India Robotics CNC Turning Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

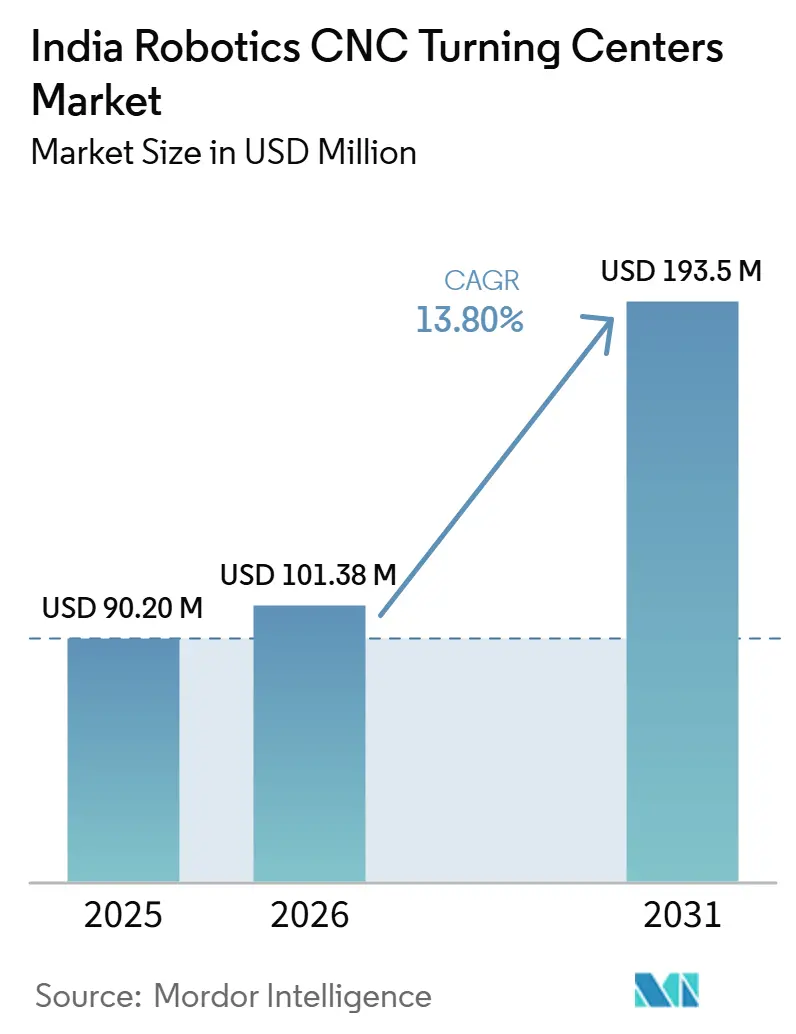

| Base Year Market Size (2025) | USD 90.20 Million |

| Market Size (2026) | USD 101.38 Million |

| Market Size (2031) | USD 193.5 Million |

| Growth Rate (2026 - 2031) | 13.80% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Robotics CNC Turning Centers Market Analysis by Mordor Intelligence

The India Robotics CNC Turning Centers Market size is expected to grow from USD 90.20 million in 2025 to USD 101.38 million in 2026 and is forecast to reach USD 193.5 million by 2031 at 13.80% CAGR over 2026-2031.

Policy support for capital goods, production-linked manufacturing, and smart factory adoption is lowering barriers to the adoption of automated turning systems across the India robotics CNC turning centers market. Industrial robot installations reached 9,123 units in 2024, and the broader automation base is supporting demand for CNC turning centers designed for automated loading and unloading. Domestic machine tool production rose from INR 6,152 crore (USD 684.7 million) in 2019-20 to INR 13,571 crore (USD 1.5 billion) in 2023-24, which shows that the local supply base is strengthening alongside demand. Competition remains fragmented, and vendors that can combine precision, automation readiness, retrofit support, and local service coverage are best placed to capture opportunity in the India robotics CNC turning centers market while managing import dependence, skill gaps, and India's still-low automation intensity relative to global leaders.

Key Report Takeaways

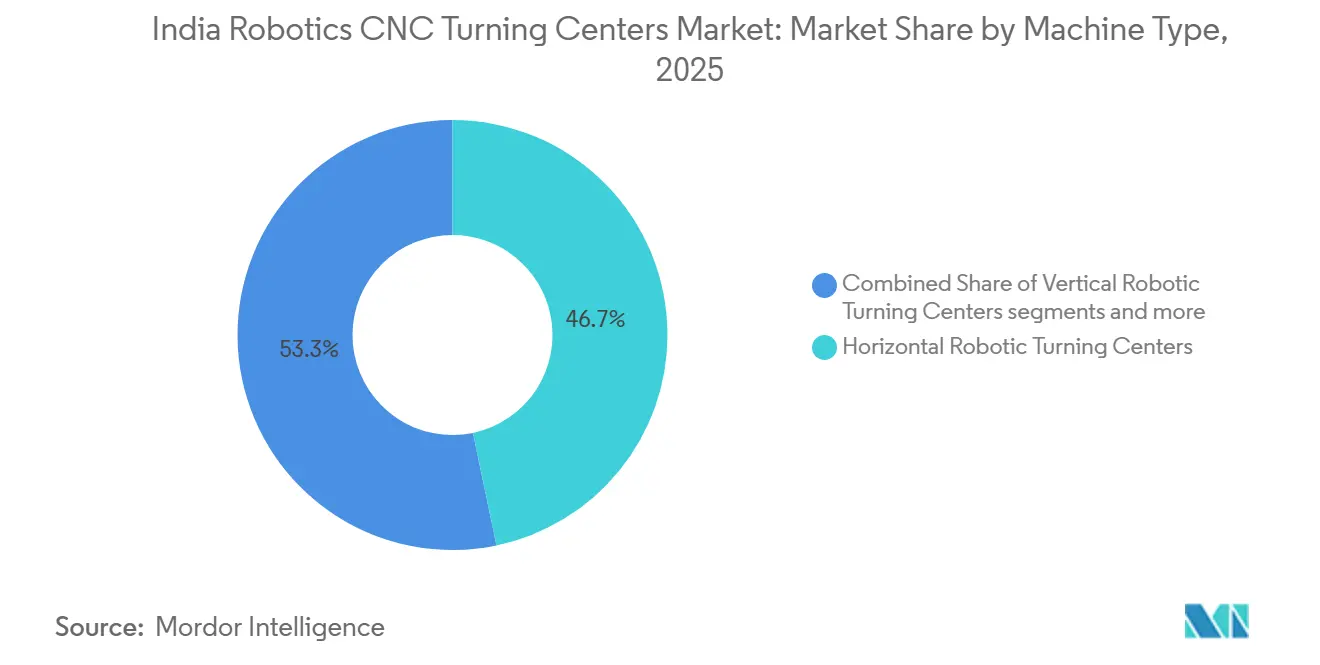

- By machine type, horizontal robotic turning centers held 46.7% of the India robotics CNC turning centers market share in 2025, while multi-tasking robotic turning centers are projected to grow at a 14.1% CAGR through 2031.

- By robot type, articulated robots accounted for 56.2% of the India robotics CNC turning centers market size in 2025, while collaborative robots are set to expand at a 15.8% CAGR through 2031.

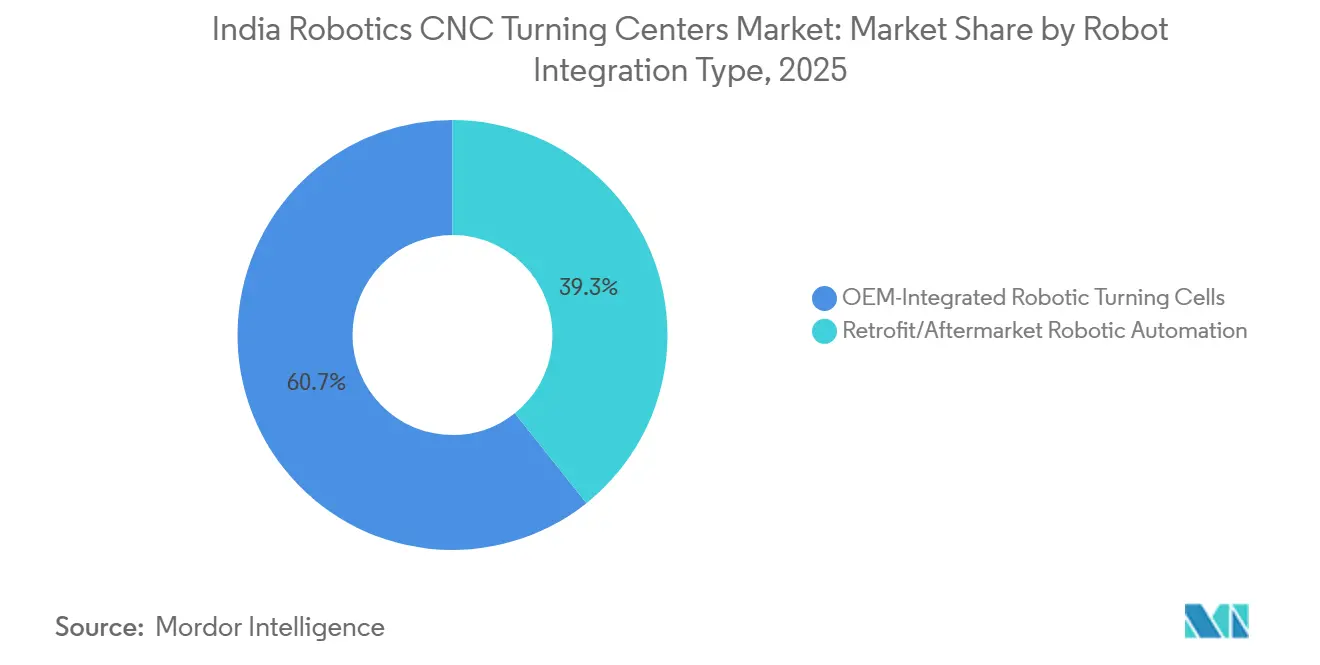

- By robot integration type, OEM-integrated robotic turning cells captured 60.7% of the India robotics CNC turning centers market size in 2025, while retrofit or aftermarket robotic automation is forecast to grow at a 17.3% CAGR through 2031.

- By end-user industry, automotive and commercial vehicles led with 37.2% of the India robotics CNC turning centers market size in 2025, while medical devices and surgical instruments are expected to advance at a 15.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Robotics CNC Turning Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Make in India and PLI Incentivizing CNC and Robotics Manufacturing | +2.8% | National, with early gains in Gujarat, Maharashtra, Karnataka, and Tamil Nadu | Medium term (2-4 years) |

| Automotive Sector Driving Robot Adoption | +2.3% | National, concentrated in Pune, Chennai, Gurugram, and Sanand industrial clusters. | Medium term (2-4 years) |

| Rapid Robot Installation Growth | +2.0% | National | Short term (≤ 2 years) |

| MSME Automation Subsidies Expanding Robot Adoption | +1.6% | National, with targeted spillover to Tier-2 manufacturing cities | Medium term (2-4 years) |

| Industry-Led Initiatives Promoting Advanced Manufacturing Technologies | +1.2% | National | Long term (≥ 4 years) |

| Domestic CNC Turning OEMs Adding Automation Readiness | +0.9% | National, strongest in Gujarat, Karnataka, and Tamil Nadu | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Make in India and PLI (Production-Linked Incentive) Incentivizing CNC and Robotics Manufacturing

Policy support is actively changing the cost structure of automation investment in the India robotics CNC turning centers market. The Scheme for Enhancement of Competitiveness in the Indian Capital Goods Sector Phase II has a total outlay of INR 1,207 crore (USD 134.3 million), of which INR 975 crore (USD 108.5 million) is budgetary support. As of August 2024, 33 projects have been sanctioned.[1]Ministry of Heavy Industries, Government of India, “Make in India and the Capital Goods Revolution,” Press Information Bureau, pib.gov.in These projects span centers of excellence in machine tool robotics, Industry 4.0 testbeds, and skilling facilities, helping build the operating base needed for broader adoption of CNC and robotics. The Technology Acquisition Fund Program under Phase I also completed domestic acquisitions of a Turn Mill Center and a Four-Guideway CNC Lathe, which support local development of multi-tasking turning platforms. PLI-linked investment in electronics, automotive, and medical devices is also driving demand for precision manufacturing, and the larger 2025-26 allocation for automobiles and auto components further strengthens this pull on automated turning demand. SAMARTH Udyog Bharat 4.0 reinforces the same direction because its demonstration model keeps smart manufacturing integration visible and practical for Indian manufacturers.[2]Ministry of Heavy Industries, Government of India, “SAMARTH Udyog Bharat 4.0,” Official Portal, heavyindustries.gov.in

Automotive Sector Driving Robot Adoption

The automotive sector remains the clearest demand anchor for the India robotics CNC turning centers market. Automotive installations totaled 4,070 units in 2024, representing 45% of all industrial robot deployments in India.[3]International Federation of Robotics, “India Rises to Sixth in Global Factory Robot Installations,” World Robotics 2025 Press Release, ifr.org Automotive parts suppliers alone added 2,100 units and grew by 40%, keeping the procurement channel active for turning systems used in shafts, hubs, flanges, and transmission elements. The shift toward electric vehicle production is also changing machine requirements, as EV components require tighter tolerances and greater process consolidation within a single setup. Jyoti CNC Automation developed its VST 160 Vertical Shaft Turning Center for EV component machining. It integrated an automated loading and unloading system, demonstrating how suppliers are aligning their products with this demand. Demand is concentrated in Pune, Chennai, Gurugram, and Sanand, so vendors with stronger service networks in these clusters hold a clear operating advantage in the India robotics CNC turning centers market.

Rapid Robot Installation Growth

India's recent growth in robot installations provides the India robotics CNC turning centers market with a firm near-term demand base. Installations rose 59% to 8,510 units in 2023 and then increased 7.2% to 9,123 units in 2024, putting India in sixth place globally. Growth is spreading beyond automotive, as metal processing installations increased 30% to 420 units in 2024 and plastic and chemical products rose 33% to 600 units, broadening the robot footprint across new end-use settings. India's operational robot stock reached 52,570 units in 2024, creating secondary demand for upgrades, maintenance, and robotic cell reconditioning. Even with this progress, global robot density benchmarks show that India remains early in the automation cycle, leaving long-term headroom but slowing broad-based adoption in the near term. The IFR (International Federation of Robotics) also expected installations to rise further in 2025, which made 2026 an important year for vendors trying to lock in robotic turning orders.

MSME Automation Subsidies Expanding Robot Adoption

The MSME base remains the largest latent opportunity pool within the India robotics CNC turning centers market. The Mutual Credit Guarantee Scheme for MSMEs, launched in January 2025 and modified in March 2026, provides a 60% guarantee on credit facilities up to INR 100 crore (USD 11.1 million) for eligible equipment and machinery purchases. The Credit Linked Capital Subsidy Scheme adds a 15% upfront capital subsidy for technology upgradation and explicitly covers CNC machines, robotics, and process automation. This dual structure matters because one scheme reduces lender risk while the other lowers the buyer's net acquisition cost, which improves payback conditions for mid-tier automated turning cells. The Ministry of MSME also confirmed that its technology centers are being strengthened with CNC machines, robotics and process automation, laser machining, and additive manufacturing, which lowers first-mover risk for smaller buyers through trial and demonstration exposure. In practical terms, that support makes the India robotics CNC turning centers market more accessible to smaller job shops that would otherwise delay automation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Import Dependency for Core Robotics Components | -1.8% | National | Long term (≥ 4 years) |

| High Upfront Cost of Robot-Integrated CNC Turning Cells | -1.4% | National, more acute in Tier-2 and Tier-3 manufacturing clusters | Medium term (2-4 years) |

| Shortage of Skilled Manpower for CNC and Robotics-Integrated Systems | -1.1% | National, most acute in Coimbatore, Rajkot, and Ludhiana clusters | Short term (≤ 2 years) |

| Low Robot Density Compared to Peer Manufacturing Economies | -0.8% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Import Dependency for Core Robotics Components

The India robotics CNC turning centers market still faces a structural cost problem because core robotics components are largely imported. India remains a net importer of critical electronic components and subsystems, and NITI Aayog's Trade Watch for Q2 FY 2025-26 confirmed that the export profile remains concentrated in final-assembly products. The same dependency affects semiconductors, integrated circuits, controllers, and motion systems used in CNC and robotic applications. This keeps system pricing exposed to currency movements and limits how far local machine builders can absorb cost swings when key subsystems are not localized. The Ministry of Heavy Industries supported local technology acquisition for a Turn Mill Center and a Four-Guideway CNC Lathe, but localization of servo motors and harmonic drives remains incomplete.

High Upfront Cost of Robot-Integrated CNC Turning Cells

The high initial cost remains a direct adoption barrier for the India robotics CNC turning centers market, especially at the lower end. A full robotic turning cell combines the turning center, robot or gantry, end-of-arm tooling, safety enclosure, and control integration, and that package is difficult for many SME job shops to justify on short payback periods. The residual burden is heavier because site preparation, tooling, and system integration services add 15-25% to equipment costs. This creates hesitation when production volumes are still too low to support a rapid return, even with subsidy support. The VDMA HR Report 2025 found that only 37% of surveyed companies considered their workforce ready for IoT, robotics, and Industry 4.0 operations, and nearly 60% of SMEs said that only a small fraction of employees could independently manage advanced technologies. That is why modular, staged, and retrofit-ready offers are likely to outperform fully integrated high-capex packages in cost-sensitive parts of the India robotics CNC turning centers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Horizontal Dominance Challenged by Multi-Tasking Precision Needs

Horizontal robotic turning centers held 46.7% of the India robotics CNC turning centers market share in 2025, making them the leading machine type. They remain the default choice for high-volume cylindrical part production across automotive, general engineering, and oil and gas applications. Their wide workholding range and compatibility with standard gantry and articulated robot loaders support both new installations and retrofit projects. This makes them the most practical choice for buyers who still prioritize line stability, familiar tooling, and broad service support.

Vertical robotic turning centers continue to serve large-diameter and heavy-workpiece jobs in energy equipment, large-bore fittings, and heavy automotive castings. Multi-tasking robotic turning centers are the fastest-growing machine type, and the India robotics CNC turning centers market size for this segment is projected to expand at a 14.1% CAGR through 2031. Buyers are shifting toward these systems because process consolidation reduces secondary milling, drilling, and tapping steps within a single setup. That change is especially relevant in aerospace, medical devices, and EV powertrains, where multiple setups can introduce unwanted dimensional variation. The others category, which includes inverted and Swiss-type turning centers, is also gaining traction in miniature precision applications, and recent product moves from Jyoti CNC Automation and AceMicromatic show that domestic OEMs are broadening their complex-process turning portfolios.

By Robot Type: Articulated Robots Lead, Cobots Redefine Small-Batch Economics

Articulated robots accounted for 56.2% of the India robotics CNC turning centers market size in 2025, giving them the largest share among robot types. Their six-axis motion supports complex loading paths, workpiece flipping, and in-cell inspection in automotive and heavy engineering settings. This makes them the preferred setup for high-speed part transfer and precision placement in demanding production lines. Their installed base also benefits from stronger familiarity among large manufacturers that already operate conventional industrial robots elsewhere on the shop floor.

Gantry or cartesian robots still hold a steady role in high-volume single-part-family production because their linear axes offer repeatability and lower cost for simple pick-and-place tasks. Collaborative robots are the fastest-growing robot type with a 15.8% CAGR through 2031 in the India robotics CNC turning centers market. Their appeal is strongest in MSME job shops because they reduce the need for fixed safety guarding and allow more flexible layouts for high-mix production. The broader rise of general industry robot use in India supports this pattern, and global IFR data also points to stronger cobot adoption trends. IMTMA's (India Machine Tool Manufacturers' Association) automation symposium in Pune devoted dedicated attention to collaborative robotics in smart factories, which shows rising industry readiness for cobot use in CNC environments.

By Robot Integration Type: OEM-Integrated Cells Drive Quality, Retrofit Solutions Unlock the Installed Base

OEM-integrated robotic turning cells held 60.7% of the market in 2025 and remained the preferred option for large automotive and aerospace manufacturers. These systems offer tighter machine-robot communication, stronger cycle-time optimization, and factory-backed process warranties. They also fit better with compliance-heavy environments where quality assurance standards, such as IATF (International Automotive Task Force) 16949, are in place. This keeps OEM-integrated cells important in programs with high downtime risk and stringent validation requirements.

Retrofit/aftermarket robotic automation is the fastest-growing integration type, and the India robotics CNC turning centers market size for this segment is projected to grow at a 17.3% CAGR through 2031. The main driver is India's large installed base of standalone CNC turning centers that smaller operators cannot retire but still need to automate. Vendors such as Macpower CNC are targeting this opportunity with gantry and automation kits, plus in-house control systems, to lower entry costs compared with new cells. This supports aging single-turret machines that are still mechanically useful but lack robot interfaces, pallet changers, or vision integration. The growth gap between retrofit and OEM-integrated solutions also shows that the India robotics CNC turning centers market is still in an early automation phase, where incremental upgrades remain the more practical path for many buyers.

By End-User Industry: Automotive Anchors Demand as Medical Devices Emerge as a High-Growth Vertical

Automotive and commercial vehicles accounted for 37.2% of the market in 2025 and remained the primary demand center for robotic CNC turning systems. The segment relies heavily on precision-machined components, including crankshafts, camshafts, transmission shafts, wheel hubs, and suspension links. Automotive robot installations reached 4,070 units in 2024, and parts suppliers remained the main procurement channel for robotic turning cells in this vertical. Oil, gas, and energy demand remained steady, supported by valve bodies and pressure vessel fittings, while electrical, electronics, and semiconductor equipment emerged as a newer source of demand for miniature precision parts amid PLI-led manufacturing expansion.

The medical devices and surgical instruments segment is the fastest-growing end-user segment, and the India robotics CNC turning centers market size for this segment is set to rise at a 15.2% CAGR through 2031. Growth is tied to domestic expansion of medical device manufacturing and the need for sub-10-micron tolerance in implants, surgical tools, and endoscopic components. Aerospace and defense is also gaining weight, and Jyoti CNC Automation reported that 41% of its FY26 order book came from this segment, where multi-axis capability and precision support premium pricing. General industrial machinery and other applications remain the long tail of the India robotics CNC turning centers market and are the most likely entry point for cobot-enabled retrofit solutions.

Geography Analysis

The India robotics CNC turning centers market remained a single-country market in 2025, and demand was concentrated in the country's established manufacturing corridors. Maharashtra, especially the Pune-Nashik-Aurangabad belt, was the largest regional demand center because it combines automotive OEMs, tier-1 suppliers, and aerospace component production. Pune also hosts Yamazaki Mazak's India production facility, and the company plans to increase production capacity in 2026 to meet higher local demand. The western and southern corridor that runs through Pune, Nashik, Chennai, Coimbatore, Kolhapur, and Aurangabad, remains the densest service and support zone for the India robotics CNC turning centers market. IMTMA's Machine Tool Industry Summit also pointed to Maharashtra and Tamil Nadu as the states where automation adoption is deepest and policy-industry alignment is strongest.

Tamil Nadu, centered on Chennai and Coimbatore, forms the second major demand cluster. Chennai's vehicle manufacturing base supports a deep supply chain of turned components, while Coimbatore's dense network of small- and mid-sized job shops keeps replacement and retrofit demand active. The skill shortage is especially visible in Coimbatore, which increases the appeal of automation for owners who need more stable throughput with fewer trained operators. Karnataka, led by Bengaluru, is seeing faster growth in demand for high-precision multi-axis systems, supported by aerospace and defense manufacturing and by the 4.0 India initiative at IISc Bengaluru, which developed 6 smart technologies relevant to robotic machining environments.

Gujarat, especially Rajkot, Ahmedabad, and Sanand, is the fastest-emerging regional demand zone in the India robotics CNC turning centers market. Sanand adds EV-linked automotive investment, Rajkot contributes a strong MSME machining base, and Ahmedabad is becoming more important as local assembly capacity rises. Ace Designers opened a new assembly facility in Ahmedabad in April 2026, targeting 4,000 machines annually and deeper vendor localization in the state. Jyoti CNC Automation is also expanding capacity from 6,000 to 16,000 machines annually by September 2026, with capital expenditure of INR 4.0-4.5 billion (USD 44.5 - 50.1 million), thereby strengthening Gujarat's role as a supply anchor for the national market. Northern India, including Ludhiana, Gurugram, and Faridabad, serves the auto components and precision engineering markets, while eastern India remains smaller but is gradually emerging in steel and heavy engineering applications.

Competitive Landscape

The India robotics CNC turning centers market is fragmented, with global OEMs and domestic manufacturers competing from different strengths. Global suppliers leverage broader robotics ecosystems and deeper turnkey integration to differentiate, especially when buyers want certified automation with proven controller and robot compatibility. Domestic OEMs such as Jyoti CNC Automation, Ace Designers, LMW Limited, and Macpower CNC compete on localization, service responsiveness, retrofit readiness, and alignment with public-sector tender requirements. Ace Designers reported an annual capacity of 8,000 turning centers and 3,400 machining centers after the merger of Ace Manufacturing Systems and Micromatic Machine Tools, making it the largest domestic producer of CNC turning platforms in India. Jyoti CNC Automation's January 2025 design patent, Patent No. 4417-01-2025, for a machine panel interface also shows that local players are investing in product differentiation rather than relying only on price.

The biggest open space in the India robotics CNC turning centers market sits in cobot-integrated retrofit solutions for MSME machine shops, where no single vendor currently controls demand. A second opening is in medical device precision turning, where local manufacturing expansion is outpacing the installed base of certified automation-integrated turning cells. Domestic suppliers are also using proprietary software and control systems to raise switching costs, including Macpower's Macatrol controller and Jyoti CNC's 7th Sense Industry 4.0 platform. These moves show that competition is shifting away from hardware alone toward a broader offering built around controls, connectivity, and shopfloor integration.

Robotics system integrators are becoming more relevant because they can bundle turning centers from several OEMs with robot automation, vision inspection, and connectivity as complete unmanned cells. This creates a parallel competitive layer that can challenge machine builders on project execution rather than just on base machine supply. Certification standards such as ISO 9001 and IATF 16949 continue to separate stronger automation suppliers from lower-tier assembly-led operators. In this setting, companies that can pair local service coverage with reliable automation integration are likely to gain the most share in the India robotics CNC turning centers market.

India Robotics CNC Turning Centers Industry Leaders

Jyoti CNC Automation Limited

Ace Micromatic Group

Bharat Fritz Werner Ltd. (BFW)

HMT Machine Tools Limited

LMW Limited (Lakshmi Machine Works)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: AceMicromatic Group debuted the Turn Mill LT2 LM M, a high-precision CNC turning center with C- and Y-axis capability handling milling, drilling, tapping, and turning in a single setup, at the INDUS-tech Expo Kolkata, marking the model's East India debut and underscoring the group's strategy to deepen market penetration in eastern India's MSME machining ecosystem.

- April 2026: Ace Designers Limited inaugurated a new assembly facility at Panchratna Industrial Park, Ahmedabad, with an investment of INR 50 crore (USD 5.6 million), targeting annual production of 4,000 machines over the next five years and focusing on regional vendor development to support further localization of CNC turning center manufacturing in Gujarat; the company expects to cross INR 2,800 crore (USD 311.6 million) in annual turnover in FY26 and currently maintains capacity to manufacture 8,000 turning centers and 3,400 machining centers annually.

India Robotics CNC Turning Centers Market Report Scope

The India Robotics CNC Turning Centers Market is Segmented by Machine Type (Horizontal Robotic Turning Centers, Vertical Robotic Turning Centers, and More), by Robot Type (Articulated Robots, and More), by Robot Integration Type (OEM, Retrofit/Aftermarket Robotic Automation), and by End-User Industry (Oil, Gas, & Energy, Aerospace & Defense, and More), The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Horizontal Robotic Turning Centers |

| Vertical Robotic Turning Centers |

| Multi-Tasking Robotic Turning Centers |

| Others |

| Articulated Robots |

| Collaborative Robots (Cobots) |

| Gantry/Cartesian Robots |

| OEM-Integrated Robotic Turning Cells |

| Retrofit/Aftermarket Robotic Automation |

| Automotive & Commercial Vehicles |

| Aerospace & Defense |

| Medical Devices & Surgical Instruments |

| Oil, Gas, & Energy |

| Electrical, Electronics & Semiconductor Equipment |

| General Industrial Machinery |

| Others |

| By Machine Type | Horizontal Robotic Turning Centers |

| Vertical Robotic Turning Centers | |

| Multi-Tasking Robotic Turning Centers | |

| Others | |

| By Robot Type | Articulated Robots |

| Collaborative Robots (Cobots) | |

| Gantry/Cartesian Robots | |

| By Robot Integration Type | OEM-Integrated Robotic Turning Cells |

| Retrofit/Aftermarket Robotic Automation | |

| By End-User Industry | Automotive & Commercial Vehicles |

| Aerospace & Defense | |

| Medical Devices & Surgical Instruments | |

| Oil, Gas, & Energy | |

| Electrical, Electronics & Semiconductor Equipment | |

| General Industrial Machinery | |

| Others |

Key Questions Answered in the Report

What is the expected value of the India robotics CNC turning centers market by 2031?

The India robotics CNC turning centers market is forecast to reach USD 193.5 million by 2031, up from USD 90.2 million in 2025, with a 13.8% CAGR over 2026-2031.

What is driving demand for robotic CNC turning centers in India?

Demand is being supported by policy incentives, rising industrial robot installations, stronger domestic machine tool output, and higher automation needs in automotive, EV, aerospace, and medical device manufacturing.

Which machine type leads demand in India?

Horizontal robotic turning centers led in 2025 with a 46.7% share because they remain well-suited for high-volume cylindrical part production and standard automation layouts.

Which robot type is growing the fastest in CNC turning applications?

Collaborative robots are projected to grow the fastest, at a 15.8% CAGR through 2031, because they reduce guarding requirements and fit high-mix MSME job shop environments.

Why is retrofit automation gaining traction across India machine shops?

Retrofit/aftermarket robotic automation is forecast to grow at a 17.3% CAGR because many operators have usable standalone CNC turning centers that need automation but cannot be replaced outright.

Which end-user sector creates the strongest demand base?

Automotive and commercial vehicles remained the largest end-user segment in 2025, with a 37.2% share, while medical devices and surgical instruments are the fastest-growing segment, with a 15.2% CAGR through 2031.

Page last updated on: