Indonesia Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

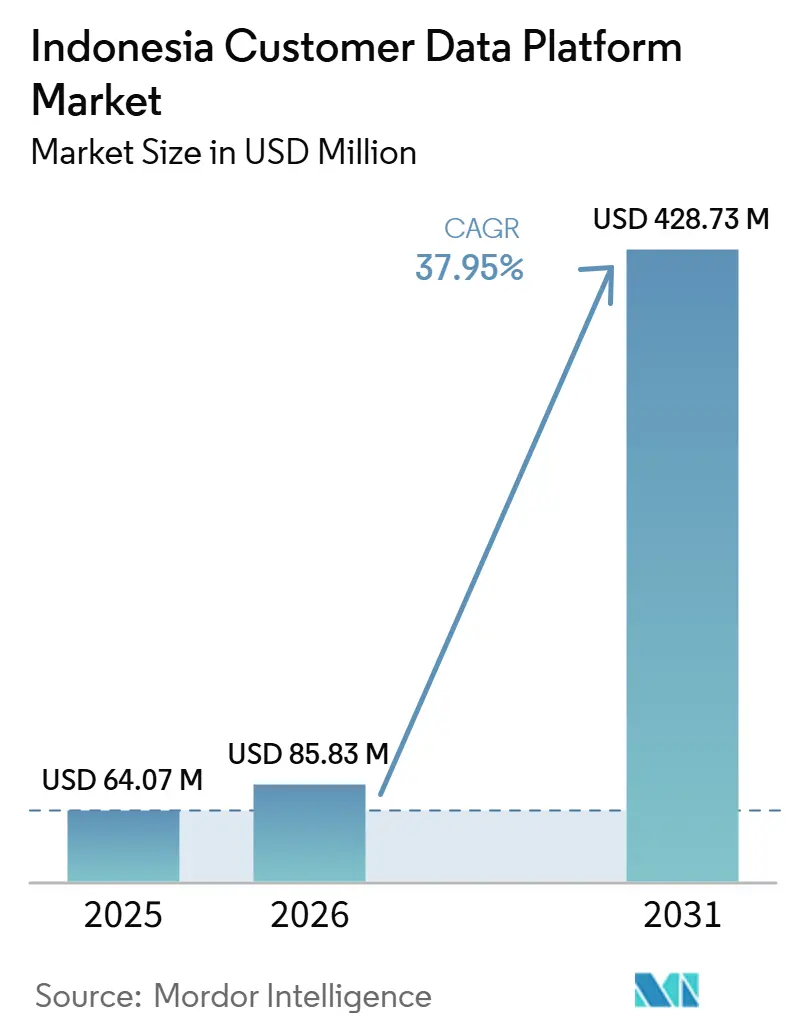

| Base Year Market Size (2025) | USD 64.07 Million |

| Market Size (2026) | USD 85.83 Million |

| Market Size (2031) | USD 428.73 Million |

| Growth Rate (2026 - 2031) | 37.95% CAGR |

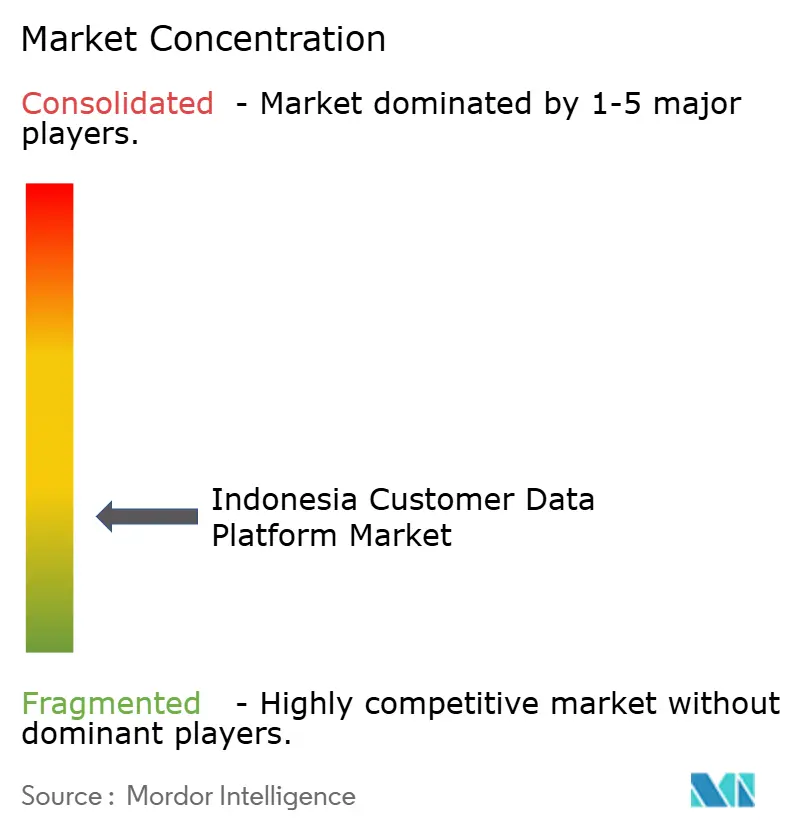

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Customer Data Platform Market Analysis by Mordor Intelligence

The Indonesia customer data platform market size is expected to increase from USD 64.07 million in 2025 to USD 85.83 million in 2026 and reach USD 428.73 million by 2031, growing at a CAGR of 37.95% over 2026-2031. The Indonesia customer data platform market is expanding as companies need first-party data systems that can operate after changes to third-party tracking and under stricter privacy rules. Demand is also rising because AI-led marketing, service, and customer engagement tools need unified, consented, and identity-resolved data to perform well at scale. The spread of omnichannel commerce across marketplaces, social commerce, live-stream shopping, mobile apps, and physical stores is making fragmented customer records harder to manage without a dedicated platform. Competition in the Indonesia customer data platform market now spans global suite vendors, warehouse-native specialists, and local martech providers, which is improving product breadth while also keeping pricing pressure high. Adoption still faces delays due to legacy systems, data silos, implementation complexity, and the full ownership costs of enterprise-grade deployments, especially outside the largest enterprise accounts.

Key Report Takeaways

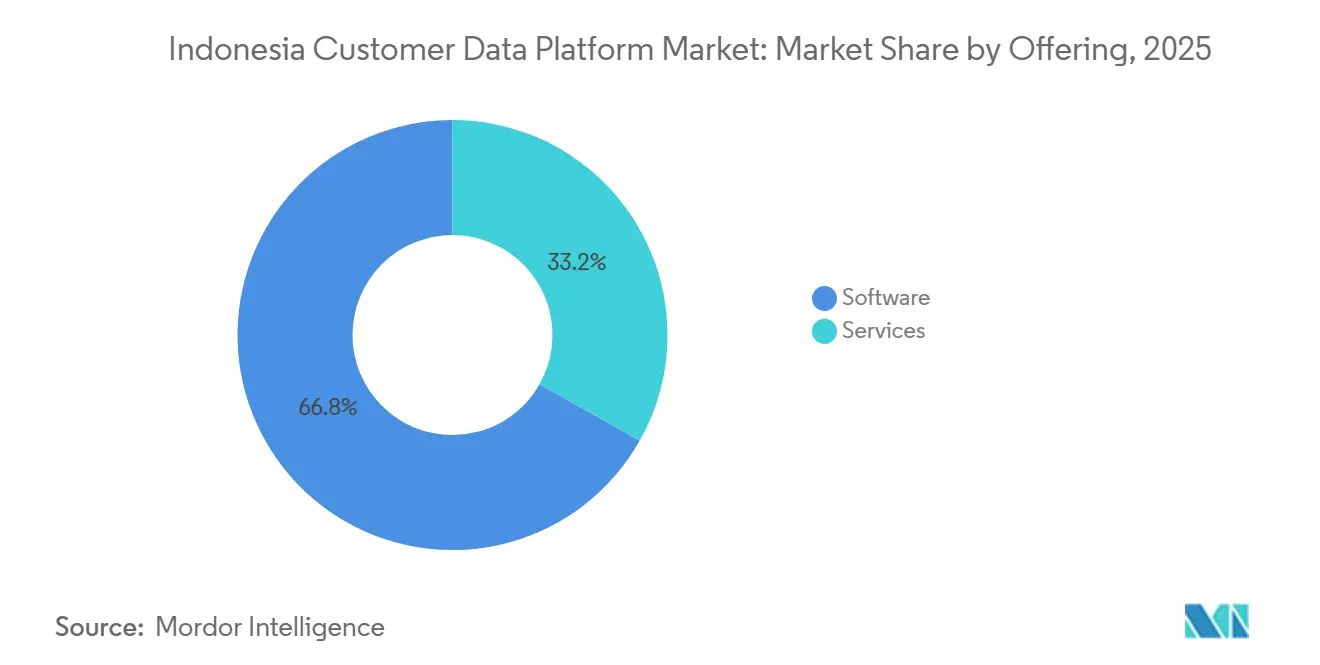

- By offering, software held 66.81% of the Indonesia customer data platform market in 2025, while services are projected to expand at a 39.24% CAGR through 2031.

- By deployment mode, cloud accounted for 74.19% of the market share in 2025, while hybrid is expected to record the fastest CAGR of 42.48% through 2031.

- By organization size, large enterprises held 60.74% share in 2025, while small and medium enterprises are projected to expand at a 40.81% CAGR through 2031.

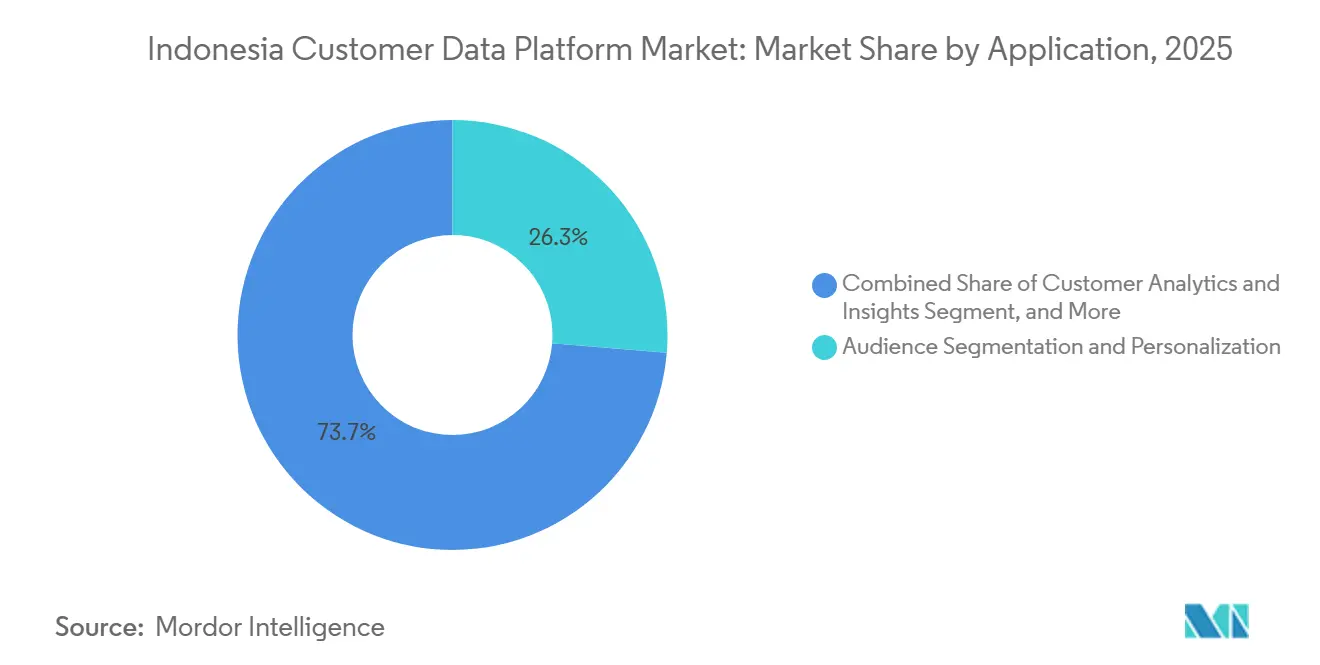

- By application, audience segmentation and personalization accounted for 26.31% of the market share in 2025, while customer analytics and insights are projected to grow at a 43.62% CAGR through 2031.

- By end-user industry, retail and e-commerce held 28.83% share in 2025, while media and entertainment is expected to advance at a 41.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Third-Party Cookie Phase-Out and First-Party Data Strategies | +7.2% | Global, with concentrated urgency in Indonesia's e-commerce and digital advertising ecosystems | Short term (≤ 2 years) |

| Generative AI Adoption and Unified Customer Graphs | +6.8% | Indonesia-wide, with early concentration in Jakarta's enterprise corridor | Medium term (2-4 years) |

| Headless and Omnichannel Commerce Expansion | +5.4% | Indonesia and Southeast Asia, highest intensity in Java-based urban retail clusters | Medium term (2-4 years) |

| Real-Time Personalization Demand in Retail and BFSI | +5.1% | Indonesia-wide, across Tier-1 and emerging Tier-2 cities | Short term (≤ 2 years) |

| Data Localization and Sovereignty Requirements | +4.2% | National, with highest compliance urgency in BFSI and healthcare | Medium term (2-4 years) |

| Warehouse-Native and Zero-Copy Architectures | +3.6% | Global, with adoption acceleration in Indonesia's cloud-forward digital-native companies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Third-Party Cookie Phase-Out Accelerating First-Party Data Strategies

The shift away from third-party tracking is pushing companies to build their own persistent customer records across marketing, sales, service, and commerce systems. For the Indonesia customer data platform market, that change matters because a CDP can combine fragmented customer interactions into a portable profile that teams can actually use in activation and analytics. Privacy rules are reinforcing the same direction, since consent, lawful processing, and data governance are much harder to manage when customer information sits across disconnected tools. This is turning first-party data from a marketing preference into a business requirement for companies that depend on digital customer acquisition and retention. The result is that the Indonesia customer data platform market is benefiting from both a technical shift in digital advertising and a governance shift in enterprise data management.

Generative AI Adoption Requiring Unified Customer Graphs

Generative AI is increasing the value of clean customer data because AI tools produce stronger outputs when profiles, preferences, and recent behaviors are unified in a single environment. Microsoft reported that 33% of Indonesian workers were Frontier Professionals in 2026, more than double the global average, indicating how quickly advanced AI use is taking shape in the country.[1]Microsoft, “Microsoft's Work Trend Index 2026, 33% of Indonesian Workers Are at the Forefront of AI Adoption,” Microsoft News, news.microsoft.com That matters for the Indonesia customer data platform market because AI-driven personalization, automated recommendations, and customer agents all depend on timely and identity-resolved data feeds. Companies that build unified customer graphs earlier are likely to improve model relevance faster because each interaction adds more usable context for future decisions. This is why the Indonesia customer data platform market is moving beyond simple profile storage and toward a broader role as the data layer behind AI-led customer engagement.

Headless and Omnichannel Commerce Expansion in Indonesia and Southeast Asia

Indonesia's commerce environment now spans marketplaces, live-stream channels, social commerce, brand-owned apps, websites, and physical stores, and each channel can create a separate customer identifier. That fragmentation makes it harder to understand the same customer across the full journey, especially when sessions are short and buying behavior changes quickly. In the Indonesia customer data platform market, there is an increasing demand for systems that can unify events in real time and support activation across multiple channels without relying on batch updates. Headless commerce setups make the need stronger because they increase the number of data touchpoints while reducing the usefulness of isolated front-end records. Vendors that can connect quickly to leading marketplaces and engagement systems are therefore better placed in the Indonesia customer data platform market than providers that still depend on slower custom integrations.

Rising Demand for Real-Time Personalization in Retail and BFSI

Real-time personalization has become a core operating need in retail and BFSI, where the value of customer data depends heavily on timing and context. Bank Mandiri's Livin' super-app leveraged AI-led pre-login personalization across a broad feature set, demonstrating how local institutions are using unified data to support more relevant engagement.[2]The Digital Banker, “Banking on Experience, How Bank Mandiri Is Redefining Customer Satisfaction Across Segments,” The Digital Banker, thedigitalbanker.com Jenius also used a locally hosted customer engagement platform for 6 million app customers, in line with Indonesian regulatory expectations, highlighting how personalization and compliance are now closely linked.[3]MoEngage, “Jenius Chooses MoEngage to Improve Automation and Customer Engagement,” MoEngage, moengage.com For the Indonesia customer data platform market, this means buyers increasingly expect fast response times, local data handling, and consistent profile access across service and campaign workflows. As that expectation spreads, the Indonesia customer data platform market is gaining support from both revenue priorities and operating requirements in high-value customer-facing sectors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Data Silos and Mainframe Dependencies | -4.2% | National, highest severity in state-owned enterprises and traditional banking institutions | Long term (≥ 4 years) |

| High Total Cost of Ownership for Enterprise-Grade CDP Implementations | -3.6% | Indonesia-wide, disproportionate impact on mid-market enterprises outside Jakarta | Medium term (2-4 years) |

| Shortage of Reverse-ETL and Customer Identity Expertise | -2.8% | National, particularly acute in Tier-2 cities and non-financial verticals | Medium term (2-4 years) |

| Privacy Compliance Complexity Across Multi-Jurisdiction Deployments | -2.4% | APAC core, with spillover to Indonesian multinationals operating cross-border | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Legacy Data Silos and Mainframe Dependencies Delaying Integration

Legacy environments are slowing adoption because many companies still store customer data in separate operational systems that were not built for real-time sharing. In the Indonesia customer data platform market, this raises implementation risk because identity resolution only works well when data can move reliably across core systems, engagement tools, and reporting layers. The issue is especially evident in large institutions where duplicate records, inconsistent formats, and outdated integration methods can extend deployment timelines well beyond original plans. That delay has a direct commercial cost because companies cannot improve targeting, analytics, or orchestration until the underlying data problems are addressed. As a result, the Indonesia customer data platform market is growing quickly, but actual rollout speed still depends on how much legacy cleanup buyers need before a CDP can deliver value.

High Total Cost of Ownership For Enterprise-Grade CDP Implementations

The full cost of a CDP often exceeds the software fee, as buyers also need integration work, governance design, engineering support, and long-term maintenance. In the Indonesia customer data platform market, the cost burden is one reason adoption is more straightforward for large enterprises than for smaller firms with limited technical teams. Even buyers who prefer composable or warehouse-native models can still face meaningful staffing needs, which shifts the cost from licenses to specialist data work rather than removing it. Platform migration can add another layer of expense, since moving identity logic, journeys, and data pipelines from one system to another is rarely simple. This means the Indonesia customer data platform market still has a meaningful affordability gap, even when demand for better customer data capabilities is already in place.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Leads While Services-Driven Deployment Accelerates

Software accounted for 66.81% of the market in 2025, while services are projected to grow at a 39.24% CAGR through 2031. That split shows that license revenue still anchors the category, but deployment work is becoming more valuable as more buyers move from evaluation into execution. In the Indonesia customer data platform market, software remains central because companies still need a core system for unification, governance, segmentation, and activation. Large suite vendors benefit here because long contracts and broad product portfolios help them retain enterprise accounts once the platform is embedded. The installed base effect also supports software leadership, as replacing a CDP usually requires a much broader rebuild across workflows and data pipelines.

Services are expanding faster because implementation complexity is rising as use cases become more advanced and more cross-functional. Buyers are no longer choosing platforms solely for segmentation; they also want consent management, orchestration, analytics, and AI-readiness within a single operating model. That raises the value of local delivery support, partner ecosystems, and migration expertise inside the Indonesia customer data platform industry. Vendors that can package advisory, integration, and ongoing optimization are likely to defend accounts better than those that compete on features alone. This is why the services side of the Indonesia customer data platform market is growing faster even though software still captures the larger revenue base.

By Deployment Mode: Hybrid Architectures Rise On Sovereign Data Dynamics

Cloud held 74.19% of the market in 2025, while hybrid is projected to grow at a 42.48% CAGR through 2031. The cloud lead reflects the appeal of faster setup, lower infrastructure burden, and easier access to updates across campaign and analytics teams. At the same time, the hybrid pattern shows that many buyers are trying to combine cloud flexibility with local processing or storage requirements where regulation or internal policy demands it. In the Indonesia customer data platform market, this balance is especially important for banks, public institutions, and other sectors with stronger data control expectations. Hybrid setups also help companies keep sensitive customer records within a defined infrastructure perimeter while still using modern activation and testing tools.

The growth of hybrid models suggests that deployment decisions are no longer just technical; they are now tied to governance and procurement choices as well. Zero-copy and warehouse-native approaches fit this direction because they reduce unnecessary data movement and can simplify audits when companies already rely on established cloud warehouses. On-premises remains the smallest mode, but it still matters for organizations that cannot rely on a cloud-only model for customer data processing. The cloud segment still led with 74.19% of Indonesia customer data platform market share in 2025, yet the fastest change is clearly moving toward mixed environments that can satisfy both usability and control needs. This dynamic shows that the Indonesia customer data platform market is not moving toward one deployment model, but toward a more selective mix based on sector needs.

By Organization Size: SME Adoption Accelerates On Warehouse-Native Tooling

Large enterprises accounted for 60.74% of the market share in 2025, while small and medium enterprises are projected to expand at a 40.81% CAGR through 2031. Large companies led because they usually had the budgets, data volumes, and internal teams needed to manage identity resolution across many brands and channels. They also had stronger reasons to invest early because fragmented customer records create bigger operating costs at enterprise scale. In the Indonesia customer data platform market, these factors kept large enterprises ahead in current revenue even as the buyer base began to broaden. Their lead also reflects the fact that many enterprise contracts are multi-year, which makes revenue more stable once a platform is selected.

SME growth is faster because newer tools are lowering some of the historical barriers to entry, especially for companies that already use modern cloud data environments. Warehouse-native activation models have made it easier for smaller firms to work with customer data without maintaining a separate, expensive, and proprietary stack. That matters in the Indonesia customer data platform market because the long-term expansion opportunity is much wider outside the current large-enterprise base. Compliance pressure is also relevant, as companies with significant digital customer activity still need workable consent and preference controls, regardless of size. As adoption spreads, vendors with self-serve onboarding, clearer pricing, and lighter deployment requirements are likely to capture a larger share of this fast-growing segment of the Indonesia customer data platform market.

By Application: Customer Analytics And Insights Pulls Ahead As The AI Feeding Layer

Audience segmentation and personalization held 26.31% share in 2025, while customer analytics and insights is projected to grow at a 43.62% CAGR through 2031. The current lead for segmentation shows that many buyers still value the direct commercial use of grouped audiences and targeted engagement. The faster growth in analytics suggests that companies increasingly want the CDP to do more than store and route data. In the Indonesia customer data platform market, that shift reflects a broader move toward predictive use cases, decision support, and AI-driven customer interaction. The change also means the platform is becoming more central to how companies interpret customer behavior rather than just how they activate it.

Profile unification still matters because it supports every downstream application, from campaign design to consent management to service personalization. Marketing campaign and journey orchestration remain important because teams need a practical way to turn customer signals into actions across channels and moments. Consent and preference management are also becoming increasingly important as companies need clearer records of how personal data is used and changes over time. Customer analytics and insights represented the fastest-growing segment of the Indonesia customer data platform market, with a 43.62% CAGR through 2031, indicating where future platform value is moving. This pattern suggests the Indonesia customer data platform market is evolving from a segmentation toolset into a wider intelligence layer for customer decision-making.

Geography Analysis

Indonesia represented the full geographic scope of this study, and the Indonesia customer data platform market size was valued at USD 60 million in 2025 and is estimated at USD 90 million in 2026. The forecast to USD 430 million by 2031 at a 36.72% CAGR shows that Indonesia remains one of the higher-growth customer data platform opportunities in the region. The size of the opportunity stems from a combination of digital commerce breadth, growing AI adoption, and rising pressure to manage customer data more governably. The Indonesia customer data platform market is also shaped by the country's wide mix of digital channels, which makes customer identity fragmentation harder to solve with basic CRM or campaign tools alone. This is why the market is developing around platforms that can unify data, support activation, and meet local control requirements simultaneously.

Regulation is a major geographic factor because it affects where data can be stored, how it can be processed, and what buyers expect from vendors during procurement. That is especially important in sectors such as banking and healthcare, where local data handling expectations are more stringent and can influence platform architecture decisions. The Indonesia customer data platform market is therefore not just a software opportunity, since it also depends on local infrastructure readiness, delivery support, and trust in compliance execution. Buyers increasingly prefer vendors that can show local or in-country operating capability rather than only regional coverage from outside Indonesia. This is one reason hybrid models, local cloud presence, and controlled data movement are becoming more relevant across the Indonesia customer data platform market.

The internal distribution of demand is still uneven because enterprise procurement remains concentrated in major urban centers such as Jakarta and Surabaya. Large organizations in those cities tend to move earlier because they have stronger budgets, broader data estates, and greater pressure to coordinate across brands or business units. At the same time, the long-term expansion path for the Indonesia customer data platform market is likely to extend beyond those hubs as SMEs improve their data environments and digital operating maturity. That broadening will favor vendors with simpler onboarding, Indonesian-language support, and deployment models that do not assume large in-house engineering teams. Geography within the country, therefore, matters less as a limit on customer need and more as a measure of where organizational readiness is strongest today.

Competitive Landscape

The Indonesia customer data platform market remained fragmented in 2026, with global platform suites, composable specialists, and local martech providers competing across different buyer needs. No single vendor dominated all enterprise, mid-market, and regulated-sector use cases, which kept the field open across both software breadth and implementation quality. In practical terms, competition centered on who could combine unification, activation, governance, and AI support in the most usable way for Indonesian buyers. The Indonesia customer data platform market also showed clear tiering, with large-suite vendors competing on breadth, specialists on simplicity, and local players on fit with domestic channels and operational requirements. This structure is keeping innovation active while also making it harder for mid-tier vendors to stand out without a sharper product or delivery angle.

Salesforce made one of the clearest strategic moves when it signed a definitive agreement in May 2025 to acquire Informatica for approximately USD 8 billion in equity value.[4]Salesforce, “Salesforce Signs Definitive Agreement to Acquire Informatica,” Salesforce, salesforce.com That move matters for the Indonesia customer data platform market because master data management, data quality, and AI-readiness are closely tied to enterprise CDP performance. Adobe also expanded its agentic AI ecosystem in June 2026 through new agency and technology partnerships built on Adobe Experience Platform and Real-Time CDP governance controls. Treasure Data's rebrand to Treasure AI in April 2026 showed another strategic direction, where the CDP becomes the governed operating layer for AI-led marketing execution rather than only a profile store. These moves show that the Indonesia customer data platform market is now being shaped as much by AI execution strategy as by traditional data unification features.

Another notable move came in August 2025, when Bank Negara Indonesia expanded its partnership with Cloudera to scale AI-powered business transformation using NVIDIA-supported infrastructure. That example matters because enterprise demand in Indonesia increasingly links customer data platforms with a wider data and AI operating stack rather than treating the CDP as a stand-alone purchase. The Indonesia customer data platform market is therefore favoring vendors that can integrate governance, activation, warehouse access, and AI workflows into a single practical environment. At the same time, buyers in regulated sectors still care deeply about local control, implementation support, and proof that the platform can fit existing systems without excessive disruption. Competitive advantage in the Indonesia customer data platform market now depends less on one feature and more on how well each vendor can align architecture, compliance, and AI enablement for Indonesian customer-facing enterprises.

Indonesia Customer Data Platform Industry Leaders

Salesforce, Inc.

Adobe Inc.

Oracle Corporation

Segment.io, Inc.

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Adobe announced an expansion of its agentic AI ecosystem through new agency and technology partnerships built on Adobe Experience Platform and Real-Time CDP governance controls. The initiative deepens Adobe's competitive position in enterprise AI orchestration across APAC markets and broadens interoperability with third-party AI agents operating on Anthropic, Google, and AWS infrastructure.

- February 2026: Treasure Data announced the general availability of Treasure Code, an AI-native command-line interface enabling technical teams and AI agents to operate the full CDP platform as code, bringing DevOps discipline to CDP operations and reducing overhead for data engineering teams managing complex identity and segmentation workflows.

- January 2026: Treasure Data launched Marketing Super Agent, a multi-agent AI marketing system built into its AI Marketing Cloud. The product handles audience intelligence, strategy, creative, activation, and real-time optimization in a single governed workspace, targeting a reduction in manual campaign management overhead for enterprise marketing teams.

- August 2025: Bank Negara Indonesia strengthened its partnership with Cloudera to scale AI-powered business transformation, with full deployment of the new platform expected by end-2025 using NVIDIA technology for performance-optimized AI workloads. The partnership signals growing demand for CDP-adjacent data platform infrastructure within Indonesia's state-owned banking sector.

Indonesia Customer Data Platform Market Report Scope

The Indonesia customer data platform market refers to the ecosystem of software and associated services that enable organizations in Indonesia to collect, unify, and manage customer data from multiple touchpoints into a single, persistent database. These platforms are designed to break down data silos, creating comprehensive customer profiles that can be leveraged for advanced audience segmentation, personalized marketing campaigns, customer journey orchestration, and predictive analytics. The market encompasses cloud, on-premises, and hybrid deployment models tailored to the operational needs of large and small and medium enterprises across sectors such as retail, BFSI, healthcare, and IT. By integrating consent and preference management capabilities, CDPs help Indonesian businesses comply with evolving local data protection regulations while enhancing customer experience, driving brand loyalty, and improving overall marketing return on investment.

The Indonesia Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), and End-User Industry (Retail and E-Commerce, BFSI, Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the 2026 size of the Indonesia customer data platform space?

It is valued at USD 85.83 million in 2026 and is forecast to reach USD 428.73 million by 2031, at a 37.95% CAGR.

What is driving adoption in Indonesia?

The main drivers are first-party data needs, AI-led customer engagement, omnichannel commerce complexity, and stronger privacy and data control expectations.

Which offering type leads current revenue?

Software led with 66.81% share in 2025, while services is expanding faster at a 39.24% CAGR through 2031.

Which deployment model is growing the fastest?

Hybrid is projected to record the fastest CAGR at 42.48% through 2031, even though cloud held the largest 74.19% share in 2025.

Which application area is expanding the quickest?

Customer analytics and insights is projected to grow at a 43.62% CAGR through 2031, ahead of other application groups.

Which end-user segment is largest and which is fastest growing?

Retail and e-commerce held the largest 28.83% share in 2025, while media and entertainment is expected to grow fastest at a 41.19% CAGR through 2031.

Page last updated on: