India Social Commerce Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

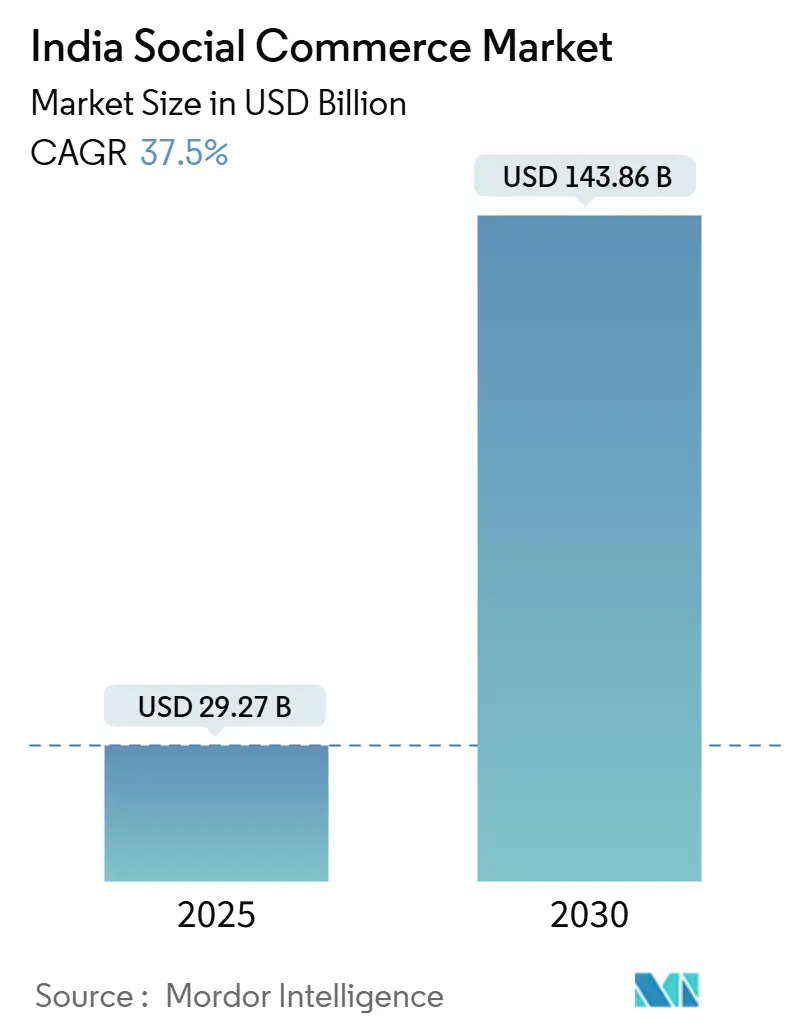

| Market Size (2025) | USD 29.27 Billion |

| Market Size (2030) | USD 143.86 Billion |

| Growth Rate (2025 - 2030) | 37.50% CAGR |

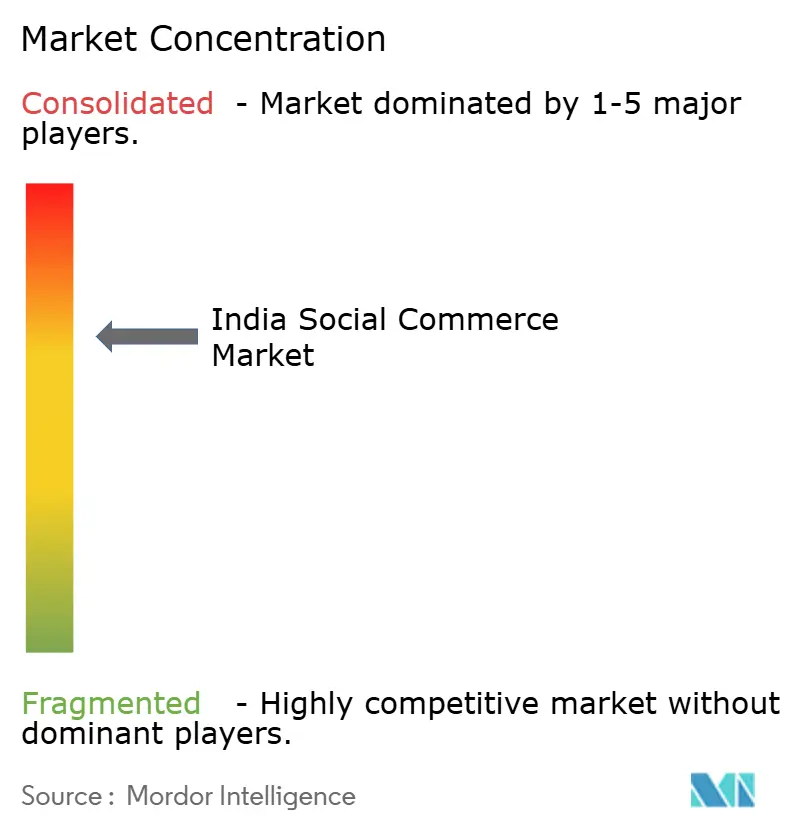

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Social Commerce Market Analysis by Mordor Intelligence

The India social commerce market size reached USD 29.27 billion in 2025 and is forecast to grow at a 37.5% CAGR to USD 143.86 billion in 2030, reflecting rapid adoption of digital payments, creator-led trust mechanisms, and mobile-first discovery behaviors. The government's zero-MDR policy on UPI transactions has removed processing fees, enabling the feasibility of micro-orders. UPI has experienced a notable increase in transaction volume. A significant share of new online shoppers is emerging from Tier-2 and Tier-3 cities, driven by the growing adoption of smartphones and increased consumption of vernacular content. These developments are fostering the expansion of India's social commerce market into non-urban areas. Interoperability on the Open Network for Digital Commerce (ONDC) has simplified market entry for smaller sellers. The platform has recorded 14 million transactions across over 616 cities, 13 active domains, 239 network participants, and more than 775,000 sellers and service providers. [1]PIB Delhi, “Revolutionizing Digital Commerce: The ONDC Initiative”, pib.gov.inVideo commerce is gaining prominence, while social reselling is experiencing significant growth, reflecting a shift toward peer-to-peer models that seamlessly integrate shopping into social interactions.

Key Report Takeaways

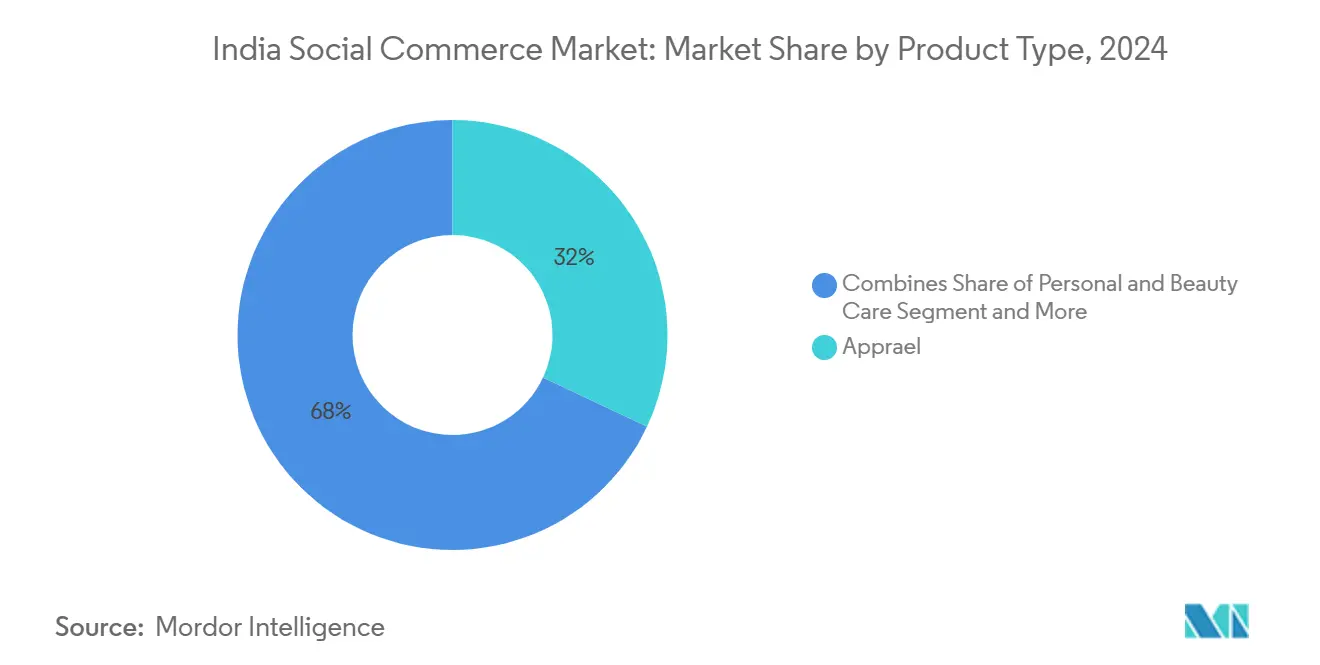

- By product type, apparel led with 31.57% revenue share in 2024, while personal and beauty care is projected to expand at a 39.31% CAGR through 2030.

- By device, smartphones commanded 89.77% share of the India social commerce market size in 2024 and are advancing at a 37.97% CAGR through 2030.

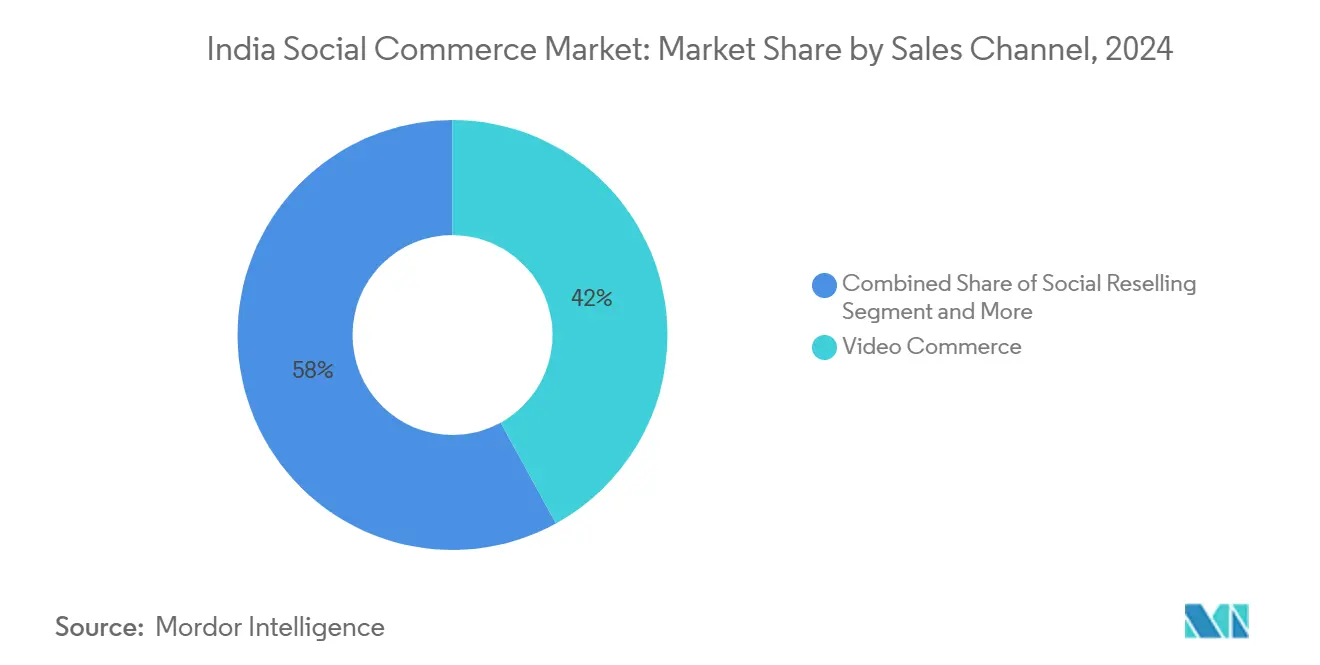

- By sales channel, video commerce accounted for 41.82% of the India social commerce market share in 2024, whereas social reselling is forecast to grow at a 38.17% CAGR between 2025 and 2030.

Worldwide, activity is shaped by contributions from multiple countries and regions, with India representing one among them. The global report on social commerce market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

India Social Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid UPI penetration and zero-MDR policy | +8.2% | National; strongest in urban centers | Short term (≤ 2 years) |

| Creator-economy trust flywheel | +7.5% | Tier-1 and Tier-2 cities, spreading to rural areas | Medium term (2-4 years) |

| Social-first discovery in Tier-2/3 markets | +9.1% | Tier-2, Tier-3, and rural regions | Medium term (2-4 years) |

| Short-form video conversion uplift | +6.8% | Nationwide; highest among Gen Z | Short term (≤ 2 years) |

| ONDC interoperability | +4.3% | National; MSME-dense states | Long term (≥ 4 years) |

| WhatsApp Business API scaling chat-commerce | +5.7% | National; faster uptake in smaller cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid UPI Penetration and Zero-MDR Policy

India's Unified Payments Interface (UPI) has become a critical component in the social commerce ecosystem, facilitating efficient and cost-effective digital transactions. In March 2025, UPI processed 18.3 billion transactions, amounting to ₹24.77 lakh crore, reflecting a 13.5% increase in transaction volume compared to the previous month.[2]DDNews, “UPI transaction volume up 13.5% in March, value at record Rs 24.77 lakh crore”, ddnews.gov.in This growth reduces payment-related barriers for micro-entrepreneurs and small vendors, enabling operations without incurring high gateway fees. The government's zero merchant discount rate (MDR) policy for UPI transactions has redefined the cost structure of social commerce by removing payment processing fees for small-value transactions. This policy enhances platform profitability on low-value orders and allows micro-entrepreneurs to process payments without fee-related deductions. The Reserve Bank of India (RBI) is actively promoting the adoption of point-of-sale (PoS) systems in smaller towns, where social commerce is still developing. Through initiatives like the Payments Infrastructure Development Fund, supported by substantial financial resources, the RBI is driving this expansion. For instance, rural kirana stores collaborating with social commerce platforms can now accept digital payments without additional costs, enabling their participation in group-buying and reseller networks that were previously limited to cash transactions. Additionally, UPI's interoperability simplifies integration with various payment providers, reducing technical challenges for new entrants and fostering advancements in embedded finance solutions.

The RBI's allocation of ₹500 crore from the Payments Infrastructure Development Fund to expand PoS devices in smaller towns further supports rural kirana stores in joining group-buying networks. UPI's interoperability enables social commerce applications to integrate multiple payment partners without added technical complexity, encouraging innovation in embedded finance. This development allows creators and small businesses to offer secure, instant payments within chat or app interfaces, enhancing platform engagement and contributing to the growth of India's social commerce market, which is valued at USD 8–10 billion.

Creator-Economy Trust Flywheel

Platforms such as Roposo illustrate the transformation of the creator economy into "creator-preneurship," where creators generate revenue through branded content, memberships, and live product launches. This model fosters trust through peer recommendations, which serve as a key driver for purchase decisions, resulting in higher conversion rates compared to traditional e-commerce discovery methods. The creator ecosystem is expanding significantly, with nano and micro-creators demonstrating strong conversion potential due to their close connections with audiences and perceived authenticity. For example, beauty and personal care brands collaborate with micro-influencers in smaller cities to showcase product usage through short-form videos, encouraging immediate purchase decisions and bypassing conventional decision-making processes. Revenue-sharing arrangements between creators and platforms further enhance this trust-based model. These arrangements reward creators based on actual sales rather than impressions, motivating them to endorse products they genuinely use. This structure strengthens the foundation of trust, which is critical for driving repeat purchases and increasing customer lifetime value within social commerce platforms.

Social-First Discovery Among Tier-2/3 Shoppers

Consumers in Tier-2 and Tier-3 markets exhibit distinct discovery behaviors compared to those in metropolitan areas, with a strong preference for social validation over traditional search-driven product research. These consumers rely significantly on community recommendations and peer endorsements. Additionally, the use of vernacular content has been increasing steadily as platforms adapt to local language preferences and cultural nuances. This social-first approach addresses the information gap often encountered by first-time online buyers in traditional e-commerce. In this context, community-driven models have emerged, where local entrepreneurs act as intermediaries, offering product education, managing fulfillment, and providing post-purchase support within their networks. The growing adoption of voice search among mainstream consumers further highlights a shift toward discovery mechanisms that align with social interaction patterns rather than text-based searches. This behavior, concentrated in specific geographic areas, creates a ripple effect. Successful adoption of social commerce in one community often accelerates adoption in neighboring areas through word-of-mouth and demonstration effects. This dynamic enables platforms to expand their reach efficiently while keeping customer acquisition costs relatively low.

WhatsApp Business API Enabling Chat-Commerce

India, with a substantial WhatsApp user base, is experiencing a notable shift toward chat-commerce, facilitated by the WhatsApp Business API. This integration enables businesses and small sellers to efficiently share catalogs, process payments, and track orders within a single chat interface. Platforms leveraging catalog sharing demonstrate the scalability of this model. For consumers in smaller cities, conversational commerce is particularly advantageous as it eliminates the need for multiple app installations while offering a familiar and accessible interface. Additionally, generative AI-powered auto-reply bots are helping small businesses reduce operational costs by managing routine queries and support tasks. Meta’s implementation of click-to-WhatsApp ads, combined with UPI-enabled payments, simplifies the checkout process, enhancing revenue generation. This integration of messaging, payments, and commerce underscores WhatsApp's role in advancing the social commerce ecosystem in India, enabling personalized engagement and expanding opportunities for micro-entrepreneurs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and quality-control challenges | -3.8% | Nationwide; higher risk in unregulated categories | Medium term (2-4 years) |

| Fragmented rural logistics | -4.2% | Rural and remote pin-codes | Long term (≥ 4 years) |

| Low average order value | -2.9% | Nationwide; heavier burden on new entrants | Short term (≤ 2 years) |

| Data-privacy concerns | -2.1% | Urban centers; educated demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and Quality-Control Challenges

Social commerce platforms face significant challenges related to product authenticity, which undermines consumer trust. Peer-to-peer selling models, in particular, lack the centralized quality control typically found in traditional e-commerce marketplaces. The presence of unverified sellers and resellers increases the likelihood of counterfeit products entering the supply chain. This issue is especially critical in the beauty and personal care sectors, where substandard cosmetics and skincare products pose safety risks. To address these concerns, social commerce platforms are allocating resources toward seller verification, product authentication technologies, and customer protection mechanisms. However, these measures lead to higher operational costs and impact profitability in the short term. For instance, adopting technologies such as blockchain for product tracking and AI for image-based authenticity verification requires substantial investment, affecting overall cost structures. The challenge is further compounded in Tier-2 and Tier-3 markets, where consumers often lack the experience to distinguish between genuine and counterfeit products. This can result in negative customer experiences, which harm the platform's reputation and reduce customer retention. Additionally, compliance with the Consumer Protection Act of 2019 obligates platforms to ensure product quality and authenticity. This creates additional costs and exposes platforms to legal and regulatory risks, which can be particularly burdensome for smaller social commerce entities with limited resources to manage these requirements effectively.

Fragmented Logistics in Rural Pin-Codes

In rural India, last-mile delivery infrastructure remains underdeveloped, as traditional logistics providers face challenges in reaching remote pin-codes. These areas are critical for social commerce platforms aiming to expand their customer base. The fragmented logistics network in these regions results in delivery delays, increased shipping costs, and inconsistent service quality, which undermine the convenience essential for social commerce adoption. Meesho's Valmo initiative, which incorporates regional micro-entrepreneurs into its logistics operations, highlights the complexities of addressing rural delivery challenges.[3]Singh, Manish, “Meesho taps micro-entrepreneurs to plug gaps in India’s supply chain network”, techcrunch.com A single shipment often requires coordination among multiple micro-entrepreneurs before reaching its final destination. While this approach has achieved cost efficiencies, the operational intricacies and coordination demands underscore the structural barriers to social commerce growth in underserved regions. Additional challenges, such as inadequate road infrastructure, limited transportation options, and seasonal accessibility issues, further exacerbate delivery uncertainties. These factors negatively impact customer satisfaction and increase return-to-origin costs for platforms. The fragmented logistics network particularly affects the distribution of perishable and time-sensitive goods, restricting the range of products that social commerce platforms can effectively offer in rural areas. This limitation hampers revenue growth opportunities in these high-potential segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Beauty Care Drives Premium Shift

The personal and beauty care segment is expanding at a 39.31% CAGR, almost matching the overall India social commerce market growth pace, while apparel maintains the largest 31.57% share. Smartphone-optimized try-on filters and creator tutorials are streamlining purchase decisions for serums, masks, and color cosmetics. Meesho's recent sales of face packs and press-on nails highlight the growing demand for cost-effective self-care kits. Increasing disposable incomes in smaller cities are encouraging a shift towards premium products, with imported K-beauty lines entering the market through community-based resellers. To address counterfeit risks and enhance customer trust, authenticity programs with QR-based verification are being introduced. Home products and health supplements are achieving significant growth, supported by live demonstrations that provide clarity on product usage and build consumer confidence. In contrast, food and beverages face challenges due to regulatory compliance complexities, though regional snack brands are effectively using group buying to connect with diaspora communities. Accessories, due to their lightweight nature and ease of sharing on social platforms, are performing well in flash-sale formats. Although smaller in scale, categories like pet care and books are expanding rapidly, reflecting a shift in consumer preferences beyond traditional product categories.

The social commerce market in India for personal and beauty care is expected to grow substantially in the coming years. While the share of apparel within the market may see a slight decline due to a broader category mix, overall revenue from apparel is anticipated to increase significantly as the market expands. Video-led content, such as “get ready with me” streams, is fostering the adoption of premium skincare routines. Additionally, nano-creators from smaller cities are driving the discovery of Ayurvedic brands by leveraging their local credibility. Brands that customize packaging and instructions in regional languages, such as Gujarati, Marathi, and Kannada, are experiencing improved conversion rates and reduced return rates.

By Device: Smartphone-Centric Adoption Accelerates

Smartphones held an 89.77% revenue share in 2024 and are forecast to grow at a 37.97% CAGR. Smartphones priced under USD 200 are now equipped with multicore processors, enabling smooth AR try-ons, which are becoming increasingly important for beauty and fashion consumers. The deployment of 5G has significantly reduced buffering, ensuring reliable HD livestreaming even in less urbanized areas, thereby enhancing viewer engagement. Voice commerce is expanding as platforms like WhatsApp and regional voice assistants support product searches in multiple local languages. Laptops and desktops remain essential for B2B resellers to manage bulk catalog uploads and oversee analytics across various stores, although their relevance in this context is expected to decline gradually.

The social commerce market in India, primarily driven by smartphone usage, is expected to grow substantially, emphasizing the importance of designing user experiences tailored for mobile devices. AI-powered auto-captioning is facilitating real-time translations, thereby broadening accessibility for bilingual audiences. Additionally, user-generated unboxing videos, created using smartphone cameras, are serving as a cost-effective advertising method by reducing reliance on traditional paid media. Hardware manufacturers are integrating commerce shortcuts into devices and collaborating with platforms to share revenue, further strengthening the role of smartphones in the distribution ecosystem.

By Sales Channel: Reselling Model Outpaces All Others

Video commerce accounted for a 41.82% share in 2024, leveraging algorithmic feeds that surface shoppable clips within seconds. Social reselling, though smaller, is surging at a 38.17% CAGR as homemakers and students monetize personal networks. Tier-3 households with a focus on cost savings are increasingly adopting group buying, where orders are combined to access factory-level discounts. Social network-driven commerce through platforms like Instagram Shops and Facebook Marketplace continues to provide visibility for branded catalogs but is experiencing slower growth compared to peer-driven models. Additionally, product review forums significantly influence purchasing decisions, particularly for high-value items such as electronics and health supplements.

The social commerce market in India is witnessing substantial growth, with video commerce emerging as a key driver. Social reselling is also expanding, supported by the introduction of affiliate dashboards that enable real-time tracking of seller earnings, enhancing transparency and motivation. In addition, Tier-3 resellers are addressing trust issues in last-mile deliveries by managing localized cash-on-delivery reconciliations. Content designed around entertainment is proving to be more engaging than static browsing, contributing to the increasing prominence of video commerce in the market.

Geography Analysis

Uttar Pradesh and Bihar, two northern states, are experiencing significant growth in user additions due to their large populations, increasing smartphone usage, and a cultural preference for community purchasing. Hindi-language content sees the highest engagement, driving the adoption of apparel and affordable beauty products. In the northeastern region, which includes Arunachal Pradesh, Assam, Manipur, Meghalaya, Mizoram, Nagaland, Tripura, and Sikkim, a substantial portion of orders is influenced by content created by micro-influencers, emphasizing their role in addressing cultural nuances. Karnataka records the highest density of transactions on the ONDC platform, followed by Delhi and Telangana, reflecting a positive response to evolving commerce frameworks.

In southern states such as Karnataka, Tamil Nadu, and Telangana, advanced features like voice search and augmented reality try-ons are widely utilized, showcasing the region's strong digital infrastructure. Maharashtra and Gujarat are prominent in B2B social commerce, with textile and jewelry manufacturers leveraging peer platforms to connect with retailers across the country. Emerging towns like Ambur, Rourkela, Sangli, and Zirakpur are demonstrating rapid repeat purchases in women's fashion and baby care, indicating increased customer retention as initial barriers to entry are reduced.

Rural areas represent a vast untapped opportunity, with a significant number of potential users. Government initiatives, including Digital India and ONDC-linked Common Service Centers, are addressing digital literacy challenges by providing shared devices and facilitating order placements. Numerous farmer-producer organizations and self-help groups are already engaging with ONDC buyer applications. Seasonal cash flow patterns influence purchasing behavior, prompting platforms to adjust inventory and financing options to align with agricultural cycles, thereby fostering customer loyalty. Consequently, the distribution of social commerce activity in India is expected to align more closely with the availability of regional content, logistical networks, and the presence of content creators, rather than traditional urbanization trends.

Mordor Intelligence provides coverage of the social commerce market across other key regional markets. Detailed country-level analysis extends to China, Brazil, Canada, and France incorporating local coverage and market participation, as required.

Competitive Landscape

Competition remains moderately fragmented. Meesho processes millions of WhatsApp-enabled catalog orders annually, with Built Valmo now managing 50% of those orders, reflecting a twofold increase compared to the previous year. Over the past year, the company’s logistics division has extended its coverage to approximately 15,000 pin codes, supported by a network of 6,000 logistics partners and contributing to the creation of 85,000 jobs as of December 2024.[4]Business Standard, “Meesho's logistics arm Valmo handles 50% of orders, doubling from last year”, business-standard.comCityMall secured USD 47 million in Series D funding in September 2025 to strengthen its private-label offerings in Tier-III and IV towns. DealShare focuses on bulk grocery purchases through gamified discount strategies. Concurrently, Flipkart's Shopsy integrates its supply chain with influencer-driven merchandising approaches. To maintain relevance in urban areas, Amazon and Myntra are experimenting with live commerce streams.

Technology plays a pivotal role in enhancing operations. Platforms utilize generative AI for efficient product tagging and language translation, enabling creators to upload shoppable videos quickly. Collaborations with logistics startups facilitate expedited deliveries across urban regions. Payment system integrations offer contextual credit options by leveraging UPI profiles for seamless KYC processes, which contribute to higher order values. Companies emphasizing vernacular languages concentrate on specific state languages and engage community moderators from local institutions to strengthen their presence.

Emerging opportunities include social commerce tailored for MSME wholesale, leveraging ONDC corridors for cross-border exports, and incorporating hyperlocal services such as repairs or installations during the checkout process. As the social commerce ecosystem in India develops, businesses that effectively combine trust, logistics, and credit within a single platform are well-positioned to achieve sustainable growth.

India Social Commerce Industry Leaders

Fashnear Technologies Private Limited (Meesho)

Amazon Retail India Private Limited

Flipkart Internet Private Limited (Shopsy.in)

Merabo Labs Private Limited (DealShare)

City Mall Commerce Private Limited (CityMall)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Myntra's GlamStream Fest, hosted in Mumbai, recorded attendance exceeding 10,000, featuring prominent brands and creators. The event combined live fashion showcases with influencer-driven engagement. By enabling real-time product discovery and interactive shopping, Myntra reinforces its role within the creator economy, a significant component of social commerce. These initiatives contribute to the growth of content-driven commerce and highlight India's expanding USD 8–10 billion social commerce market, demonstrating how brands utilize influencers and experiential marketing to enhance conversions.

- November 2025: Amazon has introduced Tez Quick Commerce, a platform that integrates rapid delivery with a social-driven approach to product discovery. This enables influencers and micro-sellers to promote products with swift delivery. The model supports impulse purchases and aligns social engagement with immediate fulfillment, reflecting a key trend in India's social commerce ecosystem. By combining convenience with community-focused commerce, Amazon aims to cater to mobile-first, time-sensitive consumers.

- September 2025: CityMall raised USD 47 million in Series D funding to expand delivery networks, launch private labels, and partner with national brands across Tier-III and IV markets.

- March 2025: Snapchat India has introduced 'Sponsored Snaps' for brands, integrating advertisements directly into user-generated content. This approach facilitates product discovery and consumer engagement within a social media environment. The initiative aligns with the increasing adoption of influencer-driven commerce and the preferences of mobile-first consumers in India. By combining advertisements with organic content, Snapchat aims to enhance conversion opportunities, reinforcing the role of social platforms in supporting the growth of social commerce in the region.

- December 2024: ONDC, through its subsidiary Nirmit Bharat, has introduced the DigiHaat buyer app to enhance digital commerce accessibility for micro-businesses and self-help groups. The initiative focuses on supporting sellers in rural and semi-urban regions by providing a localized, digital-first platform. DigiHaat integrates vernacular language support and hyperlocal commerce features to connect small businesses with online buyers, fostering inclusivity within India's social commerce ecosystem. This approach aligns with government-supported digitalization initiatives, enabling micro-entrepreneurs to utilize social networks for efficient product discovery and seamless transactions.

India Social Commerce Market Report Scope

The India social commerce market enables transactions directly on platforms like WhatsApp, Instagram, and Facebook, bypassing traditional brand websites. It gains traction in smaller cities (Tier 2 and 3) through models like reselling and group buying, driven by community trust. Growth is supported by increasing smartphone usage, digital payment systems like UPI, and shoppable content such as live videos and product tags.

The India Social Commerce Market Report is Segmented by Product Type (Apparel, Personal and Beauty Care, Accessories, Home Products, Health Supplements, Food and Beverages, Other Product Types), Device (Laptops and Desktops, Smartphone), Sales Channel (Video Commerce, Social Network-Led Commerce, Social Reselling, Group Buying/Team Purchase, Product Review and Discovery Platforms), and Geography (India). The Market Forecasts are Provided in Terms of Value (USD).

| Apparel |

| Personal and Beauty Care |

| Accessories |

| Home Products |

| Health Supplements |

| Food and Beverages |

| Other Product Types |

| Laptops and Desktops |

| Smartphone |

| Video Commerce |

| Social Network-Led Commerce |

| Social Reselling |

| Group Buying / Team Purchase |

| Product Review and Discovery Platforms |

| By Product Type | Apparel |

| Personal and Beauty Care | |

| Accessories | |

| Home Products | |

| Health Supplements | |

| Food and Beverages | |

| Other Product Types | |

| By Device | Laptops and Desktops |

| Smartphone | |

| By Sales Channel | Video Commerce |

| Social Network-Led Commerce | |

| Social Reselling | |

| Group Buying / Team Purchase | |

| Product Review and Discovery Platforms |

Key Questions Answered in the Report

How large will India’s social commerce GMV be by 2030?

Forecasts place the India social commerce market at USD 143.86 billion in 2030, expanding from USD 29.27 billion in 2025 on a 37.5% CAGR trajectory.

Which category is growing fastest on social platforms?

Personal and beauty care products are projected to grow at a 39.31% CAGR, outpacing all other segments thanks to video tutorials and creator endorsements.

What role does ONDC play in social commerce growth?

ONDC lowers entry barriers for 700,000+ sellers by providing open payment and logistics rails, enabling decentralized catalog access across 1,100+ cities.

Why are smartphones so dominant in social shopping?

Smartphones account for 89.77% of 2024 GMV because mobile apps integrate discovery, video, chat, and UPI payments in one seamless journey.

How do creators influence purchasing decisions?

Eighty percent of buyers cite trust in nano-influencers as their primary reason to purchase, driving conversion rates higher than search-based e-commerce.

What is the biggest operational hurdle for rural expansion?

Fragmented last-mile logistics in remote pin-codes adds cost and delivery uncertainty, tempering growth unless shared infrastructure scales quickly.

Page last updated on: