India Specialty Oil Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

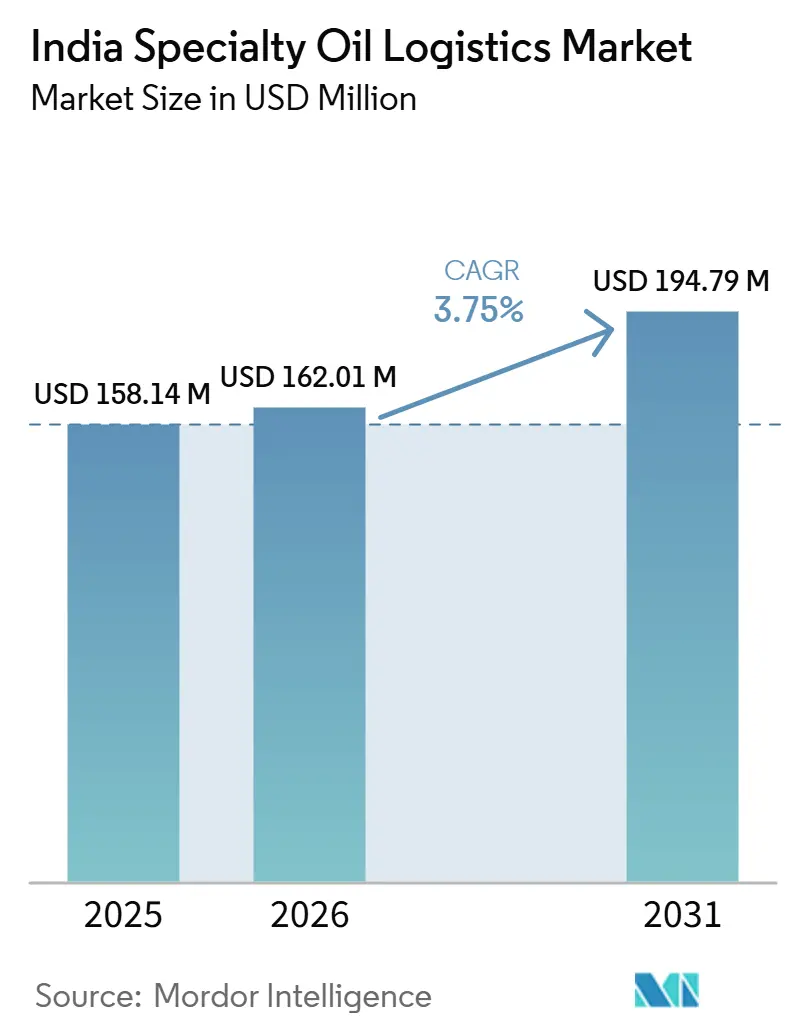

| Base Year Market Size (2025) | USD 158.14 Million |

| Market Size (2026) | USD 162.01 Million |

| Market Size (2031) | USD 194.79 Million |

| Growth Rate (2026 - 2031) | 3.75% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Specialty Oil Logistics Market Analysis by Mordor Intelligence

The India specialty oil logistics market size is expected to increase from USD 158.14 million in 2025 to USD 162.01 million in 2026 and reach USD 194.79 million by 2031, growing at a CAGR of 3.75% over 2026-2031.

The India specialty oil logistics market is being supported by steady underlying demand, since India’s lubricant and specialty fluid consumption reached 4.83 million tons in 2025, up 9.40% year over year, while base oil imports exceeded 3.00 million tons, up 11.00% from the prior year. This keeps port receipt, inland haulage, storage, and handling activity active even when broader freight demand is uneven. The India specialty oil logistics market is also moving beyond basic transportation, as shippers increasingly look for compliant storage, repacking, relabeling, inventory control, and product segregation in the same contract. Demand is strongest where grid expansion, pharmaceutical production, personal care output, and industrial machining create recurring movement of transformer oils, white oils, and process oils. The India specialty oil logistics market remains moderately fragmented, and its growth path is shaped by rising multimodal options on one side and by port congestion, freight disruption, and a still-fragmented tanker base on the other.

Key Report Takeaways

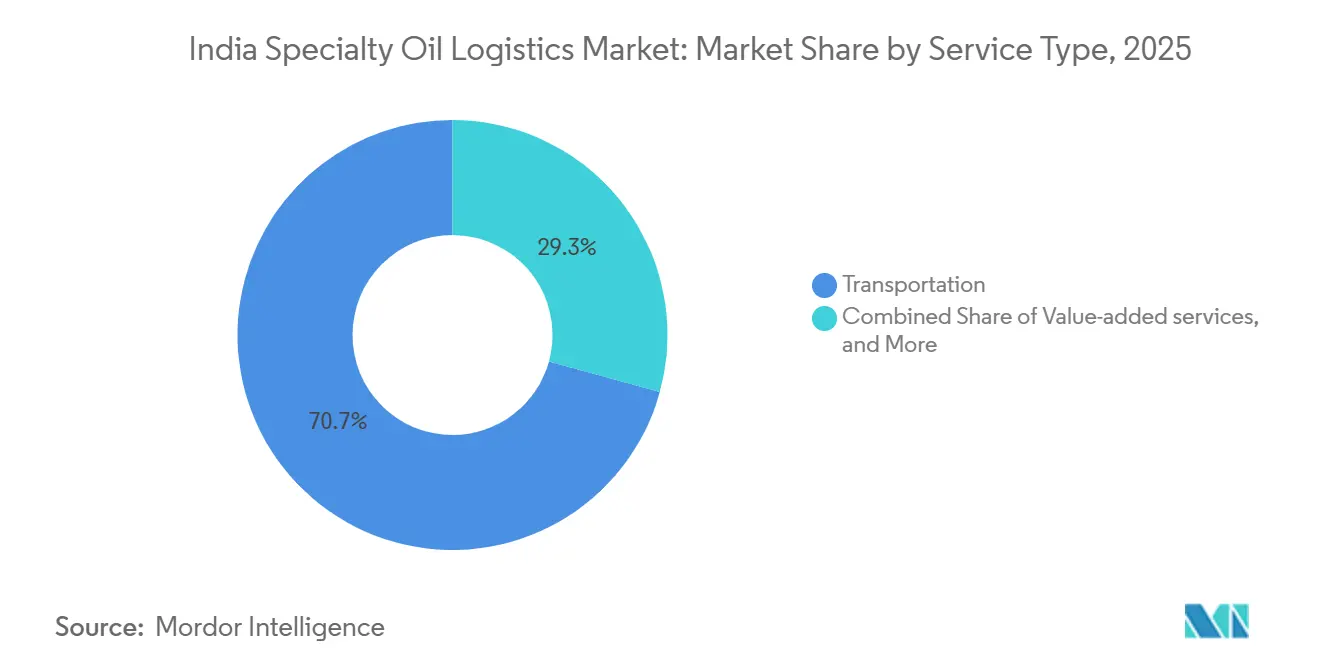

- By service type, transportation held 70.72% of the India specialty oil logistics market share in 2025, while value-added services are forecast to grow at a 5.24% CAGR through 2031.

- By transportation mode under the service type category, road transport accounted for 78.08% of freight movement in the India specialty oil logistics market size in 2025, while multimodal transport is projected to record the highest CAGR at 4.96% through 2031.

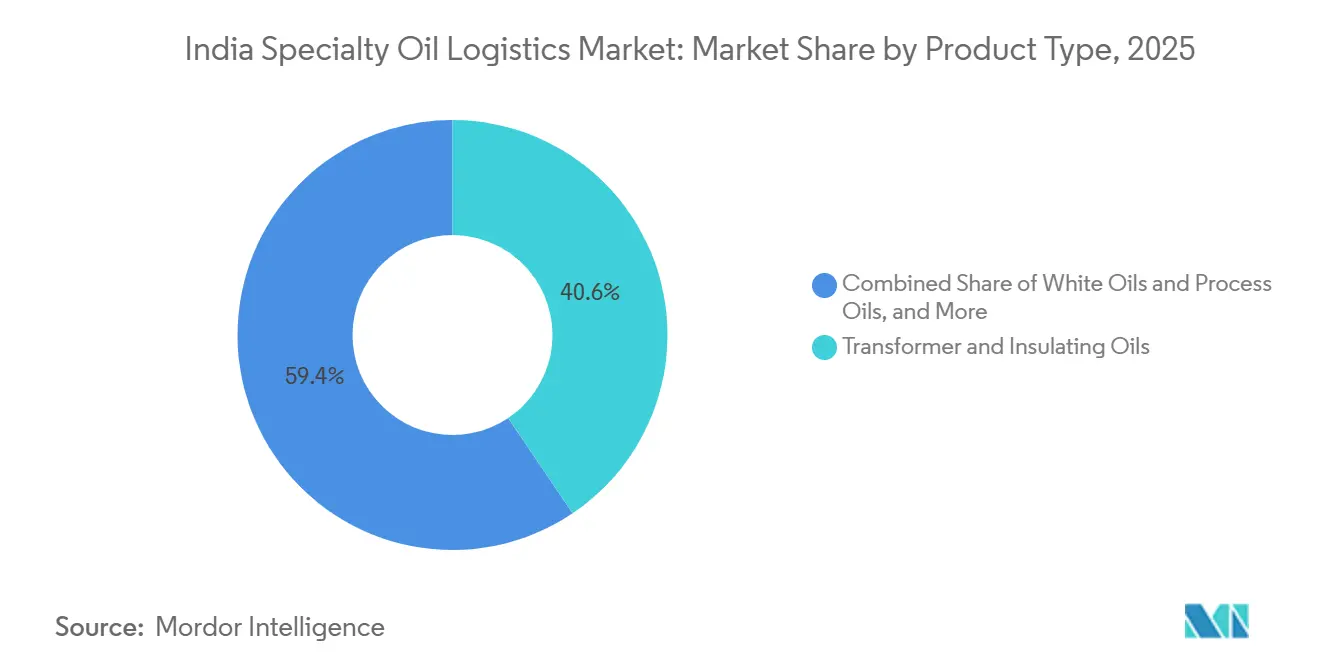

- By product category, transformer and insulating oils captured 40.57% of the India specialty oil logistics market in 2025, while white oils and process oils are expected to grow at a 5.01% CAGR through 2031.

- By handling/shipment format, drums accounted for 45.45% of the India specialty oil logistics market in 2025, while IBCs are forecast to expand at a 4.68% CAGR through 2031.

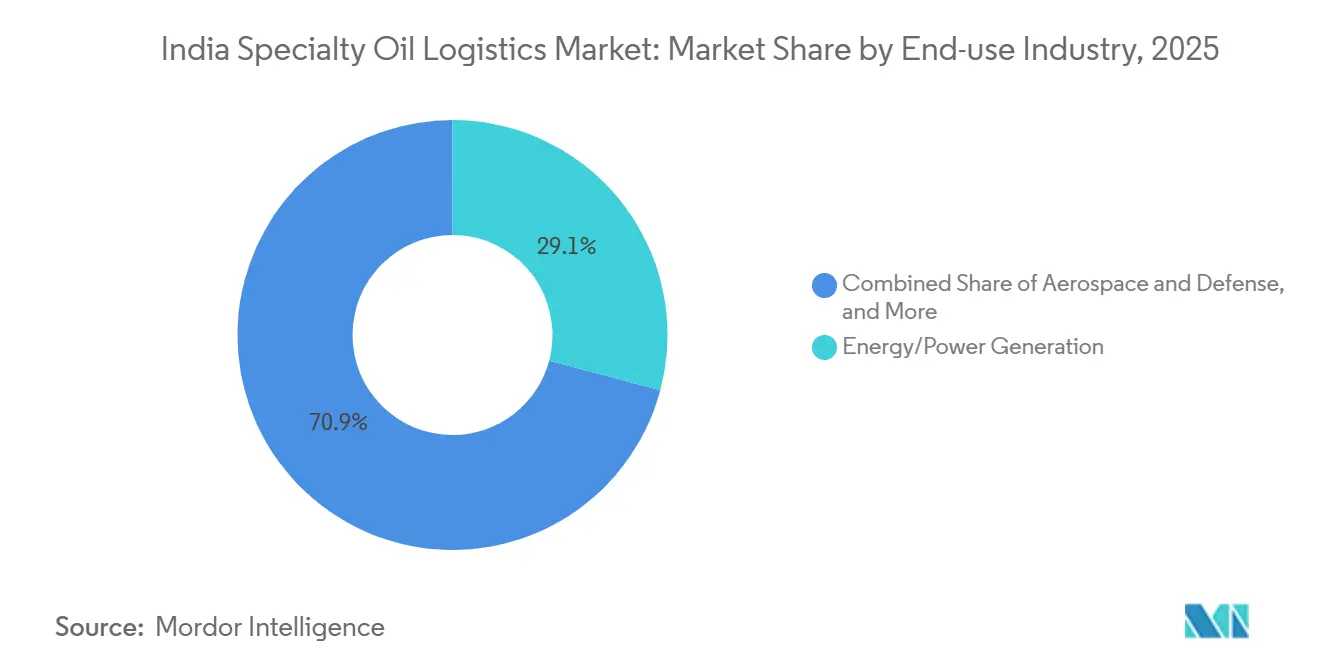

- By end-use industry, energy/power generation accounted for 29.13% of the India specialty oil logistics market in 2025, while personal care and pharmaceuticals are projected to grow at a 5.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Specialty Oil Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industrial lubricant and specialty fluid demand expansion | +1.10% | National, concentrated in Gujarat, Maharashtra, Tamil Nadu, and Uttar Pradesh industrial corridors | Short term (≤ 2 years) |

| Base oil import dependence sustaining port to inland bulk movements | +0.85% | West coast ports including Kandla, JNPT, and Mumbai, with inland spillover to Delhi-NCR, Pune, and Chennai | Short term (≤ 2 years) |

| Compliant storage and handling needs rising for high value specialty fluids | +0.65% | National, with early gains in Gujarat PCPIR, the Vizag petrochemical belt, and the Pune pharma cluster | Medium term (2-4 years) |

| Used oil EPR formalizing reverse logistics networks | +0.45% | National, with stronger regulatory pull in Maharashtra, Tamil Nadu, and Haryana | Medium term (2-4 years) |

| DFC led multimodal corridors improving inland liquid movement economics | +0.55% | Eastern DFC and Western DFC, with spillover toward the planned East Coast corridor | Medium term (2-4 years) |

| Expansion of OEM-approved and premium branded lubricant distribution networks | +0.35% | National, with stronger pull in Maharashtra and Gujarat, Karnataka, and Tamil Nadu automotive manufacturing clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Industrial Lubricant and Specialty Fluid Demand Underpins Volume Growth

India’s lubricant consumption reached 4.83 million tons in 2025, up 9.40% year over year, and that volume increase directly widened the freight and storage base available to service providers in the India specialty oil logistics market. More finished lubricant and specialty fluid output means more shipments to OEMs, industrial plants, workshops, and retail channels. The product mix is also shifting, as industrial and specialty fluids are gaining weight even as automotive lubricants face pressure from the adoption of electric vehicles. That shift matters because metalworking fluids, transformer oils, and food and pharma grade oils need tighter handling standards, cleaner equipment, and stronger documentation. Castrol India’s FY2025 revenue reached a record INR 5,722 crores (USD 636.84 million), and its distribution network covered 150,000 outlets, underscoring how broader channel reach drives recurring logistics demand across India's specialty oil logistics market.

Base-Oil Import Dependence Generates Sustained Port-to-Inland Corridor Demand

The India specialty oil logistics market continues to depend on import-led movement because domestic production does not fully cover demand for key base oils, especially naphthenic grades used in transformer and insulating oils. Base oil imports crossed 3.00 million tons in 2025, which kept liquid bulk reception, tank storage, and inland dispatch active across the main import corridors. South Korea supplied 1,322,161 tons, while Malaysia’s shipments rose sharply, which reinforced the importance of west coast ports in the India specialty oil logistics market. This import pattern creates two practical inland systems, one centered on Kandla for road tanker dispatch to northern and western blending hubs, and another centered on JNPT and Nhava Sheva with stronger multimodal potential. Even if new domestic lube capacity comes online, the India specialty oil logistics market will still see fresh short-haul movement between new complexes, downstream distributors, and industrial customers[1]"India's Base Oil Imports Rise by 11pc in 2025." Argus Media, argusmedia.com.

Compliant Storage and Handling Needs Rising for High-Value Specialty Fluids

The India specialty oil logistics market is seeing stronger demand for storage and handling that goes beyond simple tank-to-tank transfer. Transformer oils, white oils, and process oils often need dedicated tanks, contamination control, product segregation, batch traceability, and clean filling or repacking conditions. This is encouraging asset owners to expand liquid storage and terminal capacity near major gateways. Aegis Logistics moved ahead with a 318,100 cubic meter liquid products facility at JNPA under the J2 project framework in November 2025, which reflects the scale of investment being made around compliant liquid handling. The market is benefiting from this shift because customers in power, pharma, personal care, and chemicals increasingly prefer providers that can combine storage, documentation, quality segregation, and last-mile dispatch in one operating model.

Used-Oil EPR Formalizes Reverse Logistics Networks

The used-oil EPR framework is pushing a formal structure into a part of the India specialty oil logistics market that had long relied on informal collection. Producers and importers now need documented movement, traceable pickup, and clearer chain-of-custody for used oil flows. That changes the role of logistics providers because reverse movement becomes a compliance function, not just a transport task. Organized operators are better placed to manage route planning, documentation, and recycler linkage under this model. The transition is still uneven, but the India specialty oil logistics market is likely to gain a more formal reverse-logistics layer as compliance obligations deepen across the forecast period[2]"Extended Producer Responsibility (EPR) for Used Oils — FAQs-Based Article." TaxTMI, taxtmi.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported base oil and freight volatility pressuring logistics costs | -0.65% | National, amplified at west coast import ports and inland blending clusters | Short term (≤ 2 years) |

| Fragmented tanker ecosystem limiting network standardization | -0.45% | National, most acute in eastern India and tier 2 and tier 3 industrial towns beyond DFC reach | Medium term (2-4 years) |

| Hazardous waste compliance burden slowing informal channel conversion | -0.30% | National, with higher pressure in Uttar Pradesh, Rajasthan, and Bihar | Medium term (2-4 years) |

| Port and terminal congestion during import surges | -0.35% | West coast including JNPT and Kandla, with spillover to Chennai during east coast import peaks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Imported Base-Oil and Freight Volatility Creates Margin Pressure Throughout the Chain

The India specialty oil logistics market remains exposed to imported feedstock and freight volatility because so much of the value chain depends on seaborne base oil arrivals. When import costs and freight rates rise together, landed costs move up quickly and the pressure spreads to storage, road movement, and delivery scheduling. This matters because many domestic haulage contracts are fixed for a period and cannot be repriced quickly. In 2026, Gulf conflict rerouting contributed to congestion at Jawaharlal Nehru Port and forced the Ministry of Ports, Shipping, and Waterways to hold an emergency session with liquid bulk importers[3]"Govt Lines Up Fresh Coastal Shipping, Waterways Push with New Incentive Scheme." Maritime Gateway, maritimegateway.com. The result is tighter margin management and less planning certainty across the India specialty oil logistics market during import-heavy periods.

Fragmented Tanker Ecosystem Caps Network Standardization

The India specialty oil logistics market still relies on a large number of small tanker operators, especially in road freight. This makes national network standardization difficult because fleet quality, documentation, driver capability, and telematics adoption can vary sharply from one corridor to another. Shippers that need PESO-compliant movement for transformer oil, white oil, and process fluids often cannot source the same service standard across all regions. That limits their ability to consolidate volumes with a single provider and weakens service predictability in eastern India and in smaller industrial towns. The slow shift toward organized hazmat transport is keeping the India specialty oil logistics market more fragmented than many adjacent chemical logistics segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Value-Added Services Gaining Ground on Core Transportation

Transportation held 70.72% of the India specialty oil logistics market share in 2025, which shows how strongly the sector still depends on physical movement between ports, plants, terminals, and end users. The India specialty oil logistics market has historically been shaped by bulk movement economics, so transportation remains the base layer of most customer contracts. Road tankers, line-haul planning, and port-to-plant transfer still absorb the largest part of logistics spend. That pattern is unlikely to disappear, because base oil imports, inland blending, and downstream delivery continue to define the operating rhythm of the market.

Value-added services, however, are growing faster than the core transport layer and are forecast to expand at a 5.24% CAGR through 2031. This reflects a change in customer preference inside the India specialty oil logistics market, where simple freight execution is no longer enough for many accounts. Pharmaceutical, personal care, and specialty industrial users increasingly request inventory management, repacking, relabeling, quality segregation, and order-specific kitting within a single workflow. Warehousing and distribution remain the middle layer that connects import receipt with final dispatch, and operators are scaling those assets to improve service depth. Aegis Logistics’ terminal expansion at JNPA shows that liquid storage is being built ahead of future demand, not just to support current throughput. As a result, the India specialty oil logistics market is gradually shifting from an asset-only model toward a more integrated service model with better customer retention and higher revenue per ton.

By Product Category: Transformer Oil Logistics Reshaped by Grid Expansion Scale

Transformer and insulating oils accounted for 40.57% of the India specialty oil logistics market size in 2025, making them the largest product category by a wide margin. This leadership is closely tied to the pace of grid investment and transformer deployment across India. The Economic Times reported that India’s power transmission sector is set to receive INR 9.00 trillion in capex through 2032, giving this product segment a strong demand base. Power Line Magazine also noted that India must add 776,330 MVA of transformer capacity by FY2027, which supports continued movement of insulating oils between import points, blending locations, transformer manufacturers, and project sites.

White oils and process oils are the fastest-growing product segment, with a 5.01% CAGR projected for 2026-2031. In the India specialty oil industry, this growth is being supported by rising pharmaceutical and personal care manufacturing, where product purity and handling discipline matter more than in standard bulk fluid chains. APAR Industries supplies pharmaceutical- and food-grade white oils under its POWEROIL PEARL brand and exports to more than 125 countries, underscoring the need for inbound sourcing and tightly managed outbound dispatch. Metalworking and process fluids also remain important in machining clusters across Maharashtra, Tamil Nadu, and the broader automotive belt. According to research, the automotive metal forming sector is advancing in a fast pace, which supports stable movement of industrial oils and fluids. Taken together, these patterns show that the India specialty oil logistics market is led by grid-linked oils today, while higher-value white oil and process oil flows are becoming more important to future growth.

By Handling / Shipment Format: IBC Adoption Reshaping Mid-Tier Industrial Distribution

Drums held 45.45% of the India specialty oil logistics market in 2025, which reflects their long-established role in workshop, plant, and distributor-level handling. The India specialty oil logistics market still depends on drums because they suit smaller order sizes, are easy to stack and count, and fit mixed-load distribution. Many industrial users continue to buy specialty fluids in standard 210-litre units because consumption is spread across multiple sites and product types. This keeps drum handling central in sectors such as metalworking, maintenance fluids, greases, and smaller-batch process oil demand.

IBCs are gaining ground and are forecast to grow at a 4.68% CAGR through 2031. In the India specialty oil logistics market, IBCs appeal to industrial buyers that want fewer handling points and better unit economics on larger repeat orders. This format works especially well where customers need cleaner dispensing, easier internal movement, and stronger batch visibility than drums typically provide. The shift also changes warehouse design because cage racking, forklift handling, container return flow, and controlled filling become more important. Bulk liquid continues to serve the largest transformer oil movements, while the smallest pack formats support automotive retail and personal care channels. At the same time, the India specialty oil logistics market is seeing more specialized filling activity near JNPT free trade and warehousing zones, where operators such as Amfico support drum and IBC handling for hazardous and specialty liquids.

By End-use Industry: Power Generation Anchors Volume, Pharma Drives Margin Expansion

Energy and power generation accounted for 29.13% of the India specialty oil logistics market in 2025, making it the largest end-use segment. This reflects the scale of transformer deployment, grid reinforcement, and routine maintenance demand across the power system. The peak demand could reach 459 GW by 2035-36, which implies ongoing expansion of supporting electrical assets. Every new transformer, substation, and related grid asset supports first-fill and maintenance demand for insulating oils, which keeps movement recurring rather than one-time.

Personal care and pharmaceuticals are the fastest-growing end-use segment, with a 5.18% CAGR projected through 2031. This part of the India specialty oil logistics market benefits from the need for white oils and process oils that move under stricter quality and documentation conditions. Automotive, heavy equipment, mining and construction, and steel and metal machining remain major volume users, and they keep baseline demand stable when industrial activity is firm. Food and beverage, rubber and tire manufacturing, and aerospace and defense are smaller in scale but more specialized in handling needs. This mix means the India specialty oil logistics market is anchored by grid-linked volume while pharma and personal care help improve margin quality and service complexity.

Geography Analysis

Western India remains the main operating center of the India specialty oil logistics market because Gujarat and Maharashtra combine import terminals, blending assets, petrochemical clusters, and large industrial demand centers. Kandla and JNPT handle a large share of inbound base oil flow, which makes the west coast the first point of control for much of the country’s specialty oil movement. The region also benefits from strong downstream consumption in Dahej, Hazira, Vadodara, Mumbai, Pune, and nearby industrial belts. Aegis Logistics is adding 61,000 kL of liquid capacity at Mumbai and is commissioning 318,100 cubic meters at JNPA by Q1 FY2027, which shows that terminal operators are expanding liquid infrastructure where demand is most concentrated. This also means the India specialty oil logistics market carries concentrated port risk in the west, as seen when JNPT faced congestion in May 2026 after war-led cargo rerouting.

Southern India is the second major geography in the India specialty oil logistics market because it brings together transformer demand, pharmaceutical manufacturing, and a growing base of advanced logistics infrastructure. Chennai remains important for lube and specialty fluid movement, while Hyderabad and Bengaluru support demand for white oils and regulated industrial inputs. IOCL’s integrated lube complex in Manali, Chennai entered trial operations and is expected to shift regional movement patterns by linking pipeline-fed inputs with inland and coastal dispatch. Lubrizol also described its Aurangabad additives plant as its second-largest globally, which reinforces the region’s role in specialty fluid supply chains. The India specialty oil logistics market in the south is therefore becoming stronger not only because of end demand, but also because manufacturing assets and compliant logistics facilities are being added close to each other.

Northern and eastern India form the next growth frontier for the India specialty oil logistics market, supported by dense industrial consumption and improving freight links. Delhi-NCR, Haryana, and Uttar Pradesh absorb significant volumes of industrial lubricants and specialty fluids that move from western ports and blending centers. The Western DFC improves this corridor, while future eastern connectivity could reduce cost and transit pressure for long-haul movement[4]"Dedicated Freight Corridor Records 48% Surge in Train Operations in 2024-25." The Hindu Business Line, thehindubusinessline.com. Om Logistics secured land for a INR 150.00 crores (USD 16.69 million) logistics hub in Unnao, which points to a recognized capacity gap in the Uttar Pradesh corridor. Eastern India still has a wider role for unorganized operators, especially in metalworking fluid and industrial lubricant delivery to steel, mining, and heavy industry clusters. That leaves room for organized providers with compliant tanker fleets to gain share as the India specialty oil logistics market becomes more service-driven.

Competitive Landscape

The India specialty oil logistics market is moderately fragmented, with no single provider holding a dominant position across all service types, product categories, and corridors. Organized national operators compete with global contract logistics firms, while a large tail of smaller tanker businesses still handles a meaningful share of road-based movement. The main names visible in the India specialty oil logistics market include Transport Corporation of India, Container Corporation of India, Ltd., AllCargo Logistics Pvt. Ltd., AEGIS Logistics, Den Hartogh Logistics, VRL Logistics, CJ Darcl, DHL Supply Chain, Kuehne+Nagel, DSV, etc. Their roles differ: some are stronger in transport networks, others in contract logistics, and others in terminal infrastructure. This keeps pricing, service scope, and regional strength uneven across the India specialty oil logistics market.

Strategy is increasingly tied to specialization rather than simple fleet scale. VRL Logistics ordered 500 new commercial vehicles in Q3 FY2026, demonstrating continued investment in transport capacity even as the market demands higher service quality. Transport Corporation of India planned to add 2 coastal vessels for delivery in 2026, which supports a broader multimodal approach for high-margin freight lanes. CJ Darcl has focused on safety systems, including Advanced Driver Assistance Systems and Driver Fatigue Monitoring Systems, and reported a 40.00% reduction in safety incidents. In the India specialty oil logistics market, those investments matter because specialty oil customers increasingly view compliance, visibility, and incident prevention as part of service quality, not as optional extras.

The strongest whitespace in the India specialty oil logistics market sits in compliant drum and IBC logistics for pharma-grade white oils, in reverse logistics for used oil under EPR, and in multimodal liquid corridors linked to DFC terminals. TCI Chemlog’s PESO-compliant setup with ISO tank and flexi-bag capability fits this direction, because customers need operators that can handle regulated liquid cargo with standardized processes. Aegis Vopak Terminals’ June 2025 IPO also showed that investors are willing to fund long-term liquid infrastructure in India, which supports the buildout side of the India specialty oil logistics market. Global firms are also widening their footprint, with DHL Group committing EUR 1.00 billion (USD 1.14 billion) in India by 2030 and Kuehne+Nagel expanding fulfillment capacity across major cities. That combination of infrastructure investment, technology adoption, and compliance capability is likely to define who gains ground in the India specialty oil logistics market over the next 5 years.

India Specialty Oil Logistics Industry Leaders

-

Container Corporation of India, Ltd.

-

AllCargo Logistics Pvt. Ltd.

-

AEGIS Logistics

-

Den Hartogh Logistics

-

Transport Corporation of India, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Kuehne+Nagel opened a new 3,500 sqm Container Freight Station near JNPA in Mumbai, CTPAT, AEO, and ISO certified with electric material-handling equipment and solar-powered lighting, enhancing specialty cargo handling at India's largest container port.

- January 2026: Aegis Logistics' subsidiary executed a INR 52.50 crore Framework Agreement with Aegis Vopak Terminals Limited for LPG rail loading infrastructure and a bottling plant at New Mangalore Port Authority, extending Aegis's liquid infrastructure network to a third major west coast port location.

- November 2025: DHL Group announced a EUR 1.00 billion investment program in India by 2030, including India's first DHL Health Logistics hub in Bhiwandi and an Electric Vehicle and Battery Logistics Center of Excellence in Chennai and Mumbai, investments that build compliant, specialty-grade logistics infrastructure directly relevant to specialty oil-adjacent categories.

- October 2025: Kuehne+Nagel announced a 100,000 sqm fulfilment centre expansion across 5 Indian cities, Gurgaon, Kolkata, Nagpur, Mumbai, and Rajpura, bringing its total India footprint to nearly 500,000 sqm and generating 1,500 jobs.

India Specialty Oil Logistics Market Report Scope

| Transportation | Road | Full-Truck-Load (FTL) |

| Less than-Truck-Load (LTL) | ||

| Rail | ||

| Multimodal Transport | ||

| Warehousing and Distribution | ||

| Value-added Services (Inventory management, Repacking, Relabeling, and Kitting etc.) |

| Transformer and insulating oils |

| White oils and process oils |

| Metalworking and process fluids |

| Other Product Categories |

| Bulk liquid |

| Intermediate Bulk Containers (IBCs) |

| Drums |

| Small Retail and Commercial (Bottles and Jerry Cans, Stand-up Pouches, Pails, Kegs, etc.) |

| Automotive and Transportation |

| Heavy Equipment, Mining and Construction |

| Steel and Metal Machining |

| Energy/Power Generation |

| Rubber and Tire Manufacturing |

| Personal Care and Pharmaceuticals |

| Food and Beverage Processing |

| Aerospace and Defense |

| Other End-user Industries |

| By Service Type | Transportation | Road | Full-Truck-Load (FTL) |

| Less than-Truck-Load (LTL) | |||

| Rail | |||

| Multimodal Transport | |||

| Warehousing and Distribution | |||

| Value-added Services (Inventory management, Repacking, Relabeling, and Kitting etc.) | |||

| By Product Category | Transformer and insulating oils | ||

| White oils and process oils | |||

| Metalworking and process fluids | |||

| Other Product Categories | |||

| By Handling / Shipment Format | Bulk liquid | ||

| Intermediate Bulk Containers (IBCs) | |||

| Drums | |||

| Small Retail and Commercial (Bottles and Jerry Cans, Stand-up Pouches, Pails, Kegs, etc.) | |||

| By End-use Industry | Automotive and Transportation | ||

| Heavy Equipment, Mining and Construction | |||

| Steel and Metal Machining | |||

| Energy/Power Generation | |||

| Rubber and Tire Manufacturing | |||

| Personal Care and Pharmaceuticals | |||

| Food and Beverage Processing | |||

| Aerospace and Defense | |||

| Other End-user Industries |

Key Questions Answered in the Report

What is the current size of the India specialty oil logistics sector?

The India specialty oil logistics market stood at USD 162.01 million in 2026 and is projected to reach USD 194.79 million by 2031 at a 3.75% CAGR.

Which service type leads in India specialty oil logistics?

Transportation remained the largest service type with a 70.72% share in 2025 because most specialty oil flows still depend on physical port-to-plant and plant-to-customer movement.

Which product category contributes the most to specialty oil logistics demand in India?

Transformer and insulating oils led with a 40.57% share in 2025, supported by continued grid investment and large planned additions in transformer capacity.

Why are white oils and process oils becoming more important in this space?

White oils and process oils are forecast to grow at a 5.01% CAGR through 2031 because pharmaceutical and personal care manufacturing need cleaner, more compliant, and better-segregated logistics.

What is the biggest structural challenge for logistics providers handling specialty oils in India?

The biggest challenge is fragmentation in the tanker ecosystem, since many corridors still depend on smaller operators and that slows standardization, compliance rollout, and national service consistency.

Page last updated on: