India Staple Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

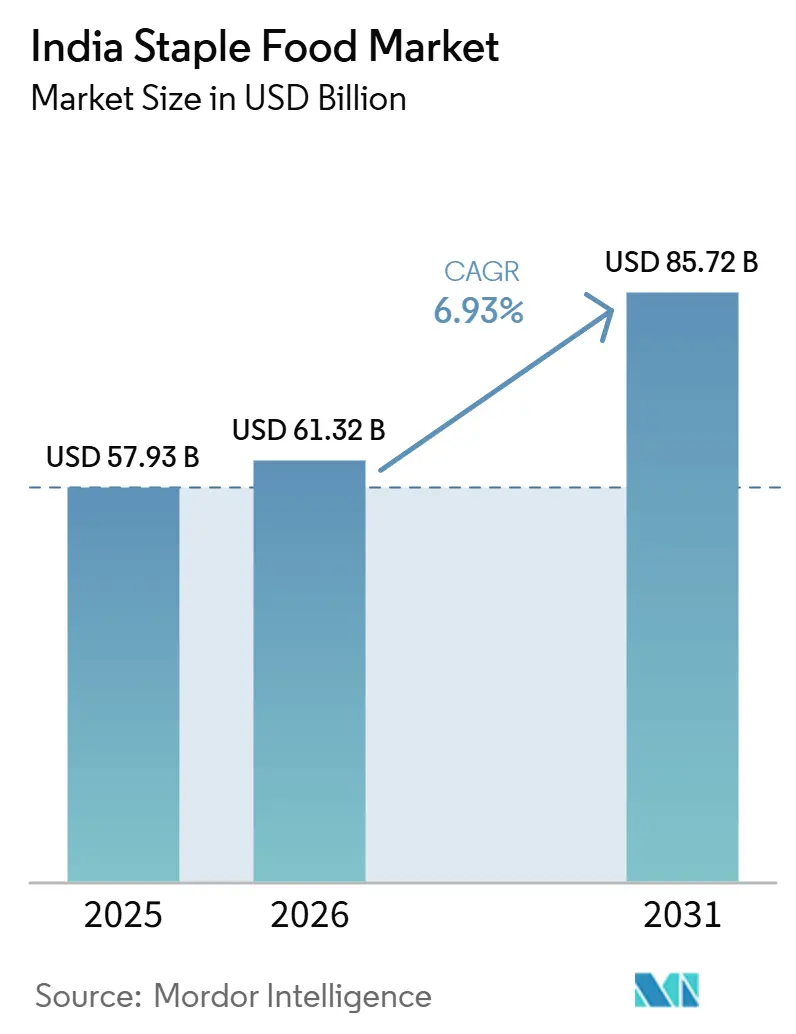

| Base Year Market Size (2025) | USD 57.93 Billion |

| Market Size (2026) | USD 61.32 Billion |

| Market Size (2031) | USD 85.72 Billion |

| Growth Rate (2026 - 2031) | 6.93% CAGR |

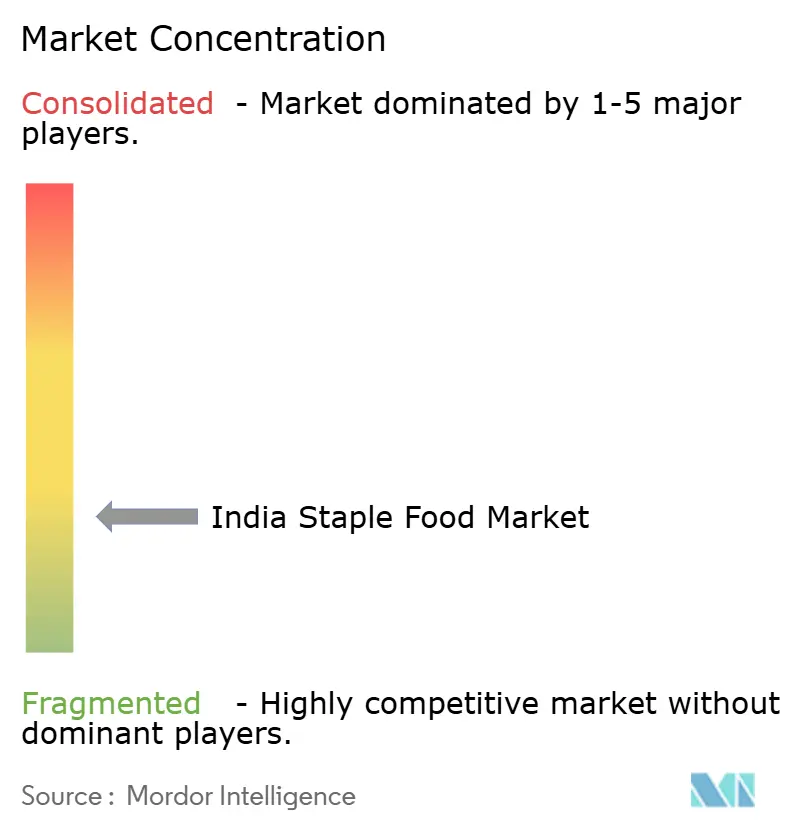

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Staple Food Market Analysis by Mordor Intelligence

The India staple food market size is expected to grow from USD 57.93 billion in 2025 to USD 61.32 billion in 2026 and reach USD 85.72 billion by 2031, registering a CAGR of 6.93% during 2026-2031. A young consumer base, continued urban migration, and the rise of dual-income households are supporting the growth of the India staple food market by shifting everyday demand toward cleaner and more dependable packaged staples. India’s foodgrain output is projected to reach 376.56 million tonnes in 2025-26, improving raw material availability while increasing competition for branded shelf space and procurement access, according to the Department of Agriculture and Farmers Welfare, under the Ministry of Agriculture and Farmers Welfare[1]Source: Ministry of Agriculture and Farmers Welfare, “Second Advance Estimates of Production of Major Agricultural Crops for 2025-26,” Government of India, agricoop.nic.in. Government-backed distribution remains an important stabilizer, as PMGKAY continues to support more than 800 million beneficiaries and provides processors and millers with a large, recurring volume base. At the same time, digital traceability and quality reforms are raising standards across the value chain, creating opportunities for branded players that can manage sourcing, processing, and packaging more consistently. The India staple food market is also witnessing stronger competitive positioning through portfolio expansion, distribution build-out, and selective consolidation by larger food and agri players, such as Wilmar, AWL, ITC, LT Foods, KRBL, and Marico.

Key Report Takeaways

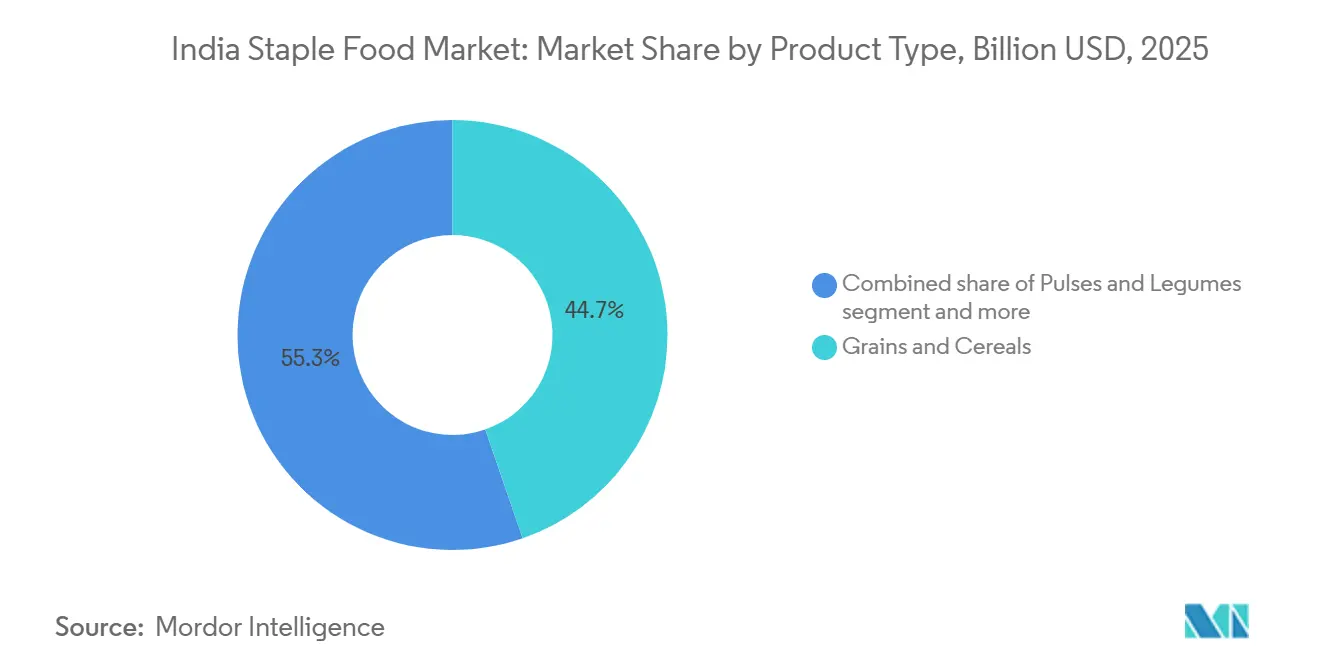

- By product type, Grains and Cereals held 44.71% share in 2025, while Pulses and Legumes recorded the highest projected CAGR at 7.96% through 2031.

- By product format, Raw or Unprocessed products accounted for 48.62% share in 2025, while Processed products advanced at the fastest CAGR of 7.81% through 2031.

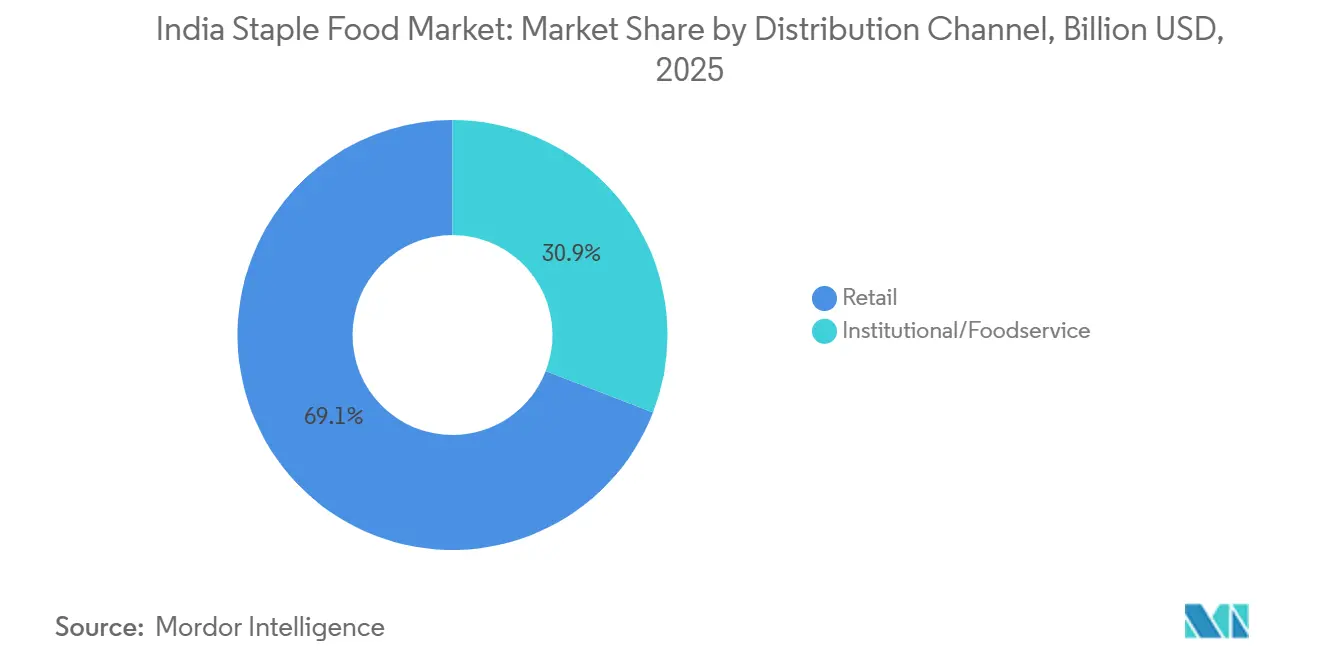

- By distribution channel, Retail held 69.13% of the India staple food market share in 2025, while Institutional or Foodservice posted the highest projected CAGR at 8.51% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Staple Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift from loose staples to branded packaged staples | +1.8% | Pan-India, most pronounced in Tier 1 and Tier 2 cities; North and West India leading | Short term (≤ 2 years) |

| Expansion of organized retail and quick commerce access points | +1.5% | Metro markets (Delhi-NCR, Mumbai, Bengaluru, Chennai, Pune); spill-over to Tier 2+ India | Short term (≤ 2 years) |

| Fortification and premiumization of daily-use staples | +0.8% | National, early traction in urban markets, FSSAI compliance framework applicable nationwide | Medium term (2–4 years) |

| Rising demand for convenience, shelf stability, and traceability | +0.7% | Urban India core; emerging in semi-urban pockets; global for export-oriented players | Medium term (2–4 years) |

| Margin optimization through tech-driven supply chains | +0.6% | Global supply chain nodes; highest impact in North India grain belts and Western India edible-oil corridors | Medium term (2–4 years) |

| High-volume, predictable B2G institutional revenue | +0.9% | National; concentrated in large procuring states, including Uttar Pradesh, Punjab, Andhra Pradesh, Telangana, Odisha | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid shift from loose staples to branded packaged staples

India's shift toward packaged staples is not merely a gradual change in consumer preference; supply-side economics are actively shaping it. FMCG urban sales outpaced rural sales in 2025 for the first time in several quarters, supported by urban volume growth. ITC's Aashirvaad staples franchise sustained double-digit revenue growth in FY26, with value-added variants accounting for approximately 16% of its staples portfolio, up from negligible levels two years earlier. A critical second-order dynamic is that branded staples generate structurally higher gross margins, encouraging distributors and modern trade buyers to prioritize stocked branded SKUs over loose commodities. This margin advantage improves channel willingness to allocate shelf space, inventory, and promotional support to branded offerings. It also strengthens the business case for wider distribution, better in-store visibility, and faster replenishment cycles across organized retail formats. This incentive alignment, rather than consumer demand alone, is driving one of the fastest formalizations of a commodity market in India since the packaged water transition.

Expansion of organized retail and quick commerce access points

The expansion of organized retail and quick commerce is accelerating growth in the India staple food market by improving product accessibility, assortment, and purchase frequency for essentials such as rice, wheat flour, pulses, edible oils, and millets. According to industry estimates, organized retail and e-commerce channels accounted for 40–50% of food category sales in major Indian cities during 2025, with quick commerce emerging as a key driver of staple purchases through rapid delivery and wider SKU availability. Simultaneously, the Food Safety and Standards Authority of India (FSSAI) strengthened oversight by directing e-commerce platforms to maintain stringent hygiene standards across warehouses and storage facilities, reinforcing consumer confidence in online grocery purchases. Product innovation has also supported channel expansion, with ITC introducing new Aashirvaad millet-based flour variants through modern retail and digital commerce in 2025, while Tata Consumer Products expanded its Tata Sampann staples portfolio with value-added pulses and millet-based products across organized retail and quick-commerce platforms in 2026, enhancing premiumization and convenience in India's staple food market.

Fortification and premiumization of daily-use staples

Fortification and premiumization of daily-use staples are driving growth in the India staple food market by encouraging consumers to upgrade from unbranded commodities to value-added products offering enhanced nutrition, quality, and convenience. The Government of India's continued implementation of the fortified rice program under PMGKAY and other welfare schemes, along with FSSAI's promotion of the +F logo for fortified staples, has increased awareness of micronutrient-enriched rice, wheat flour, edible oils, and salt, strengthening consumer acceptance of fortified packaged foods. During FY 2025–26, large volumes of fortified rice continued to be distributed through TPDS, ICDS, and PM-POSHAN, supporting nationwide adoption of fortified staples. Meanwhile, manufacturers are differentiating through premium offerings; in 2025, Fortune expanded its premium Super Food range with nutrient-rich millet-based staples, while in 2026, ITC Aashirvaad broadened its premium portfolio with multigrain and high-fiber atta variants targeting health-conscious households. These developments are increasing value realization, improving brand loyalty, and accelerating premiumization across India's staple food market.

Rising demand for convenience, shelf stability, and traceability

Declining consumer tolerance for opaque supply chains is reshaping procurement and packaging standards for staple producers. India’s Digital Agriculture Mission, approved in 2024 and scheduled for nationwide rollout in 2026, has committed INR 2,817 crore to build agricultural digital public infrastructure[2]Source: Ministry of Agriculture and Farmers Welfare, “Digital Agriculture Mission,” Government of India, agricoop.nic.in. The mission will integrate IoT, AI, satellite imagery, and drones into a unified Agri-Stack, targeting coverage of all 30 crore farm plots by Kharif 2026. The CCEA’s July 2026 approval to introduce QR-code tagging of rice bags under PMGKAY, aimed at enabling end-to-end traceability, is expected to indicate that traceability is shifting from a premium export requirement to a baseline expectation in government procurement. This shift will push the industry toward compliant digital tracking. For consumer-facing brands, shelf-stable formats with verifiable supply provenance are expected to command price premiums, as reflected in KRBL’s February 2026 launch of low-GI rice under the health-oriented India Gate Uplife brand, which positions a commodity as a functional food.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High dependency on volatile, climate-sensitive monsoon patterns | -1.2% | National; Odisha, Chhattisgarh, Madhya Pradesh, and Uttar Pradesh most exposed due to low irrigation coverage | Short term (≤ 2 years) |

| Severe financial leakages from post-harvest storage losses | -0.9% | National: highest in grain-surplus states such as Punjab, Haryana, UP; also significant in eastern rice belts | Medium term (2–4 years) |

| Margin erosion due to complex intermediary-driven mandis | -0.7% | Pan-India; most acute in states where APMC reform adoption remains low | Long term (≥ 4 years) |

| Strict regulatory compliance regarding price control mandates | -0.6% | National; Essential Commodities Act-linked interventions concentrated in high-price cycles for wheat, pulses, edible oils | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High dependency on volatile, climate-sensitive monsoon patterns

India's meteorological authority forecasts a below-normal southwest monsoon for 2026 at 92% of the long-period average, driven by El Niño conditions. Although record foodgrain production of 376.56 million tonnes in 2025-26 provides a buffer, IMD data indicate that rice production can decline by 10% or more in vulnerable districts during sub-normal rainfall years. Care Edge Ratings assesses Odisha, Chhattisgarh, and Uttar Pradesh as structurally exposed due to their reliance on rainfed cropping and water-intensive crops. Food and beverage categories account for approximately 46% of India's Consumer Price Index, which means monsoon-linked supply shocks directly translate into consumer price volatility. This volatility can compress staple brand margins or prompt government price-control interventions. A second-order risk is that repeated climate shocks increase raw material cost uncertainty for processors, discouraging long-term fixed-price supply contracts, which remain a prerequisite for organized retail's volume scaling.

Severe financial leakages from post-harvest storage losses

India faces a 47% storage capacity shortfall relative to its foodgrain production, with current infrastructure handling only 145 million tonnes against an estimated annual production of 350 million tonnes. Research published in Foods (2024) estimates that inadequate post-harvest handling and storage cause annual cereal losses of approximately 23 million tonnes in India, a volume comparable to the combined annual wheat output of several mid-sized cereal-producing countries. The government has committed USD 15 billion to overhaul grain storage infrastructure[3]Source: Press Information Bureau, “Grain Storage Capacity and Food Infrastructure Measures,” Government of India, pib.gov.in. However, implementation timelines extend across the forecast period, indicating that value leakage from storage-related losses will remain a structural drag on supply chain economics through at least 2028. These storage losses also disproportionately affect smaller millers and trader-aggregators that lack silo infrastructure, sustaining their financial fragility and slowing the market’s transition from informal to organized processing at the mid-tier level, where branded staple value is generated.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Packaged Grains Lead, Pulses Fastest to Convert

Grains and cereals are expected to hold 44.71% of the product type segmentation in 2025, supported by rice and wheat consumption across households and institutions. Government rice procurement is expected to reach 463.06 lakh tonnes in the Kharif Marketing Season 2025-26, up 6% year-on-year. Millets are emerging as a strategic secondary category, with India accounting for approximately 40% of global output. The Production Linked Incentive Scheme for millet-based products allocates INR 793.27 crore to 29 food processing companies for value-added formats. Flours, including atta (whole wheat), maida, and rice flour, remain a premiumization segment, with multigrain and high-protein variants commanding 30-40% price premiums. KRBL's India Gate Uplife Lite low-GI rice and ITC's Aashirvaad High Protein Atta in FY26 reflect the shift toward functional foods.

The pulses and legumes segment is expected to grow fastest, at a CAGR of 7.96% through 2031, driven by protein awareness and dietary diversification among health-conscious urban consumers. Arhar (tur/pigeon pea) accounts for 30.9% of total pulse consumption, followed by gram at 23.8% and masoor at 13.9%, according to a 2024 Indian Journal of Food Legumes study. Branded chana dal and moong dal packaged SKUs are gaining supermarket visibility over loose products. India is expected to import 65.69 lakh tonnes of pulses in calendar year 2025, down 4.45% year-on-year, while a 301% surge in chana imports signals supply gaps for branded packagers. Edible oils, sugar and sweeteners, and spices and condiments remain significant sub-markets. Domestic edible oil production covers only approximately 40% of national consumption, reinforcing import dependence and affecting retail price stability for processed-format players, according to the Indian Vegetable Oil Producers' Association.

By Product Format: Processing Margin Gap Widens as Branded Conversion Accelerates

Raw/unprocessed formats are expected to account for 48.62% of the product format segment in 2025, reflecting the still-large volume of loose grains, unpackaged pulses, and bulk edible oils sold through kirana stores and wet markets. This dominance remains structural but is declining. The processed segment is expected to grow at a CAGR of 7.81% through 2031, gaining share as urban consumers increasingly move away from loose commodities due to convenience and hygiene concerns. This shift has direct financial implications, as processed and packaged staples generate gross margin rates roughly 15–25 percentage points higher than their unprocessed equivalents. This margin advantage helps explain the expected growth of the Indian FMCG packaged foods market.

The fastest growth in the processed format does not come only from premium or urban segments. A less obvious driver is the shift among mid-income rural consumers toward processed formats, as mobile and quick-commerce platforms expand access to packaged staples in Tier 2+ geographies. Value-commerce platforms, targeting households across cities with populations exceeding five lakh (500,000), are expected to increase the annual transacting user base to 320–340 million by FY26. As a result, processed-format staples now have a viable last-mile channel in markets that lacked organized retail infrastructure two years ago. The FSSAI compliance mandate, which requires front-of-pack quality and ingredient disclosures on packaged foods, also indirectly benefits processed-format players that can afford labeling investments. This regulatory influence effectively raises the cost of informalization at scale.

By Distribution Channel: Institutional Fastest but Retail Remains the Volume Engine

Retail is expected to command 69.13% of the distribution channel in 2025, supported by offline kirana stores and a growing online segment. Quick commerce is expected to shape online retail, with dark-store infrastructure across Blinkit, Swiggy Instamart, and Zepto projected to reach 5,026 locations in May 2026, up from 3,405 a year earlier. India’s quick commerce channel is expected to grow by 40% year-on-year. In staples, this reflects consumer preference for small-basket, high-frequency purchases over bulk shopping, favoring smaller packs such as 500g sachets and 1-kg pouches with higher per-unit margins. Offline retail is also becoming more organized through direct-distribution programs, even as kirana stores are expected to retain about 91% of the grocery market share in 2025. LT Foods plans to double its retail reach from 160,000 to 320,000 outlets over the next 2-3 years through pin-code-level distribution expansion.

The institutional/foodservice segment is expected to grow the fastest at an 8.51% CAGR. The Indian government’s PMGKAY scheme serves over 80 crore beneficiaries, while rice offtake under the NFSA and related welfare programs is projected to reach 38.1 million tonnes in 2025-26. The Cabinet’s expected approval of the INR 25,530 crore Sarthak PDS program in June 2026, combining support for intra-state foodgrain movement with AI-driven registry modernization, indicates more technology-enabled institutional procurement. This shift favors large organized millers with QR-code-compliant supply chains over informal intermediaries. Beyond PDS, the hotel, restaurant, and canteen (HoReCa) segment is recovering after the pandemic, increasing demand for bulk pulses, rice, and edible oils across hospitality, defense, and educational institutions. Branded staple manufacturers are increasingly treating this demand as a dedicated go-to-market vertical.

Geography Analysis

North and West India account for the highest revenue concentration in the India staple food market, as these regions combine large wheat demand, strong edible-oil processing bases, and well-developed distribution systems. Uttar Pradesh, Punjab, and Haryana remain important centers for wheat procurement and branded atta demand, giving the northern belt a strong role in everyday staple movement. Maharashtra and Gujarat anchor a large share of edible-oil processing and organized distribution activity, supporting companies such as AWL and Marico in western India. The government’s wheat procurement target for the Rabi Marketing Season 2026-27 is set at 303 lakh metric tons, underscoring the northern system’s central role in the national grain chain, according to the Press Information Bureau.

South India remains the main rice consumption belt in the India staple food market. Tamil Nadu, Andhra Pradesh, Telangana, Karnataka, and Kerala together support a substantial base for branded rice demand, while the region’s stronger urban purchasing power accelerates the shift toward premium staple formats. Bengaluru and Chennai also provide a supportive environment for fortified rice, multigrain atta, and other value-added daily staples. In July 2026, the Cabinet is expected to approve tighter quality norms for PMGKAY rice, including lower broken-grain limits, a change directly relevant to rice-heavy southern procurement systems, according to the Press Information Bureau. East India, including West Bengal, Odisha, Bihar, and Jharkhand, remains a high-volume zone with lower branded penetration, creating meaningful room for future packaged growth as organized trade and distribution improve.

Northeast India, along with parts of Madhya Pradesh and Chhattisgarh, represents an earlier-stage opportunity for branded expansion in the India staple food market. KRBL’s India Gate Poha launch identified Madhya Pradesh and Chhattisgarh as next-stage markets after the first phase, indicating how companies are expanding outward from stronger core territories. The Digital Agriculture Mission is expected to gradually improve farm-level visibility across central and eastern regions, helping processors build more reliable sourcing and traceability systems over time. Record central pool stocks of 122.64 million tons in June 2026 are expected to provide the country with a food security buffer, reducing the risk that one weak season could sharply destabilize the broader India staple food market, according to the Food Corporation of India.

Competitive Landscape

The India staple food market remains moderately fragmented. Leading branded companies hold meaningful positions, but the broader category continues to operate alongside a large, unorganized base. Wilmar International is expected to complete the acquisition of Adani Group’s full stake in AWL Agri Business in 2025, reinforcing its direct commitment to staples, edible oils, and related food categories in India. AWL is also expected to acquire GD Foods in March 2025, indicating that large players are expanding into adjacent food categories rather than remaining focused on a single staple line. ITC’s packaged foods business is projected to cross USD 2 billion in FY26, while Aashirvaad continues to support the company’s expansion into health-led and value-added staple extensions. As a result, the India staple food market is moving toward stronger branded scale, although loose and local trade still shapes a large share of total demand.

Competitive behavior is now divided between companies focused on scale and companies prioritizing brand-led margin improvement. LT Foods is expanding its domestic reach through a structured outlet expansion plan, highlighting the continued importance of physical distribution in staple categories. Marico is reducing its dependence on commodity-linked revenue and shifting more attention toward branded wellness foods, reflecting a similar focus on improving the quality of growth rather than only increasing volume. These developments show that the India staple food market rewards companies that can balance procurement strength with pricing power, portfolio depth, and stronger channel execution.

The largest opportunity remains in the unbranded middle tier, where many local millers and aggregators continue to play an important operational role but face financial constraints. Government initiatives focused on grain storage modernization and digital procurement reform may gradually formalize this part of the chain, creating opportunities for new branded businesses that compete through compliance and distribution rather than scale alone. QR-code traceability, improved forecasting, and more disciplined supply visibility can also help companies manage raw material volatility more effectively than firms that continue to rely on manual systems. Therefore, the India staple food market favors players that can combine sourcing discipline, processing reliability, and broad route-to-market capabilities across both retail and institutional demand.

India Staple Food Industry Leaders

ITC Limited

Wilmar International Limited

KRBL Limited

LT Foods Limited

Marico Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: KRBL Limited had launched India Gate Poha under its India Gate brand, marking its first expansion beyond basmati rice into everyday kitchen staples. The product had targeted India’s poha market, where branded products accounted for only 2.2 lakh metric tons, highlighting significant headroom for branded conversion. The launch phase had covered Delhi-NCR, Uttar Pradesh, and Punjab, with Madhya Pradesh and Chhattisgarh in the pipeline.

- April 2026: KRBL launched India Gate Uplife Lite Everyday Low-GI Rice, targeting blood sugar management and sustained energy release. The launch marked the company’s first entry into the premium functional-food rice segment under its Uplife brand portfolio.

- January 2026: Wilmar International finalized its acquisition of Adani Group’s remaining 31.06% stake in AWL Agri Business (formerly Adani Wilmar) for approximately USD 2 billion (approximately SGD 2 billion), making AWL a Wilmar subsidiary. Wilmar stated that it intended to consolidate AWL’s leadership in edible oils while accelerating the growth of its food staples portfolio, which included wheat flour, rice, pulses, and soya nuggets, across rural and institutional segments.

India Staple Food Market Report Scope

A staple food is a basic, everyday food that makes up the dominant part of a population's diet. The India staple food market is segmented by product type, product format, and distribution channel. By product type, the market is segmented into Grains and cereals, flours, pulses and legumes, edible oils, sugar and sweeteners, spices and condiments, and other staple foods. The grains segment is further sub-segmented into rice, wheat, millets, maize, and other coarse cereals. The flours segment is further sub-segmented into whole wheat flour (atta), maida, rice flour, and other flour types. The pulses and legumes segment is further sub-segmented into tur and arhar dal, chana dal, moong dal, masoor dal, and other pulses and legumes. Similarly, the edible oil segment is further sub-segmented into mustard oil, palm oil, soybean oil, groundnut oil, and other edible oils. By product format, the market is segmented into raw/unprocessed and processed. By distribution channel, the market is segmented into institutional/foodservice and retail. The retail segment is further sub-segmented into online and offline. The Market Forecasts are Provided in Terms of Value (USD) and Volume.

| Grains and Cereals | Rice |

| Wheat | |

| Millets | |

| Maize | |

| Other Coarse Cereals | |

| Flours | Whole wheat flour (Atta) |

| Maida | |

| Rice Flour | |

| Other Flour Types | |

| Pulses and Legumes | Tur and Arhar Dal |

| Chana Dal | |

| Moong Dal | |

| Masoor Dal | |

| Other Pulses and Legumes | |

| Edible Oils | Mustard Oil |

| Palm Oil | |

| Soybean Oil | |

| Groundnut Oil | |

| Other Edible Oils | |

| Sugar and Sweeteners | |

| Spices and Condiments | |

| Other Staple Foods |

| Raw/Unprocessed |

| Processed |

| Institutional/Foodservice | |

| Retail | Online Retail |

| Offline Retail |

| Product Type | Grains and Cereals | Rice |

| Wheat | ||

| Millets | ||

| Maize | ||

| Other Coarse Cereals | ||

| Flours | Whole wheat flour (Atta) | |

| Maida | ||

| Rice Flour | ||

| Other Flour Types | ||

| Pulses and Legumes | Tur and Arhar Dal | |

| Chana Dal | ||

| Moong Dal | ||

| Masoor Dal | ||

| Other Pulses and Legumes | ||

| Edible Oils | Mustard Oil | |

| Palm Oil | ||

| Soybean Oil | ||

| Groundnut Oil | ||

| Other Edible Oils | ||

| Sugar and Sweeteners | ||

| Spices and Condiments | ||

| Other Staple Foods | ||

| Product Format | Raw/Unprocessed | |

| Processed | ||

| Distribution Channel | Institutional/Foodservice | |

| Retail | Online Retail | |

| Offline Retail | ||

Key Questions Answered in the Report

What is the 2026 value of the India staple food market?

The India staple food market was valued at USD 61.32 billion in 2026 and is projected to reach USD 85.72 billion by 2031 at a 6.93% CAGR.

Which product type leads staple food sales in India?

Grains and Cereals led product type demand with a 44.71% share in 2025, supported by the central role of rice and wheat in both household and welfare consumption.

Which product type is growing the fastest in India staple foods?

Pulses and Legumes are projected to grow the fastest, with an 7.96% CAGR through 2031, supported by broader protein-focused eating habits and category diversification.

Why are branded staples gaining ground over loose staples in India?

Branded staples offer better hygiene, pack consistency, traceability, and margin structure, which supports both consumer trust and distributor preference.

Page last updated on: