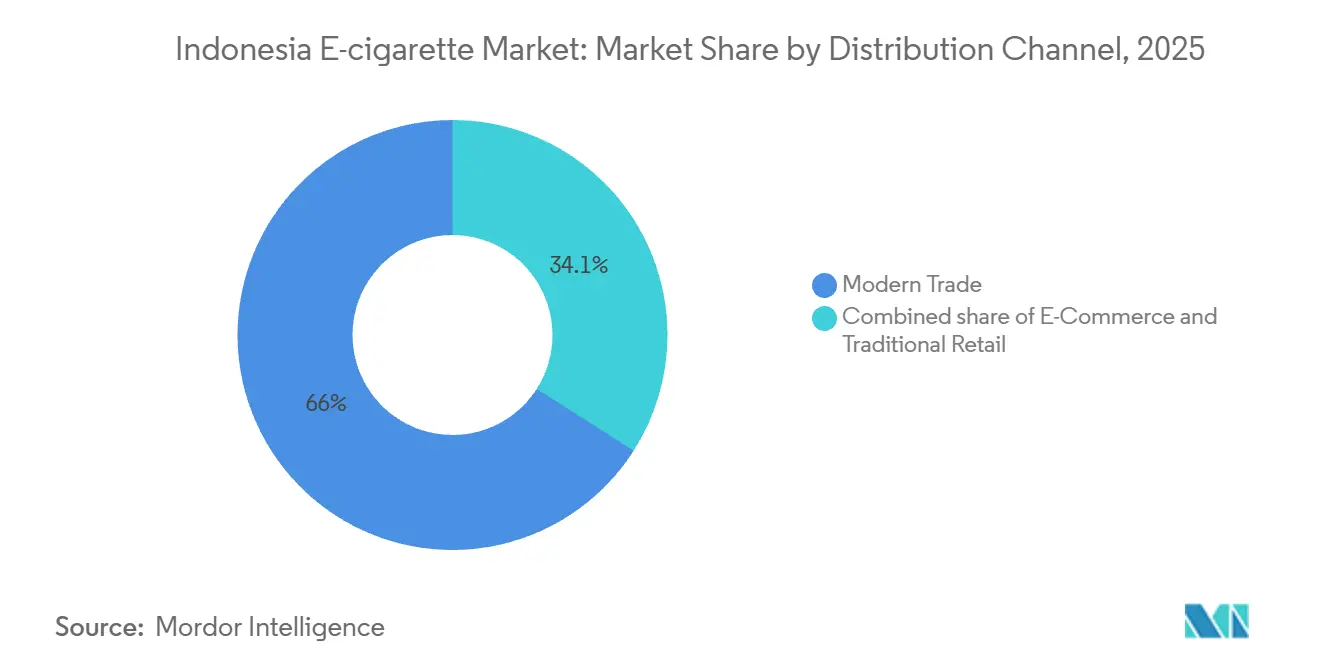

- By distribution channel, modern trade held 65.95% of the Indonesia e-cigarette market size in 2025, while e-commerce is projected to grow at 15.41% CAGR through 2031.

- By city, Jakarta held 40.49% of the Indonesia e-cigarette market share in 2025, while Surabaya is forecast to advance at 14.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia E-cigarette Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing awareness of alternative smoking products | +2.4% | National, with concentrated impact in Jakarta, Surabaya, Bandung | Medium term (2-4 years) |

| Rising acceptance of vaping as a lifestyle choice | +2.1% | National, with higher intensity in Jakarta, Bali, Medan | Medium term (2-4 years) |

| Strong influence of youth and young-adult preferences | +2.3% | National, predominantly among the 15-24 age cohort in Java and Bali | Short term (≤ 2 years) |

| Product innovation and device variety | +1.8% | National, with innovation-led uptake strongest in Jakarta and Surabaya | Long term (≥ 4 years) |

| Marketing and promotion efforts | +1.5% | Java-centric, with spillover to Bali, Medan, Makassar | Short term (≤ 2 years) |

| Technological improvements in user experience | +1.3% | National, with strongest impact among premium buyers in tier-1 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Awareness of Alternative Smoking Products

The Indonesia e-cigarette market benefited from the country’s large conventional smoking base. Adult male smoking prevalence reached 57.9% in 2023, creating a broad group of consumers who may consider alternative nicotine products[1]Source: World Health Organization Indonesia, “World No Tobacco Day 2025, WHO Hails Indonesia's Bold Reforms, Calls for Decisive Action on Standardized Packaging”, who.int . Awareness has also moved beyond niche hobby users. APVI indicated that active e-cigarette users exceeded 4 million in 2024, rising from a much smaller base only a few years earlier. In major cities such as Jakarta and Surabaya, product trials spread through workplaces, cafes, vape shops, and social circles, making e-cigarettes more visible to potential users. The Indonesia e-cigarette market also gained from GR 28/2024, which treated e-cigarettes as a separate addictive substance category rather than fully combining them with conventional tobacco. This regulatory distinction helped consumers view e-cigarettes as a separate product class. As testing and registration rules became clearer, formal products gained more credibility than illicit and unregistered items, supporting stronger conversion from curiosity to paid use.

Rising Acceptance of Vaping as a Lifestyle Choice

The Indonesia e-cigarette market showed demand patterns driven largely by lifestyle use rather than smoking cessation alone. Vaping gained cultural relevance in cafes, nightlife venues, and youth social settings, increasing its visibility as a daily accessory rather than as a medical or quitting tool. A 2025 study in Jurnal Sosial Teknologi found that social media content on e-cigarettes in Indonesia was largely positive, while warnings were often limited or visually weak, helping create a more favorable public image. Bali clearly reflected this trend, as BPS-reported e-cigarette prevalence in the province reached 2.24% in March 2025, the highest in Indonesia, indicating that tourism-heavy and outward-looking environments accelerated adoption. The market also showed a shift toward culturally localized products, as brands developed flavors around local taste cues and competed on familiarity and identity, in addition to hardware features.

Strong Influence of Youth and Young-Adult Preferences

The Indonesia e-cigarette market remained highly exposed to youth and young-adult behavior, despite stricter formal legal purchasing-age requirements. The 2023 Global School-Based Health Survey found that 12.4% of Indonesian students aged 13 to 17 currently used e-cigarettes, indicating strong upstream demand signals before many consumers reached the legal purchasing age. A 2025 study in BMC Public Health found that social media exposure and peer influence were the strongest drivers of initiation, with both factors reinforcing each other rather than acting independently. Research from Diponegoro University in 2024 showed that adolescents exposed to online e-cigarette advertising were 2.91 times more likely to have ever used e-cigarettes, highlighting the continued importance of digital discovery for this age group. As nearly 40% of Indonesia’s population is under 25, the Indonesia e-cigarette market continued to receive a steady inflow of new legal-age consumers, even if average penetration moderated over time.

Product Innovation and Device Variety

The Indonesia e-cigarette market has shifted from open-system devices and do-it-yourself liquids to a wider mix of closed pods, refillable devices, disposables, and heated tobacco products. This shift reflects rising demand for convenience, portability, consistent quality, and easier use as the consumer base expands beyond hobby-led early adopters. PT Delta Sukses Teknologi’s planned launch of the DJOY BEAM Series in September 2025 shows that local manufacturers are competing not only on price but also on interface design, coil technology, and user experience. Regulation is also shaping product development, as GR 28/2024 packaging rules and cartridge volume limits fit more easily with standardized pod systems than with unbranded open systems. PMI’s VEEV NOW ULTRA, which offers 1,100 puffs and uses 75% recycled aluminum, shows how companies are combining device design, convenience, and sustainability-led positioning to appeal to urban consumers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uncertain regulatory enforcement | -1.6% | National, with particularly complex local enforcement in tier-2 cities outside Java | Short term (≤ 2 years) |

| Ban or limits on certain additives and flavors | -1.2% | National, with highest impact on e-liquid producers in Java and Surabaya clusters | Medium term (2-4 years) |

| Negative perception of addictiveness | -0.9% | National, strongest in lower-income and rural-adjacent demographics | Long term (≥ 4 years) |

| Mandatory health warnings and packaging controls | -0.8% | National, with costs hitting small-batch domestic producers most strongly | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Uncertain Regulatory Enforcement

The Indonesia e-cigarette market faced its biggest restraint from uncertainty in how rules would be enforced across cities and districts. GR 28/2024 imposed age verification, school-distance restrictions, and testing obligations, but implementation capacity was uneven across Indonesia’s large and fragmented administrative structure. APVI warned that strict application of the 200-meter school-distance rule in dense cities could force many vape stores to relocate or close, especially in Java where urban retail clusters are tightly packed. The Indonesia e-cigarette market also faced a difficult balance between compliance and affordability, because stronger enforcement against illicit supply could raise prices in the formal channel and push some consumers toward unregulated products instead of away from vaping. BPOM’s expanded supervisory role under the 2025 framework was an important step, but turning central authority into consistent field enforcement across an archipelagic country remained a multi-year task.

Ban or Limits on Certain Additives and Flavors

The Indonesia e-cigarette market remained vulnerable to flavor and additive controls, as demand depended more on a wide range of flavors than on nicotine delivery alone. GR 28/2024 allowed the Health Ministry to maintain and update lists of prohibited substances, creating ongoing uncertainty for producers that relied on specific formulations. This pressure was already evident by 2025, when PPEI reported that successive excise hikes and expectations of tighter additive controls had reduced active liquid producers from more than 300 to 170. As a result, the market could shift further toward closed-system pods if local liquid makers lose the ability to refresh flavors quickly or manage compliance costs. BPOM’s mandatory laboratory testing rules also raised barriers, as flavor innovation had long helped domestic e-liquid brands retain users, and pre-market testing slowed that product refresh cycle.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Devices Anchor Share, E-Liquids Set the Pace

E-cigarette devices held 77.54% of the Indonesia e-cigarette market in 2025, which showed that category entry still depended heavily on an initial hardware purchase before repeat liquid spending built up. The Indonesia e-cigarette market developed around hardware-led adoption because users typically began with a device decision and only later formed brand loyalty around pods or liquids. Closed-system and pod-based formats gained ground over open-system mods between 2020 and 2025 as convenience, portability, and easier everyday use became more important in urban settings. This shift also aligned with GR 28/2024 cartridge rules, so device formats that already fit those specifications were better placed to scale in formal retail.

E-liquid accounted for the remaining 22.5% share in 2025 and is forecast to grow at 13.23% CAGR through 2031, making it the faster-moving side of the Indonesia e-cigarette market as the installed base of device users expands recurring consumption. That growth path reflected repeat purchase behavior, since once a device entered regular use, liquid and pod replenishment became the more frequent spending line. The Indonesia e-cigarette industry had historically supported a wide local flavor culture with hundreds of producers, which made liquids the most diverse part of the category. That diversity gave local brands an edge in taste familiarity and price flexibility, even when multinational brands led in device systems.

By Distribution Channel: Modern Trade Organizes the Market, E-Commerce Redefines Access

Modern trade held 65.95% of the Indonesia e-cigarette market size in 2025, reflecting how strongly the category was moving toward formal retail environments with better control over age checks and product display. The Indonesia e-cigarette market favored modern trade because regulation increasingly rewarded channels that could show clear operating procedures and stable store standards. Organized minimarkets and chain-led outlets also gave brands better visibility, more predictable merchandising, and wider reach than fragmented independent stores. This made formal retail not just a sales route, but also a compliance signal for both consumers and regulators.

E-commerce is projected to grow at 15.41% CAGR from 2026 to 2031, which makes it the fastest-moving channel in the Indonesia e-cigarette market even though formal restrictions remain. Digital retail benefited from Indonesia’s broad online shopping culture and from the fact that adult buyers already used major platforms for other lifestyle and personal products. The Indonesia e-cigarette market also showed an unusual digital pattern, because web-based transactions remained more relevant than mobile app listings due to platform restrictions on vaping products. This did not stop online demand, but it did make the channel more intentional and less impulse-driven.

Geography Analysis

Jakarta held 40.49% of the Indonesia e-cigarette market share in 2025, which reflected the city’s concentration of purchasing power, formal retail infrastructure, and flagship brand activity. The Indonesia e-cigarette market centered heavily on Jakarta because the capital combined dense consumer traffic with a stronger modern trade footprint than any other city in the country. Premium closed-pod products found a natural base there, as higher disposable incomes supported more frequent spending on branded devices and refills. The wider Jabodetabek area deepened that advantage by linking Jakarta to adjacent urban clusters where vape boutiques, specialty stores, and chain outlets were already established.

Jakarta’s lead was not only about population scale. It also reflected how multinational brands typically used the capital as the first launch point for new devices, pods, and retail partnerships before broader expansion. That gave Jakarta a role as both the largest revenue center and the most important testing ground for pricing, promotion, and compliance-led retail models. In the Indonesia e-cigarette market, brands that performed poorly in Jakarta often lacked the confidence or cash flow to scale nationally. The city therefore shaped national competition more than its raw share alone suggested.

Surabaya is forecast to grow at 14.54% CAGR through 2031, which makes it the fastest-moving city in the Indonesia e-cigarette market. That pace reflected the city’s balance of purchasing power, local brand presence, and lower competitive saturation compared with Jabodetabek. PT Rokok Elektrik Enak, known through the Vapeboss brand, is based in Surabaya, which gave the city a stronger embedded domestic ecosystem than many other regional markets. The Indonesia e-cigarette market also treated Surabaya as a practical second-city expansion target because it combined a large young-adult consumer base with its role as the main commercial hub for East Java.

Competitive Landscape

The Indonesia e-cigarette market remained moderately consolidated, with a few multinational tobacco companies holding clear advantages in distribution, regulatory readiness, and brand recognition. PT HM Sampoerna, under Philip Morris International, and PT Bentoel Internasional Investama, under British American Tobacco, led the premium segment through smoke-free and next-generation products. The market favored these firms because they had broad distributor networks, stronger working capital, and the ability to manage testing, packaging, and registration costs. Their advantage remained structural, as GR 28/2024 compliance required systems, documentation, and time that many smaller operators could not easily build. However, the market did not become fully concentrated, as local liquid makers and imported hardware brands continued to serve large parts of the mid-market and value segments.

RELX followed a different path by expanding into formal retail channels. Through its distributor relationship and partnership with Indomaret, the brand moved from specialist vape stores into chain retail, improving visibility where access and compliance mattered. PMI also made a long-term move with its USD 330 million Karawang smoke-free facility, adding local manufacturing and advanced testing capability in Indonesia instead of relying only on imports. These steps showed that the market was no longer shaped only by branding. Companies also needed shelf space, compliant products, reliable supply, and stronger quality control under tighter rules.

Competition also developed between multinational premium systems and unbranded low-cost devices. Chinese hardware brands such as Geekvape, Vaporesso, Aspire, and Innokin offered strong engineering and fast price moves, but many lacked local regulatory relationships and flavor partnerships that could improve consumer retention. Domestic e-liquid makers understood Indonesian taste preferences better, but many lacked a device ecosystem to support repeat purchases. This gap created room for hybrid models, with DJOY BEAM standing out by combining local production with more advanced hardware positioning. As BPOM supervision tightened, the strongest competitive edge was likely to come from registered products, formal channel access, stable supply, and enough product depth to serve premium and mid-market users.

Indonesia E-cigarette Industry Leaders

RELX Technology Co., Ltd.

British American Tobacco plc

Philip Morris International Inc.

Japan Tobacco Inc.

Shenzhen Smoore Technology Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: PT Delta Sukses Teknologi launched the DJOY BEAM Series, comprising BEAM Pro, BEAM Pod, and BEAM Go, making DJOY the first Indonesian e-cigarette brand to introduce a Closed System Device with Interactive UI. The BEAM Pro incorporates Next Generation Ceramic Coil, FEELM Pro, technology and supports up to 1,200 puffs per refillable pod.

- July 2025: PT HM Sampoerna (HMSP), in partnership with Philip Morris International (PMI), inaugurated a USD 330 million (IDR 5.35 trillion) smoke-free tobacco product factory in Karawang, West Java. The facility, Southeast Asia's first dedicated smoke-free manufacturing plant and PMI's seventh globally, houses PMI's only Advanced Lab in Asia, staffed by approximately 200 local specialists, and is designed to supply both the Indonesian domestic market and the broader Asia-Pacific region

- July 2025: PMI's VEEV brand launched the VEEV NOW ULTRA disposable pod in Indonesia with a 1,100-puff capacity, more than double the prior VEEV NOW model, constructed from 75% recycled aluminium, and including a low-liquid detection system, marking an upgrade in both product performance and sustainability credentials for the disposable segment.

Indonesia E-cigarette Market Report Scope

| E-Liquid | |

| E-Cigarette Devices | Disposable E-Cigarette |

| Non-Disposable E-Cigarette |

| Traditional Retail |

| Modern Trade |

| E-Commerce |

| Jakarta |

| Surabaya |

| Medan |

| Bandung |

| Bali |

| Rest of Indonesia |

| By Product Type | E-Liquid | |

| E-Cigarette Devices | Disposable E-Cigarette | |

| Non-Disposable E-Cigarette | ||

| By Distribution Channel | Traditional Retail | |

| Modern Trade | ||

| E-Commerce | ||

| By City | Jakarta | |

| Surabaya | ||

| Medan | ||

| Bandung | ||

| Bali | ||

| Rest of Indonesia | ||

Key Questions Answered in the Report

What is the projected value of Indonesia e-cigarette market by 2031?

The Indonesia e-cigarette market is projected to reach USD 703.77 million by 2031, up from USD 374.76 million in 2025, at an 11.21% CAGR from 2026 to 2031.

Which product category leads sales in Indonesia e-cigarette market?

E-cigarette devices led the Indonesia e-cigarette market with 77.54% share in 2025, showing that hardware remains the main entry point for category spending.

Which channel is growing fastest for e-cigarette sales in Indonesia?

E-commerce is the fastest-growing channel, with forecast growth of 15.41% CAGR through 2031, even though modern trade still held the largest share in 2025.

Why is Surabaya important for future category growth?

Surabaya is expected to grow at 14.54% CAGR through 2031, helped by its young-adult base, commercial importance in East Java, and stronger local brand ecosystem.

Page last updated on: