India Lubricants Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

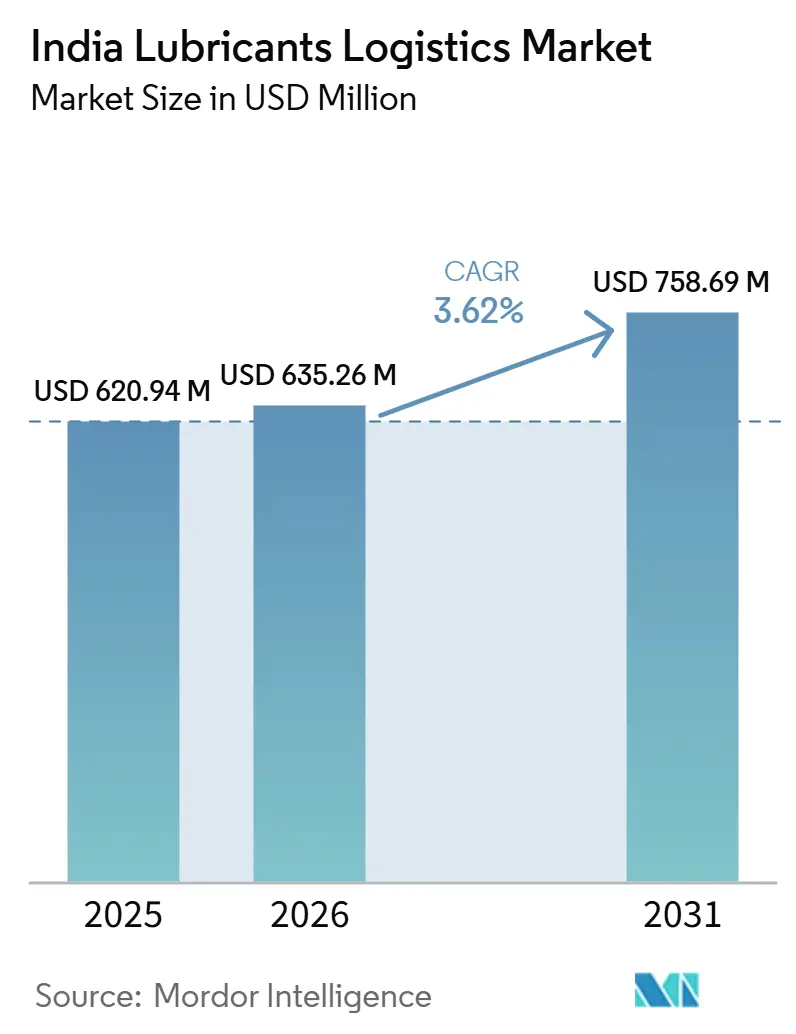

| Base Year Market Size (2025) | USD 620.94 Million |

| Market Size (2026) | USD 635.26 Million |

| Market Size (2031) | USD 758.69 Million |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

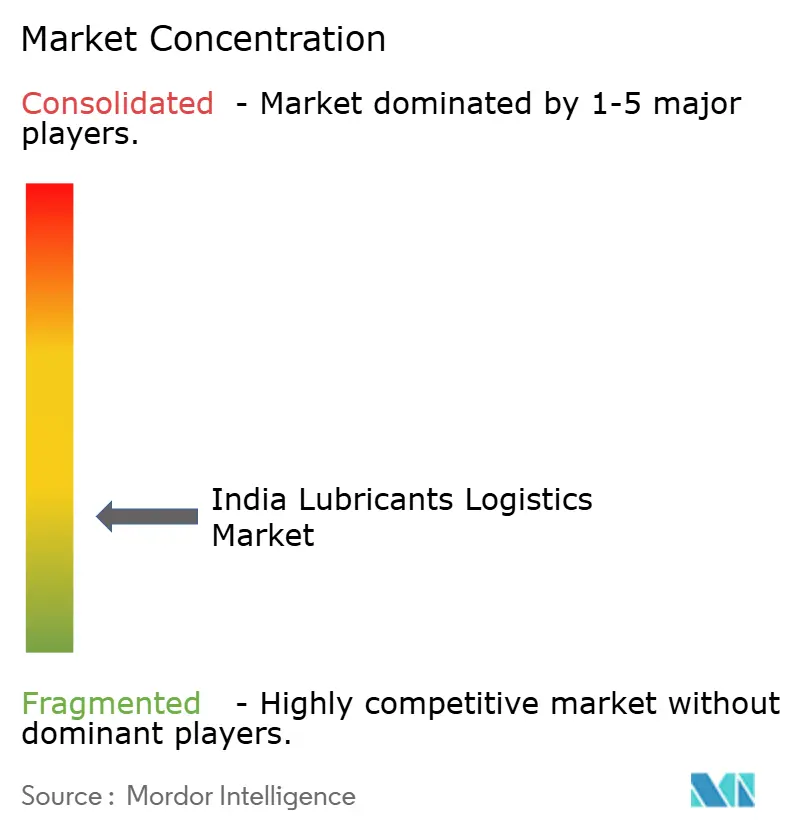

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Lubricants Logistics Market Analysis by Mordor Intelligence

The India lubricants logistics market size is expected to increase from USD 620.94 million in 2025 to USD 635.26 million in 2026 and reach USD 758.69 million by 2031, growing at a CAGR of 3.62% over 2026-2031.

Demand is being supported by stronger commercial vehicle activity and firmer industrial output, which together are keeping refill cycles active across transport and factory-linked channels. The India lubricants logistics market is also being shaped by a wider spread of workshop and industrial demand beyond the largest cities, which is pushing distribution systems deeper into Tier-2 and Tier-3 corridors. At the same time, the move toward premium and synthetic lubricant grades is raising the need for cleaner handling, better packaging control, and closer shipment monitoring. This is creating more room for providers that can combine transport with warehousing, inventory support, repacking, relabeling, and kitting. Supply conditions remain uneven because base-oil dependence, tighter compliance needs, and gradual electric vehicle adoption are all influencing how much throughput the India lubricants logistics market can sustain over the forecast period.

Key Report Takeaways

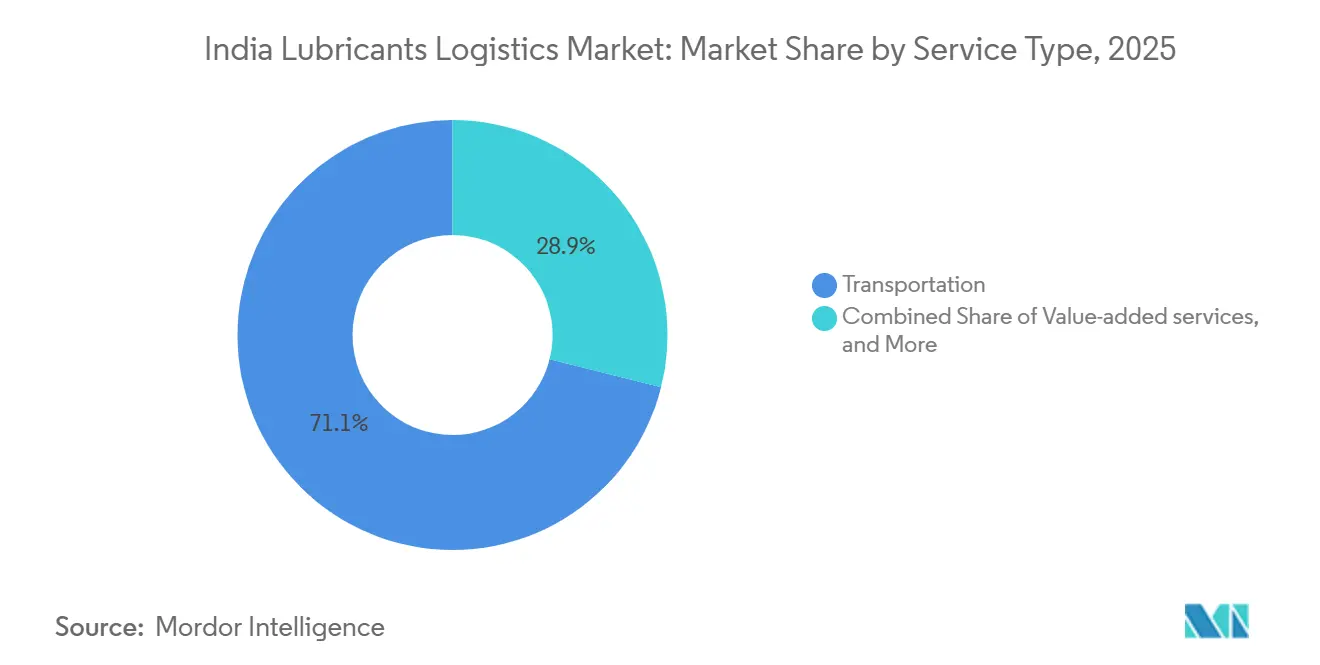

- By service type, transportation held 71.09% of the India lubricants logistics market size in 2025, while value-added services are forecast to expand at a 5.12% CAGR through 2031.

- By transportation mode within the service type category, road haulage accounted for 88.16% of the India lubricants logistics market share in 2025, while multimodal transport is projected to grow at a 4.84% CAGR through 2031.

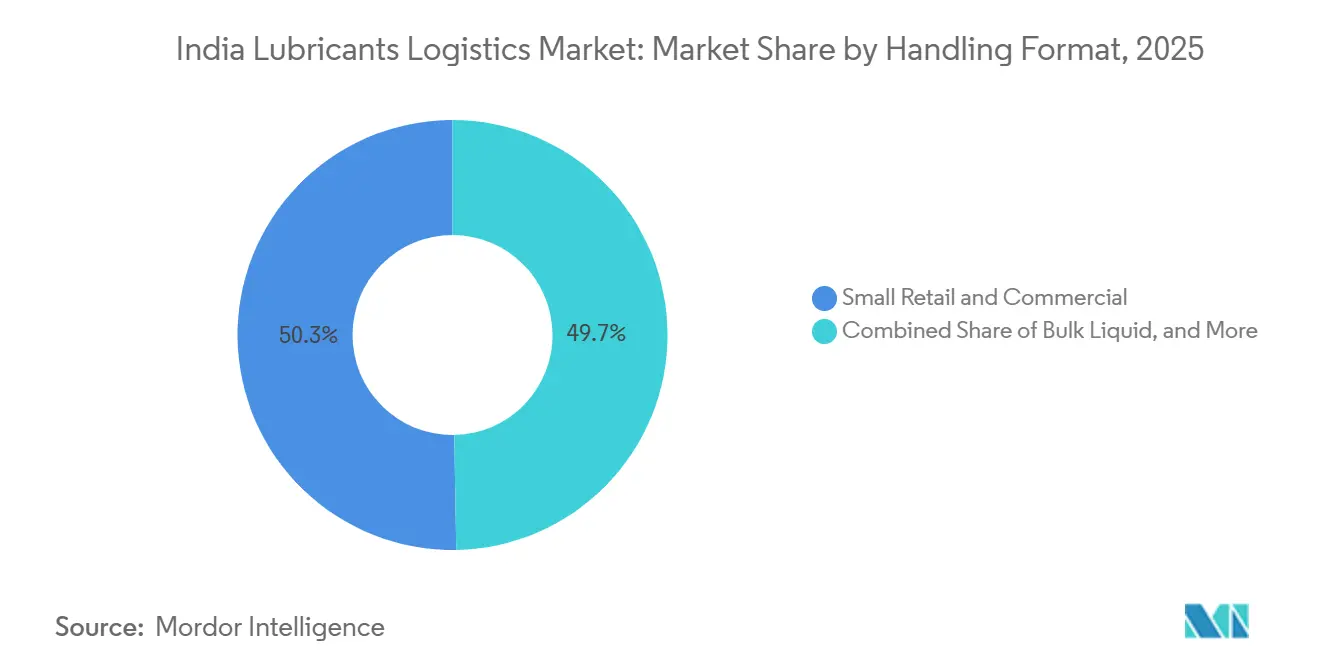

- By handling/shipment format, small retail and commercial packs captured 50.28% of the India lubricants logistics market size in 2025, while IBCs are expected to advance at a 4.56% CAGR through 2031.

- By end-user industry, automotive commanded 44.86% of the India lubricants logistics market share in 2025, while aerospace is projected to record the highest CAGR at 5.06% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Lubricants Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vehicle Parc and commercial fleet intensity | +0.40% | National, concentrated in Gujarat, Maharashtra, and Tamil Nadu auto corridors | Short term (≤ 2 years) |

| Manufacturing, construction, and mining activity lifting industrial lubricant flows | +0.40% | National, highest in Maharashtra, Gujarat, Odisha, and Chhattisgarh industrial belts | Medium term (2-4 years) |

| Post-GST warehouse consolidation and 3PL adoption | +0.30% | National, early gains in NCR, Mumbai Metropolitan Region, Bengaluru, and Pune corridors | Medium term (2-4 years) |

| Premium and synthetic lubricant shift increasing handling complexity | +0.30% | National, led by South and West India OEM corridors | Medium term (2-4 years) |

| Taluka-level availability gaps increasing district-deep replenishment demand | +0.20% | Northern and Eastern India, with spillover to Central India | Long term (≥ 4 years) |

| Used-oil EPR expanding reverse-logistics requirements | +0.20% | National, with initial gains in major industrial clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle Parc and Commercial Fleet Intensity

India’s commercial vehicle base is moving through a renewal phase that keeps lubricant demand active and raises delivery frequency across service networks. Commercial vehicle retail sales reached 1,060,906 units in FY2026, which was the first time the segment crossed 10 lakh units, and sales rose 11.74% year over year. A larger operating fleet means more routine oil changes, more workshop visits, and tighter reorder cycles across highway-led service corridors. That pushes the India lubricants logistics market toward denser less-than-truckload runs, especially where fleet garages and dealer workshops cluster near freight routes. As BS-VI trucks replace older vehicles, lubricant handling requirements become more specification-sensitive, which increases the value of controlled delivery and accurate stock positioning.

Manufacturing, Construction, and Mining Activity Lifting Industrial Lubricant Flows

Industrial activity is sustaining a strong pull on hydraulic fluids, gear oils, and metalworking fluids across plant-heavy corridors. MoSPI recorded 8.1% manufacturing output growth in December 2025, and the updated series showed manufacturing growth at 6.2% year over year in April 2026, while capital goods rose 16.0%, signaling continued additions to productive capacity[1]“Index of Industrial Production, December 2025 Press Release,” MoSPI, mospi.gov.in. The Government of India’s Economic Survey FY2026 also placed industrial GVA growth at 6.2% for the year and manufacturing GVA growth at 9.13% in Q2 FY2026. Even as equipment sales softened during the transition to emission norms, the existing installed fleet still required preventive maintenance and steady lubricant replenishment. The India lubricants logistics market therefore benefits not only from more industrial output, but also from a higher-value lubricant mix that needs cleaner storage, better dispatch control, and more disciplined handling.

Post-GST Warehouse Consolidation and 3PL Adoption

The post-GST supply chain model has made it easier for lubricant blenders to run broader networks from fewer regional hubs. That shift matters because the first leg from plant to hub becomes more concentrated, while the second leg into district and taluka channels becomes longer and more fragmented. The result is stronger demand for logistics providers that can combine compliant warehousing, route planning, transport visibility, and packaged handling under one contract. This structure also favors larger operators that can support repacking, labeling, and inventory services without breaking compliance standards. The India lubricants logistics market is therefore moving toward providers with better capital, better systems, and stronger multi-location execution rather than simple haulage-only operators.

Premium and Synthetic Lubricant Shift Increasing Handling Complexity

Premium and synthetic lubricants are raising the handling bar for transport and warehouse operators. These products need tighter lot traceability, cleaner storage separation, and more careful movement controls than standard mineral grades. BS-VI lubricant requirements and BIS-linked formulation standards have already made contamination control more important in day-to-day distribution. The ILMA and Kline study also projected 6.0% annual growth in hybrid vehicle engine oils through 2040, which supports a longer-term shift toward a more complex lubricant mix rather than a simple drop in fluid demand[2]“EV Study Final Report, Impact of Electric Vehicles on the Lubricants Industry,” ILMA, ilma.org. For the India lubricants logistics market, that means operators that have already invested in compliant handling, documentation, and specialized bays carry stronger customer stickiness than transport firms competing only on price.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Base-oil import dependence and raw-material volatility | -0.50% | National, with highest exposure at coastal import hubs such as JNPA, Mundra, and Chennai | Short term (≤ 2 years) |

| EV transition moderating long-run engine-oil throughput in select channels | -0.30% | National, most pronounced in metro and NCR EV-dense corridors | Long term (≥ 4 years) |

| Hazardous-goods compliance and lubricant-compliant warehousing capex | -0.20% | National, with highest compliance burden in MIDC, GIDC, and CMDA industrial estates | Medium term (2-4 years) |

| Channel opacity reducing true retail-demand visibility | -0.20% | National, greatest in semi-urban and rural Tier-2 and Tier-3 markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Base-Oil Import Dependence and Raw-Material Volatility

Base-oil dependence remains the clearest supply-side risk for the India lubricants logistics market. India relied heavily on imported base oil in 2025, and that leaves blenders exposed to freight cost changes, geopolitical disruptions, and overseas refinery run-rate decisions. When inbound supply tightens, production planning at blending sites absorbs the first shock and logistics networks then face uneven dispatch patterns, sudden stock draws, and weaker asset utilization. Buffer storage near ports and blending plants can reduce some of that risk, but it also raises capital intensity and works poorly in soft demand phases. This keeps returns under pressure for operators that commit too much capacity to volatility protection without stable contract recovery.

EV Transition Moderating Long-Run Engine-Oil Throughput in Select Channels

Electric vehicle adoption is likely to reduce some recurring engine-oil flows over the long run, especially in passenger vehicle channels. The immediate effect is more about the demand mix than a direct collapse in volumes, because commercial vehicles and industrial users still account for a large share of lubricant movement. Research found that hybrid vehicle engine oils are projected to grow 6.0% annually through 2040, indicating that fluid demand will shift before fading in some channels. That means operators in metro and premium passenger-car corridors need to prepare for smaller, more specialized shipments rather than just large engine oil consignments. The India lubricants logistics market still has a cushion from the legacy vehicle fleet, but electric mobility is shaping the outer limit of long-range throughput growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Value-Added Logistics Captures Outsourcing Momentum

Transportation represented 71.09% of the India lubricants logistics market share in 2025, which kept it as the largest service category. That lead came from the heavy volume of road-led movement between blending plants, depots, workshops, and industrial users. Warehousing and distribution still played an important support role because they absorbed import timing mismatches and seasonal stock builds.

Value-added services are forecast to grow at a 5.12% CAGR through 2031, which makes them the fastest-growing service segment. This part of the India lubricants logistics market is benefiting from more outsourcing of inventory management, repacking, relabeling, and kitting. The deeper reason is the rising complexity of SKUs across viscosity grades, base stocks, and use cases. More product variants mean more pick-pack combinations, more labeling checkpoints, and more order customization across dealers, workshops, and industrial buyers. That favors logistics partners with warehouse systems, compliant handling areas, and disciplined documentation. BIS labeling and quality requirements further strengthen the case for larger providers with certified infrastructure. As a result, value-added work is growing faster than pure transport, and it is steadily becoming a more important revenue pool within the India lubricants logistics industry.

By Handling/Shipment Format: Small Packs Lead Volume, IBCs Reshape B2B Flows

Small retail and commercial packs held 50.28% of the the India lubricants logistics market size format-level spending in 2025, giving them the largest format position. Their lead reflects the fragmented maintenance structure across India, where roadside mechanics and smaller workshops depend on sub-5-liter deliveries. Drums remain relevant for mid-sized industrial buyers that need manageable bulk volumes without on-site tank infrastructure. Bulk liquid movements continue to serve larger industrial users with dedicated storage and regular replenishment cycles.

IBCs are forecast to grow at a 4.56% CAGR through 2031, making them the fastest-growing format. Organized buyers in manufacturing, energy, and steel are shifting from 200-liter drums to 1,000-liter IBCs to lower per-tonne logistics costs and reduce spill exposure. That shift is also supported by compliance needs under hazardous chemicals handling rules, which favor cleaner, more controlled movement systems[3]“Hazardous and Other Wastes Management and Transboundary Movement Second Amendment Rules, 2023,” EPR Used Oil Portal, eprusedoil.cpcb.gov.in. For operators, the change raises demand for bunded floors, forklift-ready warehouses, taller racking, and certified containment systems. This is why IBC-led flows are reshaping formal B2B distribution even though small packs still account for the largest India lubricants logistics market share at the format level.

By End-user Industry: Automotive Anchors Demand, Aerospace Records Fastest Growth

Automotive accounted for 44.86% of the India lubricants logistics market in 2025, which made it the largest demand base for end-users. That position came from the wide vehicle parc across 2-wheelers, passenger cars, and commercial vehicles, each with different pack sizes and refill cycles. Route density also strengthens automotive demand because dealer workshops, fleet garages, and quick-lube points cluster along major freight and urban corridors. This keeps drop frequency high and delivery economics favorable for transport and warehouse operators.

Aerospace is projected to grow at a 5.06% CAGR through 2031, which makes it the fastest-growing end-user segment. Growth is being supported by India’s expanding commercial aviation fleet and the related maintenance, repair, and overhaul supply chain. Aerospace lubricants also need stricter approval, traceability, and custody controls than general automotive or industrial fluids. That creates space for specialist logistics providers with cleaner facilities and better documentation standards. The India lubricants logistics market is therefore seeing a small but important high-margin niche emerge alongside its larger automotive base.

Geography Analysis

Western India remained the most consolidated corridor in the India lubricants logistics market in 2025. Maharashtra carried the highest density of blending activity and automotive production, while Gujarat provided major petrochemical and port-linked support to national lubricant flows. This combination makes the western belt central to plant dispatches, import-linked storage, and regional redistribution. DHL Group announced a EUR 1 billion (USD 1.14 billion) investment in India through 2030 with capacity additions in Bhiwandi and Chennai, highlighting the importance of gateway-led infrastructure for chemical and lubricant supply chains.

Northern India is the largest consumption belt for automotive lubricants because of its truck-heavy freight economy and dense highway network. Demand stays firm across Delhi-NCR, Uttar Pradesh, Haryana, Punjab, and Rajasthan, where fleet operations, workshops, and roadside service channels keep replenishment cycles short. The region also benefits from heavy movement on the Delhi-Mumbai and Delhi-Kolkata corridors, which supports strong less-than-truckload density. Eastern India and the Northeast remain less penetrated, but their role is becoming more important as steel, mining, and industrial activity pulls organized logistics investment further east. Mahindra Logistics added 400,000 sq ft of Grade-A warehousing in Guwahati and Agartala in October 2025, taking its Northeast capacity build to 1,000,000 sq ft under its Go-East strategy. That move signals a clear commercial case for district-deeper industrial distribution in under-served zones.

Southern India presents the most balanced end-user mix in the India lubricants logistics market. Tamil Nadu and nearby corridors support automotive production, while Karnataka adds aerospace and advanced industrial demand. This mix helps the south because it combines workshop-led automotive replenishment with more specialized and higher-value contract logistics needs. Kuehne+Nagel expanded by 100,000 sqm across 5 Indian cities in 2026, taking its footprint to nearly 500,000 sqm and strengthening multi-nodal distribution reach that supports both industrial and lubricant-adjacent flows. NX Group also said it plans to grow India revenue to JPY 60 billion (USD 400 million) by 2028, with North and South India as key growth clusters.

Competitive Landscape

The India lubricants logistics market remains fragmented, with no single operator dominating across transportation, warehousing, handling formats, and end-user industries. Domestic firms such as TCI, VRL Logistics, Om Logistics, Safexpress, Delhivery, Mahindra Logistics, AEGIS, and CJ Darcl compete largely on branch reach, cross-docking speed, and price. Global operators such as DHL Supply Chain, Kuehne+Nagel, DSV Solutions, and Nippon Express focus more on higher-value contract logistics, larger warehouses, and better compliance-led handling. This split keeps the India lubricants logistics market competitive across both cost-sensitive and service-sensitive parts of the value chain.

A clear divide has opened between operators investing in Grade-A, automation-ready facilities and those staying focused on standard freight execution. DHL Group’s India investment plan through 2030 shows how global players are building larger multi-client platforms that can serve lubricant, chemical, and energy-linked contracts under one operating model. Kuehne+Nagel’s 100,000 sqm expansion across 5 cities is another example of this strategy, with fulfillment capacity rising in locations that support industrial and aftermarket distribution. Mahindra Logistics also widened its eastern warehousing footprint, showing that regional depth is becoming as important as national branding in this space. These moves matter because shippers increasingly want one provider to cover storage, secondary distribution, and handling support with consistent compliance.

White space remains strongest in 3 areas, certified hazardous-material handling for small-format kitting, reverse logistics for used oil, and aerospace-grade lubricant movement. The used-oil EPR framework, effective from April 1, 2024, is gradually increasing the need for traceable reverse flows and more formal collection networks[4]“Extended Producer Responsibility for Used Oil Management, EPR Portal,” CPCB, eprusedoil.cpcb.gov.in. Technology is becoming more important as well, because blenders want proof of handling quality, movement visibility, and chain-of-custody control. CJ Darcl’s annual report highlighted ADAS deployment and IoT-based real-time tracking across its fleet, showing how operators are using data systems to strengthen service credibility. This leaves the India lubricants logistics market open to specialists that can combine compliance, visibility, and network depth without depending only on freight pricing.

India Lubricants Logistics Industry Leaders

Delhivery, Ltd.

DHL Group

AEGIS

Mahindra Logistics, Ltd.

Transport Corporation of India, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Kuehne+Nagel India opened a 248 sqm temperature-controlled airfreight cross-dock in Hyderabad, with dedicated zones at +2 °C to +8 °C and +15 °C to +25 °C for healthcare and pharmaceutical logistics. This is Kuehne+Nagel's second HealthChain-certified facility in India, following the Bengaluru Cool Zone, advancing specialized handling capabilities for pharmaceutical-grade lubricant and specialty fluid logistics.

- May 2026: Transport Corporation of India (TCI) announced a capital expenditure plan of INR 550-600 crore (USD 66-72 million) for FY2027, with nearly half earmarked for the acquisition of 2 new cellular container vessels (7,300 DWT each) for coastal shipping. This investment accelerates TCI's multimodal logistics pivot, targeting bulk lubricant and industrial goods flows between western and eastern seaboard industrial clusters.

- January 2026: VRL Logistics commenced delivery of a 500-unit fleet of new 20-tonne commercial vehicles (total capex approximately INR 1.6-1.7 billion), with 100 units received in January. Aligned with guidance of 10% capacity growth, this fleet renewal supports projected FY2027 tonnage growth across VRL's 24-state, 1,293-branch LTL network.

- October 2025: Kuehne+Nagel India announced a 100,000 sqm fulfillment center expansion across 5 cities, Gurgaon, Kolkata, Nagpur, Mumbai, and Rajpura, bringing its total India footprint to nearly 500,000 sqm and creating over 1,500 new jobs. Equipped with telescopic conveyors and high-performance sorting systems enabling a 75% increase in peak order-handling capacity, this expansion strengthens the company's position in industrial and lubricant-adjacent contract logistics.

India Lubricants Logistics Market Report Scope

| Transportation | Road | Full-Truck-Load (FTL) |

| Less than-Truck-Load (LTL) | ||

| Rail | ||

| Multimodal Transport | ||

| Warehousing and Distribution | ||

| Value-added Services (Inventory management, Repacking, Relabeling, and Kitting etc.) |

| Bulk liquid |

| Intermediate Bulk Containers (IBCs) |

| Drums |

| Small Retail and Commercial (Bottles and Jerry Cans, Stand-up Pouches, Pails, Kegs, etc.) |

| Automotive |

| Heavy Equipment |

| Steel and Metal Machining |

| Energy/Power Generation |

| Industrial Manufacturing |

| Textile |

| Marine |

| Aerospace |

| Other End-user Industries |

| By Service Type | Transportation | Road | Full-Truck-Load (FTL) |

| Less than-Truck-Load (LTL) | |||

| Rail | |||

| Multimodal Transport | |||

| Warehousing and Distribution | |||

| Value-added Services (Inventory management, Repacking, Relabeling, and Kitting etc.) | |||

| By Handling / Shipment Format | Bulk liquid | ||

| Intermediate Bulk Containers (IBCs) | |||

| Drums | |||

| Small Retail and Commercial (Bottles and Jerry Cans, Stand-up Pouches, Pails, Kegs, etc.) | |||

| By End-user Industry | Automotive | ||

| Heavy Equipment | |||

| Steel and Metal Machining | |||

| Energy/Power Generation | |||

| Industrial Manufacturing | |||

| Textile | |||

| Marine | |||

| Aerospace | |||

| Other End-user Industries |

Key Questions Answered in the Report

What is the 2031 outlook for India lubricants logistics?

The India lubricants logistics market is projected to reach USD 758.69 million by 2031 from USD 635.26 million in 2026, at a 3.62% CAGR over 2026-2031.

Which service segment leads current spending in lubricant logistics across India?

Transportation remained the largest service segment, with 71.09% of market revenue in 2025, because road-led distribution still anchors plant-to-depot and workshop replenishment flows.

Which format is expanding fastest for industrial lubricant deliveries?

IBCs are projected to grow at a 4.56% CAGR through 2031 as larger organized buyers shift from drums to cleaner and more efficient bulk handling formats.

Why does automotive remain the main demand center for lubricant movement?

Automotive held 44.86% of end-user spending in 2025 because India has a large active vehicle parc, dense service networks, and frequent replenishment needs across workshops and fleet channels.

What is driving demand for value-added services in this space?

Value-added services are forecast to grow at a 5.12% CAGR through 2031 as blenders outsource repacking, relabeling, inventory management, and kitting to providers with compliant infrastructure.

How is electric mobility affecting lubricant logistics in India?

The near-term effect is mainly a shift in product mix rather than a sharp drop in volumes, but over time EV adoption is expected to reduce engine-oil throughput in select passenger vehicle channels.

Page last updated on: