India Inflight Catering Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

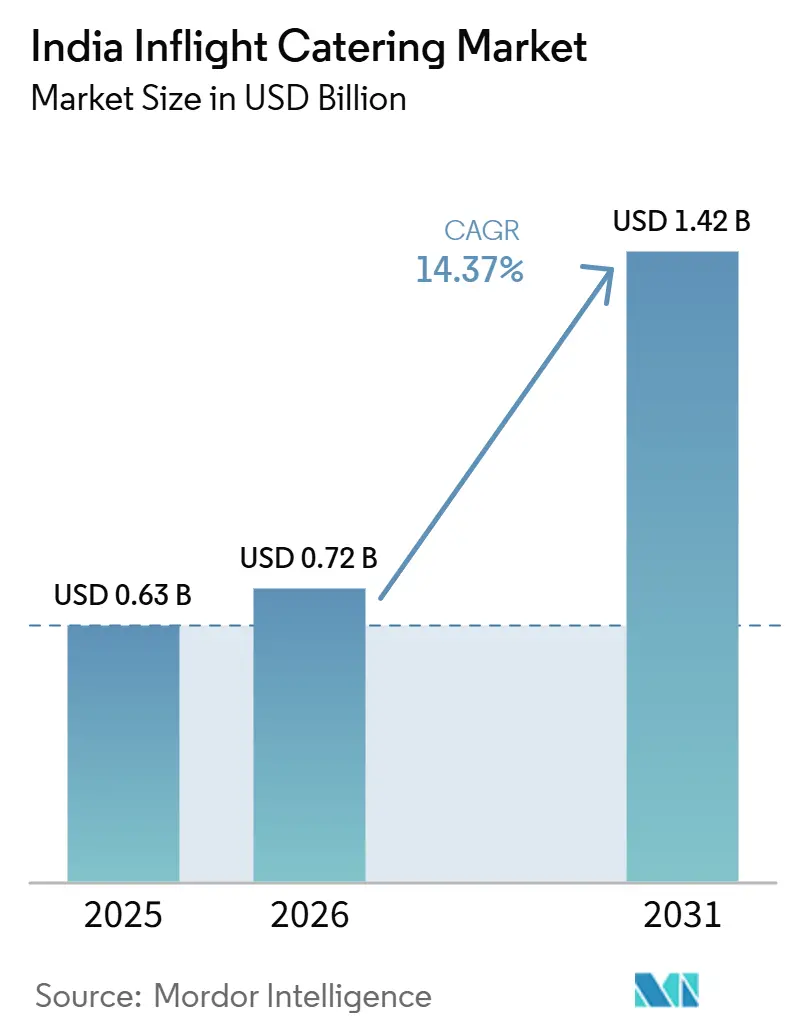

| Base Year Market Size (2025) | USD 0.63 Billion |

| Market Size (2026) | USD 0.72 Billion |

| Market Size (2031) | USD 1.42 Billion |

| Growth Rate (2026 - 2031) | 14.37% CAGR |

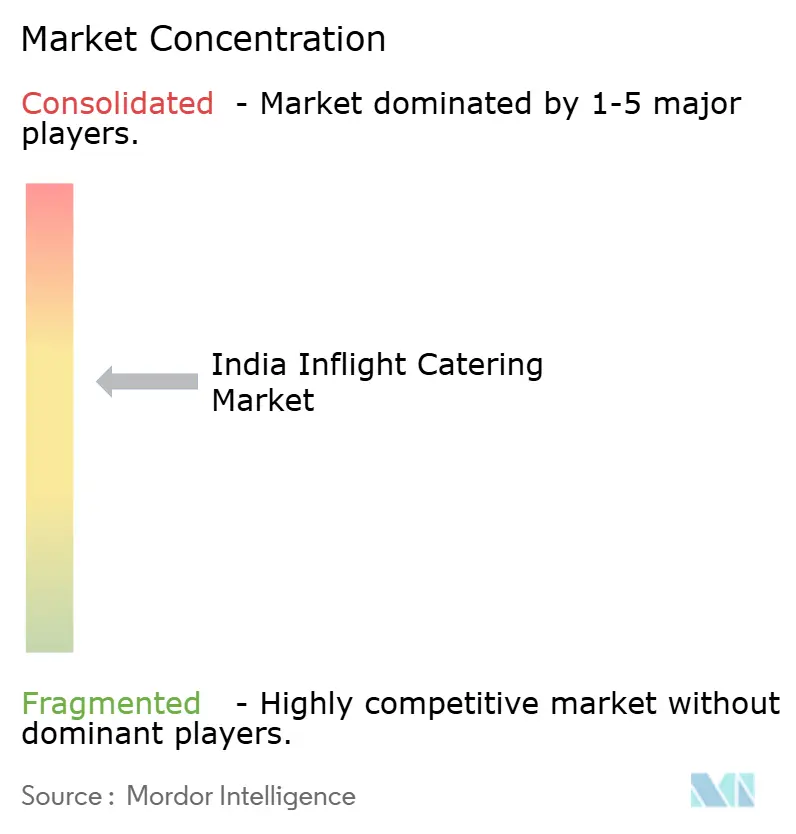

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Inflight Catering Market Analysis by Mordor Intelligence

The India inflight catering market size is expected to grow from USD 631.30 million in 2025 to USD 723.69 million in 2026 and reach USD 1,416.31 million by 2031, growing at a CAGR of 14.37% over 2026-2031. India’s domestic aviation base remained large in 2025, and domestic carriers transported 166.90 million passengers, keeping meal production volumes firm across the India inflight catering market.[1]Directorate General of Civil Aviation, “Domestic Traffic Report, May 2026,” Directorate General of Civil Aviation, dgca.gov.in The market is also being shaped by fare unbundling, as airlines shift from bundled meal service toward pre-order and buy-on-board models that elevate the commercial role of onboard food. Capacity additions at major airlines, new airport kitchens at Jewar, and the expansion of international networks are creating a broader production footprint for the India inflight catering market. Competitive positioning still depends heavily on airport concessions, kitchen scale, and airline menu collaboration, which gives established operators a durable advantage in the India inflight catering market. Food safety enforcement and airside operating complexity will continue to pressure execution. Yet, the combination of traffic growth, premium meal upgrades, and greenfield airport investment keeps the India inflight catering market on a strong expansion path.

Key Report Takeaways

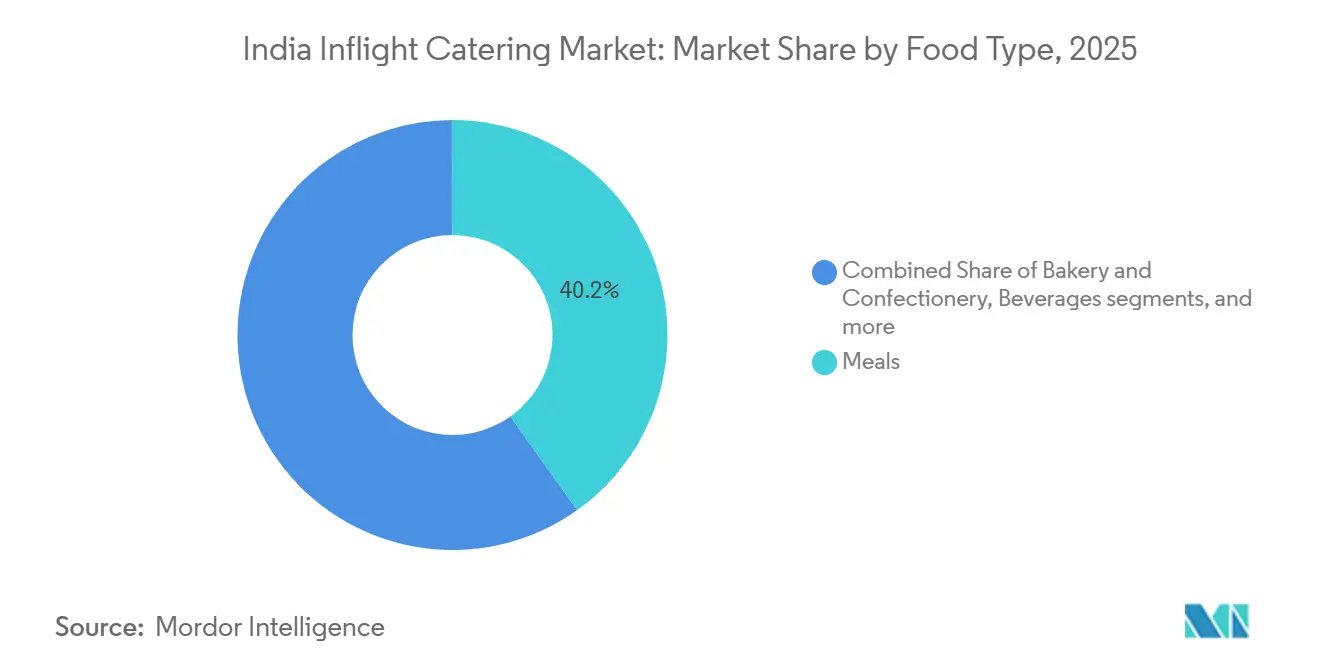

- By food type, meals led with 40.15% revenue share in 2025, while bakery and confectionery are forecast to expand at a 16.35% CAGR through 2031.

- By flight type, FSCs held 45.95% of the India inflight catering market share in 2025, while LCCs are forecast to grow at a 16.80% CAGR through 2031.

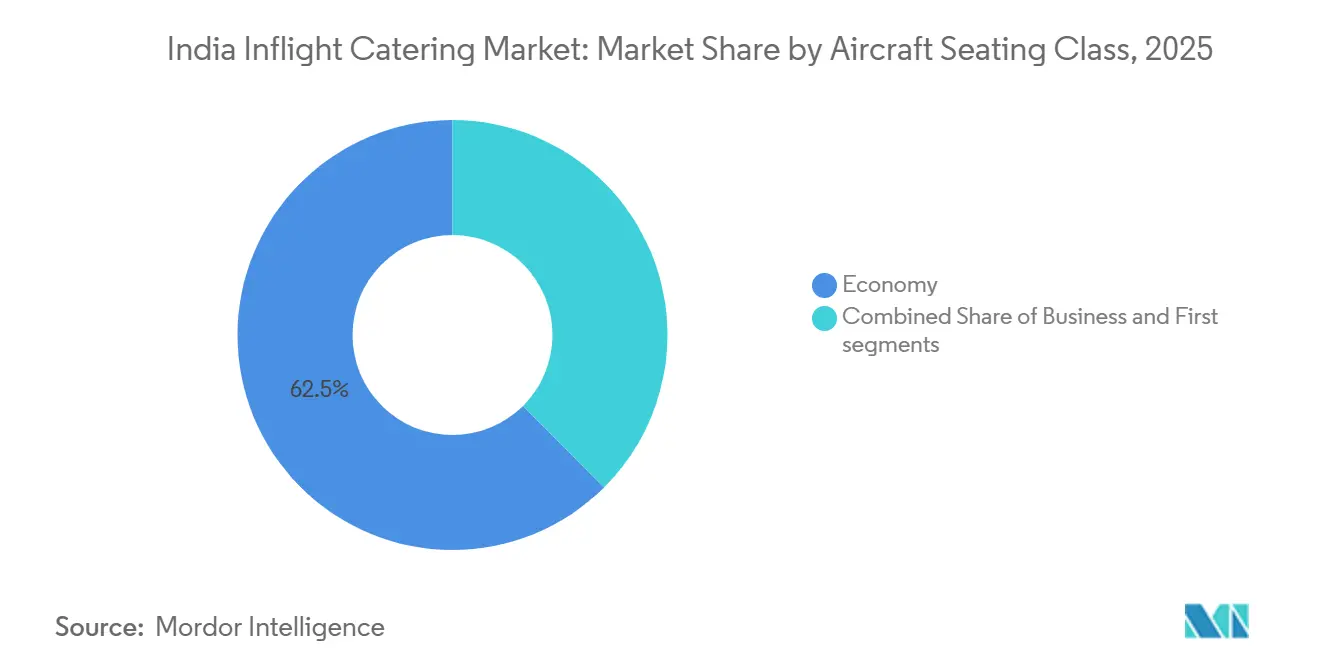

- By seating class, economy class accounted for 62.45% market share in 2025, while first class is projected to grow at a 16.04% CAGR through 2031.

- By catering type, retail on-board captured 58.20% of the India inflight catering market size in 2025 and is forecast to grow at a 16.52% CAGR through 2031.

- By flight duration, long-haul routes accounted for 52.90% market share in 2025, while short-haul routes are projected to grow at a 16.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Inflight Catering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising domestic and international air passenger traffic | +3.50% | National, with early concentration at metro airports including Delhi, Mumbai, Bengaluru, and Hyderabad | Short term (≤ 2 years) |

| Fleet growth and route expansion by LCCs and FSCs | +3.00% | National, accelerating on Tier-2 and Tier-3 city routes | Medium term (2-4 years) |

| Shift toward pre-order, buy-on-board, and ancillary revenue models | +2.50% | National, concentrated in LCC-heavy domestic corridors | Short term (≤ 2 years) |

| Premiumization of onboard meals and personalized passenger experience | +2.00% | National, with emphasis on international ex-India routes | Medium term (2-4 years) |

| Airport-centric kitchen network expansion in emerging aviation hubs | +2.00% | National, with near-term focus on Noida and Navi Mumbai | Long term (≥ 4 years) |

| Strengthening food safety, traceability, and compliance requirements | +1.50% | National, with near-term concentration among hub-airport and multi-kitchen operators | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Domestic And International Air Passenger Traffic

India’s domestic carriers transported 166.90 million passengers in 2025, and scheduled domestic traffic reached 729.40 lakh passengers during January to May 2026, which kept the India inflight catering market closely tied to rising base travel volumes. May 2026 traffic also rose 9.49% month on month, showing that peak travel periods can sharply raise flight kitchen output needs in a short span. International traffic from Indian carriers also expanded by 7.70% during April to February of FY25, which extended demand toward longer and more complex meal cycles. As passenger volume rises across both domestic and international routes, kitchen operators need larger surge capacity, tighter dispatch planning, and stronger ingredient control across the India inflight catering market. This traffic mix matters because domestic routes offer frequency and scale, while international routes increase revenue per uplift due to more service-intensive catering requirements. The result is a broader and more stable demand base for the India inflight catering market than a single-network model would provide.

Fleet Growth And Route Expansion By LCCs and FSCs

Fleet additions remain one of the clearest demand supports for the India inflight catering market because each aircraft induction adds recurring catering volume to an airline’s network. IndiGo stated in 2026 that it is inducting 52-56 aircraft this year and targets a fleet of 550 aircraft and 3,000 daily departures by FY30. Its 39 confirmed A321XLR orders also point to wider international reach, which will require longer-haul service formats and more demanding production planning. Air India is also expanding its widebody product base in 2026, including B787-9 and A350-1000 deliveries tied to the development of premium cabin service.[2]Air India, “Air India Elevates Its Inflight Dining Experience with Refreshed Global Menu,” Air India Newsroom, airindia.com Akasa Air reported 37% revenue growth in FY2025-26, which further supports the view that airline scale is broadening the buyer base for the India inflight catering market. This expansion pipeline gives caterers better forward visibility than many other food service categories because route and fleet growth translate into repeatable production demand.

Shift Toward Pre-Order, Buy-On-Board, And Ancillary Revenue Models

Fare unbundling is reshaping the India inflight catering market as airlines reduce default meal inclusion on price-sensitive routes and expand pre-purchase or onboard-sale options. Air India introduced a Basic Fare on select domestic sectors in June 2026, removed complimentary meals from the base fare, and allowed passengers to pre-purchase meals up to 24 hours before departure. IndiGo’s 6E Eats system and broader menu structure already support this retail logic, providing caterers with more item-level planning signals than standard complimentary service does.[3]IndiGo, “6E Eats, Snacks, Food Menu, Beverages,” IndiGo, goindigo.in That shift changes the production model across the India inflight catering market because kitchens must prepare retail-ready packaging, manage a wider SKU mix, and align inventory with purchase behavior rather than standard load assumptions. As this model deepens, the India inflight catering market will increasingly depend on demand-forecasting accuracy and product-mix discipline rather than solely on bulk meal throughput.

Premiumization Of Onboard Meals And Personalized Passenger Experience

Premium meal development is raising the quality threshold in the India inflight catering market, especially on international and premium-cabin routes. Air India launched a refreshed global menu in 2025 with more than 18 special meal types, which widened the dietary and presentation demands placed on caterers. IndiGo also upgraded its Stretch business-class meal service in June 2026 with fine chinaware, steel cutlery, and a time-of-day menu rotation on domestic sectors. This means the India inflight catering market is no longer driven solely by scale, as airlines are using food to support product differentiation and the passenger experience. Operators now need stronger menu development, allergen control, plating capability, and airline collaboration, which increases the value of larger, more specialized kitchens. This lifts per-meal value and strengthens the position of caterers that can move beyond standardized volume production.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food wastage from forecast error and schedule volatility | -1.50% | National, intensified at high-frequency hub airports | Short term (≤ 2 years) |

| Margin pressure from packaging, labor, and utility inflation | -1.30% | National | Short term (≤ 2 years) |

| High food safety, security, and multi-airport compliance burden | -1.20% | National, with higher complexity in multi-airport operations | Medium term (2-4 years) |

| Airside logistics complexity and tight turnaround windows | -1.00% | National, most acute at constrained hub airports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Food Wastage From Forecast Error And Schedule Volatility

Food wastage remains a significant operational challenge in the India inflight catering market, as production must often be completed before final passenger demand is confirmed. Airbus cited industry work showing global airline cabin and catering waste at 3.6 million tons annually based on 2024 and 2025 data, with volumes projected to approach 4 million tons by the end of 2025. In India, aircraft swaps, cancellations, standby loads, and late schedule changes increase the risk of overproduction across both complimentary and retail meal formats. The issue becomes harder in the India inflight catering market as buy-on-board expands, because item-level retail demand is less predictable than with fixed-tray service. Airbus published an AI-based smart catering framework in April 2026 that projected double-digit reductions in preventable cabin food waste through machine learning-based load optimization. Adoption in India remains limited, so forecast error will remain a meaningful source of margin leakage until airlines and caterers tighten their system integration.

High Food Safety, Security, And Multi-Airport Compliance Burden

Regulatory compliance is a threshold cost in the India inflight catering market because operators must satisfy both food safety and aviation security requirements across every kitchen location. FSSAI reinforced this burden in January 2024 and March 2024 through directives on labeling compliance, kind-of-business registration, separate licenses for off-airport food activity, and date-and-time manufacturing labels on packed meals. Airside operations also require trolley screening, bonded storage, controlled access, and consistent audit readiness, which raises fixed operating intensity. Each new airport kitchen must replicate this compliance structure, so expansion costs rise quickly when operators enter multiple locations. Larger networks are better positioned in the India inflight catering market because they can spread these costs across more contracts and more kitchens. This leaves smaller players with less room to absorb certification costs and still compete on price.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Food Type: Diversification Beyond Meals Is Gaining Commercial Weight

Meals accounted for 40.15% of the India inflight catering market share in 2025, keeping them the largest food type even as buying behavior shifted on domestic routes. That position reflects the continued importance of structured tray service on full-service, long-haul, and premium cabin operations across the India inflight catering market. Beverages also remained important in short domestic sectors, where coffee, tea, and snack combinations serve as frequent onboard purchases. Other food types, including dietary meals, regional dishes, and dessert-led options, also gained relevance as airlines widened their service mix. This means the food basket in the India inflight catering market is becoming more varied even before the largest category changes hands.

Bakery and confectionery is projected to grow at a 16.35% CAGR through 2031, making it the fastest-moving food sub-segment in the India inflight catering market. Its momentum is tied to lighter, snackable, and individually sold formats that suit short-haul and buy-on-board demand. As airlines reduce complimentary hot meals in some fare types, packaged pastries, cookies, and confectionery become easier to stock, sell, and forecast than bulk hot food. Air India’s menu expansion to more than 18 special meal types also shows that caterers must manage a broader ingredient matrix, which supports niche food categories alongside core meals. The India inflight catering industry is therefore moving from a simpler meal-led structure toward a wider retail and dietary product mix without losing the central role of conventional meal service.

By Flight Type: LCC Meal Expansion Is Redefining Revenue Architecture

FSCs accounted for 45.95% of the India inflight catering market in 2025, supported by complimentary meal inclusion and higher average revenue per meal. Their position remained tied to longer-haul service, premium cabin complexity, and menu expectations that are harder to simplify. Airlines such as Air India are also investing in refreshed menus and upgraded long-haul experience, which supports stronger value capture per uplift. This keeps FSC demand important in the India inflight catering market, even as domestic LCC volume grows faster. It also preserves a clear quality-based segment where catering value is linked to service depth, not just throughput.

LCC inflight meals are forecast to grow at a 16.80% CAGR through 2031, which makes them the fastest-growing flight-type segment. That pace reflects the scale of IndiGo, Akasa Air, and other budget carriers in terms of domestic departures and route additions. The LCC model is changing the India inflight catering market because food is becoming a retail item rather than a standard ticket inclusion. That creates stronger dependence on packaging, SKU planning, and conversion rates during the flight. Charter and business aviation remain much smaller, but they add a specialized niche where customization and low-volume premium handling matter more than scale. The India inflight catering industry, therefore, faces a dual structure, with FSCs preserving value-rich service formats and LCCs expanding transaction-led demand more quickly.

By Aircraft Seating Class: Economy Holds the Base While Premium Cabins Raise Value

Economy class accounted for 62.45% of the India inflight catering market in 2025, making it the clear volume anchor across airline networks. This dominance reflects the size of India’s price-sensitive traveler base and the large number of seats operated in single-aisle domestic fleets. Even when the meal format changes, the economy still drives the largest absolute number of units handled in the India inflight catering market. That gives scale-oriented kitchens a strong production base, especially in dense domestic corridors. It also means that any change in fare design or onboard food pricing directly affects the largest demand pool in the India inflight catering market.

First class is projected to grow at a 16.04% CAGR through 2031, making it the fastest-growing seating class by value growth. This growth is tied to Air India’s premium product investment across widebody aircraft, where gourmet meals, pairing options, and pre-selection features raise service intensity. Business class is also becoming more important as IndiGo scales Stretch with upgraded service elements on domestic sectors. These premium cabins account for fewer seats, yet they generate much higher meal value and operational complexity per passenger. IATA’s cabin sustainability work also matters more in these segments because packaging, serviceware, and waste intensity are higher. The India inflight catering market is therefore seeing value growth shift upward even while economy remains the core volume base.

By Catering Type: Retail On Board Leads on Scale and Growth

Retail On Board captured 58.20% of the India inflight catering market in 2025, giving it leadership within the catering-type split. That large share shows that the India inflight catering market has already moved well beyond a model centered only on complimentary trays. LCCs adopted this structure earlier, and FSCs are now applying parts of it on selected domestic routes. Retail formats also suit the wider use of packaged snacks, beverages, and lighter items that are easier to merchandise and sell onboard. This makes retail the most commercially active segment of the India inflight catering market, even as classic catering remains important on specific routes and in cabin settings.

Retail On Board is also forecast to grow at a 16.52% CAGR through 2031, confirming it is the strongest growth engine in this segment. Its expansion is being supported by pre-order capability, menu visibility, and airline interest in ancillary revenue. Classic catering still retains meaningful demand on long-haul full-service routes, premium cabins, and situations where service inclusion remains part of the ticket promise. The operational divide is important because retail formats require item-level labeling, inventory control, and point-of-sale compatibility. In contrast, classic catering relies more on bulk hot-meal flow and trolley coordination. This split raises execution complexity across the India inflight catering market because both models now need to run in parallel. It also gives better-positioned operators room to serve airlines across multiple fare and service models rather than just one.

By Flight Duration: Long-Haul Holds Revenue While Short-Haul Drives Growth

Long-haul flights accounted for 52.90% of the market in 2025, placing them at the center of higher-value revenue generation within the India inflight catering market. Routes lasting more than 4 hours typically require more than one food service cycle, tighter cold-chain planning, and more premium service content. That lifts revenue per flight and strengthens the role of established kitchens serving major international hubs. Air India’s wider international network, including routes to London, New York, Toronto, and Melbourne, reinforces this position. Long-haul demand, therefore, remains critical to the value structure of the India inflight catering market.

Short-haul is projected to grow at a 16.20% CAGR through 2031, making it the fastest-growing flight duration segment. This growth is tied to rising domestic departures as IndiGo works toward 3,000 daily flights by FY30 and other carriers add route depth. Short-haul sectors favor retail conversion and lighter menus because passengers often make quick and lower-value purchase decisions during the trip. At the same time, international medium- and long-haul additions will continue to raise compliance and service expectations in the India inflight catering market. That includes stricter documentation, labeling, and specialized meal handling on routes with more demanding airline standards. The India inflight catering market, therefore, balances 2 distinct dynamics: short-haul expanding frequency faster, while long-haul continues to anchor revenue intensity.

Geography Analysis

India is the sole geographic scope of this study, and the India inflight catering market remains centered on the country’s largest aviation hubs, especially Delhi, Mumbai, and Bengaluru. Delhi remains highly important because it supports a large share of India’s international long-haul catering activity through Air India’s expanding widebody network. Mumbai remains a core demand center because it combines high domestic frequency with high demand for premium international service. Bengaluru is becoming a stronger growth node as the airport moves toward a much larger passenger base by 2030 and attracts longer-dated kitchen investment. Domestic traffic in India reached 167.74 million in FY26, and May 2026 traffic also showed a sharp month-on-month rise, which keeps pressure high on metro kitchen capacity. These metro airports, therefore, still define the operational core of the India inflight catering market.

Greenfield airports are now widening that footprint and creating the next investment cycle in the India inflight catering market. Navi Mumbai International Airport began domestic operations in December 2025 and is preparing for international passenger and freighter services from July 2026. Noida International Airport already has 2 major catering commitments, including TajSATS’s new facility and AISATS’s larger cargo and catering plan. Nagpur’s expansion roadmap also shows that demand for catering will spread beyond the established metro triangle. This means geographic growth in the India inflight catering market will increasingly depend on how quickly new airports convert infrastructure into regular airline activity.

Tier-2 and tier-3 airports represent the next layer of routes, but service quality in the India inflight catering market still depends on access to strong airport-adjacent kitchen infrastructure. Premium, freshly prepared meals remain more feasible at large hubs, while smaller locations are more likely to rely on packaged or pre-assembled items. That creates a two-speed national structure in the India inflight catering market, with higher revenue intensity at metro hubs and faster departure growth at secondary airports. As airline networks deepen, operators will need satellite kitchens or stronger distribution models to support emerging airports more efficiently. This shift will matter because geography in the India inflight catering market is no longer only about today’s hubs, it is also about how quickly capacity follows new airport demand.

Competitive Landscape

The India inflight catering market is moderately concentrated. TajSATS also operated across 10 kitchens at 8 airport locations, giving it a scale advantage in production, airline coverage, and network replication. At many major airports, only 2 licensed caterers hold concession agreements, so competitive intensity is shaped more by access rights than by open entry. Ambassadors Sky Chef remains a notable alternative in Mumbai and Delhi, serving more than 35 airlines, including Air India, Lufthansa, and IndiGo, which keeps it relevant in 2 of the country’s most important hubs. Skygourmet Catering in Hyderabad and the Bengaluru kitchen, formerly under LSG Sky Chefs, also illustrate how each airport can function as a localized concession market rather than a freely contestable space. This structure gives India inflight catering market durable barriers, stable contracts, and a strong premium on long-term operating rights.

Recent strategic moves show how competition in the India inflight catering market is evolving around assets, network reach, and route specialization. TajSATS opened a 45,000 sq ft inflight kitchen at Noida International Airport in June 2026, with a capacity of over 20,000 meals per day, positioning it early at a major new aviation node. Gategroup was also named IndiGo’s catering partner for its inaugural European long-haul routes, which linked the airline's international expansion to global catering expertise. These moves suggest that the India inflight catering market is expanding not through broad fragmentation, but through selective reinforcement of scale and concession-backed positions.

Competitive differentiation is narrowing around menu co-development, compliance capability, and multi-airport execution. TajSATS’s The Atelier at Noida reflects the growing need for caterers to work closely with airlines on menu design and service presentation. FSSAI’s labeling and licensing directives raise the importance of formal food safety systems, which favor larger operators with stronger process discipline. Airbus’s smart catering framework also points to an emerging technology layer around waste control and load planning that stronger operators can evaluate earlier. There is still room for expansion in greenfield airports, charter aviation, and specialized dietary production. Still, the market continues to favor operators that can combine scale, compliance, and airline-facing product development.

India Inflight Catering Industry Leaders

Taj SATS Air Catering Limited

Casino Air Caterers & Flight Services

Skygourmet Catering Private Limited

LSG Sky Chefs India Pvt. Ltd.

Ambassadors Sky Chef

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: IndiGo launched its 'Lite Fare' product effective July 2026, targeting a 15% ancillary revenue mix and removing complimentary meals from the base fare. IndiGo's unbundling deepens the structural shift toward buy-on-board food retail, reshaping per-flight meal planning for its caterer partners across the country's largest airline network.

- June 2026: TajSATS opened a 45,000 sq ft inflight kitchen at Noida International Airport (Jewar) in June 2026, with an initial production capacity of over 20,000 meals per day. Operated under a 37-year DBFOT agreement, the facility includes 'The Atelier' menu co-development space and is equipped with X-ray screening, goods scanners, and bonded airline storage, serving both domestic and international carriers at Delhi NCR's second major airport.

- February 2026: The Uttar Pradesh government signed an MoU with Air India SATS Airport Services Pvt. Ltd. (AISATS), committing INR 4,458 crore (USD 472.85 million) to develop an integrated cargo campus and air catering kitchen at Noida International Airport (Jewar). The catering unit is designed to supply inflight meals to multiple airports across northern India, serving as a regional catering hub.

India Inflight Catering Market Report Scope

Inflight catering refers to the specialized preparation and delivery of food and beverages served to passengers and crew during commercial airline operations. These meals are prepared by aviation-approved catering providers in controlled kitchen facilities and are packed, stored, transported, and loaded onto aircraft under strict food safety, hygiene, temperature-control, and security requirements.

The India inflight catering market is segmented by food type, flight type, aircraft seating class, catering type, flight duration, and geography. By food type, the market is segmented into meals, bakery and confectionery, beverages, and other food types. By flight type, the market is segmented into full-service carriers (FSCs), low-cost carriers (LCCs), and other flight types. By seating class, the market is segmented into economy, business, and first class. By catering type, the market is segmented into retail onboard and classic catering. By flight duration, the market is segmented into long-haul and short-haul. For each segment, the market size is provided in terms of value (USD).

| Meals |

| Bakery and Confectionery |

| Beverages |

| Other Food Types |

| Full‑Service Carriers (FSCs) |

| Low‑Cost Carriers (LCCs) |

| Other Flight Types |

| Economy |

| Business |

| First |

| Classic (Complimentary and Pre‑ordered) |

| Retail On Board (Buy‑on‑board) |

| Short‑Haul |

| Long‑Haul |

| By Food Type | Meals |

| Bakery and Confectionery | |

| Beverages | |

| Other Food Types | |

| By Flight Type | Full‑Service Carriers (FSCs) |

| Low‑Cost Carriers (LCCs) | |

| Other Flight Types | |

| By Aircraft Seating Class | Economy |

| Business | |

| First | |

| By Catering Type | Classic (Complimentary and Pre‑ordered) |

| Retail On Board (Buy‑on‑board) | |

| By Flight Duration | Short‑Haul |

| Long‑Haul |

Key Questions Answered in the Report

What is the current size of inflight catering in India?

The India inflight catering market size reached USD 723.69 million in 2026 and is forecast to reach USD 1,416.31 million by 2031 at a 14.37% CAGR.

Which catering format is leading airline food sales in India?

Retail On Board led with 58.20% share in 2025 and is also the fastest-growing catering type at a 16.52% CAGR through 2031.

Which airline segment is driving the fastest expansion in onboard food demand?

LCC inflight meals are growing fastest at a 16.80% CAGR, supported by route expansion and fare unbundling.

Why are premium cabin meals becoming more important for service providers?

First class is forecast to grow at a 16.04% CAGR, and premium cabins carry higher meal value because they require more complex service and menu standards.

Which flight duration category brings the highest revenue intensity?

Long-haul held 52.90% share in 2025 because these flights require multiple meal cycles and more service-intensive catering.

How concentrated is the supplier base for airline caterers in India?

The structure is moderately concentrated, with TajSATS holding around 56% share of meals catered in India and major airports often limited to 2 licensed caterers.

Page last updated on: