India Turning Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

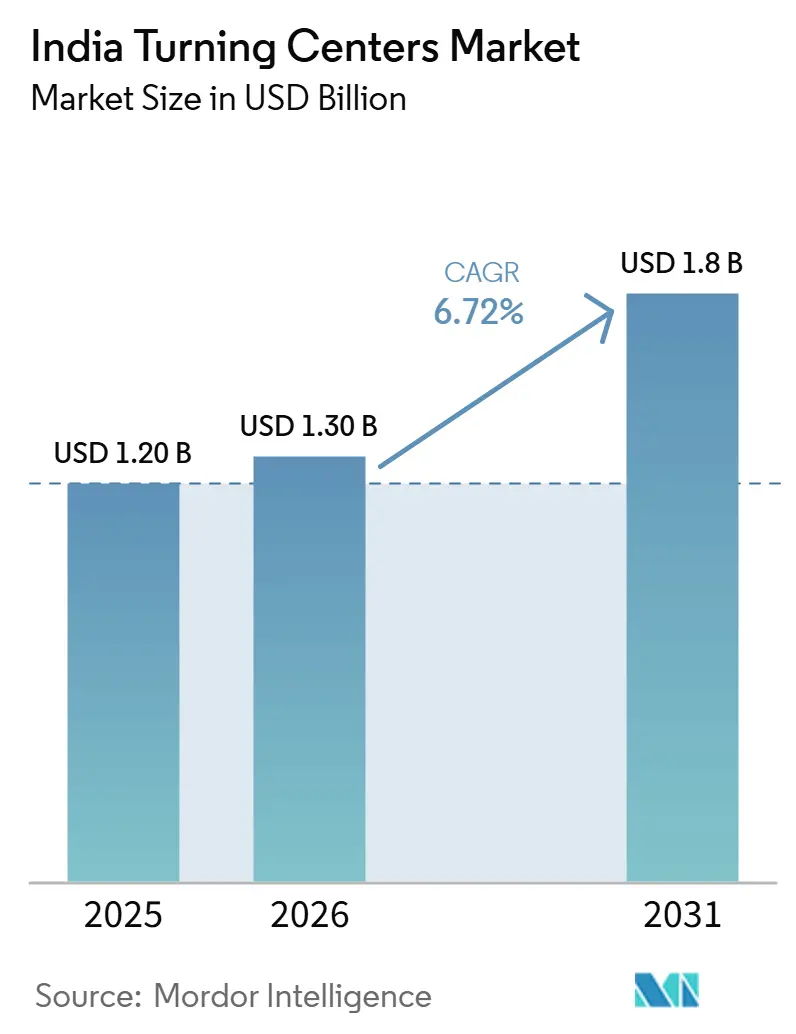

| Base Year Market Size (2025) | USD 1.20 Billion |

| Historical Data Period | 2020 - 2024 |

| Market Size (2026) | USD 1.30 Billion |

| Market Size (2031) | USD 1.8 Billion |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Turning Centers Market Analysis by Mordor Intelligence

The India Turning Centers Market size was valued at USD 1.20 billion in 2025 and is estimated to grow from USD 1.30 billion in 2026 to reach USD 1.8 billion by 2031, at a CAGR of 6.72% during the forecast period (2026-2031).

India's Production-Linked Incentive scheme, with a total incentive outlay of USD 22.5 billion across 14 sectors, is channeling industrial investment into local manufacturing and supporting multi-year equipment purchases across major user industries. The current expansion cycle is broader than earlier ones because automotive manufacturers are investing in both ICE and EV platforms, defense units are expanding CNC capacity for aerospace parts, and semiconductor facilities are opening a new source of precision equipment demand in India. Demand in the India turning centers market is also spreading across established corridors in Maharashtra, Tamil Nadu, Gujarat, and Karnataka, while semiconductor-linked projects are widening the procurement map into newer locations. Competition in the India turning centers market remains split between domestic suppliers that compete on cost and service reach and international suppliers that hold strength in premium multi-axis systems, which keeps localization and application support at the center of strategy.

Key Report Takeaways

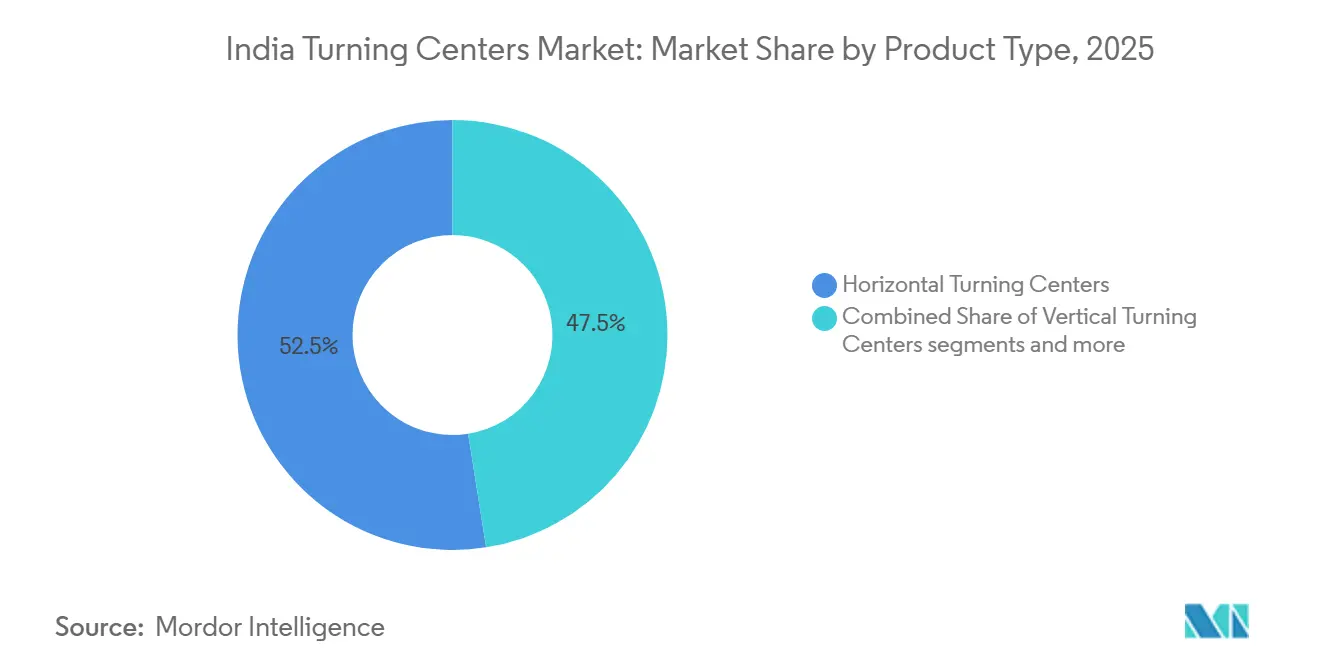

- By product type, horizontal turning centers led with 52.5% of the India turning centers market share in 2025, while vertical turning centers are forecast to expand at 7.8% CAGR through 2031.

- By axis configuration, 3-axis turning centers held 65% share in 2025, while the 4-axis segment is projected to grow at an 8.5% CAGR through 2031.

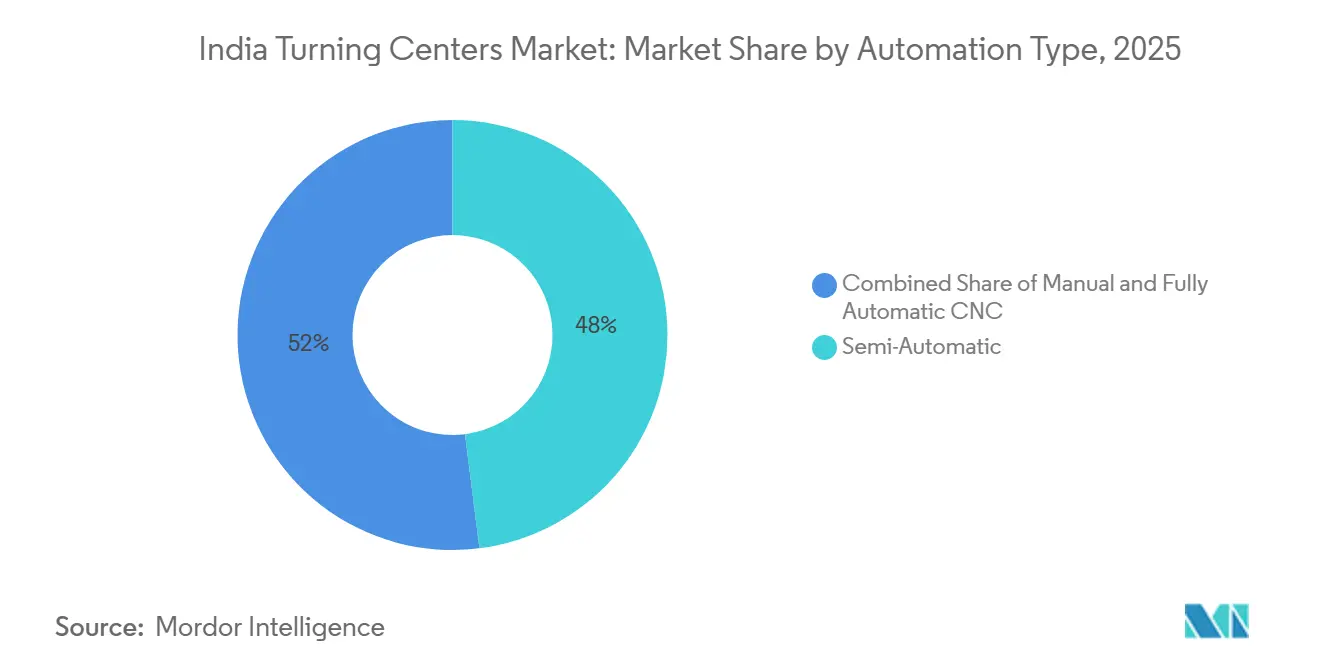

- By automation type, semi-automatic turning centers accounted for 48% of the India turning centers market size in 2025, while fully automatic CNC systems are projected to expand at 9.2% CAGR through 2031.

- By end-user industry, automotive and commercial vehicles accounted for 38.5% of the India turning centers market in 2025, while medical devices and surgical instruments are expected to record the fastest CAGR of 9.8% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Turning Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Production Linked Incentive (PLI) Scheme Across Key Sectors | +1.8% | Pan-India, concentrated in Maharashtra, Gujarat, Tamil Nadu, Karnataka | Medium term (2-4 years) |

| India’s Automotive Sector Driving Turning Center Demand | +1.5% | Pan-India, with high intensity in Pune, Chennai, Gurugram, Bengaluru | Short term (≤ 2 years) |

| MSME Modernization and SAMARTH Udyog Initiative | +1.0% | Pan-India, with early gains in Gujarat, Maharashtra, and Rajasthan clusters | Medium term (2-4 years) |

| Growing Domestic Turning Center OEM Capabilities | +0.8% | Rajkot, Bengaluru, Coimbatore, Ludhiana | Medium term (2-4 years) |

| Semiconductor and Electronics Manufacturing Investments | +0.7% | Gujarat, Karnataka, Uttar Pradesh | Long term (≥ 4 years) |

| HAL (Hindustan Aeronautics Limited) and Defense Aerospace Expansion Under Aatmanirbhar Bharat | +0.6% | Bengaluru, Nashik, Lucknow, Hyderabad | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Production Linked Incentive (PLI) Scheme Across Key Sectors

The PLI scheme remains the strongest policy support for India becoming a manufacturing hub because it ties incentives to manufacturing expansion rather than only to assembly output.[1]Ministry of Heavy Industries, “Machinery and Electrical Equipment Safety Order and Related Industrial Policy References,” heavyindustries.gov.in As of December 2025, 836 applications had been approved under the scheme, cumulative investment had reached USD 25.4 billion, and the linked ecosystem had generated more than 1.44 million direct and indirect jobs. The automotive PLI budget for 2025-26 rose from USD 40.8 million in the revised estimate to USD 332 million, while electronics and IT hardware allocation increased to USD 1.06 billion, which is building deeper equipment demand across both sectors. Companies seeking these incentives must meet domestic value-addition conditions. That requirement is pushing fresh capital spending into machining capacity, component lines, and plant-level automation rather than into imported finished assemblies. This is keeping the India turning centers market tied to a policy-backed manufacturing cycle that is broad, multi-sector, and likely to sustain equipment demand over several years.

India's Automotive Sector Driving Turning Center Demand

India’s automotive and auto components base remains the largest consumption engine for the India turning centers market, with automotive and commercial vehicles accounting for 38.5% of demand in 2025.[2]Automotive Component Manufacturers Association of India, “Industry Performance Review, H1 FY26,” acma.in The Indian auto component industry recorded turnover of USD 41.9 billion in H1 FY26, up 6.8% year on year, confirming continued demand across the supplier network. More than 70% of tier-1 auto component suppliers use CNC technology for precision machining, making the automotive supply chain one of the most stable markets for turning centers in the country. Demand is being reinforced by the parallel investment cycle in ICE and EV production, as manufacturers add separate machining capability for motor housings, battery structural parts, lightweight connectors, crankshafts, and camshafts rather than replacing one platform with another. This is giving the India turning centers market a wider equipment requirement across both traditional and new automotive component categories.

MSME (Micro, Small & Medium Enterprises) Modernization and SAMARTH Udyog Initiative

MSME modernization is broadening the buyer base of the India turning centers market beyond large industrial groups and is bringing smaller manufacturing clusters into structured CNC adoption.[3]Press Information Bureau, “SAMARTH Udyog Bharat 4.0, SAMARTH Centre Activities,” pib.gov.in The Ministry of Heavy Industries established 4 SAMARTH centers at IIT Delhi, C4i4 Lab Pune, CMTI (Central Manufacturing Technology Institute) Bengaluru, and IISc Bengaluru under the Capital Goods Competitiveness Scheme, backed by government funding of USD 115 million. C4i4 Lab Pune also rolled out 10 additional cluster-level Industry 4.0 experience centers, and by 2025, 29 projects with a combined value of USD 105 million had been sanctioned under Phase II. These live demonstration centers reduce adoption risk by allowing MSMEs to test machine layouts, process settings, and digital workflows before committing capital to fully automatic CNC systems. With more than 63 million registered MSMEs in India, even a modest rise in CNC penetration can meaningfully boost demand for entry-level and semi-automatic systems in the India turning centers market.

Growing Domestic Turning Center OEM Capabilities

Domestic manufacturing capability is improving in the India turning centers market, especially in mid-range and multi-axis configurations, where local suppliers were previously weaker. Jyoti CNC Automation is expanding annual capacity from 6,000 machines to 16,000 machines by September 2026, supported by capital expenditure of USD 47-53 million and a new large-format facility under development at Tumakuru Machine Tools Park. LMW reported an order book of USD 306 million as of February 2026, and its machine tool division is giving greater strategic attention to machining and turning centers within its portfolio. ACE Designers launched the 4-axis 2TSL1212 horizontal turning center and the CDL 65 center-drive lathe at IMTEX (Indian Machine Tool Exhibition) 2025, where the event generated USD 412 million in orders and USD 4.4 billion in inquiries, indicating strong purchase intent among OEMs and end users. This rise in local capacity is gradually narrowing the gap between imported and domestic solutions in standard and mid-tier applications across the India turning centers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heavy Import Dependency on Advanced Turning Centers | -1.2% | Pan-India, most acute in 5-axis and multi-tasking configurations | Long term (≥ 4 years) |

| Fragmented Aftermarket and Long OEM Service Response Times Outside Major Cities | -0.9% | Tier-2 and Tier-3 clusters outside Pune, Chennai, Bengaluru, Delhi NCR | Medium term (2-4 years) |

| Shortage of Skilled CNC Operators and Programmers in Manufacturing Clusters | -0.8% | National, acute in Coimbatore, Ludhiana, Rajkot, and Faridabad | Short term (≤ 2 years) |

| Price Sensitivity Limiting Premium Turning Center Adoption in India | -0.7% | MSME-dominated regions, including Rajkot, Ludhiana, Tiruppur, and Bhiwadi | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heavy Import Dependency on Advanced Turning Centers

Import dependence continues to limit the upside of the India turning centers market, especially in premium 5-axis and multi-tasking systems, where domestic capability remains narrower. Machine tool imports rose 23% year on year to USD 2.5 billion in CY2025, and China, Japan, and Germany together accounted for 62% of those imports. Turning centers accounted for 9% of total machine tool imports by type in CY2025, according to the Association for Manufacturing Technology, underscoring the country's continued reliance on overseas supply for several advanced configurations. Buyers also face greater compliance efforts because imported equipment must navigate additional safety and certification requirements under the Machinery and Electrical Equipment Safety Order, which increases due diligence requirements and can lengthen procurement cycles. Until local suppliers move further into premium CNC capability, the India turning centers market will remain exposed to cost shifts, lead-time risk, and supplier concentration in imported systems.

Fragmented Aftermarket and Long OEM Service Response Times Outside Major Cities

Aftermarket coverage remains uneven in the India turning centers market, and that gap is most visible in tier-2 and tier-3 manufacturing clusters, where uptime is critical, but OEM service density is lower. International OEMs such as Yamazaki Mazak, DMG MORI, and Okuma maintain strong technical support in large industrial centers. This weakens the ownership case for premium systems in smaller clusters and opens the door to lower-cost Taiwanese and Chinese offerings backed by faster local dealer support. The IMTMA (Indian Machine Tool Manufacturers' Association) Advanced Machine Tool Testing Facility completed more than 920 technical assignments in FY2024-25, reflecting the scale of calibration and performance issues that still require organized service support across the installed base. When service access is slow, machine utilization falls, and buyers delay upgrades, which restricts the premium end of the India turning centers market, even when demand fundamentals remain healthy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Horizontal Centers Lead, Verticals Gain Precision-Driven Momentum

Horizontal turning centers commanded 52.5% of the India turning centers market share in 2025, which reflects their entrenched role in high-volume automotive and engineering applications that depend on spindle rigidity, stable chip evacuation, and repeatable cycle times. These machines remain the default choice for crankshafts, cylinder liners, and transmission shafts because those parts require throughput and dimensional consistency more than flexible multi-process layouts. This base keeps horizontal machines at the center of procurement in large automotive plants and in supplier facilities that serve powertrain and driveline programs. Their installed base also supports repeat orders because manufacturers often expand with machine families that match existing tooling, operator familiarity, and maintenance routines. In the India turning centers market, that replacement and expansion cycle keeps horizontals tied to the broadest part of current demand.

Vertical turning centers are projected to grow at 7.8% CAGR through 2031, driven by applications in wind energy, heavy industrial equipment, and large-diameter aerospace parts where gravity-assisted clamping improves workholding stability. Their appeal is increasing where out-of-roundness control, reduced fixturing complexity, and safer handling of larger workpieces matter more than line speed. Multi-tasking turning centers are also advancing in aerospace and defense subcontracting because they combine turning, milling, and drilling in a single setup, reducing setup losses on high-mix programs. LMW’s IMTEX 2025 launches included LR30T L30, LR40TM L25, LTV 30 Plus, and LTV 40 Plus configurations, demonstrating that domestic suppliers are widening their portfolios to capture both vertical and heavy-duty demand. Special-purpose and pipe-turning systems remain niche but steady, serving railways, pressure vessels, and defense fabrication where customization matters more than standard volume.

By Axis Configuration: 3-Axis Baseline Faces Structural Pressure from Multi-Axis Adoption

3-axis turning centers held a 65% share of the India turning centers market in 2025, supported by their lower cost and wide fit with general engineering and automotive suppliers operating in standard-tolerance environments. This segment remains the baseline across a large installed base because many workshops still prioritize dependable production over complex part consolidation. For pump housings, shafts, flanges, and conventional machined parts, 3-axis systems remain aligned with prevailing volume and budget constraints. The strength of this category also reflects the structure of India’s MSME manufacturing base, where investment decisions still favor faster payback and simpler programming. That keeps 3-axis machines relevant even as the performance mix in the India turning centers market shifts upward.

The 4-axis segment is forecast to expand at a 8.5% CAGR through 2031, making it the fastest-growing axis class as manufacturers adopt Y-axis capability to reduce setup time for transmission casings, pump bodies, and aerospace brackets. Demand for 5-axis and above remains concentrated in aerospace, defense, and medical device machining, where single-setup accuracy matters and scrap costs are high. Jyoti CNC’s Q4 FY2026 order book showed aerospace and defense accounting for 38% of its USD 553 million pipeline, signaling how strongly premium multi-axis demand influences value even when unit volumes remain smaller. India also reported that 93% of cutting machines produced domestically are now CNC-operated, so axis upgrades are increasingly moving with the wider digitalization trend rather than remaining limited to a few early adopters. Domestic launches such as Jyoti CNC’s BTM 100 twin-spindle turning center and ACE Designers’ 4-axis platform indicate that local OEMs are starting to absorb demand that once moved almost entirely to imports.

By Automation Type: Semi-Automatic Dominates Today; CNC Automation Accelerates Through the Forecast

Semi-automatic turning centers held 48% of the India turning centers market share in 2025, indicating that the installed base still reflects the needs of cost-sensitive MSMEs seeking a balance between productivity and manageable capital outlay. These systems remain useful for job shops and mixed production runs where part volumes cannot always justify full automation. They also fit clusters where operator skill is uneven and where staged migration toward advanced CNC remains the safer route for owners. Manual turning centers are losing relevance and are now largely limited to small-batch work and training settings. This makes the semi-automatic category the present-day bridge between legacy machining practice and the more automated future of the India turning centers market.

Fully automatic CNC systems are projected to grow at 9.2% CAGR through 2031, supported by labor cost pressure, export-quality requirements, and the demonstration effect created by the SAMARTH network. Adoption is moving fastest where consistent tolerances, higher throughput, and lower operator dependence matter most, especially in electronics and semiconductor-adjacent manufacturing. Jyoti CNC’s FY2026 order book showed that electronics manufacturing services customers accounted for 20% of total orders, underscoring the link between precision, scale, and higher automation intensity. LMW also pointed to rising demand for automation-integrated turning and machining platforms from electronics and precision engineering clients in its Q3 FY26 communication, indicating that automation is becoming a broader portfolio priority rather than a niche requirement. As more MSMEs gain exposure through live Industry 4.0 centers, purchase hesitation is easing, and the automation mix within the India turning centers market is moving steadily upward.

By End-User Industry: Automotive Anchors Demand; Medical Devices Drive the Premium Growth Tier

Automotive and commercial vehicles accounted for 38.5% of end-user demand in 2025, making the segment the primary volume anchor for the India turning centers market. This position sits within a large supplier ecosystem spanning engines, drivetrains, structural parts, braking components, and export-oriented precision parts. The sector’s demand is not limited to legacy powertrain programs, as EV platforms are adding separate machining requirements for motor housings, battery structures, and lightweight connectors. Oil, gas, and energy applications continue to provide a steady outlet for large-bore horizontal machines used in pipelines, flanges, and refinery maintenance parts. General industrial machinery also accounts for a significant share of standard turning center demand through hydraulic components, pump bodies, gearbox housings, and precision fittings produced across MSME clusters.

Medical devices and surgical instruments are projected to grow at a 9.8% CAGR through 2031, making them the fastest-growing end-user category as India expands precision production of orthopedic implants, surgical tools, and diagnostic hardware. Aerospace and defense are also becoming more important at the premium end, supported by HAL’s provisional FY2025-26 revenue of USD 3.77 billion and an order book of USD 29.7 billion, including the 97 LCA (Light Combat Aircraft) Mk1A aircraft program valued at USD 7.3 billion. HAL has also commissioned advanced CNC machining facilities for ISRO’s LVM3 rocket propellant tank production. It has been issuing machining subcontract tenders for aircraft components, thereby strengthening demand for high-precision equipment. Semiconductor-linked demand is beginning to add a new layer, as Micron’s ATMP (Assembly, Testing, Marking & Packaging) facility in Sanand started commercial production in February 2026, followed by Kaynes Semicon’s OSAT (Outsourced Semiconductor Assembly & Test) facility in March 2026, both of which require precision-machined housings, fixtures, and support components. The result is a more value-oriented demand mix in the India turning centers market, where higher-spec machines are gaining importance even as total unit growth remains broadly distributed across sectors.

Geography Analysis

The India turning centers market remains concentrated in a small number of high-density industrial corridors, even though the buyer base is now spreading into newer manufacturing zones. Maharashtra stands out as the largest demand center because the Pune-Nashik corridor combines automotive, engineering, and aerospace activities within a single procurement region. Pune supports large tier-1 automotive and engineering plants, while Nashik has gained added relevance following HAL's operationalization of the 3rd Tejas production line and the 2nd HTT-40 line at its Nashik division during FY2025-26. That combination keeps Maharashtra central to both volume-driven and high-spec equipment demand. The state’s mix of automotive scale and aerospace machining needs also gives it a broader machine profile than most other regions.

Tamil Nadu forms the second major cluster in the India turning centers market through the Chennai, Coimbatore, and Hosur belt. This region supports the manufacturing of two-wheelers, commercial vehicles, industrial machinery, and aerospace components, so machine demand is diversified across both serial production and precision programs. The Rolls-Royce and HAL joint venture IAMPL completed a 12-acre expansion of its Hosur aerospace manufacturing hub in 2026 to produce compressor and turbine components, thereby strengthening the local supply chain's high-precision pull. Coimbatore also remains important because it links machine tool supply, component manufacturing, and industrial engineering in one dense ecosystem.

Gujarat is rapidly gaining weight in the India turning centers market because it combines the legacy Rajkot machining cluster with new semiconductor-linked investment in Sanand and Dholera. Rajkot supports a deep network of small- and mid-sized CNC workshops serving pumps, valves, and general engineering, while Jyoti CNC’s base in the state underscores the state's manufacturing importance. Karnataka remains a second major pillar through the Bengaluru-Tumakuru axis, where aerospace, defense, and the SAMARTH centers at IISc and CMTI support both demand and process upgrading. Northern clusters such as Delhi NCR, Faridabad, Ludhiana, and Peethampur-Bhopal form the next tier, and their gradual CNC upgrading is widening the regional footprint of the India turning centers market beyond the traditional core corridors.

Competitive Landscape

The India turning centers market is moderately fragmented, with domestic and international suppliers operating in distinct price-performance bands rather than competing head-to-head across every application. Domestic OEMs such as Jyoti CNC Automation, BFW, LMW, and ACE Designers focus on the mid-range and entry-level segments, where cost of ownership, local-language support, service responsiveness, and price discipline matter most. International suppliers from Japan, Germany, South Korea, and Taiwan remain stronger in premium multi-axis systems, where controller sophistication, higher process integration, and application engineering still shape purchase decisions more than upfront price. This tiered structure keeps the India turning centers market open to both value-led local competition and premium imported technology.

Several company actions show how competition is evolving in the India turning centers market. Jyoti CNC is expanding production capacity from 6,000 to 16,000 machines by September 2026, signaling a deliberate effort to capture more local demand and strengthen scale economics. Its FY2026 order mix also shows a pivot toward aerospace and defense at 38% and EMS at 20%, reducing earlier dependence on automotive demand alone. LMW’s Q3 FY26 commentary pointed to a strategic preference for machining centers over turning centers, which reflects the broader shift toward multi-operation platforms across customer requirements. Jyoti CNC’s HUMA operator interface patent, granted in January 2025, also shows how domestic players are trying to differentiate through easier human-machine interaction rather than competing only on price.

The main gap across the field remains the lack of service depth outside the top industrial cities. International OEMs have stronger controller ecosystems and premium application capabilities, but many do not yet have equally dense field support in tier-2 and tier-3 clusters. Domestic players have greater access to the lower and mid-range, but they still depend heavily on imported controllers and advanced subsystems in several higher-spec models. This leaves room for competition to shift toward lifecycle services, faster diagnostics, predictive maintenance, and improvements in local content rather than only machine pricing. As compliance expectations rise and end users seek fewer stoppages, the India turning centers market is likely to reward suppliers that can pair application support with local service reach and steady component availability.

India Turning Centers Industry Leaders

Jyoti CNC Automation

Bharat Fritz Werner (BFW)

Lakshmi Machine Works (LMW)

ACE Designers Ltd.

Batliboi Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: India’s Cabinet approved 2 new semiconductor projects under ISM (India Semiconductor Mission) 2.0, Crystal Matrix in Dholera, Gujarat, and Suchi Semicon in Surat, Gujarat, with cumulative investment exceeding USD 456 million. These precision-intensive facilities require advanced turning centers for equipment component manufacturing and maintenance, deepening semiconductor-linked machine tool demand in Gujarat.

- March 2026: Kaynes Semicon commenced commercial production at its OSAT facility in Sanand, Gujarat, becoming India’s second operational semiconductor manufacturing unit. Precision-machined components for equipment housings and test fixtures form part of the local precision manufacturing ecosystem supporting the facility.

- February 2026: ISM 2.0, launched by the Government of India, expanded the India Semiconductor Mission’s scope to Equipment and Materials, Design IP, Supply Chains, and R&D Centers, directly signaling future demand for precision machine tools in semiconductor equipment fabrication.

- February 2026: International Aerospace Manufacturing Private Limited, the Rolls-Royce and HAL joint venture, completed a 12-acre expansion of its Hosur aerospace manufacturing hub in Tamil Nadu to produce compressor and turbine components for civil and defense aerospace programs, adding a new precision-machining demand node in the state.

India Turning Centers Market Report Scope

The India Turning Centers Market Report is Segmented by Product Type (Horizontal Turning Centers, Vertical Turning Centers, and More), by Axis Configuration (3-Axis, 4-Axis, 5-Axis & Above), by Automation Type (Manual, Semi-Automatic, Fully Automatic CNC), by End-User Industry (Automotive and Commercial Vehicles, Aerospace & Defense, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Horizontal Turning Centers |

| Vertical Turning Centers |

| Multi-Tasking Turning Centers |

| Others |

| 3-Axis |

| 4-Axis |

| 5-Axis and Above |

| Manual |

| Semi-Automatic |

| Fully Automatic CNC |

| Automotive and Commercial Vehicles |

| Aerospace & Defense |

| Medical Devices and Surgical Instruments |

| Oil, Gas, and Energy |

| Electrical, Electronics and Semiconductor Equipment |

| General Industrial Machinery |

| Others |

| By Product Type | Horizontal Turning Centers |

| Vertical Turning Centers | |

| Multi-Tasking Turning Centers | |

| Others | |

| By Axis Configuration | 3-Axis |

| 4-Axis | |

| 5-Axis and Above | |

| By Automation Type | Manual |

| Semi-Automatic | |

| Fully Automatic CNC | |

| By End-User Industry | Automotive and Commercial Vehicles |

| Aerospace & Defense | |

| Medical Devices and Surgical Instruments | |

| Oil, Gas, and Energy | |

| Electrical, Electronics and Semiconductor Equipment | |

| General Industrial Machinery | |

| Others |

Key Questions Answered in the Report

What is the 2031 value outlook for turning centers in India?

The India turning centers market is expected to reach USD 1.8 billion by 2031 from USD 1.3 billion in 2026, growing at a 6.72% CAGR over 2026-2031.

Which product category leads demand in India?

Horizontal turning centers led demand with 52.5% share in 2025 because they remain central to automotive and general engineering production.

Which machine configuration is growing the fastest?

The 4-axis segment is expected to record the fastest growth among axis types at 8.5% CAGR through 2031 as manufacturers seek fewer setups and more part complexity in a single machine.

Why are fully automatic CNC systems gaining traction in India?

Fully automatic CNC turning centers are projected to grow at 9.2% CAGR because labor cost pressure, export-quality requirements, and SAMARTH demonstration centers are making automation easier to justify .

Which end-use sector creates the largest volume opportunity?

Automotive and commercial vehicles accounted for 38.5% of demand in 2025, making them the largest source of recurring machine purchases across the supplier network

How is semiconductor investment affecting turning center demand in India?

Semiconductor projects in Sanand, Dholera, and Surat are adding demand for precision-machined housings, fixtures, and equipment parts, which is opening a new growth layer for high-precision turning systems

Page last updated on: