India Turning Machine and Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

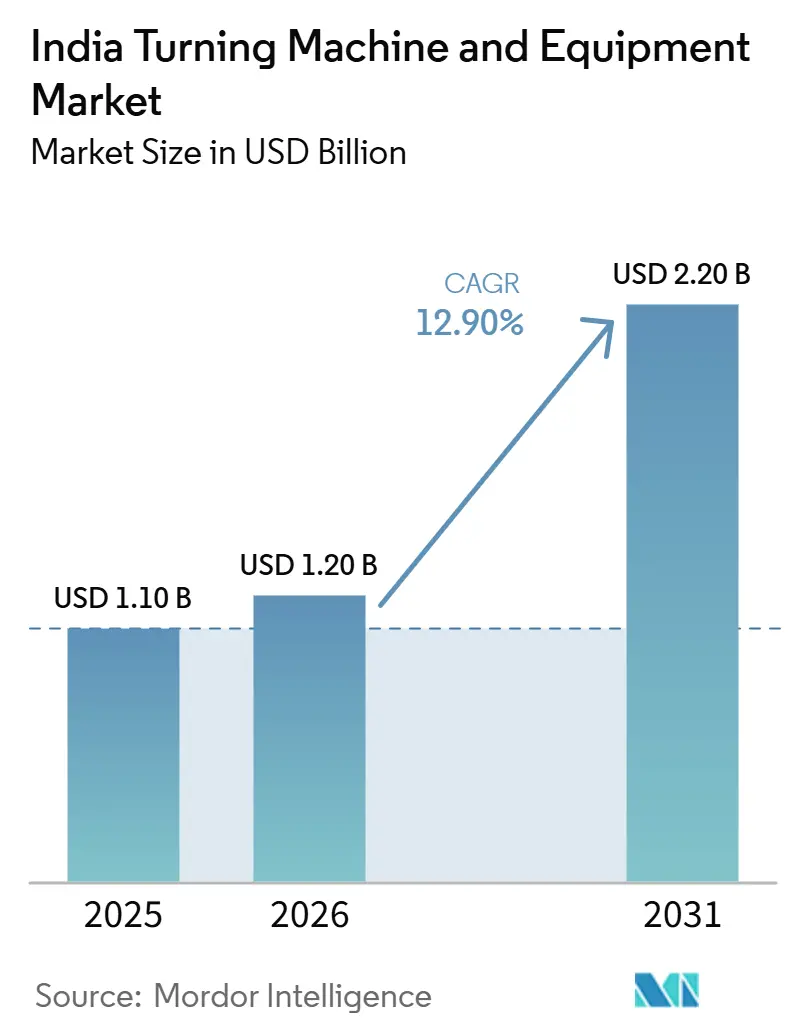

| Base Year Market Size (2025) | USD 1.10 Billion |

| Market Size (2026) | USD 1.20 Billion |

| Market Size (2031) | USD 2.20 Billion |

| Growth Rate (2026 - 2031) | 12.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Turning Machine and Equipment Market Analysis by Mordor Intelligence

The India Turning Machine and Equipment Market size is expected to grow from USD 1.10 billion in 2025 to USD 1.20 billion in 2026 and is forecast to reach USD 2.20 billion by 2031 at 12.90% CAGR over 2026-2031.

The market is being supported by steady demand for precision turned parts used in powertrain, suspension, steering, and other critical assemblies, as India’s auto component turnover reached USD 80.2 billion in FY2025 and exports climbed to USD 22.9 billion. Export-oriented machining investments are also supporting the market, as engineering goods exports rose to a record USD 116.7 billion in FY2025, encouraging domestic capacity expansion instead of overseas sourcing for precision fabrication. Policy support has strengthened this backdrop, as the capital goods PLI program sanctioned 29 projects with government support of INR 7.15 billion (USD 85 million), improving the case for local machine building and lowering import dependence over time. Demand is no longer confined to large automotive belts, as smaller machining clusters are also moving toward CNC adoption through skilling support, shared infrastructure initiatives, and technology upgrade programs, broadening the market's demand base. The main pressure points remain buyer affordability and operator availability, as CNC operators, turners, and toolmakers continued to rank among the most acute vacancies in manufacturing during 2025, which may delay commissioning and lower machine utilization even when order pipelines remain healthy.

Key Report Takeaways

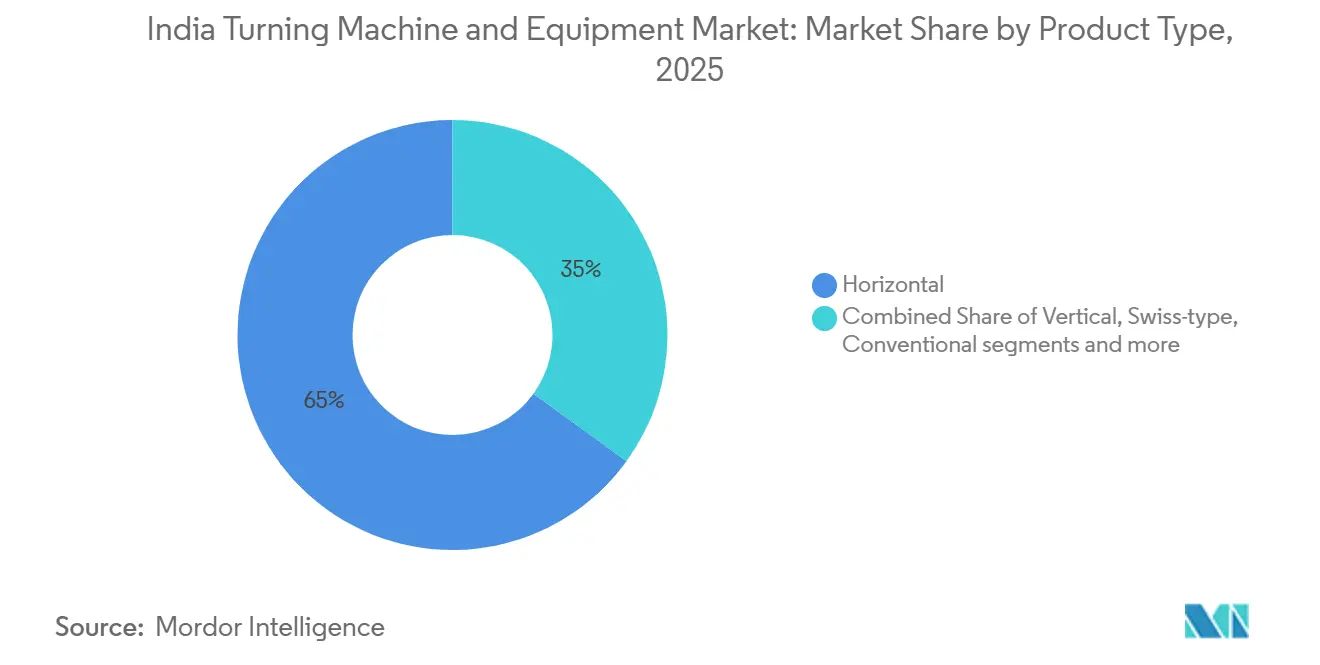

- By product type, the horizontal segment led with 65% revenue share in 2025, while the multi-tasking segment is forecast to expand at a 15.2% CAGR through 2031.

- By automation type, fully automatic CNC accounted for 68% of the India turning machine and equipment market share in 2025 and also recorded the highest projected CAGR at 14.8% through 2031.

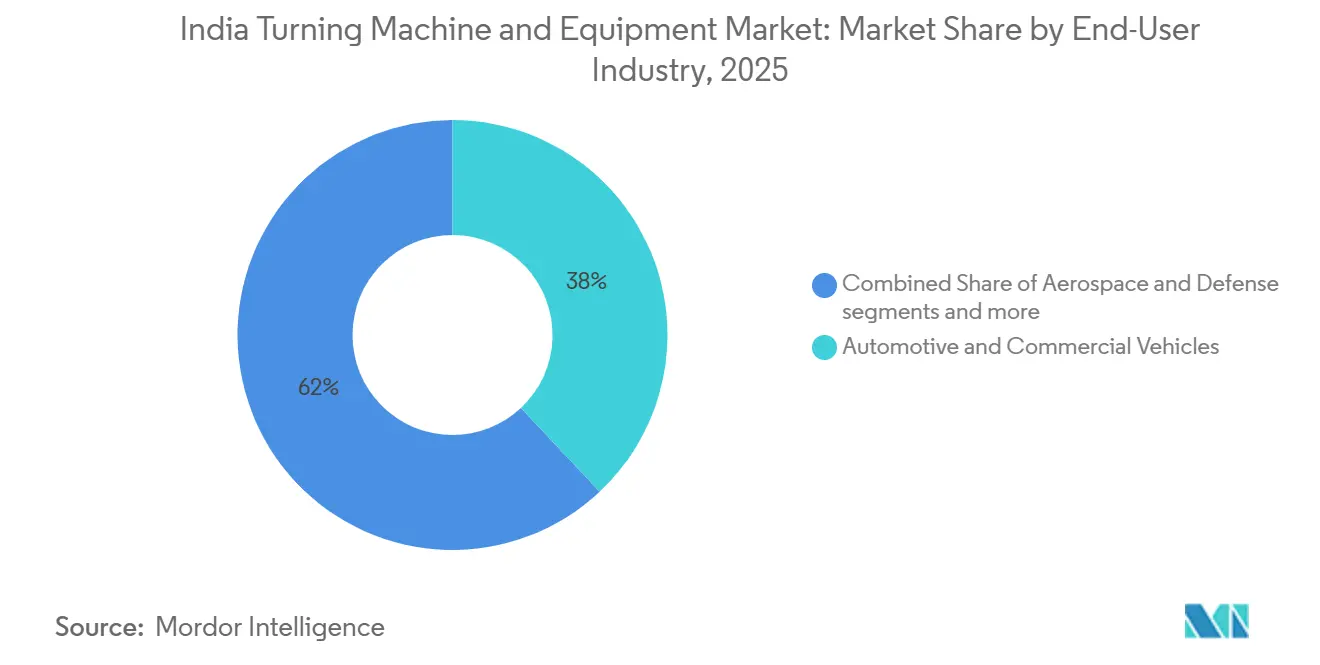

- By end-user industry, automotive and commercial vehicles accounted for 38% share of the India turning machine and equipment market size in 2025, while aerospace and defense are advancing at an 15.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Turning Machine and Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of India’s Auto Component Manufacturing Base | +2.8% | Pan-India, with concentration in Maharashtra, Tamil Nadu, and Gujarat | Medium term (2-4 years) |

| Rapid CNC Penetration Across India’s MSME Machining Ecosystem | +2.4% | Pan-India, with early adoption in Pune-Chakan, Coimbatore, Rajkot, Ludhiana, and Bengaluru clusters | Short term (≤ 2 years) |

| Localization of High-Precision Manufacturing Under Import Substitution Initiatives | +2.2% | National, with greenfield investments in Karnataka, Tamil Nadu, and Uttarakhand | Medium term (2-4 years) |

| Emergence of India as an Alternative Global Manufacturing Hub | +2.0% | Export-oriented zones in Bengaluru, Hyderabad, and Chennai | Long term (≥ 4 years) |

| Growth of Engineering Goods Exports Driving Investments in Precision Machining | +1.6% | Western and Southern India, especially Maharashtra and Tamil Nadu | Medium term (2-4 years) |

| Growth in Railway and Metro Rolling Stock Manufacturing | +1.4% | National, with early gains in Chennai, Bengaluru, Raebareli, and Kapurthala | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of India’s Auto Component Manufacturing Base

India’s auto component base has moved well beyond domestic replacement demand and now serves as a broad manufacturing platform for both domestic and export programs. The sector generated USD 80.2 billion in FY2025 and grew by 14% between FY2020 and FY2025, underscoring the need to expand capacity for engine parts, transmission systems, suspension components, and steering components. Export demand has reinforced this pattern, as auto component exports rose 8% to USD 22.9 billion in FY2025, with Asia-bound shipments growing 15.1%. This means Indian suppliers need to sustain tighter process control and more repeatable machining output across large production runs. Smart factory adoption is also raising the role of CNC turning centers from a support asset to a core production asset, as an ACMA and BCG study released in 2025 showed that more than two-thirds of surveyed firms were already at the pilot, scale-up, or fully integrated stage of digital factory implementation. This shift matters because, even as electric vehicle localization changes the mix of combustion-linked parts, it still creates new demand for precision structural and drivetrain components that require comparable or tighter tolerances on the shop floor. H1 FY26 kept that momentum intact, as industry turnover reached INR 3.6 lakh crore (USD 40.0 billion), indicating that the auto-led capex cycle for the India turning machine and equipment market remains active.[1]Automotive Component Manufacturers Association of India, “Industry Performance Review FY 2024-25,” ACMA Press Release, acma.in

Rapid CNC Penetration Across India’s MSME Machining Ecosystem

India’s MSME machining base is steadily shifting from conventional lathes toward CNC platforms as buyer expectations for repeatability, productivity, and contract compliance continue to rise across supplier tiers. This change is being supported by public funding, as the Capital Goods Sector Phase II program carries a total outlay of INR 12.07 billion (USD 134.3 million), including INR 9.75 billion in budgetary support, lowering technology-upgrade barriers for smaller machining units.[2]Press Information Bureau, Government of India, “Government Scales Up PLI Budget to Accelerate Manufacturing,” PIB, pib.gov.in The transition is also being reinforced by ecosystem support, as IMTMA’s 2024-25 annual report highlighted industry efforts, such as the SAHAYOG initiative and discussions on shared testing infrastructure, aimed at improving access to advanced machine tool capabilities in northern clusters. Once an MSME installs its first CNC turning center, the operating model usually changes quickly because customer quality demands, machine utilization expectations, and depreciation cycles begin to favor additional CNC purchases over a return to conventional machine and equipment. That pattern widens the market’s demand base because follow-on machine buying often comes from firms that started with one cautious upgrade and then moved toward a more stable CNC fleet. As a result, adoption is spreading from large organized buyers to smaller machining clusters, where even modest productivity gains can reshape order eligibility and supplier positioning over a few contract cycles.

Localization of High-Precision Manufacturing Under Import Substitution Initiatives

The import substitution policy are changing, where precision machining capability is built, and that shift supports local demand for turning machines, tooling ecosystems, and manufacturing support services. As of 2025, realized investments under the PLI framework reached INR 1.76 lakh crore (USD 21 billion) across 806 approved applications, which shows that the policy push has already translated into physical manufacturing commitments rather than remaining a planning exercise. The policy signal became even stronger in automobiles and auto components, as the FY26 PLI allocation rose from INR 346.9 crore (USD 41 million) to INR 2,818.9 crore (USD 335 million), supporting higher domestic content and deeper local precision manufacturing capabilities. Industrial sites such as the Tumakuru Machine Tools Park also matter because integrated foundry, fabrication, and assembly capability can reduce lead times for machine builders and improve supply discipline across critical components. Local content rules in defense and railway procurement add another layer of support by pushing contractors toward certified domestic machining capacity, thereby creating demand for turning machines and equipment through compliance requirements as much as through end-market growth. Greenfield investments in states such as Karnataka and Tamil Nadu, therefore, support India's turning machine and equipment market not only by adding factories, but also by deepening the domestic precision manufacturing chain that those factories need to run effectively.[3]Ministry of Commerce and Industry, Government of India, “Engineering Goods Exports Hit Record High in FY25 Despite Global Challenges,” IndBiz, indbiz.gov.in

Emergence of India as an Alternative Global Manufacturing Hub

Global supply chain diversification has raised India’s role in aerospace, defense, and advanced engineering manufacturing, pushing machine specifications upward across parts of the India turning machine and equipment market. Boeing now sources more than USD 1 billion in components annually from India. At the same time, Airbus has committed to sourcing USD 2 billion annually by 2030, which reflects a much deeper integration of Indian suppliers into global aerospace programs. India’s defense exports reached INR 23,622 crore (USD 2.76 billion) in FY2025, and export authorizations rose 16.9% to 1,762, indicating that complex industrial demand is now coming from programs with long approval cycles and stringent quality controls rather than solely from private capex trends. These programs usually require turning of titanium, Inconel, and high-strength aluminum alloys, so buyers are moving toward machines with greater rigidity, thermal stability, and multi-axis capability than standard industrial lathes can provide. The effect spreads downstream because certification systems such as AS 9100D and other customer audits push even sub-tier machining firms toward higher-precision equipment if they want to remain on approved supplier lists. That quality migration expands the premium end of the India turning machine and equipment market and raises the value mix, even as unit growth remains more moderate than broader installed-base expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Sensitivity Among MSME Manufacturers | -1.8% | Pan-India, with the greatest pressure in Rajkot, Ludhiana, Coimbatore, and Faridabad | Medium term (2-4 years) |

| Shortage of Skilled CNC Programmers and Machinists | -1.5% | Pan-India, with strong pressure in southern precision hubs and northern MSME belts | Medium term (2-4 years) |

| Dependence on Imported CNC Controls and High-Precision Components | -1.2% | National, with major exposure in Karnataka, Maharashtra, and Tamil Nadu, supplier parks | Long term (≥ 4 years) |

| Intense Price Competition from Imported Asian Machine Tools | -0.9% | National, especially where the upfront price dominates procurement decisions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost Sensitivity Among MSME Manufacturers

Capital cost remains the biggest filter in buying behavior for many smaller workshops, even when productivity gains from CNC adoption are clear on paper. This matters because the India turning machine and equipment market depends heavily on MSME buyers by unit count, and many of those firms make purchase decisions based on cash flow visibility, financing access, and near-term order certainty rather than lifetime machine economics. Government support programs exist to lower that barrier, but their presence also underlines how real the affordability gap remains for sub-tier machining enterprises seeking modern turning capacity. When buyers place more weight on sticker price than on uptime, service response, or tooling life, lower-cost imported options gain traction, and domestic producers find it harder to defend pricing based solely on support quality. The challenge becomes sharper when firms are not confident that they can staff or fully utilize the machine they buy, because weak utilization stretches payback and delays the next replacement cycle. In that sense, affordability pressure is not only a financing issue, because it interacts directly with labor availability, utilization rates, and the willingness of smaller firms to move from conventional setups into full CNC workflows.

Shortage of Skilled CNC Programmers and Machinists

Skill availability remains a practical operating constraint because new machine demand does not automatically translate into effective machine use. The 2025 skills survey from the Ministry of Skill Development and Entrepreneurship identified CNC operators, turners, and toolmakers as among the most acute roles in automotive component manufacturing, confirming that the shortage is evident in production-facing occupations rather than only in broad labor statistics. This gap slows the India turning machine and equipment market because buyers often hesitate to add capacity when they are unsure that trained setters, programmers, and operators will be available to run the machines at planned output levels. The constraint is especially serious in precision clusters where order books are strong, because even a good machine can run below rated capacity when programming depth and setup quality are inconsistent across shifts. That undercuts the productivity story that usually supports second- and third-machine purchases, and it can delay expansion decisions even when end-market demand remains favorable. The result is a slower equipment replacement and scaling cycle, which means that workforce capability becomes a direct commercial variable for machine builders rather than a background issue for end users alone.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Horizontal Machines Dominate, Multi-Tasking Redraws the Value Mix

The horizontal segment accounted for 65% of revenue in 2025, making it the largest product category in the India turning machine and equipment market by a wide margin. Their lead comes from deep use in automotive and general engineering, where crankshafts, axle shafts, flanges, valve bodies, and similar concentric parts still require reliable, high-volume turning performance. This installed-base advantage also reflects buyer familiarity, because many workshops expand first with a proven horizontal format before moving into more specialized configurations. Vertical machines, Swiss-type machines, multi-tasking systems, and conventional turning machines and equipment each serve narrower use cases that depend on workpiece geometry, tolerance requirements, and budget constraints. The conventional segment still has a role in cost-sensitive shops where moderate tolerances and lower batch sizes make full CNC economics less compelling for every operation.

The multi-tasking segment is projected to grow at a 15.2% CAGR through 2031, which makes it the fastest-growing product type in the India turning machine and equipment market. These systems combine turning, milling, and drilling in a single setup, reducing handling steps and improving dimensional consistency for complex parts. That capability is increasingly important in aerospace structures, surgical implants, and other precision jobs where one-clamp processing supports both tolerance control and traceability requirements. Swiss-type turning machines and equipment remain smaller in revenue terms, but they are gaining relevance as medical devices, electronics miniaturization, and export-oriented precision manufacturing expand in India. Over time, this mix shift is likely to push the India turning machine and equipment market toward a higher average selling price, as premium machines capture more value even when unit volumes remain smaller than those of mainstream horizontal platforms. The Indian turning machine and equipment market, therefore, keeps its volume base in horizontal machines, while more specialized categories are changing the revenue mix and the specification benchmark.

By Automation Type: Fully Automatic CNC Anchors, Both Scale and Speed

Fully automatic CNC accounted for 68% of revenue in 2025, making it the leading segment in the India turning machine and equipment market in both installed value and buyer preference. This segment also recorded the fastest projected growth at 14.8% through 2031, which is unusual because it shows that the dominant format is still taking share rather than simply defending an installed base. The preference for full CNC reflects a broader shift in procurement logic, as repeatability, program control, labor productivity, and quality compliance now matter across a wider range of contracts than they did a few years ago. It also aligns with the reality that many customers now want vendors to document dimensions, hold tighter tolerances, and reduce setup inconsistency across repeat orders. As a result, fully automatic CNC has become the default path for firms that want to scale from job work into longer-cycle supplier relationships.

Manual turning machines and equipment remain present in training environments and conventional job shops, but new commercial additions are under pressure as productivity gaps become more visible. Semi-automatic machines still serve a transitional role for buyers that want better cycle discipline without taking on the full programming and process-control demands of a more advanced CNC platform. Even so, the operating case continues to favor full CNC because it supports more stable repeatability, stronger contract compliance, and easier movement into export-oriented or audited production environments. This is why the India turning machine and equipment market is seeing the broadest momentum around machines that combine deep automation with dependable output across multiple shifts. The India turning machine and equipment market size for fully automatic CNC is therefore growing not only because organized manufacturers are buying more, but also because smaller workshops increasingly view full CNC as the safer long-term investment path. The Indian turning machine and equipment market is also being reshaped by this transition, as support services, training needs, controller familiarity, and after-sales expectations become more important as CNC penetration rises.

By End-User Industry: Automotive Drives Volume, Aerospace Sets the Precision Benchmark

Automotive and commercial vehicles accounted for 38% of the India turning machine and equipment market in 2025, keeping the segment firmly in the lead in terms of end-user demand. That leadership is rooted in the number of turned parts used across powertrain, braking, steering, and driveline systems, where machining scale and repeatability directly affect supplier competitiveness. India’s vehicle-linked supplier base also has a strong export orientation, which further strengthens the case for machines that can maintain repeatable tolerances across long production runs and withstand customer audits. Auto component exports reached USD 22.9 billion in FY2025, with major categories including drive transmission and steering parts, both of which are highly turning-intensive families. General industrial machinery, oil and gas and energy, medical devices, and electrical and electronics applications add meaningful demand diversity, but none match automotive on overall scale.

Aerospace and defense is forecast to grow at a 15.5% CAGR through 2031, which makes it the fastest-growing end-user segment in the India turning machine and equipment market. Defense exports rose to INR 23,622 crore (USD 2.76 billion) in FY2025, while broader aerospace sourcing commitments from global OEMs continue to deepen India’s role in high-precision manufacturing chains. These applications require machines that can handle titanium, Inconel, and high-strength aluminum with stronger rigidity, thermal control, and spindle performance than typical automotive setups. Medical devices and surgical instruments remain smaller in absolute market size but continue to support steady demand for Swiss-type and multi-axis turning because implants, dental parts, and minimally invasive tools require fine dimensional control. Compliance frameworks such as AS 9100D and ISO 13485 further reinforce CNC-led buying, as traceability and process repeatability are built into supplier qualification requirements. The India turning machine and equipment market share is therefore likely to stay volume-led by automotive. At the same time, value-led growth increasingly comes from aerospace, defense, and medical applications with stricter tolerance requirements.

Geography Analysis

Maharashtra, Tamil Nadu, and Karnataka remain the core demand states for the India turning machine and equipment market because they combine large OEM bases, dense supplier networks, and strong export exposure. Maharashtra contributed USD 19.2 billion in engineering exports in April-October 2025-26, accounting for a 28% share of the national total, making it the largest export-linked machining state in the current cycle. The Pune, Chakan, and Aurangabad belt provides the state with a strong base in automotive and general engineering. Hence, buyers there often prioritize mid- to high-specification CNC platforms that can support both scale and export-grade quality. Tamil Nadu contributed 20% of national engineering exports, or USD 13.6 billion in April-October 2025-26, and its Chennai and Coimbatore zones remain important demand centers for horizontal and swiss-type turning machines and equipment. This regional structure gives the India turning machine and equipment market a strong western and southern foundation, where automotive, pump, compressor, and precision engineering activities continue to sustain demand for machine replacement and expansion.

Karnataka is emerging as the fastest-growing major engineering export state, with export value up 40% year over year to USD 3.9 billion in April-October 2025-26. Bengaluru has a heavier concentration of aerospace, defense, and precision electronics work than most Indian clusters, which pushes local demand toward multi-tasking and higher-precision CNC turning systems. Gujarat also remains significant with USD 10 billion in engineering exports and 14% growth in the same period, while northern belts such as Ludhiana, Faridabad, and Ghaziabad are becoming stronger secondary markets as MSME CNC adoption broadens. Demand across these regions is therefore shaped by two parallel trends.

Eastern India remains less penetrated, but it is no longer peripheral to the India turning machine and equipment market. The eastern region accounted for 8.8% of the national engineering export value in April-November 2025-26, which is still modest compared with western and southern India. Still, it signals an industrial base becoming more relevant to machine demand. Engineering activity in and around Kolkata, Odisha, and Jharkhand is supported by steel, heavy engineering, mining equipment, and energy-linked fabrication, which favor horizontal and vertical turning applications. Fresh demand is also being supported by railway and power sector activity, which adds a layer of machine demand that is less exposed to the automotive cycle than the western and southern clusters. This creates room for the India turning machine and equipment market to expand geographically over the next few years, even if the highest-value demand remains concentrated in the west and south.

Competitive Landscape

The India turning machine and equipment market remains moderately fragmented, with domestic companies strongest in volume-oriented, cost-sensitive segments, while Japanese, Korean, German, and other global OEMs are stronger in premium precision applications. Domestic participants such as Ace Micromatic Group, Jyoti CNC Automation, Lakshmi Machine Works, Lokesh Machines, and Batliboi compete through local engineering familiarity, service reach, and price-performance positioning suited to MSME and mid-tier buyers. Global suppliers such as DMG MORI, Mazak, Okuma, DN Solutions, Hyundai WIA, and INDEX-Werke are better placed in aerospace, defense, and advanced multi-tasking programs where controller depth, spindle performance, and thermal stability matter more than entry price alone. This split means no single company controls the full India turning machine and equipment market, because customer priorities differ sharply by product mix, tolerance requirement, and buyer budget. It also means that competitive advantage often depends on how well a supplier matches machine specification with service capability, training support, and response time rather than on machine price alone.

Recent company actions show that competition is moving beyond simple pricing. Jyoti CNC stated in May 2026 that its capacity expansion from 6,000 to 16,000 machines annually was progressing on schedule, with the new facility expected to begin commercial operations by September 2026, which shows confidence in sustained demand and a push for scale. The same company also highlighted its HUMA operator panel design patent registration in January 2025, indicating growing domestic investment in operator interfaces and machine differentiation rather than a narrow focus on price competition alone. Lakshmi Machine Works used DMTX 2025 to showcase its S Turn, LR, LL, and LTV compact CNC turning lines, reflecting a clear effort to address the MSME precision machining segment, where volume growth potential remains strong. These moves show that suppliers are competing through capacity, product range, usability, and depth of localization rather than relying on a single lever.

A key structural gap persists in core subsystems, as domestic differentiation remains weaker in controllers, servo systems, and certain high-precision components than in machine assembly and service execution. That keeps the India turning machine and equipment market dependent on external technology even as local manufacturing capability improves. It also preserves room for global brands in premium contracts, especially where buyers want proven controller ecosystems, higher-end automation integration, and tighter process assurances from the first installation. At the same time, domestic firms retain a strong position, where local support, commercial flexibility, and familiarity with Indian shop-floor conditions outweigh the need for the most advanced specification. The competitive balance in the India turning machine and equipment market is therefore likely to remain mixed, with domestic firms broadening their reach in core CNC categories. At the same time, global players hold stronger positions in high-precision and multi-tasking niches.

India Turning Machine and Equipment Industry Leaders

Ace Micromatic Group

Jyoti CNC Automation Limited

Lakshmi Machine Works Limited

Lokesh Machines Limited

Batliboi Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Ace Designers (Ace Micromatic Group) invested approximately INR 50 crore (USD ~5.6 million) to establish a new CNC machine assembly facility in Ahmedabad, Gujarat. The plant is designed to achieve an annual production capacity of approximately 3,000 turning machines and 1,000 machining centers within five years, strengthening domestic turning equipment manufacturing and localization of component supply chains.

- January 2026: Jyoti CNC Automation announced an investment plan exceeding INR 10,000 crore (USD ~1.1 billion) over five years to expand manufacturing capacity, R&D capabilities, and advanced CNC technologies for aerospace, defense, electronics, and semiconductor applications, increasing India's competitiveness in high-precision turning and multi-axis machining solutions.

India Turning Machine and Equipment Market Report Scope

The India Turning Machine and Equipment Market is Segmented by Product Type (Horizontal, Vertical, Swiss-Type, and More), by Automation Type (Manual, Semi-Automatic, and Fully Automatic CNC), and by End-User Industry (Automotive & Commercial Vehicles, Aerospace & Defense, Medical Devices & Surgical Instruments, Oil, Gas, & Energy, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Horizontal |

| Vertical |

| Swiss-Type |

| Multi-Tasking |

| Conventional |

| Manual |

| Semi-Automatic |

| Fully Automatic CNC |

| Automotive & Commercial Vehicles |

| Aerospace & Defense |

| Medical Devices & Surgical Instruments |

| Oil, Gas, & Energy |

| Electrical, Electronics & Semiconductor Equipment |

| General Industrial Machinery |

| Others (Consumer Goods, Defense Ordnance) |

| By Product Type | Horizontal |

| Vertical | |

| Swiss-Type | |

| Multi-Tasking | |

| Conventional | |

| By Automation Type | Manual |

| Semi-Automatic | |

| Fully Automatic CNC | |

| By End-User Industry | Automotive & Commercial Vehicles |

| Aerospace & Defense | |

| Medical Devices & Surgical Instruments | |

| Oil, Gas, & Energy | |

| Electrical, Electronics & Semiconductor Equipment | |

| General Industrial Machinery | |

| Others (Consumer Goods, Defense Ordnance) |

Key Questions Answered in the Report

What is the market size of the India turning machine and equipment market in 2026, and how is it expected to grow by 2031?

The India turning machine and equipment market is projected to reach USD 2.2 billion by 2031, up from USD 1.2 billion in 2026, at a 12.9% CAGR over 2026-2031.

Which product category drives demand for turning machine and equipment in India?

Horizontal segment led with 65% revenue share in 2025 because they remain the standard choice for automotive and general engineering applications.

Which automation format is growing fastest in India?

Fully automatic CNC is both the largest and the fastest-growing automation format, with 68% share in 2025 and a projected 14.8% CAGR through 2031.

Why is aerospace and defense becoming more important for turning machine suppliers in India?

Aerospace and defense is forecast to grow at a 15.5% CAGR through 2031, driven by the need for high-precision machining of advanced materials and strict compliance standards.

Which Indian states are the most important for machine demand?

Maharashtra, Tamil Nadu, and Karnataka remain the main demand centers because they combine automotive, export machining, aerospace, and precision engineering activity.

What is the biggest constraint on CNC turning adoption among smaller Indian workshops?

Cost sensitivity and skill shortages are the main constraints, because many MSMEs still face financing pressure and shortages of CNC operators, turners, and toolmakers.

Page last updated on: