India Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

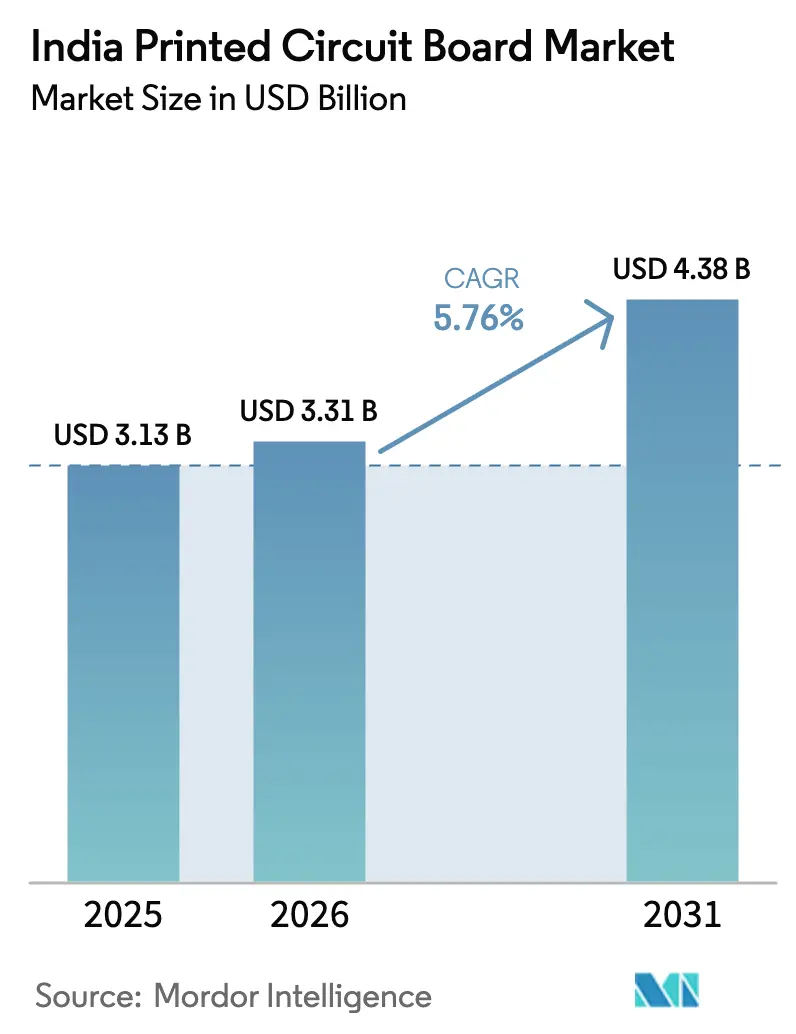

| Base Year Market Size (2025) | USD 3.13 Billion |

| Market Size (2026) | USD 3.31 Billion |

| Market Size (2031) | USD 4.38 Billion |

| Growth Rate (2026 - 2031) | 5.76% CAGR |

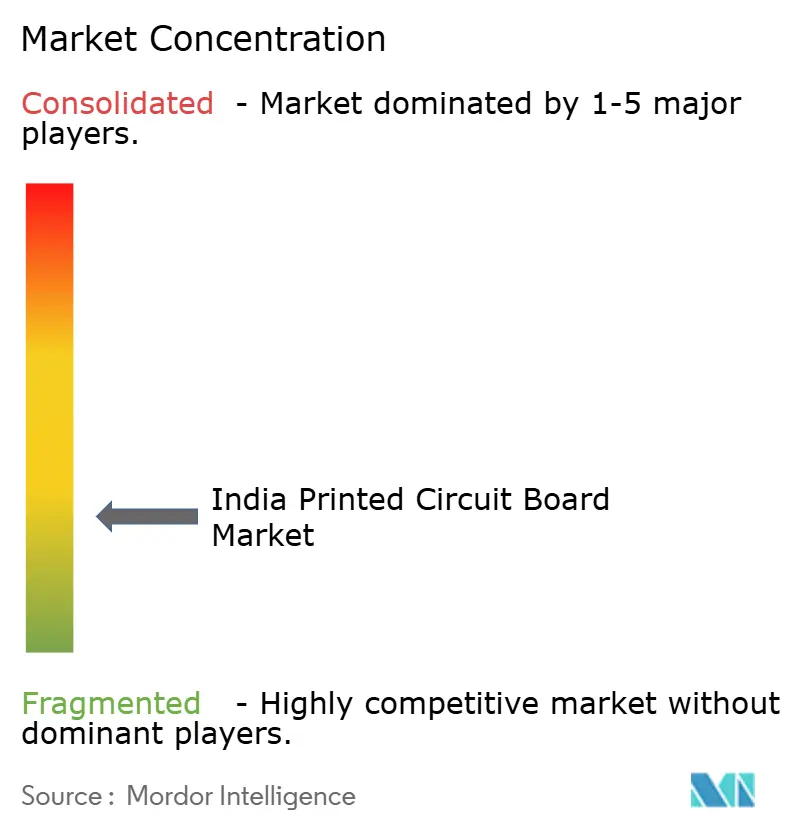

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Printed Circuit Board Market Analysis by Mordor Intelligence

The India printed circuit board market size is expected to grow from USD 3.13 billion in 2025 to USD 3.31 billion in 2026 and is forecasted to reach USD 4.38 billion by 2031 at 5.76% CAGR over 2026-2031. Government production-linked incentives, expanded smartphone and telecom manufacturing footprints, and the migration from low-layer boards to advanced high-density interconnect designs underpin this expansion. Capital inflows from approved Electronics and Components Manufacturing Scheme projects have shortened prototype lead times, while domestic content rules in telecom and electric-vehicle programs anchor demand visibility. At the same time, foreign exchange exposure on copper-clad laminate imports and tighter effluent-treatment norms are squeezing margins for smaller fabricators. Competitive intensity is rising as vertically integrated players pursue laminate, substrate, and final board assembly inside a single campus to recapture value currently lost to imports. Against this backdrop, the India PCB market is evolving from cost-optimized 4-6-layer supply toward technology-rich 10-14-layer and rigid-flex offerings that command higher average selling prices.

Key Report Takeaways

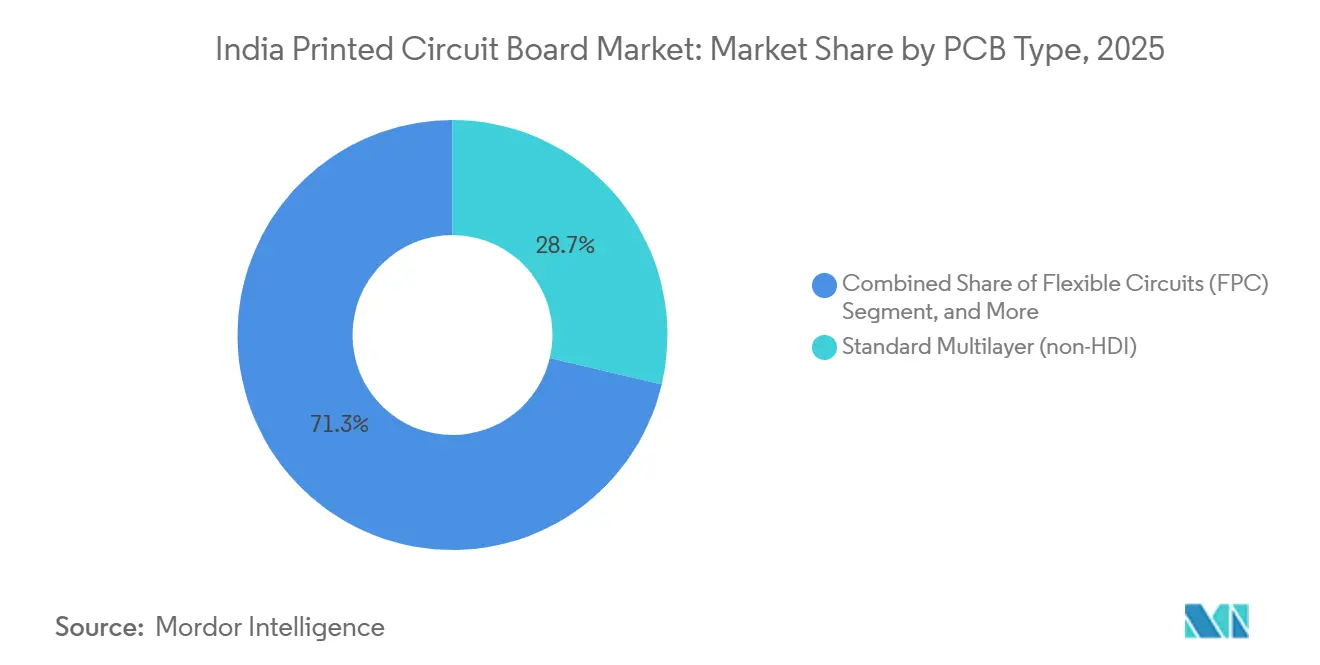

- By PCB type, standard multilayer boards led with 28.69% of the India PCB market share in 2025, while flexible circuits are forecast to expand at a 7.12% CAGR through 2031.

- By substrate material, glass epoxy FR-4 held a 43.71% of the India PCB market share in 2025, and high-speed, low-loss laminates are projected to grow at a 6.82% CAGR through 2031.

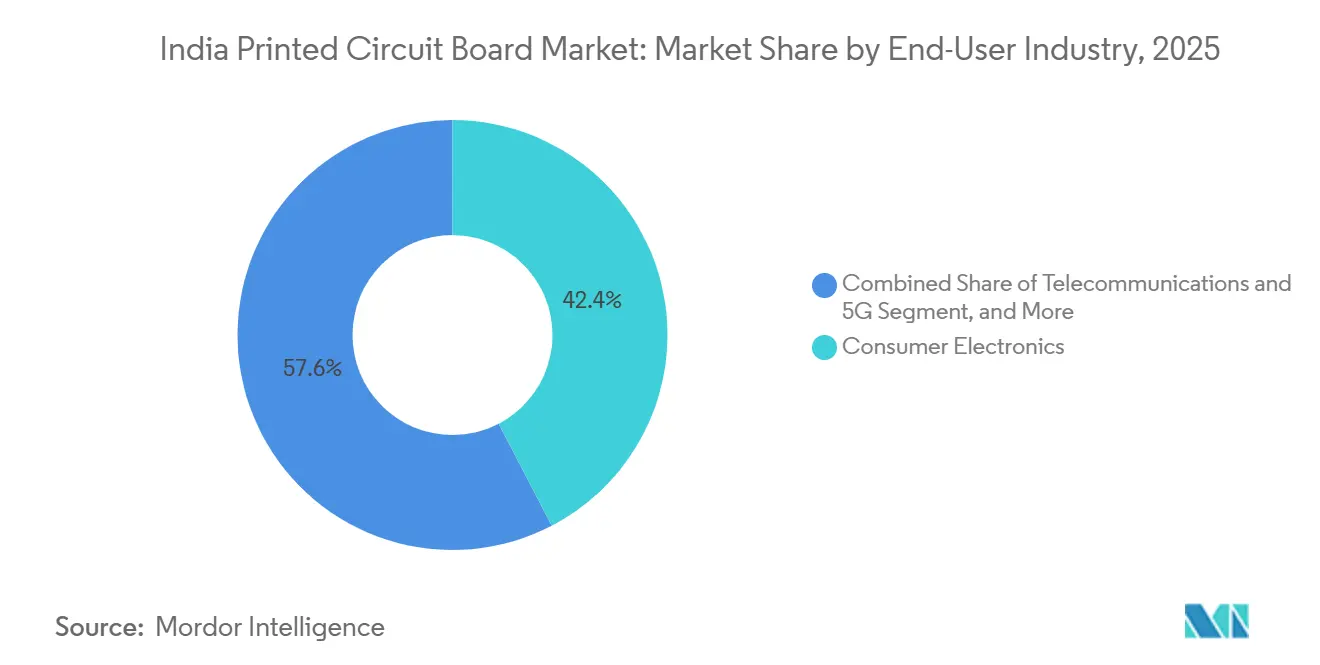

- By end-user industry, consumer electronics accounted for 42.36% of the India PCB market share in 2025, whereas telecommunications and 5G applications are advancing at a 7.34% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone and consumer electronics expansion post-PLI incentives | +1.2% | Tamil Nadu, Karnataka, Uttar Pradesh | Medium term (2-4 years) |

| Government PLI schemes for telecom equipment | +1.0% | Haryana, Maharashtra | Medium term (2-4 years) |

| Rising electric-vehicle production | +0.9% | Gujarat, Maharashtra, Tamil Nadu | Long term (≥ 4 years) |

| Roll-out of 5G infrastructure | +0.8% | Metros and tier-1 cities | Short term (≤ 2 years) |

| IoMT adoption driving flex boards | +0.5% | Maharashtra, Karnataka | Long term (≥ 4 years) |

| Smallsat constellations need radiation-hardened boards | +0.4% | Karnataka, Andhra Pradesh | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Smartphone and Consumer Electronics Manufacturing in India Post-PLI Incentives

Foxconn’s Bharat FIH and Tata Electronics have moved from spot procurement to multi-year PCB contracts that guarantee volume offtake, enabling local suppliers to plan capacity with lower inventory risk. Tata Electronics’ USD 1.6 billion commitment in Tamil Nadu includes an internal rigid-flex line, cutting import reliance on Vietnamese and Thai boards. Dixon Technologies’ Noida complex, operational since 2024, has boosted domestic sourcing ratios by offsetting the cost premium of Indian boards with PLI rebates. ECMS support for Tier-2 fabricators, such as Kaynes Circuits, accelerates the shift to eight-layer capability, slashing prototype cycles to 6 weeks. Together, these dynamics position the India printed circuit board (PCB) market as a strategic beneficiary of handset value-chain localization.

Government PLI Schemes for Telecom and Networking Products Driving Local PCB Demand

The Department of Telecommunications now requires that 60% of the board value of public-sector 5G equipment be sourced locally, rising to 75% by 2027.[1]Department of Telecommunications Staff, “5G Technology in India,” Department of Telecommunications, dot.gov.in This mandate anchors a captive annual demand pool of INR 8,000 crore for boards meeting IPC-6012 Class 3 specifications. Kaynes Technology and Ascent Circuits have secured ECMS funding to build six-layer and eight-layer lines with stacked microvias aligned to Ericsson and Nokia antenna platforms. The National Telecom Policy 2025 earmarks INR 1,200 crore for PCB R and D, underwriting materials, and stacked via research with leading institutes. As foreign suppliers retrench, domestic fabricators capture design wins in optical transport and small-cell equipment, raising utilization rates on new HDI lines.

Rising Electric-Vehicle Production Escalates Need for High-Power Automotive PCBs

FAME-III rules stipulate 70% domestic value addition in battery management systems by 2026, pushing carmakers to dual-source between Chinese and Indian board suppliers.[2]Ministry of Heavy Industries Staff, “FAME-III Production and Manufacturing Plan,” heavyindustries.gov.in Tata Motors already sources 55% of Nexon EV boards locally, up from 30% two years earlier, signaling a structural shift in the automotive supply chain. ECMS-funded AT&S India will target 800 V architectures that enable rapid charging, while new Automotive Electronics Council standards lock in multi-year orders for suppliers that can meet 1,000-hour thermal-cycling tests. For the India printed circuit board (PCB) market, automotive demand offers a high-margin complement to volatile smartphone cycles.

Rollout of 5G Infrastructure Requiring Advanced HDI Boards

India installed 469,000 5G base stations by 2024, but the migration to standalone cores by 2026 requires antenna boards with blind and buried vias, and layer counts up to fourteen. Global HDI’s Karnataka plant brings laser drilling and sequential lamination to domestic soil, bridging a critical capability gap. BARC’s PTFE-ceramic composites address insertion-loss challenges at millimeter-wave frequencies.[3]Bhabha Atomic Research Centre Scientists, “Development of Indigenous RF and Microwave Substrate Materials,” BARC Newsletter, barc.gov.in Wipro Electronics will leverage its IT client base to win open-RAN small-cell programs, widening the customer pool for HDI suppliers. These technical advances raise the ceiling on domestic content in 5G radios, reinforcing growth momentum for the India printed circuit board (PCB) market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import dependence for copper-clad laminates | -0.8% | Nationwide | Short term (≤ 2 years) |

| Environmental compliance costs for effluent treatment | -0.5% | Maharashtra, Karnataka, Tamil Nadu | Medium term (2-4 years) |

| Scarcity of domestic ultra-low-loss resins | -0.3% | Nationwide | Long term (≥ 4 years) |

| Power-quality issues in fine-line fabs | -0.4% | Uttar Pradesh, Haryana industrial belts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Import Dependence for Copper-Clad Laminates Raising Cost Volatility

Ninety percent of laminates were imported in 2024, exposing fabricators to price swings amplified by a 30% anti-dumping duty on Chinese supplies. Landed cost increases of USD 1.2-1.5 per square meter compressed gross margins to below 20% at mid-scale shops. ECMS-backed laminate capacity from Kaynes Circuits will cover only 15% of projected 2027 demand, leaving the India printed circuit board (PCB) market vulnerable to copper price volatility that lifted laminate costs by up to 15% in 2024. Extended inventory buffers tie up working capital and blunt the cash-flow benefits of PLI incentives.

Complex Environmental Compliance Costs for PCB Manufacturing Effluent Treatment

Revised hazardous-waste rules now force on-site treatment of spent etchants before discharge, adding 8-12% to greenfield project costs. Syrma Strategic Electronics has allocated 9% of capex to zero-liquid-discharge systems at its Andhra Pradesh plant, nearly double the pre-2024 norm. Extended Producer Responsibility mandates require the funding board to take back and recycling, imposing additional recurring costs. Quarterly audits by state boards can levy six-figure penalties, pushing small fabricators to outsource finishing steps or delay HDI upgrades. These compliance burdens temper the pace of capacity adds in the India printed circuit board (PCB) market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PCB Type: Flexible Circuits Gain Share on Miniaturization Trend

Flexible circuits held a mid-teen share yet posted the fastest trajectory, expanding at a forecast 7.12% CAGR as foldable smartphones, wearables, and camera modules demand bend-tolerant interconnects. Standard multilayer boards captured 28.69% of the India printed circuit board (PCB) market share in 2025, anchored in televisions, laptops, and power supplies. Rigid 1-2-sided boards dominate price-sensitive appliances, but their share is slipping as OEMs migrate to higher-layer counts to integrate power and signal on a single board. High-density interconnect designs, benefiting from Global HDI’s and Wipro’s new lines, bring laser-drilled microvias and sub-75 micron traces into domestic mass production, positioning the India printed circuit board (PCB) market for higher value per square inch.

The premium IC substrate niche commands unit prices of USD 8-15 and remains largely import-dependent, but ECMS incentives for Kaynes Circuits’ camera-module project pave the way for local suppliers to enter. Metal-core boards for LED lighting and ceramic substrates for power electronics hold a niche but sticky demand where thermal conductivity is paramount. Over the forecast horizon, the combined pull of smartphone compactness and automotive radar systems is set to cut commodity rigid board share to the mid-twenties, while flexible and HDI architectures are set to gain incrementally.

By Substrate Material: High-Speed Low-Loss Laminates Accelerate

Glass epoxy FR-4 retained 43.71% share in 2025 due to balanced cost and performance, but its dominance is eroding as 400G data-center switches and 26 GHz radio units require dielectric constants below 3.5. High-speed, low-loss materials are projected to grow at a 6.82% CAGR, supplementing FR-4 in the India printed circuit board (PCB) market for millimeter-wave and high-bit-rate designs. Polyimide laminates, priced severalfold above FR-4, serve flex and rigid-flex boards in engine control and avionics where 200 °C operating windows are common. Packaging resins such as bismaleimide-triazine enable 15-micron dielectric layers in IC substrates, an area ripe for import substitution once domestic resin production scales.

Kaynes Circuits’ high-Tg FR-4 line will raise the ceiling for automotive solder-reflow cycles, while BARC’s PTFE-ceramic composite initiative offers a homegrown alternative to Rogers and Taconic products. Aluminum-core laminates remain the default for LED thermal management, but rising lumen-per-watt targets may drive adoption of copper-core boards despite their higher weight. Overall, the tilt toward low-loss and polyimide materials will shave FR-4’s share by roughly 4-5 points by 2031 as the India printed circuit board (PCB) market pivots to signal-integrity-critical applications.

By End-User Industry: Telecom and 5G Lead Growth Curve

Consumer electronics accounted for 42.36% of 2025 revenue, reflecting India’s 150 million annual smartphone shipments, yet its share is gradually slipping as PCB unit prices plateau. Telecommunications and 5G demand is forecast to climb at a 7.34% CAGR, propelled by public-sector content mandates and ongoing 5G macro and small-cell rollout. Data-center builders are doubling installed megawattage, driving switch and router orders that specify low-loss boards. Automotive and EV programs, backed by FAME-III and Nexon EV sourcing shifts, inject multilayer and metal-core volume with higher copper weights.

Industrial drives and power inverters continue to require heavy-copper boards, anchoring a stable mid-single-digit growth pocket. Medical devices, particularly wearable patches and imaging scopes, lean heavily on flexible circuits that now meet biocompatibility standards. Aerospace and defense designs secure premium pricing but represent a low-volume, high-mix niche. As telecom and automotive segments outpace handset growth, consumer electronics are expected to slide to just under 40% by 2031, reshaping capacity allocation across the India printed circuit board market.

Geography Analysis

India’s dominant production corridor of Tamil Nadu, Karnataka, and Maharashtra accounted for nearly 70% of fabrication output in 2025, giving the region the largest share of the India printed circuit board market among all state groupings. Tamil Nadu leads because Foxconn’s Bharat FIH and Tata Electronics assemble more than 20 million iPhones annually in Sriperumbudur and Hosur, creating a stable base load for nearby multilayer and rigid-flex suppliers. Karnataka follows closely, anchored by AT&S India’s long-standing Nanjangud plant and reinforced by Global HDI’s and Wipro Electronics’ new HDI investments that promise ten-to-fourteen-layer capability by 2026. Maharashtra rounds out the top tier through Pune and Aurangabad clusters that focus on automotive and industrial customers tied to Tata Motors, Mahindra Electric, and Bajaj Auto, allowing suppliers to specialize in heavy-copper and high-temperature boards. Together, these three states account for most PLI disbursements, reinforcing their infrastructure advantages and attracting new laminate and substrate projects that expand the local India printed circuit board market.

Uttar Pradesh’s Noida and Greater Noida belt is emerging as a secondary hub because Dixon Technologies’ USD 240 million handset complex now sources 40% of its multilayer boards domestically, yet chronic voltage sags and harmonic distortion in the regional grid reduce yields on sub-75 micron traces and force plants to invest in expensive power-conditioning gear. Andhra Pradesh entered the map in December 2025 when Syrma Strategic Electronics broke ground on an INR 1,595 crore facility designed for automotive and industrial HDI volumes, lured by state subsidies and power tariffs below INR 5 per kWh. Gujarat courts high-power automotive PCB projects tied to rising electric-vehicle production, although most fabs remain in the prototype stage. Haryana retains a small but strategic share through telecom equipment lines that serve public-sector 5G rollouts and benefit from proximity to Delhi-NCR design centers. These developing clusters widen geographic diversity but still trail the leading trio in supplier density, skilled labor pools, and end-to-end ecosystem depth.

Himachal Pradesh and Uttarakhand host niche-oriented plants that specialize in defense and industrial control boards, leveraging lower labor costs and state tax holidays to offset longer logistics routes to coastal ports. Rajasthan and Telangana have announced land-grant packages for prospective investors, but power-quality concerns and limited ancillary suppliers temper immediate uptake. Looking ahead, analysts expect the PLI scoring criteria to continue favoring brownfield expansions in Tamil Nadu, Karnataka, and Maharashtra, as those states already offer proven supply chains, stable power, and quick access to component distributors. As new ECMS-funded lines ramp, the combined India printed circuit board market in these three states is projected to grow faster than the national average through 2031, while emerging regions capture incremental share by focusing on specialized applications such as space-grade or heavy-copper boards. Overall, the production landscape is likely to remain concentrated, with selective diversification driven by targeted state incentives and customer proximity requirements.

Competitive Landscape

The India PCB market is moderately fragmented, with the five largest companies together accounting for about 35-40% of 2025 revenue, and no single firm exceeding a 10% share. This structure reflects the diversity of customer needs, because smartphones prioritize cost-optimized four-layer supply, while automotive, aerospace, and defense users demand boards that meet AEC-Q200 or MIL-PRF-55110 standards and accept only vetted suppliers. Scale alone is not a decisive moat, since the market rewards process capability and breadth of certification over raw production volume. As a result, regional specialists that focus on high-mix, low-volume programs for industrial controls or medical devices remain viable alongside larger national players. Competitive intensity is rising, however, because new ECMS-funded entrants are adding both capacity and technology depth that converge on the mid-range six-to-eight-layer sweet spot.

Vertical integration and technology upgrading define the current strategic playbook. Kaynes Technology is building laminate, multilayer, HDI, and camera-module lines on the same campus to insulate margins from volatile laminate imports and to shorten internal logistics loops. AT&S India still leads in sub-50-micron trace geometries, yet it faces fresh competition as Global HDI brings sequential lamination and laser drilling to Karnataka and as Wipro Electronics exploits long-standing IT relationships to capture open-RAN board programs. These investments shift the competitive frontier from commodity four-layer panels to ten-to-fourteen-layer HDI and rigid-flex formats that command double the average selling price. Stronger technology capabilities also help domestic firms satisfy tightening procurement rules that favor high local value addition in telecom and electric-vehicle systems.

Materials innovation and compliance requirements are widening the gap between scale leaders and smaller shops. The Bhabha Atomic Research Centre has patented PTFE-ceramic composites that could reduce dependence on Rogers and Taconic for millimeter-wave laminates, giving early adopters a differentiated cost position. At the same time, adherence to IS 16900, IPC-6012 Class 3, ISO 9001, and IATF 16949 has become a prerequisite for public-sector tenders, raising annual audit and documentation costs that many micro-scale fabricators struggle to carry. Buyers are also pushing for automated optical inspection and direct imaging, which cut defect rates below 100 ppm but require multimillion-dollar capex. These forces point toward gradual consolidation, yet regional family-owned firms that specialize in appliance or lighting boards still find room to operate by leveraging close customer ties and flexible lot sizes. Overall, competitive dynamics are moving the India PCB market toward a technology-driven structure in which certification readiness and process sophistication increasingly trump sheer square-meter output.

India Printed Circuit Board Industry Leaders

AT & S India Private Limited

Shogini Technoarts Private Limited

Fine-Line Circuits Limited

SFO Technologies Private Limited

Genus Electrotech Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Syrma Strategic Electronics began building its INR 1,595 crore (USD 191 million) Andhra Pradesh plant, targeting trial output in Dec 2026 and commercial launch by Apr 2027.

- November 2025: Wipro Electronics committed INR 500 crore (USD 60 million) for a PCB unit in Doddaballapura, Karnataka, with production slated within nine months.

- November 2025: Global HDI unveiled a INR 1,500 crore (USD 180 million) Karnataka facility for HDI and multilayer boards, aiming for Q3 2026 pilot runs.

- November 2025: The Ministry of Electronics and Information Technology cleared 17 ECMS projects worth INR 7,172 crore (USD 860 million), including AT&S India and Meena Electrotech.

India Printed Circuit Board Market Report Scope

The India Printed Circuit Board Market is Segmented by PCB Type (Standard Multilayer (non-HDI), Rigid 1-2 Sided, High-Density Interconnect (HDI), Flexible Circuits (FPC), IC Substrates (Package Substrates), Rigid-Flex, Other PCB Types), Substrate Material (Glass Epoxy (FR-4), High-Speed / Low-Loss, Polyimide (PI), Packaging Resins (BT / ABF), Other Substrate Materials), End-user Industry (Consumer Electronics, Computing and Data Centers, Telecommunications and 5G, Automotive and EV, Industrial and Power, Healthcare / Medical, Aerospace and Defense, Other End-user Industries). The Market Forecasts are Provided in Terms of Value in USD.

| Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided |

| High-Density Interconnect (HDI) |

| Flexible Circuits (FPC) |

| IC Substrates (Package Substrates) |

| Rigid-Flex |

| Other PCB Types |

| Glass Epoxy (FR-4) |

| High-Speed / Low-Loss |

| Polyimide (PI) |

| Packaging Resins (BT / ABF) |

| Other Substrate Materials |

| Consumer Electronics |

| Computing and Data Centers |

| Telecommunications and 5G |

| Automotive and EV |

| Industrial and Power |

| Healthcare / Medical |

| Aerospace and Defense |

| Other End-user Industries |

| By PCB Type | Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided | |

| High-Density Interconnect (HDI) | |

| Flexible Circuits (FPC) | |

| IC Substrates (Package Substrates) | |

| Rigid-Flex | |

| Other PCB Types | |

| By Substrate Material | Glass Epoxy (FR-4) |

| High-Speed / Low-Loss | |

| Polyimide (PI) | |

| Packaging Resins (BT / ABF) | |

| Other Substrate Materials | |

| By End-user Industry | Consumer Electronics |

| Computing and Data Centers | |

| Telecommunications and 5G | |

| Automotive and EV | |

| Industrial and Power | |

| Healthcare / Medical | |

| Aerospace and Defense | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the forecast growth rate for the India PCB market between 2026 and 2031?

The market is expected to register a 5.76% CAGR, rising from USD 3.31 billion in 2026 to USD 4.38 billion by 2031.

Which PCB type is projected to expand the fastest?

Flexible circuits are forecast to grow at a 7.12% CAGR, driven by foldable smartphones, wearables, and camera modules.

How will telecom and 5G policy changes affect domestic PCB demand?

Public-sector procurement rules mandating up to 75% local PCB content by 2027 create a captive market for high-density interconnect boards.

Why are high-speed low-loss laminates gaining share?

400G data-center and millimeter-wave 5G applications need dielectric constants below 3.5 and low loss tangents, which FR-4 cannot deliver.

What are the main challenges facing PCB fabricators in India?

Heavy reliance on imported copper-clad laminates, high effluent-treatment capex, and power-quality issues that impact yield on fine-line processes.

Which states lead PCB production capacity?

Tamil Nadu, Karnataka, and Maharashtra collectively hold nearly 70% of national fabrication capacity due to established ecosystems and reliable power.

Page last updated on: