India Sweets Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.11 Billion |

| Market Size (2026) | USD 1.19 Billion |

| Market Size (2031) | USD 1.76 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Sweets Market Analysis by Mordor Intelligence

The India sweets market was valued at USD 1.11 billion in 2025 and is estimated to reach USD 1.19 billion in 2026, anticipated to grow to USD 1.76 billion by 2031, registering a CAGR of 8.12% during 2026–2031. The market is driven by growing demand for premium and artisanal Indian sweets, increasing festive and corporate gifting culture, and continuous innovation in healthier formulations such as sugar-free, millet-based, and clean-label products. The rapid expansion of organized retail, online food delivery, and quick-commerce platforms is improving accessibility to branded sweets, while advances in packaging and shelf-life enhancement technologies are enabling wider distribution across domestic and export markets. Additionally, rising consumer preference for hygienically packaged, premium-quality, and regionally authentic sweets is accelerating the transition from unorganized retail to branded packaged offerings, supporting sustained market growth over the forecast period.

Key Report Takeaways

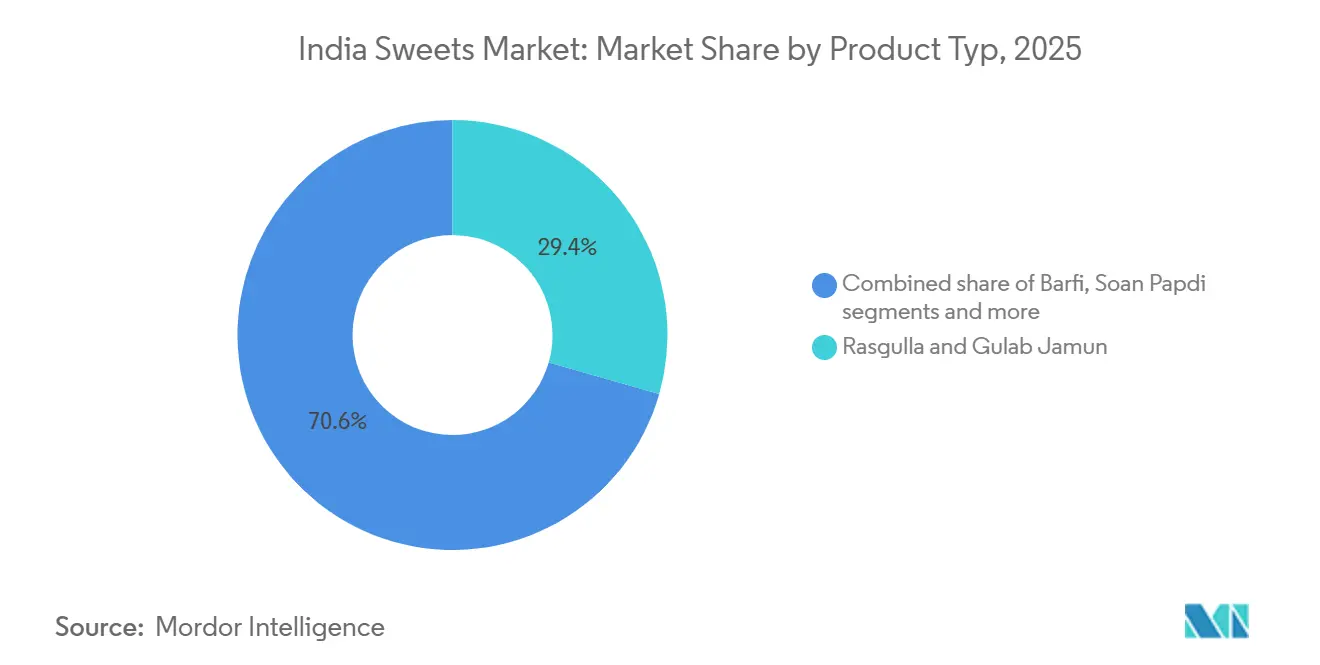

- By product type, Rasgulla and Gulab Jamun led with a 29.43% share in 2025, while Barfi is forecast to grow at a 9.09% CAGR through 2031.

- By ingredient type, Milk and Milk Derivatives held a 57.89% share in 2025, while Dry Fruits is projected to expand at a 9.33% CAGR through 2031.

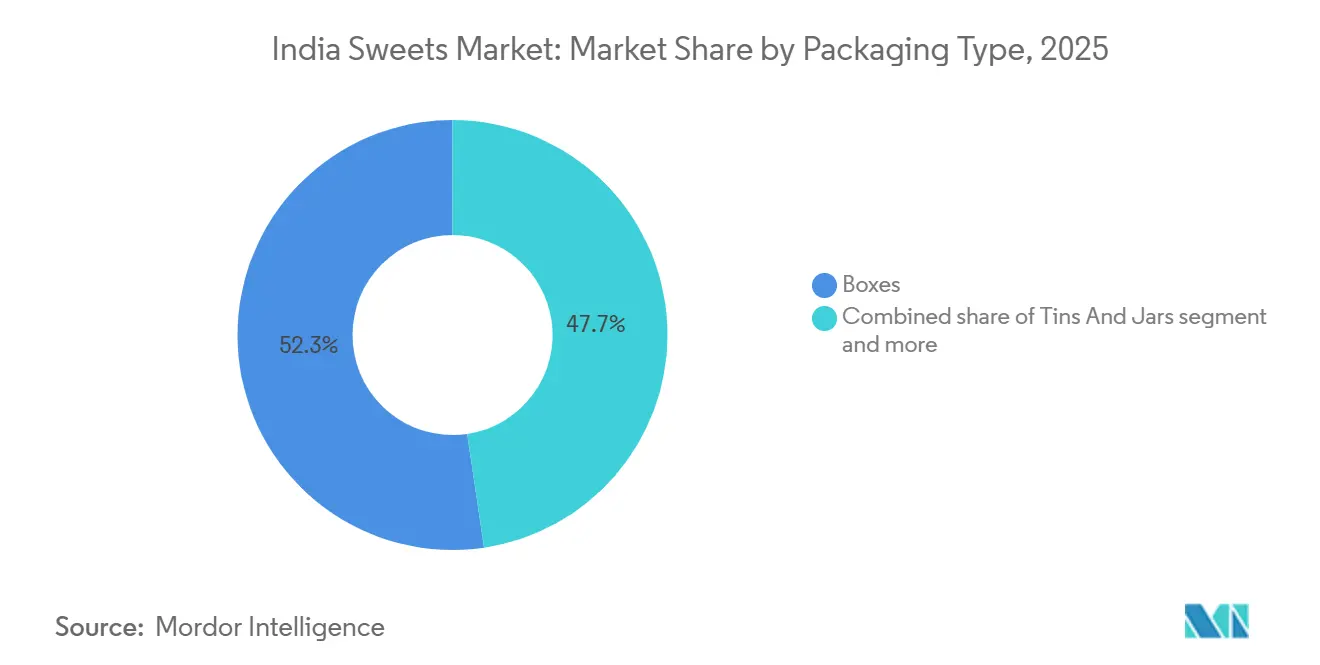

- By packaging type, Boxes accounted for 52.34% of the India sweets market size in 2025, while Flexible Packs are advancing at an 8.95% CAGR through 2031.

- By distribution channel, Supermarkets and Hypermarkets held 38.92% of the India sweets market share in 2025, while Online Retail Stores recorded the highest projected CAGR at 9.81% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Sweets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

| Growing demand for premium and artisanal Indian sweets | +2.0% | National, with concentrated impact in metro cities (Mumbai, Delhi, Bengaluru, Hyderabad) | Medium term (2–4 years) |

| Rising popularity of festive and gifting culture | +1.8% | National, with peak demand spikes in northern and western regions during Diwali, Eid, and wedding season | Short term (≤ 2 years) |

| Innovation in healthier sweet formulations | +1.2% | National, primarily Tier-1 and Tier-2 urban centres with health-conscious demographics | Medium term (2–4 years) |

| Growth of online food delivery and quick commerce platforms | +1.5% | National, with early gains in top 30 cities across Bengaluru, Delhi NCR, Mumbai, and Hyderabad | Short term (≤ 2 years) |

| Increasing demand for regional and traditional specialty sweets | +0.8% | National, with state-specific anchors (West Bengal, Karnataka, Rajasthan, Odisha) | Medium term (2–4 years) |

| Product innovation through fusion and contemporary flavors | +0.7% | National, urban consumers and Indian diaspora-export corridors | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growing demand for premium and artisanal Indian sweets

Consumers are increasingly seeking premium-quality Indian sweets made using authentic recipes, high-grade ingredients, and artisanal production methods, prompting manufacturers to expand their premium product portfolios. Demand is growing for sweets made with pure desi ghee, premium dry fruits, saffron, natural flavors, and preservative-free formulations, particularly for festive gifting and special occasions. Premium packaging, handcrafted presentation, and regional specialty offerings are further adding product value and supporting brand differentiation. For instance, in September 2024, Priniti Foods entered the premium Indian sweets category by launching five traditional sweets such as Rasgulla, Gulab Jamun, Dry Fruit Panjeeri Ladoo, Dry Fruit Besan Ladoo, and Soan Papdi, strengthening its presence in the premium packaged sweets segment. This trend continues to drive innovation and premiumization across the India sweets market.

Rising popularity of festive and gifting culture

India's festive and gifting culture remains a key driver of the sweets market, as traditional sweets are an integral part of festivals, weddings, religious ceremonies, family celebrations, and corporate gifting. Growing consumer preference for premium packaged sweets, curated gift hampers, and customized assortments is encouraging manufacturers to introduce festive collections, premium packaging, and value-added offerings. This seasonal demand supports both higher sales volumes and product premiumization. For instance, according to the Agricultural and Processed Food Products Export Development Authority (APEDA), Diwali spending in 2025 reached approximately USD 69 billion, with food and grocery purchases accounting for a significant share, highlighting the role of festive consumption in driving demand for sweets across India [1]Source: Agricultural and Processed Food Products Export Development Authority (APEDA), "Diwali Sales Lit Up Indian Consumer Market in 2025", apeda.gov.in.

Innovation in healthier sweet formulations

Innovation in healthier sweet formulations is emerging as a significant driver of the India sweets market, as consumers increasingly seek products that balance traditional taste with improved nutritional profiles. Manufacturers are developing sugar-free, low-sugar, high-protein, millet-based, vegan, and clean-label sweets using natural sweeteners, functional ingredients, and healthier fats to address evolving dietary preferences without compromising authenticity. These innovations are expanding the appeal of traditional sweets among health-conscious consumers while creating new opportunities for premium product differentiation and year-round consumption. For instance, Healthy Mithai, an Indian brand, specializes in traditional mithais made without added sugar, offering healthier alternatives to conventional sweets while preserving authentic Indian flavors. Such product innovations are encouraging wider consumer adoption and supporting the evolution of India's traditional sweets industry.

Growth of online food delivery and quick commerce platforms

The rapid expansion of online food delivery and quick commerce platforms is making traditional and packaged sweets more accessible for everyday consumption, festive purchases, and last-minute gifting, thereby driving the India sweets market. Manufacturers are increasingly partnering with digital commerce platforms and introducing delivery-friendly packaging to ensure product freshness and convenience while expanding their customer reach. The availability of premium and regional sweets through instant delivery services has further encouraged impulse purchases and strengthened the organized sweets segment. For instance, according to Zomato, Blinkit generated revenue of more than INR 52.04 billion in FY2025, reflecting the rapid growth of quick commerce in India and the increasing role of digital retail channels in supporting sales of food products, including sweets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short shelf life of traditional sweets | -0.6% | National, with higher constraint severity in Tier-2/3 cities and export corridors lacking cold chain | Short to medium term (≤ 3 years) |

| Stringent food safety and quality compliance requirements | -0.5% | National (particularly for micro and small manufacturers), with compliance infrastructure concentrated in metros | Medium term (2–4 years) |

| Adulteration and counterfeit products affecting consumer trust | -0.7% | National, with elevated risk in unorganised supply chains across Uttar Pradesh, Madhya Pradesh, Rajasthan | Short term (≤ 2 years) |

| Dependence on perishable dairy ingredients | -0.5% | National, with higher sensitivity in interior regions lacking reliable cold storage and milk procurement networks | Medium to long term (≥ 3 years) |

| Source: Mordor Intelligence | |||

Short shelf life of traditional sweets

The short shelf life of traditional Indian sweets is a significant restraint on market growth, particularly for fresh and dairy-based products that are vulnerable to microbial contamination, moisture migration, texture degradation, and flavor deterioration. Many popular sweets require immediate consumption or refrigerated storage to maintain freshness, taste, and quality, limiting their commercial viability over extended periods. This creates challenges in inventory planning, stock rotation, and demand forecasting, often resulting in higher product wastage and increased returns for manufacturers and retailers. Limited shelf life also restricts interstate distribution, export potential, and expansion into distant markets where longer transportation times are involved. To address these challenges, manufacturers must invest in advanced preservation technologies, improved packaging solutions, cold-chain infrastructure, and quality assurance systems, all of which increase production complexity and operational costs.

Stringent food safety and quality compliance requirements

Stringent food safety and quality compliance requirements act as a significant restraint on the India sweets market. Manufacturers must comply with comprehensive regulations governing ingredient quality, hygiene, manufacturing practices, packaging, labeling, storage, and distribution. Traditional sweets often contain highly perishable ingredients such as milk, khoa (khoya), ghee, and paneer, which require strict process controls to prevent contamination and ensure product safety. Meeting evolving standards requires continuous investment in quality assurance systems, laboratory testing, traceability, employee training, sanitation protocols, and certified manufacturing facilities. Frequent regulatory inspections, mandatory labeling requirements, and adherence to food safety management systems further increase operational complexity, particularly for small and unorganized sweet manufacturers with limited resources.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Syrup-Based Sweets Anchor Volume While Barfi Premiumises the Mix

Rasgulla and Gulab Jamun together accounted for the largest product-type share at 29.43% in 2025, driven by their enduring cultural relevance, widespread consumer acceptance, and year-round demand across multiple consumption occasions. Their strong association with celebrations, festivals, family gatherings, and religious traditions ensures consistent purchase frequency throughout the year. Improvements in hygienic production, packaging, and shelf-life extension have enabled manufacturers to expand availability while maintaining product freshness and quality. Premiumization through the use of high-quality dairy ingredients, authentic recipes, and attractive gifting formats has further strengthened their market position. Their ability to retain traditional appeal while adapting to evolving retail and packaging standards continues to reinforce their dominance within the India sweets market.

Barfi is the fastest-growing product type at a CAGR of 9.09% during 2026–2031, driven by increasing innovation in premium formulations, ingredient diversification, and value-added product offerings. Manufacturers are introducing variants enriched with dry fruits, saffron, chocolate, millet, and reduced-sugar ingredients to meet changing consumer preferences for differentiated sweets. Improved packaging, premium gifting appeal, and better preservation technologies have expanded the product's accessibility across organized retail and online channels while maintaining quality. Growing consumer interest in artisanal products, regional specialties, and contemporary flavor combinations is further accelerating demand, positioning Barfi as one of the most rapidly expanding categories in the India sweets market.

By Ingredient Type: Dairy Foundations Endure While Dry Fruits Command a Premium Growth Runway

Milk and milk derivatives held a 57.89% ingredient share in 2025, reflecting their fundamental role in defining the taste, texture, aroma, and richness of traditional Indian sweets. Their functional properties enable the preparation of a wide variety of products while delivering the creaminess and mouthfeel that consumers associate with premium-quality mithai. Improvements in dairy processing, quality assurance, and cold-chain infrastructure have enhanced ingredient consistency and product quality, allowing manufacturers to maintain traditional characteristics at larger production scales. The growing emphasis on purity, authentic recipes, and high-quality dairy ingredients has further reinforced the preference for milk-based formulations, ensuring that dairy remains the cornerstone of India's sweets industry.

Dry fruits are projected to be the fastest-growing ingredient segment at a CAGR of 9.33% during 2026–2031, driven by increasing demand for premium, nutrient-rich, and value-added sweet offerings. Manufacturers are incorporating ingredients such as almonds, pistachios, cashews, walnuts, and dates to enhance taste, texture, visual appeal, and perceived product quality. The rising popularity of premium gifting, festive assortments, and artisanal sweets has further accelerated the use of dry fruits as a key differentiating ingredient. Additionally, product innovation featuring dry fruit-rich formulations, clean-label positioning, and healthier indulgence options is expanding consumer appeal, supporting sustained growth of this ingredient segment across the forecast period.

By Packaging Type: Rigid Boxes Lead Gifting Volume While Flexible Packs Win the Convenience Channel

Boxes accounted for 52.34% of the India sweets market by packaging in 2025, supported by their ability to preserve product quality while enhancing presentation and gifting appeal. Premium boxes offer better protection for delicate sweets, facilitate organized assortments, and provide greater scope for branding and customization, making them the preferred packaging format for traditional and premium mithai. Manufacturers are increasingly adopting food-grade, tamper-evident, and sustainable packaging materials to improve product safety and consumer confidence. Evolving packaging regulations, including the Food Safety and Standards (Packaging) First Amendment Regulations, 2025, have encouraged the use of compliant packaging materials that ensure product integrity and regulatory adherence, further strengthening the dominance of box packaging across the market [2]Source: Food Safety and Standards Authority of India (FSSAI), "Food Safety and Standards (Packaging) First Amendment Regulations, 2025", fssai.gov.in.

Flexible packs represent the fastest-growing packaging segment, expanding at a CAGR of 8.95% during 2026–2031, driven by increasing demand for lightweight, convenient, and cost-efficient packaging solutions suitable for modern retail and e-commerce distribution. Their ease of handling, reduced material usage, and compatibility with single-serve and smaller pack sizes make them well suited to changing consumer purchasing patterns. Advances in multilayer barrier films and resealable packaging technologies have improved freshness retention and extended shelf life while maintaining product quality. Growing emphasis on recyclable materials, improved packaging efficiency, and convenience-oriented product formats is further accelerating the adoption of flexible packaging across India's sweets market.

By Distribution Channel: Organised Retail Remains the Volume Pillar While Online Retail Disrupts Unit Economics

Supermarkets and hypermarkets held the largest distribution share at 38.92% in 2025. Their ability to offer a wide assortment of branded and premium sweets in a hygienic and organized retail environment supports this position. These outlets provide standardized product quality, attractive in-store displays, seasonal promotions, and convenient shopping experiences that encourage both impulse and planned purchases. The availability of premium gifting packs, exclusive festive assortments, and value-added product offerings has further strengthened their position. In addition, cold storage facilities, efficient inventory management, and compliance with food safety and packaging standards enable supermarkets and hypermarkets to maintain product freshness and consumer confidence, reinforcing their dominance in the India sweets market.

Online retail stores are projected to be the fastest-growing distribution channel at a CAGR of 9.81% during 2026–2031. The rapid expansion of e-commerce and quick-commerce has transformed the way consumers purchase traditional sweets. Enhanced digital storefronts, doorstep delivery, scheduled gifting options, and wider product availability have made online platforms increasingly attractive for both everyday purchases and festive occasions. Manufacturers and retailers are investing in digital marketing, direct-to-consumer platforms, insulated packaging, and real-time order tracking to improve the online buying experience while preserving product quality during transit. Growing consumer preference for convenience, digital payments, personalized gifting, and same-day delivery continues to drive the adoption of online retail for sweets across India

Geography Analysis

North and West India represent the largest concentration of the India sweets market, supported by deeply embedded traditions of festive gifting, religious celebrations, weddings, and family occasions that sustain year-round demand. The region benefits from a well-developed network of organized retail, branded sweet chains, supermarkets, and expanding quick-commerce platforms, enabling broader availability of packaged and premium sweets. Large metropolitan centers continue to shape consumption trends through increasing preference for hygienically packaged, premium-quality, and gift-oriented products. According to the World Bank, 36% of India's population resided in urban areas in 2025, supporting the expansion of modern retail infrastructure and improving accessibility to branded sweets across major cities [3]Source: World Bank, "Urban population (% of total population) - India", worldbank.org.

Eastern India remains a distinctive regional market characterized by its rich heritage of traditional sweet-making and strong preference for authentic regional delicacies. Long-established culinary traditions continue to preserve demand for fresh, artisanal sweets while encouraging manufacturers to retain authentic recipes and geographical identity. The region is witnessing increasing adoption of organized retail, improved packaging technologies, and branded offerings that enhance shelf life without compromising traditional taste and texture. Growing tourism, inter-state trade, and demand for regional specialties as premium gifting products are further expanding the commercial reach of Eastern India's traditional sweets beyond their place of origin.

South India contributes a robust and diversified demand base driven by its unique confectionery traditions, religious customs, and strong preference for region-specific sweet varieties. Temple festivals, cultural celebrations, and ceremonial occasions ensure consistent consumption throughout the year, while growing domestic tourism increases demand for locally renowned specialties purchased as souvenirs and gifts. Manufacturers are increasingly combining traditional recipes with modern packaging, food safety standards, and longer shelf-life technologies to expand distribution through organized retail and online channels. The region is also witnessing rising innovation in premium formulations, clean-label ingredients, and attractive packaging, enabling traditional sweets to reach a broader consumer base while preserving their regional authenticity.

Competitive Landscape

The India sweets market features a consolidated top layer of national brands such as Haldiram's, Bikaji Foods International, and Bikanervala, alongside regional specialists and cooperative dairy players such as Amul and Nandini. This structure balances nationwide scale with strong regional influence. Established players continue to strengthen their market position through standardized manufacturing, extensive retail networks, food safety compliance, and investments in modern packaging technologies. Regional manufacturers maintain their competitiveness by preserving authentic recipes, catering to local taste preferences, and leveraging strong regional brand recognition.

Strategic differentiation is increasingly driven by intellectual property, proprietary recipes, distinctive packaging designs, premium formulations, and product innovation, rather than distribution reach alone. Manufacturers are focusing on clean-label ingredients, fusion flavors, healthier recipes, and premium gifting collections to build brand identity and customer loyalty. Investments in packaging, shelf-life enhancement technologies, and premium presentation are enabling brands to command higher value while meeting evolving consumer expectations for quality, authenticity, and convenience.

The market is also witnessing the rapid emergence of new-age startups such as Bombay Sweet Shop, GoDesi, and India Sweet House. These companies are leveraging branded storytelling, artisanal production claims, premium packaging, and digital-first business models to compete on value rather than volume. Their focus on curated gifting experiences, authentic regional flavors, contemporary branding, and direct-to-consumer engagement is reshaping competitive dynamics and encouraging the broader industry to accelerate premiumization and innovation in gifting-optimized product formats.

India Sweets Industry Leaders

-

Haldirams Snacks Pvt. Ltd

-

Bikaji Foods International Limited

-

Bikanervala Foods Private Limited

-

Adyar Ananda Bhavan Sweets Pvt Ltd

-

K. C. Das Grandson Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Haldiram's has opened a new restaurant in Ayodhya, strengthening its retail presence in North India. Located on Ram Path Road near the Railway Station, the outlet will serve residents as well as the large number of pilgrims and tourists visiting the city throughout the year.

- September 2025: Anmol Industries Limited has launched a traditional sweets portfolio, starting with Soan Papdi, available in 200 gm and 450 gm pack sizes to cater to individual consumption as well as gifting during the festival season.

India Sweets Market Report Scope

Sweets, commonly known as Mithais in India, are traditional confectionery products deeply rooted in the country's cultural heritage, culinary traditions, and festive customs. The India sweets market is segmented by product type, ingredient type, packaging type, and distribution channel. Based on product type, the market is segmented into rasgulla and gulab jamun, barfi, soan papdi, peda, laddoo, and others. Based on ingredient type, the market is segmented into milk and milk derivatives, cereal and pulses, dry fruits, and others. Based on packaging type, the market is segmented into boxes, tins and jars, plastic containers, and flexible packs. Based on distribution channel, the market is segmented into supermarkets/hypermarkets, convenience and grocery stores, specialty stores, online retail stores, and other distribution channels. The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

| Rasgulla and Gulab Jamun |

| Barfi |

| Soan Papdi |

| Peda |

| Laddoo |

| Others |

| Milk and Milk Derivatives |

| Cereal and Pulses |

| Dry Fruits |

| Others |

| Boxes |

| Tins And Jars |

| Plastic Containers |

| Flexible Packs |

| Supermarkets/Hypermarkets |

| Convenience and Grocery Stores |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Rasgulla and Gulab Jamun |

| Barfi | |

| Soan Papdi | |

| Peda | |

| Laddoo | |

| Others | |

| By Ingredient Type | Milk and Milk Derivatives |

| Cereal and Pulses | |

| Dry Fruits | |

| Others | |

| By Packaging Type | Boxes |

| Tins And Jars | |

| Plastic Containers | |

| Flexible Packs | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience and Grocery Stores | |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the forecast growth rate for sweets in India through 2031?

The India sweets market is forecast to grow at an 8.11% CAGR from 2026 to 2031, reaching USD 1.76 billion by 2031.

Which product category leads sales in India sweets?

Rasgulla and Gulab Jamun led product demand with a 29.43% share in 2025, supported by broad regional acceptance and year-round availability.

Which ingredient group is expanding the fastest in Indian mithai?

Dry Fruits are projected to grow at a 9.33% CAGR through 2031 because they fit premium gifting, health positioning, and longer shelf life.

Why are online channels becoming important for branded sweets?

Online Retail Stores are expected to grow at a 9.8% CAGR through 2031 as quick commerce improves impulse buying, last-minute gifting, and digital assortment visibility.

Page last updated on: